Efficient valuation method for the SABR model111The views represented herein are the author’s own views and do not necessarily represent the views of Morgan Stanley or its affiliates, and are not a product of Morgan Stanley Research

Abstract

In this article, we show how the scaling symmetry of the SABR model can be utilized to efficiently price European options. For special kinds of payoffs, the complexity of the problem is reduced by one dimension. For more generic payoffs, instead of solving the dimensional SABR PDE, it is sufficient to solve uncoupled dimensional PDE’s, where is the number of points used to discretize one dimension. Furthermore, the symmetry argument enables us to obtain prices of multiple options, whose payoffs are related to each other by convolutions, by valuing one of them. The results of the method are compared with the Monte Carlo simulation.

1 SABR Model

The SABR model[8, 9, 1] is one of the most commonly used models to price European swaptions. It is a two factor model with stochastic volatility and is described by a pair of coupled SDE’s:

| (1) | ||||

where

-

•

is the forward swap rate

-

•

is the stochastic volatility

-

•

and are the Brownian motions with correlation

-

•

The above equations are taken from the forward swap annuity measure444Throughout the article, we will only work in this measure and all payoffs and valuations are expressed in the unit of the measure’s numéraire, namely, the forward swap annuity., where is a martingale. When , can reach with non-zero probability. Once it hits , must stay there to maintain its martingale property. It has the absorbing boundary condition at . is the log-normal process and can be easily solved:

| (2) |

In this article, we will only consider European options whose payoffs at the maturity are functions of and . With this restriction, the problems become Markov and the prices of the options can be obtained by solving the Kolmogorov backward equation, we call SABR PDE. This PDE is dimensional: 1 dimension for time and 2 dimensions for Markovian state variables: and . As mentioned earlier, it has the absorbing boundary condition at . Unfortunately, no-closed form solutions to this equation are known except for some special cases. Instead, asymptotic expansions in can be computed analytically and they are commonly used to price European swaptions[8, 9, 2, 10, 14, 15, 1]. Note that these are asymptotic expansions. Hence, their convergence is not guaranteed. One can easily see that, with any finite value of , the probability of hitting is non-zero, which cannot be obtained from the series expansion in around .

When , there are semi-analytic solutions to the PDE[11, 1]. Conditioned on a path of , becomes a time-changed CEV process. Closed-form solutions to the CEV PDE are known since a simple change of variable would transform this PDE into the CIR PDE[1]. The solutions will have dependency in the path of only through the elapsed time, . The distribution of this integral is also known semi-analytically[1, 16, 13, 5, 6, 3, 4]. Therefore, the unconditional solutions to the SABR PDE will be given as integrals of the CEV solutions over this distribution.

2 Symmetry Argument

In this section, we will introduce the scaling symmetry of the SABR model and examine its consequences in pricing European options. Special attention will be paid to swaption cases.

2.1 Scaling Symmetry

The SABR SDE’s are invariant under the following scaling transformation,

| (3) | ||||

for any . Instead of and , it is convenient to work with a different set of variables where one of the variables in the set is invariant under the scaling transformation. This will make it easy to analyze scaling properties of solutions. We will consider 2 such sets. The first is given below:

| (4) | ||||

Under the scaling transformation, is invariant while where . Note that when , the change of variables from and to and becomes singular at locus . This means that not all solutions of the SABR PDE can be expressed as a function of and . For most of our applications, payoff functions are independent of when . This, together with the absorbing boundary condition at guarantees that solutions are also independent of when . In such cases, variables and can be used to express solutions.

The second set of variables we are going to use is

| (5) | ||||

is invariant under the scaling and . For a fixed set of model parameters, these variables are good to use for all values of and , and, unlike and , there will be no restriction on kinds of payoff functions for which these variables can be utilized. However, the change of variables becomes singular as approaches to . This causes large numerical errors in solutions when is too close to .

To deal with these two sets of variables uniformly, we will use following notation. and will denote the variables. will be invariant and under the scaling transformation. For the first set of variables, , and . For the second set, , , and .

2.2 Special Payoff

The scaling symmetry can be utilized to reduce complexity of solving the SABR PDE. To see this, let’s consider an European option whose payoff at maturity is for some function 555 is an example of such payoffs.. The value of this option at time is the expected value of the payoff conditioned on , a filtration generated by all information available by time :

| (6) |

Here, we have used the fact that the problem at hand is Markovian and the solution has dependency on only through and . Using the symmetry, one can show

| (7) |

for any . In particular, one can choose and conclude

| (8) | ||||

for some function . Note that is a solution to the SABR PDE, which is dimensional666One dimension for time and other 2 dimensions for Markovian state variables, and .. By applying it to the SABR PDE, we obtain another PDE that satisfies:

| (9) |

where , and are functions of only and their functional forms depend on the choice of variables and .

For variables and , the corresponding functions are

| (10) | ||||

Note that the above PDE777After completion of this research, the author became aware that a similar PDE for payoff has been derived in [12]. Instead of the symmetry argument used here, Islah noted that the SDE for is uncoupled from and used the measure change to derive the PDE. has a singularity at . This is due to the singularity of the change of variables we discussed in section 2.1. For this PDE to work, should go to fast enough as .

For variables and ,

| (11) | ||||

The PDE in eq. 9 is dimensional since does not depend on . can be obtained by solving this PDE with terminal condition . Hence, using the symmetry, we have reduced the complexity of the problem by one dimension.

2.3 Generic Payoff

The payoffs we have considered so far are rather limited. For more generic payoffs, the benefit of the symmetry is much more subtle. Consider a generic payoff function . Using the Fourier transform along direction, we can decompose it as follows:

| (12) |

where

| (13) |

The value of the option at time , , is given by the expected value of the payoff. With sufficiently regular , we can interchange the integration and the expectation:

| (14) | ||||

Now, the same symmetry argument in section 2.2 applies and we can use this to separate dependency:

| (15) |

for some functions ’s. As before, ’s are solutions of dimensional PDE’s that are all uncoupled from each other:

| (16) |

These PDE’s are obtained by replacing in eq. 9 with . ’s can be obtained by solving the PDE’s with terminal condition .

In practice, we cannot solve these PDE’s analytically. Instead, we discretize variables and resort to numerical techniques. For our discussion, it is enough to discretize along the direction only. After discretization, we impose the periodic boundary condition in the direction on the payoff function and decompose it into a Fourier series:

| (17) |

with

| (18) |

where takes a value from the discretized grid for , is from the dual grid888The dual grid is defined as , and is the number of points in the grid.

For variables and , this step requires some clarification. The Fourier series used here needs to be seen as an approximation of the original payoff function. Inside the grid, it is a good approximation since it matches the value of the function exactly for all points in the grid. However, it may not be such a good approximation outside of it.

When , locus is of special concern. implies , which is outside the grid, and it can be reached with non-zero probability. To make sure that the Fourier series is still a good approximation for this case, we slightly change the definition of when :

| (19) |

As discussed in section 2.1, we use variables and only for payoffs that are independent of when . For such payoffs, is the value of the payoff function at . Changing can be understood as deforming the payoff function around . For example, the following deformation with very small would produce the equivalent change in :

| (20) |

The deformed payoff function will differ from the original payoff function when is very small and is finite. Since it implies is very large and is finite, the probability of this happening is very small and it will not introduce much error in pricing. Due to the singularity, also implies and now, with the modified definition of , the Fourier series matches the payoff function value when .

When is large and outside the grid, the Fourier series will not be a good approximation. For this, we need to make sure the grid is large enough so that the probability of reaching such is very small.

The second set of variables, and , does not have similar issues. is a Normal process and it cannot reach its boundaries at and . As long as the grid is sufficiently large, the Fourier series is a good approximation to the original payoff function.

Using the same symmetry argument, we conclude that the value of the option is given by

| (21) |

for some functions ’s, where is taken from the dual grid. ’s are solutions of the same PDE’s in eq. 16 and can be obtained by solving them with terminal condition . With the symmetry argument, we have reduced the complexity of the problem from solving an dimensional PDE to solving the uncoupled dimensional PDE’s. Since they are uncoupled, they can be solved parallelly, independent from each other.

We can go further with the symmetry argument. Once, ’s are computed, we can use them to price other options. Consider an option whose payoff function is a convolutions of ) with another function . For this payoff,

| (22) | ||||

with

| (23) |

where and are taken from the grid and is from the dual grid. Interchanging expectation and summation, one can show the option value is given as follows

| (24) |

With ’s computed already, the option value can be obtained without solving any more PDE’s. By pricing one option, we can price a whole class of options whose payoff functions are related to the original payoff function by convolutions.

2.4 Swaption Valuation

The argument in section 2.3 can be applied to swaption valuation and we can price swaptions with all strikes at once by solving the PDE’s for one strike999One such choice is the at-the-money strike.. To show this explicitly, we consider the payer swaption with strike :

| (25) |

Using the symmetry, one can show

| (26) |

for any . We choose for some fixed and obtain

| (27) | ||||

where is the value of the payer swaption with strike . Therefore, once we compute the value of this swaption, for example, following the steps highlighted in section 2.3, the swaption values for all strikes can be obtained.

3 Numerical Tests

We numerically tested the swaption valuation method developed in the previous section. We will call this method the “PDE + Symmetry” method. We first solve the PDE’s for the at-the-money swaption, following the steps highlighted in section 2.3. Then, we apply eq. 27 to obtain swaption prices for different strikes.

The computational complexity of the method is following. To solve the PDE’s, we discretize time and stochastic variables. We denote, by , , and , the numbers of points used to discretize time, , and . The decomposition of the payoff in eq. 18 and the recombination in eq. 21 can be broken into parallelizable independent computational units, each of which takes operations. Usually, the number of operations in the these steps is negligible compared to the number of operations in solving the PDE’s. As noted before, the PDE’s can be solved parallelly and each PDE takes operations. All in all, the method takes operations to price swaptions with all strikes.

3.1 Monte Carlo simulation

To test our method, we compared pricing results with the Monte Carlo simulation. We used the Euler scheme to generate Monte Carlo paths and adjusted them for the absorbing boundary condition:

| (28) | ||||

where and are standard normal random variables and is a uniform random variable. , and are all uncorrelated. Note that the above scheme consists of two steps. In the first step, we follow the standard Euler step to generate values for and at the next time step . In the second step, we adjust for the absorbing boundary condition at . The uniform random variable is used to compensate the probability of hitting zero between and even if . The approximate value of the probability

| (29) |

is obtained as follows[7]. Between time and , is approximated with a normal process by keeping its drift and volatility constant to values given at time . Then, we use the measure change to get rid of its drift and use the reflection principle of the Brownian motion to compute the probability of hitting zero. For small value of , this adjustment is not insignificant and sometimes changes swaption values by as much as a few basis points.

3.2 Analytic Limit

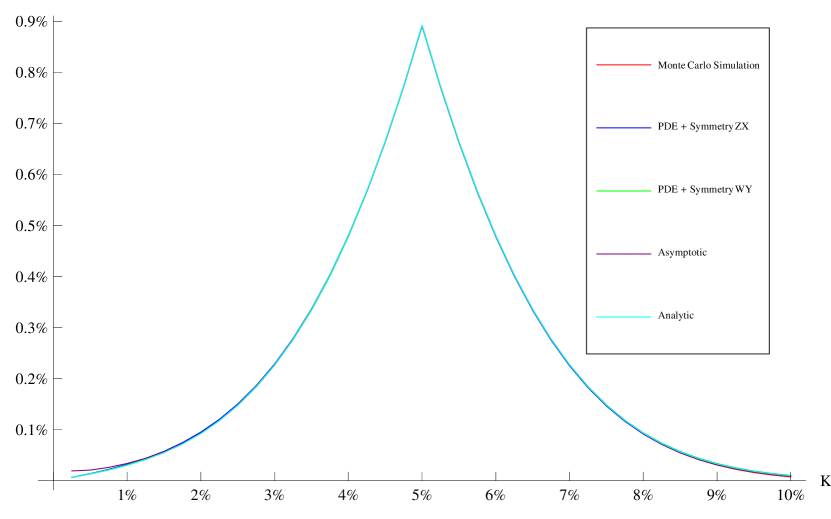

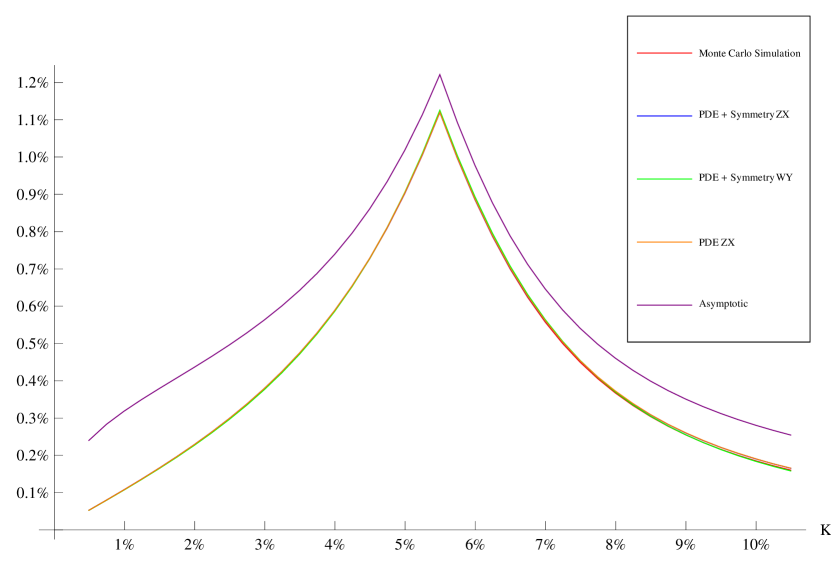

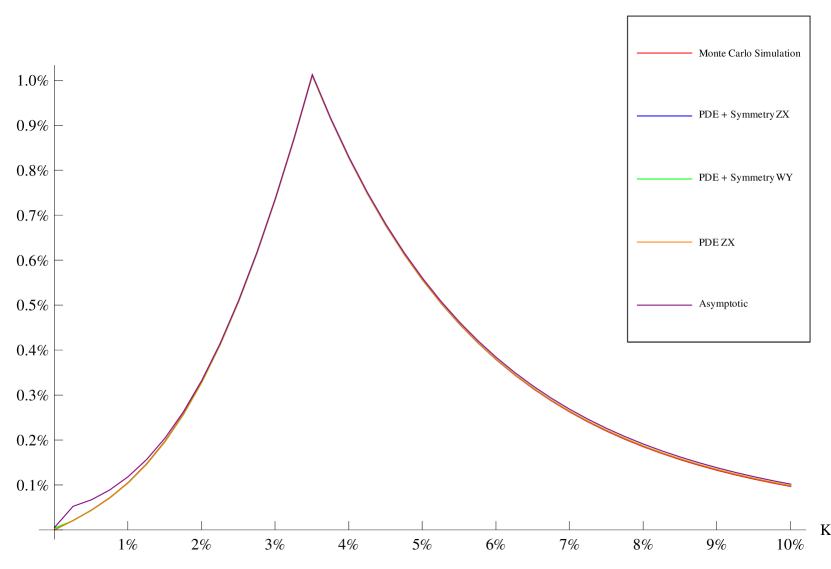

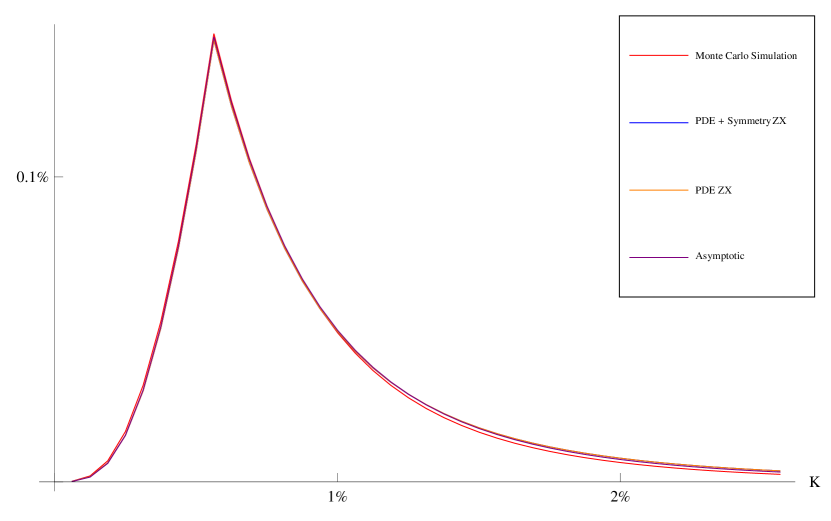

As a first test, we looked at a special limit of the SABR model where prices of swaptions are known analytically:

| , , , , , | (30) |

Here, the parameter values are shown in their natural units. is constant since . This, together with , implies is a normal process with the absorbing boundary condition at . The analytic swaption price is obtained by applying the reflection principle of the Brownian motions:

| (31) |

where and .

The time values of swaptions in the unit of forward swap annuity:

| (32) |

were computed using the following methods: were computed using the following methods:

-

•

Monte Carlo simulation: Monte Carlo method developed in section 3.1

-

•

PDE + Symmetry ZX: “PDE + Symmetry” method with the choice of variables and

-

•

PDE + Symmetry WY: “PDE + Symmetry” method with the choice of variables and

-

•

Asymptotic: The first order asymptotic series in [14]

-

•

Analytic: analytic solution in eq. 31

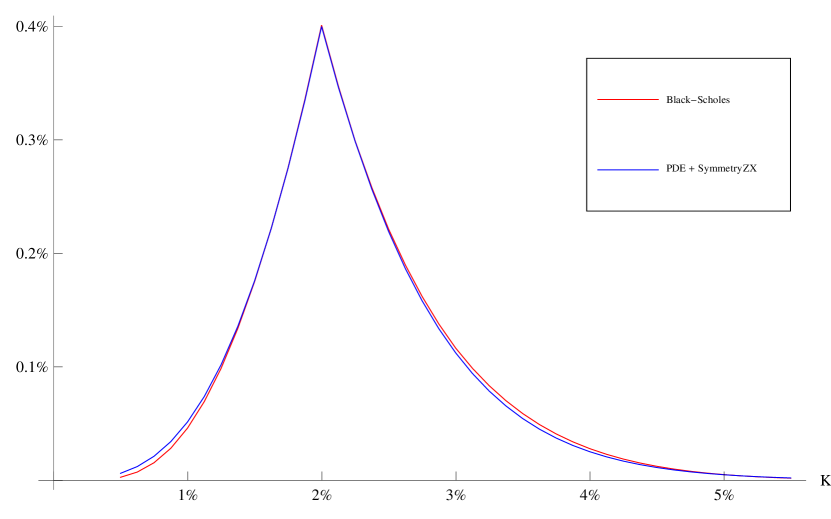

The results are shown in fig. 1 and table 1. The asymptotic series shows small difference from the other methods at very low strikes. All other methods produced virtually identical prices.

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE + Symmetry WY | Asymptotic | Analytic |

|---|---|---|---|---|---|

| 0.50% | 0.01% | 0.01% | 0.01% | 0.02% | 0.01% |

| 1.00% | 0.03% | 0.03% | 0.03% | 0.03% | 0.03% |

| 1.50% | 0.06% | 0.06% | 0.06% | 0.06% | 0.06% |

| 2.00% | 0.09% | 0.10% | 0.09% | 0.09% | 0.09% |

| 2.50% | 0.15% | 0.15% | 0.15% | 0.15% | 0.15% |

| 3.00% | 0.23% | 0.23% | 0.23% | 0.23% | 0.23% |

| 3.50% | 0.34% | 0.34% | 0.33% | 0.34% | 0.34% |

| 4.00% | 0.48% | 0.48% | 0.48% | 0.48% | 0.48% |

| 4.50% | 0.66% | 0.66% | 0.66% | 0.66% | 0.66% |

| 5.00% | 0.89% | 0.89% | 0.89% | 0.89% | 0.89% |

| 5.50% | 0.66% | 0.66% | 0.66% | 0.66% | 0.66% |

| 6.00% | 0.48% | 0.48% | 0.48% | 0.48% | 0.48% |

| 6.50% | 0.33% | 0.33% | 0.34% | 0.34% | 0.34% |

| 7.00% | 0.23% | 0.23% | 0.23% | 0.23% | 0.23% |

| 7.50% | 0.15% | 0.15% | 0.15% | 0.15% | 0.15% |

| 8.00% | 0.09% | 0.09% | 0.09% | 0.09% | 0.09% |

| 8.50% | 0.05% | 0.06% | 0.06% | 0.06% | 0.06% |

| 9.00% | 0.03% | 0.03% | 0.03% | 0.03% | 0.03% |

| 9.50% | 0.02% | 0.02% | 0.02% | 0.02% | 0.02% |

| 10.00% | 0.01% | 0.01% | 0.01% | 0.01% | 0.01% |

3.3 USD Swaption

We compared the “PDE + Symmetry” method with the Monte Carlo simulation in actual USD swaption valuation. We chose the USD swaption market on the following dates to represent various market conditions:

-

•

October 9th, 2007: The S&P 500 index reached its highest before the Great Recession.

-

•

September 15th, 2008: The Lehman Brothers filed for the bankruptcy protection.

-

•

March 9th, 2009: The S&P 500 index reached its lowest during the Great Recession.

-

•

October 29th 2013: Recent market

We manually calibrated the model for various expiry-tenor combinations on these dates. As noted in [8], and affect swaption prices in similar ways and it is difficult to determine both by fitting the market prices. Hence, we chose the value of arbitrarily and calibrated the rest of the model parameters by fitting market prices. Once the calibration was done, we compared swaptions prices computed using our “PDE + Symmetry” method to the Monte Carlo simulation results to test the accuracy of our method.

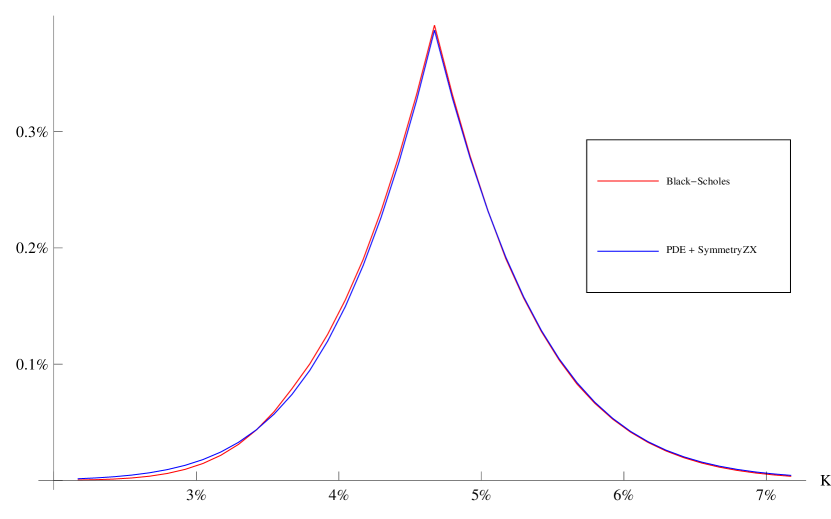

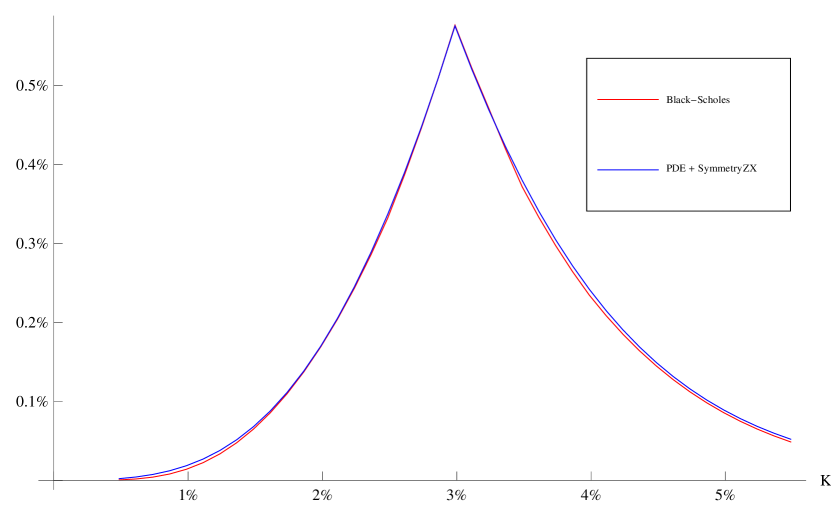

3.3.1 October 9th, 2007

Table 2 shows the USD swaption lognormal volatilities with 1 year expiry and 1 year tenor as of October 9th, 2007.

| Strike(%) | 2.67 | 3.67 | 4.17 | 4.42 | 4.67 | 4.92 | 5.17 | 5.67 | 6.67 |

| Volatility(%) | 24.70 | 23.70 | 22.20 | 21.63 | 21.06 | 20.50 | 19.97 | 19.39 | 18.69 |

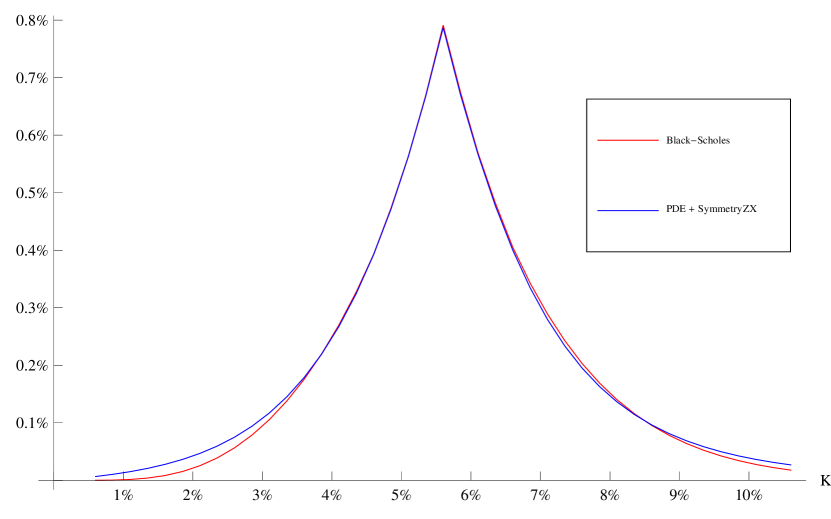

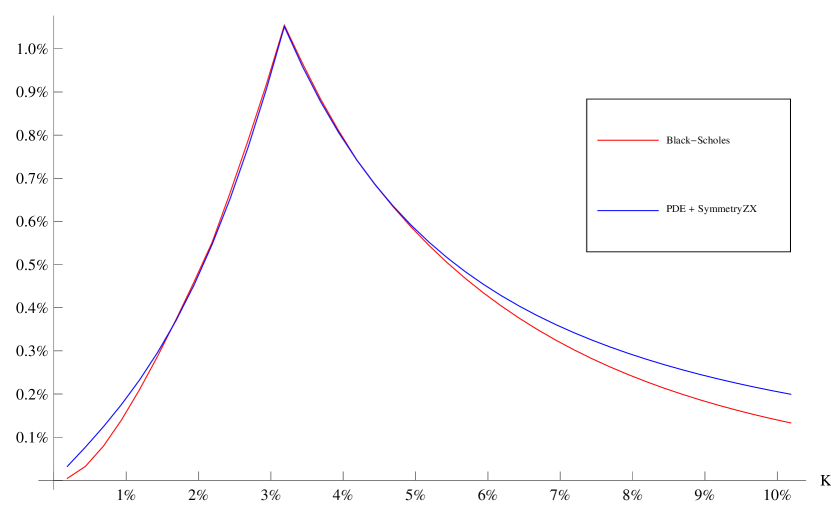

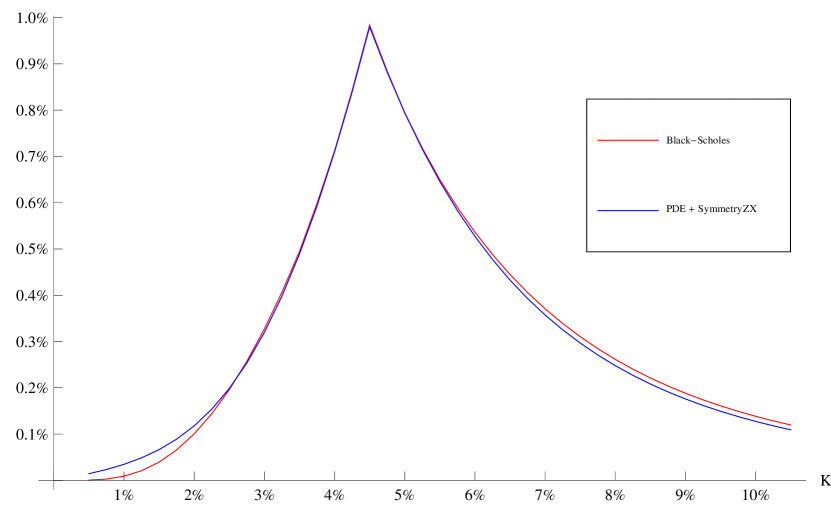

The observed forward swap rate was 4.67%. We chose the value of to be and manually calibrated the model. For the calibration, the “PDE + Symmetry” method with variables and was used. We obtained the following values of parameters:

| , , , , , | (33) |

As before, the above parameters are in their natural units. Figure 2 and table 3 show the goodness of the calibration101010The calibration may be improved by using a good optimizer, but for our purpose, it should be good enough..

| Strike | Black-Scholes | SABR |

|---|---|---|

| 2.67% | 0.00% | 0.01% |

| 3.67% | 0.08% | 0.07% |

| 4.17% | 0.19% | 0.19% |

| 4.42% | 0.28% | 0.27% |

| 4.67% | 0.39% | 0.39% |

| 4.92% | 0.28% | 0.28% |

| 5.17% | 0.19% | 0.19% |

| 5.67% | 0.08% | 0.08% |

| 6.67% | 0.01% | 0.01% |

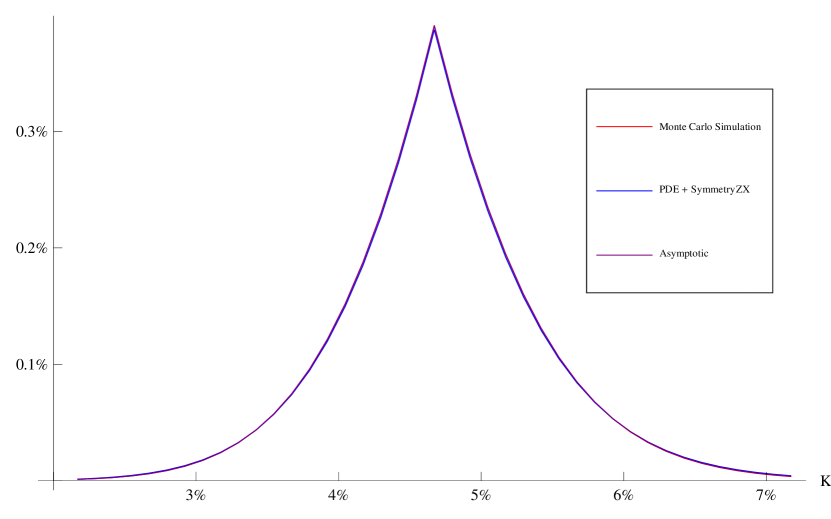

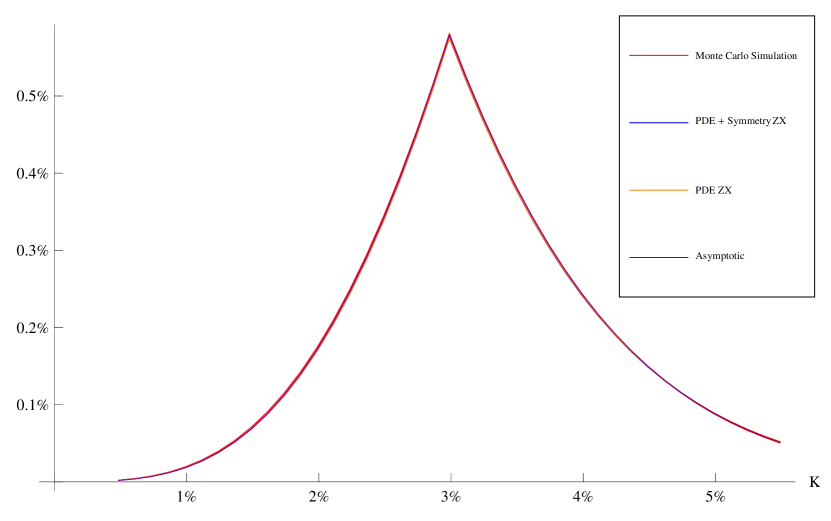

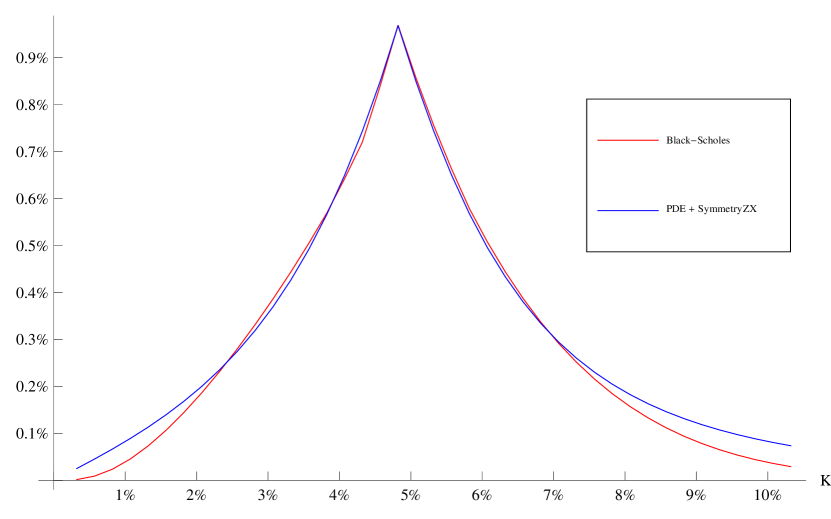

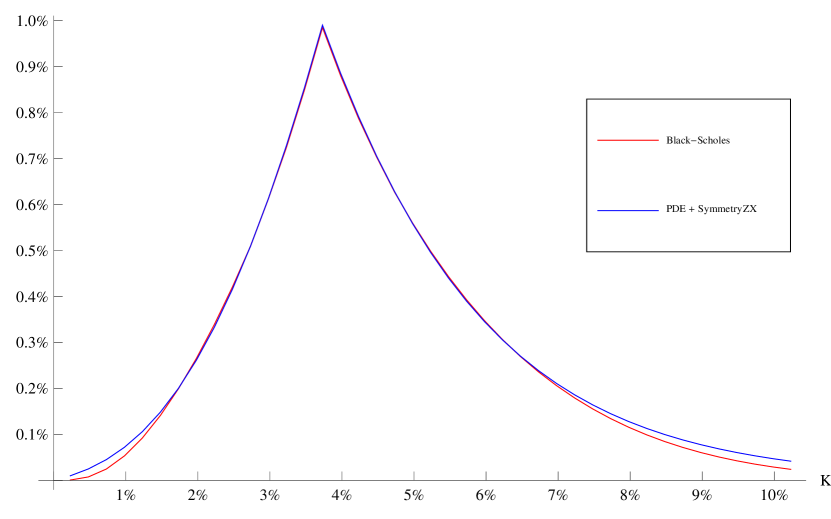

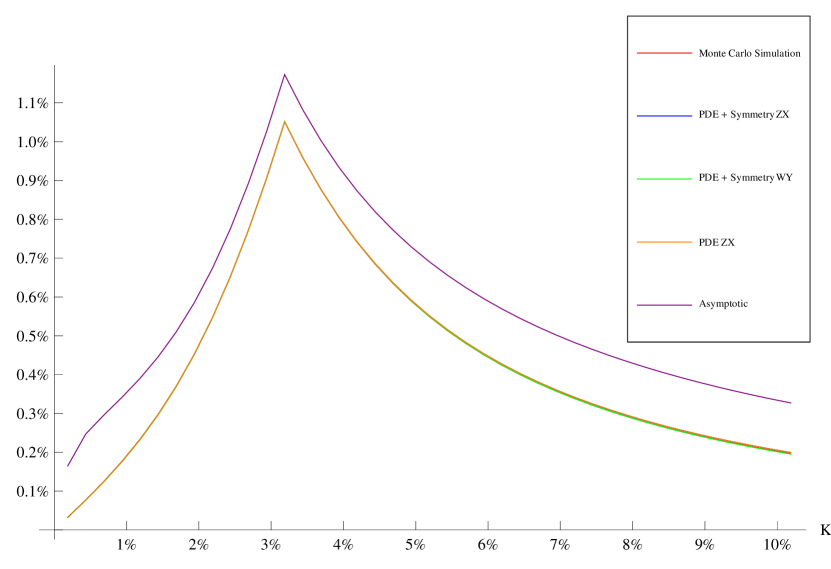

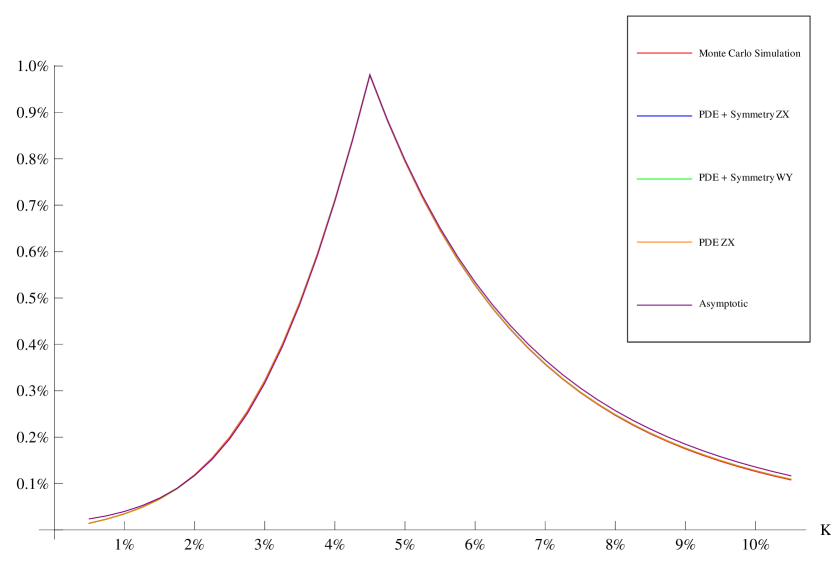

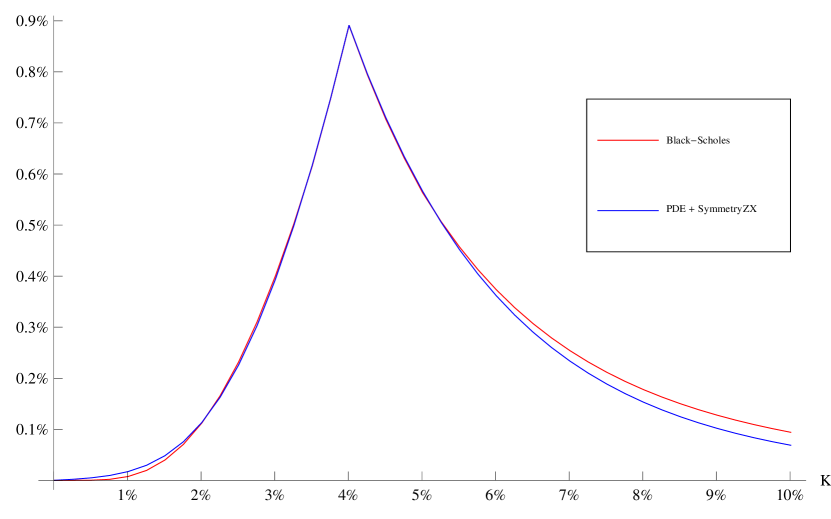

With the calibration done, we priced swaptions with various strikes using the Monte Carlo simulation, the “PDE + Symmetry” method with variables and , and the asymptotic formula. The value of was too high for and variables, causing large numerical errors in swaption prices. The results are shown in fig. 3 and table 4. The results from all three methods show very little difference.

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | Asymptotic |

|---|---|---|---|

| 2.17% | 0.00% | 0.00% | 0.00% |

| 2.67% | 0.01% | 0.01% | 0.01% |

| 3.17% | 0.02% | 0.02% | 0.02% |

| 3.67% | 0.07% | 0.07% | 0.07% |

| 4.17% | 0.19% | 0.19% | 0.19% |

| 4.42% | 0.28% | 0.27% | 0.28% |

| 4.67% | 0.39% | 0.39% | 0.39% |

| 4.92% | 0.28% | 0.28% | 0.28% |

| 5.17% | 0.19% | 0.19% | 0.19% |

| 5.67% | 0.08% | 0.08% | 0.08% |

| 6.17% | 0.03% | 0.03% | 0.03% |

| 6.67% | 0.01% | 0.01% | 0.01% |

| 7.17% | 0.00% | 0.00% | 0.00% |

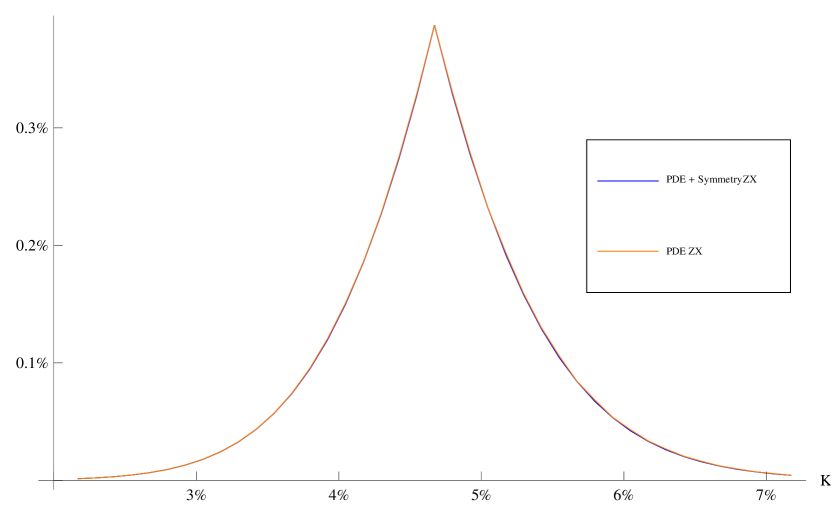

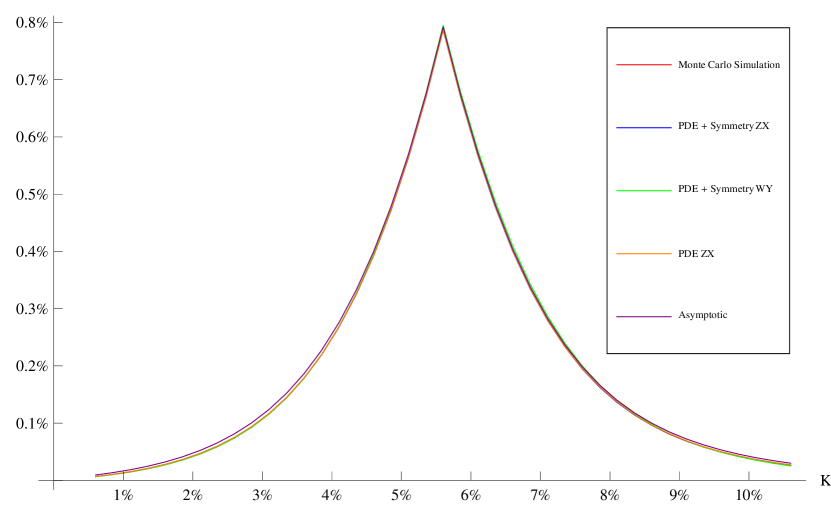

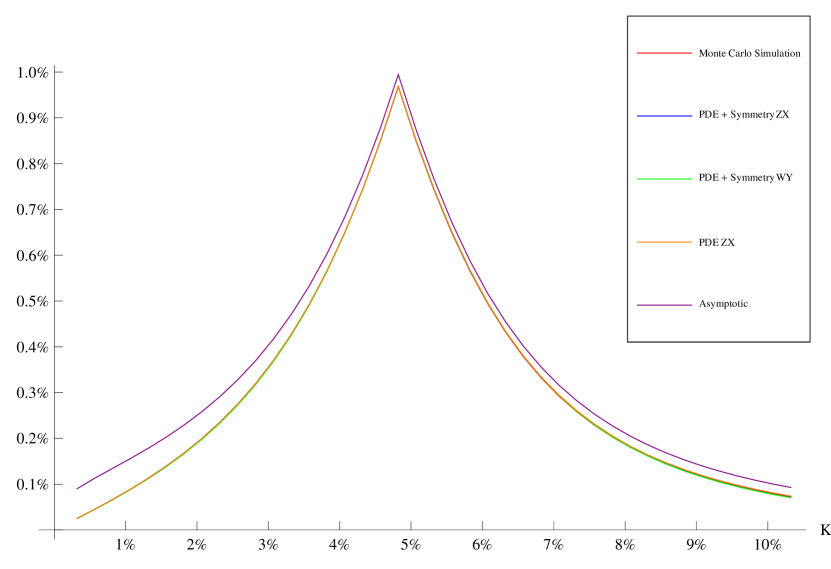

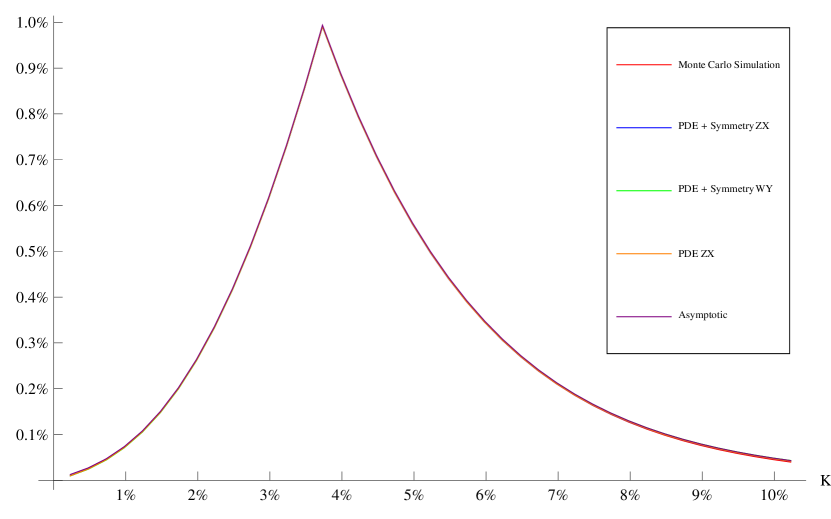

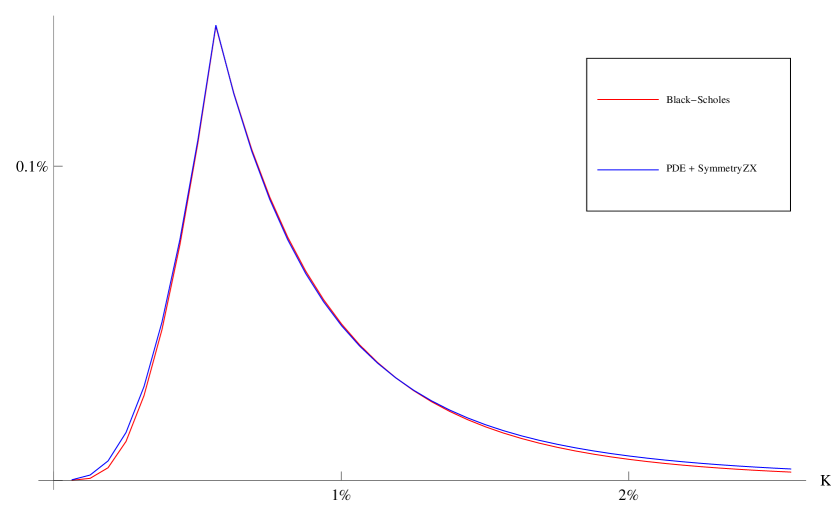

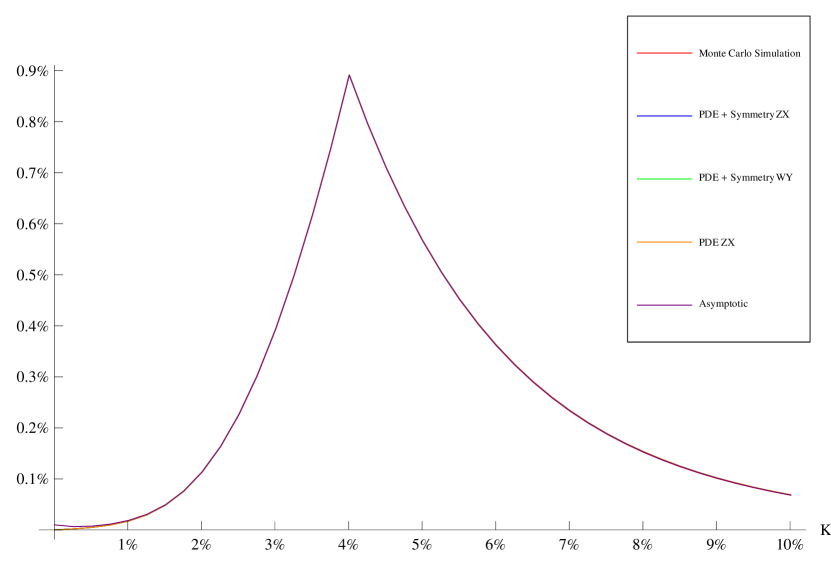

To further test how well the symmetry is respected in the solutions of the PDE’s, we computed the swaption prices by solving the PDE’s for each strike separately and compared them with the results of the “PDE + Symmetry” method. Note that numerically computed solutions do not necessarily show the symmetry since the discretization of the variables breaks it. Figure 4 and table 5 show the comparison result. These two methods produced identical results with no noticeable differences.

| Strike | PDE + Symmetry ZX | PDE ZX |

|---|---|---|

| 2.17% | 0.00% | 0.00% |

| 2.67% | 0.01% | 0.01% |

| 3.17% | 0.02% | 0.02% |

| 3.67% | 0.07% | 0.07% |

| 4.17% | 0.19% | 0.19% |

| 4.42% | 0.27% | 0.27% |

| 4.67% | 0.39% | 0.39% |

| 4.92% | 0.28% | 0.28% |

| 5.17% | 0.19% | 0.19% |

| 5.67% | 0.08% | 0.08% |

| 6.17% | 0.03% | 0.03% |

| 6.67% | 0.01% | 0.01% |

| 7.17% | 0.00% | 0.00% |

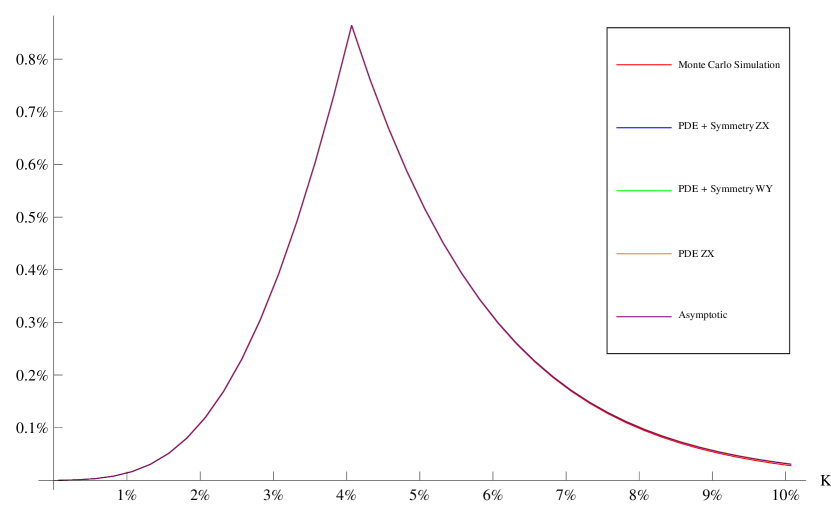

We repeated the same tests for 5 year expiry and 5 year tenor, 10 year expiry and 10 year tenor, and 20 year expiry and 20 year tenor combinations. Let’s start with the 5Y5Y combination. The 5Y5Y forward swap rate was and the market volatilities are shown in table 6.

| Strike(%) | 3.60 | 4.60 | 5.10 | 5.35 | 5.60 | 5.85 | 6.10 | 6.60 | 7.60 |

| Volatility(%) | 20.29 | 17.64 | 16.63 | 16.23 | 15.92 | 15.61 | 15.31 | 14.97 | 14.71 |

We chose and calibrated the rest of the parameters:

| , , , , , | (34) |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 3.60% | 0.18% | 0.18% |

| 4.60% | 0.39% | 0.39% |

| 5.10% | 0.56% | 0.56% |

| 5.35% | 0.67% | 0.67% |

| 5.60% | 0.79% | 0.79% |

| 5.85% | 0.67% | 0.67% |

| 6.10% | 0.57% | 0.57% |

| 6.60% | 0.41% | 0.40% |

| 7.60% | 0.20% | 0.19% |

With the calibrated parameters in eq. 34, we priced swaptions in the various methods and compared the results in fig. 6 and table 8.

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE + Symmetry WY | PDE ZX | Asymptotic |

|---|---|---|---|---|---|

| 0.60% | 0.01% | 0.01% | 0.01% | 0.01% | 0.01% |

| 1.10% | 0.01% | 0.02% | 0.01% | 0.02% | 0.02% |

| 1.60% | 0.03% | 0.03% | 0.03% | 0.03% | 0.03% |

| 2.10% | 0.05% | 0.05% | 0.05% | 0.05% | 0.05% |

| 2.60% | 0.07% | 0.08% | 0.07% | 0.08% | 0.08% |

| 3.10% | 0.12% | 0.12% | 0.12% | 0.12% | 0.12% |

| 3.60% | 0.18% | 0.18% | 0.18% | 0.18% | 0.19% |

| 4.10% | 0.27% | 0.27% | 0.27% | 0.27% | 0.28% |

| 4.60% | 0.39% | 0.39% | 0.40% | 0.39% | 0.40% |

| 5.10% | 0.56% | 0.56% | 0.57% | 0.56% | 0.57% |

| 5.35% | 0.67% | 0.67% | 0.68% | 0.67% | 0.67% |

| 5.60% | 0.79% | 0.79% | 0.80% | 0.79% | 0.79% |

| 5.85% | 0.67% | 0.67% | 0.68% | 0.67% | 0.67% |

| 6.10% | 0.57% | 0.57% | 0.58% | 0.57% | 0.57% |

| 6.60% | 0.40% | 0.40% | 0.41% | 0.40% | 0.40% |

| 7.10% | 0.28% | 0.28% | 0.29% | 0.28% | 0.28% |

| 7.60% | 0.20% | 0.19% | 0.20% | 0.20% | 0.20% |

| 8.10% | 0.14% | 0.14% | 0.14% | 0.14% | 0.14% |

| 8.60% | 0.10% | 0.10% | 0.10% | 0.10% | 0.10% |

| 9.10% | 0.07% | 0.07% | 0.07% | 0.07% | 0.07% |

| 9.60% | 0.05% | 0.05% | 0.05% | 0.05% | 0.05% |

| 10.10% | 0.04% | 0.04% | 0.04% | 0.04% | 0.04% |

| 10.60% | 0.03% | 0.03% | 0.03% | 0.03% | 0.03% |

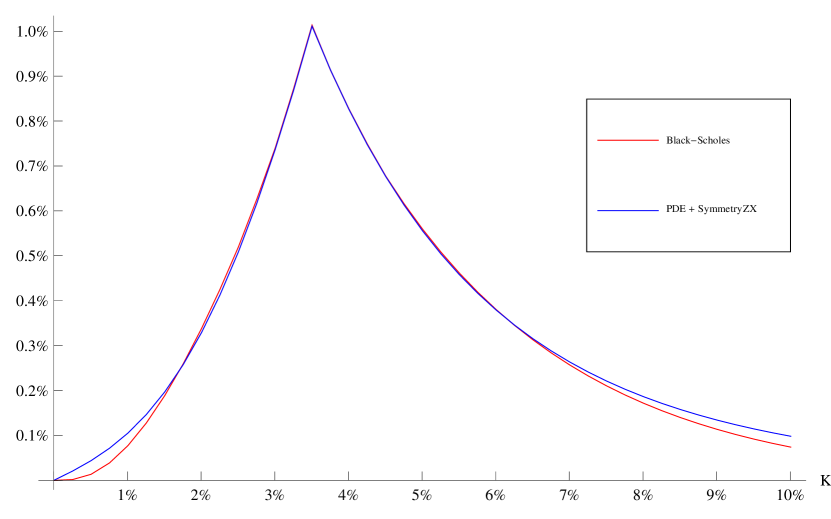

This time, the value of was small enough to use variables and . All methods produced the results that were very close to each other. It is a little difficult to see, but upon closer inspection at fig. 6, it was noted that the asymptotic formula produced prices slightly different from the other methods.

| Strike(%) | 3.80 | 4.80 | 5.30 | 5.55 | 5.80 | 6.05 | 6.30 | 6.80 | 7.80 |

| Volatility(%) | 17.34 | 15.05 | 13.97 | 13.67 | 13.45 | 13.22 | 13.04 | 12.75 | 12.41 |

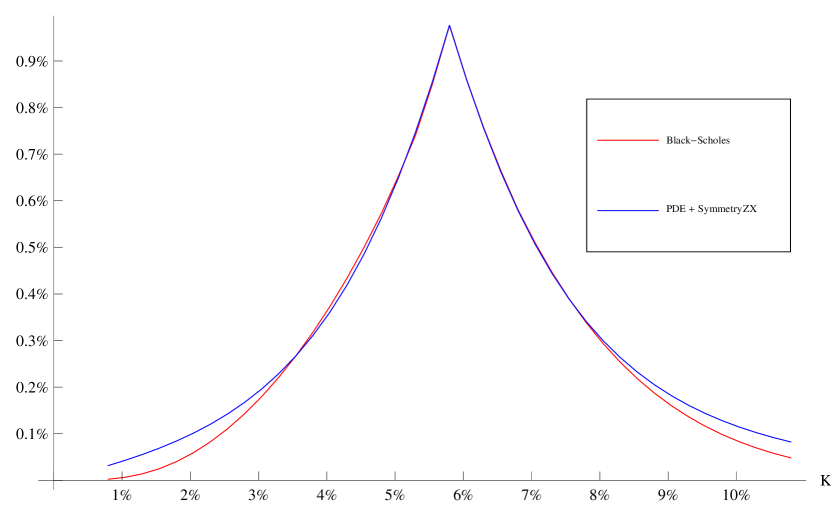

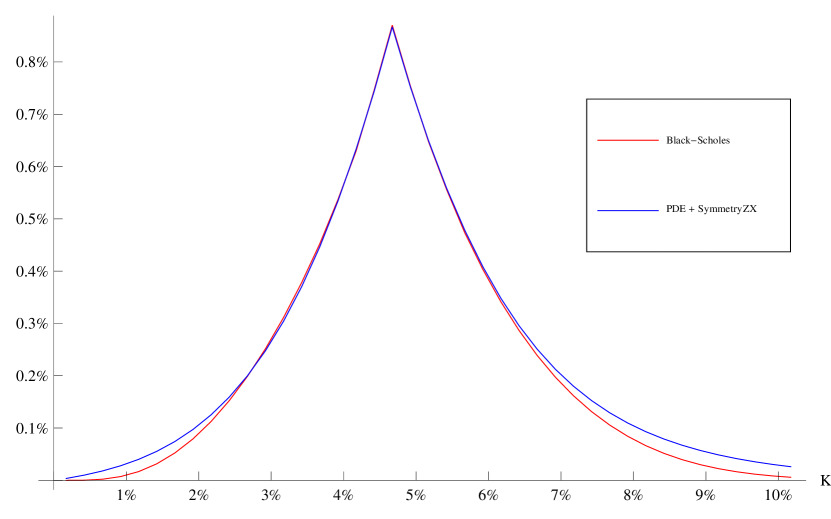

Table 9 shows the USD 10Y10Y swaption volatilities. The forward swap rate was and was chosen. The calibrated parameters are:

| , , , , , | (35) |

Figure 7 and table 10 show the goodness of the calibration and fig. 8 and table 11 show how different methods priced the swaptions. All methods other than the asymptotic formula showed almost identical results. The difference between the asymptotic formula and the other methods is noticeable, more so at low strikes.

| Strike | Black-Scholes | SABR |

|---|---|---|

| 3.80% | 0.32% | 0.31% |

| 4.80% | 0.57% | 0.56% |

| 5.30% | 0.74% | 0.75% |

| 5.55% | 0.85% | 0.86% |

| 5.80% | 0.98% | 0.98% |

| 6.05% | 0.86% | 0.86% |

| 6.30% | 0.76% | 0.76% |

| 6.80% | 0.58% | 0.58% |

| 7.80% | 0.34% | 0.34% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE + Symmetry WY | PDE ZX | Asymptotic |

|---|---|---|---|---|---|

| 0.80% | 0.03% | 0.03% | 0.03% | 0.03% | 0.06% |

| 1.30% | 0.05% | 0.06% | 0.05% | 0.06% | 0.08% |

| 1.80% | 0.08% | 0.08% | 0.08% | 0.08% | 0.10% |

| 2.30% | 0.12% | 0.12% | 0.12% | 0.12% | 0.14% |

| 2.80% | 0.16% | 0.17% | 0.16% | 0.17% | 0.18% |

| 3.30% | 0.23% | 0.23% | 0.22% | 0.23% | 0.24% |

| 3.80% | 0.31% | 0.31% | 0.31% | 0.31% | 0.32% |

| 4.30% | 0.42% | 0.42% | 0.42% | 0.42% | 0.43% |

| 4.80% | 0.56% | 0.56% | 0.56% | 0.56% | 0.57% |

| 5.30% | 0.74% | 0.75% | 0.75% | 0.75% | 0.75% |

| 5.55% | 0.85% | 0.86% | 0.86% | 0.86% | 0.86% |

| 5.80% | 0.97% | 0.98% | 0.98% | 0.98% | 0.98% |

| 6.05% | 0.86% | 0.86% | 0.86% | 0.86% | 0.86% |

| 6.30% | 0.75% | 0.76% | 0.76% | 0.76% | 0.76% |

| 6.80% | 0.58% | 0.58% | 0.58% | 0.58% | 0.58% |

| 7.30% | 0.44% | 0.44% | 0.45% | 0.45% | 0.45% |

| 7.80% | 0.34% | 0.34% | 0.34% | 0.34% | 0.35% |

| 8.30% | 0.26% | 0.26% | 0.26% | 0.26% | 0.27% |

| 8.80% | 0.20% | 0.21% | 0.20% | 0.21% | 0.21% |

| 9.30% | 0.16% | 0.16% | 0.16% | 0.16% | 0.17% |

| 9.80% | 0.13% | 0.13% | 0.12% | 0.13% | 0.14% |

| 10.30% | 0.10% | 0.10% | 0.10% | 0.10% | 0.11% |

| 10.80% | 0.08% | 0.08% | 0.08% | 0.08% | 0.09% |

Finally, we look at the USD 20Y20Y swaptions. The lognormal volatilities are shown in table 12.

| Strike(%) | 3.49 | 4.49 | 4.99 | 5.24 | 5.49 | 5.74 | 5.99 | 6.49 | 7.49 |

| Volatility(%) | 15.77 | 13.34 | 12.31 | 11.92 | 11.60 | 11.35 | 11.10 | 10.84 | 10.48 |

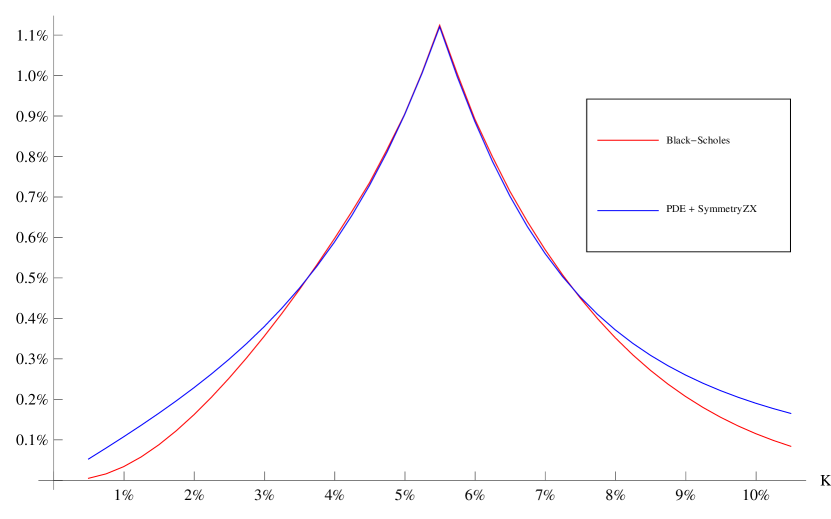

The forward swap rate was and was chosen. The calibrated parameters are:

| , , , , , | (36) |

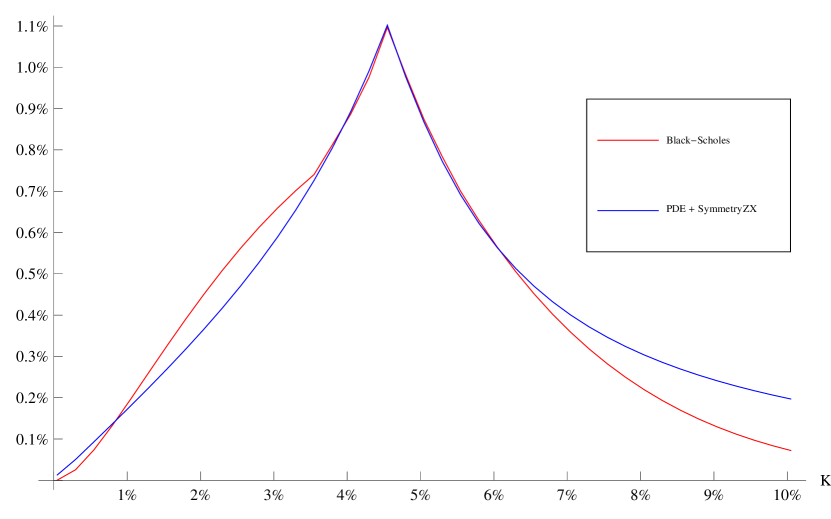

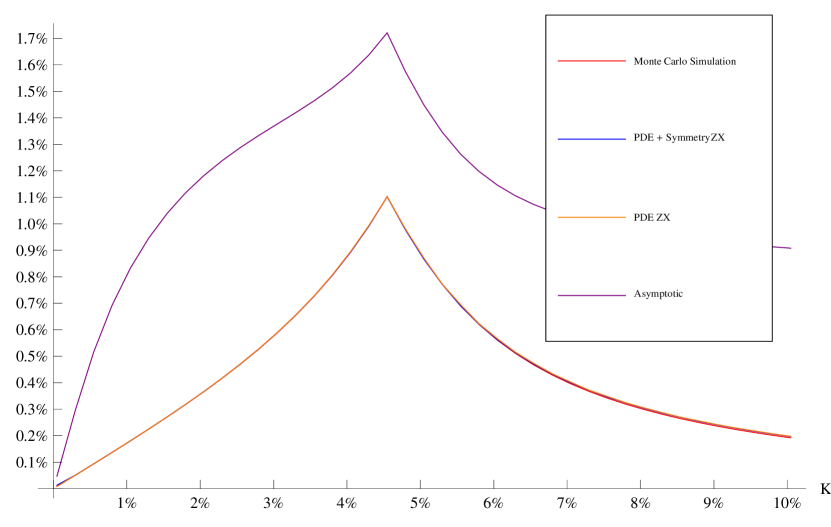

The calibration results are shown in fig. 9 and table 13. Figure 10 and table 14 show swaption pricing results. Now, with longer expiry, the asymptotic series shows fairly large difference from the other methods’ pricing results. The difference is larger at lower strikes. All other methods produced virtually identical prices.

| Strike | Black-Scholes | SABR |

|---|---|---|

| 3.49% | 0.47% | 0.47% |

| 4.49% | 0.73% | 0.73% |

| 4.99% | 0.90% | 0.90% |

| 5.24% | 1.01% | 1.01% |

| 5.49% | 1.12% | 1.12% |

| 5.74% | 1.00% | 1.00% |

| 5.99% | 0.89% | 0.89% |

| 6.49% | 0.71% | 0.70% |

| 7.49% | 0.45% | 0.45% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE + Symmetry WY | PDE ZX | Asymptotic |

|---|---|---|---|---|---|

| 0.49% | 0.05% | 0.05% | 0.05% | 0.05% | 0.24% |

| 0.99% | 0.11% | 0.11% | 0.11% | 0.11% | 0.32% |

| 1.49% | 0.17% | 0.17% | 0.16% | 0.17% | 0.38% |

| 1.99% | 0.23% | 0.23% | 0.23% | 0.23% | 0.44% |

| 2.49% | 0.30% | 0.30% | 0.30% | 0.30% | 0.50% |

| 2.99% | 0.38% | 0.38% | 0.38% | 0.38% | 0.56% |

| 3.49% | 0.47% | 0.47% | 0.47% | 0.47% | 0.64% |

| 3.99% | 0.59% | 0.59% | 0.59% | 0.59% | 0.74% |

| 4.49% | 0.73% | 0.73% | 0.73% | 0.73% | 0.86% |

| 4.99% | 0.90% | 0.90% | 0.90% | 0.90% | 1.02% |

| 5.24% | 1.01% | 1.01% | 1.01% | 1.01% | 1.11% |

| 5.49% | 1.12% | 1.12% | 1.13% | 1.12% | 1.22% |

| 5.74% | 1.00% | 1.00% | 1.00% | 1.00% | 1.09% |

| 5.99% | 0.89% | 0.89% | 0.89% | 0.89% | 0.98% |

| 6.49% | 0.70% | 0.70% | 0.71% | 0.70% | 0.79% |

| 6.99% | 0.56% | 0.56% | 0.56% | 0.56% | 0.65% |

| 7.49% | 0.45% | 0.45% | 0.45% | 0.45% | 0.54% |

| 7.99% | 0.37% | 0.37% | 0.37% | 0.37% | 0.46% |

| 8.49% | 0.30% | 0.31% | 0.31% | 0.31% | 0.40% |

| 8.99% | 0.26% | 0.26% | 0.26% | 0.26% | 0.35% |

| 9.49% | 0.22% | 0.22% | 0.22% | 0.22% | 0.31% |

| 9.99% | 0.19% | 0.19% | 0.18% | 0.19% | 0.28% |

| 10.49% | 0.16% | 0.17% | 0.16% | 0.17% | 0.25% |

The same tests were performed for the USD swaption market on different dates. Since the testing results were qualitatively similar to the previous one, we present the results without much explanations.

3.3.2 September 15th, 2008

We make some comments on the tests done for the USD swaption market on September 15th, 2008. First, the calibration results for the 20Y20Y swaptions were not quite good. We could not find the model parameters that match volatilities at all strikes equally good. The implied volatility() at the lowest strike() seems to be too high for the SABR model to match. Hence, we calibrated the model trying to match market prices of swaptions at other strikes better.

Also, the “PDE + Symmetry” method with variable and produced large errors for the 1Y1Y and 20Y20Y swaptions, and was not included in the pricing method comparisons. This method seems to struggle with the high value(0.9) of in the 1Y1Y case and with the large value(50%) of in the 20Y20Y case. The “PDE + Symmetry” method with variable and performed well for the both cases.

| Expiry/Tenor | -200bp | -100bp | -50bp | -25bp | 0bp | +25bp | +50bp | +100bp | +200bp | ATM |

|---|---|---|---|---|---|---|---|---|---|---|

| 1Y1Y | 61.09% | 54.18% | 50.70% | 49.76% | 48.82% | 47.84% | 46.03% | 44.37% | 41.97% | 2.99% |

| 5Y5Y | 27.00% | 23.54% | 21.95% | 21.55% | 21.08% | 20.60% | 20.12% | 19.40% | 18.30% | 4.67% |

| 10Y10Y | 22.56% | 18.49% | 16.67% | 16.39% | 16.11% | 15.83% | 15.57% | 15.08% | 14.52% | 4.82% |

| 20Y20Y | 22.51% | 16.71% | 14.88% | 14.13% | 13.73% | 13.43% | 13.12% | 12.76% | 12.36% | 4.55% |

| Expiry/Tenor | ||||||

|---|---|---|---|---|---|---|

| 1Y1Y | 0.90 | 30.0% | -75.0% | 35.40% | 2.99% | 1 |

| 5Y5Y | 0.40 | 25.0% | -20.0% | 3.29% | 4.67% | 5 |

| 10Y10Y | 0.10 | 30.0% | -10.0% | 1.00% | 4.82% | 10 |

| 20Y20Y | 0.00 | 50.0% | -25.0% | 0.72% | 4.55% | 20 |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 0.99% | 0.01% | 0.02% |

| 1.99% | 0.17% | 0.17% |

| 2.49% | 0.33% | 0.34% |

| 2.74% | 0.45% | 0.45% |

| 2.99% | 0.58% | 0.57% |

| 3.24% | 0.47% | 0.47% |

| 3.49% | 0.37% | 0.38% |

| 3.99% | 0.23% | 0.24% |

| 4.99% | 0.09% | 0.09% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE ZX | Asymptotic |

|---|---|---|---|---|

| 0.49% | 0.00% | 0.00% | 0.00% | 0.00% |

| 0.99% | 0.02% | 0.02% | 0.02% | 0.02% |

| 1.49% | 0.07% | 0.07% | 0.07% | 0.07% |

| 1.99% | 0.17% | 0.17% | 0.17% | 0.17% |

| 2.49% | 0.34% | 0.34% | 0.34% | 0.34% |

| 2.74% | 0.45% | 0.45% | 0.45% | 0.45% |

| 2.99% | 0.58% | 0.57% | 0.57% | 0.58% |

| 3.24% | 0.47% | 0.47% | 0.47% | 0.47% |

| 3.49% | 0.38% | 0.38% | 0.38% | 0.38% |

| 3.99% | 0.24% | 0.24% | 0.24% | 0.24% |

| 4.49% | 0.15% | 0.15% | 0.15% | 0.15% |

| 4.99% | 0.09% | 0.09% | 0.09% | 0.09% |

| 5.49% | 0.05% | 0.05% | 0.05% | 0.05% |

| 5.99% | 0.03% | 0.03% | 0.03% | 0.03% |

| 6.49% | 0.01% | 0.02% | 0.02% | 0.02% |

| 6.99% | 0.01% | 0.01% | 0.01% | 0.01% |

| 7.49% | 0.00% | 0.01% | 0.01% | 0.00% |

| 7.99% | 0.00% | 0.00% | 0.00% | 0.00% |

| 8.49% | 0.00% | 0.00% | 0.00% | 0.00% |

| 8.99% | 0.00% | 0.00% | 0.00% | 0.00% |

| 9.49% | 0.00% | 0.00% | 0.00% | 0.00% |

| 9.99% | 0.00% | 0.00% | 0.00% | 0.00% |

| 10.49% | 0.00% | 0.00% | 0.00% | 0.00% |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 2.67% | 0.20% | 0.20% |

| 3.67% | 0.45% | 0.45% |

| 4.17% | 0.63% | 0.63% |

| 4.42% | 0.75% | 0.74% |

| 4.67% | 0.87% | 0.87% |

| 4.92% | 0.75% | 0.75% |

| 5.17% | 0.65% | 0.65% |

| 5.67% | 0.47% | 0.48% |

| 6.67% | 0.24% | 0.25% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE + Symmetry WY | PDE ZX | Asymptotic |

|---|---|---|---|---|---|

| 0.17% | 0.00% | 0.00% | 0.00% | 0.00% | 0.01% |

| 0.67% | 0.02% | 0.02% | 0.02% | 0.02% | 0.02% |

| 1.17% | 0.04% | 0.04% | 0.04% | 0.04% | 0.04% |

| 1.67% | 0.07% | 0.07% | 0.07% | 0.07% | 0.08% |

| 2.17% | 0.12% | 0.13% | 0.12% | 0.13% | 0.13% |

| 2.67% | 0.20% | 0.20% | 0.20% | 0.20% | 0.21% |

| 3.17% | 0.30% | 0.30% | 0.30% | 0.30% | 0.31% |

| 3.67% | 0.45% | 0.45% | 0.45% | 0.45% | 0.45% |

| 4.17% | 0.63% | 0.63% | 0.63% | 0.63% | 0.64% |

| 4.42% | 0.74% | 0.74% | 0.75% | 0.74% | 0.75% |

| 4.67% | 0.87% | 0.87% | 0.87% | 0.87% | 0.87% |

| 4.92% | 0.75% | 0.75% | 0.76% | 0.75% | 0.76% |

| 5.17% | 0.65% | 0.65% | 0.65% | 0.65% | 0.65% |

| 5.67% | 0.48% | 0.48% | 0.48% | 0.48% | 0.48% |

| 6.17% | 0.35% | 0.35% | 0.35% | 0.35% | 0.35% |

| 6.67% | 0.25% | 0.25% | 0.25% | 0.25% | 0.25% |

| 7.17% | 0.18% | 0.18% | 0.18% | 0.18% | 0.18% |

| 7.67% | 0.13% | 0.13% | 0.13% | 0.13% | 0.13% |

| 8.17% | 0.09% | 0.09% | 0.09% | 0.09% | 0.10% |

| 8.67% | 0.07% | 0.07% | 0.07% | 0.07% | 0.07% |

| 9.17% | 0.05% | 0.05% | 0.05% | 0.05% | 0.05% |

| 9.67% | 0.04% | 0.04% | 0.04% | 0.04% | 0.04% |

| 10.17% | 0.03% | 0.03% | 0.03% | 0.03% | 0.03% |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 2.82% | 0.33% | 0.32% |

| 3.82% | 0.57% | 0.57% |

| 4.32% | 0.72% | 0.74% |

| 4.57% | 0.84% | 0.85% |

| 4.82% | 0.97% | 0.97% |

| 5.07% | 0.86% | 0.85% |

| 5.32% | 0.76% | 0.74% |

| 5.82% | 0.58% | 0.57% |

| 6.82% | 0.34% | 0.33% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE + Symmetry WY | PDE ZX | Asymptotic |

|---|---|---|---|---|---|

| 0.32% | 0.03% | 0.03% | 0.03% | 0.03% | 0.09% |

| 0.82% | 0.07% | 0.07% | 0.07% | 0.07% | 0.13% |

| 1.32% | 0.11% | 0.11% | 0.11% | 0.11% | 0.18% |

| 1.82% | 0.17% | 0.17% | 0.17% | 0.17% | 0.23% |

| 2.32% | 0.23% | 0.24% | 0.23% | 0.24% | 0.29% |

| 2.82% | 0.32% | 0.32% | 0.32% | 0.32% | 0.37% |

| 3.32% | 0.43% | 0.43% | 0.42% | 0.43% | 0.47% |

| 3.82% | 0.57% | 0.57% | 0.56% | 0.57% | 0.60% |

| 4.32% | 0.74% | 0.74% | 0.74% | 0.74% | 0.77% |

| 4.57% | 0.85% | 0.85% | 0.85% | 0.85% | 0.88% |

| 4.82% | 0.97% | 0.97% | 0.97% | 0.97% | 0.99% |

| 5.07% | 0.85% | 0.85% | 0.85% | 0.85% | 0.87% |

| 5.57% | 0.65% | 0.65% | 0.65% | 0.65% | 0.67% |

| 6.07% | 0.49% | 0.50% | 0.50% | 0.50% | 0.52% |

| 6.57% | 0.38% | 0.38% | 0.38% | 0.38% | 0.40% |

| 7.07% | 0.29% | 0.29% | 0.29% | 0.29% | 0.32% |

| 7.57% | 0.23% | 0.23% | 0.23% | 0.23% | 0.25% |

| 8.07% | 0.18% | 0.18% | 0.18% | 0.18% | 0.20% |

| 8.57% | 0.14% | 0.15% | 0.14% | 0.15% | 0.17% |

| 9.07% | 0.12% | 0.12% | 0.12% | 0.12% | 0.14% |

| 9.57% | 0.10% | 0.10% | 0.09% | 0.10% | 0.12% |

| 10.07% | 0.08% | 0.08% | 0.08% | 0.08% | 0.10% |

| 10.57% | 0.07% | 0.07% | 0.06% | 0.07% | 0.09% |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 2.55% | 0.56% | 0.47% |

| 3.55% | 0.74% | 0.73% |

| 4.05% | 0.89% | 0.89% |

| 4.30% | 0.98% | 0.99% |

| 4.55% | 1.10% | 1.10% |

| 4.80% | 0.98% | 0.98% |

| 5.05% | 0.87% | 0.87% |

| 5.55% | 0.70% | 0.69% |

| 6.55% | 0.45% | 0.47% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE ZX | Asymptotic |

|---|---|---|---|---|

| 0.05% | 0.01% | 0.01% | 0.01% | 0.05% |

| 0.55% | 0.09% | 0.09% | 0.09% | 0.51% |

| 1.05% | 0.18% | 0.18% | 0.18% | 0.83% |

| 1.55% | 0.27% | 0.27% | 0.27% | 1.04% |

| 2.05% | 0.37% | 0.37% | 0.37% | 1.18% |

| 2.55% | 0.47% | 0.47% | 0.47% | 1.29% |

| 3.05% | 0.59% | 0.59% | 0.59% | 1.38% |

| 3.55% | 0.73% | 0.73% | 0.73% | 1.46% |

| 4.05% | 0.89% | 0.89% | 0.89% | 1.57% |

| 4.30% | 0.99% | 0.99% | 0.99% | 1.64% |

| 4.55% | 1.10% | 1.10% | 1.10% | 1.72% |

| 4.80% | 0.98% | 0.98% | 0.98% | 1.57% |

| 5.30% | 0.77% | 0.77% | 0.77% | 1.35% |

| 5.80% | 0.62% | 0.62% | 0.62% | 1.20% |

| 6.30% | 0.51% | 0.51% | 0.51% | 1.11% |

| 6.80% | 0.43% | 0.43% | 0.43% | 1.05% |

| 7.30% | 0.37% | 0.37% | 0.37% | 1.01% |

| 7.80% | 0.32% | 0.32% | 0.32% | 0.98% |

| 8.30% | 0.28% | 0.29% | 0.29% | 0.96% |

| 8.80% | 0.25% | 0.25% | 0.26% | 0.94% |

| 9.30% | 0.22% | 0.23% | 0.23% | 0.92% |

| 9.80% | 0.20% | 0.21% | 0.21% | 0.91% |

| 10.30% | 0.18% | 0.19% | 0.19% | 0.90% |

3.3.3 March 9th, 2009

As before, the “PDE + Symmetry” method with variable and did not perform well for the 1Y1Y swaptions due to the high value(0.9) of and was not included in the pricing method comparison.

| Expiry/Tenor | -200bp | -100bp | -50bp | -25bp | 0bp | +25bp | +50bp | +100bp | +200bp | ATM |

|---|---|---|---|---|---|---|---|---|---|---|

| 1Y1Y | 58.43% | 54.53% | 52.59% | 50.88% | 49.23% | 48.11% | 46.26% | 43.35% | 2.00% | |

| 5Y5Y | 37.69% | 33.09% | 31.42% | 30.76% | 30.18% | 29.67% | 29.24% | 28.51% | 27.38% | 3.73% |

| 10Y10Y | 28.88% | 25.59% | 24.23% | 23.82% | 23.44% | 23.08% | 22.86% | 22.47% | 22.03% | 3.51% |

| 20Y20Y | 25.30% | 21.25% | 20.16% | 19.61% | 19.12% | 18.96% | 18.77% | 18.50% | 18.36% | 3.19% |

| Expiry/Tenor | ||||||

|---|---|---|---|---|---|---|

| 1Y1Y | 0.90 | 30.0% | -75.0% | 35.44% | 2.00% | 1 |

| 5Y5Y | 0.40 | 15.0% | 15.0% | 4.15% | 3.73% | 5 |

| 10Y10Y | 0.10 | 21.0% | 60.0% | 1.10% | 3.51% | 10 |

| 20Y20Y | 0.00 | 30.0% | 40.0% | 0.60% | 3.19% | 20 |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 1.00% | 0.05% | 0.05% |

| 1.50% | 0.18% | 0.18% |

| 1.75% | 0.28% | 0.28% |

| 2.00% | 0.40% | 0.40% |

| 2.25% | 0.30% | 0.30% |

| 2.50% | 0.22% | 0.22% |

| 3.00% | 0.12% | 0.11% |

| 4.00% | 0.03% | 0.03% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE ZX | Asymptotic |

|---|---|---|---|---|

| 0.50% | 0.01% | 0.01% | 0.01% | 0.01% |

| 1.00% | 0.05% | 0.05% | 0.05% | 0.05% |

| 1.50% | 0.18% | 0.18% | 0.18% | 0.18% |

| 1.75% | 0.28% | 0.28% | 0.28% | 0.28% |

| 2.00% | 0.40% | 0.40% | 0.40% | 0.40% |

| 2.25% | 0.30% | 0.30% | 0.30% | 0.30% |

| 2.50% | 0.22% | 0.22% | 0.22% | 0.22% |

| 3.00% | 0.11% | 0.11% | 0.11% | 0.11% |

| 3.50% | 0.05% | 0.05% | 0.05% | 0.05% |

| 4.00% | 0.02% | 0.03% | 0.03% | 0.02% |

| 4.50% | 0.01% | 0.01% | 0.01% | 0.01% |

| 5.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 1.73% | 0.20% | 0.20% |

| 2.73% | 0.51% | 0.51% |

| 3.23% | 0.72% | 0.73% |

| 3.48% | 0.85% | 0.85% |

| 3.73% | 0.99% | 0.99% |

| 3.98% | 0.88% | 0.89% |

| 4.23% | 0.79% | 0.79% |

| 4.73% | 0.63% | 0.63% |

| 5.73% | 0.39% | 0.39% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE + Symmetry WY | PDE ZX | Asymptotic |

|---|---|---|---|---|---|

| 0.23% | 0.01% | 0.01% | 0.01% | 0.01% | 0.01% |

| 0.73% | 0.05% | 0.05% | 0.04% | 0.05% | 0.05% |

| 1.23% | 0.11% | 0.11% | 0.11% | 0.11% | 0.11% |

| 1.73% | 0.20% | 0.20% | 0.20% | 0.20% | 0.20% |

| 2.23% | 0.33% | 0.33% | 0.33% | 0.33% | 0.34% |

| 2.73% | 0.51% | 0.51% | 0.51% | 0.51% | 0.51% |

| 3.23% | 0.73% | 0.73% | 0.73% | 0.73% | 0.73% |

| 3.48% | 0.86% | 0.85% | 0.85% | 0.85% | 0.86% |

| 3.73% | 0.99% | 0.99% | 0.99% | 0.99% | 0.99% |

| 3.98% | 0.89% | 0.89% | 0.89% | 0.89% | 0.89% |

| 4.23% | 0.79% | 0.79% | 0.79% | 0.79% | 0.80% |

| 4.73% | 0.63% | 0.63% | 0.63% | 0.63% | 0.63% |

| 5.23% | 0.50% | 0.50% | 0.50% | 0.50% | 0.50% |

| 5.73% | 0.39% | 0.39% | 0.39% | 0.39% | 0.39% |

| 6.23% | 0.31% | 0.31% | 0.31% | 0.31% | 0.31% |

| 6.73% | 0.24% | 0.24% | 0.24% | 0.24% | 0.24% |

| 7.23% | 0.19% | 0.19% | 0.19% | 0.19% | 0.19% |

| 7.73% | 0.14% | 0.14% | 0.15% | 0.15% | 0.15% |

| 8.23% | 0.11% | 0.11% | 0.11% | 0.11% | 0.11% |

| 8.73% | 0.09% | 0.09% | 0.09% | 0.09% | 0.09% |

| 9.23% | 0.07% | 0.07% | 0.07% | 0.07% | 0.07% |

| 9.73% | 0.05% | 0.05% | 0.06% | 0.05% | 0.06% |

| 10.23% | 0.04% | 0.04% | 0.04% | 0.04% | 0.04% |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 1.51% | 0.19% | 0.20% |

| 2.51% | 0.52% | 0.51% |

| 3.01% | 0.74% | 0.74% |

| 3.26% | 0.87% | 0.87% |

| 3.51% | 1.01% | 1.01% |

| 3.76% | 0.91% | 0.91% |

| 4.01% | 0.83% | 0.83% |

| 4.51% | 0.68% | 0.68% |

| 5.51% | 0.46% | 0.46% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE + Symmetry WY | PDE ZX | Asymptotic |

|---|---|---|---|---|---|

| 0.01% | 0.00% | 0.00% | 0.00% | 0.00% | 0.01% |

| 0.51% | 0.04% | 0.04% | 0.04% | 0.04% | 0.07% |

| 1.01% | 0.11% | 0.11% | 0.10% | 0.11% | 0.12% |

| 1.51% | 0.20% | 0.20% | 0.20% | 0.20% | 0.20% |

| 2.01% | 0.33% | 0.33% | 0.33% | 0.33% | 0.33% |

| 2.51% | 0.51% | 0.51% | 0.51% | 0.51% | 0.51% |

| 3.01% | 0.74% | 0.74% | 0.74% | 0.74% | 0.74% |

| 3.26% | 0.87% | 0.87% | 0.87% | 0.87% | 0.87% |

| 3.51% | 1.01% | 1.01% | 1.01% | 1.01% | 1.01% |

| 3.76% | 0.91% | 0.91% | 0.91% | 0.91% | 0.92% |

| 4.01% | 0.83% | 0.83% | 0.83% | 0.83% | 0.83% |

| 4.51% | 0.68% | 0.68% | 0.68% | 0.68% | 0.68% |

| 5.01% | 0.56% | 0.56% | 0.56% | 0.56% | 0.56% |

| 5.51% | 0.46% | 0.46% | 0.46% | 0.46% | 0.46% |

| 6.01% | 0.38% | 0.38% | 0.38% | 0.38% | 0.38% |

| 6.51% | 0.31% | 0.32% | 0.32% | 0.32% | 0.32% |

| 7.01% | 0.26% | 0.26% | 0.26% | 0.26% | 0.27% |

| 7.51% | 0.22% | 0.22% | 0.22% | 0.22% | 0.23% |

| 8.01% | 0.18% | 0.19% | 0.19% | 0.19% | 0.19% |

| 8.51% | 0.16% | 0.16% | 0.16% | 0.16% | 0.16% |

| 9.01% | 0.13% | 0.13% | 0.13% | 0.13% | 0.14% |

| 9.51% | 0.11% | 0.11% | 0.11% | 0.11% | 0.12% |

| 10.01% | 0.10% | 0.10% | 0.10% | 0.10% | 0.10% |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 1.19% | 0.21% | 0.23% |

| 2.19% | 0.55% | 0.55% |

| 2.69% | 0.79% | 0.77% |

| 2.94% | 0.92% | 0.91% |

| 3.19% | 1.05% | 1.05% |

| 3.44% | 0.97% | 0.96% |

| 3.69% | 0.88% | 0.88% |

| 4.19% | 0.74% | 0.74% |

| 5.19% | 0.54% | 0.55% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE + Symmetry WY | PDE ZX | Asymptotic |

|---|---|---|---|---|---|

| 0.19% | 0.03% | 0.03% | 0.03% | 0.03% | 0.16% |

| 0.69% | 0.12% | 0.12% | 0.12% | 0.12% | 0.30% |

| 1.19% | 0.23% | 0.23% | 0.23% | 0.23% | 0.39% |

| 1.69% | 0.37% | 0.37% | 0.37% | 0.37% | 0.51% |

| 2.19% | 0.55% | 0.55% | 0.55% | 0.55% | 0.67% |

| 2.69% | 0.77% | 0.77% | 0.77% | 0.77% | 0.89% |

| 2.94% | 0.91% | 0.91% | 0.91% | 0.91% | 1.03% |

| 3.19% | 1.05% | 1.05% | 1.05% | 1.05% | 1.17% |

| 3.44% | 0.96% | 0.96% | 0.96% | 0.96% | 1.08% |

| 3.69% | 0.88% | 0.88% | 0.88% | 0.88% | 1.00% |

| 4.19% | 0.74% | 0.74% | 0.74% | 0.74% | 0.87% |

| 4.69% | 0.63% | 0.64% | 0.64% | 0.64% | 0.77% |

| 5.19% | 0.55% | 0.55% | 0.55% | 0.55% | 0.69% |

| 5.69% | 0.48% | 0.48% | 0.48% | 0.48% | 0.62% |

| 6.19% | 0.42% | 0.43% | 0.43% | 0.43% | 0.57% |

| 6.69% | 0.38% | 0.38% | 0.38% | 0.38% | 0.52% |

| 7.19% | 0.34% | 0.34% | 0.34% | 0.34% | 0.48% |

| 7.69% | 0.31% | 0.31% | 0.31% | 0.31% | 0.45% |

| 8.19% | 0.28% | 0.28% | 0.28% | 0.28% | 0.42% |

| 8.69% | 0.25% | 0.26% | 0.25% | 0.26% | 0.39% |

| 9.19% | 0.23% | 0.23% | 0.23% | 0.23% | 0.37% |

| 9.69% | 0.21% | 0.22% | 0.21% | 0.22% | 0.35% |

| 10.19% | 0.20% | 0.20% | 0.20% | 0.20% | 0.33% |

3.3.4 October 29th, 2013

Again, the “PDE + Symmetry” method with variable and did not perform well for the 1Y1Y swaptions due to the high value(0.9) of and the method was not included in the pricing method comparison.

| Expiry/Tenor | -200bp | -100bp | -50bp | -25bp | 0bp | +25bp | +50bp | +100bp | +200bp | ATM |

|---|---|---|---|---|---|---|---|---|---|---|

| 1Y1Y | 65.43% | 65.43% | 65.43% | 65.42% | 65.41% | 65.39% | 65.38% | .56% | ||

| 5Y5Y | 27.31% | 25.55% | 24.64% | 24.33% | 24.03% | 23.78% | 23.54% | 23.20% | 22.69% | 4.07% |

| 10Y10Y | 20.01% | 18.35% | 17.80% | 17.66% | 17.55% | 17.44% | 17.33% | 17.34% | 17.51% | 4.50% |

| 20Y20Y | 13.80% | 13.10% | 12.74% | 12.68% | 12.62% | 12.55% | 12.49% | 12.43% | 12.58% | 4.01% |

| Expiry/Tenor | ||||||

|---|---|---|---|---|---|---|

| 1Y1Y | 0.90 | 30.0% | 5.0% | 38.98% | 0.56% | 1 |

| 5Y5Y | 0.40 | 10.0% | 60.0% | 3.48% | 4.07% | 5 |

| 10Y10Y | 0.10 | 23.0% | 55.5% | 1.03% | 4.50% | 10 |

| 20Y20Y | 0.00 | 13.0% | 85.0% | 0.50% | 4.01% | 20 |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 0.06% | 0.00% | 0.00% |

| 0.31% | 0.03% | 0.03% |

| 0.56% | 0.14% | 0.14% |

| 0.81% | 0.08% | 0.08% |

| 1.06% | 0.04% | 0.04% |

| 1.56% | 0.02% | 0.02% |

| 2.56% | 0.00% | 0.00% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE ZX | Asymptotic |

|---|---|---|---|---|

| 0.06% | 0.00% | 0.00% | 0.00% | 0.00% |

| 0.31% | 0.03% | 0.03% | 0.03% | 0.03% |

| 0.56% | 0.15% | 0.14% | 0.14% | 0.15% |

| 0.81% | 0.08% | 0.08% | 0.08% | 0.08% |

| 1.06% | 0.04% | 0.04% | 0.04% | 0.04% |

| 1.56% | 0.01% | 0.02% | 0.02% | 0.02% |

| 2.06% | 0.01% | 0.01% | 0.01% | 0.01% |

| 2.56% | 0.00% | 0.00% | 0.00% | 0.00% |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 2.07% | 0.12% | 0.12% |

| 3.07% | 0.40% | 0.39% |

| 3.57% | 0.60% | 0.60% |

| 3.82% | 0.73% | 0.73% |

| 4.07% | 0.86% | 0.86% |

| 4.32% | 0.76% | 0.76% |

| 4.57% | 0.67% | 0.67% |

| 5.07% | 0.52% | 0.51% |

| 6.07% | 0.30% | 0.30% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE + Symmetry WY | PDE ZX | Asymptotic |

|---|---|---|---|---|---|

| 0.07% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| 0.57% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| 1.07% | 0.02% | 0.02% | 0.02% | 0.02% | 0.02% |

| 1.57% | 0.05% | 0.05% | 0.05% | 0.05% | 0.05% |

| 2.07% | 0.12% | 0.12% | 0.12% | 0.12% | 0.12% |

| 2.57% | 0.23% | 0.23% | 0.23% | 0.23% | 0.23% |

| 3.07% | 0.39% | 0.39% | 0.39% | 0.39% | 0.39% |

| 3.57% | 0.60% | 0.60% | 0.60% | 0.60% | 0.60% |

| 3.82% | 0.73% | 0.73% | 0.73% | 0.73% | 0.73% |

| 4.07% | 0.86% | 0.86% | 0.86% | 0.86% | 0.86% |

| 4.32% | 0.76% | 0.76% | 0.76% | 0.76% | 0.76% |

| 4.82% | 0.59% | 0.59% | 0.59% | 0.59% | 0.59% |

| 5.32% | 0.45% | 0.45% | 0.45% | 0.45% | 0.45% |

| 5.82% | 0.34% | 0.34% | 0.34% | 0.34% | 0.34% |

| 6.32% | 0.26% | 0.26% | 0.26% | 0.26% | 0.26% |

| 6.82% | 0.20% | 0.20% | 0.20% | 0.20% | 0.20% |

| 7.32% | 0.15% | 0.15% | 0.15% | 0.15% | 0.15% |

| 7.82% | 0.11% | 0.11% | 0.11% | 0.11% | 0.11% |

| 8.32% | 0.08% | 0.08% | 0.08% | 0.08% | 0.08% |

| 8.82% | 0.06% | 0.06% | 0.06% | 0.06% | 0.06% |

| 9.32% | 0.04% | 0.05% | 0.05% | 0.05% | 0.05% |

| 9.82% | 0.03% | 0.04% | 0.04% | 0.04% | 0.04% |

| 10.32% | 0.02% | 0.03% | 0.03% | 0.03% | 0.03% |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 2.50% | 0.20% | 0.20% |

| 3.50% | 0.49% | 0.49% |

| 4.00% | 0.71% | 0.71% |

| 4.25% | 0.84% | 0.84% |

| 4.50% | 0.98% | 0.98% |

| 4.75% | 0.88% | 0.88% |

| 5.00% | 0.79% | 0.79% |

| 5.50% | 0.65% | 0.65% |

| 6.50% | 0.44% | 0.43% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE + Symmetry WY | PDE ZX | Asymptotic |

|---|---|---|---|---|---|

| 0.50% | 0.01% | 0.01% | 0.01% | 0.01% | 0.02% |

| 1.00% | 0.03% | 0.03% | 0.03% | 0.03% | 0.04% |

| 1.50% | 0.07% | 0.07% | 0.07% | 0.07% | 0.07% |

| 2.00% | 0.12% | 0.12% | 0.12% | 0.12% | 0.12% |

| 2.50% | 0.20% | 0.20% | 0.20% | 0.20% | 0.20% |

| 3.00% | 0.32% | 0.32% | 0.32% | 0.32% | 0.32% |

| 3.50% | 0.49% | 0.49% | 0.49% | 0.49% | 0.49% |

| 4.00% | 0.71% | 0.71% | 0.71% | 0.71% | 0.71% |

| 4.25% | 0.84% | 0.84% | 0.84% | 0.84% | 0.84% |

| 4.50% | 0.98% | 0.98% | 0.98% | 0.98% | 0.98% |

| 4.75% | 0.88% | 0.88% | 0.88% | 0.88% | 0.88% |

| 5.25% | 0.72% | 0.72% | 0.72% | 0.72% | 0.72% |

| 5.75% | 0.58% | 0.58% | 0.58% | 0.58% | 0.59% |

| 6.25% | 0.48% | 0.48% | 0.48% | 0.48% | 0.48% |

| 6.75% | 0.39% | 0.39% | 0.39% | 0.39% | 0.40% |

| 7.25% | 0.32% | 0.33% | 0.33% | 0.33% | 0.33% |

| 7.75% | 0.27% | 0.27% | 0.27% | 0.27% | 0.28% |

| 8.25% | 0.23% | 0.23% | 0.23% | 0.23% | 0.24% |

| 8.75% | 0.19% | 0.19% | 0.19% | 0.19% | 0.20% |

| 9.25% | 0.16% | 0.16% | 0.16% | 0.16% | 0.17% |

| 9.75% | 0.14% | 0.14% | 0.14% | 0.14% | 0.15% |

| 10.25% | 0.12% | 0.12% | 0.12% | 0.12% | 0.13% |

| 10.75% | 0.10% | 0.10% | 0.10% | 0.10% | 0.11% |

| Strike | Black-Scholes | SABR |

|---|---|---|

| 2.01% | 0.11% | 0.11% |

| 3.01% | 0.40% | 0.39% |

| 3.51% | 0.62% | 0.62% |

| 3.76% | 0.75% | 0.75% |

| 4.01% | 0.89% | 0.89% |

| 4.26% | 0.79% | 0.80% |

| 4.51% | 0.71% | 0.71% |

| 5.01% | 0.56% | 0.57% |

| 6.01% | 0.37% | 0.36% |

| Strike | Monte Carlo simulation | PDE + Symmetry ZX | PDE + Symmetry WY | PDE ZX | Asymptotic |

|---|---|---|---|---|---|

| 0.01% | 0.00% | 0.00% | 0.00% | 0.00% | 0.01% |

| 0.51% | 0.00% | 0.00% | 0.00% | 0.00% | 0.01% |

| 1.01% | 0.02% | 0.02% | 0.02% | 0.02% | 0.02% |

| 1.51% | 0.05% | 0.05% | 0.05% | 0.05% | 0.05% |

| 2.01% | 0.11% | 0.11% | 0.11% | 0.11% | 0.11% |

| 2.51% | 0.23% | 0.23% | 0.23% | 0.23% | 0.23% |

| 3.01% | 0.39% | 0.39% | 0.39% | 0.39% | 0.39% |

| 3.51% | 0.62% | 0.62% | 0.62% | 0.62% | 0.62% |

| 3.76% | 0.75% | 0.75% | 0.75% | 0.75% | 0.75% |

| 4.01% | 0.89% | 0.89% | 0.89% | 0.89% | 0.89% |

| 4.26% | 0.80% | 0.80% | 0.80% | 0.80% | 0.80% |

| 4.76% | 0.63% | 0.63% | 0.63% | 0.63% | 0.63% |

| 5.26% | 0.51% | 0.51% | 0.51% | 0.51% | 0.51% |

| 5.76% | 0.40% | 0.40% | 0.40% | 0.40% | 0.40% |

| 6.26% | 0.32% | 0.32% | 0.32% | 0.32% | 0.32% |

| 6.76% | 0.26% | 0.26% | 0.26% | 0.26% | 0.26% |

| 7.26% | 0.21% | 0.21% | 0.21% | 0.21% | 0.21% |

| 7.76% | 0.17% | 0.17% | 0.17% | 0.17% | 0.17% |

| 8.26% | 0.14% | 0.14% | 0.14% | 0.14% | 0.14% |

| 8.76% | 0.11% | 0.11% | 0.11% | 0.11% | 0.11% |

| 9.26% | 0.09% | 0.09% | 0.09% | 0.09% | 0.09% |

| 9.76% | 0.08% | 0.08% | 0.08% | 0.08% | 0.08% |

| 10.26% | 0.06% | 0.06% | 0.06% | 0.06% | 0.06% |

3.4 Final Comments

After all tests in this section, we conclude that our “PDE + Symmetry” method, especially with variables and , produces accurate swaption prices. This method requires significantly less computational effort than the conventional method of solving the SABR PDE. We finish this article with a brief comment on performance. All numerical routines have a trade-off between performance and accuracy. We can always speed up the routine at the expense of accuracy. That being said, we believe that the performance of our implementation is good enough for commercial applications. Our routine was implemented in Scala(version 2.10.2) and was tested on a 6-core hyper-threading enabled Intel®Xeon®processor E5-1650 running at 3.20GHz. With reasonable accuracy(error 1bp of the forward swap annuity), 10 year swaptions can be priced in as little as milliseconds with . This should be fast enough to allow real time calibration and pricing.

References

- Antonov and Spector [2012] Alexandre Antonov and Michael Spector. Advanced analytics for the SABR model. Available at http://ssrn.com/abstract=2026350, March 2012.

- Berestycki et al. [2004] Henri Berestycki, Jérôme Busca, and Igor Florent. Computing the implied volatility in stochastic volatility models. Comm. Pure Appl. Math., 57(10):1352–1373, 2004. ISSN 0010-3640. doi: 10.1002/cpa.20039. URL http://dx.doi.org/10.1002/cpa.20039.

- Carmona et al. [1997] Philippe Carmona, Frédérique Petit, and Marc Yor. On the distribution and asymptotic results for exponential functionals of Lévy processes. In Exponential functionals and principal values related to Brownian motion, Bibl. Rev. Mat. Iberoamericana, pages 73–130. Rev. Mat. Iberoamericana, Madrid, 1997.

- Donati-Martin et al. [2001] Catherine Donati-Martin, Raouf Ghomrasni, and Marc Yor. On certain Markov processes attached to exponential functionals of Brownian motion; application to Asian options. Rev. Mat. Iberoamericana, 17(1):179–193, 2001. ISSN 0213-2230. doi: 10.4171/RMI/292. URL http://dx.doi.org/10.4171/RMI/292.

- Dufresne [1989] Daniel Dufresne. Weak convergence of random growth processes with applications to insurance. Insurance Math. Econom., 8(3):187–201, 1989. ISSN 0167-6687. doi: 10.1016/0167-6687(89)90056-5. URL http://dx.doi.org/10.1016/0167-6687(89)90056-5.

- Dufresne [1990] Daniel Dufresne. The distribution of a perpetuity, with applications to risk theory and pension funding. Scand. Actuar. J., (1-2):39–79, 1990. ISSN 0346-1238. doi: 10.1080/03461238.1990.10413872. URL http://dx.doi.org/10.1080/03461238.1990.10413872.

- Glasserman and Staum [2001] Paul Glasserman and Jeremy Staum. Conditioning on one-step survival for barrier option simulations. Operations Research, 49:2001, 2001.

- Hagan et al. [2002] Patrick S. Hagan, Deep Kumar, Andrew S. Lesniewski, and Diana E. Woodward. Managing smile risk. Wilmott Magazine, pages 84–108, July 2002.

- Hagan et al. [2005] Patrick S. Hagan, Andrew S. Lesniewski, and Diana E. Woodward. Probability distribution in the SABR model of stochastic volatility. Available at http://www.lesniewski.us/papers/working/ProbDistrForSABR.pdf, 2005.

- Henry-Labordère [2009] Pierre Henry-Labordère. Analysis, geometry, and modeling in finance. Chapman & Hall/CRC Financial Mathematics Series. CRC Press, Boca Raton, FL, 2009. ISBN 978-1-4200-8699-7. Advanced methods in option pricing.

- Islah [2009] Othmane Islah. Solving SABR in exact form and unifying it with LIBOR market model. Available at http://ssrn.com/abstract=1489428, October 2009.

- Islah [2011] Othmane Islah. Heun solutions to the SABR model. Available at http://ssrn.com/abstract=1742942, January 2011.

- Linetsky [2004] Vadim Linetsky. Spectral expansions for Asian (average price) options. Oper. Res., 52(6):856–867, 2004. ISSN 0030-364X. doi: 10.1287/opre.1040.0113. URL http://dx.doi.org/10.1287/opre.1040.0113.

- Obłój [2008] Jan Obłój. Fine-tune your smile: Corretion to Hagan et al. Wilmott Magazine, May 2008.

- Paulot [2009] Louis Paulot. Asymptotic implied volatility at the second order with application to the SABR model. Available at http://ssrn.com/abstract=1413649, June 2009.

- Yor [1992] Marc Yor. On some exponential functionals of Brownian motion. Adv. in Appl. Probab., 24(3):509–531, 1992. ISSN 0001-8678. doi: 10.2307/1427477. URL http://dx.doi.org/10.2307/1427477.

Disclaimer

The information herein has been prepared solely for informational purposes and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security or instrument or to participate in any trading strategy. Any such offer would be made only after a prospective participant had completed its own independent investigation of the securities, instruments or transactions and received all information it required to make its own investment decision, including, where applicable, a review of any offering circular or memorandum describing such security or instrument, which would contain material information not contained herein and to which prospective participants are referred. No representation or warranty can be given with respect to the accuracy or completeness of the information herein, or that any future offer of securities, instruments or transactions will conform to the terms hereof. Morgan Stanley and its affiliates disclaim any and all liability relating to this information. Morgan Stanley, its affiliates and others associated with it may have positions in, and may effect transactions in, securities and instruments of issuers mentioned herein and may also perform or seek to perform investment banking services for the issuers of such securities and instruments.

The information herein may contain general, summary discussions of certain tax, regulatory, accounting and/or legal issues relevant to the proposed transaction. Any such discussion is necessarily generic and may not be applicable to, or complete for, any particular recipient’s specific facts and circumstances. Morgan Stanley is not offering and does not purport to offer tax, regulatory, accounting or legal advice and this information should not be relied upon as such. Prior to entering into any proposed transaction, recipients should determine, in consultation with their own legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences, of the transaction.

Notwithstanding any other express or implied agreement, arrangement, or understanding to the contrary, Morgan Stanley and each recipient hereof are deemed to agree that both Morgan Stanley and such recipient (and their respective employees, representatives, and other agents) may disclose to any and all persons, without limitation of any kind, the U.S. federal income tax treatment of the securities, instruments or transactions described herein and any fact relating to the structure of the securities, instruments or transactions that may be relevant to understanding such tax treatment, and all materials of any kind (including opinions or other tax analyses) that are provided to such person relating to such tax treatment and tax structure, except to the extent confidentiality is reasonably necessary to comply with securities laws (including, where applicable, confidentiality regarding the identity of an issuer of securities or its affiliates, agents and advisors).

The projections or other estimates in these materials (if any), including estimates of returns or performance, are forward-looking statements based upon certain assumptions and are preliminary in nature. Any assumptions used in any such projection or estimate that were provided by a recipient are noted herein. Actual results are difficult to predict and may depend upon events outside the issuer’s or Morgan Stanley’s control. Actual events may differ from those assumed and changes to any assumptions may have a material impact on any projections or estimates. Other events not taken into account may occur and may significantly affect the analysis. Certain assumptions may have been made for modeling purposes only to simplify the presentation and/or calculation of any projections or estimates, and Morgan Stanley does not represent that any such assumptions will reflect actual future events. Accordingly, there can be no assurance that estimated returns or projections will be realized or that actual returns or performance results will not be materially different than those estimated herein. Any such estimated returns and projections should be viewed as hypothetical. Recipients should conduct their own analysis, using such assumptions as they deem appropriate, and should fully consider other available information in making a decision regarding these securities, instruments or transactions. Past performance is not necessarily indicative of future results. Price and availability are subject to change without notice. The offer or sale of securities, instruments or transactions may be restricted by law. Additionally, transfers of any such securities, instruments or transactions may be limited by law or the terms thereof. Unless specifically noted herein, neither Morgan Stanley nor any issuer of securities or instruments has taken or will take any action in any jurisdiction that would permit a public offering of securities or instruments, or possession or distribution of any offering material in relation thereto, in any country or jurisdiction where action for such purpose is required. Recipients are required to inform themselves of and comply with any legal or contractual restrictions on their purchase, holding, sale, exercise of rights or performance of obligations under any transaction. Morgan Stanley does not undertake or have any responsibility to notify you of any changes to the attached information.

With respect to any recipient in the U.K., the information herein has been issued by Morgan Stanley & Co. International Limited, regulated by the U.K. Financial Services Authority. THIS COMMUNICATION IS DIRECTED IN THE UK TO THOSE PERSONS WHO ARE MARKET COUNTERPARTIES OR INTERMEDIATE CUSTOMERS (AS DEFINED IN THE UK FINANCIAL SERVICES AUTHORITY’S RULES).

ADDITIONAL INFORMATION IS AVAILABLE UPON REQUEST.