A data mining approach using transaction patterns for card fraud detection111This research was supported by the MKE (Ministry of Knowledge Economy), Korea, under the “Employment Contract based Master’s Degree Program for Information Security” supervised by the KISA (Korea Internet Security Agency)

Abstract

Credit and debit cards, rather than actual money, have become the universal payment means. With these cards, it has become possible to buy expensive items easily without an additional complex authentication procedure being conducted. However, card transaction features are targeted by criminals seeking to use a lost or stolen card and looking for a chance to replicate it. Accidents, whether caused by the negligence of users or not, that lead to a transaction being performed by a criminal rather than the authorized card user should be prevented. Therefore, card companies are providing their clients with a variety of policies and standards to cover this eventuality. Card companies must therefore be able to distinguish between the rightful user and illegal users according to these standards in order to minimize damage resulting from unauthorized transactions.

However, there is a limit to applying the same fixed standards to all card users, since the transaction patterns of people differ and even individuals’ transaction patterns may change frequently due to changes income and consumption preference. Therefore, when only a specific threshold is applied, it is difficult to distinguish a fraudulent card transaction from a legitimate one.

In this paper, we present methods for learning the individual patterns of a card user’s transaction amount and the region in which he or she uses the card, for a given period, and for determining whether the specified transaction is allowable in accordance with these learned user transaction patterns. Then, we classify legitimate transactions and fraudulent transactions by setting thresholds based on the learned individual patterns.

keywords:

Pattern mining , Fraud detection , Autoregressive , Gaussian Processes , Association ruleurl]https://sites.google.com/site/securesiplab/

1 Introduction

A lot of crime involving card fraud is being perpetrated due to transaction card cloning or theft. Thus, in order to prevent fraudulent transactions due the replication of a card at source, financial authorities in many countries are moving from the Magnetic Stripe (MS) card to the Integrated Circuit (IC) card. However in contrast to banks which can easily introduce ATMs dedicated to IC cards, it is not easy for retail stores to replace the previous card reader at Point of Sale (POS) terminals with an IC reader device. Therefore, at present, the card data, which include the consumer’s credit information and transaction data are included in both the MS and IC of a card, and as a result, it seems still difficult to prevent illegal card use resulting from theft or replication.

Card companies currently have introduced a variety of measures to prevent damage being caused to the consumer by an unauthorized card transaction, such as sending an SMS about the transaction and a copy of the transaction by E-mail, suspending the use of the credit card, and so on. However, these methods are dependent on consumer’s attention. When they do not pay attention to the received billing messages and are therefore not aware of a fraudulent transaction perpetrated using their card, it is difficult to detect fraud cases early and take appropriate action.

The card companies may take voluntary action to prevent unauthorized payments by determining in what location and the amount of the transaction for which a card is used. For example, if a payment involving a large amount of money is made in Southeast Asia, and the previous transaction had occurred on hour previously in Seoul, Republic of Korea, the company may conduct a verification process through a phone call to the customer. Because the same card cannot be used almost simultaneously in two distant locations, a rational explanation is that a duplicate of the card was used.

However, there is a limit to the number of fraudulent transactions that can be detected by simply using a fixed threshold value for the geographic distance between transactions, and the location or amount of payment, because the consumption levels of people differ, and a cloned or lost card can be used in a location close to the legitimate owner’s normal use area.

In this paper, we therefore propose methods for detecting an illegal card transaction using large scale data analysis. The customers’ unique billing pattern is used in the process. In the next section, we provide related studies and discuss the differences between these and our study. In section 3, we provide the background of statistical methods and data mining approaches. In section 4, we discuss the model for our experiment on the detection of fraudulent transactions, which is based on transaction patterns. In section 5, we present our experimental results, and we discuss the reasons for the results in section 6. Finally, we present our conclusions in section 7.

2 Material and methods

Data mining is finding patterns in data that are statistically reliable, previously unknown, and can be analyzed to provide useful insights (ref1). Fraud detection is a main research area in the field of data mining. The goal of using the data mining approach in the detection of card fraud is to determine whether the card used in a transaction has been used by the legitimate card user. Here, a card is a means of payment used for transactions, such as a credit, debit, or purchase card, and the user is the authorized owner of the card. The data used for data mining constitutes a user’s transaction records.

Statistical fraud detection methods have been classified into two broad categories: “supervised” and “unsupervised” (ref2; ref3). In supervised methods, estimated statistical models are used to discriminate between fraudulent and legitimate purchase behaviors by classifying new observations into the appropriate class: fraudulent or legitimate transaction (ref2; ref3). This method requires samples from both classes, fraudulent and legitimate observations, as the models are trained based on examples of observations in both classes (ref3). The models created by the method are assessed by measuring their accuracy in correctly classifying new observations as fraudulent or non-fraudulent (ref3). Since 2001, most fraud detection studies using supervised algorithms have focused on the misclassification rate (i.e., the false positive and false negative error rate) (ref4).

Related works in which supervised methods are used for classifying credit card transactions into legitimate and fraudulent transactions have been published: ref3 employed a transaction aggregation strategy to create variables for the estimation of a logistic regression model, and ref6 used a binary support vector system based on the support vectors in support vector machines and a genetic algorithm to solve credit card fraud problems that had not been well identified (ref5).

Unsupervised methods attempt to detect unusual observations, such as customers, transactions, or accounts whose behavior may be different from the norm (ref3), which can be identified by clustering based on normal legitimate behavior patterns. As unsupervised methods do not require samples of fraudulent and legitimate transactions, there may be cases where there is no prior knowledge of classes of observations (ref3).

In earlier studies, unsupervised methods were also used for clustering to detect credit card fraud. ref7 built a Hidden Markov Model for the sequence of operations in credit card transaction processing. ref8 focused on real-time fraud detection and presented a new model. ref9 created a model of typical cardholder behavior and analyzed deviations in transactions in order to identify suspicious ones. The studies of ref8 and ref9 were based on a self-organizing map algorithm (ref5).

A data mining approach for mobility patterns is also used to predict the location of drivers or mobile phone users. ref12 presented a Hidden Markov Model-based approach to provide real-time predictions of a driver’s destination and route. ref13 focused on the regions of interest and the typical travel time of moving objects from region to region. They introduced a novel form of spatio-temporal pattern, which formalizes the idea of aggregate movement behavior which they discuss. ref15 proposed a context model, based on classification using a certain moving profile and history of movements. They evaluated their schemes with Bayesian algorithms, decision-tree, and rule induction.

Using supervised methods to detect fraudulent card transaction involves many constraints. Because academicians have difficulty acquiring credit card transaction datasets, it is not easy to exchange ideas and possible innovations related to credit card fraud detection because of the dearth of published literature in this subject (ref10; ref11; ref3).

In this paper, we therefore detect fraudulent transaction based on the pattern of the amount of a customer’s payment using the purchase card data that are publicly available. The pattern is analyzed through Gaussian Processes (GPs) and the Autoregressive (AR) model, which have not previously been well documented in the area of fraud detection. Further, to characterize the pattern of a customer’s payment region, we collect the location of the customer and track the mobility confidence. Then, we find abnormal values by extracting the association rules of the payment region of a card user by applying an association rule algorithm (ref16), which has previously been used to predict the movement of mobile phone users.

3 Theory and calculation

3.1 Autoregressive model

Given a dataset of observations , where , is the autoregressive model that expresses the -th data with prior data . The equation of is defined as

where are parameters of the model, is a constant, and is white noise.

We can express the terms from to by

| (1) |

Here, , where , are training data and used to estimate a target . In order to impose a restriction such that not all previous data can be used to infer the target data, it is also possible to utilize only the data close to the target data by using a fixed small window size. Let the left hand term of equation (1) be , the matrix of the right term be , and the matrix that contains unknown values , be . Then, the equation can be rewritten as a simple linear form given by

| (2) |

This represents that equation (2) is a simple linear model with input data and parameters . The observed data have a noise term , which is assumed to be independent and identically distributed (i.i.d.) Gaussian distribution

where denotes a Gaussian distribution with mean and variance , and is a precision value that is an inverse of the variance.

This noise assumption, together with the model, directly gives rise to the likelihood (i.e., the probability density of the observations given the parameters), which is factored over the cases in the training set (because of the independence assumption) to give (Gaussian06, chap. 2)

| (3) | |||||

Then, the residual vector is . A generalized least squares method is used to estimate by minimizing the squared Mahalanobis length of this residual vector:

Hence,

| (4) |

The variance of an error term , , is obtained by the maximum likelihood

Substituting for the form of the Gaussian distribution, we obtain the log likelihood function in the form (bishop07, chap. 1)

| (5) | |||||

Now, we can obtain the estimated precision by inducing the differential equation of equation (5) equal to 0 as

| (6) |

Now, based on the probability distribution of equation (3), the target data can be predicted by expectation with a confidence level with the range:

3.2 Gaussian Processes

Gaussian Processes (GPs) are the extension of multivariate Gaussians to infinite-sized collections of real-valued variables and distributions over random functions (GP08). That is, they predict the subsequent data by revealing the distribution of the nonlinear function , which represents the relationship between the output data and the input data .

Each observation from its corresponding input data is given by

through the Gaussian noise model with variance . The function can be expressed as given by

where is the mean function and is the covariance function (GP08). Usually, for notational simplicity we take the mean function to be zero. We now choose the covariance function by writing

| (7) |

where is the Kronecher delta function (Gaussian06). Its parameters can be estimated through Bayes’ theorem. According to Bayes and Gaussian06, when we have little prior knowledge about what should be, this corresponds to maximizing , given by

| (8) |

For estimating the parameters, the Nelder-Mead simplex, multivariate optimization algorithm (ref20) is one method that can be used.

However, in this study it is not enough to determine the parameters using equation (8). Because there is no restriction on parameter , it can have any value from a negative value to . In this case, we use maximum a posteriori (MAP) to find parameter as

| (9) | |||||

We can replace the term in equation (9) with equation (8). In addition, we need to constrain parameter in order to interpret testing data as an event related to the close training data. That is, to estimate the 101-st testing data we focus more on the 100-th training data than on the 50-th. We thus assume that the parameter follows a non-negative distribution , where it is the gamma distribution with a shape parameter 2 and a scale parameter 2. It is given by

| (10) |

Hence, we can obtain restricted parameter , as well as and , by calculating the arguments that maximize equation (10). For simplicity, we assumed the prior distribution of and follow uniform distribution, which is an improper distribution.

Now, given observations of , in order to predict not the actual but , we prepare three matrices.

| (11) | |||||

| (12) | |||||

| (13) |

Then, can be predicted based on observations of as a sample from a multivariate Gaussian distribution:

Given the data, a certain prediction for can be obtained by conditional Gaussian distributions as

That is, the best estimate for follows the distribution that has the expectation of , , and the uncertainty, . Therefore, is decided with the range:

giving a 95% confidence level.

3.3 Extreme-value theory

Extreme-value theory is a branch of statistics that concerns the distributions of data of unusually low or high value (ref23). It forms representations for the tails of distributions, in this article especially the right-hand tail.

Assume a set with i.i.d. random variables drawn from the one-sided standard Gaussian (i.e., ) and define , which means the largest element observed in samples of . Then, the extreme value probability (EVP) of is its probability of being the largest value in the set and is obtained in the form of the Gumbel distribution as (ref23; ref24)

| (14) |

where the location parameter is

| (15) |

and the scale parameter is

| (16) |

Since the parameters and depend on the number of data, , should be specified first in order to evaluate an EVP. However, because we are not directly interested in , we obtain the EVP at time by marginalizing out the run length (ref24):

| (17) |

The run length means the time since the last outlier (ref25), and its probability (ref24) is

where . Then, the EVP can be used as a novelty measure and an outlier can be detected in the case of , where is a threshold with (ref24).

3.4 Association rule

Association rule analysis is a data mining technique used to find which events are likely to co-occur. In this study, it is used to extract the region where transactions occur frequently and the pattern of the movement path, by indicating the transaction locations as a sequence. For notational convenience, defines the path sequence of a customer who made payments with a card times in region to times in region . For instance, a path sequence represents the transition of a customer’s location, such as, . Table 1 is an example that shows the route where the transactions of a certain customer occurred during a month.

| Week(s) ago | Actual transaction path sequence |

|---|---|

| 4 | |

| 3 | |

| 2 | |

| 1 |

By padding the end of each row of Table 1 with 0’s so that the rows have the same number of columns, we obtain the matrix of the collected transaction path, , as

| (18) |

We can now infer which regions (i.e., numbers) are likely to follow each other and which regions (i.e., numbers) are associated with others based on each row of . Let be a collection of row spaces of matrix . By applying the association rule to the row spaces, , movement patterns are mined using the support value by discovering the correlation between the regions where a card user made payments.

From Table 1, the supports of the length- pattern, , are determined by the number of row spaces that contain the pattern’s element. The support value of , an element of , is calculated by

| (19) |

The supports of the length- pattern, , are obtained from the sum of the number of row spaces that contain the length- sequences and an incident support, :

| (20) |

The incident support is a value that reflects the region where the customer’s transactions diverged from the pattern of arriving at along the original path (i.e., ) from , and is given by

| (21) |

That is, the incident support plays the role of improving the supports by correcting the result value, even when a customer goes indirectly to the destination moving along a slightly different path from that which was mined. For instance, the support value for a pattern based on is , since for , the second row space of , and for , the third row space of , .

| Support | Support | Support | |||

|---|---|---|---|---|---|

| 3 | 3 | 2 | |||

| 1 | 1 | 1 | |||

| 1 | 0.5 | 0.2 | |||

| 1 | 1 | 0.5 | |||

| 2 | 1 | 1 | |||

| 1 | 0.5 | 0.33 | |||

| 1 | 1 | 1 | |||

| 1 | 1 | 0.2 | |||

| 1 | 1.17 | 1 | |||

| 1 | 0.33 | 0.25 | |||

| 1 | 0.5 | 1 | |||

| 1 |

In Table 2, the support values of length- patterns and length- patterns are given. The supports of can be obtained likewise.

Now, if a card payment in a particular region has occurred, it is possible to calculate the confidence by analyzing the association between the movement path of the current consumer and the patterns of the locations of payments that were made in the past. For an association rule of transaction region , the confidence is given by

| (22) |

For example, suppose that we have recent transaction data where the region is and the card owner is currently in location number 1. Then, there are three possible association rules:

The confidence values of each rule are , , and , and the maximum value of these results, , is kept as the confidence score of the transaction path .

3.5 Adjacency matrix

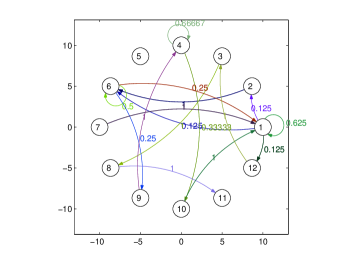

An adjacency matrix is a means of representing which vertices (or nodes) of a graph are adjacent to which other vertices (wiki:AD). We set the transaction region, , as the vertices of a graph and put edges on a graph when a customer moves from to (i.e., ). This graph is called a directed graph. Furthermore, it has cycles (i.e., ) because it is possible to make more than one payment in the same area. By giving a weight, that is, the conditional probability of the location given , on the edges of a graph, we can obtain an square adjacency matrix. Fig. 1 shows an example of a directed graph and the conditional probability of Table 1 based on the adjacency matrix.

For instance, given the current transaction data in the region , the confidence score (or conditional probability) is , from Fig. 1.

4 Model and algorithm

We compare the accuracy of the methods of AR model (ref18) and GPs (Gaussian06) for detecting large payments according to the transaction amount pattern, and also compare the accuracy of the methods of association rule analysis (ref16) and adjacency matrix (ref19) for detecting abnormal movement according to the transaction region pattern.

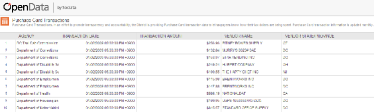

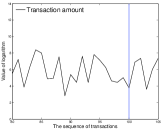

The data used for the experiments in this study were classified into two broad categories: legitimate transactions and fraudulent transactions. In our experiments, as legitimate transaction data, we used “Purchase Card Transactions”. We used the data in the “Transaction amount” and “Vendor State/Province” columns. The data are publicly available (Fig. 2, https://opendata.socrata.com/).

Fraudulent transaction data were extracted from the statistical results of ref3 using a dataset of real-world credit card transactions. The dataset contains 2,420 fraudulent transactions; a good summary of the dataset is given in ref3. Given the fraudulent dataset, the transaction amount of fraudulent event is generated by non-negative distribution with the mean and standard deviation of the attribution, that is, the average amount spent per transaction over a month on all transactions up to this transaction. The transaction region of a fraudulent event is generated with the legitimate transaction location by random permutation based on the assumption that the transaction region pattern of perpetrators is distinguishable from that of a legitimate normal user of a card.

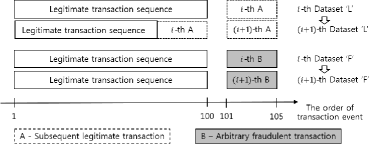

The datasets used our experiments are shown in Fig. 3. We first train with 100 transactions, which is called a “legitimate transaction sequence”, and learn the pattern of a legitimate card user. Then, we test the next transaction data whether it is legitimate or fraudulent. There are two kinds of testing data with length 5: “subsequent legitimate transaction” data and “arbitrary fraudulent transaction” data . The legitimate transaction data are the subsequent continuous transaction data of the training data, and the fraudulent transaction data are independent of the previous training data. It should be noted that the number of the testing data is even smaller than that of the training data. Because perpetrators attempt to use stolen credit cards quickly to maximize the amount of the fraudulent payments, the sooner these transactions are detected, the greater the loss that can be avoided by stopping transactions made with the fraudulent credit cards (ref3).

Now, let the 105 legitimate transaction data be dataset and other transaction data inserted into the fraudulent transaction data be dataset . We prepared 20 dataset s and s each to conduct our experiment for various transaction data. Both of dataset s and s include 105 transactions, and -th dataset consists of 100 training data and 5 testing data as:

-

1.

-th dataset (rear part of legitimate transaction sequence 1-th i-th -th )

-

2.

-th dataset (original legitimate transaction sequence -th ),

where “” represents a concatenation and “” represents a division between training data and testing data.

The characteristics of them are distinguishable with existence of transaction patterns. All dataset s preserve a certain transaction patterns, but s do not. While dataset s consist of continuous legitimate transaction sequence, dataset s consist of fraudulent transactions padded to a certain legitimate transaction sequence.

We conduct experiments using two methods to determine which method is better for detecting outliers that do not follow the pattern of the legitimate consumer and what threshold value is optimal for classifying the transactions of a legitimate customer and those of a perpetrator as:

-

1.

For the transaction amount, we set a threshold value and confirm whether the threshold allows a transaction amount to be identified as legitimate or fraudulent.

-

2.

For transactions with amount and region, we give a confidence score for each transaction, that is, the similarity of the current transaction to previous transaction patterns, and confirm the distribution of these scores over legitimate and fraudulent cases. Then, we set a threshold based on the distribution.

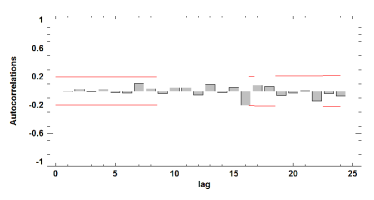

In we should first make a decision over the number of AR terms, , and the order of differencing, . Here, represents the number of previous transactions used to express a transaction with a linear combination of previous transactions, and represents the number of differences needed to stationarize a sample of the legitimate transaction sequence.

The root mean square error (RMSE) shows the estimated white noise standard deviation, and the autocorrelation function (ACF) plot shows the coefficients of correlation between data and lags for the sample. It is helpful to decide and by focusing on the lowest standard deviation and the small and patternless autocorrelations.

| RMSE | |

|---|---|

| (1, 1) | 1.92049 |

| (2, 1) | 1.91002 |

| (3, 0) | 1.64051 |

| (4, 0) | 1.64892 |

| (5, 0) | 1.61823 |

In the AR model and GPs, we calculate the estimated mean and variance of , and respectively, EVP of , and the confidence score of , from the training data, , and testing data, using algorithm 1 and 2.

In algorithm 1, “” represents a cumulative distribution function value of normal distribution with mean and variance at .

In the association rule and adjacency matrix, we calculate only the confidence score of the transaction region of the testing data from transaction path of the training data using algorithms 3 and 4. In algorithm 3, means the -th row of matrix . In algorithm 4, means an entry value of the -th row, -th column of matrix .

5 Results

5.1 Outlier detection for the transaction amount

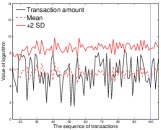

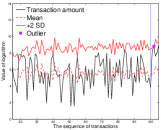

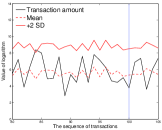

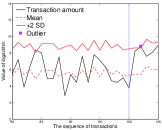

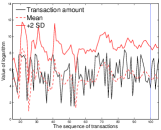

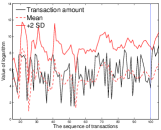

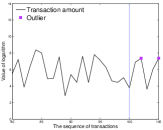

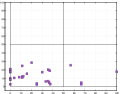

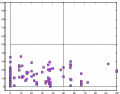

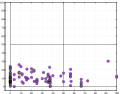

We first apply the logarithmic functions to datasets and in the experiment, and perform outlier detection for the transaction amount using GPs and at a confidence level of 95% (i.e., +2 SD), as shown in Fig. 5 and 6. The upper plots in these figures help us to obtain a comprehensive grasp of the transaction amount and its mean and upper bound, while the lower plots focus on the range of testing data, and , from the 101-st to 105-th transaction.

In the case of , as shown in Fig. 5, all the legitimate transactions in dataset are identified as legitimate. However, in dataset , the fraudulent transactions are not detected as such except one transaction, because the upper bound for dataset was too high to identify the amount of the fraudulent transactions.

|

|

|

|

| (a) Dataset | (b) Dataset |

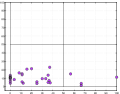

In the case of GPs, as shown in Fig. 6, GPs also identified the legitimate transactions in dataset , and not the fraudulent transactions in dataset . It seems that the arbitrary fraudulent transactions, , in dataset do not overwhelm the large amount of legitimate transaction sequences that sometimes occurred.

|

|

|

|

| (a) Dataset | (b) Dataset |

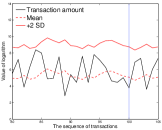

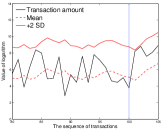

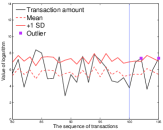

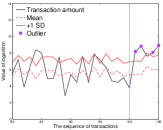

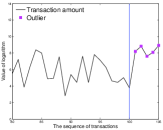

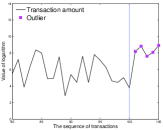

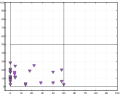

When the confidence level threshold is adjusted to 68% (i.e., +1 SD), in Figs. 7 and 8, outliers, indicated by magenta square, are found more easily than when threshold is 95% (i.e., +2 SD). However, false-positive errors were incurred because the legitimate transactions were detected, as well as the dataset that contains fraudulent transactions.

|

|

| (a) Dataset | (b) Dataset |

|

|

| (a) Dataset | (b) Dataset |

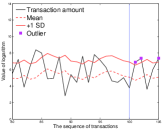

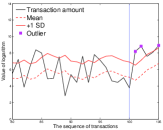

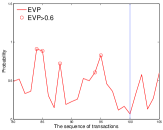

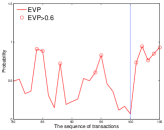

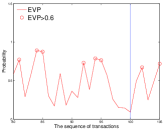

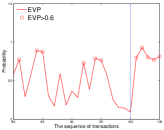

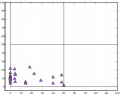

Figs. 9 and 10 show the results of outlier detection for and using not the standard deviations but extreme-value probability (EVP) with the threshold . The red circles in the upper plots represent EVPs (i.e., ) larger than 0.6, and the corresponding testing data are indicated as magenta squares in the lower plots. In Fig. 9, the distribution of testing data is supposed to be one-sided standard Gaussian having the estimated mean and standard deviation from the AR(5) model. The distribution of testing data in Fig. 10 is from GPs. In these cases, we found that EVP gives a more reliable result because not only did both and GPs identify the fraudulent transactions in dataset as fraud more accurately than the +1 SD method, but also identified the legitimate transactions in dataset as normal more accurately than the +1 SD method. However, since there are some data such that in a legitimate transaction sequence (i.e., on the left side of the vertical blue line in the upper plots), we can assume that it still gives rise to false-positive errors for the large amount transactions that are sometimes generated by a legitimate consumer.

|

|

|

|

| (a) Dataset | (b) Dataset |

|

|

|

|

| (a) Dataset | (b) Dataset |

Therefore, we consider the association rule and adjacency matrix, as well as and GPs, which handle the movement pattern of a consumer path, and determine the difference in the transaction pattern distribution of legitimate and fraudulent transactions. Then, we propose a optimal threshold for classifying them.

5.2 Confidence on the transaction amount and region

| -axis: Association rule | -axis: Association rule | -axis: Adjacency matrix | -axis: Adjacency matrix | |

|---|---|---|---|---|

| -axis: GPs | -axis: | -axis: GPs | -axis: | |

| Dataset |

|

|

|

|

| Dataset |

|

|

|

|

The confidence score for the transaction amount uses the cumulative distribution function (CDF) of Gaussian distribution, which has mean and standard deviations estimated from or GPs. In the case of Gaussian distribution with 0 mean and 1 variance (i.e., standard normal distribution), if the random variable of a newly occurred transaction amount is close to zero, (i.e., the average payment), we can understand that it follows the transaction pattern. On the other hand, if the random variable of a transaction amount is negative in standard normal distribution, we can ignore that event due to the small transaction amount, which is not threatening. In another case, when a random variable of the amount is positive in the distribution, we should pay attention to the event, since it represents that a large amount transaction exceeds the existing pattern has occurred. In order to express this possible threat as a numerical value, we define the confidence score for the transaction amount as “1-CDF”. That is, when the confidence score is higher, a smaller transaction amount will not cause concern, and when the confidence score is lower, a relatively large transaction amount that exceeds the pattern of the existing customer’s transactions will be seen as threatening.

The confidence score for the transaction region is defined as the result value of the association rule analysis and the conditional probability of the adjacency matrix method.

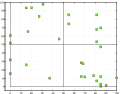

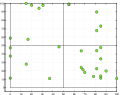

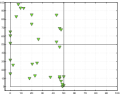

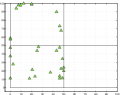

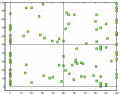

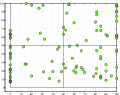

Now, we can draw two attributions in a two-dimensional plane by placing the confidence score of the transaction region on the coordinate and that of the transaction amount on the coordinate. For each of 6 and datasets with a total of 30 transaction data (i.e., 30 testing data), we drew a simple distribution of the confidence score using the transaction amount and region data. Fig. 11 shows 30 legitimate transaction data indicated by green points in the upper part and 30 fraudulent transaction data indicated by magenta points in the lower part. As shown in Fig. 11, the distribution of the experimental results for dataset is spread evenly, but in the case of dataset it is confirmed that the confidence scores are gathered at and coordinate values of less than 50. In particular, when the adjacency matrix is used for the confidence score for the transaction region (right side of Fig. 11), the coordinate value is biased at less than 50. This means that the association rule that considers the correlation between a variety of regions is a more appropriate method for processing the movement pattern of users than is the adjacency matrix, which deals with only the prior location.

Thus, we constrain the method for finding the confidence score of the transaction region to the association rule and not allow the adjacency matrix. With the association rule to obtain the confidence score of the transaction region, Method 1 uses GPs, and Method 2 uses to obtain that of the transaction amount. For each of 20 and datasets, a total 100 transaction data (i.e., 100 testing data), the comparison of the two methods is plotted in Fig. 12. As in Fig. 11 the data are gathered at and coordinate values of less than 50. However, since the distribution of the confidence score for the data, indicated by circles in the upper part of the figure, has spread in various places, it is difficult to separate the dataset from the mixed dataset with and completely.

Therefore, even allowing some errors, we need to find a threshold ( and ) that maximizes the accuracy and minimizes the error rate, where the accuracy rate is defined as the ratio of the number of correctly predicted transaction to the total number of transaction data based on a given threshold. The errors are divided into false-positive and false-negative. The false-negative error rate is the ratio of the number of transactions that failed to identify a fraudulent transaction to the number of data, and the false-positive error rate is the ratio of the number of transactions that raised a false alarm for a legitimate transaction to the number of data.

For example, based on a threshold , the accuracy at is the sum of the number of markers in dataset where or and the number of markers in dataset where and . The false-positive error is the number of markers in dataset where and , and the false-negative error is the number of markers in dataset where or .

| Method 1 | Method 2 | |

| -axis: Association rule | -axis: Association rule | |

| -axis: GPs | -axis: | |

| Dataset |

|

|

| Dataset |

|

|

| Method 1 | Accuracy | 115(.58) | 129(.65) | 144(.72) | 160(.80) | 159(.80) |

|---|---|---|---|---|---|---|

| Method 2 | 115(.58) | 135(.68) | 146(.73) | 161(.81) | 153(.77) | |

| Method 1 | False-positive | 3 | 10 | 14 | 20 | 23 |

| False-negative | 82 | 61 | 42 | 20 | 18 | |

| Method 2 | False-positive | 4 | 7 | 14 | 19 | 29 |

| False-negative | 81 | 58 | 40 | 20 | 18 |

As a result, for Method 1 and for Method 2 is the optimal threshold that maximizes the accuracy and minimizes the error rate, as shown in detail in Table 4.

6 Discussion

Until now, we gave the confidence scores to a customer’s transaction amount and region according to the previous transaction patterns, and examined the characteristics of the distribution of the values by plotting them in a coordinate plane. As a result, it was not easy to discriminate completely the data as legitimate or fraudulent, but by setting the appropriate threshold we can obtain the optimal solution. In spite of these contributions, a discussion about the false-positive errors and false-negative errors that occurred in this experiment is required. The reasons for the errors and countermeasures that can be considered are as follows:

-

1.

The fraudulent transaction amount induced from Table 4 of ref3 was not very significantly higher than the legitimate transaction amount. Some samples of fraudulent transaction data contain a normal transaction amount that is not larger than the legitimate transaction amount.

However, this may not be a problem in real-life transactions because perpetrators attempt to use stolen cards or duplicate cards quickly to maximize the amount of fraudulent transactions so that they can complete before the fraud comes to light.

-

2.

Immediately after a legitimate transaction involving the payment of a large amount of money occurs, the estimated amount of the next transaction is increased in accordance the amount of the previous transaction. Therefore, a fraudulent transaction involving a relatively small amount is not identified, and hence, a false-negative error occurs.

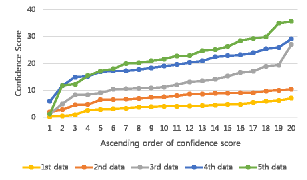

This issue can be resolved by reducing the length of the testing data, the number of transactions processed to identify the fraud. We used 20 datasets as testing data in dataset . Each the fraudulent set had five transactions (i.e., 5-length). In our experiment using dataset , confidence scores of the first and second data of the fraudulent sets were generally lower than those of the third, fourth, and fifth data.

Fig. 13 shows the confidence scores of 20 arbitrary fraudulent transaction data of the datasets obtained by GPs. They are plotted in ascending order. The confidence scores of the first data are represented by a yellow line, which is lower than 10. Confidence scores of the second data in the dataset are represented by an orange line, which is almost lower than 10. This means that if we constrained the number of testing data as 2, there would be less false-negative errors for the fraudulent transactions in GPs using a threshold .

Figure 13: Confidence scores of fraudulent transaction set in the order of testing data obtained by GPs. An arbitrary fraudulent transaction set has 5 transactions. For each of 20 fraudulent testing datasets, the confidence scores of the first data in the datasets are represented by orange dots and lines in ascending order. The second to fifth data are also represented by different colors. This figure shows that the first and second transactions of the datasets almost never exceeded a confidence score of 10. This demonstrates that the shorter the length of the testing data used, the lower is the false-negative error rate in not only GPs but also . -

3.

Conversely, after a legitimate transaction involving the payment of a small amount of money occurs, the estimated amount of the next transaction is decreased in accordance the amount of the previous transaction. Therefore, a legitimate transaction involving a relatively large amount raises a false-alarm, and hence, gives rise to a false-positive error.

This issue can also be resolved by adding a certain transaction amount that may have occurred in a fraudulent transaction to the threshold of confidence scores.

-

4.

Because the confidence score is 0 for the first visit location, many data are gathered on the -axis, whether the transaction is legitimate or fraudulent.

For consumers whose lifestyle is fixed and regular, it seems that the cases where the data are clustered on the -axis are usually fewer. In addition, in this experiment the region of a fraudulent transaction is obtained randomly from the region of a legitimate transaction. However, since in real life the region of a fraudulent transaction is completely independent of the region of a legitimate transaction, there may be more fraudulent transaction data near the -axis.

7 Conclusion

This paper proposed methods that use the transaction patterns of a consumer to detect fraudulent card use.

For many reasons, such as changes in income, lifestyle, and place of abode, the consumption patterns of credit card users also change frequently. Therefore, it is difficult to detect a fraudulent card transaction when only certain fixed conditions have been set. In this paper, we present a method for learning automatically the consumption pattern of a customer, and detecting the fraudulent use of a card that has been duplicated or stolen based on the pattern.

This study also addressed 2-dimensional methods by not only dealing with the amount of transactions but also highlighting the patterns in the region in which a transaction occurs.