Forecasting Intermittent Demand by Hyperbolic-Exponential Smoothing

Abstract

Croston’s method is generally viewed as superior to exponential smoothing when demand is intermittent, but it has the drawbacks of bias and an inability to deal with obsolescence, in which an item’s demand ceases altogether. Several variants have been reported, some of which are unbiased on certain types of demand, but only one recent variant addresses the problem of obsolescence. We describe a new hybrid of Croston’s method and Bayesian inference called Hyperbolic-Exponential Smoothing, which is unbiased on non-intermittent and stochastic intermittent demand, decays hyperbolically when obsolescence occurs and performs well in experiments.

1 Introduction

Inventory management is of great economic importance to industry, but forecasting demand for spare parts is difficult because it is intermittent: in many time periods the demand is zero. Various methods have been proposed for forecasting, some simple and others statistically sophisticated, but relatively little work has been done on intermittent demand.

We now list the methods most relevant to this paper. Single exponential smoothing (SES) generates estimates of the demand by exponentially weighting previous observations via the formula

where is a smoothing parameter. The smaller the value of the less weight is attached to the most recent observations. An up-to-date survey of exponential smoothing algorithms is given in [7]. They perform remarkably well, often beating more complex approaches [6], but SES is known to perform poorly (under some measures of accuracy) on intermittent demand.

A well-known method for handling intermittency is Croston’s method [4] which applies SES to the demand sizes and intervals independently. Given smoothed demand and smoothed interval at time , the forecast is

Both and are updated at each time for which . According to [7] it is hard to conclude from the various studies that Croston’s method is successful, because the results depend on the data used and on how forecast errors are measured. But it is generally regarded as one of the best methods for intermittent series [8], and versions of the method are used in leading statistical forecasting software packages such as SAP and Forecast Pro [21].

To remove at least some of the known bias of Croston’s method on stochastic intermittent demand (in which demands occur randomly), a correction factor is introduced by Syntetos & Boylan [17]:

where is the smoothing factor used for inter-demand intervals, which may be different to the smoothing factor used for demands.111In [17] this factor is denoted by because it is used to smooth both and . This works well for intermittent demand but is incorrect for non-intermittent demand. This problem is cured by Syntetos [16] who uses a forecast

This reduces bias on non-intermittent demand, but slightly increases forecast variance [20].

Another modified Croston method is given by Levén & Segerstedt [13], who claim that it also removes the bias in the original method but in a simpler way: they apply SES to the ratio of demand size and interval length each time a nonzero demand occurs. That is, they update the forecast using

However, this also turns out to be biased [2].

A more recent development is the TSB (Teunter-Syntetos-Babai) algorithm [21], which updates the demand probability instead of the demand interval. This allows it to solve the problem of obsolescence which was not previously dealt with in the literature. An item is considered obsolete if it has seen no demand for a long time. When many thousands of items are being handled automatically, this may go unnoticed by Croston’s method and its variants. One of the authors of this paper (Prestwich) has worked with an inventory company who used Croston’s method, but were forced to resort to ad hoc rules such as: if an item has seen no demand for 2 years then forecast 0. TSB is designed to overcome this problem. Instead of a smoothed interval it uses exponential smoothing to estimate a probability where is 1 when demand occurs at time and 0 otherwise. Different smoothing factors and are used for and respectively. is updated every period, while is only updated when demand occurs. The forecast is

In this paper we shall use CR to denote the original method of Croston, SBA the variant of Syntetos & Boylan, SY that of Syntetos, and TSB that of Teunter, Syntetos & Babai. We explore a new variant of Croston’s method that is unbiased and handles obsolescence. Its novelty is that during long periods of no demand its forecasts decay hyperbolically instead of exponentially (as in TSB), a property that derives from Bayesian inference. The new method is described in Section 2 and evaluated in Section 3, and conclusions are summarised in Section 4. This paper is an extended version of [15].

2 Hyperbolic-exponential smoothing

We take a Croston-style approach, separating demands into demand sizes and the inter-demand interval . As in most Croston methods, when non-zero demand occurs the estimated demand size and inter-demand period are both exponentially smoothed, using factors and respectively. The novelty of our method is what happens when there is no demand.

Suppose that at time , up to and including the last non-zero demand we have smoothed demand size and inter-demand period , and that we have observed consecutive periods without demand since the last non-zero demand. What should be our estimate of the probability that a demand will occur in the next period? A similar question was addressed by Laplace [12]: given that the sun has risen times in the past, what is the probability that it will rise again tomorrow? His solution was to add one to the count of each event (the sun rising or not rising) to avoid zero probabilities, and estimate the probability by counting the adjusted frequencies. So if we have observed sunrises and 0 non-sunrises, in the absence of any other knowledge we would estimate the probability of a non-sunrise tomorrow as . This is known as the rule of succession. But he noted that, given any additional knowledge about sunrises, we should adjust this probability. These ideas are encapsulated in the modern pseudocount method which can be viewed as Bayesian inference with a Beta prior distribution. We base our discussion on a recent book [14] (Chapter 7) that describes the technique we need in the context of Bayesian classifiers.

For the two possibilities and we add non-negative pseudocounts and respectively to the actual counts and of observations.222These pseudocounts are often denoted from the Beta distribution hyperparameters, but we already use these symbols for smoothing factors. As well as addressing the problem of zero observations, pseudocounts allow us to express the relative importance of prior knowledge and new data when computing the posterior distribution. By Bayes’ rule the posterior probability of a nonzero demand occurring is estimated by

(This is actually a conditional probability that depends on the recent observations and prior probabilities, but we follow [14] and write for simplicity.) In our problem we have seen no demand for periods so and :

We can eliminate one of the pseudocounts by noting that the prior probability of a demand found by exponential smoothing is , and that the pseudocounts must reflect this:

hence and

As with TSB, to obtain a forecast we multiply this probability by the smoothed demand size:

We can also eliminate by choosing a value that gives an unbiased forecaster on stochastic intermittent demand, as follows. Consider the demand sequence as a sequence of substrings, each starting with a nonzero demand: for example the sequence has substrings , and . Within a substring and remain constant so our forecaster has expected forecast

The derivation used the linearity of expectation, the constancy of and , the fact that , and the approximation for small which can be found by taking the first two terms of geometric series . Choosing , and therefore , we obtain a forecast

with expected value

which is identical to the actual SBA forecast. So on any substring our forecaster has the same expected forecast as SBA, given the same values of and . Moreover, it updates and in exactly the same way as SBA at the start of each substring, therefore it has the same expected forecast as SBA over the entire demand sequence. Thus by [17] it is unbiased on stochastic intermittent demand.

A drawback with this forecaster is that, like SBA, it is biased on non-intermittent demand. This can be overcome by a slight adjustment to the forecast:

Following a similar derivation of the expected forecast:

The final expression is exactly the forecast made by the SY method throughout the substring. But SY is unbiased on standard stochastic intermittent demand and also on non-intermittent demand [16], so (using the same arguments as above) our forecaster is too. This is the forecaster we shall use, and we call it Hyperbolic-Exponential Smoothing (HES) because of its combination of exponential smoothing with hyperbolic decay.

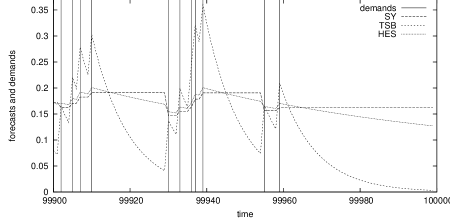

An illustration of the different behaviour of SY, TSB and HES is shown in Figure 1. Demand is stochastic intermittent with probability 0.25, all nonzero demands (shown as impulses) are 1, and the forecasters use . On stochastic intermittent demand the HES forecasts are similar to those of SY, though there is some decay between demands. TSB also has greater variation, though this difference could be reduced by using smaller smoothing parameters. When demand becomes zero, for example because the item becomes obsolete, SY remains constant, TSB decays exponentially and HES decays hyperbolically.

3 Experiments

We now test HES empirically to evaluate its bias and forecasting accuracy. In all experiments, for CR, SBA and SY we let as is usual with those methods.

3.1 Accuracy measures

In any comparison of forecasting methods we must choose accuracy measures. [9] lists 17 measures, noting that a “bewildering array of accuracy measures have been used to evaluate the performance of forecasting methods”, that no single method is generally preferred, and that some are not well-defined on data with intermittent demand. We shall use measures that have been recently recommended for intermittent demand. To measure bias we use MASE (Mean Absolute Scaled Error), recommended by [10] and defined as where is a scaled error defined by

is the error and are the time periods of the samples used for forecasting, which we take to be the samples used to initialise the smoothed estimates. We take these means over multiple runs. MASE effectively evaluates a forecasting method against the naive (or random walk) forecaster, which simply forecasts that the next demand will be identical to the current demand.

As a measure of deviation we use the MAD/Mean Ratio (MMR), which has been argued to be superior to several other methods used in forecasting competitions [11] and is defined by

Again the summations are taken over multiple runs.

As another measure of deviation we also use the Relative Root Mean Squared Error, defined as RMSE/RMSEb where RMSE is measured on the method being evaluated and RMSEb on a baseline measure, both taken over multiple runs. When the baseline is random walk this is Thiel’s U2 statistic [22], and this is the baseline we use. The motivation behind using these two measures of deviation is that MMR is based on absolute errors while U2 is based on root mean squared errors; the latter penalises outliers more than the former so any differences between them could be revealing.

For stationary demand experiments we shall also compare TSB and HES using two relative measures. Firstly we use the Relative Geometric Root Mean Squared Error (RGRMSE) of HES with respect to TSB, analysed by [5] and defined in our case as the geometric mean of taken over all periods in multiple runs. RGRMSE is also known as the Geometric Mean Relative Absolute Error and was used by [17]. [1] recommends the use of such relative error-based measures, though they have the drawback of potentially infinite variance because the denominator can be arbitrarily small [3, 10]. Secondly we use the Percentage of times Better (PB), recommended by [11] and defined as the percentage of times the absolute HES error is less than the absolute TSB error.

3.2 Logarithmic demand sizes

We base our first experiments on those of Teunter et al. [21] in which demands occur with some probability in each period, hence inter-demand intervals are distributed geometrically, and we use a logarithmic distribution for demand sizes. Geometrically distributed intervals are a discrete version of Poisson intervals, and the combination of Poisson intervals and logarithmic demand sizes yields a negative binomial distribution, for which there is theoretical and empirical evidence: see for example the recent discussion in [19].

Teunter et al. compare several forecasters on demand that is nonzero with probability where is either 0.2 or 0.5, and whose size is logarithmically distributed. The logarithmic distribution is characterised by a parameter and is discrete with for . They use two values: to simulate low demand and to simulate lumpy demand. They use values 0.1, 0.2 and 0.3, and values 0.01, 0.02, 0.03, 0.04, 0.05, 0.1, 0.2, 0.3. We add SY and HES to these experiments, but we drop SES as they found it to have large errors. They take mean results over 10 runs, each with 120 time periods, whereas we use 100 runs. They initialise each forecaster with “correct” values whereas we initialise with arbitrary values then run them for periods using demand probability . A final difference is that instead of mean error and mean squared error we use MASE and MMR/U2 respectively.

The results are shown in Tables 1–4. Because CR, SBA and SY use only one smoothing factor we do not show their results for cases in which . Comparing MASE best-cases in each table, TSB and SY are least biased, closely followed by HES, then CR and SBA. Comparing MMR best-cases, SBA is best, followed by TSB and HES, then CR and SY. Comparing U2 best-cases HES is always at least as good as TSB, though there is little difference. Comparing MMR-worst cases, neither TSB nor HES dominates the other though HES seems slightly better. Again SBA gives best results, CR and SY generally the worst. Comparing U2-worst cases HES beats TSB and seems to be more robust under different smoothing factors. SBA again gives best results, while CR and SY have variable performance.

To examine the relative best-case performance of HES and TSB more closely, Table 5 compares TSB and HES using RGRMSE and PB. To make this comparison we must choose smoothing factors for both methods, and we do this in two different ways: those giving the best MMR results and those giving the best U2 results. The table also shows the best factors, denoted by . Using the MMR-best factors HES performs rather less well than TSB on lumpy demand, under both RGRMSE and PB. But using U2-best factors there is little difference between the methods. The table also shows that to optimise U2 we should use small factors for both TSB and HES, but to optimise MMR the best factors depend on the form of the demand.

3.3 Geometric demand sizes

Another demand distribution that has recieved interest, and for which there is also theoretical and empirical support, is the stuttering Poisson distribution [19] in which demand intervals are Poisson and demand sizes are geometrically distributed. Again we use a discrete version with geometrically distributed intervals. The geometric distribution is characterised by a probability we shall denote by , and is discrete with for . We use two values of : 0.2 and 0.8 to simulate low and lumpy demand respectively. Otherwise the experiments are as in Section 3.2.

The results are shown in Tables 6–9. Though the numbers are different, qualitatively the TSB and HES results are the same as for logarithmic demand sizes. However, CR, SBA and SY now give similar results to each other, and SBA no longer has the best best-case U2 result, though it still has the best worst-case U2 result. Table 10 compares TSB and HES using the RGRMSE and PB measures. Qualitatively the results are the same as with logarithmic demand sizes, except that HES is now worse than TSB in all 4 tables for MMR best-cases — though there is still little difference between the U2-best cases.

3.4 Decreasing demand

The experiments so far use stationary demand, but Teunter et al. also consider nonstationary demand. Again demand sizes follow the logarithmic distribution, while the probability of a nonzero demand decreases linearly from in the first period to 0 during the last period. Demand sizes are again logarithmically distributed. As pointed out by Teunter et al., none of the forecasters use trending to model the decreasing demand so all are positively biased.

The results are shown in Tables 11–14. TSB clearly has the best best-case MASE, MMR and U2 results, while HES is next-best, though SBA occasionally beats HES. HES has the worst worst-case MASE, MMR and U2 results, followed by TSB. However, if we only consider HES and TSB results for which then CR, SBA and SY have the worst worst-cases, with HES also poor on lumpy demand.

The best for all methods is larger: as pointed out by Teunter et al., large smoothing factors are best at handling non-stationary demand, while small factors are best when demand is stationary. The best value is relatively unimportant here, which makes sense as demand sizes are stationary.

3.5 Sudden obsolescence

We repeat the experiments of Section 3.4, but instead of linearly decreasing the probability of demand we reduce it immediately to 0 after half (60) of the periods, again following Teunter et al. Demand sizes are again logarithmically distributed. The results are shown in Tables 15–18. As found by Teunter et al. the differences between TSB and CR, SBA and SY are more pronounced because the latter are given no opportunity to adjust to the change in demand pattern. The results are qualitatively similar to those for decreasing demand, but with greater differences.

3.6 Bias at issue points only

It is noted in [21] that although TSB is unbiased in the above sense, it is biased if we only compare forecasts with expected demand at issue points only (that is when demand occurs). SES is similarly biased, but not Croston methods such as SBA or SY. The cause is the decay in forecast size between demands, and HES will clearly suffer from a similar bias. We repeated the stationary demand experiments with logarithmically and geometrically distributed demand sizes, and measured the bias of TSB and HES based on issue points only. Both had greater bias than SY (as expected) but neither dominated the other.

3.7 Summary of empirical results

On stationary demand SBA performs very well, followed by TSB and HES. The relative performance of HES and TSB depends on how they are tuned. If we tune them using MMR then TSB beats HES under both the RGRMSE and PB measures, but the best smoothing factors are erratic; while if we tune them using U2 there is no significant difference between them, and the best smoothing factors are small. We prefer to take the U2-based results, not because they are better for our method but because they are more consistent with other work: Teunter et al. found that small smoothing factors are best for stationary demand, though admittedly this could simply be because they used another (unscaled) mean squared error measure. Intuitively this makes sense, whereas using MMR we found no consistent results for the best smoothing factors. [8] also recommend tuning by U2. Thus we recommend tuning forecasting methods using U2 rather than MMR, and when doing this small smoothing factors are best for stationary demand. Under these conditions TSB and HES seem to be equally good under two different measures, though they are slightly beaten by SBA.

HES is more robust than TSB under changes to the smoothing factors, with better worst-case behaviour as measured by both MMR and U2. We believe that this is because HES’s hyperbolic decay between demands is slower than TSB’s exponential decay, so large smoothing factors are less harmful. But on non-stationary demand, with intervals increasing linearly or abruptly, TSB is best followed by HES, with CR, SBA and SY giving worse performance if we consider the same range of smoothing factor settings. Here TSB’s greater reactivity serves it well. As found by other researchers, and as is intuitively clear, large smoothing factors are best at handling changes in demand pattern. However, HES’s robustness means that we can recommend smoothing factors that behave reasonably well on both stationary and non-stationary demand: . The results in all cases are not much worse than with optimally-tuned factors.

4 Conclusion

We presented a new forecasting method called Hyperbolic-Exponential Smoothing (HES), which is based on an application of Bayesian inference when no demand occurs. We showed theoretically that HES is approximately unbiased, and compared it empirically with Croston variants CR, SBA, SY and TSB. On stationary demand we found little difference between TSB and HES, though HES was more robust under changes to smoothing factors, and both performed well against other Croston methods. On non-stationary demand TSB performed best, followed by HES.

Like TSB, HES has two smoothing factors and . In common with other methods, HES performs best on stationary demand with small smoothing factors, and best on non-stationary demand with larger factors. Using smoothing factors gave reasonable results on a variety of demand patterns and we recommend these values.

Acknowledgment

Thanks to Aris Syntetos for helpful advice, and to the anonymous referees for useful criticism. This work was partially funded by Enterprise Ireland Innovation Voucher IV-2009-2092.

References

- [1] J. S. Armstrong, F. Collopy. Error Measures for Generalizing About Forecasting Methods: Empirical Comparisons. International Journal of Forecasting 8:69–80, 1992.

- [2] J. E. Boylan, A. A. Syntetos. The Accuracy of a Modified Croston Procedure. International Journal of Production Economics 107:511–517, 2007.

- [3] D. C. Chatfield, J. C. Hayyab. All-Zero Forecasts for Lumpy Demand: a Factorial Study. International Journal of Production Research 45(4):935–950, 2007.

- [4] J. D. Croston. Forecasting and Stock Control for Intermittent Demands. Operational Research Quarterly 23(3):289–304, 1972.

- [5] R. Fildes. The Evaluation of Extrapolative Forecasting Methods. International Journal of Forecasting 8(1):81–98, 1992.

- [6] R. Fildes, K. Nikolopoulos, S. F. Crone, A. A. Syntetos. Forecasting and Operational Research: a Review. Journal of the Operational Research Society 59:1150–1172, 2008.

- [7] E. S. Gardner Jr. Exponential Smoothing: the State of the Art — Part II. International Journal of Forecasting 22(4):637–666, 2006.

- [8] A. A. Ghobbar, C. H. Friend. Evaluation of Forecasting Methods for Intermittent Parts Demand in the Field of Aviation: a Predictive Model. Computers & Operations Research 30:2097–2114, 2003.

- [9] J. D. de Gooijer, R. J. Hyndman. 25 Years of IIF Time Series Forecasting: a Selective Review, Tinbergen Institute Discussion Paper No 05-068/4, Tinbergen Institute, 2005.

- [10] R. J. Hyndman, A. B. Koehler. Another Look at Measures of Forecast Accuracy. International Journal of Forecasting 22(4):679–688, 2006.

- [11] S. Kolassa, W. Schütz. Advantages of the MAD/mean ratio over the MAPE. Foresight 6:40-–43, 2007.

- [12] P.-S. Laplace. Essai Philosophique sur les Probabilités. Paris: Courcier, 1814.

- [13] E. Levén, A. Segerstedt. Inventory Control With a Modified Croston Procedure and Erlang Distribution. International Journal of Production Economics 90(3):361-367, 2004.

- [14] D. Poole, A. Mackworth. Artificial Intelligence: Foundations of Computational Agents. Cambridge University Press, 2010.

- [15] S. D. Prestwich, S. A. Tarim, R. Rossi, and B. Hnich. Forecasting Intermittent Demand by Hyperbolic-Exponential Smoothing. International Journal of Forecasting, 2014 (to appear).

- [16] A. A. Syntetos. Forecasting for Intermittent Demand. Unpublished PhD thesis, Buckinghamshire Chilterns University College, Brunel University, 2001.

- [17] A. A. Syntetos, J. E. Boylan. The Accuracy of Intermittent Demand Estimates. International Journal of Forecasting 21:303–314, 2005.

- [18] A. A. Syntetos, J. E. Boylan, S. M. Disney. Forecasting for Inventory Planning: a 50-Year Review. Journal of the Operations Research Society 60:149–160, 2009.

- [19] A. Syntetos, Z. Babai, D. Lengu, N. Altay. Distributional Assumptions for Parametric Forecasting of Intermittent Demand. In: N. Altay & A. Litteral (eds.), Service Parts Management: Demand Forecasting and Inventory Control, Springer Verlag, NY, USA, 2011, pp.31–52.

- [20] R. Teunter, B. Sani. On the Bias of Croston’s Forecasting Method. European Journal of Operations Research 194:177–183, 2007.

- [21] R. Teunter, A. A. Syntetos, M. Z. Babai. Intermittent Demand: Linking Forecasting to Inventory Obsolescence. European Journal of Operations Research 214(3):606–615, 2011.

- [22] H. Thiel. Applied Economic Forecasting. Rand McNally, 1966.

Appendix 0.A Results

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.015 | 1.219 | 0.717 | -0.019 | 1.194 | 0.717 | -0.001 | 1.207 | 0.717 |

| 0.20 | 0.20 | 0.032 | 1.249 | 0.730 | -0.037 | 1.197 | 0.726 | -0.000 | 1.225 | 0.728 |

| 0.30 | 0.30 | 0.051 | 1.283 | 0.745 | -0.056 | 1.200 | 0.735 | 0.003 | 1.247 | 0.741 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | -0.006 | 1.200 | 0.715 | -0.007 | 1.198 | 0.715 |

| 0.10 | 0.02 | -0.004 | 1.203 | 0.716 | -0.006 | 1.200 | 0.715 |

| 0.10 | 0.03 | -0.003 | 1.204 | 0.716 | -0.005 | 1.201 | 0.715 |

| 0.10 | 0.04 | -0.002 | 1.206 | 0.717 | -0.004 | 1.202 | 0.716 |

| 0.10 | 0.05 | -0.002 | 1.207 | 0.717 | -0.003 | 1.203 | 0.716 |

| 0.10 | 0.10 | -0.001 | 1.211 | 0.720 | -0.001 | 1.207 | 0.717 |

| 0.10 | 0.20 | -0.000 | 1.223 | 0.726 | 0.001 | 1.212 | 0.720 |

| 0.10 | 0.30 | -0.000 | 1.236 | 0.732 | 0.004 | 1.219 | 0.722 |

| 0.20 | 0.01 | -0.007 | 1.211 | 0.723 | -0.009 | 1.209 | 0.722 |

| 0.20 | 0.02 | -0.005 | 1.214 | 0.723 | -0.007 | 1.211 | 0.723 |

| 0.20 | 0.03 | -0.004 | 1.215 | 0.724 | -0.006 | 1.213 | 0.723 |

| 0.20 | 0.04 | -0.004 | 1.216 | 0.725 | -0.005 | 1.214 | 0.723 |

| 0.20 | 0.05 | -0.003 | 1.218 | 0.725 | -0.005 | 1.214 | 0.724 |

| 0.20 | 0.10 | -0.003 | 1.223 | 0.728 | -0.003 | 1.218 | 0.725 |

| 0.20 | 0.20 | -0.002 | 1.234 | 0.734 | -0.001 | 1.224 | 0.728 |

| 0.20 | 0.30 | -0.002 | 1.247 | 0.741 | 0.002 | 1.230 | 0.731 |

| 0.30 | 0.01 | -0.007 | 1.224 | 0.731 | -0.009 | 1.222 | 0.731 |

| 0.30 | 0.02 | -0.005 | 1.226 | 0.732 | -0.007 | 1.224 | 0.731 |

| 0.30 | 0.03 | -0.005 | 1.227 | 0.732 | -0.006 | 1.225 | 0.732 |

| 0.30 | 0.04 | -0.004 | 1.229 | 0.733 | -0.006 | 1.226 | 0.732 |

| 0.30 | 0.05 | -0.004 | 1.230 | 0.734 | -0.005 | 1.227 | 0.732 |

| 0.30 | 0.10 | -0.003 | 1.235 | 0.737 | -0.003 | 1.230 | 0.734 |

| 0.30 | 0.20 | -0.003 | 1.247 | 0.744 | -0.001 | 1.236 | 0.737 |

| 0.30 | 0.30 | -0.002 | 1.259 | 0.751 | 0.002 | 1.243 | 0.740 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.027 | 1.651 | 0.707 | -0.000 | 1.617 | 0.707 | 0.005 | 1.624 | 0.707 |

| 0.20 | 0.20 | 0.053 | 1.695 | 0.714 | -0.004 | 1.621 | 0.711 | 0.008 | 1.637 | 0.712 |

| 0.30 | 0.30 | 0.082 | 1.746 | 0.723 | -0.008 | 1.626 | 0.717 | 0.013 | 1.654 | 0.719 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.007 | 1.623 | 0.706 | 0.014 | 1.631 | 0.706 |

| 0.10 | 0.02 | 0.004 | 1.621 | 0.707 | 0.012 | 1.629 | 0.706 |

| 0.10 | 0.03 | 0.002 | 1.620 | 0.707 | 0.010 | 1.627 | 0.706 |

| 0.10 | 0.04 | 0.002 | 1.620 | 0.708 | 0.008 | 1.625 | 0.706 |

| 0.10 | 0.05 | 0.002 | 1.621 | 0.709 | 0.007 | 1.624 | 0.706 |

| 0.10 | 0.10 | 0.003 | 1.627 | 0.712 | 0.004 | 1.622 | 0.707 |

| 0.10 | 0.20 | 0.003 | 1.639 | 0.720 | 0.005 | 1.624 | 0.708 |

| 0.10 | 0.30 | 0.002 | 1.651 | 0.728 | 0.008 | 1.631 | 0.709 |

| 0.20 | 0.01 | 0.009 | 1.634 | 0.709 | 0.016 | 1.642 | 0.709 |

| 0.20 | 0.02 | 0.005 | 1.630 | 0.710 | 0.014 | 1.640 | 0.709 |

| 0.20 | 0.03 | 0.004 | 1.628 | 0.711 | 0.012 | 1.638 | 0.709 |

| 0.20 | 0.04 | 0.003 | 1.628 | 0.711 | 0.010 | 1.636 | 0.709 |

| 0.20 | 0.05 | 0.003 | 1.629 | 0.712 | 0.009 | 1.635 | 0.709 |

| 0.20 | 0.10 | 0.003 | 1.634 | 0.716 | 0.006 | 1.632 | 0.710 |

| 0.20 | 0.20 | 0.003 | 1.646 | 0.724 | 0.006 | 1.633 | 0.711 |

| 0.20 | 0.30 | 0.003 | 1.657 | 0.733 | 0.009 | 1.638 | 0.713 |

| 0.30 | 0.01 | 0.010 | 1.643 | 0.713 | 0.018 | 1.652 | 0.713 |

| 0.30 | 0.02 | 0.007 | 1.638 | 0.714 | 0.016 | 1.650 | 0.713 |

| 0.30 | 0.03 | 0.005 | 1.637 | 0.714 | 0.014 | 1.647 | 0.713 |

| 0.30 | 0.04 | 0.004 | 1.636 | 0.715 | 0.012 | 1.645 | 0.713 |

| 0.30 | 0.05 | 0.003 | 1.636 | 0.715 | 0.011 | 1.644 | 0.713 |

| 0.30 | 0.10 | 0.003 | 1.641 | 0.719 | 0.008 | 1.640 | 0.714 |

| 0.30 | 0.20 | 0.003 | 1.652 | 0.728 | 0.007 | 1.641 | 0.715 |

| 0.30 | 0.30 | 0.002 | 1.663 | 0.738 | 0.010 | 1.646 | 0.717 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.023 | 0.988 | 0.718 | -0.029 | 0.989 | 0.717 | -0.002 | 0.988 | 0.718 |

| 0.20 | 0.20 | 0.051 | 0.988 | 0.729 | -0.055 | 0.989 | 0.725 | 0.001 | 0.989 | 0.728 |

| 0.30 | 0.30 | 0.080 | 0.989 | 0.741 | -0.084 | 0.990 | 0.733 | 0.006 | 0.990 | 0.740 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | -0.008 | 0.987 | 0.710 | -0.011 | 0.987 | 0.709 |

| 0.10 | 0.02 | -0.004 | 0.988 | 0.711 | -0.008 | 0.988 | 0.710 |

| 0.10 | 0.03 | -0.003 | 0.988 | 0.713 | -0.006 | 0.988 | 0.711 |

| 0.10 | 0.04 | -0.003 | 0.988 | 0.715 | -0.005 | 0.988 | 0.712 |

| 0.10 | 0.05 | -0.002 | 0.988 | 0.717 | -0.004 | 0.988 | 0.712 |

| 0.10 | 0.10 | -0.002 | 0.988 | 0.726 | -0.002 | 0.988 | 0.717 |

| 0.10 | 0.20 | -0.002 | 0.989 | 0.746 | 0.001 | 0.988 | 0.726 |

| 0.10 | 0.30 | -0.001 | 0.989 | 0.768 | 0.004 | 0.989 | 0.735 |

| 0.20 | 0.01 | -0.008 | 0.987 | 0.710 | -0.011 | 0.987 | 0.709 |

| 0.20 | 0.02 | -0.004 | 0.988 | 0.711 | -0.008 | 0.988 | 0.710 |

| 0.20 | 0.03 | -0.003 | 0.988 | 0.713 | -0.006 | 0.988 | 0.711 |

| 0.20 | 0.04 | -0.003 | 0.988 | 0.715 | -0.005 | 0.988 | 0.712 |

| 0.20 | 0.05 | -0.002 | 0.988 | 0.717 | -0.004 | 0.988 | 0.712 |

| 0.20 | 0.10 | -0.002 | 0.988 | 0.726 | -0.002 | 0.988 | 0.717 |

| 0.20 | 0.20 | -0.002 | 0.989 | 0.746 | 0.001 | 0.988 | 0.726 |

| 0.20 | 0.30 | -0.001 | 0.989 | 0.768 | 0.004 | 0.989 | 0.735 |

| 0.30 | 0.01 | -0.008 | 0.987 | 0.710 | -0.011 | 0.987 | 0.709 |

| 0.30 | 0.02 | -0.004 | 0.988 | 0.711 | -0.008 | 0.987 | 0.710 |

| 0.30 | 0.03 | -0.003 | 0.988 | 0.713 | -0.006 | 0.988 | 0.711 |

| 0.30 | 0.04 | -0.003 | 0.988 | 0.715 | -0.005 | 0.988 | 0.712 |

| 0.30 | 0.05 | -0.002 | 0.988 | 0.717 | -0.004 | 0.988 | 0.712 |

| 0.30 | 0.10 | -0.002 | 0.988 | 0.726 | -0.002 | 0.988 | 0.717 |

| 0.30 | 0.20 | -0.002 | 0.989 | 0.746 | 0.001 | 0.988 | 0.726 |

| 0.30 | 0.30 | -0.001 | 0.989 | 0.768 | 0.004 | 0.989 | 0.735 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.026 | 1.635 | 0.711 | -0.005 | 1.603 | 0.710 | 0.001 | 1.610 | 0.710 |

| 0.20 | 0.20 | 0.053 | 1.663 | 0.716 | -0.011 | 1.597 | 0.714 | 0.003 | 1.611 | 0.715 |

| 0.30 | 0.30 | 0.086 | 1.697 | 0.724 | -0.015 | 1.592 | 0.718 | 0.008 | 1.616 | 0.720 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.002 | 1.610 | 0.708 | 0.009 | 1.618 | 0.707 |

| 0.10 | 0.02 | -0.001 | 1.607 | 0.710 | 0.007 | 1.616 | 0.707 |

| 0.10 | 0.03 | -0.002 | 1.605 | 0.711 | 0.005 | 1.614 | 0.707 |

| 0.10 | 0.04 | -0.002 | 1.605 | 0.713 | 0.004 | 1.612 | 0.708 |

| 0.10 | 0.05 | -0.002 | 1.605 | 0.715 | 0.003 | 1.611 | 0.708 |

| 0.10 | 0.10 | -0.001 | 1.605 | 0.724 | 0.000 | 1.608 | 0.710 |

| 0.10 | 0.20 | -0.001 | 1.606 | 0.744 | 0.001 | 1.608 | 0.713 |

| 0.10 | 0.30 | -0.001 | 1.606 | 0.765 | 0.005 | 1.611 | 0.717 |

| 0.20 | 0.01 | 0.002 | 1.611 | 0.708 | 0.009 | 1.618 | 0.707 |

| 0.20 | 0.02 | -0.001 | 1.607 | 0.710 | 0.007 | 1.616 | 0.707 |

| 0.20 | 0.03 | -0.001 | 1.606 | 0.711 | 0.005 | 1.614 | 0.707 |

| 0.20 | 0.04 | -0.002 | 1.605 | 0.713 | 0.004 | 1.613 | 0.708 |

| 0.20 | 0.05 | -0.001 | 1.605 | 0.715 | 0.003 | 1.611 | 0.708 |

| 0.20 | 0.10 | -0.001 | 1.605 | 0.724 | 0.000 | 1.608 | 0.710 |

| 0.20 | 0.20 | -0.001 | 1.606 | 0.744 | 0.001 | 1.608 | 0.713 |

| 0.20 | 0.30 | -0.001 | 1.606 | 0.766 | 0.005 | 1.612 | 0.717 |

| 0.30 | 0.01 | 0.002 | 1.611 | 0.708 | 0.010 | 1.618 | 0.707 |

| 0.30 | 0.02 | -0.000 | 1.607 | 0.710 | 0.007 | 1.616 | 0.707 |

| 0.30 | 0.03 | -0.001 | 1.606 | 0.711 | 0.006 | 1.614 | 0.708 |

| 0.30 | 0.04 | -0.001 | 1.605 | 0.713 | 0.004 | 1.613 | 0.708 |

| 0.30 | 0.05 | -0.001 | 1.605 | 0.715 | 0.003 | 1.612 | 0.708 |

| 0.30 | 0.10 | -0.000 | 1.606 | 0.724 | 0.001 | 1.609 | 0.710 |

| 0.30 | 0.20 | -0.001 | 1.606 | 0.744 | 0.001 | 1.608 | 0.713 |

| 0.30 | 0.30 | -0.001 | 1.606 | 0.766 | 0.005 | 1.612 | 0.717 |

| RGRMSE | PB | ||||||

| MMR-best factors | |||||||

| 0.900 | 0.5 | 0.1 | 0.01 | 0.1 | 0.01 | 1.630 | 35 |

| 0.900 | 0.2 | 0.1 | 0.03 | 0.1 | 0.06 | 2.578 | 20 |

| 0.001 | 0.5 | 0.1 | 0.01 | 0.1 | 0.01 | 1.001 | 50 |

| 0.001 | 0.2 | 0.1 | 0.03 | 0.1 | 0.06 | 1.015 | 50 |

| U2-best factors | |||||||

| 0.900 | 0.5 | 0.1 | 0.01 | 0.1 | 0.01 | 0.997 | 53 |

| 0.900 | 0.2 | 0.1 | 0.01 | 0.1 | 0.01 | 1.011 | 47 |

| 0.001 | 0.5 | 0.1 | 0.01 | 0.1 | 0.01 | 1.001 | 50 |

| 0.001 | 0.2 | 0.1 | 0.01 | 0.1 | 0.01 | 1.016 | 47 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.022 | 1.169 | 0.713 | -0.014 | 1.150 | 0.712 | 0.005 | 1.160 | 0.712 |

| 0.20 | 0.20 | 0.039 | 1.190 | 0.723 | -0.034 | 1.149 | 0.719 | 0.005 | 1.171 | 0.722 |

| 0.30 | 0.30 | 0.057 | 1.212 | 0.735 | -0.055 | 1.147 | 0.726 | 0.006 | 1.184 | 0.732 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.001 | 1.156 | 0.710 | 0.000 | 1.156 | 0.710 |

| 0.10 | 0.02 | 0.003 | 1.157 | 0.711 | 0.002 | 1.156 | 0.710 |

| 0.10 | 0.03 | 0.004 | 1.158 | 0.711 | 0.003 | 1.157 | 0.710 |

| 0.10 | 0.04 | 0.004 | 1.159 | 0.712 | 0.003 | 1.157 | 0.711 |

| 0.10 | 0.05 | 0.004 | 1.160 | 0.713 | 0.004 | 1.158 | 0.711 |

| 0.10 | 0.10 | 0.004 | 1.165 | 0.716 | 0.005 | 1.160 | 0.712 |

| 0.10 | 0.20 | 0.003 | 1.176 | 0.724 | 0.006 | 1.164 | 0.715 |

| 0.10 | 0.30 | 0.003 | 1.188 | 0.733 | 0.007 | 1.170 | 0.719 |

| 0.20 | 0.01 | 0.001 | 1.163 | 0.716 | 0.000 | 1.162 | 0.716 |

| 0.20 | 0.02 | 0.003 | 1.164 | 0.717 | 0.002 | 1.163 | 0.716 |

| 0.20 | 0.03 | 0.004 | 1.165 | 0.717 | 0.003 | 1.163 | 0.716 |

| 0.20 | 0.04 | 0.004 | 1.166 | 0.718 | 0.003 | 1.164 | 0.717 |

| 0.20 | 0.05 | 0.004 | 1.167 | 0.719 | 0.004 | 1.164 | 0.717 |

| 0.20 | 0.10 | 0.004 | 1.171 | 0.722 | 0.005 | 1.167 | 0.718 |

| 0.20 | 0.20 | 0.003 | 1.182 | 0.731 | 0.005 | 1.171 | 0.722 |

| 0.20 | 0.30 | 0.003 | 1.194 | 0.740 | 0.007 | 1.176 | 0.725 |

| 0.30 | 0.01 | 0.001 | 1.170 | 0.723 | 0.000 | 1.170 | 0.722 |

| 0.30 | 0.02 | 0.003 | 1.171 | 0.723 | 0.001 | 1.170 | 0.723 |

| 0.30 | 0.03 | 0.003 | 1.172 | 0.724 | 0.002 | 1.171 | 0.723 |

| 0.30 | 0.04 | 0.004 | 1.173 | 0.725 | 0.003 | 1.172 | 0.723 |

| 0.30 | 0.05 | 0.004 | 1.174 | 0.725 | 0.004 | 1.172 | 0.724 |

| 0.30 | 0.10 | 0.003 | 1.179 | 0.729 | 0.004 | 1.174 | 0.725 |

| 0.30 | 0.20 | 0.003 | 1.189 | 0.738 | 0.005 | 1.178 | 0.728 |

| 0.30 | 0.30 | 0.002 | 1.201 | 0.747 | 0.007 | 1.184 | 0.732 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.041 | 1.668 | 0.714 | 0.012 | 1.633 | 0.713 | 0.018 | 1.640 | 0.713 |

| 0.20 | 0.20 | 0.067 | 1.708 | 0.721 | 0.007 | 1.633 | 0.718 | 0.020 | 1.649 | 0.719 |

| 0.30 | 0.30 | 0.097 | 1.754 | 0.731 | 0.003 | 1.634 | 0.724 | 0.024 | 1.662 | 0.726 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.020 | 1.641 | 0.712 | 0.023 | 1.645 | 0.712 |

| 0.10 | 0.02 | 0.017 | 1.639 | 0.713 | 0.024 | 1.645 | 0.712 |

| 0.10 | 0.03 | 0.016 | 1.639 | 0.714 | 0.023 | 1.644 | 0.712 |

| 0.10 | 0.04 | 0.015 | 1.639 | 0.715 | 0.022 | 1.643 | 0.712 |

| 0.10 | 0.05 | 0.014 | 1.639 | 0.716 | 0.021 | 1.642 | 0.712 |

| 0.10 | 0.10 | 0.012 | 1.641 | 0.720 | 0.018 | 1.640 | 0.713 |

| 0.10 | 0.20 | 0.010 | 1.648 | 0.731 | 0.018 | 1.642 | 0.715 |

| 0.10 | 0.30 | 0.009 | 1.655 | 0.743 | 0.020 | 1.648 | 0.717 |

| 0.20 | 0.01 | 0.021 | 1.646 | 0.715 | 0.025 | 1.650 | 0.714 |

| 0.20 | 0.02 | 0.019 | 1.644 | 0.716 | 0.025 | 1.650 | 0.715 |

| 0.20 | 0.03 | 0.017 | 1.643 | 0.717 | 0.024 | 1.649 | 0.715 |

| 0.20 | 0.04 | 0.016 | 1.643 | 0.718 | 0.023 | 1.648 | 0.715 |

| 0.20 | 0.05 | 0.015 | 1.643 | 0.718 | 0.022 | 1.647 | 0.715 |

| 0.20 | 0.10 | 0.012 | 1.644 | 0.723 | 0.019 | 1.645 | 0.716 |

| 0.20 | 0.20 | 0.010 | 1.650 | 0.734 | 0.019 | 1.647 | 0.718 |

| 0.20 | 0.30 | 0.009 | 1.657 | 0.746 | 0.021 | 1.652 | 0.720 |

| 0.30 | 0.01 | 0.022 | 1.650 | 0.718 | 0.025 | 1.653 | 0.717 |

| 0.30 | 0.02 | 0.019 | 1.647 | 0.719 | 0.025 | 1.653 | 0.717 |

| 0.30 | 0.03 | 0.018 | 1.647 | 0.720 | 0.024 | 1.652 | 0.718 |

| 0.30 | 0.04 | 0.016 | 1.646 | 0.721 | 0.023 | 1.651 | 0.718 |

| 0.30 | 0.05 | 0.016 | 1.646 | 0.721 | 0.022 | 1.650 | 0.718 |

| 0.30 | 0.10 | 0.012 | 1.647 | 0.726 | 0.020 | 1.648 | 0.719 |

| 0.30 | 0.20 | 0.009 | 1.651 | 0.737 | 0.019 | 1.650 | 0.721 |

| 0.30 | 0.30 | 0.008 | 1.658 | 0.750 | 0.021 | 1.656 | 0.723 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.021 | 1.014 | 0.716 | -0.022 | 1.013 | 0.715 | -0.000 | 1.013 | 0.716 |

| 0.20 | 0.20 | 0.043 | 1.018 | 0.727 | -0.045 | 1.014 | 0.724 | 0.001 | 1.017 | 0.726 |

| 0.30 | 0.30 | 0.067 | 1.029 | 0.739 | -0.070 | 1.016 | 0.731 | 0.003 | 1.024 | 0.737 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.002 | 1.011 | 0.710 | 0.003 | 1.010 | 0.710 |

| 0.10 | 0.02 | 0.001 | 1.012 | 0.712 | 0.001 | 1.011 | 0.710 |

| 0.10 | 0.03 | 0.001 | 1.013 | 0.713 | 0.001 | 1.011 | 0.711 |

| 0.10 | 0.04 | 0.000 | 1.013 | 0.715 | 0.001 | 1.012 | 0.712 |

| 0.10 | 0.05 | 0.000 | 1.014 | 0.716 | 0.000 | 1.012 | 0.712 |

| 0.10 | 0.10 | -0.000 | 1.016 | 0.723 | 0.000 | 1.014 | 0.716 |

| 0.10 | 0.20 | -0.000 | 1.021 | 0.738 | 0.001 | 1.016 | 0.722 |

| 0.10 | 0.30 | -0.000 | 1.029 | 0.753 | 0.004 | 1.018 | 0.729 |

| 0.20 | 0.01 | 0.002 | 1.011 | 0.713 | 0.003 | 1.010 | 0.713 |

| 0.20 | 0.02 | 0.001 | 1.012 | 0.715 | 0.001 | 1.011 | 0.713 |

| 0.20 | 0.03 | 0.001 | 1.013 | 0.716 | 0.001 | 1.011 | 0.714 |

| 0.20 | 0.04 | 0.000 | 1.014 | 0.718 | 0.001 | 1.012 | 0.715 |

| 0.20 | 0.05 | 0.000 | 1.014 | 0.719 | 0.000 | 1.012 | 0.715 |

| 0.20 | 0.10 | -0.000 | 1.017 | 0.726 | -0.000 | 1.014 | 0.719 |

| 0.20 | 0.20 | -0.000 | 1.024 | 0.741 | 0.001 | 1.017 | 0.725 |

| 0.20 | 0.30 | -0.000 | 1.034 | 0.757 | 0.004 | 1.020 | 0.732 |

| 0.30 | 0.01 | 0.001 | 1.012 | 0.716 | 0.003 | 1.011 | 0.716 |

| 0.30 | 0.02 | 0.001 | 1.013 | 0.718 | 0.001 | 1.011 | 0.716 |

| 0.30 | 0.03 | 0.000 | 1.014 | 0.719 | 0.001 | 1.012 | 0.717 |

| 0.30 | 0.04 | 0.000 | 1.015 | 0.721 | 0.000 | 1.013 | 0.718 |

| 0.30 | 0.05 | -0.000 | 1.016 | 0.722 | 0.000 | 1.013 | 0.718 |

| 0.30 | 0.10 | -0.000 | 1.020 | 0.729 | -0.000 | 1.016 | 0.722 |

| 0.30 | 0.20 | -0.000 | 1.028 | 0.744 | 0.001 | 1.019 | 0.728 |

| 0.30 | 0.30 | -0.000 | 1.039 | 0.760 | 0.004 | 1.024 | 0.735 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.032 | 1.631 | 0.715 | 0.001 | 1.599 | 0.714 | 0.008 | 1.606 | 0.714 |

| 0.20 | 0.20 | 0.056 | 1.655 | 0.720 | -0.008 | 1.589 | 0.718 | 0.006 | 1.604 | 0.719 |

| 0.30 | 0.30 | 0.085 | 1.683 | 0.728 | -0.015 | 1.580 | 0.722 | 0.008 | 1.604 | 0.724 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.007 | 1.606 | 0.713 | 0.001 | 1.599 | 0.712 |

| 0.10 | 0.02 | 0.007 | 1.604 | 0.714 | 0.004 | 1.602 | 0.712 |

| 0.10 | 0.03 | 0.004 | 1.602 | 0.715 | 0.006 | 1.604 | 0.712 |

| 0.10 | 0.04 | 0.002 | 1.599 | 0.717 | 0.008 | 1.606 | 0.713 |

| 0.10 | 0.05 | 0.001 | 1.598 | 0.718 | 0.009 | 1.607 | 0.713 |

| 0.10 | 0.10 | -0.000 | 1.594 | 0.725 | 0.007 | 1.605 | 0.714 |

| 0.10 | 0.20 | -0.001 | 1.593 | 0.741 | 0.004 | 1.601 | 0.717 |

| 0.10 | 0.30 | -0.001 | 1.593 | 0.759 | 0.006 | 1.601 | 0.720 |

| 0.20 | 0.01 | 0.009 | 1.608 | 0.714 | 0.002 | 1.602 | 0.713 |

| 0.20 | 0.02 | 0.008 | 1.607 | 0.715 | 0.005 | 1.604 | 0.713 |

| 0.20 | 0.03 | 0.006 | 1.604 | 0.717 | 0.008 | 1.607 | 0.714 |

| 0.20 | 0.04 | 0.004 | 1.602 | 0.718 | 0.009 | 1.609 | 0.714 |

| 0.20 | 0.05 | 0.003 | 1.600 | 0.719 | 0.010 | 1.610 | 0.714 |

| 0.20 | 0.10 | 0.001 | 1.596 | 0.726 | 0.009 | 1.608 | 0.715 |

| 0.20 | 0.20 | 0.000 | 1.594 | 0.743 | 0.006 | 1.603 | 0.718 |

| 0.20 | 0.30 | -0.000 | 1.594 | 0.760 | 0.007 | 1.603 | 0.721 |

| 0.30 | 0.01 | 0.010 | 1.609 | 0.715 | 0.003 | 1.602 | 0.714 |

| 0.30 | 0.02 | 0.009 | 1.608 | 0.716 | 0.005 | 1.605 | 0.714 |

| 0.30 | 0.03 | 0.006 | 1.605 | 0.718 | 0.008 | 1.607 | 0.715 |

| 0.30 | 0.04 | 0.005 | 1.602 | 0.719 | 0.010 | 1.609 | 0.715 |

| 0.30 | 0.05 | 0.003 | 1.600 | 0.720 | 0.011 | 1.610 | 0.715 |

| 0.30 | 0.10 | 0.001 | 1.596 | 0.728 | 0.010 | 1.609 | 0.717 |

| 0.30 | 0.20 | 0.000 | 1.594 | 0.744 | 0.007 | 1.604 | 0.719 |

| 0.30 | 0.30 | 0.000 | 1.595 | 0.762 | 0.008 | 1.604 | 0.722 |

| RGRMSE | PB | ||||||

| MMR-best factors | |||||||

| 0.900 | 0.5 | 0.1 | 0.01 | 0.1 | 0.01 | 1.727 | 39 |

| 0.900 | 0.2 | 0.1 | 0.02 | 0.1 | 0.06 | 3.244 | 20 |

| 0.001 | 0.5 | 0.1 | 0.01 | 0.1 | 0.01 | 0.983 | 50 |

| 0.001 | 0.2 | 0.1 | 0.07 | 0.1 | 0.01 | 1.565 | 39 |

| U2-best factors | |||||||

| 0.900 | 0.5 | 0.1 | 0.01 | 0.1 | 0.01 | 1.001 | 51 |

| 0.900 | 0.2 | 0.1 | 0.01 | 0.1 | 0.01 | 1.004 | 50 |

| 0.001 | 0.5 | 0.1 | 0.01 | 0.1 | 0.01 | 1.000 | 51 |

| 0.001 | 0.2 | 0.1 | 0.01 | 0.1 | 0.01 | 1.000 | 53 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.161 | 1.785 | 0.722 | 0.136 | 1.736 | 0.719 | 0.146 | 1.754 | 0.720 |

| 0.20 | 0.20 | 0.135 | 1.735 | 0.728 | 0.087 | 1.642 | 0.721 | 0.105 | 1.676 | 0.724 |

| 0.30 | 0.30 | 0.131 | 1.737 | 0.738 | 0.060 | 1.599 | 0.725 | 0.088 | 1.651 | 0.731 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.234 | 1.958 | 0.734 | 0.285 | 2.088 | 0.747 |

| 0.10 | 0.02 | 0.174 | 1.812 | 0.723 | 0.250 | 2.000 | 0.738 |

| 0.10 | 0.03 | 0.136 | 1.723 | 0.718 | 0.223 | 1.935 | 0.732 |

| 0.10 | 0.04 | 0.110 | 1.666 | 0.715 | 0.202 | 1.885 | 0.728 |

| 0.10 | 0.05 | 0.092 | 1.627 | 0.714 | 0.186 | 1.844 | 0.725 |

| 0.10 | 0.10 | 0.050 | 1.540 | 0.714 | 0.134 | 1.725 | 0.718 |

| 0.10 | 0.20 | 0.024 | 1.502 | 0.720 | 0.090 | 1.630 | 0.715 |

| 0.10 | 0.30 | 0.015 | 1.499 | 0.727 | 0.070 | 1.591 | 0.715 |

| 0.20 | 0.01 | 0.235 | 1.973 | 0.744 | 0.287 | 2.105 | 0.759 |

| 0.20 | 0.02 | 0.175 | 1.825 | 0.731 | 0.252 | 2.016 | 0.749 |

| 0.20 | 0.03 | 0.137 | 1.735 | 0.725 | 0.225 | 1.950 | 0.742 |

| 0.20 | 0.04 | 0.111 | 1.677 | 0.722 | 0.204 | 1.899 | 0.737 |

| 0.20 | 0.05 | 0.094 | 1.638 | 0.720 | 0.187 | 1.858 | 0.733 |

| 0.20 | 0.10 | 0.051 | 1.550 | 0.720 | 0.135 | 1.738 | 0.725 |

| 0.20 | 0.20 | 0.025 | 1.511 | 0.726 | 0.092 | 1.642 | 0.721 |

| 0.20 | 0.30 | 0.016 | 1.508 | 0.734 | 0.072 | 1.602 | 0.721 |

| 0.30 | 0.01 | 0.236 | 1.986 | 0.754 | 0.289 | 2.119 | 0.771 |

| 0.30 | 0.02 | 0.176 | 1.837 | 0.739 | 0.253 | 2.030 | 0.760 |

| 0.30 | 0.03 | 0.137 | 1.746 | 0.732 | 0.226 | 1.963 | 0.752 |

| 0.30 | 0.04 | 0.112 | 1.688 | 0.729 | 0.205 | 1.912 | 0.746 |

| 0.30 | 0.05 | 0.094 | 1.648 | 0.727 | 0.188 | 1.871 | 0.742 |

| 0.30 | 0.10 | 0.052 | 1.560 | 0.726 | 0.136 | 1.750 | 0.732 |

| 0.30 | 0.20 | 0.026 | 1.520 | 0.732 | 0.092 | 1.654 | 0.728 |

| 0.30 | 0.30 | 0.017 | 1.516 | 0.741 | 0.073 | 1.614 | 0.728 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.208 | 2.460 | 0.713 | 0.185 | 2.386 | 0.711 | 0.189 | 2.399 | 0.711 |

| 0.20 | 0.20 | 0.185 | 2.378 | 0.714 | 0.141 | 2.237 | 0.710 | 0.149 | 2.260 | 0.711 |

| 0.30 | 0.30 | 0.178 | 2.354 | 0.718 | 0.114 | 2.146 | 0.711 | 0.126 | 2.181 | 0.712 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.192 | 2.409 | 0.711 | 0.262 | 2.666 | 0.721 |

| 0.10 | 0.02 | 0.142 | 2.226 | 0.707 | 0.247 | 2.609 | 0.718 |

| 0.10 | 0.03 | 0.111 | 2.114 | 0.705 | 0.233 | 2.560 | 0.716 |

| 0.10 | 0.04 | 0.090 | 2.041 | 0.705 | 0.221 | 2.516 | 0.715 |

| 0.10 | 0.05 | 0.075 | 1.991 | 0.705 | 0.211 | 2.478 | 0.713 |

| 0.10 | 0.10 | 0.042 | 1.878 | 0.708 | 0.172 | 2.338 | 0.709 |

| 0.10 | 0.20 | 0.022 | 1.820 | 0.716 | 0.129 | 2.183 | 0.706 |

| 0.10 | 0.30 | 0.015 | 1.805 | 0.725 | 0.105 | 2.101 | 0.706 |

| 0.20 | 0.01 | 0.193 | 2.417 | 0.715 | 0.263 | 2.676 | 0.726 |

| 0.20 | 0.02 | 0.142 | 2.230 | 0.710 | 0.247 | 2.619 | 0.723 |

| 0.20 | 0.03 | 0.110 | 2.116 | 0.708 | 0.234 | 2.569 | 0.721 |

| 0.20 | 0.04 | 0.089 | 2.041 | 0.707 | 0.222 | 2.525 | 0.719 |

| 0.20 | 0.05 | 0.074 | 1.991 | 0.707 | 0.211 | 2.486 | 0.717 |

| 0.20 | 0.10 | 0.040 | 1.878 | 0.710 | 0.172 | 2.342 | 0.712 |

| 0.20 | 0.20 | 0.021 | 1.821 | 0.719 | 0.128 | 2.184 | 0.709 |

| 0.20 | 0.30 | 0.014 | 1.807 | 0.729 | 0.104 | 2.100 | 0.708 |

| 0.30 | 0.01 | 0.193 | 2.424 | 0.719 | 0.264 | 2.687 | 0.732 |

| 0.30 | 0.02 | 0.141 | 2.234 | 0.713 | 0.248 | 2.629 | 0.729 |

| 0.30 | 0.03 | 0.109 | 2.118 | 0.711 | 0.235 | 2.578 | 0.726 |

| 0.30 | 0.04 | 0.088 | 2.043 | 0.710 | 0.223 | 2.533 | 0.724 |

| 0.30 | 0.05 | 0.073 | 1.991 | 0.710 | 0.212 | 2.494 | 0.722 |

| 0.30 | 0.10 | 0.039 | 1.878 | 0.713 | 0.172 | 2.347 | 0.716 |

| 0.30 | 0.20 | 0.020 | 1.823 | 0.722 | 0.127 | 2.186 | 0.711 |

| 0.30 | 0.30 | 0.014 | 1.809 | 0.733 | 0.103 | 2.099 | 0.710 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.243 | 1.638 | 0.748 | 0.206 | 1.606 | 0.740 | 0.221 | 1.616 | 0.743 |

| 0.20 | 0.20 | 0.201 | 1.576 | 0.744 | 0.131 | 1.518 | 0.731 | 0.158 | 1.536 | 0.736 |

| 0.30 | 0.30 | 0.194 | 1.559 | 0.750 | 0.091 | 1.475 | 0.731 | 0.131 | 1.501 | 0.739 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.352 | 1.791 | 0.784 | 0.428 | 1.905 | 0.822 |

| 0.10 | 0.02 | 0.263 | 1.661 | 0.750 | 0.376 | 1.829 | 0.795 |

| 0.10 | 0.03 | 0.207 | 1.583 | 0.736 | 0.337 | 1.772 | 0.778 |

| 0.10 | 0.04 | 0.169 | 1.532 | 0.729 | 0.305 | 1.728 | 0.766 |

| 0.10 | 0.05 | 0.142 | 1.497 | 0.726 | 0.280 | 1.694 | 0.757 |

| 0.10 | 0.10 | 0.079 | 1.421 | 0.728 | 0.203 | 1.590 | 0.737 |

| 0.10 | 0.20 | 0.042 | 1.381 | 0.746 | 0.138 | 1.507 | 0.729 |

| 0.10 | 0.30 | 0.028 | 1.368 | 0.767 | 0.109 | 1.471 | 0.731 |

| 0.20 | 0.01 | 0.352 | 1.790 | 0.784 | 0.428 | 1.905 | 0.822 |

| 0.20 | 0.02 | 0.263 | 1.661 | 0.750 | 0.376 | 1.829 | 0.795 |

| 0.20 | 0.03 | 0.207 | 1.582 | 0.736 | 0.336 | 1.772 | 0.778 |

| 0.20 | 0.04 | 0.169 | 1.532 | 0.729 | 0.305 | 1.728 | 0.766 |

| 0.20 | 0.05 | 0.142 | 1.497 | 0.726 | 0.280 | 1.694 | 0.757 |

| 0.20 | 0.10 | 0.079 | 1.421 | 0.728 | 0.203 | 1.590 | 0.737 |

| 0.20 | 0.20 | 0.042 | 1.380 | 0.746 | 0.138 | 1.507 | 0.729 |

| 0.20 | 0.30 | 0.028 | 1.368 | 0.767 | 0.109 | 1.471 | 0.731 |

| 0.30 | 0.01 | 0.352 | 1.790 | 0.784 | 0.428 | 1.905 | 0.822 |

| 0.30 | 0.02 | 0.263 | 1.661 | 0.750 | 0.376 | 1.829 | 0.795 |

| 0.30 | 0.03 | 0.207 | 1.582 | 0.736 | 0.336 | 1.772 | 0.778 |

| 0.30 | 0.04 | 0.169 | 1.532 | 0.729 | 0.305 | 1.728 | 0.766 |

| 0.30 | 0.05 | 0.142 | 1.497 | 0.726 | 0.280 | 1.694 | 0.757 |

| 0.30 | 0.10 | 0.079 | 1.420 | 0.728 | 0.203 | 1.590 | 0.737 |

| 0.30 | 0.20 | 0.042 | 1.380 | 0.746 | 0.138 | 1.507 | 0.729 |

| 0.30 | 0.30 | 0.028 | 1.367 | 0.767 | 0.109 | 1.471 | 0.731 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.234 | 2.439 | 0.738 | 0.208 | 2.367 | 0.732 | 0.213 | 2.380 | 0.733 |

| 0.20 | 0.20 | 0.210 | 2.358 | 0.735 | 0.161 | 2.222 | 0.726 | 0.169 | 2.245 | 0.728 |

| 0.30 | 0.30 | 0.207 | 2.339 | 0.740 | 0.133 | 2.138 | 0.725 | 0.146 | 2.172 | 0.728 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.217 | 2.391 | 0.732 | 0.296 | 2.643 | 0.756 |

| 0.10 | 0.02 | 0.160 | 2.211 | 0.721 | 0.278 | 2.587 | 0.750 |

| 0.10 | 0.03 | 0.125 | 2.101 | 0.717 | 0.263 | 2.538 | 0.745 |

| 0.10 | 0.04 | 0.101 | 2.029 | 0.716 | 0.249 | 2.495 | 0.741 |

| 0.10 | 0.05 | 0.085 | 1.979 | 0.717 | 0.237 | 2.458 | 0.738 |

| 0.10 | 0.10 | 0.046 | 1.865 | 0.724 | 0.194 | 2.320 | 0.728 |

| 0.10 | 0.20 | 0.023 | 1.800 | 0.743 | 0.145 | 2.169 | 0.721 |

| 0.10 | 0.30 | 0.015 | 1.777 | 0.765 | 0.119 | 2.088 | 0.720 |

| 0.20 | 0.01 | 0.217 | 2.391 | 0.732 | 0.296 | 2.643 | 0.756 |

| 0.20 | 0.02 | 0.160 | 2.212 | 0.721 | 0.278 | 2.587 | 0.750 |

| 0.20 | 0.03 | 0.125 | 2.102 | 0.717 | 0.263 | 2.538 | 0.745 |

| 0.20 | 0.04 | 0.101 | 2.029 | 0.716 | 0.249 | 2.495 | 0.741 |

| 0.20 | 0.05 | 0.085 | 1.979 | 0.717 | 0.237 | 2.458 | 0.738 |

| 0.20 | 0.10 | 0.046 | 1.865 | 0.724 | 0.194 | 2.320 | 0.728 |

| 0.20 | 0.20 | 0.023 | 1.800 | 0.743 | 0.145 | 2.169 | 0.721 |

| 0.20 | 0.30 | 0.015 | 1.777 | 0.765 | 0.119 | 2.088 | 0.720 |

| 0.30 | 0.01 | 0.217 | 2.390 | 0.732 | 0.296 | 2.643 | 0.756 |

| 0.30 | 0.02 | 0.160 | 2.211 | 0.721 | 0.278 | 2.587 | 0.750 |

| 0.30 | 0.03 | 0.125 | 2.101 | 0.717 | 0.263 | 2.538 | 0.745 |

| 0.30 | 0.04 | 0.101 | 2.029 | 0.716 | 0.249 | 2.495 | 0.741 |

| 0.30 | 0.05 | 0.085 | 1.979 | 0.717 | 0.237 | 2.457 | 0.738 |

| 0.30 | 0.10 | 0.046 | 1.865 | 0.724 | 0.194 | 2.320 | 0.728 |

| 0.30 | 0.20 | 0.023 | 1.800 | 0.743 | 0.145 | 2.169 | 0.721 |

| 0.30 | 0.30 | 0.015 | 1.777 | 0.765 | 0.119 | 2.088 | 0.720 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.348 | 2.216 | 0.800 | 0.313 | 2.142 | 0.791 | 0.331 | 2.180 | 0.795 |

| 0.20 | 0.20 | 0.359 | 2.254 | 0.820 | 0.289 | 2.101 | 0.799 | 0.326 | 2.182 | 0.810 |

| 0.30 | 0.30 | 0.375 | 2.309 | 0.846 | 0.268 | 2.073 | 0.809 | 0.326 | 2.203 | 0.831 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.249 | 1.937 | 0.760 | 0.306 | 2.106 | 0.781 |

| 0.10 | 0.02 | 0.195 | 1.779 | 0.744 | 0.289 | 2.056 | 0.775 |

| 0.10 | 0.03 | 0.156 | 1.667 | 0.736 | 0.275 | 2.013 | 0.769 |

| 0.10 | 0.04 | 0.128 | 1.587 | 0.731 | 0.262 | 1.975 | 0.764 |

| 0.10 | 0.05 | 0.108 | 1.528 | 0.728 | 0.250 | 1.942 | 0.761 |

| 0.10 | 0.10 | 0.059 | 1.389 | 0.724 | 0.208 | 1.821 | 0.748 |

| 0.10 | 0.20 | 0.032 | 1.322 | 0.727 | 0.164 | 1.691 | 0.740 |

| 0.10 | 0.30 | 0.023 | 1.309 | 0.732 | 0.141 | 1.626 | 0.738 |

| 0.20 | 0.01 | 0.243 | 1.935 | 0.769 | 0.300 | 2.101 | 0.792 |

| 0.20 | 0.02 | 0.190 | 1.778 | 0.753 | 0.283 | 2.052 | 0.785 |

| 0.20 | 0.03 | 0.152 | 1.668 | 0.744 | 0.269 | 2.009 | 0.779 |

| 0.20 | 0.04 | 0.125 | 1.589 | 0.739 | 0.256 | 1.972 | 0.774 |

| 0.20 | 0.05 | 0.105 | 1.532 | 0.736 | 0.244 | 1.939 | 0.770 |

| 0.20 | 0.10 | 0.057 | 1.396 | 0.732 | 0.203 | 1.819 | 0.757 |

| 0.20 | 0.20 | 0.030 | 1.331 | 0.735 | 0.160 | 1.694 | 0.748 |

| 0.20 | 0.30 | 0.021 | 1.318 | 0.741 | 0.137 | 1.631 | 0.747 |

| 0.30 | 0.01 | 0.240 | 1.938 | 0.779 | 0.296 | 2.104 | 0.803 |

| 0.30 | 0.02 | 0.187 | 1.783 | 0.762 | 0.279 | 2.054 | 0.795 |

| 0.30 | 0.03 | 0.149 | 1.674 | 0.753 | 0.265 | 2.012 | 0.789 |

| 0.30 | 0.04 | 0.122 | 1.596 | 0.748 | 0.252 | 1.975 | 0.784 |

| 0.30 | 0.05 | 0.103 | 1.540 | 0.745 | 0.241 | 1.942 | 0.780 |

| 0.30 | 0.10 | 0.056 | 1.407 | 0.741 | 0.200 | 1.824 | 0.767 |

| 0.30 | 0.20 | 0.030 | 1.343 | 0.745 | 0.157 | 1.701 | 0.758 |

| 0.30 | 0.30 | 0.021 | 1.330 | 0.751 | 0.135 | 1.639 | 0.757 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.285 | 2.718 | 0.732 | 0.258 | 2.631 | 0.729 | 0.264 | 2.649 | 0.729 |

| 0.20 | 0.20 | 0.300 | 2.773 | 0.743 | 0.245 | 2.591 | 0.734 | 0.257 | 2.630 | 0.736 |

| 0.30 | 0.30 | 0.318 | 2.838 | 0.757 | 0.233 | 2.554 | 0.740 | 0.252 | 2.619 | 0.745 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.202 | 2.403 | 0.716 | 0.264 | 2.647 | 0.727 |

| 0.10 | 0.02 | 0.155 | 2.220 | 0.710 | 0.256 | 2.615 | 0.725 |

| 0.10 | 0.03 | 0.124 | 2.096 | 0.708 | 0.248 | 2.586 | 0.724 |

| 0.10 | 0.04 | 0.101 | 2.008 | 0.707 | 0.241 | 2.559 | 0.723 |

| 0.10 | 0.05 | 0.085 | 1.944 | 0.706 | 0.235 | 2.534 | 0.722 |

| 0.10 | 0.10 | 0.046 | 1.799 | 0.708 | 0.210 | 2.434 | 0.718 |

| 0.10 | 0.20 | 0.025 | 1.730 | 0.714 | 0.177 | 2.302 | 0.714 |

| 0.10 | 0.30 | 0.018 | 1.716 | 0.722 | 0.156 | 2.221 | 0.713 |

| 0.20 | 0.01 | 0.200 | 2.401 | 0.719 | 0.261 | 2.643 | 0.730 |

| 0.20 | 0.02 | 0.153 | 2.219 | 0.714 | 0.253 | 2.611 | 0.729 |

| 0.20 | 0.03 | 0.122 | 2.095 | 0.711 | 0.246 | 2.582 | 0.728 |

| 0.20 | 0.04 | 0.099 | 2.007 | 0.710 | 0.239 | 2.555 | 0.726 |

| 0.20 | 0.05 | 0.083 | 1.944 | 0.709 | 0.232 | 2.531 | 0.725 |

| 0.20 | 0.10 | 0.045 | 1.802 | 0.711 | 0.207 | 2.430 | 0.721 |

| 0.20 | 0.20 | 0.024 | 1.735 | 0.718 | 0.174 | 2.297 | 0.717 |

| 0.20 | 0.30 | 0.017 | 1.721 | 0.727 | 0.153 | 2.215 | 0.716 |

| 0.30 | 0.01 | 0.197 | 2.398 | 0.724 | 0.258 | 2.637 | 0.735 |

| 0.30 | 0.02 | 0.151 | 2.218 | 0.717 | 0.250 | 2.606 | 0.734 |

| 0.30 | 0.03 | 0.120 | 2.095 | 0.715 | 0.243 | 2.577 | 0.732 |

| 0.30 | 0.04 | 0.098 | 2.008 | 0.713 | 0.236 | 2.551 | 0.731 |

| 0.30 | 0.05 | 0.082 | 1.945 | 0.713 | 0.230 | 2.526 | 0.730 |

| 0.30 | 0.10 | 0.044 | 1.804 | 0.715 | 0.204 | 2.426 | 0.726 |

| 0.30 | 0.20 | 0.024 | 1.740 | 0.723 | 0.171 | 2.293 | 0.721 |

| 0.30 | 0.30 | 0.017 | 1.727 | 0.733 | 0.150 | 2.211 | 0.720 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.527 | 2.018 | 1.012 | 0.476 | 1.968 | 0.986 | 0.502 | 1.994 | 1.000 |

| 0.20 | 0.20 | 0.556 | 2.050 | 1.042 | 0.450 | 1.945 | 0.986 | 0.506 | 2.001 | 1.017 |

| 0.30 | 0.30 | 0.588 | 2.087 | 1.075 | 0.424 | 1.924 | 0.986 | 0.514 | 2.015 | 1.040 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.376 | 1.747 | 0.881 | 0.464 | 1.923 | 0.955 |

| 0.10 | 0.02 | 0.293 | 1.580 | 0.825 | 0.438 | 1.870 | 0.932 |

| 0.10 | 0.03 | 0.234 | 1.461 | 0.794 | 0.416 | 1.824 | 0.913 |

| 0.10 | 0.04 | 0.192 | 1.377 | 0.776 | 0.396 | 1.784 | 0.897 |

| 0.10 | 0.05 | 0.160 | 1.314 | 0.765 | 0.378 | 1.748 | 0.884 |

| 0.10 | 0.10 | 0.085 | 1.166 | 0.747 | 0.314 | 1.617 | 0.840 |

| 0.10 | 0.20 | 0.043 | 1.087 | 0.755 | 0.245 | 1.474 | 0.807 |

| 0.10 | 0.30 | 0.029 | 1.062 | 0.772 | 0.209 | 1.396 | 0.797 |

| 0.20 | 0.01 | 0.376 | 1.747 | 0.881 | 0.464 | 1.923 | 0.955 |

| 0.20 | 0.02 | 0.293 | 1.580 | 0.825 | 0.438 | 1.870 | 0.932 |

| 0.20 | 0.03 | 0.234 | 1.461 | 0.794 | 0.416 | 1.824 | 0.913 |

| 0.20 | 0.04 | 0.192 | 1.376 | 0.776 | 0.396 | 1.784 | 0.897 |

| 0.20 | 0.05 | 0.160 | 1.314 | 0.765 | 0.378 | 1.748 | 0.884 |

| 0.20 | 0.10 | 0.085 | 1.166 | 0.747 | 0.314 | 1.617 | 0.840 |

| 0.20 | 0.20 | 0.043 | 1.087 | 0.755 | 0.245 | 1.474 | 0.807 |

| 0.20 | 0.30 | 0.029 | 1.062 | 0.772 | 0.209 | 1.396 | 0.797 |

| 0.30 | 0.01 | 0.376 | 1.746 | 0.881 | 0.464 | 1.923 | 0.955 |

| 0.30 | 0.02 | 0.293 | 1.579 | 0.825 | 0.438 | 1.870 | 0.932 |

| 0.30 | 0.03 | 0.234 | 1.461 | 0.794 | 0.416 | 1.824 | 0.913 |

| 0.30 | 0.04 | 0.192 | 1.376 | 0.776 | 0.396 | 1.784 | 0.897 |

| 0.30 | 0.05 | 0.160 | 1.314 | 0.765 | 0.378 | 1.748 | 0.884 |

| 0.30 | 0.10 | 0.085 | 1.166 | 0.747 | 0.314 | 1.617 | 0.840 |

| 0.30 | 0.20 | 0.043 | 1.087 | 0.755 | 0.245 | 1.474 | 0.807 |

| 0.30 | 0.30 | 0.029 | 1.062 | 0.772 | 0.209 | 1.396 | 0.797 |

| CR | SBA | SY | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.10 | 0.325 | 2.705 | 0.797 | 0.294 | 2.619 | 0.788 | 0.301 | 2.637 | 0.790 |

| 0.20 | 0.20 | 0.349 | 2.768 | 0.814 | 0.285 | 2.591 | 0.793 | 0.299 | 2.630 | 0.798 |

| 0.30 | 0.30 | 0.377 | 2.842 | 0.834 | 0.277 | 2.566 | 0.798 | 0.300 | 2.629 | 0.808 |

| TSB | HES | ||||||

|---|---|---|---|---|---|---|---|

| MASE | MMR | U2 | MASE | MMR | U2 | ||

| 0.10 | 0.01 | 0.229 | 2.391 | 0.753 | 0.301 | 2.636 | 0.783 |

| 0.10 | 0.02 | 0.176 | 2.208 | 0.737 | 0.291 | 2.604 | 0.778 |

| 0.10 | 0.03 | 0.139 | 2.082 | 0.730 | 0.282 | 2.574 | 0.775 |

| 0.10 | 0.04 | 0.113 | 1.993 | 0.726 | 0.274 | 2.547 | 0.772 |

| 0.10 | 0.05 | 0.094 | 1.928 | 0.725 | 0.267 | 2.522 | 0.769 |

| 0.10 | 0.10 | 0.049 | 1.774 | 0.727 | 0.238 | 2.422 | 0.758 |

| 0.10 | 0.20 | 0.024 | 1.692 | 0.744 | 0.201 | 2.288 | 0.748 |

| 0.10 | 0.30 | 0.016 | 1.666 | 0.765 | 0.177 | 2.203 | 0.744 |

| 0.20 | 0.01 | 0.229 | 2.391 | 0.753 | 0.301 | 2.636 | 0.782 |

| 0.20 | 0.02 | 0.176 | 2.208 | 0.737 | 0.291 | 2.604 | 0.778 |

| 0.20 | 0.03 | 0.139 | 2.082 | 0.730 | 0.282 | 2.574 | 0.775 |

| 0.20 | 0.04 | 0.113 | 1.993 | 0.726 | 0.274 | 2.547 | 0.771 |

| 0.20 | 0.05 | 0.095 | 1.928 | 0.725 | 0.267 | 2.522 | 0.769 |

| 0.20 | 0.10 | 0.049 | 1.774 | 0.727 | 0.238 | 2.422 | 0.758 |

| 0.20 | 0.20 | 0.024 | 1.692 | 0.744 | 0.201 | 2.288 | 0.748 |

| 0.20 | 0.30 | 0.016 | 1.666 | 0.765 | 0.177 | 2.203 | 0.744 |

| 0.30 | 0.01 | 0.229 | 2.391 | 0.753 | 0.301 | 2.636 | 0.782 |

| 0.30 | 0.02 | 0.176 | 2.208 | 0.737 | 0.291 | 2.604 | 0.778 |

| 0.30 | 0.03 | 0.139 | 2.082 | 0.730 | 0.282 | 2.574 | 0.775 |

| 0.30 | 0.04 | 0.113 | 1.993 | 0.726 | 0.274 | 2.547 | 0.771 |

| 0.30 | 0.05 | 0.094 | 1.928 | 0.725 | 0.267 | 2.522 | 0.769 |

| 0.30 | 0.10 | 0.049 | 1.774 | 0.727 | 0.238 | 2.422 | 0.758 |

| 0.30 | 0.20 | 0.024 | 1.692 | 0.744 | 0.201 | 2.288 | 0.748 |

| 0.30 | 0.30 | 0.016 | 1.666 | 0.765 | 0.177 | 2.203 | 0.744 |