The Network Improvement Problem for Equilibrium Routing††thanks: Supported in part by NSF Awards 1038578 and 1319745, an NSF CAREER Award (1254169), the Charles Lee Powell Foundation, and a Microsoft Research Faculty Fellowship.

Abstract

In routing games, agents pick their routes through a network to minimize their own delay. A primary concern for the network designer in routing games is the average agent delay at equilibrium. A number of methods to control this average delay have received substantial attention, including network tolls, Stackelberg routing, and edge removal.

A related approach with arguably greater practical relevance is that of making investments in improvements to the edges of the network, so that, for a given investment budget, the average delay at equilibrium in the improved network is minimized. This problem has received considerable attention in the literature on transportation research and a number of different algorithms have been studied. To our knowledge, none of this work gives guarantees on the output quality of any polynomial-time algorithm. We study a model for this problem introduced in transportation research literature, and present both hardness results and algorithms that obtain nearly optimal performance guarantees.

-

•

We first show that a simple algorithm obtains good approximation guarantees for the problem. Despite its simplicity, we show that for affine delays the approximation ratio of obtained by the algorithm cannot be improved.

-

•

To obtain better results, we then consider restricted topologies. For graphs consisting of parallel paths with affine delay functions we give an optimal algorithm. However, for graphs that consist of a series of parallel links, we show the problem is weakly NP-hard.

-

•

Finally, we consider the problem in series-parallel graphs, and give an FPTAS for this case.

Our work thus formalizes the intuition held by transportation researchers that the network improvement problem is hard, and presents topology-dependent algorithms that have provably tight approximation guarantees.

1 Introduction

Routing games are widely used to model and analyze networks where traffic is routed by multiple users, who typically pick their route to minimize their delay [26]. Routing games capture the uncoordinated nature of traffic routing. A prominent concern in the study of these games is the overall social cost, which is usually taken to be the average delay suffered by the players at equilibrium. It is well known that equilibria are generally suboptimal in terms of social cost. The ratio of the average delay of the worst equilibrium routing to the optimal routing that minimizes the average delay is called the price of anarchy; tight bounds on the price of anarchy are well-studied and are known for various classes of delay functions [21, Chapter 18].

However, the notion of price of anarchy assumes a fixed network. In reality, of course, networks change, and such changes may intentionally be implemented by the network designer to improve quality of service. This raises the question of how to identify cost-effective network improvements. Our work addresses this fundamental design problem. Specifically, given a budget for improving the network, how should the designer allocate the budget among edges of the network to minimize the average delay at equilibrium in the resulting, improved network? This crucial question arises frequently in network planning and expansion, and yet seems to have received no attention in the algorithmic game theory literature. This is surprising considering the attention given to other methods of improving equilibria, e.g., edge tolls and Stackelberg routing.

Our model of network improvement is adopted from a widely studied problem in transportation research [34] called the Continuous Network Design Problem (CNDP) [1]. In this model, each edge in the network has a delay function that gives the delay on the edge as a function of the traffic carried by the edge. Specifically, the delay function on each edge consists of a free-flow term (a constant), plus a congestion term that is the ratio of the traffic on the edge to the conductance of the edge, raised to a fixed power. The cost to the network designer of increasing the conductance of an edge by one unit is an edge-specific constant. Our objective is to select an allocation of the improvement budget to the edges that minimizes the social cost of equilibria in the improved network.

The continuous network design problem, along with the discrete network design problem that deals with the creation (rather than improvement) of edges, has been referred to as “one of the most difficult and challenging problems facing transport” [34]. The CNDP is generally formulated as a mathematical program with the budget allocated to each edge and the traffic at equilibrium as variables. Since the traffic is constrained to be at equilibrium, such a formulation is also called a Mathematical Program with Equilibrium Constraints (MPEC). Further, since the traffic at equilibrium is itself obtained as a solution to a optimization problem, this is also a bilevel optimization problems. Both bilevel optimization problems and MPECs have a number of other applications and have been studied independent of the CNDP as well (e.g., [7]).

Owing both to the rich structure of the problem and its practical relevance, the CNDP has received considerable attention in transportation research. Because of the nonconvexity and the complex nature of the constraints, the bulk of the literature focuses on heuristics, and proposed algorithms are evaluated by performance on test data rather than formal analysis. Many of these algorithms are surveyed in [34]. More recent papers give algorithms that obtain global optima [18, 19, 32], but make no guarantees on the quality of solutions that can be obtained in polynomial time.

In this paper, we consider a model with fixed demands, separable polynomial delay functions on the edges and constant improvement costs. This particular model, and further restrictions of it, have been the focus of considerable attention, e.g., [10, 13, 20], and is frequently used for test instances. The model captures many of the essential characteristics of the more general problems, such as the bilevel and nonconvex nature of the problem and the equilibrium constraints. Our work thus gives the first algorithmic results with proven output quality and runtime for the network improvement problem.

Our Contributions.

We first focus on general graphs, and show that a simple algorithm that relaxes equilibrium constraints on the flow gives an approximation guarantee that is tight for linear delays.

-

•

We show that for general networks with multiple sources and sinks and polynomial delays, a simple algorithm gives an -approximation to the optimal allocation, where is the maximum degree of the polynomial delay functions. If , this gives a -approximation algorithm.

-

•

We show that the approximation ratio for linear delays is tight, even for the single-commodity case: by a reduction similar to that used by Roughgarden [27], we show that it is NP-hard to obtain an approximation ratio better than .

The hardness result crucially depends on the generality of the network topology. The practical relevance of the network improvement problem then motivates us to consider restricted topologies of networks, for which we give both polynomial-time algorithms and further hardness results. We restrict ourselves to single source and sink networks for the following results.

-

•

In graphs consisting of parallel - paths with linear delays, we show that even though the problem is non-convex, first-order conditions are sufficient for optimality. We utilize this property and the special structure of the first-order conditions to give an optimal polynomial-time algorithm. If each path consists of a single edge, we give a particularly simple optimal algorithm.

-

•

In contrast to our previous hardness result, we show that even in graphs with linear delays and with very simple topologies consisting of a series of parallel links, called series-dipole graphs, obtaining the optimal allocation for a given investment budget is NP-hard.

-

•

Lastly, in series-parallel networks with polynomial delays, we show that there exists a fully-polynomial time approximation scheme. Our algorithm is based on discretizing simultaneously over the space of flows and allocations and showing there is a near-optimal flow and allocation in the discretized space which can be obtained efficiently for series-parallel networks. The discretized flow may not correspond to the equilibrium flow; however, in series-parallel graphs, we show that the delay at equilibrium is at most the delay of the discretized flow.

Our work thus presents a fairly comprehensive set of approximation guarantees for the problem of network improvement. We give tight bounds on the approximability of the problem in general networks, and optimal and near-optimal algorithms for restricted topologies. Further, we show that the problem is NP-hard — though weakly so — even in very restricted topologies. Our results thus supplement the work in transportation research on the problem, by formalizing the intuition that the problem is hard, and giving tight approximation algorithms for a number of cases.

2 Related Work

Routing games as a model of traffic on roads were introduced by Wardrop in 1952 [33]. Beckmann et al. [3] showed that equilibria in routing games are obtained as the solution to a strictly convex optimization problem if all delay functions are increasing, thus establishing the existence and uniqueness of equilibria. Wardrop’s model, and our work, focuses on nonatomic routing games where the traffic controlled by each player is infinitesimal. This is a good assumption for road traffic since an individual driver has negligible impact on the delay. However, many other models of traffic in routing games are studied as well. For example, in atomic games, players can control significant traffic; this traffic may be splittable (e.g., [14, 5]) or unsplittable (e.g., [23]), depending on whether a player may split her traffic among multiple routes.

The problem of obtaining formal bounds on the efficiency of equilibria in games was first studied by Koutsoupias and Papadimitriou [16]. The price of anarchy — the ratio of the social cost at the worst equilibrium routing to the social cost of an optimal routing — was later introduced by Papadimitriou [22] as a formal measure of inefficiency. For nonatomic routing games with the social cost given by the average delay, the price of anarchy is known to be 4/3 for linear delays [28], and for delay functions that are polynomials of degree [24].

Significant research has gone into the use of tolls to improve the efficiency of routing games. It is known that tolls corresponding to the marginal delay of an optimal flow induce the optimal flow as an equilibrium [3]. More generally, tolls to induce any minimal routing can be obtained as the solution to a linear program [8, 15, 35]. A similar result for atomic splittable routing games was shown independently by Swamy [31] and Yang and Zhang [36]. These results compute efficiency without adding tolls to the delay of the players, and hence disregard the effect of tolls on the utility of the players in this computation. If tolls are added to the delays in the computation of efficiency, then even for linear delays, it is NP-hard to obtain tolls that give better than a 4/3-approximation [6]. Since a 4/3-approximation can be obtained by not applying any tolls, this result says that it is NP-hard to find improving tolls.

Motivated by Braess’s paradox, where removal of an edge improves the efficiency of the equilibrium routing, Roughgarden [27] studies the problem of removing edges from a network to minimize the delay at equilibrium in the resulting network. The problem is strongly NP-hard, and there is no algorithm with an approximation ratio better than for general delay functions. Another method studied for improving the efficiency of routing is Stackelberg routing, which assumes that a fraction of the traffic is centrally controlled and is routed to improve efficiency. Obtaining the optimal Stackelberg routing is NP-hard even in parallel links [25], although a fully-polynomial time approximation scheme is known for this case [17].

The importance of the network improvement problem has caused it to receive significant attention in transportation research, where the version we are considering is known as the continuous network design problem’. Early research focused on heuristics that did not give any guarantees about the quality of the solution obtained. These were based on sensitivity analysis of the variational inequality to implement gradient-descent [11], as well as derivative-free algorithms [1]. For a survey of other algorithms and early results on the continuous network design problem, see [34].

More recent work in the transportation literature has also tried to obtain algorithms that obtain global minima for the continuous network design problem. Early approaches include the use of simulated annealing [10] and genetic algorithms [38]. Li et al. [18] reduce the problem to a sequence of mathematical programs with concave objectives and convex constraints, and show that the accumulation point of the sequence of solutions is a global optimum. If the sequence is terminated early, they show weak bounds on the quality of the solution that are consequential only under strong assumptions on the delay function and agents’ demands. Wang and Lo [32] reformulate the problem as a mixed integer linear program (MILP) by replacing the equilibrium constraints by constraints containing binary variables for each path, and using a number of linear segments to approximate the delay functions. This approach was further developed by Luathep et al. [19] who replaced the possibly exponentially many path variables by edge variables and gave a cutting constraint algorithm for the resulting MILP. The last two methods were shown to converge to a global optimum of the linearized approximation in finite time, but require solving a MILP with a possibly exponential number of variables and constraints.

A variant of the problem where the initial conductance of every edge in the network is zero, and the budget is part of the objective rather than a hard constraint, is studied by Marcotte [20] and, independent of our work, by Gairing et al. [12]. Unlike the work cited earlier, these papers give provable guarantees on the performance of polynomial-time algorithms. Marcotte gives an algorithm that is a 2-approximation for monomial delay functions and a -approximation for linear delay functions. Gairing et al. present an algorithm that improves upon these upper bounds, give an optimal polynomial-time algorithm for single-commodity instances, and show that the problem is APX-hard in general. In our problem, the budget is a hard constraint, and edges may have arbitrary initial capacities. Our problem is demonstrably harder than this variant: e.g., in contrast to the polynomial-time algorithm for single-commodity instances given by Gairing et al. [12], we show that in our problem no approximation better than is possible even in single-commodity instances.

3 Notation and Preliminaries

is a directed graph with and . If is a two-terminal graph, then it has two special vertices and called the source and the sink, collectively called the terminals. A - path is a sequence of edges with , and edges . In a two-terminal graph, each edge lies on an - path, and we use to denote the set of all - paths. Given vertices , in graph , vector is an - flow of value if the following conditions are satisfied:

We use to denote the value of flow . A path decomposition of an - flow is a set of flows along - paths that satisfies , . A path decomposition for flow so that for at most paths can be obtained in polynomial time [2]. Without reference to a path decomposition, we use to indicate that for all .

Each edge has an increasing delay function that gives the delay on the edge as a function of the flow on the edge. For flow and path , is the delay on path . Further, is the total delay on edge , and the total delay of flow is .

Routing games.

A routing game is a tuple where is a directed graph, is a vector of delay functions on edges, and is a set of triples where is the total traffic routed by players of commodity from to . Each player of commodity in a routing game controls infinitesimal traffic and picks an - path on which to route her flow, as her strategy. The strategies induce a flow . Let , then the delay of a player that selects path as her strategy is . In the single-commodity case, . We say a flow is a valid flow for routing game if where each is an - flow of value .

At equilibrium in a routing game, each player minimizes her delay, subject to the strategies of the other players. The equilibrium in a routing game is also called a Wardrop equilibrium.

Definition 1.

A set of flows where is an - flow of value is a Wardrop equilibrium if for all , for any - paths , such that , .

We use equilibrium flow to refer to the set of flows that form a Wardrop equilibrium. The equilibrium flow is also obtained as the solution to the following mathematical program. Since the delay functions are increasing, the program has a strictly convex objective with linear constraints, and hence the first-order conditions are necessary and sufficient for optimality. Further, because of strict convexity, the equilibrium flow is unique.

Network Improvement.

In the network improvement problem, we are given a routing game , where the delay function on each edge is of the form . We call the conductance, the resistance, and the length of edge . We assume and , and hence the delay is an increasing function of the flow on the edge. The delay function on an edge is affine if . Each edge has a marginal cost of improvement, . Upon spending to improve edge , the conductance of the edge increases to . For a given budget , a valid allocation is a vector so that and for each . The objective is to determine a valid allocation of the budget to the edges to minimize the average delay obtained at equilibrium with the modified delay functions . Delay functions are affine if on all edges.

Let be the vector of edge allocations. Since the flow at equilibrium is unique, for any , the average delay at equilibrium is unique. is this unique average delay as a function of the edge allocations. When considering a flow other than the equilibrium flow, we use to denote the average delay of flow with the modified delay functions. We will also have occasion to allocate budget to units other than edges, e.g., paths, and will slightly abuse notation to express the average delay in terms of these units.

Our problem corresponds to the following (non-linear, possibly non-convex) optimization problem:

| (1) |

We use to denote an optimal solution for this problem, and define . As is common in nonlinear optimization, instead of an exact solution we will obtain a solution that is within a specified additive tolerance of of the exact solution, i.e., a valid allocation so that . An algorithm is polynomial-time if it obtains such a solution in time polynomial in the input size and . Since the problem has linear constraints, the first-order conditions are necessary for optimality (e.g., [37]). By the first-order conditions for optimality, for any edges and ,

| (2) |

For any edge and allocation , define . For a path , as the length of path . For affine delay functions, define as the conductance of path , and the resistance of path as the reciprocal of the conductance: . For , . The following statement is easily verified; it is used often in our proofs, hence we state it formally below for ease of reference.

Fact 2.

For , , and ,

4 Tight Bounds in General Graphs

4.1 Simple approximation algorithms for general graphs

We start with a simple polynomial-time algorithm that gives a good approximation for the general network improvement problem: with multiple sources and sinks, in general graphs, and with polynomial delay functions. The algorithm follows from the observation that relaxing the equilibrium constraints on the flow yields a convex problem. Although the algorithm described here is a very natural one and lower bounds for its performance were given in [20], the upper bounds shown here appear not to have been noticed earlier. In fact, in the next section we will show that the bound obtained by this simple algorithm is tight in the case of affine delay functions.

Consider the following problem:

It is obvious the constraints for COPT are convex. We now show that if the delay functions are polynomial, then the objective is a convex function as well.

Lemma 3.

The objective function for COPT with polynomial delays is convex.

Proof.

We will show that the Hessian for each term in the summation in the objective is positive semi-definite. This will show that each individual term is convex, and hence the objective is convex as well. Each term in the summation is of the form

We will show that is a convex function for the proof. The following derivatives are easily obtained:

| (3) | |||

| (4) | |||

| (5) |

The Hessian for function is given by

For any vector we will show that , which proves the positive semi-definiteness of and hence the convexity of . By the expressions from (3), (4) and (5),

∎

The solution to problem COPT can thus be obtained in polynomial time. Our approximation algorithm then simply returns the allocation obtained by solving COPT.

Lemma 4.

If the delay function on every edge is affine, then the delay obtained at equilibrium for the allocation is a -approximation to the delay at equilibrium for the optimal allocation . In general if all delay functions are polynomials of degree at most , then the delay obtained at equilibrium for is an -approximation to the delay at equilibrium for the optimal allocation .

Proof.

Let be the equilibrium flow obtained for the optimal allocation , and let be the equilibrium flow for allocation . It is obvious that . For fixed affine delays, it is well-known that the total delay of the equilibrium routing is at most that of the the flow that minimizes the total delay [28]. Thus, . The statement of the lemma for affine delays follows. Further, the statement for general polynomial delays follows since the total delay of the equilibrium routing is known to be at most that of the the flow that minimizes the total delay [24]. ∎

4.2 A nearly tight lower bound for affine delays

We now show that the upper bounds obtained in the previous section are tight for affine delays, even for single-commodity routing games. We give a reduction from the problem of 2-Directed Disjoint Paths, which is known to be NP-complete [9]:

Definition 5 (2-Directed Disjoint Paths (2DDP)).

Given a directed graph and vertices , , and , do there exist - paths such that and are vertex-disjoint?

Note that the 2DDP problem is known to be solvable in polynomial-time if the graph is acyclic [30] or planar [29]. Our reduction is essentially identical to that given by Roughgarden [27] for the problem of removing edges from a network to improve the total delay at equilibrium in the resulting network.

In our reduction, we allow the budget to be unbounded. We modify the graph for the 2DDP problem by adding vertices , and edges , , and . For all edges except the ones added, we choose , and . Thus none of these edges cannot be used at equilibrium unless it is given a strictly positive allocation. For edges and , we choose , , and . For edges and , we choose , and ; thus any allocation to these edges does not affect the delay function. The demand between and is 1.

We now show that if the given instance of 2DDP contains two disjoint paths, then there exists an allocation that yields two vertex-disjoint - paths with delay functions on both, and thus an average delay of . If two vertex-disjoint paths do not exist, any allocation has average delay at least because the existence of a common vertex leads to inefficient routing, similar to that in the Braess graph.

Lemma 6.

If contains two disjoint paths, then there is an allocation for the CNDP instance constructed with average delay , otherwise any allocation has average delay at least .

Proof.

If there exist two disjoint paths, we allocate infinite budgets to exactly the edges on these paths, thus reducing the delay functions on these edges to zero. We additionally allocate infinite budgets to edges and . Then the flow that routes on the --- path and on the --- path is an equilibrium flow of average delay .

Suppose for a contradiction that there do not exist two disjoint paths but the average delay at equilibrium for an allocation is less than . Let be the subset of edges which carry strictly positive flow at equilibrium. Then must contain an - path, as well as an - path. To see this, note that cannot contain an --- path, since the delay on this path would be at least 2. However, both and must carry positive flow. Therefore, there must be an - path and an - path in . Since these paths cannot be vertex-disjoint, let be the common vertex. Then any - path in must have delay at least 1, and any - path must similarly have delay at least 1. Hence the delay at equilibrium must be at least 2. ∎

5 Single and Parallel Paths

5.1 Single Paths

We first consider the case where is a simple - path. In this case, we show that the delay at equilibrium is a convex function. Thus, obtaining the optimal allocation requires minimizing a convex function subject to linear constraints, which can be done in polynomial time by, e.g., interior-point methods [4].

Lemma 7.

If is an - path, then is convex.

Proof.

For an - path , the delay at equilibrium for an allocation is . Since and are fixed, minimizing is equivalent to minimizing , which is a convex function, since each is an affine function. ∎

5.2 Parallel Paths

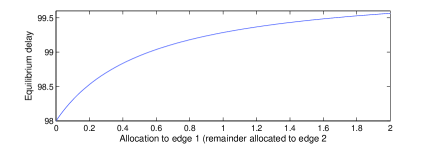

When consists of parallel paths between and , may not be a convex function of , and Figure 2 gives an example of this nonconvexity. The graph shows the delay at equilibrium as the allocation to edge 1 is increased and allocation to edge 2 is decreased, keeping the total allocation equal to the budget . We will show that for network improvement, the first-order conditions for optimality are sufficient. Hence, any solution that satisfies the first-order optimality conditions is a global minimum. We will then use this characterization to give a continuous greedy-like algorithm that uses the particular structure of the first-order optimality conditions to obtain an allocation.

\psfrag{l1}{$10x+90$}\psfrag{p1}{$\mu_{1}=1$}\psfrag{l2}{$5x$}\psfrag{p2}{$\mu_{2}=0.1$}\psfrag{d}{$d=40$}\includegraphics[scale={0.2}]{nonconvex1}

Assume the given graph consists of - paths. As before, is the set of all - paths. We relabel paths so that where is the length of path , and for simplicity, we assume that all these inequalities are strict (the case where some inequalities are not strict requires only minor modifications to the algorithm and analysis but requires tedious notation). Here, we assume that the equilibrium flow obtained for the optimal allocation , and hence by definition of the equilibrium flow all paths must carry positive flow at equilibrium. Relaxing the assumption requires us to solve the problem multiple times for increasing subsets of , and we leave this to the appendix.

By Section 5.1, we know how to maximize the conductance of any path for a fixed budget. Hence in the case of parallel paths, we will focus on obtaining an allocation to paths, rather than individual edges on paths, and assume that once the optimal allocation to paths is known, we can compute the allocation to the edges. We use to denote the (scalar) allocation to path , to denote the vector of allocations to paths, and use to denote the maximum conductance of path obtained for allocation .

We first establish the concavity of path conductance.111Note that is a convex function, since each is convex. However, this does not imply that is concave, since the reciprocal of a convex function is not necessarily concave, even in the single variable case. For example, both and are convex for .

Lemma 8.

For any path , let and be two vectors of allocations to edges in path and define for and . Then

-

1.

is concave.

-

2.

If is not strictly concave at some , then is linear for all .

Proof.

We will find it more convenient in the proof to work with resistances rather than conductances, where and for each edge , . Then

and differentiating again,

| (6) |

We will use Cauchy-Schwarz and the expression for to show that the expression on the right is nonpositive, which will complete the proof of the lemma. For any edge , is a linear function of , and hence . Equation (6) holds for edges as well as paths, and hence

| (7) |

To use Cauchy-Schwarz, define

Since ,

| (8) |

where the inequality is by Cauchy-Schwarz and the second equality follows since from (7). Replacing in (6), we get the proof of the first part of the lemma.

For the second part of the proof, assume that is not strictly concave at , i.e., . Then the inequality in (8) must be an equality, which again by Cauchy-Schwarz is possible if and only if the vectors and are parallel, i.e., for all and some constant . Thus , or from (7),

where . Since , this is equivalent to

| (9) |

We will show now that the vectors and are parallel for all . Hence the inequality in (8) is always an equality, and for all .

For any , since is a linear function,

where the second equality follows from (9). Thus the vectors and are parallel, and hence for all . ∎

The following corollary immediately follows from the first part of the lemma.

Corollary 9.

For any path and vector of allocations to the edges of , is concave.

We now obtain an expression for the delay at equilibrium. For an allocation , let be the flow at equilibrium and be the unique flow decomposition. Then iff . Since , for each path , by definition of equilibria,

| (10) |

Multiplying both sides by , and summing over all paths yields

| (11) |

We now show that if , the first order conditions for optimality are also sufficient.

Lemma 10.

Let and be two valid allocations where satisfies the first-order conditions for optimality, and define and . Then either for all , or there is a valid allocation so that .

Proof.

Our proof proceeds by considering all stationary points in . We will show that if for all , then either any stationary point is a minima, or is constant in the interval . In the former case, since there are no maxima, and maxima and minima must alternate, is the only minima in , and hence in either case, for all .

Let be a stationary point. Then . We first show that , and hence there are no maxima. From (21), and since is a function of rather than , for any path ,

and hence, by the chain rule,

| (12) |

Define to be the term in parentheses in (12); then . Note that if and only if , and hence . Further, for the second derivative, we get

and since ,

| (14) |

We will now show that is nondecreasing, and hence any stationary point cannot be a maxima. Each term in the summation for is the product of and . By assumption, , hence is constant and negative. By Corollary 9, the second term is nonincreasing, hence the product is nondecreasing. Each of the summands is nondecreasing, and hence must be nondecreasing.

Further, if , then must be a constant by (14). Since each summand is nondecreasing, each summand must in fact be constant, and in particular must be constant, i.e., must be linear. However, in this case, by the second part of Lemma 8, is linear for . Hence the second derivative is zero in , which by integration, and since , forces the first derivative to be zero in ; hence, is constant in . ∎

An optimal algorithm.

We now describe an algorithm for minimizing the delay at equilibrium on parallel paths. In order to describe our algorithm to optimize , we first show that is a strictly monotone function of the budget to be allocated. That is, the value is a strict monotone function of the budget . Note that since on every edge , is strictly monotone. Hence for every path , is strictly monotone as well.

Claim 11.

If , then is strictly decreasing in .

We first show the following claim.

Claim 12.

Let , be two vectors of allocations to paths in so that for all and the inequality strict for some . Then if , then .

Proof.

The proof follows from the observation that for every , with the inequality strict for at least one path. If , the claim is true since by assumption. Otherwise,

where the inequality follows from Fact 2 and since for all . ∎

Proof of Claim 11. Let , with , and let be the allocation that minimizes subject to the total allocation being at most . Then consider the allocation where , and on the other paths. By Claim 12, . Since is a valid allocation for budget , , and the claim follows. ∎

We now describe our algorithm. The algorithm proceeds by conducting a binary search for the optimal value . Initially, and are our lower and upper bounds, and .

-

1.

Let be the initial allocation.

-

2.

Increase the allocation to paths in so that for any path , if , then

(15) for all paths . Continue allocating in this manner until . Note that by Claim 12, is strictly decreasing in , hence any process that monotonically increases allocations to paths will obtain as long as .

-

3.

Let , where is the allocation obtained in Step 2. If , then is the optimal allocation for budget and . If , then , and otherwise.

Step 2 in the algorithm can be implemented by binary search; we give details on the implementation in the Appendix. To show that the algorithm works, we now prove the correctness of Step 3. We start with the following claim about the allocation obtained when Step 2 completes.

Claim 13.

Let . Then the allocation minimizes for budget , i.e., .

Proof.

The solution obtained satisfies

for all with . Since , and , this condition is equivalent to

for all with , which are exactly the first order conditions for minimizing . Then by Lemma 10, must minimize for budget . ∎

It follows from the claim that if , then is the optimal allocation for for budget . If , note that by Claim 11, is strictly monotone in , and hence , and similarly if , then . This proves the correctness of Step 3.

5.3 A simple algorithm for parallel links

We now consider the case where is a dipole graph, i.e., parallel edges between and . In contrast to the algorithm for the more general parallel paths case in Section 5.2, we show that a very simple algorithm gives the optimal allocation in this case. We prove that there always exists an optimal solution where the entire budget is spent on a single edge. The algorithm for obtaining the optimal allocation is then straightforward: consider each edge in turn, and compute the delay at equilibrium obtained by allocating the entire budget to that edge. The optimal allocation is to allocate the budget to the edge for which the delay obtained is minimum.

As before, we assume every edge has flow at equilibrium in every valid allocation. From (10),

| (16) |

From the first-order conditions of optimality for (1), it follows that for an optimal allocation, (2) must hold. We show that if two edges have positive allocation in an optimal allocation , then decreasing the allocation on one edge and increasing it on the other does not affect the delay at equilibrium. For , let be the allocation obtained by increasing the allocation to by and decreasing the allocation to by .

Lemma 14.

If , then .

We will use the expression for the delay at equilibrium in the following proof, obtained from (16) as

| (17) |

Proof.

Since , from (17),

or, with some algebraic manipulation,

| (18) |

Since in , the allocation to is increased and the allocation to is decreased by ,

| (19) |

The following corollary is obtained since we can start with any optimal allocation that allocates to more than a single edge and by Lemma 14 successively shift allocation onto a single edge so that we are left with an allocation on a single edge that yields the optimal delay at equilibrium.

Corollary 15.

There exists an optimal allocation where the entire budget is allocated to a single edge.

Proof.

Consider an optimal allocation of the budget to edges and edges , with strictly positive allocation. Consider the modified allocation : for ; , and . Then is a valid allocation, and since , , by the first-order conditions for optimality. Then by the lemma, . Thus, is an optimal allocation where exactly edges have strictly positive allocation, and successively removing edges from the optimal allocation in this manner gives us the corollary. ∎

Thus, the simple algorithm given earlier that allocates the entire budget to a single edge is optimal.

6 NP-Hardness in Series-Dipole Graphs

In contrast to the previous section, we show that even in fairly simple networks called series-dipole networks, the network improvement problem is NP-hard. A series-dipole graph consists of a number of subgraphs consisting of parallel edges (called dipole graphs) connected in series. In fact, we show that even when each dipole consists of just two edges, computing the optimal allocation is NP-hard. We will use to denote the number of dipoles in the graph.

The delay at equilibrium in a series-dipole graph is the sum of delays on the individual dipoles. Further, given an allocation of the budget to dipoles rather than individual edges, by Corollary 15 the optimal allocation to the edges can be determined by independently finding the edge in each dipole that minimizes the delay on the dipole on being allocated the entire budget for the dipole. Hence in this section we consider allocations to dipoles rather than individual edges, and define an allocation . Allocation is valid if and all . Further, define as the optimal delay in dipole on being allocated . Thus .

We show that the problem of network improvement is NP-hard by a reduction from partition.

Definition 16 (Partition).

Given items where item has value and , select a subset of the items so that .

For the th dipole consisting of edges and , the values for the parameters in our construction are as follows. Let and . Then

Claim 17.

For the instance constructed, there exists an allocation for the th dipole so that, for any allocation , , with equality if and only if or .

Proof.

Fix a dipole . Let and , , , , , and be the parameters given above. Since each dipole consists of two parallel edges, by Corollary 15, we only need to consider allocations to a single edge. Since , if then both edges carry flow at equilibrium, otherwise only edge has positive flow. Hence, from (11),

Define the following functions:

By definition, then . Define and . We will show the following properties for these functions:

-

1.

, with equality if and only if .

-

2.

, with equality if and only if .

-

3.

.

The proof of the claim then follows from these properties, and from definition of .

Proof of (1). The proof proceeds by showing that is a strictly convex function for , and then showing that the function is minimized at and . For convenience, we differentiate , yielding

It is obvious that the expression on the right is strictly increasing in , and hence is strictly convex. Setting the derivative to be zero gives

Replacing values for the parameters,

where the second and third equalities are obtained by replacing the values for and respectively. We now evaluate to obtain

Thus, is minimized at , and . Since is strictly convex for , for and .

Proof of (2). Our proof is very similar to the proof for . We observe that is strictly convex for . We show that is minimized at , and that . By strict convexity, for and , completing the proof.

Differentiate gives us

Again, the expression on the right is strictly increasing, and hence is strictly convex. Setting the derivative to be zero gives

We evaluate to obtain

This completes the proof for (2).

Proof of (3). We show that the minimum value of is strictly larger than . Differentiating ,

and hence, is minimized when

Let denote this value that minimizes . Then

∎

We choose our budget . Claim 17 is illustrated in Figure 3, which depicts the optimal delay at equilibrium in dipole as a function of the allocation to the dipole. By Corollary 15, for a single dipole it is always optimal to assign the entire budget to a single edge. Further, from (16) and the first-order conditions for optimality it can be obtained that the budgets for which it is optimal to assign to a fixed edge form a continuous interval, and the delay at equilibrium as a function of the allocation is convex in these intervals. This is depicted by the two convex portions of the curve in Figure 3. Our proof of hardness is based on observing that our construction from Claim 17 puts the entire curve above the line except at points and where the curve is tangent to the line.

Lemma 18.

The optimal delay for the constructed instance and the given budget is if and only if the given instance of partition has a solution.

Proof.

For any allocation , the delay obtained at equilibrium is the sum of the dipoles. Thus . By Claim 17, . Since , . We will show that this lower bound is achieved if and only if the instance of partition has a solution.

Suppose the instance has a solution . Then for the network improvement instance, allocate to each dipole , and to each dipole . For this allocation, by the claim,

completing the proof in this direction. For the other direction, suppose the instance of network improvement has an allocation that achieves the lower bound. Then the inequality in Claim 17 must hold with equality for each dipole. Hence for each dipole, either , or . Let be the set of dipoles with the latter allocation. Then

where the first equality is by Claim 17 and the second equality is because the allocation achieves the lower bound in the lemma. It follows immediately that , and hence is a solution to the partition instance. ∎

7 An FPTAS for Series-Parallel Graphs

In the previous section, we have shown that even for limited network topologies, obtaining the optimal allocation is weakly NP-hard, and thus these topologies are unlikely to have optimal polynomial time algorithms. We now show that for a large class of graphs with a single source and sink, we can obtain in polynomial time near-optimal algorithms for network improvement. Specifically, we present an FPTAS222A fully polynomial-time approximation scheme (FPTAS) is a sequence of algorithms so that, for any , runs in time polynomial in the input and and outputs a solution that is at most a factor worse than the optimal solution. for the network improvement with bounded polynomial delays on a two-terminal series-parallel graph. Our algorithm is based on appropriately discretizing the space of budgets and flows on each subgraph of the graph . We then obtain the allocation and flow that minimizes the maximum delay over all paths with positive flow in this discretized space. Although the discretized flow obtained will not be an equilibrium flow, by Lemma 20, this maximum delay will be an upper bound on the delay of the equilibrium flow for the allocation obtained. We will show that the delay of the discretized flow is a good approximation to the optimal delay.

We start with a definition for series-parallel graphs and of the corresponding decomposition tree.

Definition 19 (Series-parallel graph).

A single edge is a series-parallel graph with source and sink . Further, if two graphs and are series-parallel graphs with source and sink , and , respectively, then they can be combined to form a new series-parallel graph by either of the following operations:

-

1.

Series Composition: Merge and to obtain graph , and let and be the new source and sink of ;

-

2.

Parallel Composition: Merge and to obtain a new source , and and to obtain a new sink in the resulting graph .

The recursive definition of a series-parallel graph naturally yields a binary tree called the decomposition tree of the series-parallel graph. The root of the tree corresponds to graph , and the leaves correspond to the edges of . Each internal node corresponds to the subgraph obtained by the series or parallel composition of the subgraphs corresponding to the children. In the following discussion, a subgraph of series-parallel graph is a graph obtained during the recursive construction, and hence corresponds to a node in the decomposition tree. We use and to denote the source and sink of subgraph . We use to denote the series composition of and , and to denote the parallel composition.

We first show that in a series-parallel network, the equilibrium flow minimizes the maximum delay over all paths that have positive flow.

Lemma 20.

Let be the equilibrium flow in routing game on series-parallel graph , and be any - flow of value . Then .

We use the following result about flows in series-parallel graphs. We omit a formal proof, which follows immediately by induction on the graph.

Lemma 21.

Let be a directed two-terminal series-parallel graph with terminals and , and , be two - flows satisfying and . Then there exists an - path such that , and .

Since is an equilibrium flow, all paths carrying positive flow have minimum delay, and the lemma follows. ∎

Given a parameter , define as the maximum exponent of the delay function on any edge. Let be our unit of discretization, where as before . For clarity of presentation, we assume that is integral. For any subgraph of and , we define the set of discretized allocations as the set of all valid allocations of budget to edges in , so that the allocation to each edge is either 0 or an integral multiple of . We define as the set of all valid - flows on the edges of of value , that are additionally either zero or an integral multiple of on every edge. More formally,

As usual, let be the optimal allocation, and and be the equilibrium flow and delay for allocation . We initially make the assumption that on every edge, and will remove this assumption later. We first show that optimizing over flows and allocations in the discretized space is sufficient to obtain a good approximation to the optimal delay.

Lemma 22.

There exists flow and allocation that satisfy

We first show the following claim. The proof uses the fact that for any flow on an acyclic graph, a path-decomposition of flow can be obtained so that at most paths have strictly positive flow.

Claim 23.

There exists flow that satisfies for all , and allocation that satisfies .

Proof.

We will assume we are given and and will construct and that satisfy the conditions of the claim. We start with the allocation . On each edge, we round down to the nearest multiple of to obtain on these edges. On an abitrary edge , we allocate . Note that by assumption, is integral. Since the allocation to every other edge is an integral multiple of , so is the allocation to edge . Allocation is obviously a valid allocation of budget , and thus . Further, since on every edge by assumption, , and thus on every edge

Allocation is thus the required allocation.

To obtain flow , we start with a flow decomposition so that at most paths in have . There is some path with in this decomposition. Call this path . Then on every path except , we round down to the nearest multiple of to obtain for that path, and assign the remaining flow to path . Since we assume is integral and the flow on every other path is an integral multiple of , so is the flow on path . Flow is then a flow of value with the flow on every edge an integer multiple of , and hence . Further, on every edge , . Since ,

Hence for any edge ,

Flow is thus the required flow. ∎

Proof of Lemma 22. We will show the lemma is true for flow and allocation obtained in Claim 23. Note that for any edge , only if . Then for any path with on every edge ,

where the last equality is because for every edge . ∎

We utilise the recursive structure of series-parallel graphs to give a dynamic programming algorithm to obtain an optimal flow and allocation in the discretized spaces and respectively. For subgraph and , define recursively as follows.

From the definition, corresponds to a division of flow and budget between its subgraphs and so that the assignment to each subgraph is a multiple of for the flow and for the budget. Hence, by recursion, corresponds to an allocation of flow and budget to each edge of , so that the flow on each edge is an integral multiple of and the budget allocated to each edge is a multiple of . Further the total budget allocated is and the value of the flow in is . By dynamic programming on the series-parallel decomposition tree for , can then be computed in time . For the following lemma, for subgraph , flow and allocation , define

Lemma 24.

For any subgraph and ,

We omit a formal proof of the lemma, which follows from the recursive definition of . We now show that if on every edge, the allocation obtained for is a near-optimal allocation.

Theorem 25.

Given and an instance of CNDP in a series-parallel graph so that the optimal allocation satisfies , we can obtain in time a valid allocation so that the delay at equilibrium for this allocation is at most .

Proof.

Choose , and let and be the flow and allocation that obtains delay . By the recursive construction given, and can be obtained in time . By Lemmas 24 and 22,

Let be the equilibrium flow with allocation , and . Then by Lemma 20,

∎∎

Given , define . To remove the assumption that on every edge, consider an allocation . Then is a valid allocation. Let be the equilibrium flow for allocation . Then satisfies the conditions for Theorem 25, and hence . Further,

References

- [1] Mustafa Abdulaal and Larry J LeBlanc. Continuous equilibrium network design models. Transportation Research Part B: Methodological, 13(1):19–32, 1979.

- [2] Ravindra K. Ahuja, Thomas L. Magnanti, and James B. Orlin. Network flows: theory, algorithms, and applications. Prentice-Hall, Inc., Upper Saddle River, NJ, USA, 1993.

- [3] Martin Beckmann, C. B. McGuire, and Christopher B. Winsten. Studies in the economics of transportation. Yale University Press, 1956.

- [4] Stephen Boyd and Lieven Vandenberghe. Convex optimization. Cambridge university press, 2004.

- [5] Stefano Catoni and Stefano Pallottino. Traffic equilibrium paradoxes. Transportation Science, 25(3):240–244, August 1991.

- [6] Richard Cole, Yevgeniy Dodis, and Tim Roughgarden. How much can taxes help selfish routing? J. Comput. Syst. Sci., 72(3):444–467, 2006.

- [7] Benoît Colson, Patrice Marcotte, and Gilles Savard. An overview of bilevel optimization. Annals of operations research, 153(1):235–256, 2007.

- [8] Lisa Fleischer, Kamal Jain, and Mohammad Mahdian. Tolls for heterogeneous selfish users in multicommodity networks and generalized congestion games. In FOCS, pages 277–285, 2004.

- [9] Steven Fortune, John E. Hopcroft, and James Wyllie. The directed subgraph homeomorphism problem. Theor. Comput. Sci., 10:111–121, 1980.

- [10] Terry L Friesz, Hsun-Jung Cho, Nihal J Mehta, Roger L Tobin, and G Anandalingam. A simulated annealing approach to the network design problem with variational inequality constraints. Transportation Science, 26(1):18–26, 1992.

- [11] Terry L Friesz, Roger L Tobin, Hsun-Jung Cho, and Nihal J Mehta. Sensitivity analysis based heuristic algorithms for mathematical programs with variational inequality constraints. Mathematical Programming, 48(1-3):265–284, 1990.

- [12] Martin Gairing, Tobias Harks, and Max Klimm. Complexity and approximation of the continuous network design problem. CoRR, abs/1307.4258, 2013.

- [13] Patrick T Harker and Terry L Friesz. Bounding the solution of the continuous equilibrium network design problem. In Proceedings of the Ninth International Symposium on Transportation and Traffic Theory, pages 233–252, 1984.

- [14] Ara Hayrapetyan, Éva Tardos, and Tom Wexler. The effect of collusion in congestion games. In STOC, pages 89–98, New York, NY, USA, 2006. ACM Press.

- [15] George Karakostas and Stavros G. Kolliopoulos. The efficiency of optimal taxes. In CAAN, pages 3–12, 2004.

- [16] Elias Koutsoupias and Christos H. Papadimitriou. Worst-case equilibria. In STACS, pages 404–413, 1999.

- [17] VS Anil Kumar and Madhav V Marathe. Improved results for stackelberg scheduling strategies. In Automata, Languages and Programming, pages 776–787. Springer, 2002.

- [18] Changmin Li, Hai Yang, Daoli Zhu, and Qiang Meng. A global optimization method for continuous network design problems. Transportation Research Part B: Methodological, 46(9):1144–1158, 2012.

- [19] Paramet Luathep, Agachai Sumalee, William HK Lam, Zhi-Chun Li, and Hong K Lo. Global optimization method for mixed transportation network design problem: a mixed-integer linear programming approach. Transportation Research Part B: Methodological, 45(5):808–827, 2011.

- [20] Patrice Marcotte. Network design problem with congestion effects: A case of bilevel programming. Mathematical Programming, 34(2):142–162, 1986.

- [21] Noam Nisan, Tim Roughgarden, Éva Tardos, and Vijay V. Vazirani. Algorithmic Game Theory. Cambridge University Press, New York, NY, USA, 2007.

- [22] Christos H. Papadimitriou. Algorithms, games, and the internet. In STOC, pages 749–753, 2001.

- [23] Robert W. Rosenthal. A class of games possessing pure-strategy nash equilibria. Intl. J. of Game Theory, 2:65–67, 1973.

- [24] Tim Roughgarden. The price of anarchy is independent of the network topology. J. Comput. Syst. Sci., 67(2):341–364, 2003.

- [25] Tim Roughgarden. Stackelberg scheduling strategies. SIAM Journal on Computing, 33(2):332–350, 2004.

- [26] Tim Roughgarden. Selfish Routing and the Price of Anarchy. The MIT Press, 2005.

- [27] Tim Roughgarden. On the severity of braess’s paradox: designing networks for selfish users is hard. Journal of Computer and System Sciences, 72(5):922–953, 2006.

- [28] Tim Roughgarden and Éva Tardos. How bad is selfish routing? Journal of the ACM, 49(2):236–259, March 2002.

- [29] Alexander Schrijver. Finding k disjoint paths in a directed planar graph. SIAM J. Comput., 23(4):780–788, 1994.

- [30] Y. Shiloach and Y. Perl. Finding two disjoint paths between two pairs of vertices in a graph. J. ACM, 25(1):1–9, January 1978.

- [31] Chaitanya Swamy. The effectiveness of Stackelberg strategies and tolls for network congestion games. In SODA, pages 1133–1142, 2007.

- [32] David ZW Wang and Hong K Lo. Global optimum of the linearized network design problem with equilibrium flows. Transportation Research Part B: Methodological, 44(4):482–492, 2010.

- [33] J. G. Wardrop. Some theoretical aspects of road traffic research. In Proc. Institute of Civil Engineers, Pt. II, volume 1, pages 325–378, 1952.

- [34] Hai Yang and Michael G H. Bell. Models and algorithms for road network design: a review and some new developments. Transport Reviews, 18(3):257–278, 1998.

- [35] Hai Yang and Hai-Jun Huang. The multi-class, multi-criteria traffic network equilibrium and systems optimum problem. Transportation Research Part B: Methodological, 38(1):1–15, 2004.

- [36] Hai Yang and Xiaoning Zhang. Existence of anonymous link tolls for system optimum on networks with mixed equilibrium behaviors. Transportation Research Part B: Methodological, 42(2):99–112, 2008.

- [37] Jane J Ye. Necessary and sufficient optimality conditions for mathematical programs with equilibrium constraints. Journal of Mathematical Analysis and Applications, 307(1):350–369, 2005.

- [38] Yafeng Yin. Genetic-algorithms-based approach for bilevel programming models. Journal of Transportation Engineering, 126(2):115–120, 2000.

Appendix

Proofs from Section 5.2

Removing assumption about all paths being used at equilibrium.

Recall we order paths so that , where is the length of path and there are - paths, and assume the inequalities are strict. Define , i.e., is the set of paths with length at most . Thus, . It is easy to see that the equilibrium flow for any allocation has strictly positive flow on exactly the edges in for some .

Let be the set of paths with strictly positive flow at equilibrium. By a similar derivation as for (11), the delay at equilibrium is given by

| (20) |

For an allocation , since we do not a priori know the set of paths used in the optimal solution, we will consider all possible sets of paths. To formalize this, for an allocation , define

| (21) |

For allocation if is the set of paths used in the resulting equilibrium, then by (20), . We show that knowing for each also allows us to obtain .

Claim 26.

For allocation if , then .

Proof.

We will show that if then there is an equilibrium flow with delay . By the uniqueness of equilibrium flow, the claim must then be true.

For path , let , and for . Then

where the second equality follows from the definition of in (21). Further, each , since for . Thus is a valid flow. To see that is also an equilibrium flow, note that for any path with strictly positive flow, the delay is exactly , while any path with zero flow has delay at least . ∎

For any budget , define , i.e., is the minimal value of over all valid allocations. Then if , replacing by , by , and by , our algorithm in Section 5.2 returns the allocation that minimizes .

In order to use this algorithm, we need to know so that the set of paths used by the equilibrium for the optimal allocation is exactly , since in this case the minima of and coincide.

Since we do not know , we use the following iterative algorithm. Start with , and obtain the allocation . If , we stop; is then the allocation that minimizes , and . If , we increase and repeat the process.

To show the correctness of this process, we use the following lemma.

Lemma 27.

For and any budget , if , then .

Proof.

Let and be valid allocations that minimize and respectively. We will prove the contrapositive. Then by assumption . Further,

where the first inequality is since minimizes and the second inequality follows from the contrapositive of Fact 2, by setting and . ∎

To see that the process given above obtains an optimal allocation , let be the set of paths used by equilibrium for the optimal allocation. Suppose our process ends for , then it must have found an allocation so that . Since the process did not terminate at , and hence by Lemma 27 . Thus , and hence by Claim 26, , where the last inequality is because is the set of paths used by equilibrium for the optimal allocation and . This is obviously a contradiction, since is minimal.

Further, the process must stop for , since there exists an allocation with . The process is hence correct, and will obtain the optimal allocation.

Implementing Step 2 of the algorithm.

Given , our problem is to obtain an allocation that satisfies (15) and . To obtain such an allocation, we will use a binary search procedure together with a concave relaxation of the original problem for which the first-order conditions exactly correspond to (15).

Consider the following optimization problem , with variables and parametrized by the budget :

subject to being a valid allocation for budget . The first-order conditions for this problem are exactly (15). Further, for each path is a concave function, and hence the objective is concave. Thus for a given budget the problem can be solved to obtain the optimal allocation. We now show that by increasing the budget , we can obtain a monotone solution to .

Claim 28.

Let , and is an optimal solution to . Then there is an optimal solution to that satisfies on all paths .

Proof.

Let be an optimal solution to . If on all paths , we are done. Otherwise, let be a path such that . Since , there is a path such that . Then, by Corollary 9,

Further, by the first-order conditions for optimality, since and ,

It immediately follows that all the above inequalities must be equalities, and further, for any path ,

| (22) |

Consider the allocation , constructed as follows. Let initially. Then for where is the number of paths, if , . Then for all paths . Further, lies between and , and hence by concavity of conductance and (22), for all paths ,

Also, since and , it follows that . Thus allocation satisfies the first-order conditions for optimality of , and since is a concave maximization program, is also an optimal solution that satisfies the conditions of the claim. ∎

We now use the following binary search procedure. Let and be the lower and limits on the budget, and . Solve , and let be the optimal solution. If , set , , add constraints to and solve again. Similarly if , we set , , add constraints to and solve again.

Let and be the solution to and with . The added bounds on ensure that , and since at optimality, for some path . By Claim 12, . Hence the binary search procedure must obtain a budget and an allocation so that . Further, by Claim 28, satisfies the KKT conditions for the original problem, and hence satisfies (15) as well.