Characterizing financial crisis by means of the three states random field Ising model

Abstract

We propose a formula of time-series prediction by means of three states random field Ising model (RFIM). At the economic crisis due to disasters or international disputes, the stock price suddenly drops. The macroscopic phenomena should be explained from the corresponding microscopic view point because there are existing a huge number of active traders behind the crushes. Hence, here we attempt to model the artificial financial market in which each trader can choose his/her decision among ‘buying’, ‘selling’ or ‘staying (taking a wait-and-see attitude)’, each of which corresponds to a realization of the three state Ising spin, namely, , and , respectively. The decision making of traders is given by the Gibbs-Boltzmann distribution with the energy function. The energy function contains three distinct terms, namely, the ferromagnetic two-body interaction term (endogenous information), random field term as external information (exogenous news), and chemical potential term which controls the number of traders who are watching the market calmly at the instance. We specify the details of the model system from the past financial market data to determine the conjugate hyper-parameters and draw each parameter flow as a function of time-step. Especially we will examine to what extent one can characterize the crisis by means of a brand-new order parameter — ‘turnover’ — which is defined as the number of active traders who post their decisions , instead of .

1 Introduction

Individual human behaviour including human mental state is an attractive topic for both scientists and engineers. However, it is still extremely difficult for us to tackle the problem by making use of scientifically reliable investigation. This is because there exists quite large person-to-person fluctuation in the observation of individual behaviour.

On the other hand, in our human ‘collective’ behaviour instead of individual, we sometimes observe several universal facts which seem to be suitable materials for computer scientist to figure out the phenomena through sophisticated approaches such as agent-based simulations. In fact, collective behaviour of interacting agents such as flying birds, moving insects or swimming fishes shows highly non-trivial properties. As well-known especially in the research field of engineering, as a simplest and effective algorithm in computer simulations for flocks of intelligent agents, say, animals such as starlings, the so-called BOIDS founded by Reynolds Reynolds has been widely used not only in the field of computer graphics but also in various other research fields including ethology, physics, control theory, economics, and so on Makiguchi . The BOIDS simulates the collective behaviour of animal flocks by taking into account only a few simple rules for each interacting ‘intelligent’ agent.

In the literature of behavioral economics Kahneman , a concept of the so-called information cascade is well-known as a result of such human collective behaviour. This concept means that at the financial crisis, traders tend to behave according to the ‘mood’ (atmosphere) in society (financial market) and they incline to take rather ‘irrational’ strategies in some sense.

Apparently, one of the key measurements to understand the information cascade is ‘correlation’ between ingredients in the societies (systems). For instance, in particular for financial markets, cross-correlations between stocks, traders are quite important to figure out the human collective phenomena. As the correlation could be found in various scale-lengths, from macroscopic stock price level to microscopic trader’s level, the information cascade also might be observed ‘hierarchically’ in such various scales from prices of several stocks to ways (strategies) of trader’s decision making.

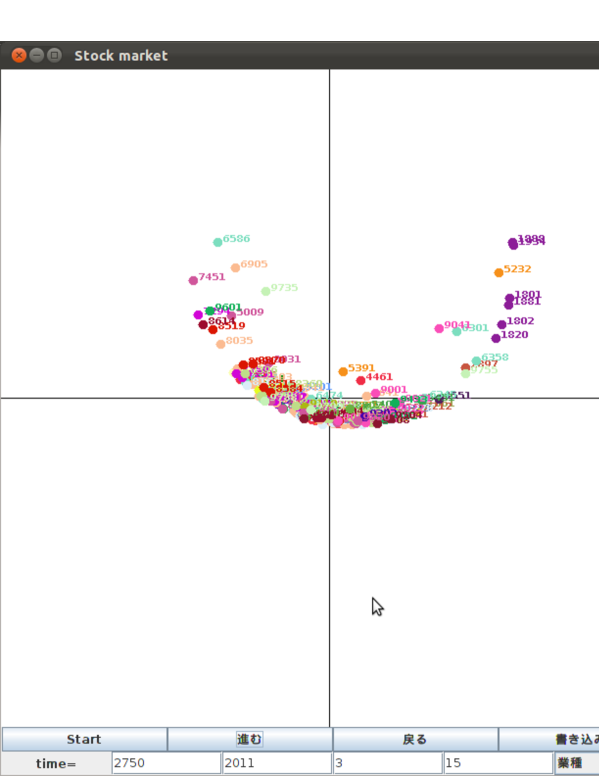

Turning now to the situation of Japan, after the earthquake on 11th March 2011, Japanese NIKKEI stock market quickly responded to the crisis and quite a lot of traders sold their stocks of companies whose branches or plants are located in that disaster stricken area. As the result, the Nikkei stock average suddenly drops after the crisis ISI ; IHSI .

It might be quite important for us to make an attempt to bring out more ‘microscopic’ useful information, which is never obtained from the averaged macroscopic quantities such as stock average, about the market. As a candidate of such ‘microscopic information’, we can use the (linear) correlation coefficient based on the two-body interactions between stocks Mantegna ; Anirban . To make out the mechanism of financial crisis, it might be helpful for us to visualize such correlations in stocks and compare the dynamical behaviour of the correlation before and after crisis.

In order to show and explain the cascade, we visualized the correlation of each stock in two-dimension ISI ; IHSI . We specified each location of stocks from a given set of the distances by making use of the so-called multi-dimensional scaling (MDS) MDS .

On the other hand, the macroscopic phenomena should be explained from the corresponding microscopic view point because there are existing a huge number of active traders behind the crushes. In the reference IHSI , we proposed a theoretical framework to predict several time-series simultaneously by using cross-correlations in financial markets. The justification of this assumption was numerically checked for the empirical Japanese stock data, for instance, those around 11 March 2011, and for foreign currency exchange rates around Greek crisis in spring 2010.

However, in the previous study IHSI , inspired by the study of Kaizoji Kaizoji2000 , we utilized Ising model and assumed that each trader does not stay at all for trading. Apparently, it is not realistic situation for trader’s decision making. Hence, here we attempt to model the artificial financial market in which each trader can choose his/her decision among ‘buying’, ‘selling’ or ‘staying (taking a wait-and-see attitude)’, each of which corresponds to a realization of the three states Ising spin, namely, , and , respectively. Especially we will examine to what extent one can characterize the crisis by means of an order parameter — ‘turnover’ — which is defined as the number of ‘active traders’ who post their decision , instead of .

This paper is organized as follows. In the next section 2, we introduce the three states RFIM and explain the thermodynamic properties including the critical phenomena such as phase transitions. In section 3, we construct a prediction formula based on the model introduced in the previous section 2. We introduce ‘turnover’ as an order parameter to characterize the crisis. In section 4, we carry out computer simulations with the assistance of empirical data set to check the usefulness of our approach. The last section 5 is concluding remark.

2 There states random field Ising model

In this paper, we extend the prediction model based on Ising model given by Kaizoji2000 ; IHSI by means of three states random field Ising model. Before we construct the prediction model for financial time-series, we consider the thermodynamics of the following Hamiltonian (energy function) that describes decision makings of traders (each of the traders is specified by a label ).

| (1) |

where each spin can take and , and here we assume that all traders are located on a complete graph (they are fully connected). We should keep in mind that in the previous studies Kaizoji2000 ; IHSI , a spin takes only (buy) and (sell). However, in our model system, besides , can take which means that the trader takes a wait-and-see attitude (stays). Namely,

| (2) |

The first term in the right hand side of (1) causes the collective behavior of the traders because the Hamiltonian (1) decreases when all traders tend to take the same decision. In this sense, the first term is regarded as endogenous information for the traders. On the other hand, the second term denotes the exogenous information which is a kind of market information available for all traders. Here one can choose the following market trend during the past -steps as .

| (3) |

where denotes a real price at time . The third term appearing in the right hand side of equation (1) controls the number of traders who are staying at the moment . From the view point of spin systems, is regarded as a ‘random field’ on each spin because the might obey a stochastic process. Therefore, the spin system described by (1) should be refereed to as random field Ising model (RFIM). Obviously, the parameter is regarded as ‘chemical potential’ in the literature of physics. For , most of the traders take ‘buying’ or ‘selling’ instead of ‘staying’ from the view point of minimization of the Hamiltonian (1). In the limit of , the fraction of traders who take vanishes, namely, the system is identical to the conventional Ising model Kaizoji2000 in this limit. As we will see later, the set of parameters (what we call ‘hyper-parameters’) should be estimated (learned) from the past time-series.

In this paper, we shall focus on the modification by means of the above three states RFIM. We investigate to what extent the prediction performance is improved. Moreover, we attempt to quantify the number of traders who are staying at the crushes in order to characterizing the financial crisis.

2.1 Equations of state

To make a link between the prediction model and statistical physics of the three states RFIM, we should investigate the equilibrium state described by the Hamiltonian (1) at unit temperature. According to statistical mechanics, each microscopic state of the Hamiltonian (1) obeys the distribution , where the normalization constant is refereed to as partition function and it is given by

| (4) |

where we defined . Here we should keep in mind that arbitrary two traders are connected each other. By using a trivial equality concerning the Gaussian integral

| (5) |

the system is reduced to a single spin ‘’ problem in the limit of as

| (6) | |||||

where we used the saddle point method to evaluate the integrals with respect to and . appearing in the final form (6) is regarded as a free energy density and it is given by

| (7) |

Then, the saddle point equation leads to

| (8) |

Apparently, the above stands for ‘magnetization’ in the literature of statistical physics, however, as we will see later, it corresponds to the ‘return’ in the context of time-series prediction for the price. This is because the number of buyers is larger than that of the sellers if the is positive, and as the result, the price increases definitely. Another saddle point equation gives

| (9) |

It should be noticed that from , we have . Hence, by substituting the into (8) and (9), we immediately have the following equations of state

| (10) | |||||

| (11) |

We should bear in mind that is a ‘slave variable’ and it is completely determined by . However, itself has an important meaning to characterize the market because the is regarded as the number of traders who are actually trading (instead of staying). In this sense, the could be ‘turnover’ in the context of financial markets. In other words, the turnover is a measurement to quantify the activity of the market, and a large means high activity of the market. Strictly speaking, the could not be regarded as ‘turnover’ because in our modeling, we assumed that each trader posts unit volume to the market. However, by introducing as volume for each trader and replacing the spin variables in (1) as , is regarded as turnover in its original meaning.

2.2 Equilibrium states and phase transitions

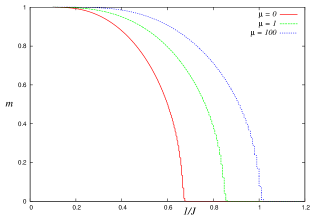

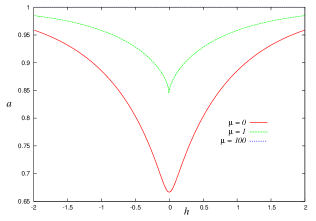

We first consider the case of in (1) or (10) and (11). For this case, we can solve the equations of states (10)(11) numerically. We show the -dependence of magnetization in Fig. 2 (left). From this panel, we find that the magnetization monotonically decreases as increases for arbitrary finite and it drops to zero at the critical point . The critical point is dependent on the value of . In order to investigate the -dependence of the critical point , we expand the right hand side of (10) up to the first order of . Then, we have

| (13) |

It should be noted that for the conventional Ising model Kaizoji2000 ; IHSI is recovered in the limit of .

We next plot the -dependence of the turnover in the right panel of Fig. 2. From this panel, we are confirmed that above the critical point, the turnover takes a constant value:

| (14) |

Here we should notice again that is recovered in the limit of , which means that there is no trader who is staying at the moment.

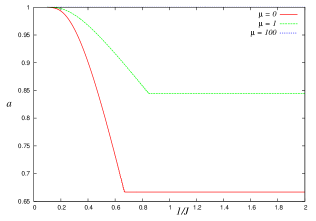

We next evaluate the behavior of magnetization as a function of keeping the value of as (we set for simplicity). Then, one observes from Fig. 3 (left) that the system undergoes a first order phase transition which is specified by a transition between bi-stable states in the free energy, namely, the states and . The critical values at the critical point is determined by

| (15) |

We should notice that one recovers , which is the result for the conventional Ising model Kaizoji2000 , in the limit of . For the case of , the critical values is given by

| (16) |

Then, the critical point is obtained as a solution of the following equation.

| (17) |

In the next section, taking into account the above equilibrium properties and phase transitions, we shall construct the prediction model based on the Hamiltonian (1) and evaluate the statistical performance by means of computer simulations with the assistance of empirical data analysis.

3 The prediction model

In this section, we construct our prediction model. Let us define as the price at time . Then, the return, which is defined as the difference between prices at successive two time steps and , is given by

| (18) |

To construct the return from the microscopic view point, we assume that each trader () buys or sells unit-volume, or stays at each time step . Then, let us call the group of buyers as , whereas the group of sellers is referred to as . As we are dealing with three distinct states including ‘staying’, we define the group of traders who are staying by . Thus, the total volumes of buying, selling and staying are explicitly given by

| (19) |

respectively. Apparently, the total number of traders should be conserved, namely, the condition holds.

Then, the return is naturally defined by means of (19) as

| (20) |

where is a positive constant. Namely, when the volume of buyers is greater than that of sellers, , the return becomes positive . As the result, the price should be increased at the next time step as .

3.1 The Ising spin representation

The making decision of each trader () is now obtained simply by an Ising spin (2). The return is also simplified as

| (21) |

where we set to make the return:

| (22) |

satisfying . Thus, corresponds to the so-called ‘magnetization’ in statistical physics, and the update rule of the price is written in terms of the magnetization as

| (23) |

as we mentioned before.

3.2 The Boltzmann-Gibbs distribution

It should be noticed that the state vectors of the traders: are determined so as to minimize the Hamiltonian (1) from the argument in the previous section. For most of the cases, the solution should be unique. However, in realistic financial markets, the decisions by traders should be much more ‘diverse’. Thus, here we consider statistical ensemble of traders and define the distribution of the ensemble by . Then, we shall look for the suitable distribution which maximizes the so-called Shannon’s entropy

| (24) |

under two distinct constraints:

| (25) |

and we choose the which minimizes the following functional :

| (26) | |||||

where are Lagrange’s multipliers. After some easy algebra, we immediately obtain the solution

| (27) |

where stands for the inverse-temperature. In following, we choose unit temperature .

Here we should assume that the magnetization as a return at time is given by the expectation of the quantity over the distribution (27), that is,

| (28) |

where we defined

| (29) |

Thus, we have the following prediction formula

| (30) | |||||

| (31) | |||||

| (32) | |||||

| (33) | |||||

| (34) |

where we introduced the cost function to determine the parameters by means of gradient descent learning as

| (35) |

and is a learning rate. To obtain the explicit form of the learning equations, we take the derivatives as

| (37) | |||||

| (38) | |||||

In the above expressions, is evaluated for the true price by

| (39) |

By substituting and the set of parameters into (11), we obtain the turnover at each time step as

| (40) |

We should remember that we defined the exogenous information by the trend and here we choose to evaluate the trend and .

4 Computer simulations

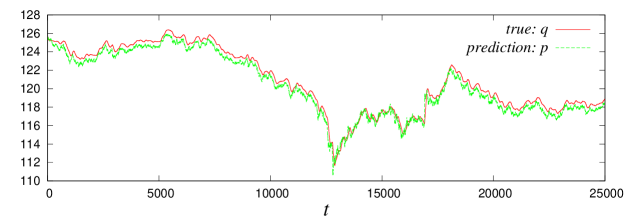

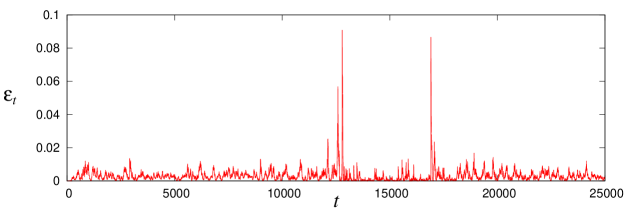

In Fig. 4, we show the true time-series which contains a crush and the prediction with mean-square error . The empirical true time-series is chosen from EUR/JPY exchange rate (high frequency tick-by-tick data) from 25th April 2010 to 13th May 2010 (it is the same data set as in the reference IHSI ). We set [ticks], and chose as the initial values of parameters. From these panels, we confirm that the mean-square error takes small value within at most several percent although the error increases around the crush. Thus, we might conclude that our three states RFIM works well on the prediction of financial data having a crush.

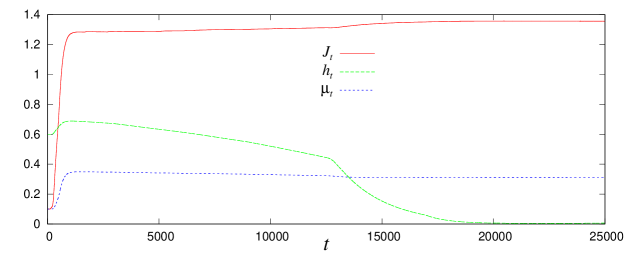

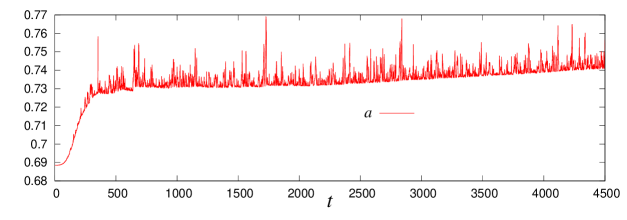

We next consider the flow of parameters which evolve across the crush. The result is shown in Fig. 5. From this figure, we clearly find that the strength of exogenous information drops to zero after the crush. Chemical potential and strength of endogenous information converge to and , respectively. In our previous study IHSI , as the critical point was for , the strength of endogenous information converged to the critical value . However, in the three states RFIM with and , the critical point is sifted to (see Fig. 2 (left)). Therefore, in this simulation, these two parameters converge to the corresponding critical point . From the result, we conclude that the system described by the Hamiltonian (1) automatically moves to the critical point after the crush.

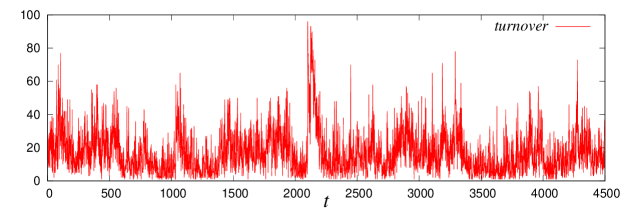

We next utilize the USD/JPY exchange rate from 12th August 2012 to 24th August 2012 as true time-series. It should be noted that the duration of this data is 1 minutes, hence, the data is not tick-by-tick data. In the simulation for this data set, we set [min]. We show the simulated turnover with the corresponding true value in Fig. 6.

From these panels, we find that the empirical data for the turnover increases instantaneously around the crush, whereas the simulated turnover does not show such striking feature although it possess a relatively large peak just before the crush. In order to convince ourselves that the simulated turnover can characterize the crush, we should carry out much more extensive simulations for various empirical data. It should be addressed as our future study.

4.1 Comparison with the conventional Ising model

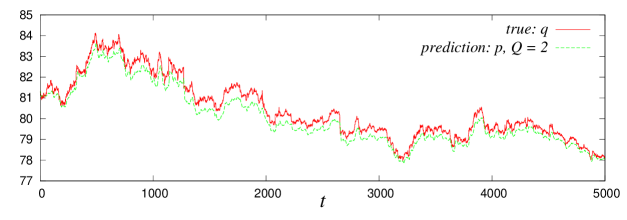

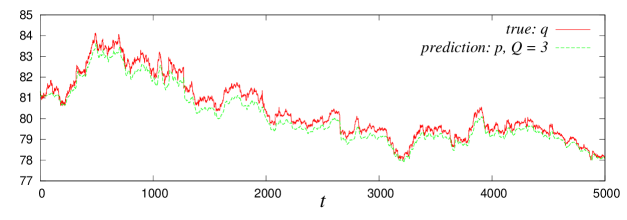

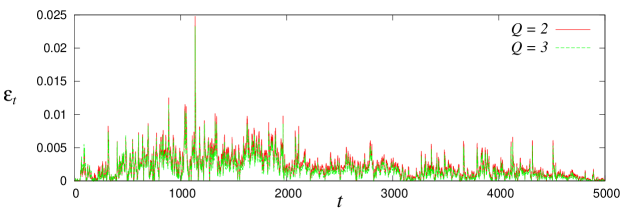

Finally we compare our result with that of the conventional Ising model Kaizoji2000 . Here we used the USD/JPY exchange rate from 1st March 2012 to 31st July 2012, whose minimum duration is 30 minutes. We choose the width of the time-window [min]. The initial values of parameters are set to for the conventional Ising model, whereas are chosen as for the three states RFIM. The results are shown in Fig. 7. From this figure as a limited result, we find that the performance of the prediction by the three states RFIM is superior to that of the conventional Ising model.

5 Concluding remark

In this paper, we extended the formulation of time-series prediction using Ising model given by Kaizoji (2001) Kaizoji2000 or Ibuki et. al. (2012) IHSI by means of three states RFIM. We found that the crisis could be ‘partially” characterized by the simulated turnover. We also confirmed that the three states in each trader’s decision making apparently improves the statistical performance in the prediction.

Acknowledgements

This work was financially supported by Grant-in-Aid for Scientific Research (C) of Japan Society for the Promotion of Science, No. 22500195. The authors acknowledge Takero Ibuki, Shunsuke Higano and Sei Suzuki for fruitful discussion and useful comments. We thank organizers of Econophysics-Kolkata VII, especially, Frederic Abergel, Anirban Chakraborti, Asim K. Ghosh, Bikas K. Chakrabarti and Hideaki Aoyama.

References

- (1) C.W. Reynolds, Flocks, Herds, and Schools: A Distributed Behavioral Model, Computer Graphics 21, 25 (1987).

- (2) M. Makiguchi and J. Inoue, Numerical Study on the Emergence of Anisotropy in Artificial Flocks: A BOIDS Modelling and Simulations of Empirical Findings, Proceedings of the Operational Research Society Simulation Workshop 2010 (SW10), CD-ROM, pp. 96-102 (the preprint version, arxiv:1004 3837) (2010).

- (3) D. Kahbeman and A. Tversky, Econometrica 47, No.2, 263 (1979).

- (4) T. Ibuki, S. Suzuki and J. Inoue, New Economic Windows (Proceedings of Econophysics-Kolkata VI), Springer-Verlag (Milan, Italy), pp.239-259 (2013).

- (5) T. Ibuki, S. Higano, S. Suzuki and J. Inoue, Hierarchical information cascade: visualization and prediction of human collective behaviour at financial crisis by using stock-correlation, ASE Human Journal 1, Issue 2, pp. 74-87 (2012).

- (6) R. Mantegna, Euro. J. Phys. B 11, 193 (1999).

- (7) J.-O. Onnela, A. Chakrabarti, K. Kaski, J. Kertesz and A. Kanto, Phys. Rev. E 68, 056110 (2003).

- (8) I. Borg and P. Groenen, Modern Multidimensional Scaling: theory and applications, Springer-Verlag, New York (2005).

- (9) http://finance.yahoo.co.jp/

- (10) T. Kaizoji, Physica A 287, 493 (2000).