Locality statistics for anomaly detection in time series of graphs

Abstract

The ability to detect change-points in a dynamic network or a time series of graphs is an increasingly important task in many applications of the emerging discipline of graph signal processing. This paper formulates change-point detection as a hypothesis testing problem in terms of a generative latent position model, focusing on the special case of the Stochastic Block Model time series. We analyze two classes of scan statistics, based on distinct underlying locality statistics presented in the literature. Our main contribution is the derivation of the limiting properties and power characteristics of the competing scan statistics. Performance is compared theoretically, on synthetic data, and on the Enron email corpus. We demonstrate that both statistics are admissible in one simple setting, while one of the statistics is inadmissible in a second setting.

Index Terms:

Anomaly detection, scan statistics, time series of graphsI Introduction

The change-point detection problem in a dynamic network is becoming increasingly prevalent in many applications of the emerging discipline of graph signal processing. Dynamic network data are often readily observed, with vertices denoting entities and time evolving edges signifying relationships between entities, and thus considered as a time series of graphs which is a natural framework for investigation. An anomalous signal is broadly interpreted as constituting a deviation from some normal network pattern, e.g. a model-based characterization such as large scan statistics (c.f. § IV) or non-model based notions such as a community structure change, while a change-point is the time-window during which the anomaly appears.

Recently, many tailor-made approaches based on different models, aiming for change-point detection in graphs, have been proposed in a growing literature. [1] designs a two-stage Bayesian anomaly detection method for social dynamic graphs. Both its model and parallelization in computation are built on the assumption that the communication between each pair of individuals independently follows a counting process. In [2], an algorithm called NetSpot is created to find arbitrary but evolutionary anomalies that are maintained over a spatial or time window, i.e., the anomalous signal does not appears and then disappears instantaneously In [3], the subgraph anomaly detection problem in static graphs were analyzed through likelihood ratio tests under a Poisson random graph model. Finally, in [4], the norm of the eigenvectors of the modularity matrix were used for detection of an (anomalous) small dense subgraph embedded inside a large, sparser graph.

In this paper, we approach the dynamic anomaly/change-point detection problem through the use of locality-based scan statistics. Scan statistics are commonly used in signal processing to detect a local signal in an instantiation of some random field [5, 6]. The idea is to scan over a small time or spatial window of the data and calculate some locality statistic for each window. The maximum of these locality statistics is known as the scan statistic. Large values of the scan statistic suggests existence of nonhomogeneity, for example, a local region with significantly excessive communications. Under some homogeneity hypothesis, change-point detection can then be reduced to statistical hypotheses testing (c.f. § III) using scan statistics. For example, [7] builds up a simple testing framework with the null hypothesis being Erdös-Rényi and the alternative hypothesis being a graph containing an unusually dense subgraph. In the static graph setting, detection boundaries and conditions are given in [7] such that the scan statistics they specified for the testing is non-negligibly powerful. To capture anomalies (e.g. hacker attacks) in computer networks, [8] employs scan statistics through two shapes of locality statistics: ’star’ and ’k-path’. The power properties of ’star’ as a locality measure will be further explored in § V here.

In this paper, we identify excessive communication activity in a subregion of a dynamic network by employing the scan statistics defined in § IV, with denoting the number of vertex-standardization steps, denoting the number of temporal-normalization steps and denoting local neighborhood distance. We consider two variations of , namely and where and are two related but distinct locality statistics. The use of the locality statistics and is based upon earlier work of [9] and [10]. In particular, is introduced in [9] to detect the emergence of local excessive activities in time series of Enron graphs whereas is proposed in [10] to detect communication pattern changes in their department email network. Using the locality statistic , [11] constructs fusion statistics of graphs for anomaly detection while [12] presents an analysis of the Enron data set to illustrate statistical inference for attributed random graphs. However, all these cited works are mostly empirical in nature and do not provide much theoretical analysis of these locality-based scan statistics. Under the assumption that the time series of graphs is stationary before a change-point, we demonstrate in this paper that for and , the limiting and are the maximum of random variables which, under proper normalizations, follow a standard Gumbel distribution in the limit. Through these limiting properties, comparative power analysis between and for and is performed We demonstrate that both and are admissible if , while is inadmissible if . We hope that these theoretical results will help motivate subsequent work in understanding the interplay between locality statistics, vertex and temporal normalizations, and inference in time-series of graphs.

Our paper is structured as follows. We discuss a generative model for time series of graphs in § II. The problem of change-point detection is formulated in § III. The formulation associates a change-point in the time series with changes in the underlying generative model. We introduce in § IV two closely related notions of locality statistic, and , and their corresponding scan statistics and . The limiting properties and power characteristics for some representative instances of are given in § V and VI, while § VII presents experimental results regarding locality-based statistics on synthetic data and the Enron email corpus. We conclude the paper in § VIII with additional discussions of the two locality statistics and comments about possible applications and extensions of the framework presented herein.

I-A Notation

We introduce some notation that will be used throughout this paper. In this paper, we consider only undirected and unweighted graphs without self-loops. Generally, a graph is denoted by , with vertex set and edge set . The number of vertices of a graph is usually denoted by . For a graph on vertices, the vertex set is usually taken to correspond to the set . In our subsequent discussion, we might also partition into subsets, or blocks. If is partitioned into blocks of size vertices, then, with a slight abuse of notation, we shall denote by the vertices in block .

Let be a graph. For any , we write if there exists an edge between and in . We write for the shortest path distance between and in . For , we denote by the set of vertices at distance at most from , i.e., . For , is the subgraph of induced by . Thus, is the subgraph of induced by vertices at distance at most from .

II Random graph models

In this section, we briefly summarize the latent position model of [13], the dot product model of [14] and stochastic blockmodel of [15] and [16], since they are the underlying generative model for our graph at each time .

The latent position model is motivated by the assumption that each vertex is associated with a dimensional latent random vector . For any pair of vertices and , conditioning on the two latent positions and , the existence of an edge between and is independently determined by a Bernoulli trial with probability where is a symmetric link function . Namely, .

The random dot product graph model (RDPM) [14] is a special case of the latent position model. In the random dot product graph model, the link function is specified to be the Euclidean inner product, i.e., . Also, for each vertex , the latent random vector takes its values in the unit simplex so that where

The stochastic block model (SBM) of [15] and [16] is a random graph model in which each vertex is randomly assigned a block membership among where is the number of blocks. Given block memberships, the connectivity probabilities among all vertices are characterized by a symmetric matrix where denotes the block connectivity probability between blocks and . Namely, given and .

In this paper, we shall assume that the time series of random graphs are generated according to a stochastic block model where the block membership of the vertices are fixed across time while the connectivity probabilities matrix may varies with time (c.f. our formulation of the change-point detection problem in § III). That is to say, at some initial time, say , we randomly assign each vertex to a block membership among . Then at each subsequent time , follows a SBM with a probability matrix , conditioned on the initial block membership at time . Under this model, the graphs are conditionally independent over time, the conditioning being on the block membership of the vertices. This assumption on the generative model for the leads to a time series of graphs where the graphs are “weakly” dependent, i.e., they are dependent only on the block membership of the vertices at the initial time . If, instead, for each time , we resample the vertices’ block membership for then the resulting time series of graphs is independent.

Our construction of a time series of graphs in terms of the SBM as outlined above is a special case of the following model constructed using the random dot product graphs111The Dirichlet distribution is a multivariate generalization of the beta distribution and correspond to a distribution of points in the unit simplex. The Dirichlet distribution, , , has density .

-

1.

For each and ,

-

2.

For each and pair of vertices ,

where is a fixed location parameter for the Dirichlet distribution and is the concentration parameter that will be explained now.

It is worthwhile to note that for all means all vertices follow the same probabilistic behavior (uniform on the simplex) and implies that has a point mass distribution at for each vertex. In the case , the random dot product model can be further reduced to the stochastic block model (SBM) by letting vertices sharing the same share the same block membership. Next, we re-denote by the common Dirichlet location parameter corresponding to block and is partitioned into distinct blocks if there are distinct ’s in total. Accordingly, as , . We note that the above Dirichlet can be viewed as generating a time-series of graphs where the graphs are also “weakly” dependent, e.g., dependency between graphs at time and being on the location and concentration parameters for the vertices. Other generalizations of the above construction for generating time series of graphs are also possible. See, e.g., [17] and [18] for examples of constructions where the time series of graphs depends on some underlying latent stochastic processes.

III Change-point detection problem in Stochastic Block model formulation

An important inference task in time series analysis is the problem of anomaly or change-point detection. An anomaly is broadly interpreted to mean deviation from a “normal” pattern and a change-point is the time-window during which the anomalous deviation occurs. For example, in social networks, we usually represent a time-evolving collection of emails, phone calls, web pages visits, etc. as a time series of graphs and we want to infer, from , if there exists anomalous activities, e.g., excessive phone calls among a subgroup in the network. In the detection problem described below in § III and its theoretical analysis presented in § V and § VI, we shall implicitly assume, for ease of exposition, that the are independent. As we pointed out in our discussion of the generative model for time-series of graphs in § II, this independence corresponds to conditioning on the right parameters. In the setup of our theoretical analysis in this paper, this corresponds to conditioning on the block membership of the vertices, which are fixed in time. Related discussions in the context of the latent process models of [17] and [18] are given in § VIII.

Statistically speaking, we want to test, for an unknown but non-random , the null hypothesis that is not a change-point against the alternative hypothesis that is a change-point. There are many different ways to formulate the notion that is a change-point. The following formulation, in the contex of our discussion, is reasonable and sufficiently general and forms the basis of our subsequent investigation.

We say that is a change-point for if there exists distinct choices of , independent of such that

where denote the stochastic blockmodel with block connectivity probabilities and unknown, but fixed in time, block memberships . In contrast, the null hypothesis, i.e. the nonexistence of change-point, is

That is to say, under the alternative, at time , a subset of the vertices change their behavior. The vertices whose behaviour changes correspond to the vertices with block memberships whose corresponding rows in the connectivity matrix changes, i.e., from to . As permutation of the vertex block labels does not affect our subsequent analysis, we will refer to as the change parameters. As a convention, if , we assume all vertices follow their original dynamics for all .

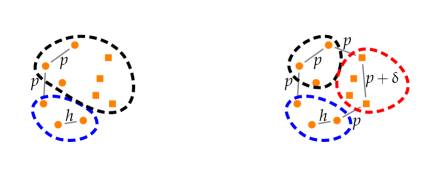

In the following, we discuss a specific form for and , illustrating, albeit in an exaggerated manner, the chatter anomaly, i.e., a subset of vertices with altered communication behavior in an otherwise stationary setting.

| (1) |

| (2) |

for some , with being of size

For this form of and , the blocks have their own (possibly distinct) self-connectivity probabilities which are diagonal entries of matrices. In other words, before the change-point, each of the blocks up to have self-connectivity probability . The block is of size with self-connectivity probability , representing the probabilistic behaviors of the vast majority of actors in a very large network. The case where is of interest because we can consider each of the as representing a “chatty” group for time , and at , the previously non-chatty group becomes more chatty. See Figure 1 for a notional depiction of and for the case of blocks with . The detection of this transition for the vertices in is one of the main reasons behind the locality statistics that will be introduced in § IV.

IV Locality statistics for change-point detection in time series of graphs

IV-A Two locality statistics

Suppose we are given a time series of graphs where is independent of , i.e., the graphs are constructed on the same vertex set . We now define two different but related locality statistics on . For a given , let be defined for all and by

| (3) |

counts the number of edges in the subgraph of induced by , the set of vertices at a distance at most from in . In a slight abuse of notation, we let denote the degree of in . The statistic was first introduced in [9]. [19] investigated the use of in analyzing the Enron data corpus.

Let and be given, with . Now define for all and by

| (4) |

The statistic counts the number of edges in the subgraph of induced by .

Once again, with a slight abuse of notation, we let denote the degree of in , where for and with denotes the graph . The statistic is motivated by a statistic named the permanent window metric introduced in [20]. The permanent window metric was meant to capture events involving not just a single individual but the whole community. As the community at time is assumed to be approximated by , the statistic uses the community structure at time in its computation of the locality statistic at time . Through this measure, a community structure shift of can be captured even when the connectivity level of remains unchanged across time, i.e., when the stays mostly constant as changes in some interval. With the purpose of determining whether is a change-point, two kinds of normalizations based on past and locality statistics and their corresponding normalized scan statistics are introduced in the next subsection.

IV-B Temporally-normalized statistics

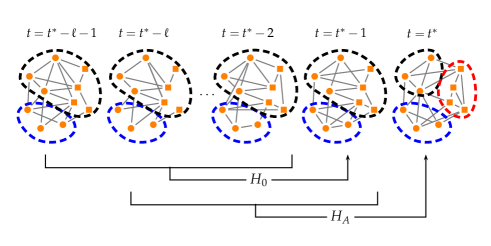

Let be either the locality statistic in Eq. (3) or in Eq. (4), where for ease of exposition the index is a dummy index when . We now define two normalized statistics for , a vertex-dependent normalization and a temporal normalization. These normalizations and their use in the change-point detection problem are depicted in Figure 2.

For a given integer and , we define the vertex-dependent normalization of by

| (5) |

where and are defined as

| (6) | |||

| (7) |

We then consider the maximum of these vertex-dependent normalizations for all , i.e., we define a by

| (8) |

We shall refer to as the standardized max-degree and to as the standardized scan statistics. From Eq. (5), we see that the motivation behind vertex-dependent normalization is to standardize the scales of the raw locality statistics . Otherwise, in Eq. (8), a noiseless vertex in the past who has dramatically increasing communications at the current time would be inconspicuous because there might exist a talkative vertex who keeps an even higher but unchanged communication level throughout time.

Finally, for a given integer , we define the temporal normalization of by

| (9) |

where and are defined as

| (10) | |||

| (11) |

The motivation behind temporal normalization, based on recent time steps, is to perform smoothing for the statistics , similar to how smoothing is performed in time series analysis. Large values of the smoothed statistic indicates an anomaly where there is an excessive increase in communications among a subset of vertices. We will use these as the test statistics for the change-point detection problem described in § III.

We note that because for when , the choice of locality statistic for does not matter when . For convenience of notation, since is essentially a function of the , we denote by and the when the underlying statistic is and , respectively.

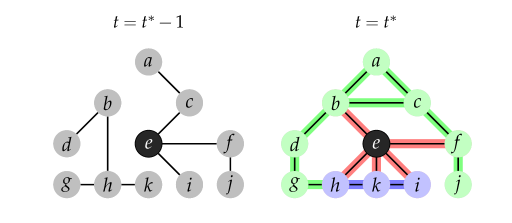

After the above introduction of the temporally-normalized statistics with three parameters , we now present a simple toy example to illustrate a key step in the calculation of , namely the calculation of the vertex-dependent normalization presented in Eq. (5). In Figure 3, the table calculates , when and , for different underlying statistics and different values of . More concretely, because , if the underlying statistic is and if the underlying statistic is .

| 5 | 7 | 3 | 3 | 2 | 4 | |

| 5 | 7 | 2 | 4 | 3 | 3 | |

V Power Estimates of

For algebraic simplicity, in Section V and VI, we consider a particularly simple form of and where

| (12) |

| (13) |

With above form of and , in this section, we will derive the limiting properties of and where and . Theorem 1 below shows that in the limit is the maximum of random variables that converge to the standard Gumbel distributions under proper normalizations.

Theorem 1.

Let be a time series of random graphs according to the alternative detailed in § III. In particular, for and for with and being of the form in Eq. (12) and Eq. (13), respectively. Let denote the statistic with , , and . Let denote the Gumbel distribution with location parameter and scale parameter . For a given , let and be given by

Then as , has following properties:

| (14) | |||

| (15) |

where

and the are given by

C is some explicit, computable constant. Similarly, let denote with , , and . Then as ,

| (16) | |||

| (17) |

where

and the in this case are

We note the following corollary to Theorem 1 for the case of blocks.

Corollary 2.

Assume the setting in Theorem 1 with . Let be given. Let be the power of the test statistic when for testing the hypothesis that is a change point at a significance level of . Similarly, let be the power of the test statistic when for testing the same hypothesis at the same significance level of . Then, as , and have the following relationship

-

1.

implies .

-

2.

implies .

-

3.

implies .

-

4.

implies

-

5.

implies .

-

6.

implies

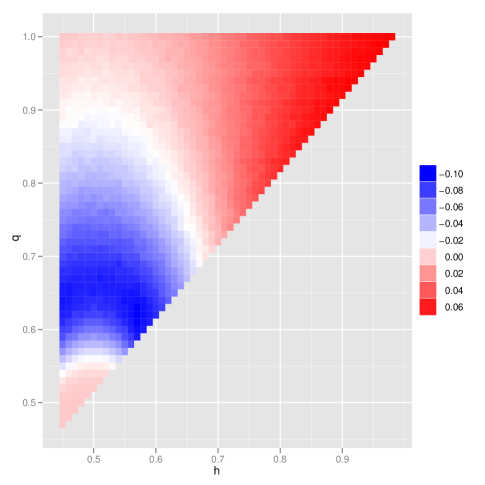

From Corollary 2, an unanswered question is whether there exists a dominance between and . By using Theorem 1, we now present an example to show that both statistics are admissible if we restrict the test statistic space to only two elements- and . That is, neither statistic has a statistical power dominance. Our setup is as follows. Let . For each pair satisfying and , we generate a null and alternative hypothesis pair and according to the model in § III with blocks, i.e.,

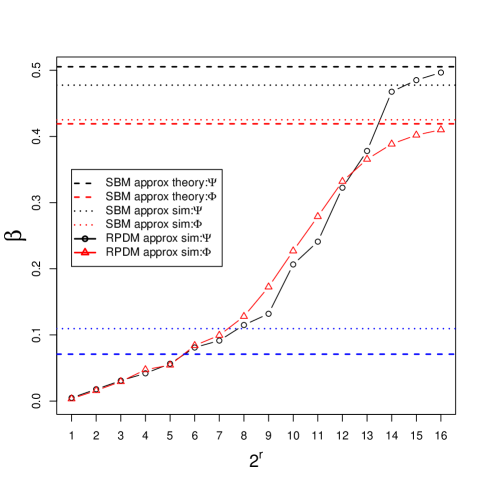

with and being functions of and ( where the constant is dependent on and ). In order to compare sensitivities of and in detection, we then calculate by deriving the limiting property of using Eqs. (14) and (15) and the limiting property of using Eqs. (16) and (17). The result is illustrated in Figure 4 where we have plotted for different combinations of and . Figure 4 indicates that the two statistics and are both admissible because achieves a larger statistical power in the blue-colored region but a smaller power in the red-colored region.

We now analyze the use of Theorem 1 as a large-sample approximation to and . From Figure 4 with , we choose a pair, with , namely and . We then estimate the power of and by repeated sampling of graphs from stochastic blockmodel with parameters, for the null distribution and for the alternative distribution. The result is presented in Figure 5. We see that the large-sample approximation obtained via Theorem 1 matches well with sampling from the stochastic blockmodel (SBM). Figure 5 also includes power estimates for the random dot product model (RDPM) with varying concentration parameter and predetermined location parameters . Specifically, are carefully chosen such that their Euclidean inner products match corresponding block connectivity probabilities i.e., specified above. We see that, as increases, the power estimates for the random dot product model matches well with those of the stochastic blockmodel and large-sample approximation. Finally Figure 5 also includes power estimates for the locality statistics based on and for , i.e., no vertex-dependent normalization and is equivalent to the use of the max degree statistic to test against . These are represented as dashed and dot blue lines, corresponding to large-sample approximation and Monte Carlo simulations, respectively. Clearly, vertex-dependent normalization leads to better performance for this and pair.

VI Power Estimates of

In this section, we provide investigations of and with a larger scale parameter instead of . We keep and the same as before and derive the limiting properties of and . To make conclusions concise and presentable, firstly, we delve into the limiting properties in the model presented in § III with number of blocks .

Proposition 3.

Assume the same setting in Theorem 1 with . As and , has the following properties:

where

and the are given by

Likewise,

where

and the are given by

Naturally, the limiting properties of and as given above offer the following power comparison result.

Proposition 4.

In the model shown in Figure1, Let be given, be the power of the test statistic when for testing the hypothesis that is change point at a significance level of and be the power of the test statistic when for testing the same hypothesis at the same significance level of . As , and have the following relationship:

-

1.

implies .

-

2.

implies .

Consequently, Proposition 4 leads to the conclusion that the performance of dominates in the -block model. Moreover, this superiority can be generalized to the case with any given number of blocks . This is because each block with in -blocks model follows a similar probabilistic behavior as block in -blocks model while the power of hypothesis testing is otherwise determined by the change of probabilistic behavior of block . In the limiting condition with , both and in -blocks model can be characterized as a function of only. In other words, though , the ”chatty” groups do not make any contribution on or . Hence, the number of ”chatty groups”, namely , is independent of the fact of dominance of . Due to the superiority of , only the limiting properties of in the general B-block model is given below.

Theorem 5.

Let be a time series of random graphs according to the alternative detailed in § III. In particular, for and for with and being of the form in Eq. (1) and Eq. (2), respectively. Let denote the statistic with , , and .

Then as , has the following properties:

where

and the are given by

Corollary 6.

Assume the setting in Theorem 5. Let be the power of the test statistic for and be the power of the test statistic for . Then, as and , and thus is inadmissible.

In §V and

§VI, for simplicity of analytic

investigations, we theoretically obtain power estimates of

and under the

restrictions of and . Besides analytic

investigations, we also empirically study power performances of

and with other

combinations via Monte Carlo simulations. In this

experiment, we let range from to and range from

to . In each Monte Carlo replicate, a time series of random

graphs based on the SBM considered in

§V, where

, is

sampled. Next,

,,

and are calculated individually

according to specific . After replicates, for

each test statistic, the largest empirical power (denoted by

) and the corresponding optimal choice

of (denoted by ) is obtained and

summarized in Table I.

| 0.571 | (1,10) | |

| 0.758 | (1,9) |

VII Experiment

We use the Enron email data used in [19] for this experiment. It consists of time series of graphs with vertices for each week , where we draw a unweighted edge when vertex sends at least one email to vertex during a one week period.

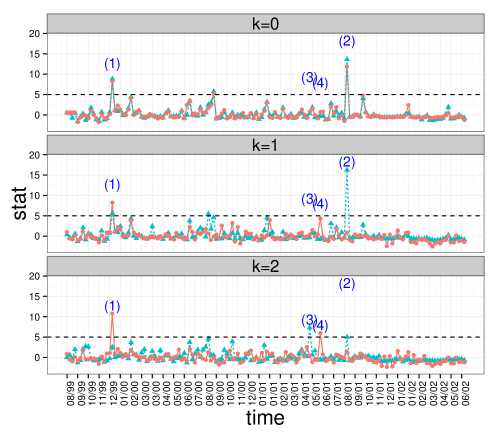

After truncating first 40 weeks for vertex-standardized and temporal normalizations, Figure 6 depicts (SeaGreen) and (Orange) in the remaining 149 weeks from August 1999 to June 2002. In this experiment, we choose both , used in [19], to keep the comparisons between the two papers meaningful. As indicated in [19], detections are defined as weeks such that . Hence, from Figure 6 we have following observations and reasonings.

-

1.

and indicate a clear anomaly at in December 1999. This coincides with the happening of Enron’s tentative sham energy deal with Merrill Lynch to meet profit expectations and boost stock price [21]. The center of suspicious community-employee is identified by all five statistics.

-

2.

, , and capture an anomaly at in the mid-August 2001. This is the period that Enron CEO Skilling made a resignation announcement when the company was surrounded by public criticisms shown in [21]. The center of suspicious community-employee is identified by these four statistics.

-

3.

signifies an anomaly at in late April 2001 where fails to alert for any . This phenomenon occurs because captures the employee whose second-order neighborhood contains emails at but email in his second-order neighborhoods of previous 20 weeks. That is, the time-dependent second-order neighborhood had no communication in the period from to . On the other hand, this behavior cannot be monitored by because the change of communication frequency in a fixed second-order neighborhood , measured by locality statistics , is not so significant. More concretely, the number of emails in the unchanged has a mean of and a standard deviation of from to . In [21], this anomaly appears after the Enron Quaterly Conference Call in which a Wall Street analyst Richard Grubman questioned Skilling on the company’s refusal of releasing balance sheet but then got insulted by Skilling.

-

4.

shows a detection on at before June 2001 over . This comes from the fact that the fixed second-order neighborhood of employee at , i.e. , has a small standard deviation in previous 20 weeks while the communications in time-dependent neighborhoods has a large standard deviation . Practically speaking, in this case, a dramatic increment of email contacts in the certain community could be captured by but ignored by because unstable communication patterns in offsets the sensitivity of signal. According to [21], this anomaly corresponds to the formal notice of closure and termination of Enron’s single largest foreign investment, the Dabhol Power Company in India.

In summary, observations 1 and 2 demonstrate that in some cases both and are capable of capturing the same community which has a significant increment of connectivity. Besides, in some situations shown in observations 3 and 4, and achieve different detections due to its adaptability.

VIII Conclusion & Discussion

This paper has summarized a generative latent position model for time series of graphs and set up the change-point detection problem in time series of graphs in terms of stochastic block models. Then we have proposed the way of dealing with change-point detection through the use of scan statistics and constructed from two different locality statistics and respectively. We derived the limiting properties for four representative instances of locality-based scan statistics and . The limiting properties were then used to derive estimates for the power of the tests.

The simulation experiments indicate that the analytic power estimates, even when they are limited in scope, are useful in answering some important questions about the locality statistics. In particular, it was shown that and are both admissible with respect to one another when . In addition, if , it is worthwhile to note that , compared with , is inadmissible but computationally inexpensive. For instance, in order to complete -step vertex-dependent normalization calculation presented in Eq.(5), we have to record previous -step graphs to calculate if the underlying locality statistic is . However, if the underlying locality statistic is , graph storage is not necessary and recording only the previous -step statistics is sufficient. Furthermore, the power estimates are also useful for reasoning about the behavior on more complicated models without independencies assumption, such as the latent process model proposed in [17]. [17] builds up a latent process model for time series of attributed graphs based on a random dot process model. Having vertices governed by individual continuous-time finite-state stochastic processes, this model generates a time series of dependent attributed random graphs, or equivalently, conditioning on the sample paths of the stochastic processes, the graphs are independent. [17] also provides two approximations to the exact latent process model. The first order approximation is the stochastic blockmodel which gives rise to a time series of independent random graphs with independent edges. The second order approximation corresponds to the random dot product model which gives rise to a time series of independent random dot product graphs. Both of these approximations are presented in § II.

The investigations presented in this paper do not take into account attributes on the edges. The incorporation of edge attributes into the current paper is, however, straightforward. For example, [22] handles attributes by linear fusion, and many of the results there can be adapted to the current paper. In particular, one can define fused locality statistics for attributed graphs. Power estimates for these locality statistics can be derived in a similar manner to those presented in this paper. Other considerations, e.g., optimal fusion parameters, can also be investigated. However, the statistics considered in [22] are only temporally normalized and does not contain a vertex dependent normalization. Thus, the derivation of their limiting properties are much less involved. In addition, as the experimental results in Fig 5 shown, the vertex dependent normalization does lead to improved statistical power in many situations of interest.

Anomaly detection in dynamic graphs has applications in diverse areas, e.g., predicting the emergence of subgroups within an organization, monitoring disease spread in public network, detecting modules of cancer and metastasis communities in Protein-protein interaction (PPI) network. We envision that these and many other applications will benefit from the kind of investigations outlined in this paper. However, much remains to be done, both mathematically and computationally. We list here some aspects that have not been (sufficiently) addressed in the paper.

-

1.

Besides this paper, [22] also investigated for cases , , and under the SBM setting. However, power-estimates for other more complex locality-based scan statistics, such as for , and , remain to be investigated.

-

2.

Locality statistics based on can be readily computed in a real-time streaming data environment, in contrast to those based on . Thus, the adaption or approximation of locality statistics based on for streaming environments is of interest.

-

3.

Power-estimates for locality statistics under the random dot product model setting. The limiting distributions, even for the simplest locality statistics, are currently unavailable.

Acknowledgment

This work was partially supported by Johns Hopkins University Human Language Technology Center of Excellence (JHU HLT COE), and the XDATA program of the Defense Advanced Research Projects Agency (DARPA) administered through Air Force Research Laboratory contract FA8750-12-2-0303.

[Proof of some stated results]

Appendix A Appendix

In this appendix, we provide proofs of theorems,

propositions and corollaries presented in

§ V and

VI.

Theorem 1.

Firstly, we investigate the case

that the underlying locality statistic is . We will derive the

limiting property of for in some detail. The property of

when can be derived in a similar

manner.

As and , for any , we have

from

Eq. (5) and Eq. (6). Without

loss of generality, let us assume and divide

into two parts with and :

where ;

where .

Since and are independent, we have

| (18) |

where

Next, plug in and into Eq. (18), we obtain

We can show that the dependency among the is negligible by showing that the correlation between any two of the goes to sufficiently fast as . For and in block ,

Hence, the sample maximum of converges to the sample maximum of i.i.d random variables where ([23], Theorem ). Also, it is known that the sample maximum of i.i.d random variables weakly converges to the Gumbel distribution ([24], § ). One then verifies that the composition of above weak convergences still holds (see e.g. proof of Proposition 5 in [22]) and we thus have

Eq.(8) and Eq. (9) then implies that

That is, the maximum of over all vertices is equivalent to the maximum of over all blocks where converges to under proper normalization

Similarly, the case when can be derived through the same approaches above. The limiting property of with then has the form in Eq. (14) with variations of and for the normalization of .

We now consider the case where the underlying locality statistic being

. The derivation of limiting property of

for is given below. The derivation of

the limiting property of for

is similar and can be obtained with minor changes.

Let’s

assume , from Eq.(4) to (6),

where and

where .

Because , counts the number of edges, for vertex , appearing in but disappearing in . Accordingly, the edge is independently counted with probability to neighbors in and to neighbors in respectively. That is,

where .

By the central limit theorem, we have

| (19) |

where

Similarly, after plugging and into Eq. (19), we obtain

For locality statistic , the dependency among is also negligible because

Therefore by following the same procedures of reasoning the limiting distribution of , we can also obtain

where .

Thus, is the maximum of over blocks as desired.

∎

Corollary 2.

The limiting distributions of and derived in the proof Theorem 1 provides that, under ,

and, under ,

Accordingly, the ratio of the shift in the mean, from null to alternative, over the standard deviation of for each vertex would be . We obtain two relationships between and on the basis of the order of :

-

1.

if , the ratio approaches to and thus implies .

-

2.

if , then such that as which implies .

Likewise, from Theorem 1, the limiting distributions of under null and alternative respectively are

The relationship between and is more involved when are included. In order to clarify the order dominance relationship between and , there are five separate cases to be considered:

-

1.

if , as , share the same mean and variance under both and , thus .

-

2.

if , and have the same order so that the increment ,, is not negligible and implies .

-

3.

if , whether is determined by if under is larger than under . In fact, if , as under both and , hence . Otherwise, in contributes to the power increment.

-

4.

if , dominates in the limit thereby the location shift in block results in and thus .

-

5.

if , whether leads to a power increment depends on the sign of . If such that being positive, under both and as because . On the contrary, if , enables to increase from to . Thus, we have

∎

Proposition 3.

We present a sketch of the proof based on arguments from [25] for the case where the underlying locality statistic is . The case where the underlying locality statistic is follows from the proof of Theorem 5.

Let , locality statistics and are respectively decomposed as follows

where

and

where

Hence, when and are substituted, we have

Thus, by using similar approaches given in the proof of lemma and lemma from [25], we obtain, as ,

and

where and . This leads to the fact that follows standard Gumbel distribution and . Similar arguments apply to . ∎

Before proving Theorem 5, we state and prove a technical lemma on the correlations among the .

Lemma 7.

Let and be two independent Erdös-Rényi graphs with connectivity probability , i.e., and . For each , is defined according to Eq. (5). Then for any pair of vertices and , the correlation between and is of order for .

Proof.

From Eq. (5) and (6), for any pair of vertices ,

| (20) |

We then consider to decompose into two parts representing the cardinalities of two disjoint sets of edges.

where the intuitive interpretations behind two terms are listed below:

Also, is decomposed into two terms as well.

where the intuitive interpretations behind two terms are listed below:

Similarly, and are

decomposed with the same structure. By expanding above decompositions

into Eq. (20), we have the following table recording

terms and their signs in (20).

In Table II, all terms

earning the same color (blue, green or

magenta) and same positive/negative sign are

symmetric. Additionally, the terms having the same mark

( or ) are canceled out due to the fact

. More concretely, for example, for four

terms marked by blue, we have

. The

first and third equality are guaranteed by symmetry property. The

second equality holds because and share the same

conditional distribution, , given

. That is,

and hence

with application of law of

total covariance.

We now return to Eq. (20). The above

reasoning gives

The last equality holds because the Cauchy-Schwarz

inequality guarantees each of fours term are where

and .

In the following, to compute , is decomposed as

where

By applying law of total variance, we reach the following variance order estimation

Therefore, it follows that

as desired. ∎

Theorem 5.

Again, to avoid redundant arguments, we only provide derivations of limiting distribution of and the case can be achieved in the same approach. Let , locality statistics and are respectively decomposed as follows:

| (21) |

where

and

| (22) |

where

Accordingly, the mean of is estimated as follows

Under our setting of and ,

the penultimate equality is obtained easily because and

share the same distribution and share the same

distribution with except .

Now let’s consider the

estimation of since the exact

derivation of , through the use

of law of total variance, is tedious. Due to the assumption

and decompositions

in Eq.(21) and

Eq.(22), instead we express variance of

as

Thus, the central limit theorem leads to

According to Lemma 7, dependencies among are negligible and thus

Through similar arguments as in Theorem 1, we can show that . ∎

Corollary 6.

This corollary is a generalization of Proposition 3 and Proposition 4. The underlying idea is as follows. In the model presented at the beginnning of § V, the variation of number of chatty blocks before makes no difference on the sensitivity of statistics and as long as the orders of chatty blocks are . Namely, in the limiting case, and are functions of and independent of . We can then extend the power comparison conclusion from Proposition 4 for to the general case. The details are somewhat tedious and are omitted. ∎

References

- [1] N. A. Heard, D. J. Weston, K. Platanioti, and D. J. Hand, “Bayesian anomaly detection methods for social networks,” The Annals of Applied Statistics, vol. 4, no. 2, pp. 645–662, 2010.

- [2] M. Mongiovi, P. Bogdanov, R. Ranca, A. K. Singh, E. E. Papalexakis, and C. Faloutsos, “Netspot: Spotting significant anomalous regions on dynamic networks,” in SIAM International Conference on Data Mining, May 2013.

- [3] B. Wang, J. M. Phillips, R. Schreiber, D. Wilkinson, N. Mishra, and R. Tarjan, “Spatial scan statistics for graph clustering,” in SIAM International Conference on Data Mining, 2008.

- [4] B. A. Miller, N. T. Bliss, and P. J. Wolfe, “Subgraph detection using eigenvector L1 norms,” in Neural Information Processing Systems Foundation, 2010.

- [5] J. Glaz, J. Naus, and S. Wallenstein, Scan Statistics. Springer, 2001.

- [6] M. Kulldorff, “A spatial scan statistic,” Communications in Statistics- Theory and Methods, vol. 26, no. 6, pp. 1481–1496, 1997.

- [7] E. Arias-Castro and N. Verzelen, “Community detection in random networks,” 2013, arXiv preprint. http://arxiv.org/abs/1302.7099.

- [8] J. C. Neil, “Scan statistics for the online discovery of locally anomalous subgraphs,” Ph.D. dissertation, The University of New Mexico, May 2011.

- [9] C. E. Priebe, “Scan statistics on graphs,” Johns Hopkins University, Tech. Rep. 650, 2004.

- [10] X. Wan, N. Kalyaniwalla, J. Janssen, and E. Milios, “Capturing causality in communications graphs,” in DIMACS/DyDAn workshop on computational methods for dynamics interaction, 2007.

- [11] Y. Park, C. E. Priebe, and A. Youssef, “Anomaly detection in time series of graphs using fusion of graph invariants,” IEEE Journal of Selected Topics in Signal Processing, vol. 7, no. 1, pp. 67–75, Feb 2013.

- [12] C. E. Priebe, Y. Park, D. J. Marchette, J. M. Conroy, J. Grothendieck, and A. L. Gorin, “Statistical inference on attributed random graphs: Fusion of graph features and content: An experiment on time series of enron graphs,” Computational Statistics and Data Analysis, vol. 54, pp. 1766–1776, 2010.

- [13] P. Hoff, A. E. Raftery, and J. M. Tantrum, “Latent space approaches to social network analysis,” Journal of the American Statistical Association, vol. 97, pp. 1090–1098, 2002.

- [14] S. Young and E. Scheinerman, “Random dot product models for social networks,” in Proceedings of the 5th international conference on algorithms and models for the web-graph, 2007, pp. 138–149.

- [15] P. W. Holland, K. Laskey, and S. Leinhardt, “Stochastic blockmodels: First steps,” Social Networks, vol. 5, pp. 109–137, 1983.

- [16] Y. J. Wang and G. Y. Wong, “Stochastic Blockmodels for Directed Graphs,” Journal of the American Statistical Association, vol. 82, pp. 8–19, 1987.

- [17] N. H. Lee and C. E. Priebe, “A latent process model for time series of attributed random graphs,” Statistical Inference for Stochastic Processes, vol. 14, pp. 231–253, 2011.

- [18] N. H. Lee, J. Yoder, M. Tang, and C. E. Priebe, “On latent position inference from doubly stochastic messaging activities,” Multiscale modeling and simulation, 2013, in press.

- [19] C. E. Priebe, J. M. Conroy, D. J. Marchette, and Y. Park, “Scan statistics on Enron graphs,” Computational and Mathematical Organization Theory, vol. 11, pp. 229–247, 2005.

- [20] X. Wan, J. Janssen, N. Kalyaniwalla, and E. Milios, “Statistical analysis of dynamic graphs,” in Proceedings of AISB06: Adapation in Artificial and Biological Systems, 2006, pp. 176–179.

- [21] J. Galasyn, “Enron chronology,” online source, http://www.desdemonadespair.net/2010/09/bushenron-chronology.html.

- [22] M. Tang, Y. Park, N. H. Lee, and C. E. Priebe, “Attribute fusion in a latent process model for time series of graphs,” IEEE Transactions on Signal Processing, vol. 61, no. 7, pp. 1721–1732, April 2013.

- [23] S. M. Berman, “Limit theorems for the maximum term in stationary sequences,” Annals of Mathematical Statistics, vol. 35, no. 2, pp. 502–516, 1964.

- [24] J. Galambos, The Asymptotic Theory of Extreme Order Statistics. John Wiley & Sons, 1987.

- [25] A. Rukhin and C. E. Priebe, “On the limiting distribution of a graph scan statistic,” Communications in statistics-Theory and Methods, vol. 41, no. 7, pp. 1151–1170, 2012.