Hierarchy of Frustrations as Supplementary Indices in Complex System Dynamics, Applied to the U.S. Intermarket

Abstract

A definition of frustration is expressed by transitivity of binary entanglement relation in considered complex system. Extending this definition into n-ary relation a hierarchy of frustrations’ notions is derived. As a complex system the U.S. Intermarket is chosen where the correlation coefficient of Intermarket indices’ sectors play the role of entanglement’s measure. In each hierarchy level the frustration and the transitivity are interpreted as values of an order’s measure for corresponding subsystem. The derived theory is applied to 1983-2012 data of the U.S. Intermarket.

pacs:

89.65.Gh, 89.75.-k, 71.45.GmIntroduction

Frustration represents situation where several optimization conditions compete with each other so that a system can not satisfy them simultaneously. Frustrated systems are characterized by the presence of metastable states among which the system ”hesitates” to choose. These metastable states often change their order of stability as a function of external parameters to exhibit phase transitions from one state to another (bib:KAWAMURA, ). In the 21st century, the research of frustrations has received a revived interest and new areas. Frustrations appear in different systems and different scales. In some systems such as modern magnetic materials and superconductors the frustrations are sources of their expected properties (bib:Cond.Matt, ) The frustrations are observed also in nature phenomena on the level of molecular scales (bib:bryng, ). The most recent discovers of frustrations have been done in Markets. In these systems the frustrations play crucial role in creation of realistic market’s models (bib:ahlg, ). In this paper we introduce our own interpretation of the frustration in a plaquette consisting of complex system’s components. Definition of frustration is expressed by transitivity of the correlation relation in considered system. Extending this definition into transitivity of the ary relation (bib:pickett, ),(bib:usan, ),(bib:cristea, ) we create a hierarchy of frustrations describing the whole complex system consisting of the components and its subsystems consisting of components, respectively. Notion of the transitivity and frustration are opposite magnitudes of an attribute characterizing bodies correlation in considered subsystems of the hierarchy, where . In order to perform investigations of this hierarchy with respect to the transitivity and frustration we need an appropriate complex system and empiric data for its members. The paper is organized in the following way. Section I approaches both system and data. In Section II using the notion of the transitivity we define frustration on different levels of hierarchy using notion of the transitivity. So far the transitive and frustrated subsystems are labelled by the two numbers +1 and -1, respectively. In order to make them more realistic we introduce in Section III extended measures of transitivity varying in the continuous domain . Section IV presents interpretation of transitivity as ordering relation. finally, in Section V using results of Sections II and III we analyse the 1983-2012 data of the U.S. Intermarket with respect to transitivity and frustration.

I 1983-2012 Empiric Data of the Considered U.S. Intermarket

An appropriate complex system should satisfy the following conditions:

1) The system and its subsystems produce data according to probability-based regime,

2) Produced data should be homogenous, reliable and complete,

3) The data produced by different subsystems should be time synchronous.

We would also like to have data which are easy to get and cheap. Following Murphy (bib:murp, ) we complete his U. S. Intermarket with Gold. In this way we choose system which satisfies our requirements. All considerations being done here base on the data supplied by (bib:NICK, ).

On basis of the 1987 Crash’s data of the U. S. markets, Murphy

derived the concept of the Intermarket Technical Analysis

involving four sectors.

Before the Murphy invention many people applied very simple technical analysis, such

as program trading and portfolio insurance. Such simple analysis could not predict the

forthcoming stock collapse.

The events of 1987 provide a textbook example of how the

intermarket scenario works and make a compelling argument as to why stock market

participants need to monitor the other three market sectors-the dollar, bonds, commodities and others. The fact that the equity collapse was global in scope, and not limited

to the U.S. markets, many would seem to argue against such a narrow view and finally supplied enough arguments for the global analysis of the considered markets. Therefore, Murphy has focused on the

commodity, bond, stock and currency markets, globally. Among the many conclusions, He presents many arguments that the U.S. dollar contributed to the weakness in equities.

Moreover, he concludes that among the four considered sectors the role of the U.S. dollar is probably the least precise and the one most difficult to pin down (bib:murp, ). However, all Murphy’s considerations are done on the basis of binary relations resulting from the binary correlations. In this paper we are going to extend his Intermarket Technical Analysis onto a hierarchy of relations including two, three, four,….. -ary relations, where is number of sectors constituting the considered complex system. In order to approach this idea we apply concept of frustrations to the U.S. Intermarket which is constituted by the following sectors: Stock, Bond, Commodity, Currency and Gold. Therefore, for the further considerations we select the following list of indexes:

SP500 - SPX,

Treasury Bonds Prices - USB,

Commodity Research Bureau Futures Price Index - CRB,

U. S. Dollar Index - USD and Gold Index - XAU.

A distribution of entanglement signs between spins play the crucial role in typical models of spin glass. In the case of Intermarket the entanglement between sectors

is described by the linear correlation coefficient. Therefore, the frustration in this system is determined by the distribution of correlation coefficient’s signs Illustrations of the all concepts derived here are presented on the example data 1987/07/01-1987/12/31. Whereas,

in order to investigate dynamics of the considered hierarchy of frustrations we analyse 1983 - 2012 statistical data (bib:NICK, ). For a test we applied some data from (bib:MURsite, ). The correlation coefficients are calculated for each half of the year. The example correlation coefficients are presented in TABLE 1.

| CRB | USB | SPX | USD | XAU | |

|---|---|---|---|---|---|

| CRB | 1 | -0,115 | -0,003 | -0,380 | 0,401 |

| USB | -0,144 | 1 | 0,544 | -0,271 | -0,666 |

| SPX | 0,376 | 0,617 | 1 | -0,124 | -0,182 |

| USD | 0,129 | -0,085 | 0,456 | 1 | -0,195 |

| XAU | 0,750 | -0,081 | 0,235 | -0,351 | 1 |

II Frustrations in correlated subsystems

Let us consider the following Intermarket’s sectors represented by their indexes:

| (1) |

and define the following binary relation:

| (2) |

where is set of two labels corresponding to signs of correlation coefficients of the pairs belonging to .

Let us determine relation on . For the binary relation we use the following notation:

| (3) |

Let are determined by the signs of Pearson’s correlation coefficients

| (4) |

where and

| (5) |

Therefore the considered relation becomes to the following function (for the period 1987/07/01-1987/12/31):

The remaining mappings of this function are presented in Fig. 1 (for the period 1987/07/01-1987/12/31).

The values of the correlation coefficients concerning the selected sectors are presented in TABLE 1. Let us investigate the transitivity of . Therefore we have to determine superposition of the two relations like the following example: . Let are different members of . According to least squares estimates (bib:Brandt, ) we can write down the following linear approximations:

| (7) | |||

| (8) |

Let us create a superposition of (7) and (8):

| (9) |

where

| (10) | |||

| (11) |

According to the least squares estimates , therefore (4) takes the following form:

| (12) |

Combining (4)-(12) we derive the following superposition’s rule for :

| (13) |

Therefore we formulate and prove the following theorem:

Theorem 1

Let

| (14) |

then is transitive in if

| (15) |

Proof

By the definition is transitive if .

On the basis of this definition and (13) as well as (14) we derive that is transitive if:

| (16) |

Taking into account above theorem we obtain:

| (17) | |||

| (18) | |||

The remaining tests of transitivity are presented in Fig. 2 and Fig. 3.

Let us call the following subset a plaquette, let be set of the all plaquettes created in .

We can see that the transitivity decomposes

into two components: ,

where the relation

is transitive and it is not transitive ,

(N, F - mean no frustration and frustration, respectively).

Definition

Lacking of ’s transitivity in we call frustration of with respect to .

II.1 Hierarchy of frustrations in correlated subsystems

Let us consider the following Intermarket’s sectors represented by their indexes: and define the following hierarchy of relations:

| (19) |

where is set of two labels corresponding to signs of correlation coefficients of the pairs belonging to .

| (20) |

where is set of two labels: - frustration, - no frustration with respect to transitivity of .

| (21) |

where is set of two labels: - frustration, - no frustration with respect to transitivity of .

| (22) |

where is set of two labels: - frustration, - no frustration with respect to transitivity of .

II.1.1 The ternary relation

Now we are ready to define .

Definition Let us create all possible points ,

where and

and define in the following way:

if frustration with respect to transitivity in

occurs in then the point is mapped to

and else

is mapped to and .

Finally

.

The subsets corresponding to and :

| (23) | |||

| (24) |

are presented in Fig. 4 and Fig. 5, respectively. It occurs the following relation between and :

| (25) |

Therefore, similarly to (12) and according to (25) we determine the values of in the following way:

| (26) | |||

In order to extent notion of frustration into

we have to define the transitivity with respect to this relation.

Definition

Let

| (27) |

If

| (28) | |||

then is transitive in (27).

Theorem 2

Let be transitive in

:

| (29) |

then

| (30) |

Proof

By the definition is transitive if .

Taking into account (27) and as well as (26) we derive that is transitive if:

| (31) | |||

Multiplying (31) by we get the thesis.

II.1.2 The 4-ary and 5-ary relations

Extending results of II.1.1 into the 4-ary and 5-ary relations (21) and (22), respectively we define the transitivity and frustration for the 4 and 5 point complexes which are presented in Figure 6 and Figure 7, respectively. For the considered system there are five 4-ary relations and one 5-ary relation. Extending (26) on we derive the following relation:

| (32) |

For presentation of transitivity and frustration in we calculate for the both selected relations (Figure 6): . Extending (32) on we derive the following value of the transitivity for the whole considered system: . Therefore, is not transitive in , whereas it is transitive in as well. Since is transitive in whereas it is not transitive in we derive the following conclusion: in the period 1987/07/01-1987/12/31 has been played an ordering role in the considered Intermarket. Thus, e.g. relating the transitivity’s measures of and we investigate roles of the all Intermarket’s sectors during 1983-2012 (Section V).

II.1.3 The n-ary relations

Derivation of and their properties suggests the following algorithm for creation of the and investigation of the properties:

1. Write down the relation between and . Let ,

in the following form:

| (33) |

where

2. Express by , where :

| (34) |

3. Define transitivity of .

Let , where and

If the following relation occurs:

| (35) |

then is transitive, else the subsystem is frustrated with respect to

.

4. Derive recurrent formula for :

| (36) |

5. Derive the superposition rules for . Writing down the complete system of (36) and performing elimination of the all correlation coefficients we derive:

| (37) |

III Measures of transitivites

For each relation belonging to the hierarchy the values of correspond to transitivity or frustration, respectively. However, they do not describe ”how much” considered system is transitive or how much frustrated. In order to derive such a measure we come back to the definition of . Let us note that , where the first factor informs whether and are correlated or anticorrelated, whereas the second one describes ”how much”. Therefore, we renamed into as an accepted measure of . Continuing this way and taking into account (26) we derive the measures of and :

| (38) |

Therefore,

| (39) | |||

| (40) |

In general case similarly to (38)-(39) we derive simplified formula for transitivity measure of the -s member of hierarchy:

| (41) |

IV Transitivity as ordering relation’s property

Proposition

Let us consider two examples of plaquettes, one by one from and , respectively (Fig. 8).

We argue for the following hypothesis: Transitivity of is responsible for stimulating of sectors to common direction evolution. However, some sectors interferes with this process leading to the frustration and in this way they preserve the sectors’ independence.There are two arguments for such interpretation of the frustration (or its contradiction - transitivity).

The first one is direct. Let us take into account the case of Fig. 8. Let us estimate influence of on . There are two ways of entanglement: and . Both of them push into opposite direction with respect to the evolution’s direction of . It is important that both ways push into the same direction (by the direction of X’s evolution we mean its increase or decrease). Therefore, the resulting effect from the both ways is at least stronger then the strongest single entanglement in this plaquette. This result is invariant with respect to a choice of starting point in the considered plaquette. Now, let us take into account the case of Fig. 8, and estimate influence of on . There are two ways of entanglement acting on : and . However, now they work in opposite directions. Therefore, the resulting effect is at least weaker then the strongest single entanglement in this plaquette. Also this result is invariant with respect to a choice of the starting point. Summarizing, we have shown argument that in a plaquette of the three different sectors without (with) frustration the influences of sectors between each other become stronger (weaker). Summarizing, we distinguish an ordering entanglement in , whereas in such an ordering does not exists.

The second argument is formal and touches the basis of the mathematics.

Let be

constrained to , respectively.

Due to symmetry, reflexibility and transitivity of

this subrelation is an equivalence relation.

Since for the considered Intermarket the sum of the all plaquettes belonging to is equal to :

| (42) |

the structure is a preorder (bib:foldes, ). Therefore, the transitivity is an inductor of at least a weak kind of order in the system.

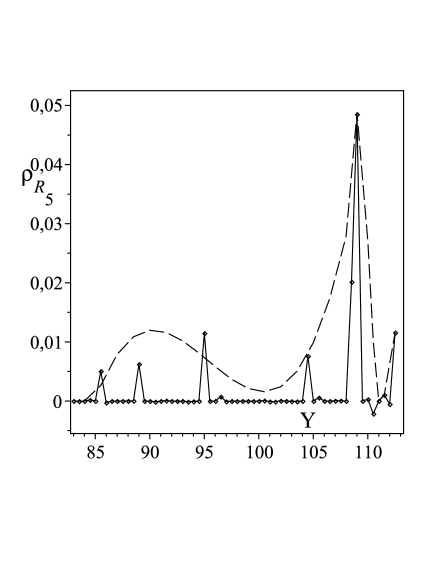

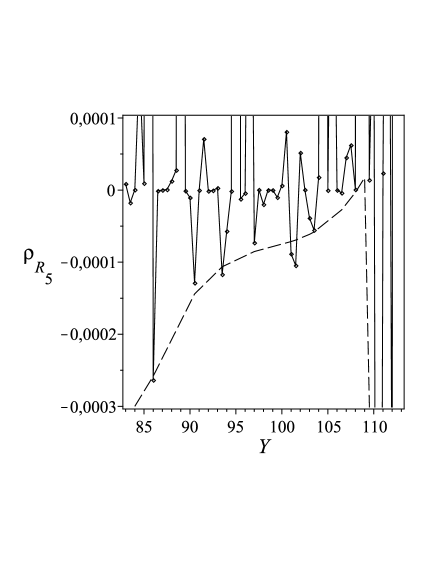

V Frustrations Hierarchy Analysis of the U.S. Intermarket’s

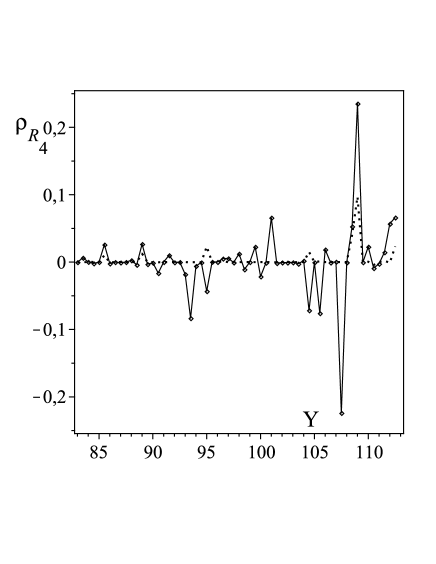

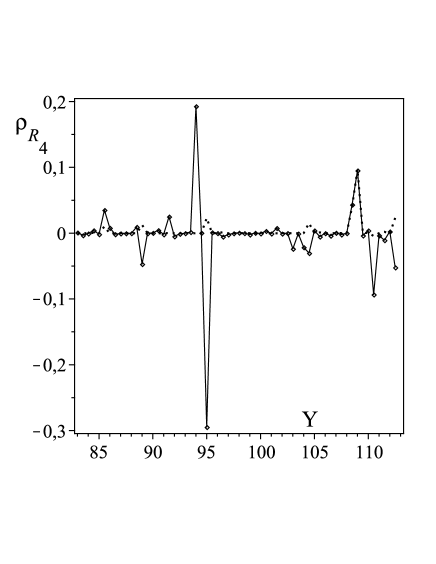

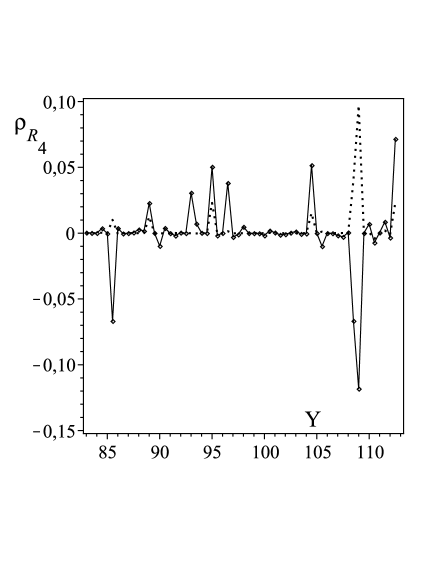

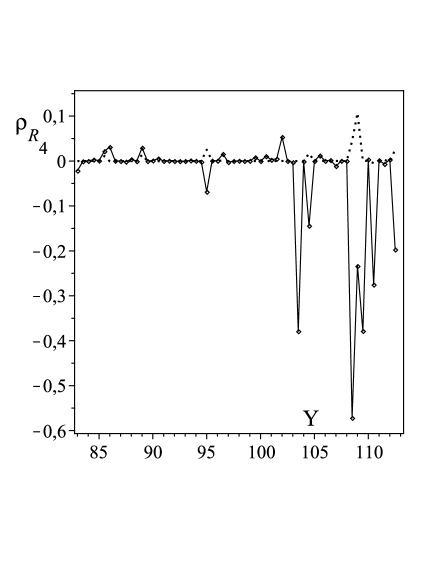

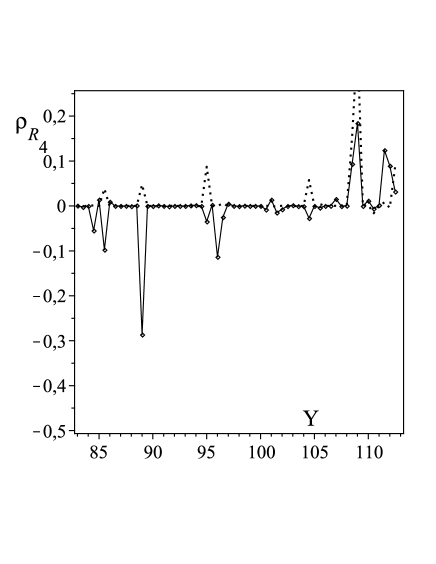

Applying (41 ) to the Intermarket’s data we have calculated the total Intermarket’s transitivity measure (see Fig.9, Fig.10) and the five measures corresponding to Subintermarkets obtained by reduction of the considered Intermarket with respect to each its element \ (see Fig.11- Fig.15).

V.1 Discussion of results for measure

The values of are presented in the two scales. The scales of Fig.9 and Fig.10 are appropriate for analysis of positive and negative , respectively. Combining both figures we see that undergoes variations like the U.S. Business Cycles which can be described by the Brownian Motion of a Harmonic Oscillator (bib:chen, )-(bib:Zarn, ). The oscillation’s amplitude for the positive direction of is two orders greater in average then the negative one. The envelopes of positive and negative values changes according to trends presented by dashed lines. Let us remind that corresponds to transitivity, whereas corresponds to frustration. From 1983 until 2009 the positive amplitude increases and the negative one decreases becoming positive. It means that the transitivity approaches a high value and the frustration disappears. Then from the second half of 2009 exhibits strong fluctuations. One can see from Fig.10 that the considered system has lost stability when the trend of frustrations got value equal to zero. On the basis of these observations we may draw the conclusion that frustration is necessary for the system’s stability. Due to the strong oscillations which have appeared after the revealed boom there is a chance to get negative values for the frustration’s trend and to recover the system’s stability.

The nearest future will show how the frustration analysis applied to an Intermarket is efficient for the predictions of the economic stability in long time horizon. Now (January 2013) performs large amplitude oscillations into both directions ( and ). The most probable event is that the envelope of frustrations will approach zero by forthcoming decades and different events of U.S. Economy will generate picks of transitivity. Unlikely but a worse one would be a situation when will oscillate above axis approaching zero value asymptotically for long time.

V.2 Discussion of results for measures

is the highest measure of transitivity in the five elements system. This is a top of the considered hierarchy .

There are five measures of the describing transitivity in a subset of four Intermarket’s entities. Let us assume that by removing selected entity from the frustration analysis we receive an approximation knowledge about the influence of this Intermarket’s member on the dynamics of the whole system. All the five measures are presented in Fig.11-Fig.15. Comparing of the selected Subintermarket with we will try to answer the question what could be the influence of the removed entity on the Intermarket’s stability.

There are seven possible reactions of picks for removing a sector from the Intermarket. All of them are listed in TABELE 2 and their interpretations are indicated. According to this Tabele we present the following discussion.

-

•

\. In the period 1983-2008 Gold has played crucial role in Intermarket’s stability. By removing Gold from the Intermarket the high picks of transitivity have change into deep frustrations. Therefore the Gold was responsible for blocking of the frustrations. However, in the period 2009-2012 this Sector has loss this influence.

-

•

\. In the period 1983-1994 Treasury Bonds Prices’ influence was marginal. Whereas, in the period 1995-2012 has changed transitivities into frustrations. Therefore, probably this sector among others was responsible for the frustrations’ decay.

-

•

\. The analysis of shows that is the most complicated Intermarket’s sector. The pick of corresponding to 1985-1986 period has been changed from frustration to transitivity. Therefore the U. S. Dollar was a creator of frustrations in this period. The pick corresponding to 1989 was invariant with respect to removing of USD from the Intermarket. Therefore for this period USD was marginal. The two next picks of have appeared at 1995 and 2009. Both of them were also invariant, however the pick from 1995 had got two sattelite picks at 1994 and 1996.5. (July of 1996). The pick at 2009 has changed from frustration into transversity whereas the last one at 2012 reminded to be invariant. Summarizing, the invariant picks are not correlated with USD, however those which have been changed from frustration into transfersity corresponded to frustrations’ creator of .

-

•

\. Influence of Commodity on the Intermarket was a little different from the influence of another sectors. In 1985-1986 the pick of was invariant. The pick at 1989 has changed the sign and became a measure of frustration. Therefore, in this year Commodity has protected Intermarket against frustration. A new pick of transitivity has appeared at 1991.5. In the period 1993.5- 1995.5 a new quality has occur. By comparing Fig. 14 and Fig. fig:rhoR5g a large increase of the pick at 1995 and its little satellite at 1996.5 into gigantic measure’s values of transitivity and frustration have been observed. This can be interpreted as an active role of Commodity in creation of the frustrations in the considered period. Next, in 2004-2005 the pair of transitivities’ picks has been collapsed into fuzzy frustrations.Therefore, the Commodity has stopped the creation of frustrations . Finally, the events of the period 2008-2011 have shown transition of the gigantic transitivities’ into picks of transitivity and frustration. Therefore, from 1993.5 the Commodity has played very important role in the Intermarket’s stabilization.

-

•

\. Two picks of transitivity at 1985 and 1989 have been conserved, whereas the pick of 1995 and its little satellite at 1996 have changed for frustration, moreover, the intensity of the satellite increased. Since 1997 it has started the oscillation of around zero characterized by increasing amplitude which was suddenly broken at 2001.5. There were not any oscillations of the measure corresponding to that ones. In the four previous cases the events after 2008 were most interesting. In the case of \ the gigantic picks of transversity and frustration has been reversed in time (frustration and transversity). The five last points in Fig.15 suggest that the black scenario for developing of without frustrations would be possible (black scenario). Note that in the period Stock and Intermarket were strongly anticorrelated, whereas in this relation become to be a strong correlation. Additionaly, this event checks the stabilizing role of frustrations.

V.3 The finale remark

The considered Intermarket is a subsystem immersed in the U.S. National Economy. Therefore, the picks and trends of the transitivity as well as the frustration measures are related to events of this global system. Analysis of the results presented here will be related to U.S. Events (bib:USE, ) and published in forthcoming monograph (bib:SokMor, ).

| Reaction | Invariant | ||||||

|---|---|---|---|---|---|---|---|

| Interpretation for sector’s | No active | Frustration’s | Transisivity’s | Frustartion’s | Transitivity’s | Frustration’s | Transitivity’s |

| activity | generator | generator | generator | generator | annihilator | annihilator |

References

- (1) Novel States of Matter Induced by Frustration, Editor: Hikaru Kawamura, J. Phys. Soc. Jpn. (Special Topics), Vol. 79 (2010).

- (2) Proceedings of the International Conference on Highly Frustrated Magnetism, Osaka, Japan,15-19 August 2006, Eds. Hiroi Z. & Tsunetsugu H., Journal of Physics: Cond. Matt.,Vol. 19. No. 14 (2007).

- (3) Bryngleson JD, Wolynes PG, Proc Nat Acad Sci USA Vol. 84 (1987):7524-7528.

- (4) Ahlgren PTH, Jensen MH, Simonsen I, Donangelo R, Sneppen K, Frustration driven stock market dynamics: Leverage effect and assymetry, (2007) Physica A, Vol. 383 :1-4.

- (5) Pickett H.E.,A Note on Generalized Equivalence Relation, Amer. Math. Manthly, Vol. 73, No. 8, (1966) 860-861.

- (6) Us̆an J., S̆es̆elja, Transitive n-Ary Relations and Characterizations of Generalized Equivalences, Rev. of Res. Faculty of Science-Univ. of Novi Sad, Vol. 11 (1981) 231-245.

- (7) Cristea I., Several Aspects on the Hypergroups Associated with n-Ary Relations, An. St. Univ. Ovidius Constanta, Vol. 17(3)(2009) 99-110.

- (8) The Statistical Data purchased from SHARELYNX GOLD, nick@sharelynx.com, January 2010. and January 2012.

- (9) Murphy J. J., Intermarket Technical Analysis: Trading Strategies For The Global Stock, Bond, Commodity And Currency Markets, John Wiley Sons, Inc. 1991

-

(10)

http://stockcharts.com/charts/performance/

perf.html?[IM]. - (11) Brandt S., Data Analysis. Statistical and Computational Methods for Scientists and Engineers, Springer Verlag, New York 1999, Ch. 9.

- (12) Foldes S., Fundamental Structures of Algebra Discrete Mathematics, John Wiley Sons, Inc. 1994.

- (13) Chen, P. ”Trends, Shocks, Persistent Cycles in Evolving Economy: Business Cycle Measurement in Time-Frequency Representation, in W. A. Barnett, A. P. Kirman, and M. Salmon Eds. Nonlinear Dynamics and Economics, Chapter 13, pp. 307-331, Cambridge University Press (1996a).

- (14) Goodwin, R. M. ”The Nonlinear Accelerator and the Persistence of Business Cycles,” Econometrica, 19, 1-17 (1951).

- (15) Hayek, F. A. Monetary Theory and the Trade Cycle, A.M. Kelley Publishers, New York (1933, 1966).

- (16) Hodrick, R. J., and E. C. Prescott. ”Post-War US. Business Cycles: An Empirical Investigation, ” Discussion Paper No. 451, Carnegie-Mellon University (1981).

- (17) Zarnowitz, V. Business Cycles, Theory, History, Indicators, and Forecasting, pp.196-198, University of Chicago Press, Chicago (1992).

-

(18)

http://en.wikipedia.org/wiki/1983_in_the_

United_States#Events, and for all the next relevant years. - (19) Sokalski K, Moroz E., Frustration Analysis of the U.S. Intermarkets, (2014) in preparation.