When to Sell a Markov Chain Asset?††thanks: This research is supported in part by the Simons Foundation (235179).

Abstract

This paper is concerned with an optimal stock selling rule under a Markov chain model. The objective is to find an optimal stopping time to sell the stock so as to maximize an expected return. Solutions to the associated variational inequalities are obtained. Closed-form solutions are given in terms of a set of threshold levels. Verification theorems are provided to justify their optimality. Finally, numerical examples are reported to illustrate the results.

Key words: Markov chain asset, optimal stopping, quasi-variational inequalities

1 Introduction

Most market models in the literature are Brownian motion based including geometric Brownian motion, diffusion with possible jumps and regime switching; see related books by Duffie [2], Hull [7], Elliott and Kopp [3], Fouque et al. [4], Karatzas and Shreve [8], and Musiela and Rutkowski [11] among others. An alternative is the binomial tree model introduced by Cox-Ross-Rubinstein. The BTM is natural for financial markets because intensive buying moves the market upwards and forceful selling pushes it downwards. All these transactions take place in discrete moments. However, a main drawback of the BTM is its non-Markovian nature, which makes it difficult to work with mathematically. In this paper, we consider a Markov chain market model. The main advantage of such a model is it preserves much of the flexibility of the binomial tree structure and, in the meantime, it is more mathematically tractable, which allows serious mathematical analysis in related optimization problems. Recently, several Markov chain based models are developed. For example, van der Hoek and Elliott [14] introduced a stock price model based on stock dividend rates and a Markov chain noise. Norberg [12] used a Markov chain to represent interest rate and considered a market model driven by a Markov chain. In particular, the market model in [12] resembles a GBM in which the ‘drift’ is approximated by the duration between jumps and the ‘diffusion’ is given in terms of jump times. An additional advantage of a Markov chain driven model is its price is almost everywhere differentiable. Such differentiability is desirable in an optimal control type analysis proposed by Barmish and Primbs [1]. In connection with dynamic programming problems, the corresponding Hamilton-Jacobi-Bellman equations are of first order, which are easier to analyze than those under traditional Brownian motion based models. Finally, the Markov chain model is not that far apart from a GBM because it can be used to approximate a GBM by varying its jump rates. In fact, it is shown in Example 1 that a properly scaled Markov chain model converges weakly to that of a GBM as the jump rates go to infinity.

When to sell a stock is a crucial component in stock trading. It determines when to take profits or to cut losses. It is probably the most emotional part for individual investors in the trading process. Selling rules in financial markets have been studied for many years. For example, Zhang [18] considered a selling rule determined by two threshold levels: a target price and a stop-loss limit. One makes a selling decision whenever the price reaches either levels. Under a switching GBM, the objective is to determine these threshold levels to maximize an expected discounted reward function. In [18], such optimal threshold levels are obtained by solving a set of two-point boundary value problems. In Guo and Zhang [5], they considered the optimal selling rule under a GBM model with regime switching. Using a smooth-fit technique, they were able to convert the optimal stopping problem to a set of algebraic equations. These algebraic equations were used to determine the optimal target levels. In addition to these analytical results, various mathematical tools have been developed to compute these threshold levels. For example, a stochastic approximation technique was used in Yin, Liu and Zhang [15] and a linear programming approach was developed in Helmes [6]. In addition, Merhi and Zervos [10] studied an investment capacity expansion/reduction problem following a dynamic programming approach under a GBM market model. Similar problem under a more general market model was treated by Løkka and Zervos [9].

In this paper, the stock price is assumed to follow a Markov chain model. Under this model, the state of the Markov chain can be estimated based on the stock price increments. This makes the Markov chain observable. In addition to its simplicity, the Markov chain model is able to capture price movements of a broader range of stocks. In this paper, under the Markov chain model, we consider an optimal stock selling rule and obtain its solution in terms of a set of threshold levels. In particular, we solve the corresponding dynamic programming problem and obtain these threshold levels. We point out that the standard smooth-fit method that works in a GBM setting is not adequate in one of the cases in this paper because of the lack of enough equations for the unknown parameters. To solve the problem, we need to explore other convexity conditions to determine uniquely these parameters. We also provide a set of sufficient conditions that guarantee their optimality. Numerical examples are reported to illustrate these results.

This paper is organized as follows. In §2, we formulate the problem and make a few assumptions. In §3, we study properties of the value functions, the associate HJB equations, and their solutions. In §4, we provide a set of sufficient conditions that guarantee the optimality of our selling rule. We also include three numerical examples in this section. Some concluding remarks are given in §5. Some technical results are provided in an appendix.

2 Problem Formulation

Let denote a two-state Markov chain with state space and generator , for given and . Let denote the stock price at time given by the equation

where represents the uptick return rate and the downtick return rate. Let denote the filtration generated by . Note that is observable and .

Let denote the fixed transaction cost. Given and , the objective of the problem is to choose an stopping time so as to maximize

where is the discount factor.

Let be the value function. Then it is easy to see that , , . Moreover, is convex in for fixed .

Let . Then the bigger root of is given by

Note that if , then following similar argument as in Guo and Zhang [5], we can show that it is optimal not to sell at all. In the rest of this paper, we only consider the case when , which implies . We summarize the conditions to be imposed in the rest of this paper:

-

(A1) and ;

-

(A2) .

Let denote the stationary distribution of and let . Then, . Moreover, it is easy to see that . This implies . Therefore, .

Note that, for any stopping time ,

In order to have finite , necessarily

In view of this, needs to be at most linear growth in . In addition, note that the stock price is differentiable and the value of can be given in terms of the derivative of .

3 HJB Equations

Let denote the generator of , i.e., for any differentiable functions , ,

where denotes the derivative of with respect to . The associated HJB equations should have the form:

| (1) |

In this section, we solve these HJB equations. First, if the price is small, then one should hold the position because the price is not attractive regardless or 2. In view of this, we expect the existence of such that no selling is . The corresponding interval gives a continuation region. Note that implies . On this interval, the equalities , , must hold. Using the generator , we can write

Using the first equation, we write

Substitute this into the second equation and simplify to obtain

| (2) |

where

| (3) |

Let and denote the roots of

| (4) |

Then,

| (5) |

The general solution to (2) can be given as

for some constants and .

On , the convexity condition implies that is bounded. Necessarily, . Therefore, . Substitute this back into the first equation to obtain , where .

Recall that is observable. One should hold the position longer under the condition (uptick) than that under (downtick). In view of this, we consider the HJB equations on for some . The idea is to sell if and hold if till reaching . Clearly, and , on . Using this, we solve the equation

which gives

It is easy to see a particular solution

| (6) |

Let . Then, the general solution can be given by

for any constant .

Next we consider two separate cases to continue solving the HJB equations.

Case I:

Assuming , we first show that . If not, we must have for . In order to satisfy the HJB equations (1), has to satisfy the inequality , for . Plugging in this inequality, we have

Therefore, , for . This contradicts . Hence .

In view of these, on , and . This means never sell when . Recall the linear growth property and nonnegativity of . It follows that because .

Next, we determine the values of and . Recall that and are convex on . Necessarily, they are continuous. In particular, they are continuous at . Therefore,

Solving these equations, we have

| (7) |

and

| (8) |

It is elementary to check that

| (9) |

The solutions to the HJB equations (1) should have the form:

| (10) |

Theorem 1

. Assume . Then the functions , , given above are continuous on and differentiable on . They satisfy the HJB equations (1). In particular, the following inequalities hold:

| (11) |

Proof. It is sufficient to show these four inequalities. First, note that implies . Under the condition , we have . The third inequality in (11) follows from . In addition, the first inequality follows from the second one because as shown in Appendix (Lemma 2). To show the second inequality, we claim that and

| (12) |

To see , notice that (9) implies

because (see Lemma 1 in Appendix). Therefore is positive, so is . To show (12), use again (9), which yields

This is equivalent to (12) because . Let . In view of the above claim and the definition of , it follows that, on ,

Consequently, is increasing on , which implies . Hence, is decreasing. Therefore, on , which implies the second inequality in (11).

It remains to show the last inequality in (11). This is equivalent to

It follows that

Using the notation and , we have

Therefore, we need

for . It suffices to show this inequality when . Using the expression in (9), we only have to show

Rewrite this to obtain

| (13) |

Now, if (i.e., ), then we are done because . Otherwise, . Under this condition, we rewrite (13) as

which is equivalent to

| (14) |

Note that

| (15) |

Therefore, implies that . Under this condition, it is easy to check

Square both sides of (14) to obtain

Simplify this inequality to have

Furthermore, using (15), we have . Substitute this into the above inequality to obtain

This is equivalent to

which leads , which holds under the assumption . Therefore, on . The proof is compete.

Case II:

We consider the second case when . Note that a large encourages selling sooner. Naturally, we expect . The solutions to the HJB equations (1) should have the form:

| (16) |

We need to determine the values of , , , and . Again, following the continuity of the value functions at and , we have

| (17) |

Note that there are only three equations, which are not adequate to determine uniquely the values of the four unknowns. We need to find further conditions. Note that to satisfy the HJB equations (1), the following inequalities have to hold:

| (18) |

| (19) |

| (20) |

First, we consider (18). Note that convexity of at implies

| (21) |

Under this condition, following from similar argument used to prove the second inequality in (11) with for possibly different , we can show the second inequality in (18) holds, so does the first one. Therefore, the inequalities in (18) are equivalent to (21), which can be simplified and written as:

| (22) |

Next, we consider (20). The first inequality implies

It follows that

| (23) |

The second inequality in (20) is automatically satisfied because .

Finally, go back to (19). Again, the convexity of at yields

| (24) |

It follows from the third equality in (17) that

| (25) |

Under the condition , it is easy to see . Note that under . Let . Then, it is direct to check that , , . Therefore, is increasing on . Thus, on , which implies is decreasing. Therefore, on . The first inequality in (19) follows from (24).

Use (25) and rewrite (24) to obtain

which leads to

Recall that and . It follows that

Combining the opposite inequality (23), we have

Next, we claim that the second inequality in (19) follows from

| (26) |

To see this, let

Then, using and , the second inequality becomes on . Under (26), . Note also that

In addition, . In view of this, is increasing. Therefore, on , which implies is decreasing. So on .

Furthermore, using (17), we can rewrite (26) as

which in turn gives

This inequality is equivalent to

because as shown in Lemma 4 in Appendix.

In view of (22), has to be bounded above by

In view of Lemma 3 (Appendix), we have

Therefore, an upper bound for

To obtain , we only need to solve the first two equations in (17). Eliminating , we obtain

| (27) |

on .

Let , Then it is easy to check that is positive, so is . In addition, because . Furthermore, it can be shown that , which implies that increasing. Using (24) to obtain , which implies is decreasing. Therefore, has a unique zero on .

We have proved the following results.

Theorem 2

Remark 2

. Note that . Recall that is decreasing on . A sufficient condition for is .

4 Verification Theorems and Numerical Examples

First, we give two verification theorems depending on and . We only prove Theorem 3. The proof of Theorem 4 can be given in a similar way.

Theorem 3

. Assume the conditions of Theorem 1. Then, , . Moreover, let denote the continuation region. Then

is an optimal selling time.

Proof. We only sketch the proof because it is similar to that of Zhang and Zhang [17, Theorem 5]. For any given stoppting time and , we have

| (28) |

Recall the linear growth of and under (A2) as . The second term goes to 0 and Note also that the first term converges to . It follows that .

Theorem 4

. Assume the conditions of Theorem 2. Then, , . Moreover, let denote the continuation region. Then

is an optimal selling time.

Corollary 1

. Let denote the class of almost sure finite stopping times. Then,

Proof. Given , we have

Set to obtain

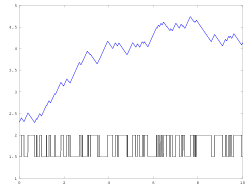

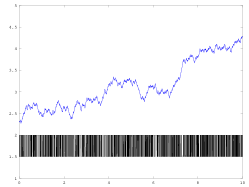

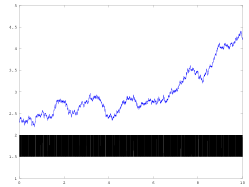

Example 1 (Convergence to a Brownian motion).

In this example, given , we consider

Using the asymptotic normality given in Yin and Zhang [16, Theorem 5.9], we can show that converges weakly to

where is a standard Brownian motion. Such a limit is the solution to the stochastic differential equation

It is elementary to show that, as ,

This implies that defined in (9) converges to the selling threshold obtained in ksendal [13, Example 10.2.2].

Taking and , we give sample paths of and with varying in Figure 1. It is clear from the pictures that as gets smaller and smaller, the fluctuation of is more and more rapidly and the corresponding approaches to a GBM.

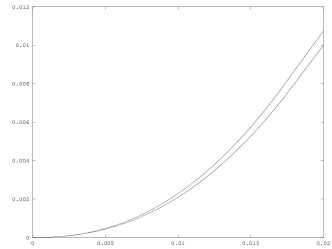

Example 2 (Case II).

In this example, we consider Case II with and use the following parameters

Solving the equation (27) with , we have and . The corresponding value functions are given in Figure 2, in which is given by the upper curve and the lower one.

Example 3 (Model Calibration and a Market Test).

First we give a model calibration method. We consider

with . Given , let , . Then, can be approximated by . To estimate and , given step size , let ,

and . Then, . In addition, using Yin an Zhang [16, Theorem 5.9], we can show

Let

Then, by the Law of Large Numbers, we have

Using , we have

Finally, we estimate and . Let . Then, .

Then, it follows that

Therefore, the jump rates are given by

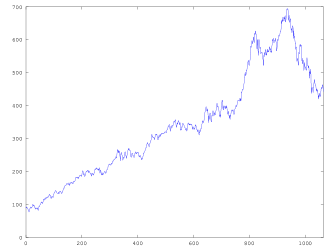

We test our selling rules using Apple Inc. (AAPL) daily closing prices during 2009/1/2 and 2013/3/28, sse Figure 3 (a). Suppose we owned 100 AAPL shares at the beginning of 2009. We evaluate at the end of each half year during this period based on that half year stock prices to determine if we should sell the shares in the near future.

We assume the risk free rate to be and transaction cost . We use the calibration method discussed earlier and obtain the following results.

| Periods | |||||

|---|---|---|---|---|---|

| 1st half of 2009 | 10.45 | -10.61 | 100.48 | 124.23 | -336.06 |

| 2nd half of 2009 | 3.21 | -2.32 | 102.15 | 141.44 | -217.41 |

| 1st half of 2010 | 3.06 | -3.15 | 97.98 | 127.02 | -83.18 |

| 2nd half of 2010 | 2.27 | -1.92 | 103.57 | 134.25 | -103.09 |

| 1st half of 2011 | 1.80 | -1.85 | 117.19 | 125.00 | -5.02 |

| 2nd half of 2011 | 3.01 | -2.72 | 97.98 | 107.95 | -60.56 |

| 1st half of 2012 | 5.39 | -4.80 | 108.21 | 127.19 | -185.32 |

| 2nd half of 2012 | 4.89 | -5.13 | 135.25 | 130.95 | 35.79 |

Table 1. Parameter Values at the End of Each Period

Note that in all periods . Therefore, only Case I applies in this example. In Table 1, we should hold through the next half year if and sell (following our selling rule) if . Clearly, a selling decision has to be made at the end of 2012. Using the parameter values , , , and , we obtain and the corresponding value functions , , which are plotted in Figure 3 (b). Therefore, one should sell as soon as turns to after the new year. This occurs on the second trading day (January 3) of 2013. The shares should be sold at the close of that day at $542.10/share. As can be seen in this example, our selling rule helps to achieve the goal of letting your profits run and cutting your losses short.

5 Conclusion

In this paper, we considered an optimal stock selling rule under a Markov chain model. The model is natural for financial markets due to its simple structure and the solutions obtained are intuitive and easy to implement.

It would be interesting to consider more general models with multi-scale structure as treated in Yin and Zhang [16] so as to capture both long-term and short-term market movements. Such extension and related optimization problems could be subjects of future studies.

6 Appendix

Lemma 1

. Under the assumption , the bigger root of (4) .

Proof. Recall the definition of and given in (3). It is easy to check implies

This leads to

Therefore, we have .

Lemma 2

. Let , where is given in (5). Then, .

Proof. To see , it suffices to show . Recall that . We only need to show , with and given in (3).

This is equivalent to

| (29) |

It is easy to check . Square both sides of (29) to obtain

Simplify this inequality to obtain

This clearly holds. Therefore, .

Similarly, to show , it suffices to show . This is equivalent to

Square and simplify to obtain . This holds because and .

Lemma 3

. Under , we have

Proof. It is easy to see this inequality is equivalent to . Using the definition of and noting that , we have

If , then we are done. Otherwise, square both sides to obtain

Simplify this inequality to have

which clearly holds because and .

Lemma 4

. Under , we have

| (30) |

which implies .

Proof. Let . Using the definition of , (30) is equivalent to

Therefore, we have

Multiply both sides by and rearrange the terms to obtain

Square both sides and simplify to have

which is exactly the assumption . This completes the proof.

References

- [1] B.R. Barmish and J.A. Primbs, On market-neutral stock trading arbitrage via linear feedback, Proc. American Control Conference, Montreal, 2012.

- [2] D. Duffie, Dynamic Asset Pricing Theory, 2nd Ed., Princeton University Press, Princeton, NJ, 1996.

- [3] R. J. Elliott and P. E. Kopp, Mathematics of Financial Markets, Springer-Verlag, New York, 1998.

- [4] J.P. Fouque, G. Papanicolaou, and R.K. Sircar, Derivatives in Financial Markets with Stochastic Volatility, Cambridge University Press, 2000.

- [5] X. Guo and Q. Zhang, Optimal selling rules in a regime switching model, IEEE Transactions on Automatic Control, Vol. 50, pp. 1450-1455, (2005).

- [6] K. Helmes, Computing optimal selling rules for stocks using linear programming, Mathematics of Finance, G. Yin and Q. Zhang, (Eds), Contemporary Mathematics, American Mathematical Society, pp. 187-198, (2004).

- [7] J. C. Hull, Options, Futures, and Other Derivatives, 3rd Ed., Prentice Hall, Upper Saddle River, NJ, 1997.

- [8] I. Karatzas and S. E. Shreve, Methods of Mathematical Finance, Springer, New York, 1998.

- [9] A. Lkka and M. Zervos, Long-term optimal real investment strategies in the presence of adjustment costs, preprint, (2007).

- [10] A. Merhi and M. Zervos, A model for reversible investment capacity expansion, SIAM J. Contr. Optim., Vol. 46, pp. 839-876, (2007).

- [11] M. Musiela and M. Rutkowski, Martingale Methods in Financial Modeling, Springer, New York, 1997.

- [12] R. Norberg, The Markov chain market, ASTIN Bulletin, Vol. 33, pp. 265-287, (2003).

- [13] B. ksendal, Stochastic Differential Equations, 6th Ed., Springer-Verlag, New York, 2003.

- [14] J. van der Hoek and R.J. Elliott, American option prices in a Markov chain market model, Applied Stochastic Models in Business and Industry, Vol. 28, pp. 35–59, (2012).

- [15] G. Yin, R.H. Liu, and Q. Zhang, Recursive algorithms for stock Liquidation: A stochastic optimization approach, SIAM J. on Optimization, Vol. 13 (2002), 240-263.

- [16] G. Yin and Q. Zhang, Continuous-Time Markov Chains and Applications, A Two-Time-Scale Approach, 2nd Ed, Springer, New York, 2013.

- [17] H. Zhang and Q. Zhang, Trading a mean-reverting asset: Buy low and sell high, Automatica, Vol. 44, pp. 1511-1518, (2008).

- [18] Q. Zhang, Stock trading: An optimal selling rule, SIAM J. on Control and Optimization, Vol. 40, pp. 64-87, (2001).