Robust VIF regression with application to variable selection in large data sets

Abstract

The sophisticated and automated means of data collection used by an increasing number of institutions and companies leads to extremely large data sets. Subset selection in regression is essential when a huge number of covariates can potentially explain a response variable of interest. The recent statistical literature has seen an emergence of new selection methods that provide some type of compromise between implementation (computational speed) and statistical optimality (e.g., prediction error minimization). Global methods such as Mallows’ have been supplanted by sequential methods such as stepwise regression. More recently, streamwise regression, faster than the former, has emerged. A recently proposed streamwise regression approach based on the variance inflation factor (VIF) is promising, but its least-squares based implementation makes it susceptible to the outliers inevitable in such large data sets. This lack of robustness can lead to poor and suboptimal feature selection. In our case, we seek to predict an individual’s educational attainment using economic and demographic variables. We show how classical VIF performs this task poorly and a robust procedure is necessary for policy makers. This article proposes a robust VIF regression, based on fast robust estimators, that inherits all the good properties of classical VIF in the absence of outliers, but also continues to perform well in their presence where the classical approach fails.

doi:

10.1214/12-AOAS584keywords:

and t1Supported by the Natural Sciences and Engineering Research Council of Canada. t2Supported by Swiss National Science Foundation Grant 100018-131906.

1 Introduction

Data sets with millions of observations and a huge number of variables are now quite common, especially in business- and finance-related fields, as well as computer sciences, health sciences, etc. An important challenge is to provide statistical tools and algorithms that can be used with such data sets. In particular, for regression models, a first data analysis requires that the number of potential explanatory variables be reduced to a reasonable and tractable amount. Consider potential explanatory variables and a response variable observed on subjects. The classical normal linear model supposes with slope parameters . The aim is to find a subset of explanatory variables that satisfies a given criterion and such that the regression model holds.

The selection criteria are numerous and can be based on prediction, fit, etc. The available selection procedures can be broadly classified into three classes according to their general strategy and, as a result, their computational speed. A first class considers all the possible combinations of covariates as potential models, evaluates each according to a fixed criterion, and chooses the model which best suits the selected criterion. A second class is formed of sequential selection procedures in which a covariate at a time is entered in (or removed from) the model, based on a criterion that can change from one step to the next and that is computed for all potential variables to enter (or to exit) until another criterion is reached. Finally, the third class of selection procedures is also sequential in nature, but each covariate is only considered once as a potential covariate. For the first class, we find criteria such as the AIC [Akaike (1973)], BIC [Schwarz (1978)], Mallows’ [Mallows (1973)], cross-validation, etc. [see also Efron (2004)]. These methods are not adapted to large data sets since the number of potential models becomes too large and the computations are no longer feasible. For the second class, we find, for example, the classical stepwise regression which can be considered as a simple algorithm to compute the estimator of regression coefficients that minimizes an penalized sum of squared errors , with and and a vector of ones, that is, [see Lin, Foster and Ungar (2011)], with if and otherwise. Fast algorithms for stepwise regressions are available, for example, Foster and Stine (2004). Procedures for the problem are also available, for example, Lasso/LARS [Efron et al. (2004)], the Dantzig Selector [Candes and Tao (2007)], or coordinate descent [Friedman, Hastie and Tibshirani (2010)]. But these algorithms may also become very slow for large data sets, not only because all remaining variables are evaluated at each stage, but also because the penalty needs to be computed, and often via cross-validation. The last class is a variation of stepwise regression in which covariates are tested sequentially but only once for addition to the model. An example is the streamwise regression of Zhou et al. (2006), which uses the -investing rule [Foster and Stine (2008)], is very fast, and guards against overfitting. An improved streamwise regression approach was recently proposed in Lin, Foster and Ungar (2011) where a very fast to compute test statistic based on the variance inflation factor (VIF) of the candidate variable, given the currently selected model, is proposed. The approach takes into account possible multicollinearity, seeking to find the best predictive model, even if it is not the most parsimonious. Comparisons in Lin, Foster and Ungar (2011) establish that the method performs well and is the fastest available.

Our concern in this paper is to provide model selection tools for the regression model that are robust to small model deviations. As argued in Dupuis and Victoria-Feser (2011) [see also Ronchetti and Staudte (1994)], spurious model deviations such as outliers can lead to a completely different, and suboptimal, selected model when a nonrobust criterion, like Mallows’ or the VIF, is used. This happens because under slight data contamination, the estimated model parameters, using, for example, the least squares estimator (LS) and, consequently, the model choice criterion, can be seriously biased. The consequence is that when the estimated criteria are compared to an absolute level (like a quantile of the distribution), the decisions are taken at the wrong level. For the first class of selection procedures, robust criteria have been proposed such as the robust AIC of Ronchetti (1982), the robust BIC of Machado (1993), the robust Mallows’ of Ronchetti and Staudte (1994), and a robust criterion based on cross-validation (CV) in Ronchetti, Field and Blanchard (1997). Since standard robust estimators are impossible to compute when the number of covariates is too large, Dupuis and Victoria-Feser (2011) proposed the use of a forward search procedure together with adjusted robust estimators when there is a large number of potential covariates. Their selection procedure, called Fast Robust Forward Selection (FRFS), falls in the second class of selection procedures. FRFS outperforms classical approaches such as Lasso/LARS when data contamination is present and outperforms, in all studied instances, a robust version of the LARS algorithm proposed by Khan, Van Aelst and Zamar (2007).

However, although FRFS is indeed very fast and robust, it too can become quite slow when the number of potential covariates is very large, as all covariates are reconsidered after one is selected for entry in the model. It is therefore important to have a robust selection procedure in the streamwise regression class so that very large data sets can be analyzed in a robust fashion. In this paper we develop a robust VIF approach that is fast, very efficient, and clearly outperforms nonrobust VIF in the presence of outliers.

The remainder of the paper is organized as follows. In Section 2 we review the classical VIF approach and present our robust VIF approach. A simulation study in Section 3 shows the good performance of the new approach. In Section 4 we analyze educational attainment data and show how policy makers are better served by robust VIF regression than by classical VIF or Lasso. In Section 5 we present a shorter analysis of a large crime data set that highlights more problems with classical VIF for real data. Section 6 contains a few closing remarks.

2 Robust VIF regression

2.1 The classical approach

Lin, Foster and Ungar (2011) propose a procedure that allows one to sweep through all available covariates and to enter those that can reduce a statistically sufficient part of the variance in the predictive model. Let be the design matrix that includes the selected variables at a given stage, and with the new potential covariate to be considered for inclusion. Without loss of generality, we suppose all variables have been standardized. Consider the following two models:

| (1) | |||||

| (2) |

where are the residuals of the projection of on . All known estimators of the parameters and will provide different estimates when the covariates present some degree of multicollinearity, and, consequently, significance tests based on estimates of or do not necessarily lead to the same conclusions. While in stepwise regression the significance of in model (1) is at the core of the selection procedure, in streamwise regression one estimates more conveniently . Lin, Foster and Ungar (2011) show that, when LS are used to estimate, where . They then compare , with suitable estimates for and , to the standard normal distribution to decide whether or not should be added to the current model. The procedure is called VIF regression since Marquardt (1970) called the VIF for .

2.2 A robust weighted slope estimator

Since the test statistic is based on the following, (1) the LS estimator , (2) , in turn based on the design matrix and , and (3) the classical estimator of , it is obviously very sensitive to outliers, a form of model deviation. An extreme response or a very badly placed design point can have a drastic effect on . The latter is then compared to the null distribution: the correct asymptotic distribution under the hypothesis that the regression model holds. With model deviations, the null distribution is not valid and, hence, selection decisions (to add the covariate or not) are taken rather arbitrarily. We propose here to limit the influence of extreme observations by considering weighted LS estimators of the form

| (3) |

with and . The weights depend on the data and are such that extreme observations in the response and/or in the design have a nil or limited effect on the value of . Dupuis and Victoria-Feser (2011) propose Tukey’s redescending biweight weights

| (4) |

where are standardized residuals that are computed in practice for chosen estimators of and (see below). The constant controls the efficiency and the robustness of the estimator. Indeed, the most efficient estimator is the LS estimator, that is, (3) with all weights equal to one (i.e., ), but it is very sensitive to (small) model deviations, while a less efficient but more robust estimator is obtained by downweighting observations that have a large influence on the estimator, that is, by setting in (4). The value corresponds to an efficiency level of 95% for the robust estimator compared to the LS estimator at the normal model and is the value used throughout the paper.

We follow Dupuis and Victoria-Feser (2011) and use for the weights in (3), where the residuals and , the median absolute deviation (MAD) of the residuals . The slope estimates are , with and , , with weights , for all , computed using (4) at the residuals , with . The slope estimators and the intercept estimators are computed on the marginal models using a robust weighted estimator defined implicitly through

| (5) |

Here we consider Huber’s weights given for the regression model by

| (6) |

with . Estimators in (5) belong to the class of -estimators [Huber (1964, 1967)]. With (6) in (5), the marginal intercepts and slope estimators are simpler (and faster) to compute than the ones based on Tukey’s biweight weights as originally proposed in Dupuis and Victoria-Feser (2011). For the scale in the weights in (5), we propose to use the MAD of the residuals.

The estimator in (3) is a one-step estimator that is actually biased when there is multicollinearity in the covariates. Dupuis and Victoria-Feser (2011) show that the bias can be made smaller and even nil if is iterated further to get, say, , computed at the updated weights based on the residuals . In the simulation study in Section 3, however, we find that the bias is very small even with relatively large multicollinearity, so that in practice there is often no need to proceed with this iterative correction.

Finally, is a coordinate-wise robust estimator and Alqallaf et al. (2009) show, through the computation of a generalized version of the influence function [Hampel (1968, 1974)] and different contamination schemes in the multivariate normal (MVN) setting, that coordinate-wise robust estimators can be less sensitive to extreme observations when they occur independently at the univariate level.

2.3 Robust VIF selection criterion

Let be the weighted design matrix at stage with, say, columns (hence covariates), and the new candidate covariate that is evaluated at the current stage . One could use the weights for instead of the weights computed at the marginal models with only as a covariate, but this would require more computational time. The simulation results in Section 3 show that one gets very satisfactory results with . Let also and define as the last element of the vector with . is actually a robust estimator of in (1). Let and , then

where are the residuals of the weighted fit of on . Let

then

with , that is, the weighted estimator of the fit of on the weighted residuals , that is, model (2). Note, however, that is not equal to the last element of unless the weights are used for . Note also that we can write

with

| (7) |

a robust estimate of the coefficient of determination . Renaud and Victoria-Feser (2010) propose a robust based on weighted responses and covariates and (7) is equivalent to their proposal (with , see their Theorem 1) but with other sets of weights. Moreover, is the partial variance of given [see Dupuis and Victoria-Feser (2011)].

Lin, Foster and Ungar (2011) note that using all the data to compute (in the classical setting) is quite computationally expensive and they propose a subsampling approach. For the same reason, we also propose to actually estimate by computing (7) on a randomly chosen subset of size .

To derive the -statistic based on , we follow Lin, Foster and Ungar (2011) who base their comparison on the expected value of the estimated variance of, respectively, and . Let and be, respectively, robust residual variance estimates for models (1) and (2). Let also denote the element of matrix . For , supposing that , we can use

with

| (8) |

and the standard normal cumulative distribution [see Heritier et al. (2009), equation (3.20)]. For , based on the model with as the response and as the explanatory variable (without intercept), we have

with the efficiency of a robust slope estimator computed using Huber’s weights relative to the LS, which is not equal to , the efficiency of a robust slope estimator computed using Tukey’s weights relative to the LS. We will see below that the computation of the former is not needed. Hence, approximating , we have

An honest approximate robust test statistic is then given by

that is,

| (9) |

with a robust mean squared error for the model with as response and as explanatory variable [i.e., model (2)]. We use .

Our fast robust evaluation procedure is summarized by the following five steps. Suppose that we are at stage and a set of covariates has been chosen in the model. We are considering covariate for possible entry. We are working with and have computed and the weights and : {longlist}[(1)]

Obtain the residuals .

Set . Compute and .

Sample a small subset of the observations and let denote the corresponding subsample from the regressor .

Let , compute , and find .

Compute the approximate -ratio and compare it to an adapted quantile to decide whether or not to add to the current set. A more detailed algorithm in which the decision rule (whether or not to add the new variable) is also specified is given in the Appendix. Note that in Step 5 above, the rejection quantile, or corresponding probability , is adapted at each step so that increases/decreases if a rejection is made/not made. As explained in Lin, Foster and Ungar (2011), one can think of as a gambler’s wealth and the game is over when .

2.4 Comparison with the robust -statistic of FRFS

The -statistic proposed by Dupuis and Victoria-Feser (2011) [equation (5)] and used to test whether a candidate covariate is entered in the current model can be written as

with . Supposing that and , then

Hence, in (9) and in (2.4) differ by a multiplicative factor of

which is the ratio of the robustly estimated covariance between and , and the robustly estimated partial covariance between and given . One can notice that in the orthogonal case (and standardized covariates), we have so that . The value of was computed in some of the simulations outlined in the following section. While maintained a median value of 1 when aggregating over the 200 simulated data sets at a given setting, its variability changed with the theoretical and the absence or presence of outliers. For example, the interquartile range went from a value near 0 for and no outliers, to 5 for and 5% outlying responses with high leverage in the case. There can thus be a considerable difference in the two test statistics.

3 Simulation study

We carry out a simulation study to assess the effectiveness of the model selection approaches outlined above. First, we create a linear model

| (11) |

where are multivariate normal (MVN) with ,, and , , and an independent standard normal variable. We choose to produce a range of theoretical values for (11) and to give values for our target regressors of about 6 under normality as in Ronchetti, Field and Blanchard (1997). The covariates are our target covariates. Let be independent standard normal variables and use the first to give the covariates

and the final to give the covariates

Variables are noise covariates that are correlated with our target covariates, and variables are independent noise covariates. Note that the covariates are then relabeled with a random permutation of so that the target covariates do not appear in position , but rather in arbitrary positions. This is necessary to test the effectiveness of the streamwise variable selection, as covariates considered early on are favored for entry when many covariates are correlated.

We consider samples without and with contamination. Samples with no contamination are generated using . To allow for 5% outliers, we generate using . These contaminated cases also have high leverage -values: as before, except , . This represents the most difficult contamination scheme: large residuals at high leverage points. We also investigate the less challenging cases of 5% outlying in response only and 5% high leverage only. We choose so that .

In all simulations we simulated independent samples, with or without contamination, to use for variable selection. Then, another independent samples without contamination were simulated for out-of-sample performance testing. The out-of-sample performance was evaluated using the mean sum of squared errors (MSE), , where is the estimated coefficient determined by the classical and robust VIF regression selection procedures or FRFS applied to the training set. Because the true predictors are known, we also compute the out-of-sample performance measure using the true . Classical VIF selection was carried out using the VIF package for R and default argument settings. Robust VIF was also implemented in R and code is available at http://neumann.hec.ca/pages/debbie.dupuis/ publicVIFfncs.R. FRFS is also implemented in R as outlined in Dupuis and Victoria-Feser (2011).

It should be noted that when evaluating the performance of a given criterion (here a selection procedure), the evaluation measure should be chosen in accordance with the performance measure [see Gneiting (2011)]. In our case, although the data are generated from contaminated conditional Gaussian models, the core model is still Gaussian and we wish to find the model that best predicts the conditional mean response. Consequently, a suitable performance measure is the expected squared error. However, when estimating the expected squared error from data, one can resort to the mean (i.e., the MSE) only if the data are purely issued from the postulated (core) Gaussian model. If this is not the case, or if there is no guarantee that this is the case, like, for example, with real data, then a more robust performance measure such as the median absolute prediction error (MAPE) should be chosen. Hence, in the simulations we use the MSE, while with real data sets we use the MAPE to estimate the evaluation measure for the comparison of the variable selection methods.

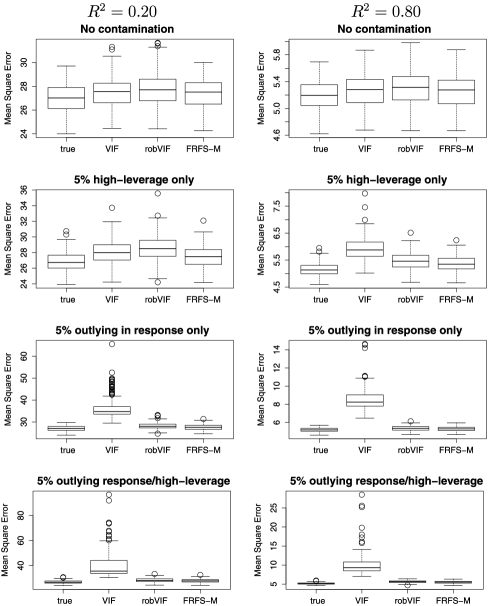

Simulations results for , , and and , are presented in Table 1 and Figures 1 and 2, respectively. Entries in the top panel of the table give the percentage of runs falling into each category. The category “Correct” means that the correct model was chosen. “Extra” means that a model was chosen for which the true model is a proper subset. “Missing 1” means that the model chosen differed from the true model only in that it was missing one of the target covariates; “Missing 2” and “Missing 3” are defined analogously. The Monte Carlo standard deviation of entries is bounded by . We also report the empirical marginal false discovery rate (mFDR) , where is the average number of true discoveries, is the average number of false discoveries, and is selected following Lin, Foster and Ungar (2011). We also report the required computation time. Note the particularly frugal robust approach to VIF regression: the cost of robustness is no more than a doubling of the computation time.

= No contam. 5% hl only 5% outliers No contam. 5% hl only 5% outliers C R F C R F C R F C R F C R F C R F %Correct %Extra %Missing 1 %Missing 2 %Missing 3 %Other %mFDR Time %Correct %Extra %Missing 1 %Missing 2 %Missing 3 %Other %mFDR Time

Both VIF algorithms do not perform well in terms of the proportion of correctly selected models and the FRFS-Marginal procedure clearly outperforms in this respect. The execution time of the FRFS-Marginal procedure, the faster of the two FRFS approaches presented in Dupuis and Victoria-Feser (2011), is roughly 25 times longer than that of the robust VIF procedure for these sizes of data sets. Both VIF algorithms do, however, choose a model for which the true model is a subset when there are no outliers. The classical VIF approach fails miserably in the presence of outliers (outlying response/high leverage), while the robust VIF approach is only slightly affected by the presence of outliers. The classical VIF approach is less affected by the presence of high leverage points only, but the effect is increased under more highly correlated regressors or a higher number of potential regressors. Results (not shown) for response variable only outliers are very similar to outlying response/high leverage outliers. Finally, other simulations (not shown) reveal that for less outlying contamination, the robust approaches always maintain good performance, while the negative impact on classical VIF is proportional to the level of outlyingness.

As the simulated data sets have noise covariates that are correlated with target covariates, the poor performance in terms of %Correct is expected given the streamwise approach of VIF regressions. But as pointed out by Lin, Foster and Ungar (2011), the goal here is different: good fast out-of-sample prediction, that is, one sacrifices parsimony for speed. The streamwise approach is fast and the main purpose of an -investing control is to avoid model overfitting. We assess the latter through out-of-sample performance. Figure 1 shows out-of-sample MSE for the case . Robust VIF is as efficient as classical VIF when there are no outliers (top panel) and clearly outperforms classical VIF when there is 5% contaminated observations (bottom panels). Robust VIF also loses very little with respect to FRFS-Marginal. Note that classical VIF seems to offer some resistance to contamination by high-leverage points only (as was also seen in Table 1), but completely falls apart in the presence of outlying response values, and this whether the outlying responses appear at high-leverage points or not. Much of the same can be seen in Figure 2 where results for the case are shown.

4 College data

Understanding the factors impacting an individual’s educational attainment is a preoccupation for many governmental and nongovernmental organizations. For example, a nation’s government that recognizes the potential economic benefits of higher education will seek to write public policies to promote it. Private industry that benefits from a well-educated labor market will let it affect decision making, for example, a company may choose to establish itself where lifelong education is easily accessible to its personnel. Finally, an individual’s family who associates personal achievement with higher levels of education may also act accordingly.

Since the first work by Wetterlind (1976) on projecting community college enrollments in Arizona, many researchers have sought to identify the factors impacting educational attainment; see, for example, Pennington, McGinty and Williams (2002), Petrongolo and San Segundo (2002), Kienzl, Alfonso and Melguizo (2007), and Clark (2011) (and references therein) for a list of various studies.

The data analyzed here are in the R package AER and are a subset of the data previously analyzed in Rouse (1995). There are 4739 observations on 14 variables. The variables are listed in Table 2. We seek to predict the number of years of education using 13 economic and demographic variables. There are continuous and binary variables along with one categorical variable with three categories which is converted to two dummy variables. When considering only first-order variables we thus have and ; when we include second-order interaction terms rises to 104 (some interaction terms are constant and are removed). We have standardized the variables. Our analysis will show how classical, that is, nonrobust, VIF regression can be inadequate for the policy maker by failing to keep important features.

| Variable | Description |

|---|---|

| gender | Factor indicating gender. |

| ethnicity | Factor indicating ethnicity (African-American, Hispanic or other). |

| score | Base year composite test score. These are achievement tests given |

| to high school seniors in the sample. | |

| fcollege | Factor. Is the father a college graduate? |

| mcollege | Factor. Is the mother a college graduate? |

| home | Factor. Does the family own their home? |

| urban | Factor. Is the school in an urban area? |

| unemp | County unemployment rate in 1980. |

| wage | State hourly wage in manufacturing in 1980. |

| distance | Distance from 4-year college (in 10 miles). |

| tuition | Average state 4-year college tuition (in 1000 USD). |

| income | Factor. Is the family income above USD 25,000 per year? |

| region | Factor indicating region (West or other). |

| education | Number of years of education. |

The selected models are compared using the median absolute prediction error (MAPE), as measured by 10-fold CV. That is, we split the data into 10 roughly equal-sized parts. For the th part, we carry out model selection using the other nine parts of the data and calculate the MAPE of the chosen model when predicting the th part of the data. We do this for and show boxplots of the 10 estimates of the MAPE. For all methods, the data were split in the same way. For the college data, we randomly generated the folds. Note here that we look at MAPE instead of mean squared prediction error, as these real data can contain outliers (as opposed to the simulated data which were clean) and the MAPE is a better choice.

| VIF | robVIF | FRFS-Marg/Full | |

| Variable | |||

| ethnicityafam | |||

| ethnicityhispanic | |||

| score | |||

| fcollegeyes | |||

| mcollegeyes | |||

| homeyes | |||

| urbanyes | – | – | |

| unemp | – | ||

| wage | – | ||

| distance | |||

| incomehigh | |||

| genderfemale | – | – |

| Variable | ||

| ethnicityafam | ||

| ethnicityhispanic | ||

| score | ||

| fcollegeyes | ||

| mcollegeyes | ||

| homeyes | ||

| urbanyes | – | |

| unemp | – | |

| wage | – | |

| distance | ||

| incomehigh | ||

| genderfemale:score | – | |

| genderfemale:fcollegeyes | – | |

| genderfemale:mcollegeyes | ||

| score:incomehigh | – | |

| fcollegeyes:homeyes | – | |

| fcollegeyes:unemp | – | |

| fcollegeyes:wage | – | |

| fcollegeyes:tuition | – | |

| mcollegeyes:wage | – |

For completeness, we compare the models selected by classical and robust VIF approaches with those of FRFS-Marginal and FRFS-Full where feasible, as well as that of the popular least angle regression (LARS) of Efron et al. (2004), an extremely efficient algorithm for computing the entire Lasso [Tibshirani (1996)] path. We use the R package lars to do the computations.

Tables 3 and 4 list the VIF and robust VIF regression selected features, along with estimated slopes, for the and scenarios, respectively. For both scenarios, the robust VIF regression approach selects slightly more, and/or slightly different, features. When considering only first-order terms, we see that the classical and robust estimates of commonly selected features are almost the same. This serves as a good form of validation for the relative importance of these features. However, the presence of outliers in the data has led classical VIF regression to completely miss two important features which are identified by robust VIF regression: unemp and wage. Even LS estimates (not shown) of the robust VIF regression selected model find these two features important with -values of 3.15 and , but the classical VIF regression selection procedure could not detect this importance for the reasons outlined in the Introduction. FRFS-Marginal and FRFS-Full selected features are identical. The latter features, along with estimated slopes, are also shown in Table 3.

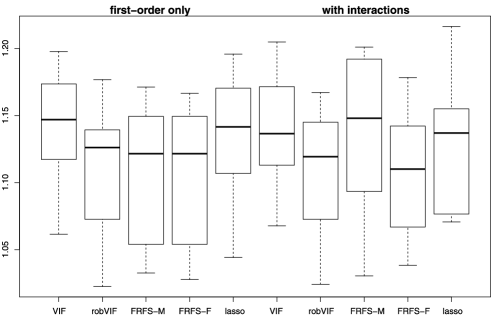

VIF regression also misses the two important features in the scenario; see Table 4. As both the county unemployment rate and the state hourly wage in manufacturing are directly impacted by economic policy, policy makers must be equipped with the best feature selection tools to have an effective strategy to reach sought after goals: in this case, increasing the level of education among its constituents. These tools, we argue, must include a robust selection procedure, as shown effectively by this example. Further evidence is given in Figure 3 where MAPE for VIF, robust VIF, FRFS-Marginal, and FRFS-Full and Lasso are shown for both scenarios. Robust VIF outperforms both of its nonrobust competitors, and even does better than FRFS-Marginal in the highly collinear case including interactions. It was shown in Dupuis and Victoria-Feser (2011) that FRFS-Marginal could select too few features in the highly collinear case and this motivated the development of FRFS-Full therein.

| # selected | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 |

|---|---|---|---|---|---|---|---|---|

| VIF | 11 | 29 | 24 | 22 | 10 | 3 | 1 | – |

| robVIF | 4 | 13 | 8 | 23 | 17 | 12 | 10 | 13 |

| Variable | VIF | robVIF |

|---|---|---|

| genderfemale | 43 | 47 |

| ethnicityafam | 100 | 100 |

| ethnicityhispanic | 67 | 73 |

| score | 100 | 100 |

| fcollegeyes | 100 | 99 |

| mcollegeyes | 100 | 100 |

| homeyes | 79 | 94 |

| urbanyes | 3 | 38 |

| unemp | 24 | 54 |

| wage | 31 | 63 |

| distance | 100 | 98 |

| tuition | 26 | 56 |

| incomehigh | 100 | 98 |

| regionwest | 31 | 57 |

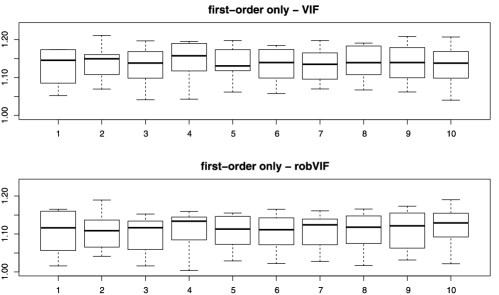

As the solution for VIF and robust VIF regression can depend on the order of the covariates, we ran each procedure several times with the covariates presented in random order to investigate the stability of the selected models in terms of model size and prediction performance. Table 5 shows the distribution of the size of the selected model over 100 analyses and Table 6 shows how often each variable was selected over these 100 analyses. As expected, there is considerable variability in the size of the model, and this both in the classical and robust approaches. We see, however, that the dominating features are nearly always present. Note also that unemp and wage are selected twice as often in the robust approach compared to the classical approach. In terms of prediction performance, we see in Figure 4 that the variability in the latter is considerably less, each of the 10 random analyses shown yielding more or less the same prediction performance despite the differences in terms of selected model size and features.

5 Crime data

In this section we present a shorter analysis of another data set to show how the classical approach can even fail to give a usable result. Also, by looking at a considerably larger data set we can show how robust VIF provides robust prediction where no other robust method is feasible.

We analyze recently made available crime data. These data are from the UCI Machine Learning Repository [Frank and Asuncion (2010)] and are available at http://archive.ics.uci.edu/ml/datasets/Communities+and+Crime. We seek to predict the per capita violent crimes rate using economic, demographic, community, and law enforcement related variables. After removing variables with missing data, we are left with observations on first-order covariates. If we include second-order interactions (removing those that are constant), we have . In both cases, we standardized the variables. VIF regression selects 33 and 1437 variables, in the respective scenarios, while robust VIF regression selects 20 variables in both cases. Classical VIF experiences problems with the larger data set, which contains outliers in a highly multicollinear setting, and chooses too many covariates. This shows how the guarantee of no overfitting only holds at the model, that is, without any outliers in the data. For these data, robust VIF regression provides the only viable option for policy makers, as the 1437 features returned by classical VIF regression do not provide useful information. As can be seen in Figure 5, robust VIF is clearly the best performer for both scenarios. VIF regression chooses too many features for many of the folds and this leads to catastrophic results out-of-sample.

6 Concluding remarks

In Lin, Foster and Ungar (2011) it was also shown that classical VIF regression equates or outperforms stepwise regression, Lasso, FoBa, an adaptive forward-backward greedy algorithm focusing on linear models [Zhang (2009)], and GPS, the generalized path-seeking algorithm of Friedman (2008). In this paper we present a very efficient robust VIF approach that clearly outperforms classical VIF in the case of contaminated data sets. This robust implementation comes with a very small cost in speed, computation time is less than doubled, and provides a much-needed robust model selection for large data sets.

Appendix: Algorithm robust VIF regression

The robust VIF regression procedure, based on a streamwise regression approach and -investing, can be summarized by the following algorithm:

Acknowledgments

The authors thank the Editor and three referees for comments that improved the presentation.

References

- Akaike (1973) {bincollection}[mr] \bauthor\bsnmAkaike, \bfnmH.\binitsH. (\byear1973). \btitleInformation theory and an extension of the maximum likelihood principle. In \bbooktitleSecond International Symposium on Information Theory (Tsahkadsor, 1971) (\beditor\binitsB. N. \bsnmPetrov and \beditor\binitsF. \bsnmCsaki, eds.) \bpages267–281. \bpublisherAkadémiai Kiadó, \blocationBudapest. \bidmr=0483125\bptokimsref\endbibitem

- Alqallaf et al. (2009) {barticle}[mr] \bauthor\bsnmAlqallaf, \bfnmFatemah\binitsF., \bauthor\bsnmVan Aelst, \bfnmStefan\binitsS., \bauthor\bsnmYohai, \bfnmVictor J.\binitsV. J. and \bauthor\bsnmZamar, \bfnmRuben H.\binitsR. H. (\byear2009). \btitlePropagation of outliers in multivariate data. \bjournalAnn. Statist. \bvolume37 \bpages311–331. \biddoi=10.1214/07-AOS588, issn=0090-5364, mr=2488353 \bptokimsref \endbibitem

- Candes and Tao (2007) {barticle}[mr] \bauthor\bsnmCandes, \bfnmEmmanuel\binitsE. and \bauthor\bsnmTao, \bfnmTerence\binitsT. (\byear2007). \btitleThe Dantzig selector: Statistical estimation when is much larger than . \bjournalAnn. Statist. \bvolume35 \bpages2313–2351. \biddoi=10.1214/009053606000001523, issn=0090-5364, mr=2382644 \bptokimsref \endbibitem

- Clark (2011) {barticle}[auto:STB—2012/09/04—06:46:48] \bauthor\bsnmClark, \bfnmD.\binitsD. (\byear2011). \btitleDo recessions keep students in school? The impact of youth unemployment on enrollment in post-compulsory education in England. \bjournalEconomica \bvolume78 \bpages523–545. \bptokimsref \endbibitem

- Dupuis and Victoria-Feser (2011) {barticle}[mr] \bauthor\bsnmDupuis, \bfnmDebbie J.\binitsD. J. and \bauthor\bsnmVictoria-Feser, \bfnmMaria-Pia\binitsM.-P. (\byear2011). \btitleFast robust model selection in large datasets. \bjournalJ. Amer. Statist. Assoc. \bvolume106 \bpages203–212. \biddoi=10.1198/jasa.2011.tm09650, issn=0162-1459, mr=2816714 \bptokimsref \endbibitem

- Efron (2004) {barticle}[mr] \bauthor\bsnmEfron, \bfnmBradley\binitsB. (\byear2004). \btitleThe estimation of prediction error: Covariance penalties and cross-validation. \bjournalJ. Amer. Statist. Assoc. \bvolume99 \bpages619–642. \biddoi=10.1198/016214504000000692, issn=0162-1459, mr=2090899 \bptnotecheck related\bptokimsref \endbibitem

- Efron et al. (2004) {barticle}[mr] \bauthor\bsnmEfron, \bfnmBradley\binitsB., \bauthor\bsnmHastie, \bfnmTrevor\binitsT., \bauthor\bsnmJohnstone, \bfnmIain\binitsI. and \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear2004). \btitleLeast angle regression. \bjournalAnn. Statist. \bvolume32 \bpages407–499. \biddoi=10.1214/009053604000000067, issn=0090-5364, mr=2060166 \bptokimsref \endbibitem

- Foster and Stine (2004) {barticle}[mr] \bauthor\bsnmFoster, \bfnmDean P.\binitsD. P. and \bauthor\bsnmStine, \bfnmRobert A.\binitsR. A. (\byear2004). \btitleVariable selection in data mining: Building a predictive model for bankruptcy. \bjournalJ. Amer. Statist. Assoc. \bvolume99 \bpages303–313. \biddoi=10.1198/016214504000000287, issn=0162-1459, mr=2109312 \bptokimsref \endbibitem

- Foster and Stine (2008) {barticle}[mr] \bauthor\bsnmFoster, \bfnmDean P.\binitsD. P. and \bauthor\bsnmStine, \bfnmRobert A.\binitsR. A. (\byear2008). \btitle-investing: A procedure for sequential control of expected false discoveries. \bjournalJ. R. Stat. Soc. Ser. B Stat. Methodol. \bvolume70 \bpages429–444. \biddoi=10.1111/j.1467-9868.2007.00643.x, issn=1369-7412, mr=2424761 \bptokimsref \endbibitem

- Frank and Asuncion (2010) {bmisc}[auto:STB—2012/09/04—06:46:48] \bauthor\bsnmFrank, \bfnmA.\binitsA. and \bauthor\bsnmAsuncion, \bfnmA.\binitsA. (\byear2010). \bhowpublishedUCI machine learning repository. Univ. California, School of Information and Computer Science, Irvine, CA. Available at http://archive.ics.uci.edu/ml. \bptokimsref \endbibitem

- Friedman (2008) {bmisc}[auto:STB—2012/09/04—06:46:48] \bauthor\bsnmFriedman, \bfnmJ. H.\binitsJ. H. (\byear2008). \bhowpublishedFast sparse regression and classification. Technical Report, Stanford Univ. \bptokimsref \endbibitem

- Friedman, Hastie and Tibshirani (2010) {barticle}[auto:STB—2012/09/04—06:46:48] \bauthor\bsnmFriedman, \bfnmJ. H.\binitsJ. H., \bauthor\bsnmHastie, \bfnmT.\binitsT. and \bauthor\bsnmTibshirani, \bfnmR.\binitsR. (\byear2010). \btitleRegularization paths for generalized linear models via coordinate descent. \bjournalJournal of Statistical Software \bvolume33 \bpages1–22. \bptokimsref \endbibitem

- Gneiting (2011) {barticle}[mr] \bauthor\bsnmGneiting, \bfnmTilmann\binitsT. (\byear2011). \btitleMaking and evaluating point forecasts. \bjournalJ. Amer. Statist. Assoc. \bvolume106 \bpages746–762. \biddoi=10.1198/jasa.2011.r10138, issn=0162-1459, mr=2847988 \bptokimsref \endbibitem

- Hampel (1968) {bmisc}[mr] \bauthor\bsnmHampel, \bfnmFrank Rudolf\binitsF. R. (\byear1968). \bhowpublishedContributions to the theory of robust estimation. Ph.D. thesis, Univ. California, Berkeley. \bidmr=2617979 \bptokimsref \endbibitem

- Hampel (1974) {barticle}[mr] \bauthor\bsnmHampel, \bfnmFrank R.\binitsF. R. (\byear1974). \btitleThe influence curve and its role in robust estimation. \bjournalJ. Amer. Statist. Assoc. \bvolume69 \bpages383–393. \bidissn=0162-1459, mr=0362657 \bptokimsref \endbibitem

- Heritier et al. (2009) {bbook}[mr] \bauthor\bsnmHeritier, \bfnmStephane\binitsS., \bauthor\bsnmCantoni, \bfnmEva\binitsE., \bauthor\bsnmCopt, \bfnmSamuel\binitsS. and \bauthor\bsnmVictoria-Feser, \bfnmMaria-Pia\binitsM.-P. (\byear2009). \btitleRobust Methods in Biostatistics. \bpublisherWiley, \blocationChichester. \biddoi=10.1002/9780470740538, mr=2604994 \bptokimsref \endbibitem

- Huber (1964) {barticle}[mr] \bauthor\bsnmHuber, \bfnmPeter J.\binitsP. J. (\byear1964). \btitleRobust estimation of a location parameter. \bjournalAnn. Math. Statist. \bvolume35 \bpages73–101. \bidissn=0003-4851, mr=0161415 \bptokimsref \endbibitem

- Huber (1967) {bincollection}[mr] \bauthor\bsnmHuber, \bfnmPeter J.\binitsP. J. (\byear1967). \btitleThe behavior of maximum likelihood estimates under nonstandard conditions. In \bbooktitleProc. Fifth Berkeley Sympos. Math. Statist. and Probability (Berkeley, Calif., 1965/66), Vol. I: Statistics \bpages221–233. \bpublisherUniv. California Press, \blocationBerkeley, CA. \bidmr=0216620 \bptokimsref \endbibitem

- Khan, Van Aelst and Zamar (2007) {barticle}[mr] \bauthor\bsnmKhan, \bfnmJafar A.\binitsJ. A., \bauthor\bsnmVan Aelst, \bfnmStefan\binitsS. and \bauthor\bsnmZamar, \bfnmRuben H.\binitsR. H. (\byear2007). \btitleRobust linear model selection based on least angle regression. \bjournalJ. Amer. Statist. Assoc. \bvolume102 \bpages1289–1299. \biddoi=10.1198/016214507000000950, issn=0162-1459, mr=2412550 \bptokimsref \endbibitem

- Kienzl, Alfonso and Melguizo (2007) {barticle}[auto:STB—2012/09/04—06:46:48] \bauthor\bsnmKienzl, \bfnmG. S.\binitsG. S., \bauthor\bsnmAlfonso, \bfnmM.\binitsM. and \bauthor\bsnmMelguizo, \bfnmT.\binitsT. (\byear2007). \btitleThe effect of local labor market conditions in the 1990s on the likelihood of community college students’ persistence and attainment. \bjournalResearch in Higher Education \bvolume48 \bpages751–774. \bptokimsref \endbibitem

- Lin, Foster and Ungar (2011) {barticle}[mr] \bauthor\bsnmLin, \bfnmDongyu\binitsD., \bauthor\bsnmFoster, \bfnmDean P.\binitsD. P. and \bauthor\bsnmUngar, \bfnmLyle H.\binitsL. H. (\byear2011). \btitleVIF regression: A fast regression algorithm for large data. \bjournalJ. Amer. Statist. Assoc. \bvolume106 \bpages232–247. \biddoi=10.1198/jasa.2011.tm10113, issn=0162-1459, mr=2816717 \bptokimsref \endbibitem

- Machado (1993) {barticle}[mr] \bauthor\bsnmMachado, \bfnmJosé A. F.\binitsJ. A. F. (\byear1993). \btitleRobust model selection and -estimation. \bjournalEconometric Theory \bvolume9 \bpages478–493. \biddoi=10.1017/S0266466600007775, issn=0266-4666, mr=1241985 \bptokimsref \endbibitem

- Mallows (1973) {barticle}[auto:STB—2012/09/04—06:46:48] \bauthor\bsnmMallows, \bfnmC. L.\binitsC. L. (\byear1973). \btitleSome comments on . \bjournalTechnometrics \bvolume15 \bpages661–675. \bptokimsref \endbibitem

- Marquardt (1970) {barticle}[auto:STB—2012/09/04—06:46:48] \bauthor\bsnmMarquardt, \bfnmD. W.\binitsD. W. (\byear1970). \btitleGeneralized inverses, ridge regression, biased linear estimation, and nonlinear estimation. \bjournalTechnometrics \bvolume12 \bpages591–612. \bptokimsref \endbibitem

- Pennington, McGinty and Williams (2002) {barticle}[auto:STB—2012/09/04—06:46:48] \bauthor\bsnmPennington, \bfnmK. L.\binitsK. L., \bauthor\bsnmMcGinty, \bfnmD.\binitsD. and \bauthor\bsnmWilliams, \bfnmM. R.\binitsM. R. (\byear2002). \btitleCommunity college enrollment as a function of economic indicators. \bjournalCommunity College Journal of Research and Practice \bvolume26 \bpages431–437. \bptokimsref \endbibitem

- Petrongolo and San Segundo (2002) {barticle}[auto:STB—2012/09/04—06:46:48] \bauthor\bsnmPetrongolo, \bfnmB.\binitsB. and \bauthor\bsnmSan Segundo, \bfnmM. J.\binitsM. J. (\byear2002). \btitleStaying-on at school at 16: The impact of labor market conditions in Spain. \bjournalEconomics of Education Review \bvolume21 \bpages353–365. \bptokimsref \endbibitem

- Renaud and Victoria-Feser (2010) {barticle}[mr] \bauthor\bsnmRenaud, \bfnmOlivier\binitsO. and \bauthor\bsnmVictoria-Feser, \bfnmMaria-Pia\binitsM.-P. (\byear2010). \btitleA robust coefficient of determination for regression. \bjournalJ. Statist. Plann. Inference \bvolume140 \bpages1852–1862. \biddoi=10.1016/j.jspi.2010.01.008, issn=0378-3758, mr=2606723 \bptokimsref \endbibitem

- Ronchetti (1982) {bmisc}[mr] \bauthor\bsnmRonchetti, \bfnmElvezio\binitsE. (\byear1982). \bhowpublishedRobust testing in linear models: The infinitesimal approach. Ph.D. thesis, ETH Zürich, Switzerland. \bidmr=2632390 \bptokimsref \endbibitem

- Ronchetti, Field and Blanchard (1997) {barticle}[mr] \bauthor\bsnmRonchetti, \bfnmElvezio\binitsE., \bauthor\bsnmField, \bfnmChristopher\binitsC. and \bauthor\bsnmBlanchard, \bfnmWade\binitsW. (\byear1997). \btitleRobust linear model selection by cross-validation. \bjournalJ. Amer. Statist. Assoc. \bvolume92 \bpages1017–1023. \biddoi=10.2307/2965566, issn=0162-1459, mr=1482132 \bptokimsref \endbibitem

- Ronchetti and Staudte (1994) {barticle}[mr] \bauthor\bsnmRonchetti, \bfnmElvezio\binitsE. and \bauthor\bsnmStaudte, \bfnmRobert G.\binitsR. G. (\byear1994). \btitleA robust version of Mallows’ . \bjournalJ. Amer. Statist. Assoc. \bvolume89 \bpages550–559. \bidissn=0162-1459, mr=1294082 \bptokimsref \endbibitem

- Rouse (1995) {barticle}[auto:STB—2012/09/04—06:46:48] \bauthor\bsnmRouse, \bfnmC. E.\binitsC. E. (\byear1995). \btitleDemocratization or diversion? The effect of community colleges on educational attainment. \bjournalJournal of Business and Economic Statistics \bvolume12 \bpages217–224. \bptokimsref \endbibitem

- Schwarz (1978) {barticle}[mr] \bauthor\bsnmSchwarz, \bfnmGideon\binitsG. (\byear1978). \btitleEstimating the dimension of a model. \bjournalAnn. Statist. \bvolume6 \bpages461–464. \bidissn=0090-5364, mr=0468014 \bptokimsref \endbibitem

- Tibshirani (1996) {barticle}[mr] \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear1996). \btitleRegression shrinkage and selection via the lasso. \bjournalJ. Roy. Statist. Soc. Ser. B \bvolume58 \bpages267–288. \bidissn=0035-9246, mr=1379242 \bptokimsref \endbibitem

- Wetterlind (1976) {bmisc}[auto:STB—2012/09/04—06:46:48] \bauthor\bsnmWetterlind, \bfnmP. J.\binitsP. J. (\byear1976). \bhowpublishedA multi-variable input model for the projection of higher education enrollments in Arizona. Ph.D. dissertation, Univ. Arizona, Tucson. \bptokimsref \endbibitem

- Zhang (2009) {barticle}[auto:STB—2012/09/04—06:46:48] \bauthor\bsnmZhang, \bfnmT.\binitsT. (\byear2009). \btitleAdaptive forward-backward greedy algorithm for sparse learning with linear models. \bjournalAdv. Neural Inf. Process. Syst. \bvolume21 \bpages1921–1928. \bptokimsref \endbibitem

- Zhou et al. (2006) {barticle}[mr] \bauthor\bsnmZhou, \bfnmJing\binitsJ., \bauthor\bsnmFoster, \bfnmDean P.\binitsD. P., \bauthor\bsnmStine, \bfnmRobert A.\binitsR. A. and \bauthor\bsnmUngar, \bfnmLyle H.\binitsL. H. (\byear2006). \btitleStreamwise feature selection. \bjournalJ. Mach. Learn. Res. \bvolume7 \bpages1861–1885. \bidissn=1532-4435, mr=2274426 \bptokimsref \endbibitem