Inference and testing for structural change in time series of counts model

Paul DOUKHAN∗ and William KENGNE

AGM, Université de Cergy Pontoise, 2 avenue Adolphe Chauvin. 95302 Cergy-Pontoise, France (111Supported by Laboratory of Excellence MME-DII http://labex-mme-dii.u-cergy.fr/).

∗ IUF, Universitary institute of France.

E-mail: paul.doukhan@u-cergy.fr ; william.kengne@u-cergy.fr

Abstract : We consider here together the inference questions and the change-point problem

in Poisson autoregressions (see Tjøstheim, 2012).

The conditional mean (or intensity) of the process is involved as a non-linear function of it past values and the past observations.

Under Lipschitz-type conditions, it is shown that the conditional mean can be written as a function of lagged observations.

In the latter model, assume that the link function depends on an unknown parameter . The consistency and the asymptotic normality

of the maximum likelihood estimator of the parameter are proved. These results are used to study change-point problem in the parameter .

We propose two tests based on the likelihood of the observations. Under the null hypothesis (i.e. no change), it is proved that both those test

statistics converge to an explicit distribution. Consistencies under alternatives are proved for both tests. Simulation results show how those procedure work practically, and an application to real data is also processed.

Keywords: time series of counts; Poisson autoregression; likelihood estimation; change-point; semi-parametric test.

1 Introduction

Count models are of a large current interest, see the discussion paper Tjøstheim (2012).

Integer-valued time series appear as natural for modeling count events. Examples may be found in epidemiology (number of new infections),

in finance (number of transactions per minute), in industrial quality control (number of defects);

see for instance Held et al. (2005), Brännäs and Quoreshi (2010) and Lambert (1992).

Real data are definitely not stationary. Several ways to consider such structural changes are possible as this was demonstrated during the thematic cycle Nonstationarity and Risk Management held in Cergy-Pontoise during year 2012 (222http://www.u-cergy.fr/en/advanced-studies-institute/thematic-cycles/thematic-cycle-2012/finance-cycle.html).

Structural breaks are a reasonable possibility for this, when no additional knowledge is available. The paper is thus aimed at considering such changes in regime for a large class of integer valued time series.

Let be an integer-valued time series and

the -field generated by the whole past at time , we denote by the

conditional distribution of given the past. Models with various marginal distributions and dependence

structures have been studied for instance Kedem and Fokianos (2002), Davis et al. (2005), Ferland et al. (2006), Davis and Wu (2009),

Wei (2009).

Fokianos et al. (2009) considered the Poisson autoregression such that is Poisson distributed with a intensity

which is a function of and . Under linear autoregression, they prove both the consistency and the asymptotic normality

of the maximum likelihood estimator of the regression parameter, by using a perturbation approach, which allows to used the standard Markov ergodic setting.

Fokianos and Tjøstheim (2012) extend the method

to nonlinear Poisson autoregression with for nonlinear measurable functions and .

In the same vein, Neumann (2011) had studied some large situation where . He focused on the absolute regularity and the

specification test for the intensity function, while the recent work of Fokianos and Neumann (2013) studied goodness-of-fit tests which

are able to detect local alternatives.

Doukhan et al. (2012), consider a more general model with infinitely many lags.

Stationarity and the existence of moments are proved by using a weak dependent approach and contraction properties.

Later, Davis and Liu (2012) studied the model where the distribution belongs to a class of

one-parameter exponential family with finite order dependence. This class contains Poisson and negative binomial distribution.

From the theory of iterated random functions, they establish the stationarity and the absolute regularity properties of the process.

They also prove the consistency and asymptotic normality of the maximum likelihood estimator of the parameter of the model.

Douc et al. (2012) considers a class of observation-driven time series which covers linear, log-linear, and threshold Poisson autoregressions.

They approach is based on a recent theory for Markov chains based upon Hairer and Mattingly (2006) recent work; this allows existence and uniqueness of the invariant distribution for Markov chains without irreducibility. They also proved consistency of the conditional likelihood estimator of the model (even under false models); the asymptotic normality is not yet considered in this setting.

For change point procedures, Kang and Lee (2009) proposed CUSUM procedure for testing for parameter change in a first-order random coefficient integer-valued autoregressive model

defined through thinning operator. Fokianos and Fried (2010, 2012) studied mean shift in linear and log-linear Poisson autoregression. The dependence between the level shift and time

allows their model to detect several types of interventions effects such as outliers. Franke et al. (2012) consider parameter change in Poisson

autoregression of order one. Their test are based on the cumulative sum of residuals using conditional least-squares estimator.

In this article, we first consider a time series of counts satisfying :

| (1) |

where and a measurable non-negative function. The properties of the general class of Poisson autoregression model (1) have been studied by Doukhan et al. [13]. According to the fact that the model (1) can take into account the whole past information of the process, it dependence structure is more general than those studied before. Proceeding as in Doukhan and Wintenberger (2008), we show that under some Lipschitz-type conditions on , the conditional mean can be written as a function of the past observations. This leads us to consider the model

| (2) |

where is a measurable non-negative function. We assume that is know up to some parameter belonging to a compact set . That is

| (3) |

Many classical integer-valued time series satisfying (3) (see the examples below).

Remark that, model (3) (as well as models (1) and (2)) can be represented in terms of Poisson processes.

Let be a sequence of independent Poisson processes of unit intensity. can be seen as a number (say ) of events

that occurred in the time interval . So, we have the representation

| (4) |

The paper is first work out the asymptotic properties of the maximum likelihood estimator of the model (3). We assume that the function satisfies some classical Lipschitz-type inequality and investigate sufficient conditions for the consistency and the asymptotic normality of the maximum likelihood estimator of . Contrary to Fokianos et al. [19] the increasing of the function (not easy to define here) as well as the existence of the fourth order derivative of the function are not needed. Although the models studied by Davis and Liu [9] and Douc et al. [11] allow large classes of marginal distributions, the infinitely many lags of model (1) (or model (3)) makes it allows a large type of dependence structure.

The second contribution of this work are the two tests for change detection in model (3). We propose a new idea to take into account the change-point

alternative. This make that, the procedures proposed will be numerically easy to apply than that proposed by Kengne (2012). The consistency under the alternative

are proved. Contrary to Franke et al. [20], the multiple change alternative has been considered and the independence between

the observation before and after the change-point is not assumed. Note that, the intervention problem studied by Fokianos and Fried

[15, 16] is intended to sudden shift in the conditional means of the process. In the classical change-point setting, such

intervention will be asymptotically negligible.

In the forthcoming Section 2, it is provided some assumptions on model with examples. Section 3 is devoted to the definition of the maximum likelihood estimator with it asymptotic properties. In Section 4, we propose the tests for detecting change in parameter of model (3). Some simulation results and real data application are presented in Sections 5 and 6 and the proofs of the main results are provided in Section 7.

2 Assumptions and examples

2.1 Assumptions

We will use the following classical notations:

-

1.

for any ;

-

2.

for any compact set and for any function , ;

-

3.

it is a random variable with finite moment of order , then ;

-

4.

for any set , denotes the interior of .

A classical Lipschitz-type conditions is assumed on the model (1).

Assumption AF : There exists a sequence of non-negative real numbers satisfying and such that for any ,

Under assumption (AF), Doukhan et al. [13] have shown that there exists a solution which is -weakly dependent strictly stationary with finite moment of any order. The following proposition show that the conditional mean of model (1) can be expressed as a function of only the past observations of the process.

Proposition 2.1

Under (AF), there exists a measurable function such that the strictly stationary ergodic solution of model (1) satisfying almost surely

Proposition 2.1 shows that, the information contained in the unobservable process can be capture by the observable process .

This shows that, in practice the autoregression on is sufficient to capture the information of the whole past.

This representation is very important in the inference framework. Note that, if one carries inference on the model (1) by assuming that

, it will not be easy to compute or to write it as a function

of . So, the asymptotic normality of the maximum likelihood estimator of (see (7) and (8))

will be very difficult to study.

We focus on the model (3) with the following assumptions. For and for any compact set ,

define

Assumption A:

and there exists a sequence of non-negative real numbers satisfying

or (for ) such that

The Lipschitz-type condition A is the version of model (3) of the assumption AF.

It is classical when studying the existence of solutions of such model (see for instance [12], [1] or [13]).

The assumptions A and A as well as the following assumptions D, Id() and Var()

are needed to define and to study the asymptotic properties of the maximum likelihood estimator of the model (3).

Assumption D: such that

for all

Assumption Id(): For all ,

Assumption Var(): For all and ,

the components of the vector are a.s. linearly independent.

2.2 Examples

2.2.1 Linear Poisson autoregression

We consider an integer-valued time series satisfying for any

| (5) |

where , the function are positive and satisfying .

Assumptions A holds automatically. If the function are twice continuous differentiable such that

and then A and A

hold. If then D holds.

Moreover, if there exists a finite subset such that the function is injective, then assumption

Id holds i.e. model (5) is identifiable.

Note that the popular Poisson INGARCH model (see [14] or [32]) is a special case of model (5). Finally, the model (5)

can be generalized by considering

where is a Lipschitz function. The threshold model can be obtained with for some , where .

2.2.2 Power Poisson autoregression

We consider a power Poisson INGARCH() process defined by

| (6) |

where , and the function and are positive.

If

, then the Lipschitz-type

condition (AF) is satisfied. In this case, we can find a sequence of non-negative function such that

.

If then D holds.

Moreover, if there exists a finite subset such that the function is injective, then assumption

Id holds i.e. model (6) is identifiable.

3 Likelihood inference

Assume that the trajectory is observed. The conditional (log)-likelihood (up to a constant) of model computed on , is given by

where . In the sequel, we use the notation Since only are observed, we will use an approximation version of the (log)-likelihood defined by

| (7) |

where and . The maximum likelihood estimator (MLE) of computed on is defined by

| (8) |

For any such as , denote

Theorem 3.1

Let and be two integer valued sequences such that , and as . Assume and , and hold with

| (9) |

It holds that

The following theorem shows the asymptotic normality of the MLE of model (3).

Theorem 3.2

Let and be two integer valued sequences such that , and as . Assume and , , Var() and hold with

| (10) |

It holds that

where

According to the Lemma 7.1 and the proof of Theorem 3.2, the matrix

are consistent estimators of the covariance matrix .

Remark 3.1

-

1.

In Theorems 3.1 and 3.2, the typical sequences and , can be chosen. This choice is the case where the estimator is computed with all the observations. But in the change-point study, the estimator needs to be calculated over a part of the observations. Results are written this way to cover the change point situation.

- 2.

4 Testing for Parameter Changes

We consider the observations generated as in model and assume that the parameter may change over time. More precisely, we assume that such that for , where the process is a stationary solution of depending on . The case where the parameter does not change corresponds to . For this problem, we consider the following hypothesis:

-

H0:

The observations are a trajectory of a process solution of , depending on .

-

H1:

There exists with such that the observations are a trajectory of the process solution of , depending on .

Let us note that, contrary to Franke et al. (2012), the independence between the observations before and after the change-point is not assumed. Moreover, we can consider more complex parameter in the model, not only the constant term of the conditional mean as in [20]. In the case of linear Poisson autoregression, the assumption (A9) of their model leads to the change in the unconditional mean. Therefore, our change-point problem is more general.

Remark 4.1

Let be the conditional mean on the segment . By using the representation (4), we can write

We can also write

So, for any and , we have

| (11) |

where the second equality follows by seen as a number of events that occur in the time interval

.

Let be the nonstationary approximation of the process

on the segment ; i.e.

By using assumption A and relation (11), one can show that the approximated process converges (in for any ) to the stationary regime (see for instance Bardet et al. [2] where similar apprimation has been done in the case of causal time series). So, the results of the Section 4.2 may be extended (modulo the validity of the approximation) by relaxing the stationarity assumption after change.

Recall that under H0, the likelihood function of the model computed on is given by

where and the maximum likelihood estimator is given by . It holds from Theorem 3.2 that, under H0, the asymptotic covariance matrix of is where

is a consistant estimator of

under H0 (see the proof of Theorem 3.2). The consistency of under H1 is not ensured. does not take into account the change-point alternative. So, the consistency under H1 of any test based on will not be easy to prove.

Let and be two integer valued sequences satisfying as . Our test statistic is based on the following matrix

Theorem 3.1 and Lemma 7.1 show that is consistent under H0. Under H1, we will use

the classical assumption that the breakpoint gown at rate . This will allow us to show that the first component

of converges to the covariance matrix of the stationary model of the first regime. It will

be a key to prove the consistency under H1.

Another way to deal is to consider the matrix

Asymptotically, both the matrices and have the same behavior under H0. In the case of non stationarity after change, the procedure using can provide more distortion; because due to the dependance the second component of will converge very slowly than the first component of .

Let us define now the tests statistics:

-

•

where

where is a weight function define on , see bellow;

-

•

where

-

•

where

The first procedure is based on the statistique and the other one is based on the statistic defined by

The weight function is used to increase the power of the test based on the statistic . In the sequel, we will assume that

is non-decreasing in a neighborhood of zero, non-increasing in a neighborhood of one and satisfying

for all .

The behavior of the weighted function can be controlled at the neighborhood of zero and one by the integral

see Csörgo et al. [6] or Csörgo and Horváth [7].

The natural weight choice is with .

Furthermore, in practice the sequences and are chosen to ensure the convergence of the numerical algorithm used to compute

and . For Poisson INGARCH model, (with )

can be chosen (see also Remark 1 of [26]).

4.1 Asymptotic behavior under the null hypothesis

The asymptotic distributions of these statistics under H0 are given in the next theorem.

Theorem 4.1

Assume , , Var() and hold with

Under H0 with ,

-

1.

if such that , then

-

2.

for ,

where is a -dimensional Brownian bridge.

The distribution of is explicitly known. In the general case, the quantile of the limit distribution of the first procedure (based on ) can be computed through Monte-Carlo simulations. In the sequel, we will take . The Theorem 4.2 below implies that the statistics and are too large under the alternative. For any , denote the -quantile of the distribution of . Then at a nominal level , take as the critical region of the test procedure based on . This test has correct size asymptotically. On the other hand, it holds that

So we can use as the critical value of the test based on i.e. as the critical region. This leads to a asymptotically conservative procedure. To get correct asymptotic size in the procedure based on , we have to study the asymptotic distribution of . This is a very difficult problem due to the dependence structure of the model and the general structure of the parameter. In the problem of discriminating between long-range dependence and changes in mean, Berkes et al. [3] have studied the limit distribution of such statistic (i.e. the maximum of the maximum between the statistic based on the estimator computed with the observations until the time and the one computed with the observations after ). We have kept this problem as a subject of our future research.

4.2 Asymptotic under the alternative

Under H1, we assume

Assumption B : there exists with such that for

, (where is the integer part of ).

The asymptotic behaviors of these test statistics are given by the following theorem.

Theorem 4.2

Assume B, , , Var() and hold with

-

1.

Under H1 with , if and then

-

2.

Under H1, if and then

It follows that the procedure based on is consistent under the alternative of one change while the statistic diverges to infinity even if there is multiple under the alternative. So, combined with an iterated cumulative sums of squares type algorithm (see [23]) the latter procedure can be used to estimate the number and the break points in the multiple change-points problem.

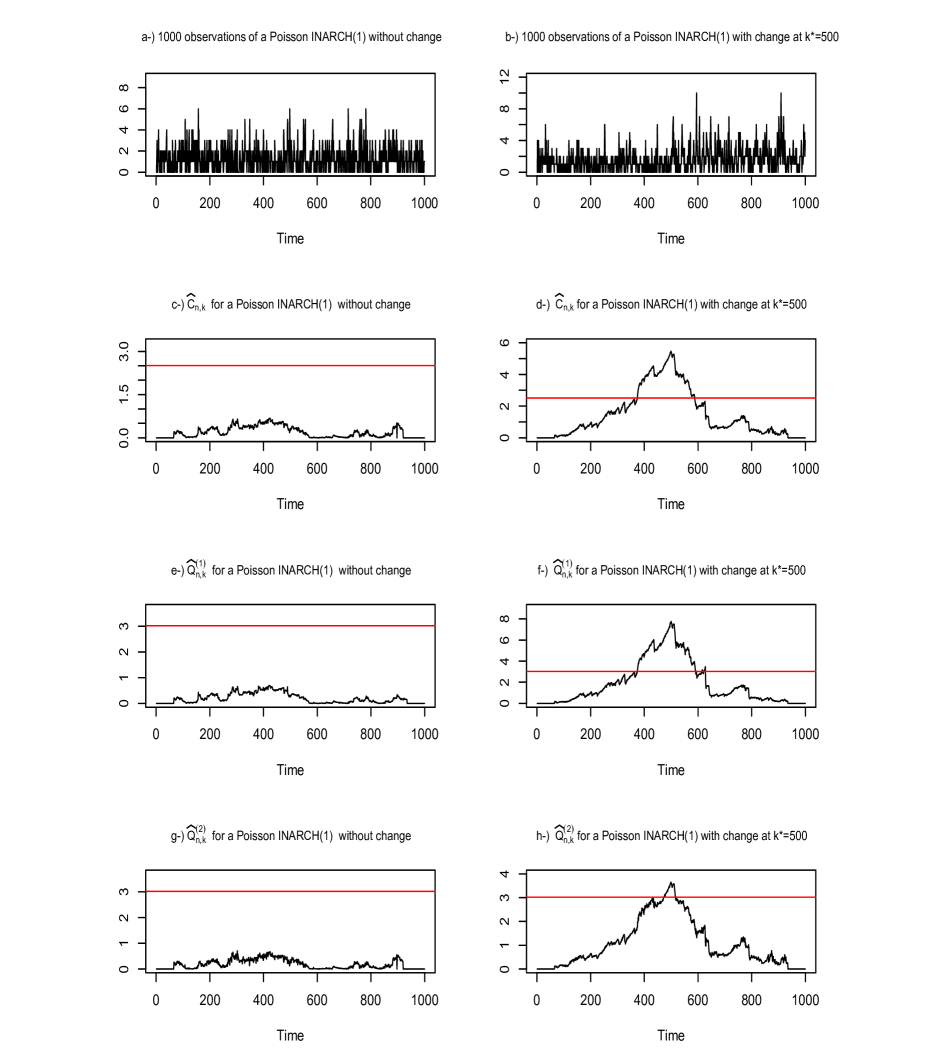

The Figure 1 is an illustration of these tests for an linear Poisson autoregression model of order

| (12) |

One can see that, under H0 the statistics , and are below the horizontal line (see c-), e-), g-) ) which represents the limit of the critical region. These statistics are greater than the critical value in the neighborhood of the breakpoint under H1 (see d-), f-), h-)). In several situations, only one of the statistics and is greater than the critical value under the alternative; so the use of is needed to get more powerful procedure.

5 Some simulations results

We provide some simulations results to show the empirical performance of these tests procedures. We consider a power Poisson INGARCH(1,1) :

| (13) |

For a sample size , the statistics and are computed with . The empirical levels and powers reported in the followings table are obtained after 200 replications at the nominal level .

-

1.

Poisson INGARCH(1,1) with one change-point alternative.

We assume in (13) that and denote by the parameter of the model. Table 1 indicates the empirical levels computed when the parameter is and the empirical powers computed when changes to at .Procedure Empirical levels : statistic 0.020 0.040 statistic 0.035 0.045 statistic 0.065 0.060 statistic 0.080 0.055 Empirical powers : ; statistic 0.415 0.840 statistic 0.595 0.910 ; statistic 0.695 0.960 statistic 0.865 0.995 Table 1: Empirical levels and powers at the nominal level of test for parameter change in Poisson INGARCH(1,1) model with one change-point alternative. -

2.

Poisson INARCH(1) with two change-points alternative.

We assume in (13) that , and denote by the parameter of the model. Table 2 indicates the empirical levels computed when the parameter is and the empirical powers computed when changes to at which changes to at .Procedure Empirical levels : statistic 0.040 0.055 statistic 0.065 0.035 statistic 0.080 0.050 statistic 0.090 0.050 Empirical powers : ; ; statistic 0.715 0.955 statistic 0.780 0.985 ; ; statistic 0.405 0.800 statistic 0.540 0.865 Table 2: Empirical levels and powers at the nominal level of test for parameter change in Poisson INARCH(1) model with two change-points alternative. -

3.

Power Poisson INGARCH(1) with one change-point alternative.

We assume in (13) that , and denote by the parameter of the model. Table 3 indicates the empirical levels computed when the parameter is and the empirical powers computed when changes to at .Procedure Empirical levels : statistic 0.020 0.045 statistic 0.065 0.055 Empirical powers : ; statistic 0.415 0.870 statistic 0.510 0.905 ; statistic 0.500 0.930 statistic 0.590 0.945 Table 3: Empirical levels and powers at the nominal level of test for parameter change in power Poisson INGARCH(1) model with one break alternative.

It appears in Table 1, 2, 3 that these two procedures produces a size distortion when ; but the empirical levels are close to the nominal one when . One can also see that the empirical powers of these procedures increase with . Although the procedure based on is little more powerful, the test based on provides satisfactory empirical powers even in the case of two change-points alternative. This will be the starting point to investigate in our future works, the consistency of this procedure under multiple change-points alternative.

6 Real data Application

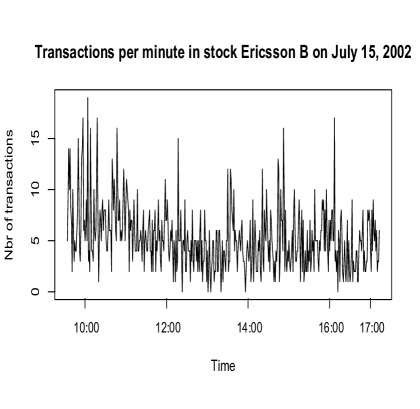

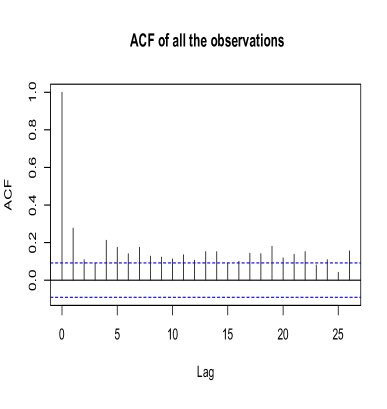

We consider the number of transactions per minute for the stock Ericsson B during July 15, 2002. There are observations which represent trading from 09:35 to 17:14. Figure 2 plot the data and its autocorrelation function.

Several works (see for instance Fokianos et al. [18], Davis and Liu [9]) on the series of July 2, 2002

led to use an INGARCH(1,1) model for this series. This model provides close to unity. It can be seen in the slow decay

of the autocorrelation function (see Figure 2). The authors saw a similarity with the high-persistence in IGARCH model.

The series in the period 2-22 July 2002 have been studied by Brännäs and Quoreshi [5]. They have pointed out the presence of long memory

in these data and applied INARMA model to both level and first difference forms.

To test the adequacy of the linearity of the transaction during July 15, 2002, we have applied the goodness-of-fit test for Poisson count processes

proposed by Fokianos and Neumann [17].

Let be the maximum likelihood estimator computed on the observations.

Denote where

.

The estimated Pearson residuals is defined by . The goodness-of-fit test is based on the

statistic

where and where is a univariate kernel. See [17] for more detail on this test

procedure.

We have applied this test with uniform and Epanechnikov kernel and the p-values and have been obtained respectively. So, the linear assumption of

the model is rejected. Recall that, Fokianos and Neumann [17] have already pointed out some doubt about the linearity assumption when they

analyzed the series of 2 July 2002.

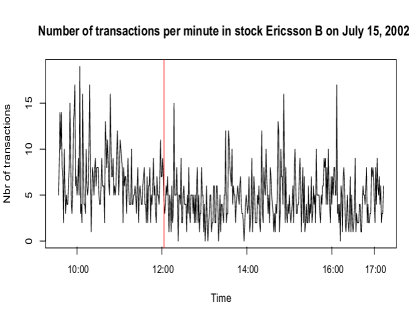

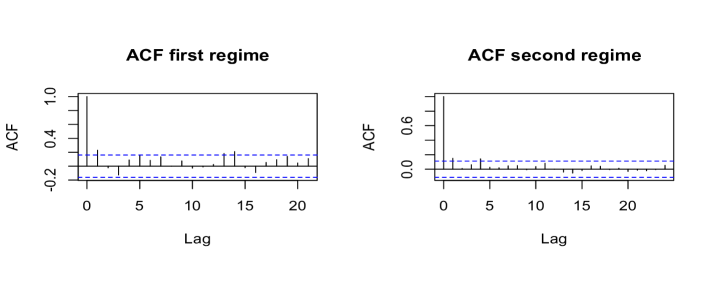

The previous test for change detection have been applied to the series of July 15, 2002. A change has been detected around the midday at .

Figure 3 shows the breakpoint and the autocorrelation function of each regime.

The previous goodness-of-fit test shows the adequacy of the linear Poisson autoregression of the first regime and raises some doubt about the linearity on the second regime. This shows that, the model structure of the transactions in the morning may be different to the structure of the transactions in the afternoon. Moreover, Figure 3 shows that the autocorrelation function of each regime decreases fast; this rules out the idea of the long memory in the series.

7 Proofs of the main results

Proof of the Proposition 2.1

We will use the same techniques as in [12].

Let two fixed non-negative integers. Definite the sequence by

| (14) |

The existence of moment of any order of the process (see [13]) and assumption (AF) imply the existence of moment of any order of . Let us show that is a Cauchy sequence in . By using (AF), we have

By definition and the strictly stationarity of , we can easily see that for , the couples and have the same distribution. Hence, if comes that

For any fixed , denote for all . It holds that

By applying the Lemma 5.4 of [12], we obtain

Hence, as . Thus, for any , the sequence is a Cauchy sequence in .

Therefore, it converges to some limit denoted . Moreover, since the sequence is measurable w.r.t to

, it is the case of the limit . So, there exists a measurable function such that

By going along similar lines, it holds that for any , the sequence converges in to some

and since , is stationary and ergodic, the process

is too stationary and ergodic.

Let and fixed. For large enough,

(see (14)). By using the continuity (which comes from Lipschitz-type conditions)

of for any fixed and by carrying to infinity, it holds that

| (15) |

Denote , , and . By going the same lines as in [12], we obtain . Therefore, as . This show that for any fixed , is a Cauchy sequence in . Thus it converges to some random . Moreover, is measurable w.r.t (because it is the case of ). Thus, there exists a measurable function such that for any . This implies that is strictly stationary and ergodic. Finally, by using equation (15) and continuity of , it comes that

| (16) |

Hence, the process is strictly stationary ergodic and satisfying (1). By the uniqueness of the solution, it holds that a.s. Thus for any .

Proof of the Theorem 3.1

Without loss generality, for simplifying notation, we will make the proof with . It will follow two steps. We will first show that where ; secondly, we will show that the function has a unique maximum in .

-

(i)

Let , recall that . We have

Hence,

We will show that, for any , . Since A holds, we have

Thus, by using the stationarity of the process , it follows that

Therefore, we have

By the uniform strong law of large number applied on , it holds that

(17) Now let us show that

We have

We will apply the Corollary of Kounias and Weng (). So, it suffices to show that

For and , we have .

-

(ii)

We will now show that the function has a unique maximum at . We will proceed as in [9]. Let , with . We have

By applying the mean value theorem at the function defined on , there exists between and such that . Hence, it comes that

Since , it follows from assumption that a.s. Moreover

-

•

if , then and hence ;

-

•

if , then and hence .

We deduce that a.s.. Hence . Thus, the function has a unique maximum at .

-

•

(i), (ii) and standard arguments lead to the consistency of .

The following lemma is needed to prove the Theorem 3.2.

Lemma 7.1

Let and two integer valued sequences such that is increasing, and as . Let , for any segment , it holds under assumptions of Theorem 3.2 that

-

(i)

;

-

(ii)

;

-

(iii)

.

Proof.

-

(i)

Let . We have

and

Hence

(19) Using the relation , we have

Hence, (19) implies

Let . Using the Minkowski and Hölder inequalities, it holds that

But we have and . Hence

Thus,

We also have . Hence

The same argument gives

Hence,

Therefore, we have (with )

This holds for any coordinate . This (i) has been proved.

-

(ii)

For , we have

(20) We will show that . We have

But, we have , and .

Similarly, we have . Using the same argument, we obtain

Hence, . Thus, for the stationary ergodicity of the sequence and the uniform strong law of large numbers, it holds that

This completes the proof of (ii).

-

(iii)

Goes the same lines as in (i) and (ii).

Proof of Theorem 3.2

Here again, without loss generality we will make the proof with . Recall that . Let ; for any and , by applying the Taylor expansion to the function , there exists between and such that

Denote

It comes that

| (21) |

By applying (21) with we obtain

| (22) |

(22) holds for any , thus

| (23) |

We can rewrite (23) as

For large enough, , because is a local maximum of . Moreover, according to Lemma 7.1 (i), it holds that

So, for large enough, we have

| (24) |

To complete the proof of Theorem 3.2, we have to show that

-

(a)

is a stationary ergodic martingable difference sequence and ;

-

(b)

and ;

-

(c)

is invertible.

-

(a)

Recall that and . Since the functions and are -measurable, we have

Moreover, since and have moment of any order, we have

- (b)

-

(c)

If is a non-zero vector of , according to assumption Var, it holds that a.s. Hence

Thus is positive definite.

From (a), apply the central limit theorem for stationary ergodic martingable difference sequence, it follows that

| (26) |

Recall that for , . For , we have

But, we have,

It comes that,

Hence

Thus, (26) becomes

| (27) |

(b) and (c) implies that the matrix converges a.s. to and is invertible for large enough. Hence, from (24) and (27), we have

Before proving the Theorem 4.1, let us prove first some preliminary lemma. Under H0, recall

Define the statistics

-

•

where

-

•

where

-

•

where

Lemma 7.2

Under assumptions of Theorem 4.1, as ,

-

(i)

;

-

(ii)

for .

Proof. (i) For any , we have as

Thus, as , it holds that

The last equality above holds because ; it is a consequence of the properties of the function

when is finite for some .

(ii) Goes the same lines as in (i).

Proof of Theorem 4.1

-

1.

According to Lemma 7.2, it suffices to show that

Let . By applying (22) with , we have

and

As , we have

Thus, we have

i. e.

Moreover we have (as )

Hence

Thus we have

By going similarly lines, we obtain

By subtracting the two above equalities, it follows that

i. e.

Thus

(28) For , we have

We have shown (see the proof of Theorem 3.2) that is a stationary ergodic square integrable difference process with covariance matrix . By the Central limit theorem for the martingale difference sequence (see Billingstey, 1968), it holds that

where is a Gaussian process with covariance matrix . Thus it follows that

in , where is a -dimensional standard motion, and is a -dimensional Brownian bridge.

- 2.

Proof of Theorem 4.2

-

1.

Assume the alternative with one change at with . The observation satisfy

Where and satisfy the main model i. e.

Recall that . It suffices to show that .

We have

Recall that the likelihood function computed on any subset is defined by

So, for any , . Then is the likelihood function of the stationary process computed on . According to Theorem 3.1, it holds that . Moreover, recall that

Remarks that the difference between and lies on the dependence with the past. can contain , but not . is the approximated likelihood of the stationary model after change. By Theorem 3.1, it holds that

Let us show that

We have, as

using again Kounias (), it suffices to show that

For , we have

We can show, as in the proof of Theorem 3.1, that . Hence

But, for , we have

Thus, by using Minkowski inequality, it holds that

Thus, it comes that

Set , we have

So, we have

Hence,

According to the proof of Theorem 3.1,

where

Moreover, the function has a unique maximum at . This is enough to conclude that . To complete the proof of this part of Theorem 4.2, remarks that the two matrices in the definition of are positive semi-definite (by definition) and the first one converges a.s. to which is positive definite. Thus, for large enough, we have

This holds because , and

which is positive definite.

This completes the first part of the proof of Theorem 4.2.

-

2.

It goes along the same line as in the proof of Theorem 2 of [26], by using the approximation of likelihood as above.

Acknowledgements

The authors thank Konstantinos Fokianos for his support, especially for his help in the real data application study.

References

- [1] Bardet, J.-M. and Wintenberger, O. Asymptotic normality of the quasi-maximum likelihood estimator for multidimensional causal processes. Ann. Statist. 37, (2009), 2730-2759.

- [2] Bardet, J.-M. , Kengne, W. and Wintenberger, O. Detecting multiple change-points in general causal time series using penalized quasi-likelihood. Electronic Journal of Statistics 6, (2012), 435-477.

- [3] Berkes, I., Horváth, L., Kokoszka, P.S. and Shao, Q.-M. On discriminating between long-range dependence and changes in mean. Ann. Statist. 34, (2006), 1140-1165.

- [4] Billingsley, P. Convergence of Probability Measures. John Wiley & Sons Inc., New York, (1968).

- [5] Brännäs, K. and Shahiduzzaman Quoreshi, A.M.M. Integer-valued moving average modelling of the number of transactions in stocks. Applied Financial Economics, 20, (2010), 1429–1440.

- [6] Csörgo, M. , Csörgo, S. , Horváth, L. and Mason, D.M. Weighted empirical and quantile processes. The Annals of Probability 14, (1986), 31-85.

- [7] Csörgo, M. and Horváth, L. Weighted Approximations in Probability and Statistics. Wiley Chichester , (1993).

- [8] Davis, R.A., Dunsmuir, W., and Streett, S. Maximum Likelihood Estimation for an Observation Driven Model for Poisson Counts. Methodol. Comput. Appl. Probab. 7, (2005) 149-159.

- [9] Davis, R.A. and Liu, H. Theory and Inference for a Class of Observation-Driven Models with Application to Time Series of Counts. Preprint, arXiv:1204.3915.

- [10] Davis, R.A. and Wu, R. A negative binomial model for time series of counts. Biometrika 96, (2009) 735-749.

- [11] Douc, R., Doukhan, P. and Moulines, E. Ergodicity of observation-driven time series models and consistency of the maximum likelihood estimator. Preprint, arXiv:1210.4739.

- [12] Doukhan, P. and Wintenberger, O. Weakly dependent chains with infinite memory. Stochastic Process. Appl. 118, (2008) 1997-2013.

- [13] Doukhan, P., Fokianos, K., and Tjøstheim, D. On Weak Dependence Conditions for Poisson autoregressions. Statist. and Probab. Letters 82, (2012), 942-948.

- [14] Ferland, R., Latour, A. and Oraichi, D. Integer-valued GARCH process. J. Time Ser. Anal. 27, (2006) 923-942.

- [15] Fokianos, K. and Fried, R. Interventions in INGARCH processes. J. Time Ser. Anal. 31, (2010), 210-225.

- [16] Fokianos, K. and Fried, R. Interventions in log-linear Poisson autoregression. Statistical Modelling 12, (2012), 1-24.

- [17] Fokianos, K. and Neumann, M. A goodness-of-fit test for Poisson count processes. Electronic Journal of Statistics 7, (2013), 793-819.

- [18] Fokianos, K., Rahbek, A. and Tjøstheim, D. Poisson autoregression. Journal of the American Statistical Association 104, (2009), 1430-1439.

- [19] Fokianos, K., and Tjøstheim, D. Nonlinear Poisson autoregression. Ann. Inst. Stat. Math. 64, (2012) 1205-1225.

- [20] Franke, J., Kirch, C. and Tadjuidje Kamgaing, J. Changepoints in times series of counts. J. Time Ser. Anal. 33, (2012) 757-770.

- [21] Hairer, M. and Mattingly, J. Ergodicity of the 2d navier-stokes equations with degenerate stochastic forcings. Ann. Math. 164, (2006), 993–1032.

- [22] Held, L., Höhle, M. and Hofmann, M A statistical framework for the analysis of multivariate infectious disease surveillance counts. Statistical Modelling 5, (2005) 187-199.

- [23] Inclán, C. and Tiao, G. C. Use of cumulative sums of squares for retrospective detection of changes of variance. Journal of the American Statistical Association 89, (1994), 913–923.

- [24] Kang, J., and Lee, S. Parameter change test for random coefficient integer-valued autoregressive processes with application to polio data analysis. Journal of Time Series Analysis, 30(2), (2009), 239-258.

- [25] Kedem, B. and Fokianos, K. Regression Models for Time Series Analysis. Hoboken, NJ: Wiley., (2002).

- [26] Kengne W. Testing for parameter constancy in general causal time-series models. J. Time Ser. Anal. 33, (2012), 503-518.

- [27] Kierfer, J. K-sample analogues of the Kolmogorov-Smirnov and Cramér-v.Mises tests. Ann. Math. Statist 30, (1959), 420-447.

- [28] Lambert, D. Zero-inflated Poisson regression, with an application to defects in manufacturing. Technometrics, 34, (1992), 1-14.

- [29] Neumann, M. Absolute regularity and ergodicity of Poisson count processes. Bernoulli 17, (2011), 1268-1284.

- [30] Rabemananjara, R. and Zakoïan, J.M. Threshold ARCH models and asymmetries in volatility. Journal of Applied Econometrics 8, (1993), 31-49.

- [31] Tjøjstheim, D. Some recent theory for autoregressive count time series. TEST 21 (2012), 413-438

- [32] Wei, C.H. Modelling time series of counts with overdispersion. Stat. Methods Appl. 18, (2009), 507-519.