Riesz representation and optimal stopping with two case studies

Abstract

In this paper we demonstrate that the Riesz representation of excessive functions is a useful and enlightening tool to study optimal stopping problems. After a short general discussion of the Riesz representation we concretize, firstly, on a -dimensional and, secondly, a space-time one-dimensional geometric Brownian motion. After this, two classical optimal stopping problems are discussed: 1) the optimal investment problem and 2) the valuation of the American put option. It is seen in both of these problems that the boundary of the stopping region can be characterized as a unique solution of an integral equation arising immediately from the Riesz representation of the value function. In Problem 2 the derived equation coincides with the standard well-known equation found in the literature.

keywords:

[class=AMS]keywords:

1 Introduction

An optimal stopping problem (OSP) can be formulated as follows: Find a function (value function) and a stopping time (optimal stopping time) such that

| (*) |

where is a strong Markov process taking values in is the time horizon of the problem, is the set of all stopping times in the natural filtration of with values in , and the function (reward function) is often assumed to be non-negative and continuous. In case, in (* ‣ 1) we define

Notice that we use boldface letters to denote non-random vectors and matrices.

Optimal stopping problems arise naturally in many different areas, such as stochastic calculus (maximal inequalities), mathematical statistics (sequential analysis), and mathematical finance (pricing of American-type derivatives and real options), for these applications and further references, see, e.g.. the monographs [45] and [41]. An explicit solution for optimal stopping problems is often hard to find. Most examples are such that the underlying process is one-dimensional, often a diffusion process, and the time horizon is infinite, see e.g. [43, 4, 16] and the references therein. In contrast, the class of explicit examples with a multidimensional underlying process or with finite-time horizon are very limited. In this article, we describe a solution method for such problems based on the Riesz representation of the excessive functions. Notice that finite-time horizon problems with one-dimensional underlying process may be seen as two-dimensional where, in fact, we use the space-time process as the underlying.

More precisely, we consider the classical problem of optimal timing for an irreversible investment decision under the assumption that the revenue and cost factors follow (possibly correlated) geometric Brownian motions. It is furthermore assumed that the cost factors consist of many different sources making the model more realistic. For the mathematical formulation, see the expression for the value function in (3.1) in Section 3.

This problem has been studied extensively over the last decades, see, e.g., [30, 37, 23, 34, 21, 22, 12], and the references therein. However, no explicit description of the optimal stopping set is known so far to the best of our knowledge. We remark that in [23] a closed form solution was presented under certain conditions on the parameters and the optimal stopping time was claimed to be a hitting time of a halfspace. Unfortunately, it turned out that this closed form solution is only valid in trivial degenerated cases if the dimension is greater than one, see [12] and [34]. Because the structure of the reward function is additive and not multiplicative, there is no hope for such an easy solution in dimensions .

Our contribution hereby is to give an implicit description of the stopping region via an integral equation which has the boundary curve of the stopping region as a unique solution. It is seen in Section 3.6 that the equation has a fairly simple form especially in the two-dimensional case. We also present an ad hoc numerical metod for solving the integral equation.

The optimal investment problem in one dimension and with finite horizon is equivalent with the optimal stopping problem for finding the price of an American put option. To characterize the exercise boundary analytically and to develop numerical algorithms for finding it explicitly is an important and much studied topic in mathematical finance with the origin in McKean [31]. We refer to Peskir and Shiryayev [41] pp. 392-395 for a discussion with many references. Our main object of interest is an integral equation for the exercise boundary derived at the beginning of the 1990s in the papers by Kim [27], Jacka [24], and Carr, Jarrow and Myneni [8]. See also Myneni [33], Karatzas and Shreve [26], Peskir and Shiryayev [41], and Pham [42], Lamberton and Mikou [29] for the problem with underlying jump diffusions. The uniqueness of the solution of the equation was proved by Peskir [39] using a delicate stochastic analysis involving local times on curves. The method presented in this paper results to the same equation and we offer here a proof for the uniqueness based on the uniqueness of the representing measure in the Riesz representation of the value function.

To briefly motivate our approach, recall that a non-negative, measurable function is called -excessive for if the following two conditions hold:

Assuming that has continuous sample paths and the reward function is lower semicontinuous and positive satisfying the condition

it can be proved that the value function exists and is characterized as the smallest -excessive majorant of see Theorem 1 p. 124 in Shiryayev [45]. Moreover, if is continuous, the optimal stopping time is then known to be the first entrance time into the set

| (1.1) |

called the stopping region. For the finite time horizon problem, analogous results hold for the space-time process since herein the first co-ordinate can also be seen as a (deterministic) Markov process. To utilize these basic theoretical facts to solve explicit problems of interest, we need a good description of -excessive functions. Such a description – the Riesz representation – is discussed in the following section with emphasis on geometric Brownian motion. From Section 3 onward the paper is organised as follows. In Section 3 we study the optimal investment problem. Section 4 is on American put option and the paper is concluded with an appendix where proofs of some more technical results are given.

2 The Riesz representation of excessive functions

Our basic tool in analyzing and solving OSP is the Riesz representation of excessive functions according to which an excessive function can be written as the sum of a potential and a harmonic function. For thorough discussions of the Riesz representation and related matters in a general framework of Hunt processes, see Blumenthal and Getoor [5] and Chung and Walsh [14]. A more detailed representation of excessive functions is derived in the Martin boundary theory which, in particular, provides representations also for the harmonic functions, see Kunita and Watanabe [28] and Chung and Walsh [14] Chapter 14. For applications of the Riesz and the Martin representations in optimal stopping, see Salminen [43], Mordecki and Salminen [32], Christensen and Irle [12], and Crocce and Mordecki [15]. We also remark that in Christensen et al. [13] an alternative representation of excessive functions via expected suprema is utilized to characterize solutions of OSPs and, moreover, the connection with the Riesz representation is studied.

2.1 Multi-dimensional geometric Brownian motion

Let

be a -dimensional Brownian motion started from such that for

It is assumed that the non-negative definite matrix with is non-singular. A -dimensional geometric Brownian motion is a diffusion in with the components defined by

where for The differential operator associated with is of the form

where The (row) vector and the matrix are called the parameters of

To be able to apply the Riesz representation on this process should satisfy some regularity conditions. Firstly, we note that is a standard Markov process, see [5] p. 45. Secondly, has a resolvent kernel given by

| (2.1) |

where and is a transition density of The following proposition shows that the transition density may be taken with respect to a measure such that the corresponding resolvent is self-dual, i.e., in duality with itself relative to this means that relationship (2.2) below holds (see, e.g., [14] p. 344). Note that, since turns out to be absolutely continuous with respect to the Lebesgue measure, it is a matter of standardization to choose the Green kernel with respect to or with respect to the Lebesgue measure. In the following, we consider with respect to and use the notation

where satisfies some appropriate measurability and integrability conditions.

Proposition 2.1.

A -dimensional geometric Brownian motion as introduced above is self-dual, i.e. for all nonnegative measurable functions and it holds that

| (2.2) |

where is the measure on with the Lebesgue density

, , and denotes transposition.

Proof. See Section A1 in the appendix.

From the self duality it follows that Hypothesis B in [28, p. 498] holds. Notice also that since the dual resolvent kernel is identical with the resolvent kernel of the process associated with the dual resolvent is a standard Markov process identical in law with Consequently, the following (strongest) form of the Riesz representation theorem holds.

Theorem 2.2.

Let be a locally integrable -excessive function for a -dimensional geometric Brownian motion Then can be represented uniquely as the sum of a (non-negative) -harmonic function and an -potential . For the potential there exists a unique Radon measure depending on and on such that for all

| (2.3) |

Moreover, if is an open set having a compact closure in then is -harmonic on if and only if

We remark that the uniqueness of follows from the fact that is a self dual standard process (see, e.g., [28, Proposition 7.11 p. 503]). The statement about -harmonicity on can be deduced from ibid. Proposition 11.2 p. 513. Recall also that a non-negative measurable function is called -harmonic on if for all

| (2.4) |

where

In general, it is often difficult to find explicit expressions for the harmonic function in the Riesz decomposition presented in Theorem 2.2. The following proposition gives an easy condition under which vanishes.

Proposition 2.3.

Let be a bounded -excessive function for a -dimensional geometric Brownian motion . Then in the integral representation of given in Theorem 2.2.

Proof.

Take a sequence of compact subsets of such that as . Then, due to the boundedness of and the -harmonicity of , it holds that

∎

In case is smooth enough the representing measure can be obtained by applying the differential operator on This is made precise in the next

Proposition 2.4.

Let be a bounded -excessive function for a -dimensional geometric Brownian motion such that and let be a convex set with on . Furthermore, assume that is locally bounded around . Then the representing measure for on in the integral representation (2.3) is absolutely continuous with respect to the measure and is given for by

Proof. See Section A2 in the appendix.

2.2 Space-time geometric Brownian motion

We now consider a one-dimensional geometric Brownian motion in space-time, that is, the two-dimensional process with the state space The differential operator associated with is

| (2.5) |

We remark that the definition of an -excessive function for can be written in the form

where denotes the expectation operator associated with The resolvent kernel of can be defined as follows

| (2.6) |

where the transition density is taken with respect to the speed measure Notice that the kernel is also defined for

Proposition 2.5.

Let be an -excessive function of locally integrable on with respect to where denotes the Lebesgue measure. Then there exists a unique Radon measure on such that for

| (2.7) |

Proof.

It is proved in the appendix, see Section A3, that there exists a (dual) resolvent kernel such that for non-negative and measurable and

| (2.8) |

It can be checked then that Hypothesis (B) in Kunita and Watanabe [28, p. 498] holds. Consequently, see ibid Theorem 2 p. 505, has the Riesz representation

| (2.9) |

where is a Radon measure, is a harmonic function and the integration is over the set consisting of the points in the state space for which is a potential. The representation of in (2.9) as the sum of a potential and a harmonic function is unique. Moreover, the representing measure is unique, cf. [28, p. 503] . To deduce (2.7) notice firstly that since is a potential for all This follows readily from the definition of where it is stated that for Secondly, applying the Martin boundary theory (we omit the details) it can be proved that the harmonic function in (2.9) has the representation

| (2.10) |

where is a Radon measure on Also here the representing measure is uniquely determined by Combining (2.9) and (2.10) yields (2.7). ∎

Remark 2.1.

The proof of the duality does not use any particular properties of geometric Brownian motion (see Appendix). Consequently, the uniqueness of the representing measure in (2.7) holds for general space-time one-dimensional diffusions.

For -excessive functions that are smooth enough, we can describe the form of the measure more explicitly. The following result is useful generalization of [44, Proposition 2.2] based on Alsmeyer and Jaeger [3].

Proposition 2.6.

Let be a bounded -excessive function for on such that and are continuous on , and is absolutely continuous as a function of the second argument. Then the representing measure for on in the representation (2.7) is absolutely continuous with respect to the Lebesgue measure on and is given by

Proof.

By [17, Teorema 8.2] (see [18, Theorem 8.2] for an English translation) it holds that for all continuous functions with compact support in we have

Therefore, we have to prove that for

| (2.11) |

exists and is equal to . From [3, Corollary 2.2] it is seen that Itô’s formula can be applied to obtain -a.s.

Using a stopping argument and taking expectations yield the existence of the limit in (2.11) and, hence, the claim is proved. ∎

Remark 2.2.

The regularity assumptions in Proposition 2.4 are fairly strong and sometimes difficult to check. However, these are possible to relax by applying other extensions of the Ito formula (without the local time terms).

2.3 Basic idea of using the Riesz representation for solving optimal stopping problems

There is a wide range of different approaches for solving OSPs. Many of these are based on considering candidates for the value function of the form

| (2.12) |

for candidate sets and associated first hitting times , and then finding properties of the true value function that characterize one candidate set as the optimal stopping set. This idea can then be translated into a free-boundary problem, as described extensively in the monograph [41]. One of the major technical problems in using this approach is that a priori the candidate functions are typically not smooth on the boundary of , so that it is not straightforward to apply tools such as Itô’s formula or Dynkin’s lemma.

Our idea for treating OSPs using the Riesz representation theorem can basically be described as follows (for the infinite time horizon): Using the general results presented earlier in this section, we first show that the value function can be written in the form

for some known function . Now, in contrast to (2.12), we characterize the unknown stopping set by considering candidates for the value function of the form

| (2.13) |

and then identify one candidate set as the optimal stopping set. From a technical point of view, these candidate solutions are easy to handle, since the strong Markov property immediately yields that a variant of Dynkin’s formula holds true for all , see Lemma 3.6 below.

To show the applicability of this approach for treating concrete problems of interest, we concentrate in this article on two case studies, namely the multidimensional optimal investment problem with infinite time horizon in Section 3 and the American put problem in Section 4. Notice that the latter problem can be viewed as the optimal investment problem under a finite time horizon with .

3 Optimal investment problem

In this section we concentrate on one of the most famous OSPs in continuous time with multidimensional underlying process: the optimal investment problem, which goes back to [30]. The value function associated with the optimal investment problem is given by

| (3.1) |

Here, we assume the time horizon to be infinite, i.e. , , is a weight vector, and is a -dimensional geometric Brownian motion as defined in Subsection 2.1 with the indices and running from 0 to As discussed in [34] and [12], we furthermore assume that to guarantee the value function to be finite and the optimal stopping time not to be infinite a.s.

3.1 Problem reduction

First, by the explicit dependence of on the starting point, we see that for all , where we write . Therefore, we may take . Because the reward function is homogeneous, it is standard to reduce the dimension of the problem, see e.g. [34]. To recall this briefly, notice that for all and all it holds that

where are geometric Brownian motions under the measure given by

To be more explicit, under has drift and volatility . Consequently, we may, without loss of generality, take (a positive constant).

To summarize, we consider the optimal stopping problem

| (3.2) |

that is, an optimal stopping problem of the form (* ‣ 1) with

where, for notational convenience, the problem (3.2) is formulated for under (instead of the transformed process ). A typical assumption in the literature for this problem is that for , see [23, 37]. This guarantees that the optimal stopping time is a.s. finite. Since some arguments can be shortened (see e.g. Lemma 3.1), we also use this assumption throughout Section 3.

3.2 Preliminary results

We first collect some elementary results of the optimal stopping set as defined in (1.1). Similar results and lines of argument can also be found in [37, 38].

Lemma 3.1.

-

(i)

is a subset of

-

(ii)

is a closed convex set.

-

(iii)

is south-west-connected, that is if , then so is for all , where we understand componentwise.

Proof.

For note that if , then the reward for immediate stopping in is 0; since, obviously, , cannot be in the optimal stopping set. Furthermore, if , then is -subharmonic in a neighborhood of , so that at it is also not optimal to stop. Moreover, since and are continuous (for the latter claim, see, e.g., [5] p. 85) it follows that cf. (1.1), is closed. For convexity, take , and let be a stopping time. Then we have

which proves that , i.e., is convex. For , note that for and , it holds for all stopping times

where we used for the second inequality that, by our assumption on the drift, i.e., for all and since , the process is a nonnegative supermartingale. This proves that . ∎

3.3 Integral representation of the value function

By the general theory of -excessive functions described in Section 2, we know that the value function has the representation

| (3.3) |

where is an -harmonic function. This is our starting point for solving the optimal stopping problem (3.2). We check first that the value function has enough regularity. This is formulated in the next lemma.

Lemma 3.2.

It holds that and . Furthermore, is locally bounded around , i.e. for each , there exists such that is bounded on

Proof. See Section A4 in the appendix.

Using now the results obtained in Subsection 2.1 we obtain the explicit form of the integral representation of the value function.

Theorem 3.3.

For all it holds that

| (3.4) |

where

Proof.

First note that in the representation (3.3), the measure vanishes on since is -harmonic on the continuation set. Since is bounded, so is . Using this fact together with Lemma 3.2 and Lemma 3.1, Propositions 2.3 and 2.4 are applicable and yield that and on

But since on , we obtain

which gives the result. ∎

Evaluating (3.4) at we obtain the following corollary.

Corollary 3.4.

For all

| (3.5) |

3.4 Uniqueness of the solution of the integral equation

In the previous section we have found the identity (3.5) which can be seen as an equation for the unknown boundary of the stopping set. When analyzing this equation from a purely analytical point of view, there does not seem to be much hope that this equation would characterize the manifold uniquely. However, using a probabilistic reasoning based on our integral representation, we now show that is indeed uniquely determined by (3.5). More precisely we prove

Theorem 3.5.

Let be a nonempty, south-west connected, convex set such that

and assume that for all it holds

| (3.6) |

Then .

In the proof of this theorem, we frequently make use of the following well-known version of Dynkin’s formula for functions of form (3.3). The proof is an easy application of the strong Markov property and can be found in Section A5 in the appendix.

Lemma 3.6.

Let be a measurable function and

Then for each stopping time and each

| (3.7) |

Proof of Theorem 3.5.

Write for

where We proceed in four steps:

- 1.

- 2.

-

3.

:

Let and write . Then by step 1, Lemma 3.6, and step 2On the other hand, by Lemma 3.6 applied to , i.e. to ,

Subtracting yields that . Since this equation holds for all and on , we obtain

(3.8) Now, if there would exist , by the closeness of , the boundary of the rectangular solid

has a positive surface area in . By the southwest connectedness of , it holds that and , in contradiction to (3.8). This proves .

- 4.

∎

Remark 3.1.

In the previous proof, we use a similar structure as, e.g., in the proof of the uniqueness in [39].

3.5 Solution of the investment problem in case

To understand how Theorem 3.5 can be used to solve OSP (3.2) explicitly, we consider the case and In other words, we consider the problem connected to pricing a perpetual American put with strike price in a Black-Scholes market. We refer to [31] for an early treatment of the problem. Hence, the underlying process is the geometric Brownian motion with drift parameter (the risk neutral interest rate) and volatility Recall (see Borodin and Salminen [6]) that the (symmetric) Green kernel with respect to the speed measure is given by

where

Lemma 3.1 shows that the optimal stopping problem is one-sided, i.e., there exists a boundary point such that . Corollary 3.4 and Theorem 3.5 characterize the boundary point as the unique solution to the equation

where and By straightforward calculations we obtain

| (3.9) |

which yields the well-known solution

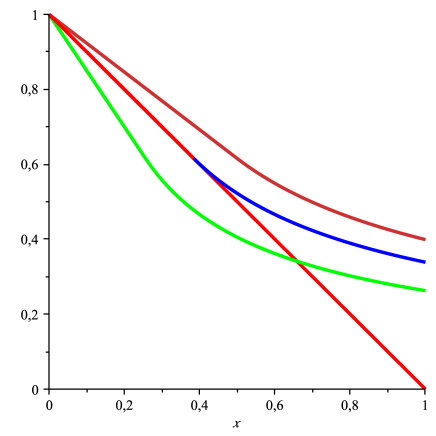

Figure 1 shows the graphs of three candidate value functions of the form (2.13) for the sets , where . As explained in Section 2.3, in contrast to candidate functions of the form (2.12), the functions are differentiable. It turns out that the true value function is the only candidate function that coincides with the reward function at the boundary point , in accordance with Theorem 3.5.

3.6 Explicit form of the integral equation in case

By parametrizing the boundary of the stopping set by a curve , we can rewrite equation (3.5) for the case more explictly as

| (3.10) |

where is the optimal value in the one-dimensional case given in (3.9). To make this integral equation explicit an expression for the Green kernel is needed. To this end, let be a 2-dimensional geometric Brownian motion started from as introduced in Section 2.1. The joint density of with respect to the Lebesgue measure is given by

| (3.11) |

where and

Introduce

with

The joint density of is obtained from (3.11):

with

Formula (29) in Erdelyi et al. p. 146 [20] yields

| (3.12) |

where is the modified Bessel function of second kind given by (see formula 9.6.21 in Abramowitz and Stegun p. 376 [1] and for other formulas, e.g., 9.6.13)

To find the resolvent kernel for consider for positive and

with

Consequently,

and, hence, from (3.12) we obtain the following expression for the resolvent kernel of with respect to the Lebesgue measure

where

Plugging this expression of the Green kernel in (3.10) (where we now have taken to be the Lebesgue measure on ) yields an explicit integral equation having the stopping boundary as a unique solution.

3.7 On the numerical solution to the integral equation

The numerical solution to the integral equation (3.5) does not seem to be standard. Here, we present an ad hoc method that works fine for the optimal investment problem. We concentrate on the case although a similar approach could be applied in higher dimensions also. The basic observation is that the equation

| (3.13) |

for the unknown boundary can be written in fixed point form as

where the (nonlinear) operator is given by

One can start with a first approximation for the unknown boundary (for example, the straight line described in [23]). Using a suitable discretization of the state space and the integral, the iterated function sequence

turns out to converge fast to an approximate solution to (3.13).

3.8 Solution for spectrally negative geometric Lévy processes

By a careful inspection of the previous proofs, it turns out that the results of the previous subsections can be generalized to an underlying jump process. To be more precise, we consider the optimal stopping problem (3.2) for an underlying geometric Lévy process

where are spectrally negative Lévy processes, that is their Lévy measures are concentrated on . Note that since the co-ordinates of may have negative jumps, overshoot may occur for the optimal stopping time in (3.2).

For our approach to work, we need to assume that is regular for for the underlying -dimensional Lévy process , i.e.

| (3.14) |

This assumption guarantees that the value function is across the boundary, which is highly related to the regularity of the stopping set , see below and the discussion in [2, 11] for the one-dimensional case. Then, we obtain the following generalization of Theorem 3.3 and Theorem 3.5:

Theorem 3.7.

Under the assumptions made above, it holds that for all

where

Furthermore, for any nonempty, south-west connected, convex set such that

it holds that .

Sketch of a proof.

As indicated above, the proof is analogous to the proof in the case without jumps. Therefore, we only mention the few changes in the arguments:

- 1.

- 2.

∎

4 American put option

As pointed out in the introduction, the problem of pricing the American put option can be seen as the investment problem under a finite time horizon with . Therefore, we found it motivated to briefly discuss our approach also in this problem setting. To be more specific, we demonstrate how the Riesz representation can be used to derive the integral equation which characterizes the early exercise boundary and, furthermore, to prove the uniqueness of the solution of the equation.

An important vehicle in the proof of the uniqueness of the solution of the integral equation in [39] (see also [41]) is an extension of the Itô-Tanaka formula developed in [40] and called the local time-space formula. This formula is needed to be able to analysis non-smooth candidate solutions. Our proof of the uniqueness uses similar ideas as presented in [39] but the advantage with the Riesz representation is that we can operate with smooth candidates (cf. Section 2.3 above).

Let denote the stock price process in the Black-Scholes model and let denote the martingale measure. Hence, under is a geometric Brownian motion with volatility and drift which is also the risk-free interest rate on the market. The fair price of the American put option is given by

| (4.1) |

where is the expiration time, is for the set of stopping times with values in is the initial price of the stock, and is the strike price.

Consider now the value of the OSP associated with the American put given via

| (4.2) |

From the general theory of optimal stopping we know that is -excessive for the space-time process and that the stopping region consists of the points, where the value equals the reward, i.e.,

The results in the next theorem are well-known. Our interest hereby is focused only on (iv) and (v) but for the readability we also indicate references for (i), (ii), and (iii).

Theorem 4.1.

There exists a function such that

-

(i)

-

(ii)

is increasing, convex and differentiable in

-

(iii)

and is an optimal stopping time,

-

(iv)

the price of the option at time when has the unique Doob-Meyer decomposition

where the first term on the right hand side (the finite variation part of the decomposition) is called the early exercise premium,

-

(v)

for any the function is the unique continuous solution of the integral equation

(4.3)

Proof.

For the existence of an increasing and continuous curve such that (i) and (iii) hold, see Jacka [24] (and also Myneni [33], Karatzas [25], and Karatzas and Shreve [26]). For the differentiablity, see Chen and Chadam [9] and for the convexity, see Chen, Chadam, Jiang and Zheng [10] and Ekström [19].

For (iv) we recall from the Riesz representation that there exists a unique -finite measure on such that

| (4.4) |

It is also well-known (see [24], [41]) or follows as in Lemma 3.2 that exists and is continuous on (smooth fit holds). The differentiability of implies that also exists and is continuous (see [33] p. 16 where a reference to Moerbeke [46] Lemma 5 is given). For the absolute continuity of as a function of , note that is everywhere (but not on ) with bounded derivative, and therefore Lipschitz continuous as a function of . Hence, using Proposition 2.6 we have for

Since , we furthermore have

and otherwise Hence using (2.6)

This proves (iv).

(v) can now be proved by following the proof of Theorem 3.5. More precisely, one considers a continuous candidate boundary function that also fulfills

and defines the associated candidate value function

| (4.5) |

where for such that is given by

and for

Then one proves – using the same arguments as in the proof of Theorem 3.5 – the following four steps:

-

1.

for all ,

-

2.

,

-

3.

,

-

4.

.

In particular, a space-time version of formula (3.7) in Lemma 3.6 is needed. To formulate this, let be a measurable function and define

where is fixed. Then for each stopping time taking values in and each

We leave the details of the proofs of this formula and steps 1-4 to the reader. ∎

Appendix A Appendix

A1 Proof of Proposition 2.1.

Let be a -dimensional geometric Brownian motion with parameters and started at as introduced in Section 2.1, and denote the Lebesgue density of by .

In the following, we understand each operation (as multiplication, division etc.) componentwise. Since is a geometric Brownian motion a short calculation yields

and

where . Let be the measure on with Lebesgue density

then for all nonnegative and measurable functions and , it holds that

∎

A2 Proof of Proposition 2.4.

By noting that convex sets have a Lipschitz surfaces there exists (see, e.g., [35, Appendix D]) a sequence of -functions such that uniformly on compacts and uniformly on compact subsets of . More precisely, this sequence is given by convolution with a sequence of -functions with compact support:

where denotes convolution. Furthermore, by the proof of

[35, Appendix D] it is immediate that

Therefore, the boundedness assumption on

implies that the sequence , is uniformly locally bounded around .

Now, take a sequence of compact subsets of such that as . By Dynkin’s formula

Letting and keeping in mind that the Green measure is absolutely continuous with respect to the Lebesgue measure, we obtain

by dominated convergence and the convention that (or any other value) on the null set . Letting and using the boundedness of , we have

and, by the uniqueness of the integral representation,

∎

A3 Proof of the duality; Proposition 2.5.

The claim is that there exists a resolvent kernel such that (2.8) holds. Consider for non-negative and measurable and

Let

We claim that constitutes a resolvent kernel as defined in [28, p. 493]. Conditions (a), (b) and (d) therein are easily verified. It remains to check condition (c), i.e., the resolvent equation

Indeed,

as claimed. ∎

A4 Proof of Lemma 3.2.

Let and with Euclidian norm 1. Then and . Therefore, for such that it holds

which yields

On the other hand, let denote the optimal stopping time and write

Then (using componentwise multiplication of vectors and the notation )

and – since –

By Lemma 3.1, the set

is a subset of , hence - keeping the continuity of the sample paths in mind -

Consequently,

This proves that the value function is differentiable on . Furthermore, on , and by the proof of Lemma 3.1, is convex. Since differentiable convex functions are (see [7, Theorem 2.2.2]), we obtain the first claim. For the second one, note that on and on , which gives the locally boundedness around ∎

A5 Proof of Lemma 3.6.

By the definition of the Green kernel and the strong Markov property it holds that for all and all stopping times

∎

Acknowledgement

Paavo Salminen thanks the Mathematisches Seminar at Christian-Albrechts-Universität for the hospitality and the support during the stay in Kiel.

References

- [1] {bbook}[author] \bauthor\bsnmAbramowitz, \bfnmM.\binitsM. and \bauthor\bsnmStegun, \bfnmI.\binitsI. (\byear1970). \btitleMathematical functions, 9th printing. \bpublisherDover publications, Inc., \baddressNew York. \endbibitem

- [2] {barticle}[author] \bauthor\bsnmAlili, \bfnmL.\binitsL. and \bauthor\bsnmKyprianou, \bfnmA. E.\binitsA. E. (\byear2005). \btitleSome remarks on first passage of Lévy processes, the American put and pasting principles. \bjournalAnn. Appl. Probab. \bvolume15 \bpages2062–2080. \bdoi10.1214/105051605000000377 \bmrnumber2152253 (2006b:60078) \endbibitem

- [3] {barticle}[author] \bauthor\bsnmAlsmeyer, \bfnmG.\binitsG. and \bauthor\bsnmJaeger, \bfnmM.\binitsM. (\byear2005). \btitleA useful extension of Itô’s formula with applications to optimal stopping. \bjournalActa Math. Sin. (Engl. Ser.) \bvolume21 \bpages779–786. \bdoi10.1007/s10114-004-0524-y \bmrnumber2156953 (2006h:60088) \endbibitem

- [4] {barticle}[author] \bauthor\bsnmBeibel, \bfnmM.\binitsM. and \bauthor\bsnmLerche, \bfnmH. R.\binitsH. R. (\byear2000). \btitleA note on optimal stopping of regular diffusions under random discounting. \bjournalTeor. Veroyatnost. i Primenen. \bvolume45 \bpages657–669. \bmrnumberMR1968720 (2004a:60086) \endbibitem

- [5] {bbook}[author] \bauthor\bsnmBlumenthal, \bfnmR. M.\binitsR. M. and \bauthor\bsnmGetoor, \bfnmR. K.\binitsR. K. (\byear1968). \btitleMarkov processes and potential theory. \bseriesPure and Applied Mathematics, Vol. 29. \bpublisherAcademic Press, \baddressNew York. \bmrnumber0264757 (41 ##9348) \endbibitem

- [6] {bbook}[author] \bauthor\bsnmBorodin, \bfnmA. N.\binitsA. N. and \bauthor\bsnmSalminen, \bfnmP.\binitsP. (\byear2002). \btitleHandbook of Brownian motion—facts and formulae, \beditionsecond ed. \bseriesProbability and its Applications. \bpublisherBirkhäuser Verlag, \baddressBasel. \bdoi10.1007/978-3-0348-8163-0 \bmrnumber1912205 (2003g:60001) \endbibitem

- [7] {bbook}[author] \bauthor\bsnmBorwein, \bfnmJonathan M\binitsJ. M. and \bauthor\bsnmVanderwerff, \bfnmJon D\binitsJ. D. (\byear2010). \btitleConvex functions: constructions, characterizations and counterexamples \bvolume32. \bpublisherCambridge University Press Cambridge. \endbibitem

- [8] {barticle}[author] \bauthor\bsnmCarr, \bfnmPeter\binitsP., \bauthor\bsnmJarrow, \bfnmRobert\binitsR. and \bauthor\bsnmMyneni, \bfnmRavi\binitsR. (\byear1992). \btitleAlternative characterizations of American put options. \bjournalMath. Finance \bvolume2 \bpages87–106. \bdoi10.1111/j.1467-9965.1992.tb00040.x \endbibitem

- [9] {barticle}[author] \bauthor\bsnmChen, \bfnmXinfu\binitsX. and \bauthor\bsnmChadam, \bfnmJohn\binitsJ. (\byear2006/07). \btitleA mathematical analysis of the optimal exercise boundary for American put options. \bjournalSIAM J. Math. Anal. \bvolume38 \bpages1613–1641 (electronic). \bdoi10.1137/S0036141003437708 \bmrnumber2286022 (2007k:91131) \endbibitem

- [10] {barticle}[author] \bauthor\bsnmChen, \bfnmXinfu\binitsX., \bauthor\bsnmChadam, \bfnmJohn\binitsJ., \bauthor\bsnmJiang, \bfnmLishang\binitsL. and \bauthor\bsnmZheng, \bfnmWeian\binitsW. (\byear2008). \btitleConvexity of the exercise boundary of the American put option on a zero dividend asset. \bjournalMath. Finance \bvolume18 \bpages185–197. \bdoi10.1111/j.1467-9965.2007.00328.x \bmrnumber2380946 (2008m:91109) \endbibitem

- [11] {barticle}[author] \bauthor\bsnmChristensen, \bfnmS.\binitsS. and \bauthor\bsnmIrle, \bfnmA.\binitsA. (\byear2009). \btitleA note on pasting conditions for the American perpetual optimal stopping problem. \bjournalStatist. Probab. Lett. \bvolume79 \bpages349–353. \bdoi10.1016/j.spl.2008.09.002 \bmrnumber2493018 (2010k:60149) \endbibitem

- [12] {barticle}[author] \bauthor\bsnmChristensen, \bfnmS.\binitsS. and \bauthor\bsnmIrle, \bfnmA.\binitsA. (\byear2011). \btitleA harmonic function technique for the optimal stopping of diffusions. \bjournalStochastics \bvolume83(4-6) \bpages347–363. \endbibitem

- [13] {barticle}[author] \bauthor\bsnmChristensen, \bfnmS.\binitsS., \bauthor\bsnmSalminen., \bfnmP.\binitsP. and \bauthor\bsnmTa, \bfnmB.\binitsB. (\byear2013). \btitleOptimal stopping of strong Markov processes. \bjournalStochastic Process. Appl. \bvolume123 \bpages1138-1159. \endbibitem

- [14] {bbook}[author] \bauthor\bsnmChung, \bfnmK. L.\binitsK. L. and \bauthor\bsnmWalsh, \bfnmJ. B.\binitsJ. B. (\byear2005). \btitleMarkov processes, Brownian motion, and time symmetry, \beditionsecond ed. \bseriesGrundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences] \bvolume249. \bpublisherSpringer, \baddressNew York. \bmrnumber2152573 (2006j:60003) \endbibitem

- [15] {barticle}[author] \bauthor\bsnmCrocce, \bfnmF.\binitsF. and \bauthor\bsnmMordecki, \bfnmE.\binitsE. (\byear2014). \btitleExplicit solutions in one-sided optimal stopping problems for one-dimensional diffusions. \bjournalStochastics \bvolume86(3) \bpages491-509. \endbibitem

- [16] {barticle}[author] \bauthor\bsnmDayanik, \bfnmS.\binitsS. and \bauthor\bsnmKaratzas, \bfnmI.\binitsI. (\byear2003). \btitleOn the optimal stopping problem for one-dimensional diffusions. \bjournalStochastic Process. Appl. \bvolume107 \bpages173-212. \endbibitem

- [17] {barticle}[author] \bauthor\bsnmDynkin, \bfnmE. B.\binitsE. B. (\byear1969). \btitleProstranstvo vyhodov markovskogo processa. \bjournalUspehi Mat. Nauk \bvolumeXXIV 4 (148) \bpages89–152. \endbibitem

- [18] {barticle}[author] \bauthor\bsnmDynkin, \bfnmE. B.\binitsE. B. (\byear1969). \btitleThe space of exits of a Markov process. \bjournalRuss. Math. Surv. \bvolume24 \bpages89-157. \bdoi10.1070/RM1969v024n04ABEH001353 \endbibitem

- [19] {barticle}[author] \bauthor\bsnmEkström, \bfnmE.\binitsE. (\byear2004). \btitleConvexity of the optimal stopping boundary for the American put option. \bjournalJ. Math. Anal. Appl \bvolume299 \bpages147-156. \endbibitem

- [20] {bbook}[author] \bauthor\bsnmErdélyi, \bfnmA.\binitsA., \bauthor\bsnmMagnus, \bfnmW.\binitsW., \bauthor\bsnmOberhettinger, \bfnmF.\binitsF. and \bauthor\bsnmTricomi, \bfnmF. G.\binitsF. G. (\byear1954). \btitleTables of Integral Transforms. \bpublisherMcGraw-Hill, \baddressNew York. \endbibitem

- [21] {barticle}[author] \bauthor\bsnmGahungu, \bfnmJ.\binitsJ. and \bauthor\bsnmSmeers, \bfnmY.\binitsY. (\byear2011). \btitleOptimal time to invest when the price processes are geometric Brownian motions. A tentative based on smooth fit. \bjournalCORE Discussion Papers 2011034, Université catholique de Louvain, Center for Operations Research and Econometrics (CORE). \endbibitem

- [22] {barticle}[author] \bauthor\bsnmGahungu, \bfnmJ.\binitsJ. and \bauthor\bsnmSmeers, \bfnmY.\binitsY. (\byear2011). \btitleSufficient and necessary conditions for perpetual multi-assets exchange options. \bjournalCORE Discussion Papers 2011035, Université catholique de Louvain, Center for Operations Research and Econometrics (CORE). \endbibitem

- [23] {barticle}[author] \bauthor\bsnmHu, \bfnmY.\binitsY. and \bauthor\bsnmØksendal, \bfnmB.\binitsB. (\byear1998). \btitleOptimal time to invest when the price processes are geometric Brownian motions. \bjournalFinance Stoch. \bvolume2(3) \bpages295–310. \endbibitem

- [24] {barticle}[author] \bauthor\bsnmJacka, \bfnmS.\binitsS. (\byear1991). \btitleOptimal stopping and the American put. \bjournalMathematical Finance \bvolume1 \bpages1–14. \endbibitem

- [25] {bbook}[author] \bauthor\bsnmKaratzas, \bfnmI.\binitsI. (\byear1997). \btitleLectures on the mathematics of finance. \bseriesCRM Monograph Series \bvolume8. \bpublisherAmerican Mathematical Society, \baddressProvidence, RI. \bmrnumber1421066 (98h:90001) \endbibitem

- [26] {bbook}[author] \bauthor\bsnmKaratzas, \bfnmI.\binitsI. and \bauthor\bsnmShreve, \bfnmS. E.\binitsS. E. (\byear1998). \btitleMethods of mathematical finance. \bseriesApplications of Mathematics (New York) \bvolume39. \bpublisherSpringer-Verlag, \baddressNew York. \bmrnumber1640352 (2000e:91076) \endbibitem

- [27] {barticle}[author] \bauthor\bsnmKim, \bfnmIN\binitsI. (\byear1990). \btitleThe analytic valuation of American options. \bjournalReview of Financial Studies \bvolume3 \bpages547-572. \bdoi10.1093/rfs/3.4.547 \endbibitem

- [28] {barticle}[author] \bauthor\bsnmKunita, \bfnmH.\binitsH. and \bauthor\bsnmWatanabe, \bfnmT.\binitsT. (\byear1965). \btitleMarkov processes and Martin boundaries. I. \bjournalIllinois J. Math. \bvolume9 \bpages485–526. \bmrnumber0181010 (31 ##5240) \endbibitem

- [29] {barticle}[author] \bauthor\bsnmLamberton, \bfnmDamien\binitsD. and \bauthor\bsnmMikou, \bfnmMohammed\binitsM. (\byear2008). \btitleThe critical price for the American put in an exponential Lévy model. \bjournalFinance and Stochastics \bvolume12 \bpages561–581. \endbibitem

- [30] {barticle}[author] \bauthor\bsnmMcDonald, \bfnmR.\binitsR. and \bauthor\bsnmSiegel, \bfnmD.\binitsD. (\byear1986). \btitleThe value of waiting to invest. \bjournalQuarterly J. Econ. \bvolume101 \bpages707–727. \endbibitem

- [31] {barticle}[author] \bauthor\bsnmMcKean, \bfnmH.\binitsH. (\byear1965). \btitleAppendix: A free boundary problem for the heat equation arising from a problem of mathematical economics. \bjournalInd. Management Rev. \bvolume6 \bpages32-39. \endbibitem

- [32] {barticle}[author] \bauthor\bsnmMordecki, \bfnmE.\binitsE. and \bauthor\bsnmSalminen, \bfnmP.\binitsP. (\byear2007). \btitleOptimal stopping of Hunt and Lévy processes. \bjournalStochastics \bvolume79 \bpages233–251. \bdoi10.1080/17442500601100232 \bmrnumber2308074 (2008e:60113) \endbibitem

- [33] {barticle}[author] \bauthor\bsnmMyneni, \bfnmR.\binitsR. (\byear1992). \btitleThe pricing of the American option. \bjournalAnn. Appl. Probab. \bvolume2 \bpages1–23. \bmrnumber1143390 (92h:90018) \endbibitem

- [34] {barticle}[author] \bauthor\bsnmNishide, \bfnmK.\binitsK. and \bauthor\bsnmRogers, \bfnmL. C. G.\binitsL. C. G. (\byear2011). \btitleOptimal time to exchange two baskets. \bjournalJ. Appl. Probab. \bvolume48(1) \bpages21–30. \endbibitem

- [35] {bbook}[author] \bauthor\bsnmØksendal, \bfnmB.\binitsB. (\byear2003). \btitleStochastic differential equations: an introduction with applications, \beditionsixth ed. \bseriesUniversitext. \bpublisherSpringer-Verlag, \baddressBerlin. \bdoi10.1007/978-3-642-14394-6 \bmrnumber2001996 (2004e:60102) \endbibitem

- [36] {bbook}[author] \bauthor\bsnmØksendal, \bfnmB.\binitsB. and \bauthor\bsnmSulem, \bfnmA.\binitsA. (\byear2007). \btitleApplied stochastic control of jump diffusions, \beditionsecond ed. \bseriesUniversitext. \bpublisherSpringer, \baddressBerlin. \bdoi10.1007/978-3-540-69826-5 \bmrnumber2322248 (2008b:93003) \endbibitem

- [37] {barticle}[author] \bauthor\bsnmOlsen, \bfnmT. E.\binitsT. E. and \bauthor\bsnmStensland., \bfnmG.\binitsG. (\byear1992). \btitleOn optimal timing of investment when cost components are additive and follow geometric diffusions. \bjournalJournal of Economic Dynamics and Control \bvolume16 \bpages39–51. \endbibitem

- [38] {barticle}[author] \bauthor\bsnmPaulsen, \bfnmV.\binitsV. (\byear2001). \btitleBounds for the American perpetual put on a stock index. \bjournalJ. Appl. Probab. \bvolume38 \bpages55–66. \bmrnumber1816113 (2002a:60074) \endbibitem

- [39] {barticle}[author] \bauthor\bsnmPeskir, \bfnmG.\binitsG. (\byear2005). \btitleOn the American option problem. \bjournalMath. Finance \bvolume15 \bpages169–181. \bdoi10.1111/j.0960-1627.2005.00214.x \bmrnumber2116800 (2005i:91066) \endbibitem

- [40] {barticle}[author] \bauthor\bsnmPeskir, \bfnmG.\binitsG. (\byear2005). \btitleA change-of-variable formula with local time on curves. \bjournalJ. Theoret. Probab. \bvolume18 \bpages499–535. \endbibitem

- [41] {bbook}[author] \bauthor\bsnmPeskir, \bfnmG.\binitsG. and \bauthor\bsnmShiryaev, \bfnmA. N.\binitsA. N. (\byear2006). \btitleOptimal stopping and free-boundary problems. \bseriesLectures in Mathematics ETH Zürich. \bpublisherBirkhäuser Verlag, \baddressBasel. \endbibitem

- [42] {barticle}[author] \bauthor\bsnmPham, \bfnmHuyên\binitsH. (\byear1997). \btitleOptimal stopping, free boundary, and American option in a jump-diffusion model. \bjournalApplied Mathematics and Optimization \bvolume35 \bpages145–164. \endbibitem

- [43] {barticle}[author] \bauthor\bsnmSalminen, \bfnmP.\binitsP. (\byear1985). \btitleOptimal stopping of one-dimensional diffusions. \bjournalMath. Nachr. \bvolume124 \bpages85–101. \bdoi10.1002/mana.19851240107 \bmrnumber827892 (87m:60177) \endbibitem

- [44] {barticle}[author] \bauthor\bsnmSalminen, \bfnmP.\binitsP. (\byear1999). \btitleOptimal stopping and American put options. \bjournalTheory of Stochastic Processes \bvolume5(21) \bpages129-144. \endbibitem

- [45] {bbook}[author] \bauthor\bsnmShiryaev, \bfnmA. N.\binitsA. N. (\byear2008). \btitleOptimal stopping rules. \bseriesStochastic Modelling and Applied Probability \bvolume8. \bpublisherSpringer-Verlag, \baddressBerlin. \bnoteTranslated from the 1976 Russian second edition by A. B. Aries, Reprint of the 1978 translation. \bmrnumber2374974 (2008m:60003) \endbibitem

- [46] {barticle}[author] \bauthor\bparticlevan \bsnmMoerbeke, \bfnmPierre\binitsP. (\byear1975/76). \btitleOn optimal stopping and free boundary problems. \bjournalArch. Rational Mech. Anal. \bvolume60 \bpages101–148. \bmrnumber0413250 (54 ##1367) \endbibitem