Inverse Density as an Inverse Problem:

the Fredholm Equation Approach

Abstract

In this paper we address the problem of estimating the ratio where is a density function and is another density, or, more generally an arbitrary function. Knowing or approximating this ratio is needed in various problems of inference and integration, in particular, when one needs to average a function with respect to one probability distribution, given a sample from another. It is often referred as importance sampling in statistical inference and is also closely related to the problem of covariate shift in transfer learning as well as to various MCMC methods. It may also be useful for separating the underlying geometry of a space, say a manifold, from the density function defined on it.

Our approach is based on reformulating the problem of estimating as an inverse problem in terms of an integral operator corresponding to a kernel, and thus reducing it to an integral equation, known as the Fredholm problem of the first kind. This formulation, combined with the techniques of regularization and kernel methods, leads to a principled kernel-based framework for constructing algorithms and for analyzing them theoretically.

The resulting family of algorithms (FIRE, for Fredholm Inverse Regularized Estimator) is flexible, simple and easy to implement.

We provide detailed theoretical analysis including concentration bounds and convergence rates for the Gaussian kernel in the case of densities defined on , compact domains in and smooth -dimensional sub-manifolds of the Euclidean space.

We also show experimental results including applications to classification and semi-supervised learning within the covariate shift framework and demonstrate some encouraging experimental comparisons. We also show how the parameters of our algorithms can be chosen in a completely unsupervised manner.

1 Introduction

Density estimation is one of the best-studied and most useful problems in statistical inference. The question is to estimate the probability density function from a sample . There is a rich literature on the subject (e.g., see the review [11]), particularly, dealing with a class of non-parametric kernel estimators going back to the work of Parzen [20].

In this paper we address the related problem of estimating the ratio of two functions, where is given by a sample and is either a known function or another probability density function given by a sample. We note that estimating such ratio is necessary when one attempts to integrate a function with respect to one density, given its values on a sample obtained from another distribution. This is typical when the process generating the data is different from the averaging problem we wish to address. To give a very simple practical example of such a situation, consider a cleaning robot equipped with a dirt sensor. We would like to know how well the robot performs cleaning, however, the probability density of the robot location depends on the program and is clearly not uniform. To obtain the cleaning quality, we need to average the sensor readings with respect to the uniform density over the floor rather than the location distribution, which requires estimating the inverse (here it the constant function ).

An important class of applications for density ratios relates to various Markov Chain Monte Carlo (MCMC) integration techniques used in various applications, in particular, in many tasks of Bayesian inference. It is often hard to sample directly from the desirable probability distribution but it may be possible to construct an approximation which is easier to sample from. The class of techniques related to the importance sampling (see, e.g., [16]) deals with this problem by using a ratio of two densities (which is typically assumed to be known in that literature).

Recently there have been a significant amount of work on estimating the density ratio (also known as te importance function) from sampled data, e.g., [8, 13, 10, 28, 3]. Many of these papers consider this problem in the context of covariate shift assumption [24] or the so-called selection bias [36]. Our Fredholm Inverse Regularized Estimator (FIRE) framework introduces a very general and flexible approach to this problem which leads to more efficient algorithms design, provides very competitive experimental results and makes possible theoretical analysis in terms of the sample complexity and convergence rates.

We will provide a more detailed discussion of these and other related papers and connections to our work in Section 2, where we also discuss how the Kernel Mean Matching algorithm [8, 10] can be viewed within our framework.

The approach taken in our paper is based on reformulating the density ratio estimation as an integral equation, known as the Fredholm equation of the first kind (in the classical one-dimensional case), and solving it using the tools of regularization and Reproducing Kernel Hilbert Spaces. That allows us to develop simple and flexible algorithms for density ratio estimation within the popular kernel learning framework. In addition the integral operator approach separates estimation and regularization problems, thus allowing us to address certain settings where the existing methods are not applicable. The connection to the classical operator theory setting makes it easier to apply the standard tools of spectral analysis to obtain theoretical results.

We will now briefly outline the main idea of this paper. We start with the following simple equality underlying the importance sampling method:

| (1) |

By replacing the function with a kernel , we obtain

| (2) |

Thinking of the function as an unknown quantity and assuming that the right hand side is known this becomes an integral equation (known as the Fredholm equation of the first type). Note that the right-hand side can be estimated given a sample from while the operator on the left can be estimated using a sample from .

To push this idea further, suppose is a “local” kernel, (e.g., the Gaussian, ) such that . Convolution with such a kernel is close to the -function, i.e., .

Thus we get another (approximate) integral equality:

| (3) |

It becomes an integral equation for , assuming that is known or can be approximated.

We address these inverse problems by formulating them within the classical framework111In fact our formulation is quite close to the original formulation of Tikhonov. of Tiknonov-Philips regularization with the penalty term corresponding to the norm of the function in the Reproducing Kernel Hilbert Space with kernel used in many machine learning algorithms.

Importantly, given a sample from , the integral operator applied to a function can be approximated by the corresponding discrete sum , while norm is approximated by an average: . Of course, the same holds for a sample from .

Thus, we see that the Type I formulation is useful when is a density and samples from both and are available, while the Type II is useful, when the values of (which does not have to be a density function at all222This could be important in various sampling procedures, for example, when the normalizing coefficients are hard to estimate.) are known at the data points sampled from .

Since all of these involve only function evaluations at the sample points, by an application of the usual representer theorem for Reproducing Kernel Hilbert Spaces, both Type I and II formulations lead to simple, explicit and easily implementable algorithms, representing the solution of the optimization problem as linear combinations of the kernels over the points of the sample (see Section 3). We call the resulting algorithms FIRE for Fredholm Inverse Regularized Estimator.

Some remarks would be useful at this point.

Remark 1: Other norms and loss functions. Norms and loss functions other that can also be used in our setting as long as they can be approximated from a sample using function evaluations.

-

•

Perhaps, the most interesting is the norm norm available in the Type I setting, when a sample from the probability distribution is available. In fact, given a sample from both and we can use the combined empirical norm . Optimization using those norms leads to some interesting looking kernel algorithms described in Section 3. We note that the solution is still a linear combination of kernel functions on centered on the sample from and can still be written explicitly.

-

•

In the Type I formulation, if the kernels and coincide, it is possible to use the RKHS norm instead of . This formulation (see Section 3) also yields an explicit formula and is related to the Kernel Mean Matching algorithm [10] (see the discussion in Section 2), although with a different optimization procedure. We note that the solution in our framework has a natural out-of-sample extension, which becomes important for proper parameter selection.

-

•

Other norms/loss functions, e.g., , -insensitive loss from the SVM regression, etc., can also be used in our framework as long as they can be approximated from a sample using function evaluations. We note that some of these may have advantages in terms of the sparsity of the resulting solution. On the other hand, a standard advantage of using the square norm is the ease of cross-validation with respect to the parameter .

Remark 2: Other regularization methods. Several regularization methods other than Tikhonov-Philips regularization are available. We will briefly discuss the spectral cut-off regularization and its potential advantages in Section 3. We note that other methods, such as early stopping (e.g., [34, 1]) can be used and may have computational advantages.

Remark 3. We note that an intermediate “Type 1.5” formulation is also available. Specifically, for two ”-kernels” and , we have , thus using two different kernels in the Type I formulation

| (4) |

The ability to use kernels with different bandwidth for and may be potentially important in practice, especially when the samples from and have very different cardinality. The resulting algorithms for this setting are described in in Section 3. Of course, the previous two remarks apply to this setting as well.

Since we are dealing with a classical inverse problem for integral operators, our formulation allows for theoretical analysis using the methods of spectral theory. In Section 4 we prove concentration and error bounds as well as convergence rates for our algorithms when data are sampled from a distribution defined in , a domain in with boundary or a compact -dimensional sub-manifold of a Euclidean space for the case of the Gaussian kernel.

It is interesting to note that unlike the usual density estimation problem the width of the kernel does not need to go to zero for convergence. However, it is necessary if we want a polynomial convergence rate. This is related to the exponential decay of eigenvalues for the Gaussian kernel.

Finally, in Section 6 we discuss the experimental results on several data sets comparing our method FIRE with the available alternatives, Kernel Mean Matching (KMM) [10] and LSIF [13] as well as the base-line thresholded inverse kernel density estimator333Obtained by dividing the standard kernel density estimator for by a thresholded kernel density estimator for Interestingly, despite its simplicity it performs quite well in many settings. (TIKDE) and importance sampling (when available).

We summarize the contributions of the paper as follows:

-

1.

We provide a formulation of estimating the density ratio (importance function) as a classical inverse problem, known as the Fredholm equation, establishing a connections to the methods of classical analysis. The underlying idea is to “linearize” the properties of the density by studying an associated integral operator.

-

2.

To solve the resulting inverse problems we apply regularization with an RKHS norm penalty. This provides a flexible and principled framework, with a variety of different norms and regularization techniques available. It separates the underlying inverse problem from the necessary regularization and leads to a family of very simple and direct algorithms within the kernel learning framework in machine learning. We call the resulting algorithms FIRE for Fredholm Inverse Regularized Estimator.

-

3.

Using the techniques of spectral analysis and concentration, we provide a detailed theoretical analysis for the case of the Gaussian kernel, for Euclidean case as well as distributions supported on a sub-manifold. We prove error bounds and as well as the convergence rates (as far as we know, it is the first convergence rate analysis for density ratio estimation). We also comment on other kernels and potential extensions of our analysis.

-

4.

We evaluate and compare our methods on several real-world and artificial different data sets and in several settings and demonstrate strong performance and better computational efficiency compared to the alternatives. We also propose a completely unsupervised technique for cross-validating the parameters of our algorithm and demonstrate its usefulness, thus addressing in our setting one of the most thorny issues in unsupervised/semi-supervised learning.

-

5.

Finally, our framework allows us to address several different settings related to a number of problems in areas from covariate shift classification in transfer learning to importance sampling in MCMC to geometry estimation and numerical integration. Some of these connections are explored in this paper and some we hope to address in the future work.

2 Related work

The problem of density estimation has a long history in classical statistical literature and a rich variety of methods are available [11]. However, as far as we know the problem of estimating the inverse density or density ratio from a sample has not been studied extensively until quite recently. Some of the related older work includes density estimation for inverse problems [7] and the literature on deconvolution, e.g., [4].

In the last few years the problem of density ratio estimation has received significant attention due in part to the increased interest in transfer learning [19] and, in particular to the form of transfer learning known as covariate shift [24]. To give a brief summary, given the feature space and the label space , two probability distributions and on satisfy the covariate assumption if for all , . It is easy to see that training a classifier to minimize the error for , given a sample from requires estimating the ratio of the marginal distributions . Some of the work on covariate shift, ratio density estimation and other closely related settings includes [36, 3, 8, 13, 28, 10, 29, 12, 18]

The algorithm most closely related to our approach is Kernel Mean Matching (KMM) [10]. KMM is based on the observation that , where is the feature map corresponding to an RKHS . It is rewritten as an optimization problem

| (5) |

The quantity on the right can be estimated given a sample from and a sample from and the minimization becomes a quadratic optimization problem over the values of at the points sampled from . Writing down the feature map explicitly, i.e., recalling that , we see that the equality is equivalent to the integral equation Eq. 2 considered as an identity in the Hilbert space . Thus the problem of KMM can be viewed within our setting Type I (see the Remark 2 in the introduction), with a RKHS norm but a different optimization algorithm.

However, while the KMM optimization problem in Eq. 5 uses the RKHS norm, the weight function itself is not in the RKHS. Thus, unlike most other algorithms in the RKHS framework (in particular, FIRE), the empirical optimization problem resulting from Eq. 5 does not have a natural out-of-sample extension444In particular, this becomes an issue for model selection, see Section 6..

Also, since there is no regularizing term, the problem is less stable (see Section 6 for some experimental comparisons) and the theoretical analysis is harder (however, see [8] and the recent paper [35] for some nice theoretical analysis of KMM in certain settings).

Another related recent algorithm is Least Squares Importance Sampling (LSIF) [13], which attempts to estimate the density ratio by choosing a parametric linear family of functions and choosing a function from this family to minimize the distance to the density ratio. A similar setting with the Kullback-Leibler distance (KLIEP) was proposed in [29]. This has an advantage of a natural out-of-sample extension property. We note that our method for unsupervised parameter selection in Section 6 is related to their ideas. However, in our case the set of test functions does not need to form a good basis since no approximation is required.

We note that our methods are closely related to a large body of work on kernel methods in machine learning and statistical estimation (e.g., [26, 22, 21]). Many of these algorithms can be interpreted as inverse problems, e.g., [5, 25] in the Tikhonov regularization or other regularization frameworks. In particular, we note interesting methods for density estimation proposed in [31] and estimating the support of density through spectral regularization in [6], as well as robust density estimation using RKHS formulations [14] and conditional density [9].

3 Settings and Algorithms

3.1 Some preliminaries

We start by introducing some objects and function spaces important for our development. As usual, the space of square-integrable functions with respect to a measure , is defined as follows:

This is a Hilbert space with the inner product defined in the usual way by .

Given a function of two variables (a kernel), we define the operator :

We will use the notation to explicitly refer to the parameter of the kernel function , when it is a -family.

If the function is symmetric and positive definite, then there is a corresponding Reproducing Kernel Hilbert space (RKHS) . We recall the key property of the kernel : for any , . The direct consequence of this is the Representer Theorem, which allows us to write solutions to various optimization problems over in terms of linear combinations of kernels supported on sample points (see [26] for an in-depth discussion or the RKHS theory and the issues related to learning).

It is important to note that in some of our algorithms the RKHS kernel will be different from the kernel of the integral operator .

Given a sample from , one can approximate the norm of a function555 needs to be in a function class where point evaluations are defined. by . Similarly, the integral operator . These approximate equalities can be made precise by using appropriate concentration inequalities.

3.2 The FIRE Algorithms

As discussed in the introduction, the starting point for our development is the integral equality

| (6) |

Notice that in Type I, the kernel is not necessary to be in -family. For example, it could be linear kernel. Thus, we omit the in the kernel for the Type I case.

Moreover, if the kernel is a Gaussian, which we will analyze in detail, or another -family and for sufficiently smooth and hence

| (7) |

In fact, for the Gaussian kernel, the term is of the order . Since it is important that the kernel is in the -family with bandwidth , so we keep in the notation in this case.

Assuming that either or are known (for simplicity we will refer to these settings as Type I and Type II, respectively) these Eqs. 6,7 become integral equations for , known as the Fredholm equations of the first kind.

To address the problem of estimating we need to obtain an approximation to the solution which (a) can be obtained computationally from sampled data, (b) is stable with respect to sampling and other perturbation of the input function666Especially in Eq. 7, where the identity has an error term depending on . and, preferably, (c) can be analyzed using the standard machinery of functional analysis.

To provide a framework for solving these inverse problems we apply the classical techniques of regularization combined with the RKHS norm popular in machine learning. In particular a simple formulation of Eq.6 in terms of Tikhonov regularization with the norm is as follows:

| (8) |

Here is an appropriate Reproducing Kernel Hilbert Space. Similarly Eq. 7 can be written as

| (9) |

We will now discuss the empirical versions of these equations and the resulting algorithms in different settings and for different norms.

3.3 Algorithms for the Type I setting.

Given an iid sample from , and an iid sample from , (we will denote the combined sample by ) we can approximate the integral operators and by

| (10) |

Thus the empirical version of Eq. 8 becomes

| (11) |

We observe that the first term of the optimization problem involves only evaluations of the function at the points of the sample .

Thus, using the Representer Theorem and the standard matrix algebra manipulation we obtain the following solution:

| (12) |

where the kernel matrices are defined as follows: , for and is defined as for and .

To compute the whole regularization path for all ’s, or computing the inverse for every , we can use the following formula for :

where is a diagonalization777Strictly speaking, an arbitrary matrix can only be reduced to the Jordan canonical form, but an arbitrarily small perturbation of any matrix can be diagonalized over the complex numbers. of (i.e., is diagonal).

When and are obtained using the same kernel function , i.e. , the expression simplifies:

In that case (or, more, generally, if they commute) the diagonalization is obtained by computing the eigen-decomposition of , where is an orthogonal matrix. Then the solution could be computed using the following formula:

Similarly to many other algorithms based on the square loss function, this formulation allows us to efficiently compute the solution for many values of the parameter simultaneously, which is very useful for cross-validation.

3.3.1 Algorithms for norm.

Depending on the setting, we may want to minimize the error of the estimate over the probability distribution , or over some linear combination of these. A significant potential benefit of using a linear combination is that both samples can be used at the same time in the loss function. First we state the continuous version of the problem:

| (13) |

Given a sample from , and a sample from , we obtain an empirical version of the Eq. 13:

Using the Representer Theorem we can derive:

where

Here , for . and are defined as and for ,.

We see that despite the loss function combining both samples, the solution is still a summation of kernels over the points in the sample from .

3.3.2 Algorithms for the RKHS norm.

In addition to using the RKHS norm for regularization norm, we can also use it as a loss function:

| (14) |

Here the Hilbert space must correspond to the kernel and can potentially be different from the space used for regularization. Note that this formulation is only applicable in the Type I setting since it requires the function to belong to the RKHS .

Given two samples , it is straightforward to write down the empirical version of this problem, leading to the following formula:

| (15) |

The result is somewhat similar to our Type I formulation with the norm. We note the connection between this formulation of using the RKHS norm as a loss function and the KMM algorithm [10]. The Eq. 15 can be viewed as a regularized version of KMM (with a different optimization procedure), when the kernels and are the same.

Interestingly a somewhat similar formula arises in [13] as unconstrained LSIF, with a different functional basis (kernels centered at the points of the sample ) and in a setting not directly related to RKHS inference.

3.4 Algorithms for the Type II and 1.5 settings.

In the Type II setting we assume that we have a sample drawn from and that we know the function values at the points of the sample.

Replacing the norm and the integral operator with their empirical versions, we obtain the following optimization problem:

| (16) |

Recall that is the empirical version of defined by

As before, using the Representer Theorem we obtain an analytical formula for the solution:

| (17) |

where the kernel matrix is defined by , and .

3.4.1 Type 1.5: The setting and the algorithm.

This case (see Eq. 4) is intermediate between Type I and Type II. The setting is the same as in Type I, in that we are given two samples from and from . But similarly to Type II, we use the fact that when and are different -function-like kernels (e.g., two Gaussians of different bandwidth). The algorithm is similar to that for Type I with the difference that the kernel matrix is computed using the kernel : .

3.5 Spectral Cutoff Regularization

In this section we briefly discuss an alternative form of regularization, based on thresholding the spectrum of the kernel matrix. It also leads to simple algorithms comparable to those for Tikhonov regularization and may have certain computational advantages.

Since is a compact self-adjoint operator on , its eigenfunctions form a complete orthogonal basis for . An alternative method of regularization is the so-called spectral cutoff where the problem is restricted to the subspace spanned by the top few eigenfunctions of Thus the regularization problems become

where and is the finite dimensional subspace of spanned by the eigenvectors of and corresponding to the largest eigenvalues.

Without going into detail, it can be seen that the corresponding empirical optimization problems are

| (18) |

| (19) |

where the span of eigenvectors of the kernel matrix is taken instead of the eigenfunctions of or .

For this algorithm, we assume and use the same kernel. Then the solution to the empirical regularization problems given in Eqs. 18,19 are respectively

| (20) |

| (21) |

where is the eigendecomposition of with orthogonal matrix and diagonal matrix , and and is the submatrices of and corresponding to the largest eigenvalues of the kernel matrix and the remaining objects are defined in the previous subsection.

We note that spectral regularization can be faster computationally as it requires to compute only the top few eigenvectors of the kernel matrix. There are several efficient algorithms for computing eigen-decomposition when only the first eigenvalues are needed. Thus spectral regularization can be more computationally efficient than the Tikhonov regularization which potentially requires a full eigen-decomposition or matrix multiplication.

3.6 Comparison of type I and type II settings.

While at first glance the type II, setting may appear to be more restrictive than type I, there are a number of important differences in their applicability.

-

1.

In Type II setting does not have to be a density function (i.e., non-negative and integrate to one).

-

2.

Eq. 11 of the Type I setting cannot be easily solved in the absence of a sample from , since estimating requires either sampling from (if it is a density) or estimating the integral in some other way, which may be difficult in high dimension but perhaps of interest in certain low-dimensional application domains.

-

3.

There are a number of problems (e.g., many problems involving MCMC) where is known explicitly (possibly up to a multiplicative constant), while sampling from is expensive or even impossible computationally [17].

- 4.

-

5.

While a number of different norms are available in the Type I setting, only the norm is available for Type II.

4 Theoretical analysis: bounds and convergence rates for Gaussian Kernels

In this section, we state our main results on bounds and convergence rates for our algorithm based on Tikhonov regularization with a Gaussian kernel. We consider both Type I and Type II settings for the Euclidean and manifold cases and make a remark on the Euclidean domains with boundary.

To simplify the theoretical development the integral operator and the RKHS will correspond to the same Gaussian kernel . Most of the proofs will be given in the next Section 5. We note that two Gaussian kernels with different bandwidth parameters can be analyzed using only minor modifications to our arguments.

4.1 Assumptions

Before proceeding to the main results, we will state the assumptions on the density functions and and the basic setting for our theorems:

-

1.

The set where the density function is defined could be one of the following: (1) the whole ; (2) a compact smooth Riemannian sub-manifold of -dimension in . In both cases, we need for any . The function should satisfy and needs to be bounded from above. We will also make some remarks about a compact domain in with boundary.

-

2.

We also require and , where is the Sobolev space of functions on (e.g., [30]). Certain properties of will be discussed later in the proof.

It will be important for us that is isometric to under the map , that is, for any . Here the integral operator uses the RKHS kernel corresponding to .

4.2 Main Theorems

4.2.1 Type I setting

We will provide theoretical results for our setting Type I, where both the operator and the regularization kernel are Gaussian with the same bandwidth parameter .

Theorem 1.

Let and be two density functions on and be another density over satisfying the assumption in Sec. 4.1. Given points, , i.i.d. sampled from and points, , i.i.d. sampled from , and for small enough , for the solution to the optimization problem in (11), with confidence at least , we have

(1) If the domain is ,

| (22) |

where are constants independent of .

(2) If the domain is a compact manifold without boundary of dimension,

| (23) |

where are constants independent of .

Proof.

See Section 5. ∎

Remark 1: convergence for fixed . For the Euclidean case in Eq. 22, with fixed kernel width , the error will converge to , as given sufficiently many data points. However the required number of points is exponential in . This is related to the fact the eigen-values of the operator decay exponentially fast, when the kernel is Gaussian. On the other hand choosing both and as a function of leads to a much better polynomial rate given below.

Remark 2. A minor modification of the proof provides the following simpler version of Eq. 22:

| (24) |

As a consequence we obtain the following corollary establishing the convergence rates:

Corollary 2.

Assuming , with confidence at least , we have the following:

-

(1)

If = ,

-

(2)

If is a -dimensional sub-manifold of a Euclidean space,

4.2.2 Type II setting

In this section we provide an analysis for the Type II setting and also make a remark about the error analysis for the compact domains in .

Recall that in Type II setting we have a set of points sampled from and assume that the values of on those points are known. Note, that does not have to be a density function.

Theorem 3.

Let be a density function on and be a function satisfying the assumptions in Sec. 4.1. Given points sampled i.i.d. from , and for sufficiently small , for the solution to the optimization problem in (16), with confidence at least , we have

(1) If the domain is ,

| (25) |

where are constants independent of . Moreover, .

(2) If is a -dimensional sub-manifold of a Euclidean space,

| (26) |

where are constants independent of . Moreover, for any .

Remark. It can be shown that if is a compact subset with sufficiently smooth boundary in , we have the same bound with (1) except for for any any .

As before, we obtain the rates as a corollary:

Corollary 4.

With confidence at least , we have:

-

(1)

If ,

-

(2)

If is a -dimensional sub-manifold of a Euclidean space, than for any

Proof.

For the case of , set . For case of sub-manifold case, set . Apply Theorem 3. ∎

5 Proofs of Theorems

In this section, we provide a proof for the our main Theorem 1 for setting I. The proof for the Theorem 3 for the setting type II is along similar lines and can be found in the appendix.

5.1 Basics about RKHS

Since is a self-adjoint operator, its eigenfunctions form a complete orthogonal basis for . Denote the eigenvalues of by . The norm of , for a constant . We know that is isometric to under the map , i.e. for any , and this is the definition we use for the norm of . This also implies that for any . And is defined using the spectrum of ,

5.2 Proof of Theorem 1

Proof.

Recall the definition of and in Eq. 8 and Eq. 11. By the triangle inequality, we have

| (27) |

The approximation error is a measure of the distance between and the optimal approximation given by algorithm (8) given infinite number of data. The sampling error term the difference between and , depending on the data points.

5.2.1 Bound for Approximation Error

First of all, let present two lemmas that are useful for bounding the approximation error.

Lemma 5.

Let . If function and for any , then

| (28) |

for constants .

Proof.

See Appendix A. ∎

Lemma 6.

Let . If function defined on a compact Riemann sub-manifold of -dimension in a Euclidean space, then

| (29) |

for constants .

Proof.

See Appendix B ∎

Now we can present the lemma that gives the bound of the approximation error in the following lemma.

Lemma 7.

Let be two density functions of probability measure over a domain satisfying the assumptions in 4.1. The solution to the optimization problem in (8), , satisfies the following inequality,

(1) when the domain is ,

for constants which are independent of and .

(2) when the domain is a compact Riemannian sub-manifold of dimension in ,

for constants which are independent of and .

Proof.

Recall the equation (8). By functional calculus, we have analytical formula for as follows,

The last equation is because

Thus the approximating error is

| (30) |

The minimum of the above optimization problem can always be bounded by any specific . And we will expend the above formula such that we can take advantages of Lemma 5 and 6. To this end, we define an operator

By functional calculus, it is not hard to see that . If , so is , this is because is an integral operator with Gaussian kernel and Gaussian kernel is in for any . Also, we should have , because .

Now let . We have is also in and . Now we could expend (31),

By inequality , we have

The last inequality is because for constant . Up to now, the proof is valid for both cases in the theorem. And we can apply Lemma 5 and 6 to get the bounds for both cases. By Lemma 5, for the densities over , we have

| (32) |

5.2.2 Bound for Sampling Error

In the next lemma, we will give concentration of the sampling error, .

Lemma 8.

Proof.

Recall that,

and

Using functional calculus, we will get the explicit formula for and as follows,

and

Then the bound for sampling error is to bound the above two objects. Let . We have . For , using the fact that , we have

And

Notice that we have and in the identity we get. For these two objects, it is not hard to verify the following identities,

And

Thus, in these two identities, the only two random variables are and . By results about concentration of and , we have with probability ,

| (35) |

And we know that for a large enough constant which is independent of and ,

and

thus, .

Notice that and , both of this could be of smaller order compared with . For simplicity we hide the term including them in the final bound without changing the dominant order. We could also hide the terms with the product of any two the random variables in Eq. 40, which is of prior order compared to the term with only one random variable. Now let us put everything together,

where . ∎

6 Experiments

In this section we explore the empirical performance of our methods under various settings. We will primarily concentrate on our setting Type II and use the same Gaussian kernel for the integral operator and the regularization term to simplify model selection.

This section is organized as follows. In Subsection 6.1 we describe a completely unsupervised procedure for parameter selection, which will be used throughout the experimental section. In Subsection 6.2 we briefly describe the data sets and the re-sampling procedures we use. In Subsection 6.3 we provide a comparison between our methods using different norms and other methods based on the expected performance under our evaluation criteria. In Subsection 6.4 we provide a number of experiments comparing our method to different methods on several different data sets for classification and regression tasks. Finally in Subsection 6.5 we study performance of different kernels in both Type-I and Type-II setting using two simulated data sets.

6.1 Experimental Setting and Model Selection

The setting: In our experiments, we have a set of a data set and another set of instances . The goal is to estimate under the assumption that is sampled from and is sampled from .

We note that our algorithms typically has two parameters, which need to be selected, the kernel width and the regularization parameter . In general choosing parameters in a unsupervised or semi-supervised setting is a hard problem as it may be difficult to validate the resulting classifier/estimator. However, certain features of our setting allow us to construct an adequate unsupervised proxy for the performance of the algorithm. Now we construct a performance measure for the quality of the estimator.

Performance Measure. We describe a set of performance measures to use for parameter selection.

For a given function , we have the following importance sampling equality (Eq. 1):

If is an approximation of the true ratio , using the samples from and respectively, we will have the following approximation to the above equation:

Therefore, after obtaining an estimate of the ratio, we can validate it by using a set of test functions using the following performance measure:

| (36) |

where is a collection of function chosen as criterion. Using this performance measure allows various cross-validation procedures to be sued for parameter selection.

We note that this way of measuring the error is related to the LSIF [13] and KLIEP [29], algorithms. However, there a similar measure is used to construct an approximation to the ratio using functions as a basis. In our setting, to choose parameters, we can use validations sets (such as linear functions) which are poorly suited as a basis for approximating the density ratio.

Choice of validation function sets for parameter selection. In principle, any set of (sufficiently well-behaved) functions can be used as a validation set. From a practical point of view we would like functions to be simple to compute and readily available for different data sets.

In the our experiments, we will use the following two families of functions for parameter tuning:

-

(1)

Sets of random linear functions where .

-

(2)

Sets of random half-space indicator functions, where .

Remark 1: We have also tried (a) coordinates functions, (b) random combination of kernel functions, and (c) random combination of kernel functions with thresholding. In our experience the coordinate functions are not rich enough for adequate parameter tuning. On the other hand, using the kernel functions significantly increases the complexity of the procedure (due to the necessity of choosing the kernel width and other parameters) without increasing the performance significantly.

Remark 2: Note that for linear functions, the cardinality of the set should not exceed the dimension of the space due to linear dependence.

Remark 3: It appears that linear functions work well for regression tasks, while half-spaces are well-suited for classification.

Procedures for parameter selection.

We optimize the performance using cross-validation by splitting the data set in two parts and used for training and and used for validation, and repeating this process five times to find the optimal values of parameters888We note that this procedure cannot be used with KMM as it has no out-of-sample extension. Therefore in subsection 6.3 we do not compare our method with KMM since there is no obvious way to extend the results to the validation data set..

For the two parameters which need to be tuned, the kernel width and the regularization parameter , we specify a parameter grid as follows. The range for kernel width is , where is the average distance of the 10 nearest neighbors, and regularization parameter is .

6.2 Data sets and Resampling

In our experiments, several data sets are considered: Bank8FM, CPUsmall and Kin8nm for regression; and USPS and 20 news groups for classification.

For each data set, we assume they are i.i.d. sampled from a distribution denoted by . We draw the first or points from the original data set as . To obtain , we apply a resampling scheme on the remaining points of the original data set. Two ways of resampling, using the features of the data and using the label information, are used (along the lines similar to those proposed in [8]).

Specifically, given a set of data points with labels we resample as follows:

-

•

Resampling using feature information (labels are not used). We subsample the data points so that the probability of selecting the instance , is defined by the following (sigmoid) function:

where are the resampling parameters, is the first principal component, and is the standard deviation of the projection to . Note that in this resampling scheme, the probability of taking one point is only conditioned on the feature information . This resampling method will be denoted by PCA.

-

•

Resampling using label information. The probability of selecting the ’th instance, denoted by , is defined by

where and is a subset of the complete label set . We apply this for binary problems obtained by aggregating different classes in the multi-class setting.

6.3 Testing the FIRE algorithm

In first experiment, we test our method for selecting the parameters, which is described in Section 6.1, by focusing on the the error in Eq. 36 for different function classes . We use different families of functions for tuning parameters and validation. This measure is important because in practice the functions we are interested may not be in the collection we chosen for validation. To avoid confusion, we denote the function for cross validation by and the function for measuring error by .

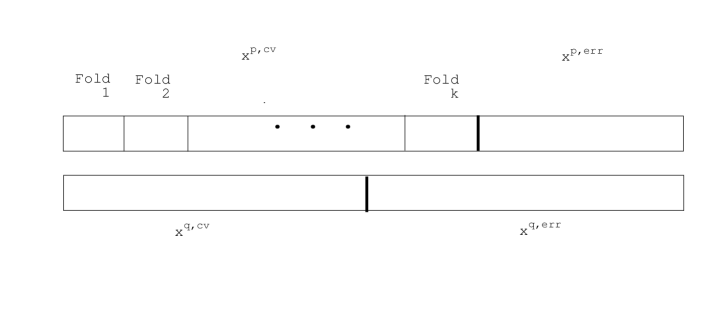

We use the CPUsmall and USPS hand-written digits data sets. For each of them, we generate two data sets and using the resampling method, PCA, describe in Section 6.2. We compare FIRE with several methods including TIKDE, LSIF. Figure 1 gives an illustration of the procedure and usage of data for the experiments. And the results are shown in Table 1 and 2. The numbers in the table are the average errors defined in Eq. 36 on held-out set over 5 trials, using different criterion functions (Columns) and error-measuring functions (Row). is the number of random function we are using for the cross-validation.

For the error-measuring functions, we have several choices as follows:

-

(1)

Linear: Sets of Random linear functions where .

-

(2)

Half-space: Sets of random half-space indicator functions, where .

-

(3)

Kernel: Sets of random linear combination of kernel functions centered at the training data, where and where are points from the data set.

-

(4)

K-indicator: Sets of random kernel indicator functions centered at the training data, where and where are points from the data set.

-

(5)

Coord: Sets of coordinate functions.

| Linear | Half-spaces | ||||

| N=50 | N=200 | N=50 | N=200 | ||

| Linear | TIKDE | 10.9 | 10.9 | 10.9 | 10.9 |

| LSIF | 14.1 | 14.1 | 26.8 | 28.2 | |

| FIRE() | 3.56 | 3.75 | 5.52 | 6.32 | |

| FIRE() | 4.66 | 4.69 | 7.35 | 6.82 | |

| FIRE() | 5.89 | 6.24 | 9.28 | 9.28 | |

| Half-spaces | TIKDE | 0.0259 | 0.0259 | 0.0259 | 0.0259 |

| LSIF | 0.0388 | 0.0388 | 0.037 | 0.039 | |

| FIRE() | 0.00966 | 0.0091 | 0.0103 | 0.0118 | |

| FIRE() | 0.0094 | 0.0102 | 0.0143 | 0.0107 | |

| FIRE() | 0.0124 | 0.0135 | 0.0159 | 0.0159 | |

| Kernel | TIKDE | 4.74 | 4.74 | 4.74 | 4.74 |

| LSIF | 16.1 | 16.1 | 15.6 | 13.8 | |

| FIRE() | 1.19 | 1.05 | 2.78 | 3.57 | |

| FIRE() | 2.06 | 1.99 | 4.2 | 2.59 | |

| FIRE() | 5.16 | 4.27 | 6.11 | 6.11 | |

| K-Indicator | TIKDE | 0.0415 | 0.0415 | 0.0415 | 0.0415 |

| LSIF | 0.0435 | 0.0435 | 0.0531 | 0.044 | |

| FIRE() | 0.00862 | 0.00676 | 0.0115 | 0.0114 | |

| FIRE() | 0.00559 | 0.00575 | 0.0191 | 0.0108 | |

| FIRE() | 0.0117 | 0.00935 | 0.0217 | 0.0217 | |

| Coord. | TIKDE | 0.0541 | 0.0541 | 0.0541 | 0.0541 |

| LSIF | 0.0647 | 0.0647 | 0.139 | 0.162 | |

| FIRE() | 0.0183 | 0.0165 | 0.032 | 0.0334 | |

| FIRE() | 0.0211 | 0.0201 | 0.0423 | 0.0355 | |

| FIRE() | 0.0277 | 0.0233 | 0.0496 | 0.0496 | |

| Linear | Half-spaces | ||||

| N=50 | N=200 | N=50 | N=200 | ||

| Linear | TIKDE | 0.102 | 0.0965 | 0.102 | 0.0984 |

| LSIF | 0.115 | 0.115 | 0.115 | 0.115 | |

| FIRE() | 0.0908 | 0.0858 | 0.0891 | 0.0924 | |

| FIRE() | 0.0832 | 0.0825 | 0.0825 | 0.0718 | |

| FIRE() | 0.0889 | 0.0907 | 0.0932 | 0.0899 | |

| Half-spaces | TIKDE | 0.00469 | 0.00416 | 0.00469 | 0.00462 |

| LSIF | 0.00487 | 0.00487 | 0.00487 | 0.00487 | |

| FIRE() | 0.00393 | 0.00389 | 0.00435 | 0.00436 | |

| FIRE() | 0.00385 | 0.00383 | 0.00383 | 0.00345 | |

| FIRE() | 0.00421 | 0.0044 | 0.00459 | 0.00427 | |

| Kernel | TIKDE | 9.82 | 8.48 | 9.82 | 9.3 |

| LSIF | 9.6 | 9.6 | 9.6 | 9.6 | |

| FIRE() | 6.96 | 6.17 | 8.02 | 8.19 | |

| FIRE() | 6.62 | 6.62 | 6.62 | 6.35 | |

| FIRE() | 7.23 | 7.17 | 7.44 | 7.38 | |

| K-Indicator | TIKDE | 0.00411 | 0.00363 | 0.00411 | 0.00404 |

| LSIF | 0.00478 | 0.00478 | 0.00478 | 0.00478 | |

| FIRE() | 0.0033 | 0.00313 | 0.0036 | 0.00373 | |

| FIRE() | 0.00306 | 0.00306 | 0.00306 | 0.00288 | |

| FIRE() | 0.00358 | 0.00354 | 0.00365 | 0.00366 | |

| Coord. | TIKDE | 0.00784 | 0.0077 | 0.00784 | 0.00758 |

| LSIF | 0.00774 | 0.00774 | 0.00774 | 0.00774 | |

| FIRE() | 0.00696 | 0.00676 | 0.00681 | 0.00734 | |

| FIRE() | 0.00647 | 0.00637 | 0.00637 | 0.00584 | |

| FIRE() | 0.00693 | 0.00692 | 0.00699 | 0.00689 | |

6.4 Supervised Learning: Regression and Classification

In our experiments, we compare our method FIRE with several methods under the setting of supervised learning, i.e. regression and classification. More specifically, we consider the situation part or all of the training set are labeled and all of are unlabeled. In the following experiments, we will estimate the density ratio function using 1000 points in and use the labeled data from to build a regression function or classifier on .

6.4.1 Regression

Given data sets where is for independent variable, and is for dependent variable, and a test data set with a different distribution, the regression problem is to obtain a function a predictor on . To make the comparison between unweighted regression method and different weighting schemes, we use the simplest regression method, the least square linear regression. With this method, the regression function is of the form

where and denotes the pseudo-inverse of a matrix. Here is a diagonal matrix with the estimated density ratio on the diagonal. These are estimated using FIRE and other density ratio estimation methods for comparison. The results on 3 regression data sets are shown in Table 5, 5 and 5.

| No. of Labeled | 100 | 200 | 500 | 1000 | ||||

|---|---|---|---|---|---|---|---|---|

| Weighting method | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces |

| OLS | 0.740 | 0.497 | 0.828 | 0.922 | ||||

| TIKDE | 0.379 | 0.359 | 0.299 | 0.291 | 0.278 | 0.279 | 0.263 | 0.267 |

| KMM | 1.857 | 1.857 | 1.899 | 1.899 | 2.508 | 2.508 | 2.739 | 2.739 |

| LSIF | 0.390 | 0.390 | 0.309 | 0.309 | 0.329 | 0.329 | 0.314 | 0.314 |

| FIRE() | 0.327 | 0.327 | 0.286 | 0.286 | 0.272 | 0.272 | 0.260 | 0.260 |

| FIRE() | 0.326 | 0.330 | 0.285 | 0.287 | 0.272 | 0.272 | 0.261 | 0.259 |

| FIRE() | 0.324 | 0.333 | 0.284 | 0.288 | 0.271 | 0.272 | 0.261 | 0.260 |

| No. of Labeled | 100 | 200 | 500 | 1000 | ||||

|---|---|---|---|---|---|---|---|---|

| Weighting method | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces |

| OLS | 0.588 | 0.552 | 0.539 | 0.535 | ||||

| TIKDE | 0.572 | 0.574 | 0.545 | 0.545 | 0.526 | 0.529 | 0.523 | 0.524 |

| KMM | 0.582 | 0.582 | 0.547 | 0.547 | 0.522 | 0.522 | 0.514 | 0.514 |

| LSIF | 0.565 | 0.563 | 0.543 | 0.541 | 0.520 | 0.520 | 0.517 | 0.516 |

| FIRE() | 0.567 | 0.560 | 0.548 | 0.540 | 0.524 | 0.519 | 0.522 | 0.515 |

| FIRE() | 0.563 | 0.560 | 0.546 | 0.540 | 0.522 | 0.519 | 0.520 | 0.515 |

| FIRE() | 0.563 | 0.560 | 0.546 | 0.541 | 0.522 | 0.519 | 0.520 | 0.515 |

| No. of Labeled | 100 | 200 | 500 | 1000 | ||||

|---|---|---|---|---|---|---|---|---|

| Weighting method | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces |

| OLS | 0.116 | 0.111 | 0.105 | 0.101 | ||||

| TIKDE | 0.111 | 0.111 | 0.100 | 0.100 | 0.096 | 0.096 | 0.092 | 0.092 |

| KMM | 0.112 | 0.161 | 0.103 | 0.164 | 0.099 | 0.180 | 0.095 | 0.178 |

| LSIF | 0.113 | 0.113 | 0.109 | 0.109 | 0.104 | 0.104 | 0.099 | 0.099 |

| FIRE() | 0.110 | 0.110 | 0.101 | 0.102 | 0.097 | 0.097 | 0.093 | 0.094 |

| FIRE() | 0.113 | 0.110 | 0.103 | 0.102 | 0.099 | 0.097 | 0.097 | 0.094 |

| FIRE() | 0.112 | 0.118 | 0.102 | 0.106 | 0.099 | 0.103 | 0.096 | 0.102 |

6.4.2 Classification

Similarly to the case of regression the density ratio can also be used for building a classifier such as SVM. Given a set of labeled data, ,, , and , we building a linear classifier by the weighted linear SVM algorithm as follows:

The weights ’s are obtained by various density ratios estimation algorithms using two data sets and . Note that estimating the density ratios using and is completely independent of the label information. We also explore the performance of these weighted SVM as the number of labeled points used for training classifier changes. In the experiments, we first estimate the density ratios on the whole with the parameters selected by cross validation. Then we subsample a portion of and use their labels to train the classifier. And the performance of the classifier in terms of prediction error is estimated using all the points in . The results on USPS hand-written digits and 20 news groups are shown in Table 7, 7, 9 and 9.

| No. of Labeled | 100 | 200 | 500 | 1000 | ||||

|---|---|---|---|---|---|---|---|---|

| Weighting method | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces |

| SVM | 0.102 | 0.081 | 0.057 | 0.058 | ||||

| TIKDE | 0.094 | 0.094 | 0.072 | 0.072 | 0.049 | 0.049 | 0.042 | 0.042 |

| KMM | 0.081 | 0.081 | 0.059 | 0.059 | 0.047 | 0.047 | 0.044 | 0.044 |

| LSIF | 0.095 | 0.102 | 0.073 | 0.081 | 0.050 | 0.057 | 0.044 | 0.058 |

| FIRE() | 0.089 | 0.068 | 0.053 | 0.050 | 0.041 | 0.041 | 0.037 | 0.036 |

| FIRE() | 0.070 | 0.070 | 0.051 | 0.051 | 0.041 | 0.041 | 0.036 | 0.036 |

| FIRE() | 0.055 | 0.073 | 0.048 | 0.054 | 0.041 | 0.044 | 0.034 | 0.039 |

| No. of Labeled | 100 | 200 | 500 | 1000 | ||||

|---|---|---|---|---|---|---|---|---|

| Weighting method | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces |

| SVM | 0.186 | 0.164 | 0.129 | 0.120 | ||||

| TIKDE | 0.185 | 0.185 | 0.164 | 0.164 | 0.124 | 0.124 | 0.105 | 0.105 |

| KMM | 0.175 | 0.175 | 0.135 | 0.135 | 0.103 | 0.103 | 0.085 | 0.085 |

| LSIF | 0.185 | 0.185 | 0.162 | 0.163 | 0.122 | 0.122 | 0.108 | 0.108 |

| FIRE() | 0.179 | 0.184 | 0.161 | 0.161 | 0.115 | 0.120 | 0.107 | 0.105 |

| FIRE() | 0.180 | 0.185 | 0.161 | 0.162 | 0.116 | 0.120 | 0.106 | 0.107 |

| FIRE() | 0.183 | 0.184 | 0.160 | 0.162 | 0.118 | 0.120 | 0.106 | 0.103 |

| No. of Labeled | 100 | 200 | 500 | 1000 | ||||

|---|---|---|---|---|---|---|---|---|

| Weighting method | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces |

| SVM | 0.326 | 0.286 | 0.235 | 0.204 | ||||

| TIKDE | 0.326 | 0.326 | 0.286 | 0.285 | 0.235 | 0.235 | 0.204 | 0.204 |

| KMM | 0.338 | 0.338 | 0.303 | 0.303 | 0.252 | 0.252 | 0.242 | 0.242 |

| LSIF | 0.329 | 0.325 | 0.297 | 0.285 | 0.238 | 0.235 | 0.210 | 0.204 |

| FIRE() | 0.314 | 0.324 | 0.276 | 0.278 | 0.231 | 0.234 | 0.202 | 0.210 |

| FIRE() | 0.315 | 0.323 | 0.276 | 0.277 | 0.232 | 0.233 | 0.200 | 0.208 |

| FIRE() | 0.317 | 0.321 | 0.277 | 0.275 | 0.232 | 0.231 | 0.197 | 0.207 |

| No. of Labeled | 100 | 200 | 500 | 1000 | ||||

|---|---|---|---|---|---|---|---|---|

| Weighting method | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces | Linear | Half-spaces |

| SVM | 0.354 | 0.333 | 0.300 | 0.284 | ||||

| TIKDE | 0.354 | 0.353 | 0.334 | 0.335 | 0.299 | 0.298 | 0.281 | 0.285 |

| KMM | 0.368 | 0.368 | 0.341 | 0.341 | 0.295 | 0.295 | 0.270 | 0.270 |

| LSIF | 0.353 | 0.354 | 0.336 | 0.334 | 0.304 | 0.305 | 0.286 | 0.284 |

| FIRE() | 0.347 | 0.348 | 0.334 | 0.332 | 0.303 | 0.300 | 0.282 | 0.277 |

| FIRE() | 0.348 | 0.348 | 0.332 | 0.332 | 0.301 | 0.301 | 0.277 | 0.277 |

| FIRE() | 0.347 | 0.349 | 0.330 | 0.330 | 0.303 | 0.300 | 0.284 | 0.278 |

6.5 Simulated Examples

6.5.1 Simulated Dataset 1.

We use a simple example, where the two densities are known, to demonstrate the properties of our methods and how the number of data points influences the performance.

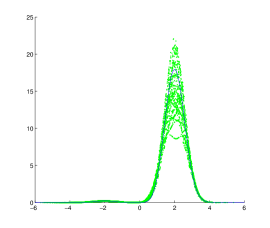

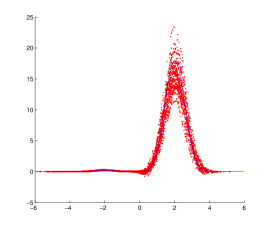

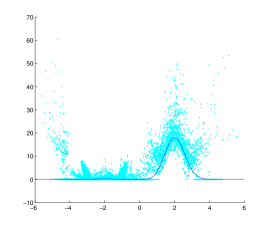

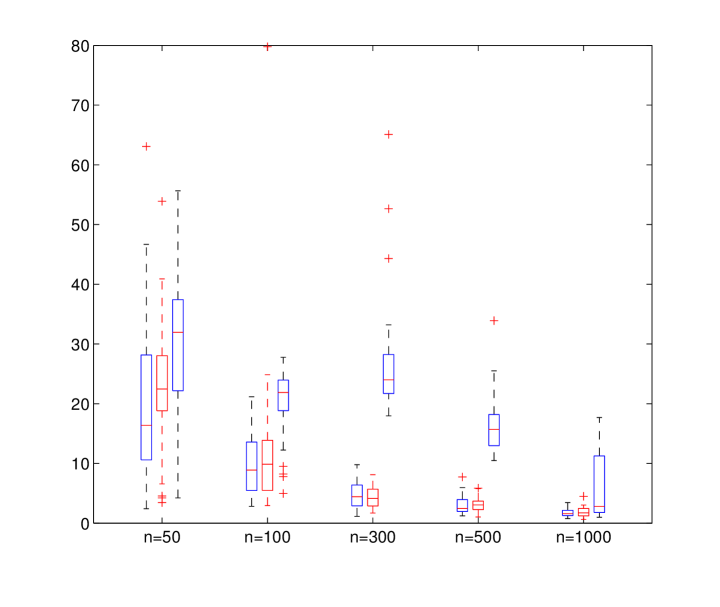

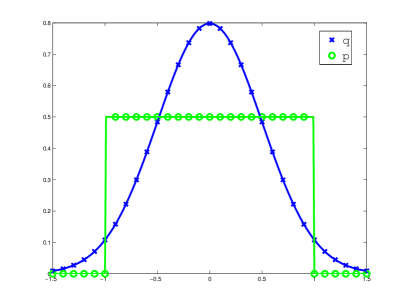

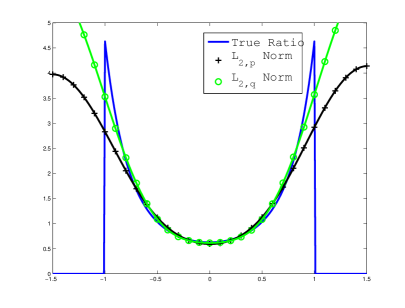

For this experiment, we suppose and and fix , and vary from 50 to 1000. We compare our method with the other two methods for the same problem: TIKDE and KMM. For all the methods we consider in this experiment, we will choose the optimal parameter based on the empirical norm of the difference between the estimated ratio and the true ratio, which is supposed to be known in this toy example. Figure 2 gives the reader an intuition about how the estimated ratios behave for different methods.

And Figure 3 shows how different methods perform when varies from 50 to 1000 and is fixed to be 2000. The boxplot is also a good way to illustrate the stability of the methods over 50 independent repetitions.

6.5.2 Simulated Dataset 2.

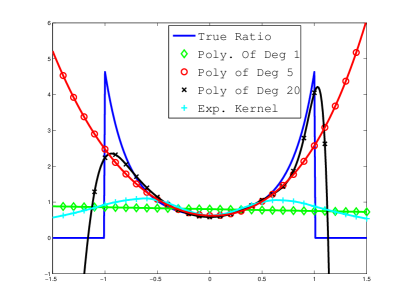

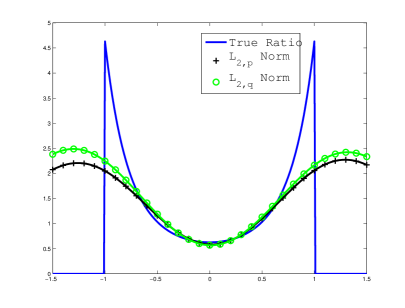

In the second simulated example, we will test our method for various kernels and different norms as the cost function. More specifically, we suppose and . We will use this example to explore the power of our methods with different kernels. Three settings are considered in this experiments: (1)Different kernels for the RKHS. We use polynomial kernels of degree 1, 5 and 20, exponential kernel and Gaussian kernel; (2) Type-I setting and Type-II setting; (3) Different norm for the cost function in the algorithm, i.e. and . In this example, focuses on the region close 0, but still has penalty outside interval ; has uniform penalty on and has no penalty at all outside the interval.

In all settings, we fix the convolution kernel to be Gaussian, . When the RKHS kernel is exponential and Gaussian, we also need to decide their width. For simplicity, we just fix their width to be , where is the width of the convolution kernel . For setting Type-I, we will set and ; for Type-II setting, we only specify . The results are shown in Figure 4.

Acknowledgements

We are grateful to Yusu Wang for many valuable discussions and suggestions. We also thank Lorenzo Rosasco for very useful discussions and Christoph Lampert for pointing us to important related papers.

We thank the Austrian Institute of Technology (ISTA) and Herbert Edelsbrunner’s research group for their hospitality during writing of the paper.

The work was partially supported by the NSF Grants IIS 0643916 and IIS 1117707.

References

- [1] Frank Bauer, Sergei Pereverzev, and Lorenzo Rosasco. On regularization algorithms in learning theory. Journal of complexity, 23(1):52–72, 2007.

- [2] Mikhail Belkin, Partha Niyogi, and Vikas Sindhwani. Manifold regularization: A geometric framework for learning from labeled and unlabeled examples. The Journal of Machine Learning Research, 7:2399–2434, 2006.

- [3] Steffen Bickel, Michael Brückner, and Tobias Scheffer. Discriminative learning for differing training and test distributions. In Proceedings of the 24th international conference on Machine learning, pages 81–88. ACM, 2007.

- [4] Raymond J Carroll and Peter Hall. Optimal rates of convergence for deconvolving a density. Journal of the American Statistical Association, 83(404):1184–1186, 1988.

- [5] Ernesto De Vito, Lorenzo Rosasco, Andrea Caponnetto, Umberto De Giovannini, and Francesca Odone. Learning from examples as an inverse problem. Journal of Machine Learning Research, 6(1):883, 2006.

- [6] Ernesto De Vito, Lorenzo Rosasco, and Alessandro Toigo. Spectral regularization for support estimation. Advances in Neural Information Processing Systems, NIPS Foundation, pages 1–9, 2010.

- [7] P. Eggermont and V. LaRicca. Maximum smoothed likelihood density estimation for inverse problems. Annals of Statistics, 23:199–220, 1995.

- [8] Arthur Gretton, Alex Smola, Jiayuan Huang, Marcel Schmittfull, Karsten Borgwardt, and Bernhard Schölkopf. Covariate shift by kernel mean matching. Dataset shift in machine learning, pages 131–160, 2009.

- [9] S Grünewälder, G Lever, L Baldassarre, S Patterson, A Gretton, and M Pontil. Conditional mean embeddings as regressors. In Proceedings of the 29th International Conference on Machine Learning, ICML 2012, volume 2, pages 1823–1830, 2012.

- [10] Jiayuan Huang, Alexander J. Smola, Arthur Gretton, Karsten M. Borgwardt, and Bernhard Schölkopf. Correcting sample selection bias by unlabeled data. In NIPS, pages 601–608, 2006.

- [11] Alan Julian Izenman. Review papers: Recent developments in nonparametric density estimation. Journal of the American Statistical Association, 86(413):205–224, 1991.

- [12] David Jacho-Chávez. k nearest-neighbor estimation of inverse density weighted expectations. Economics Bulletin, 3(48):1–6, 2008.

- [13] Takafumi Kanamori, Shohei Hido, and Masashi Sugiyama. A least-squares approach to direct importance estimation. The Journal of Machine Learning Research, 10:1391–1445, 2009.

- [14] Joo Seuk Kim and Clayton Scott. Robust kernel density estimation. In Acoustics, Speech and Signal Processing, 2008. ICASSP 2008. IEEE International Conference on, pages 3381–3384. IEEE, 2008.

- [15] Rainer Kress. Linear integral equations, volume 82. Springer Verlag, 1999.

- [16] Jun Liu. Metropolized independent sampling with comparisons to rejection sampling and importance sampling. Statistics and Computing, 6:113–119, 1996.

- [17] Radford M Neal. Annealed importance sampling. Statistics and Computing, 11(2):125–139, 2001.

- [18] XuanLong Nguyen, Martin J Wainwright, and Michael I Jordan. Estimating divergence functionals and the likelihood ratio by penalized convex risk minimization. Advances in neural information processing systems, 20:1089–1096, 2008.

- [19] Sinno Jialin Pan and Qiang Yang. A survey on transfer learning. Knowledge and Data Engineering, IEEE Transactions on, 22(10):1345–1359, 2010.

- [20] E. Parzen. On estimation of a probability density function and mode. The Annals of Mathematical Statistics, 33:1065–1076, 1962.

- [21] Bernhard Schölkopf and Alexander J Smola. Learning with kernels: Support vector machines, regularization, optimization, and beyond. MIT press, 2001.

- [22] John Shawe-Taylor and Nello Cristianini. Kernel methods for pattern analysis. Cambridge university press, 2004.

- [23] Tao Shi, Mikhail Belkin, and Bin Yu. Data spectroscopy: Eigenspaces of convolution operators and clustering. The Annals of Statistics, 37(6B):3960–3984, 2009.

- [24] Hidetoshi Shimodaira. Improving predictive inference under covariate shift by weighting the log-likelihood function. Journal of Statistical Planning and Inference, 90(2):227–244, 2000.

- [25] Alex J Smola and Bernhard Schölkopf. On a kernel-based method for pattern recognition, regression, approximation, and operator inversion. Algorithmica, 22(1):211–231, 1998.

- [26] Ingo Steinwart and Andreas Christmann. Support vector machines. Springer, 2008.

- [27] R. S. Strichartz. Analysis of the laplacian on the complete riemannian manifold. Journal of Functional Analysis, 52:48–79, 1983.

- [28] Masashi Sugiyama, Matthias Krauledat, and Klaus-Robert Müller. Covariate shift adaptation by importance weighted cross validation. The Journal of Machine Learning Research, 8:985–1005, 2007.

- [29] Masashi Sugiyama, Shinichi Nakajima, Hisashi Kashima, Paul Von Buenau, and Motoaki Kawanabe. Direct importance estimation with model selection and its application to covariate shift adaptation. Advances in Neural Information Processing Systems, 20:1433–1440, 2008.

- [30] M.E. Taylor. Partial Differential Equation. Springer, 1997.

- [31] Vladimir Vapnik and Sayan Mukherjee. Support vector method for multivariate density estimation. In NIPS, pages 659–665, 1999.

- [32] Grace Wahba. Practical approximate solutions to linear operator equations when the data are noisy. SIAM Journal on Numerical Analysis, 14(4):651–667, 1977.

- [33] Christopher Williams and Matthias Seeger. The effect of the input density distribution on kernel-based classifiers. In Proceedings of the 17th International Conference on Machine Learning. Citeseer, 2000.

- [34] Yuan Yao, Lorenzo Rosasco, and Andrea Caponnetto. On early stopping in gradient descent learning. Constructive Approximation, 26(2):289–315, 2007.

- [35] Yaoliang Yu and Csaba Szepesvári. Analysis of kernel mean matching under covariate shift. In ICML, 2012.

- [36] Bianca Zadrozny. Learning and evaluating classifiers under sample selection bias. In Proceedings of the twenty-first international conference on Machine learning, page 114. ACM, 2004.

Appendix A Proof for Lemma 5

Proof.

RKHS is unique for a given domain and kernel, so is independent of the measure used to define the . Thus for any , there should be such that and

Since this is true for arbitrary , we have

Because ,

| (37) |

To bound

We need the Fourier transform , defined as

on is the heat operator, thus . And

So, . Note that is an isometry. Thus it is the same to transform the (37) using Fourier transform. Then we have

where . And let

and . It is obvious that . And

Now we recall the definition of Sobolev space using Fourier transform, which states that for some . Thus,

Thus, we have

Let and , we have the lemma. ∎

Appendix B Proof for Lemma 6

For the compact manifold case, we also need to have similar lemma as the above one. However, the definition of Fourier transform is obscure, thus we need to consider alternative way to get the same bound. We can use the Laplace-Beltrami operator on the compact manifold. It has discrete spectrum and satisfies the Weyl’s Law, see Chapter 8 in [30], about the spectrum of the Laplace-Beltrami operator , which is discrete if the manifold is compact. It states the following: the number of eigenvalues of Laplacian operator over a bounded domain with Neumann Bounday condition that are less or equal than , denoted by , satisfies

for a constant depending on the dimensionality and volume of the domain. This implies there exists such that for any ,

Also, we can redefine the Sobolev space on a compact manifold using Laplace-Beltrami operator.

And this definition of is equivalent to common definition of Sobolev space using differentiation, see [27] for the details for this equivalence.

First we need the following lemma.

Lemma 9.

Suppose and , then we have

where is the eigenfunctions of Laplacian operator and is a constant independent of .

Proof.

First let proof that

Using the implication of Weyl’s Law, we have for , . Thus,

Let . For . We have

Thus,

∎

Now we can give the proof for Lemma 6.

Proof.

RKHS is unique for a given domain and kernel, so is independent of the measure used to define the . Thus for any , there should be such that and

Since this is true for arbitrary , we have

Because ,

Now, let

Expend using the eigenfunctions of , we have

Denote the eigenvalues of as , the heat operator defined as having eigenvalues as . Recall the Weyl’s law, we have there exists such that for any , . When is small enough, we will have . Since we order in non-decreasing order, for any , we have , also . Now denote be the operator that projects function to the subspace spanned by first eigenfunctions of . Thus

where is the eigenfunction of . And let

Thus, we have

| (38) |

Now let us proceed by bound the above formula. By Lemma 9 with and , we have

Also, for , , thus . Recall we have for a constant . Thus, we have

For the third term in (38), we have

Hence,

When is small enough, , letting , we prove the lemma. ∎

Appendix C Proof for Theorems in 4.2.2

In the second case, since we do not have samples from , we replace by . Consider corresponding ,

Thus, we need to bound the extra term . Let and , we have

The bound for is given in the following lemma.

Lemma 10.

Suppose are two density function of probability measures of the domain and satisfying the assumptions we gave in section 4.1. We have the following: (1) When is and , we have

(2) When is a manifold without boundary of dimension and , we have

for any .

Proof.

By definition of , we have

By results in [PLM_UCTHESIS_03], we have when is twice differentiable. Due to , we have . Thus, we have

For manifold case, we have , where . Thus,

For the first term, we have the same rate with . Now we proceed by bounding the second term.

We know that .

Let and is the projection of on the . In the following proof, we need to use change of variables to converting integral over a manifold to the integral over the tangent space at a specific point. For two points , let be the projection of in the tangent space of at . Let denote the Jacobian of the map at point and is the inverse. For sufficiently close to , we have

Thus, it is true that the points in are still no further than , when is small enough. Since has exponential decay, the integral is of order , and so is . Thus, for any point ,

Abusing the notation of , we have where . ∎

For the concentration of , we will consider their close formulas

| (39) |

By the similar argument to that in Lemma 8, we will have the following lemma gives the concentration bound.

Lemma 11.

Proof.

Let . We have . For , using the fact that , we have

And

Notice that we have and in the identity we get. For these two objects, it is not hard to verify the following identities,

And

Thus, in these two identities, the only two random variables are . By results about concentration of and , we have with probability ,

| (40) |

And we know that for a large enough constant which is independent of and ,

and

thus, .

Notice that and , both of this could be of smaller order compared with . For simplicity we hide the term including them in the final bound without changing the dominant order. We could also hide the terms with the product of any two the random variables in Eq. 40, which is of prior order compared to the term with only one random variable. Now let us put everything together,

where . ∎

Given the above lemmas, the main theorem for the second case follows.