Nonlinear Time Series Modeling:

A

Unified Perspective, Algorithm, and Application

Subhadeep Mukhopadhyay

Department of Statistical Science, Temple University

Emanuel Parzen

Department of Statistics, Texas A&M University

Abstract

A new comprehensive approach to nonlinear time series analysis and modeling is developed in the present paper. We introduce novel data-specific mid-distribution based Legendre Polynomial (LP) like nonlinear transformations of the original time series that enables us to adapt all the existing stationary linear Gaussian time series modeling strategy and made it applicable for non-Gaussian and nonlinear processes in a robust fashion. The emphasis of the present paper is on empirical time series modeling via the algorithm LPTime. We demonstrate the effectiveness of our theoretical framework using daily S&P 500 return data between Jan/2/1963 - Dec/31/2009. Our proposed LPTime algorithm systematically discovers all the ‘stylized facts’ of the financial time series automatically all at once, which were previously noted by many researchers one at a time.

Keywords and phrases: Nonparametric time series modeling, Nonlinearity, Unified time series algorithm, Exploratory diagnostics.

1 Introduction

When one observes a sample , of a (discrete parameter) time series , one seeks to nonparametrically learn from the data a stochastic model with two purposes: (a1) scientific understanding; (a2) forecasting (predict future values of the time series under the assumption that the future obeys the same laws as the past). Our prime focus in this paper is on developing a nonparametric empirical modeling technique for nonlinear (stationary) time series that can be used by data scientists as a practical tool for obtaining insights into (i) the temporal dynamic patterns and (ii) the internal data generating mechanism–a crucial step for achieving (a1) and (a2).

Under the assumption that the time series is stationary (which can be extended to asymptotically stationary) the distribution of is identical for all , the joint distribution of and depends only on lag . Typical estimation goals are as follows:

(1) Marginal modeling. The identification of marginal probability law (in particular, the heavy tailed marginal densities) of a time series plays a vital role in financial econometrics. Notations: Common quantile , inverse of distribution function , respectively denoted and . Mid-distribution is defined as . (2) Correlation modeling. Covariance function (defined for positive and negative lag ) . , assumed in our prediction theory. Correlation function . (3) Frequency-domain modeling. When covariance is absolutely summable, define spectral density function . (4) Time-domain modeling. Time domain model is linear filter relating to white noise , independent random variables. Autoregressive scheme of order , a predominant linear time series technique for modeling conditional mean is defined as (assuming )

| (1.1) |

with the spectral density function given by

| (1.2) |

To fit an AR model, compute linear predictor of given by

| (1.3) |

Verify that the prediction error are white noise. Best fitting AR order is identified by Akaike criterion AIC (or Schwarz’s criterion BIC) as value of minimizes

In what follows we aim to develop a parallel modeling framework for non-linear time series.

2 From Linear to Nonlinear Modeling

Our approach to nonlinear modeling, called LPTime, is via approximate calculation of conditional expectation . Because with probability one , one can prove that the conditional expectation of given past values is equal to (with probability one) conditional expectation of given past values , which can be approximated by linear orthogonal series expansion in score functions constructed by Gram Schmidt orthonormalization of powers of

| (2.1) |

where si the standard deviation of the mid-distribution transform random variable given by , denotes the probability mass function of . This score polynomials allows us to simultaneously tackle the discrete (say count-valued) and continuous time series. Note that for is continuous, The reduces to:

| (2.2) |

and all the higher-order polynomials can be compactly expressed as , where denotes orthonormal Legendre polynomials. It is worthwhile to note that are orthonormal polynomials of mid-ranks (instead of polynomials of the original ’s), which injects robustness into our analysis while allowing to capture nonlinear patterns. Having constructed score functions of denoted by , we transform into unit interval by letting and defining

| (2.3) |

In general our score functions are custom constructed for each distribution function which can be discrete or continuous.

3 Nonparametric LPTime Analysis

Our LPTime empirical time series modeling strategy to nonlinear modeling of a univariate time series is based on linear modeling of the multivariate time series:

| (3.1) |

where , our tailor-made orthonormal mid-rank based nonlinear transformed series. We summarize below the main steps of the algorithm LPTime. To better understand the functionality and applicability of LPTime we break it into several inter-connected steps each of which highlights:

- (a)

-

Algorithmic modeling aspect [how it works]

- (b)

-

Required theoretical ideas and notions [why it works]

- (c)

-

Application to daily S&P 500 return data between Jan/2/1963 - Dec/31/2009 [empirical proof-of-work].

3.1 The Data and LP-Transformation

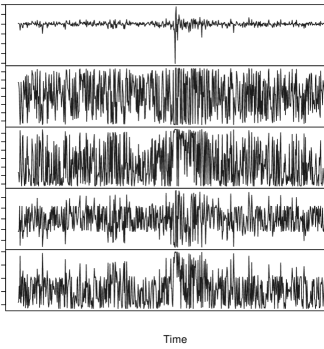

The data used in this paper is daily S&P 500 return data between Jan/2/1963 - Dec/31/2009 (defined as where is the closing price on trading day ). We begin our modeling process by transforming the given univariate time series into multiple (robust) time series by means of a special data-analytic construction rules described in (2.1)-(2.3) and (3.1). We display the original “normalized” time series and the transformed time series on a single plot.

Fig 1 shows the first look at the transformed S&P 500 return data between Oct 1986 and Oct 1988. These newly constructed time series works as a universal preprocessor for any time series modeling in contrast with other adhoc power transformations. In the next sections we will describe how the temporal patterns of these multivariate LP-transformed series generate various insights for the time series in a organized fashion.

3.2 Marginal Modeling

Our time series modeling starts with the identification of probability distributions.

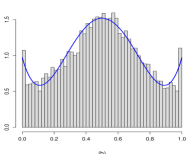

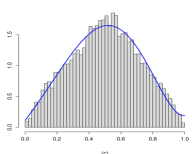

3.2.1 Non-normality Diagnosis

Does the Normal probability distribution provide a good fit to the S&P 500 return data? Fig 2(a) clearly indicates distribution of daily return is certainly non-normal. At this point the natural question is how the distribution is different from the assumed normal? A quick insight into this question can be gained by looking at the distribution of the random variable , called comparison density (Parzen, 1997, Mukhopadhyay, 2017) given by:

| (3.2) |

where is the quantile function. The flat uniform shape of the estimated comparison density provides a quick graphical diagnostic to test the fit of the parametric to the true unknown distribution . The Legendre polynomial based orthogonal series comparison density estimator is given by

| (3.3) |

where the Fourier coefficients .

For , Fig 2(b) displays the histogram of for . The corresponding comparison density estimate is shown in blue curve, which reflects the fact that distribution of daily return has (i) sharp peaked (inverted “U” shape), (ii) negatively skewed with (iii) fatter tails than the Gaussian distribution. We can carry our similar analysis by asking whether t-distribution with degrees of freedom provides a better fit. Fig 2(c) demonstrates the full analysis, where the estimated comparison density indicates (iv) t-distribution fits the data better than normal, specially in the tails, although not a fully adequate model. The shape of comparison density (along with the histogram of , ) captures and exposes the adequacy of the assumed model for the true unknown –thus act as an exploratory as well as confirmatory tool.

3.3 Copula Dependence Modeling

Distinguishing uncorrelatedness and independence by properly quantifying association is an essential task in empirical nonlinear time series modeling.

3.3.1 Nonparametric Serial Copula

We display the nonparametrically estimated smooth serial copula density to get much finer understanding of the lagged interdependence structure of a stationary time series. For continuous distribution define the copula density for the pair as the joint density of and , which is estimated by sample mid-distribution transform , . Following Mukhopadhyay and Parzen (2014) and Parzen and Mukhopadhyay (2012), we expand copula density (square integrable) in a orthogonal series of product LP-basis functions as

| (3.4) |

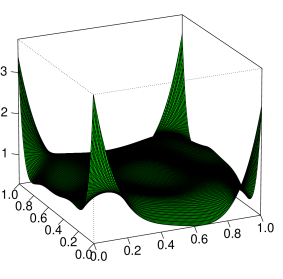

where . The Eq 3.4 allows us to pictorially represent the information present in the LP-comoment matrix via copula density. The various “shapes” of copula density gives insight into the structure and dynamics of the time series.

Now we apply this nonparametric copula estimation theory to model the temporal dependence structure of S&P return data. The copula density estimate based on the smooth LP comoments is displayed in Fig 3. The shape of the copula density shows strong evidence of asymmetric tail-dependence. Note that the dependence is only present in the extreme quantiles - another well-known stylized fact of economic and financial time series.

3.3.2 LP-Comomemnt of lag

Here we will introduce the concept of LP-comoment to get a complete understanding of the nature of serial dependence present in the data. LP-comoment of lag is defined as the joint covariance of and .

The lag 1 LP-comoment matrix for S&P 500 return data is displayed below,

| (3.5) |

To identify the significant elements we first rank order the squared LP comoments. Then we take the penalized cumulative sum of comoments using BIC criterion , is sample size and choose the for which BIC is maximum. The complete BIC path for S&P 500 data is shown in figure 3, which selects top six comments also denoted by in the LP-comoment matrix display (Eq. 3.5). By making all those uninteresting “small” comoments equal to zero we get the “smooth” LP Comoment matrix denoted by . The linear auto-correlation is capture by the term. The presence of higher order significant terms in the LP comoment matrix indicate the possible nonlinearity. Another interesting point to note that , where as the auto-correlation between the mid-rank transformed data , considerably larger and picked by BIC criterion. This is an interesting fact as it indicates rank-transform time series () is much more predictable than the original raw time series .

3.3.3 LP-Correlogram, Evidence and Source of Nonlinearity

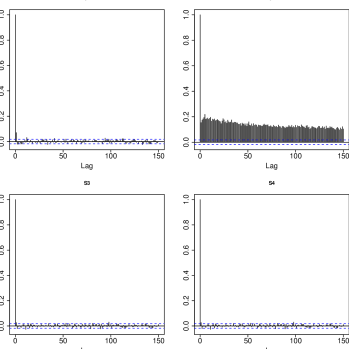

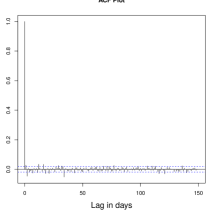

We provide nonparametric exploratory test for (non)linearity (spectral domain test is given in Sec 3.6). Plot the correlogram of : (a) diagnose possible nonlinearity, and (b) identify possible sources. This constitutes the important building block for methods of model identification. LP-correlogram generalizes the classical sample autocorrelation function (ACF). Applying the acf() R function on generates the graphical display of our proposed LP-correlogram plot.

Fig 4 shows the LP-correlogram of S&P stock return data. Panel A shows the absence of linear autocorrelation which is known as a efficient market hypothesis in finance literature. A prominent auto-correlation pattern for the series (panel B Fig 4) is the source of nonlinearity. This fact is known as “volatility clustering”, which says that large price fluctuation is more likely to be followed by large price fluctuations. Also the slow decay of the autocorrelation of the series can be interpreted as an indication of long-memory volatility structure.

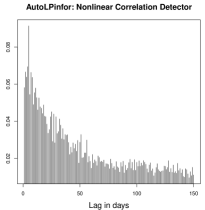

3.3.4 AutoLPinfor: Nonlinear Correlation Measure

We display the sample AutoLPinfor plot - diagnostic tool for nonlinear autocorrelation. We define the lag AutoLPinfor as the squared Frobenius norm of the smooth-LP comoment matrix of lag ,

| (3.6) |

where sum is over BIC selected for which LP comoments are significantly non-zero.

Our robust nonparametric measure can be viewed as capturing the deviation of copula density from uniformity:

| (3.7) |

which is closely related to the entropy measure of association proposed in Granger and Lin (1994)

| (3.8) |

It can be showed using Taylor series expansion that asymptotically

| (3.9) |

An excellent discussion on the role of information theory methods for unified time series analysis is given in Parzen (1992) and Brillinger (2004). For an extensive survey of tests of independence for nonlinear processes see Chapter 7.7 of Terasvirta et al. (2010). AutoLPinfor is a new information theoretic nonlinear autocorrelation measure which detects generic association and serial dependence present in a time-series. Contrast the AutoLPinfor plot for S&P 500 return data shown in Fig 5 with the acf plot (left panel). This underlies the need for building a nonlinear time series model, which we will be discussing next.

3.3.5 Nonparametric Estimation of Blomqvist’s Beta

Estimate the Blomqvist’s (also known as medial correlation coefficient) of lag by using the LP-copula estimate in the following equation,

| (3.10) |

The values and interpreted as reverse correlation, independence and perfect correlation, respectively. Note that,

| AutoLPinfor |

For S&P 500 return data we compute the following dependence numbers,

3.3.6 Nonstationarity Diagnosis, LP-Comoment Approach

Viewing the time index as covariate we propose a nonstationarity diagnosis based on LP-comoments of and the time index variable . Our treatment has the ability to detect time varying nature of mean, variance, skewness and so on represented by various custom-made LP-transformed time series.

For S&P data we computed the following LP comoment matrix to investigate the nonstationarity:

| (3.11) |

This indicates presence of slight non-stationarity behavior of variance or volatility () and kurtosis of tail-thickness(). Similar to AutoLPinfor we propose the following statistic for detecting nonstationarity

| (3.12) |

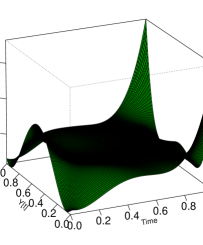

We can also generate the corresponding smooth copula density of based on smooth matrix to visualize the time varying information as in Fig 6.

3.4 Local Dependence Modeling

3.4.1 Quantile Correlation Plot and Test for Asymmetry

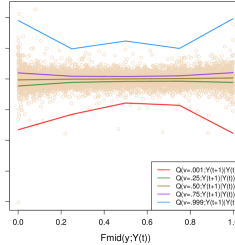

Display the quantile correlation plot, a copula distribution based graphical diagnostic to visually examine the asymmetry of dependence. The goal is to get more insight into the nature of tail-correlation.

Motivated by the concept of lower and upper tail-dependence coefficient we define the Quantile Correlation Function (QCF) as the following in terms of copula distribution function of denoted by ,

| (3.13) |

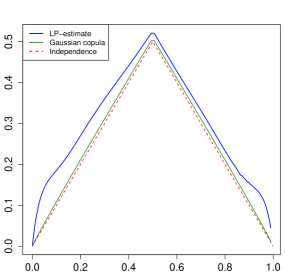

Our nonparametric estimate of quantile correlation function is based on the LP-copula density which we denote as . Fig 7 shows the corresponding quantile correlation plot for S&P 500 data. The dotted-line represent QCF under Independence assumption. Deviation from this line helps us to better understand the nature of asymmetry. We compute using the fitted Gaussian copula

| (3.14) |

where is sample covariance matrix. The dark-green line in Fig 7 shows the corresponding curve which is almost identical with the “no dependence” curve, albeit misleading. The reason is Gaussian copula is characterized by linear correlation, while S&P data is highly nonlinear in nature. As the linear auto-correlation of stock return is almost zero, we have approximately . Similar to Gaussian copula there are several others parametric copula families, which can give similar misleading conclusions. This simple illustration reminds us the pernicious effect of not “looking into the data”.

3.4.2 Conditional LPinfor Dependence Measure

For more transparent and clear insights into the asymmetric nature of the tail dependence we need to introduce the concept of conditional dependence. In what follows we propose a conditional LPinfor function - quantile based diagnostic for tracking how the dependence of on changing at various quantiles.

To quantify the conditional dependence, we seek to estimate . A brute force approach estimates separately the conditional distribution and the unconditional distribution and take the ratio to estimate this arbitrary function. An alternative elegant way is to recognize that by “going to quantile domain” (i.e., and ) we can interpret the ratio as “slices” of copula density, which we call conditional comparison density:

| (3.15) |

where the LP-Fourier orthogonal coefficients are given by

Define conditional LPinfor as

| (3.16) |

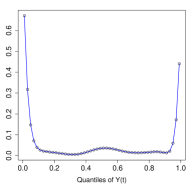

We use this theory to investigate the conditional dependency structure of S&P 500 return data. Fig 8(a) traces out the complete path of the estimated function, which indicates the high asymmetric tail-correlation. This conditional correlation curves can be viewed as “local” dependence measure. An excellent discussion on this topic is given in Section 3.3.8 of Terasvirta, Tjostheim, and Granger (2010).

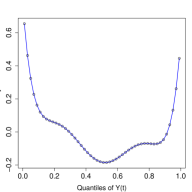

At this point we can legitimately ask what aspects of the conditional distributions are changing most? Fig 8 (b,c) display only the two coefficients and for the S&P 500 return data for the pairs . These two coefficients represent how the mean and the volatility levels of the conditional density changing with respect to the unconditional reference distribution. The typical asymmetric shape of conditional volatility shown in right panel of Fig 8 (b,c) indicates what is known as the “leverage effect” - future stock volatility negatively correlated with past stock return, i.e. stock volatility tends to increase when stock prices drop.

3.5 Non-Crossing Conditional Quantile Modeling

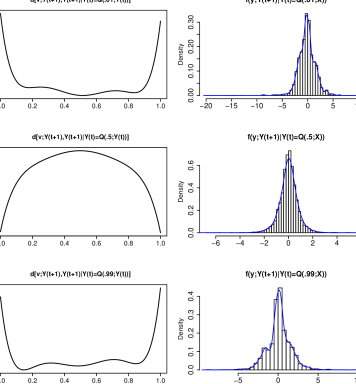

Display the nonparametrically estimated conditional quantile curves of given . Our new modeling approach uses the estimated conditional comparison density to simulate from by utilizing the given sample via accept-reject rule to arrive at the “smooth” nonparametric model for . See Parzen and Mukhopadhyay (2013b) for details about the method. Our proposed algorithm generates “large” additional simulated samples from the conditional distribution, which allows us to accurately estimate the conditional quantiles (especially the extreme quantiles). By construction, our method guaranteed to produce non-crossing quantile curves - thus tackles a challenging practical problem.

For S&P 500 data we first nonparametrically estimate the conditional comparison densities shown in Left panel of Fig 9 for and , which can be thought of as a “weighting function” for unconditional marginal distribution to produce the conditional distributions:

| (3.17) |

This density estimation technique belongs to the skew-G modeling class (Mukhopadhyay, 2016). We simulate samples from the by accept-reject sampling from , . The histograms and the smooth conditional densities are shown in the right panel of Fig 9. It shows some typical shapes in terms of long-tailedness.

Next we proceed to estimate the nonparametric conditional quantiles , for from the simulated data. Fig 10 shows the estimated conditional quantiles. The extreme conditional quantiles have a special significance in the context of financial time series. They sometimes popularly known as Conditional Value at Risk (CoVaR) - currently the most popular quantitative risk management tool (see Adrian and Brunnermeier (2011), Engle and Manganelli (2004)). The red solid line in Fig 10 is the , which is known as .1% CoVar function for one-day holding period for S&P 500 daily return data. Although the upper conditional quantile curve (blue solid line) show symmetric behaviour around , the lower quantile has a prominent asymmetric shape. These conditional quantiles give ultimate description of the auto-regressive dependence of S&P 500 return movement in the tail-region.

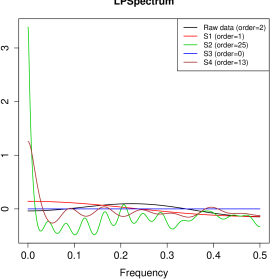

3.6 Nonlinear Spectrum Analysis

Here we extends the concept of spectral density for nonlinear processes. Display the LPSpectrum - autoregressive (AR) spectral density estimates of . Spectral density for each LP-transformed series is defined as

| (3.18) | |||||

We separately fit the univariate AR model for the components of and use BIC order selection criterion to select the “best” parsimonious parametrization using Burg method.

Finally we use the estimated model coefficients to produce the “smooth” estimate of spectral density function (see Eq. 1.2). The copula spectral density is defined as

| (3.19) |

To estimate the copula spectral density we use the LP comoment based nonparametric copula density estimate. Note that both the serial copula (3.12) and the corresponding spectral density (3.25) captures the same amount of information for serial dependence of . For that reason, we recommend to compute AutoLPinfor as a general dependence measure for non-gaussian nonlinear processes.

Application of our LPSpectral tool on S&P 500 return data is shown in Fig 11. Few interesting observations: (i) the conventional spectral density (black solid line) provides no insight into the (complex) serial dependency present in the data. (ii) The nonlinearity in the series is captured by the interesting shapes of our specially-designed times series and , which classical (linear) correlogram based spectra can not account for. (iii) The shape of the spectra of and the rank-transformed time series looks very similar. and a (iv) pronounced singularity near zero of the spectrum of hints some kind of “long memory” behavior. This phenomena also known as regular variation representation at frequency (Granger and Joyeux, 1980).

A quick diagnostic measure for screening significant spectrums can be computed via the information number . The LPSpectrum methodology is highly robust and thus can tackle the heavy-tailed S&P data quite successfully.

3.7 Nonparametric Model Specification

The ultimate goal of empirical time series analysis is nonparametric model identification. To model the univariate stationary nonlinear process we specify multiple autoregressive model based on of the form

| (3.20) |

where is multivariate mean zero Gaussian white noise with covariance . These system of equation jointly describe the dynamics of the nonlinear process and how it evolves over time. We use BIC criterion to select the model order which selects the model order which minimizes

| (3.21) |

We carry out this steps for our S&P 500 return data. We estimate our multiple AR model based on . We discard due to it’s flat spectrum (see Fig 11). BIC selects “best” order . Although, the complete description of the estimated model is clearly cumbersome, we provide below the approximate structure by selecting few large coefficients from the actual matrix equation. The goal is to interpret the coefficients (statistical parameters) of the estimated model and relate it with economic theory (scientific parameters/theory). This multiple AR LP-model (in short we call LPVAR) is given by

| (3.22) |

and the residual covariance matrix is

The autoregressive model of can be considered as a robust stock return volatility model - LPVolatility Modeling, which is less affected by unusually large extreme events. The model for automatically discover many known facts: (a) the sign of the coefficient linking volatility and return is negative -confirming “leverage effect”; (b) is positively autocorrelated, known as volatility clustering; (c) The positive interaction with lagged accounts for the “excess kurtosis”.

4 Conclusion

This article provides a pragmatic and comprehensive framework for nonlinear time series modeling that is easier to use, more versatile and has a strong theoretical foundation based on recently developed theory on unified algorithms of data science via LP modeling (Parzen and Mukhopadhyay, 2012, 2013a, 2013b, Mukhopadhyay and Parzen, 2014, Mukhopadhyay, 2016, 2017). Summary and broader implications of the proposed research: From the theoretical standpoint, the unique aspect of our proposal lies in its ability to simultaneously embrace and employ spectral domain, time domain, quantile domain, and the information domain analysis for enhanced insights, which to the best of our knowledge has not appeared in the nonlinear time series literature before.

From a practical angle, the novelty of our technique is that it permits us to use the techniques from linear Gaussian time series to create non-Gaussian nonlinear time series models with highly interpretable parameters. This aspect makes LPTime computationally extremely attractive for the data scientists as they can now borrow all the standard time series analysis machinery from R libraries for implementation purpose.

From the pedagogical side, we believe that these concepts and methods can easily be augmented with the standard time series analysis course to modernize the current curriculum so that students can handle complex time series modeling problems (McNeil et al., 2010) using the tools they are already familiar with.

The main thrust of this article is to describe and interpret the steps of LPTime technology to create a realistic general-purpose algorithm for empirical time series modeling. In addition, many new theoretical results and diagnostic measures are presented which laid the foundation for the algorithmic implementation of LPTime. We showed how LPTime can systematically explore the data to discover empirical facts hidden in time series. For example, LPTime empirical modeling of S&P 500 return data reproduces the ‘stylized facts’: (a) heavy tails; (b) non-Gaussian;(c) nonlinear serial dependence; (d) tail-correlation; (e) asymmetric dependence; (f) volatility clustering; (g) long-memory volatility structure; (h) efficient market hypothesis; (i) leverage effect; (j) excess kurtosis, in a coherent manner under single general unified framework. We have emphasized how the statistical parameters of our model can be interpreted in the light of established economic theory. We have recently applied this theory for large-scale eye-movement pattern discovery problem, which came out as the winner (among 82 competing algorithms) of the 2014 IEEE International Biometric Eye Movements Verification and Identification Competition (Mukhopadhyay and Nandi, 2017).

We conclude with some general references. Few popular articles Granger (2003, 1993), Granger and Lin (1994), Engle (1982), Parzen (1979, 1967), Tukey (1980), Brillinger (1977, 2004), Salmon (2012); Books Terasvirta et al. (2010), Woodward et al. (2011), Tsay (2010); and Review articles Granger (1998), Hendry (2011). The proposed algorithm is implemented in the R package LPTime, which is available on CRAN.

References

- Adrian and Brunnermeier (2011) Adrian, T. and M. K. Brunnermeier (2011). Covar. Technical report, National Bureau of Economic Research.

- Brillinger (1977) Brillinger, D. R. (1977). The identification of a particular nonlinear time series system. Biometrika, 509–515.

- Brillinger (2004) Brillinger, D. R. (2004). Some data analyses using mutual information. Brazilian Journal of Probability and Statistics 18(6), 163–183.

- Engle (1982) Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation. Econometrica: Journal of the Econometric Society, 987–1007.

- Engle and Manganelli (2004) Engle, R. F. and S. Manganelli (2004). Caviar: Conditional autoregressive value at risk by regression quantiles. Journal of Business & Economic Statistics 22(4), 367–381.

- Granger and Lin (1994) Granger, C. and J.-L. Lin (1994). Using the mutual information coefficient to identify lags in nonlinear models. Journal of time series analysis 15(4), 371–384.

- Granger (1993) Granger, C. W. (1993). Strategies for modelling nonlinear time-series relationships. Economic Record 69(3), 233–238.

- Granger (1998) Granger, C. W. (1998). Overview of nonlinear time series specification in economics. NSF Symposium on Nonlinear Time Series Models, University of California, Berkeley.

- Granger (2003) Granger, C. W. (2003). Time series concepts for conditional distributions. Oxford Bulletin of Economics and Statistics 65(s1), 689–701.

- Granger and Joyeux (1980) Granger, C. W. and R. Joyeux (1980). An introduction to long-memory time series models and fractional differencing. Journal of time series analysis 1(1), 15–29.

- Hendry (2011) Hendry, D. F. (2011). Empirical economic model discovery and theory evaluation. Rationality, Markets and Morals 2, 115–145.

- McNeil et al. (2010) McNeil, A. J., R. Frey, and P. Embrechts (2010). Quantitative risk management: concepts, techniques, and tools. Princeton university press.

- Mukhopadhyay (2016) Mukhopadhyay, S. (2016). Large scale signal detection: A unifying view. Biometrics 72(2), 325–334.

- Mukhopadhyay (2017) Mukhopadhyay, S. (2017). Large-scale mode identification and data-driven sciences. Electronic Journal of Statistics 11(1), 215–240.

- Mukhopadhyay and Nandi (2017) Mukhopadhyay, S. and S. Nandi (2017). LPiTrack: Eye movement pattern recognition algorithm and application to biometric identification. Machine Learning, doi 10.1007/s10994-017-5649-1.

- Mukhopadhyay and Parzen (2014) Mukhopadhyay, S. and E. Parzen (2014). LP approach to statistical modeling. Preprint arXiv:1405.2601.

- Parzen (1967) Parzen, E. (1967). On empirical multiple time series analysis. In Proc. Fifth Berkeley Symp. Math. Statist. Prob, Volume 1, pp. 305–340.

- Parzen (1979) Parzen, E. (1979). Nonparametric statistical data modeling (with discussion). Journal of the American Statistical Association 74, 105–131.

- Parzen (1992) Parzen, E. (1992). Time series, statistics, and information. New Directions in Time Series Analysis (ed. E. Parzen et al). Springer Verlag: New York., 265–286.

- Parzen (1997) Parzen, E. (1997). Comparison distributions and quantile limit theorems. International Conference on Asymptotic Methods in Probability and Statistics (Carleton University, Canada, 8-13 July 1997).

- Parzen and Mukhopadhyay (2012) Parzen, E. and S. Mukhopadhyay (2012). Modeling, Dependence, Classification, United Statistical Science, Many Cultures. arXiv:1204.4699.

- Parzen and Mukhopadhyay (2013a) Parzen, E. and S. Mukhopadhyay (2013a). United Statistical Algorithms, LP comoment, Copula Density, Nonparametric Modeling. 59th ISI World Statistics Congress (WSC), Hong Kong.

- Parzen and Mukhopadhyay (2013b) Parzen, E. and S. Mukhopadhyay (2013b). United Statistical Algorithms, Small and Big Data, Future of Statisticians. arXiv:1308.0641.

- Salmon (2012) Salmon, F. (2012). The formula that killed wall street. Significance 9(1), 16–20.

- Terasvirta et al. (2010) Terasvirta, T., D. Tjostheim, and C. W. Granger (2010). Modelling nonlinear economic time series. OUP Catalogue.

- Tsay (2010) Tsay, R. S. (2010). Analysis of financial time series. Wiley.

- Tukey (1980) Tukey, J. (1980). Can we predict where “time series” should go next. Directions in Times Series, IMS, Hayward, Calif, 1–31.

- Woodward et al. (2011) Woodward, W. A., H. L. Gray, and A. C. Elliott (2011). Applied time series analysis. CRC press.