(Date: . We are grateful to Andrew Abrahams, Jose Blanchet, Terry Lyons, and Marek Musiela for insightful comments. We also thank participants of seminars at Columbia University, University of Michigan, Rutgers University, the Oxford-Man Institute, the University of Southern California, the Office of Financial Research, the SIAM Conference on Financial Mathematics and Engineering, and the INFORMS Annual Meeting for comments.)

1. Introduction

Reduced-form point process models of correlated firm-by-firm default timing are widely used to measure the credit risk in portfolios of defaultable assets such as loans and corporate bonds. In these models, defaults arrive at intensities governed by a given system of stochastic differential equations. Computing the distribution of the loss from default in these models is often challenging. Transform methods are tractable only in special cases, for example, if defaults are assumed to be conditionally independent. Monte Carlo simulation methods have a much wider scope but can be slow for the large portfolios and longer time horizons common in industry practice. A major US bank might easily have wholesale loans, to mid-market and commercial loans, and derivatives trades with to different legal entities. Simulation of such large pools is extremely burdensome.

This paper develops a conditionally Gaussian approximation to the distribution of the loss from default in large pools. The approximation applies to a broad class of empirically motivated reduced-form models in which a name defaults at an intensity that is influenced by an idiosyncratic risk factor process, a systematic risk factor process common to all names in the pool, and the portfolio loss. It is based on an analysis of the fluctuation of the loss around its large portfolio limit, i.e., a central limit theorem (CLT). More precisely, we show that the signed-measure-valued process describing the fluctuation of the loss around its law of large numbers (LLN) limit weakly converges to a unique distribution-valued process in a certain weighted Sobolev space. The limiting fluctuation process satisfies a stochastic evolution equation driven by the Brownian motion governing the systematic risk and a distribution-valued martingale that is centered Gaussian given . The fluctuation limit, and thus the resulting approximation to the loss distribution, is Gaussian only in the special case that the names in the pool are not sensitive to .

In the general case, the approximation is conditionally Gaussian.

The weak convergence result proven in this paper extends the LLNs for the portfolio loss established in our earlier work \citeasnounGieseckeSpiliopoulosSowers2011 and \citeasnounGieseckeSpiliopoulosSowersSirigano2012. The fluctuation analysis performed here involves challenging topological issues that do not arise in the analysis of the LLN. Firstly, the fluctuations process takes values in the space of signed measures. This space is not well suited for the study of convergence in distribution; the weak topology, which is the natural topology to consider here, is in general not metrizable (see, for example, \citeasnounBarrioDeheuvelsGeer2007). We address this issue by analyzing the convergence of the fluctuations as a process taking values in the dual of a suitable Sobolev space of test functions. Weights are introduced in order to control the norm of the fluctuations and establish tightness. Related ideas appear in \citeasnounMetivier1985, \citeasnounFernandezMeleard, \citeasnounKurtzXiong and other articles, but for other systems and under different assumptions. Additional issues are the growth and degeneracies of the coefficients of our stochastic system, which make it difficult to identify the appropriate weights for the Sobolev space in which the convergence is established and uniqueness of the limiting fluctuation process is proved. \citeasnounPurtukhia1984, \citeasnounGyongiKrylov1992, \citeasnounKryLot1998, \citeasnounLot2001, \citeasnounKim2009, and others face similar issues in settings that are different from ours. The approach we pursue is inspired by the class of weights that were introduced by \citeasnounPurtukhia1984 and further analyzed by \citeasnounGyongiKrylov1992.

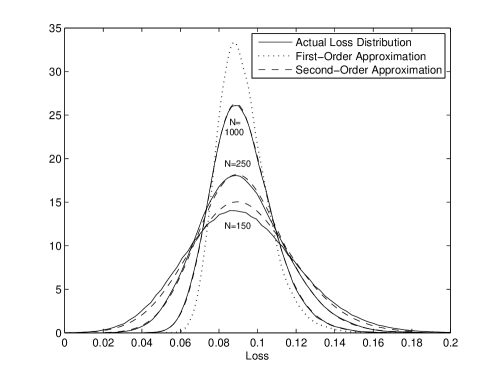

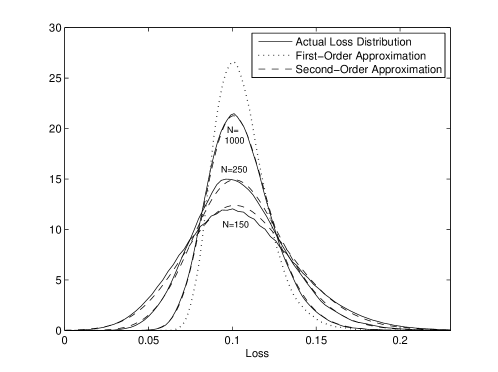

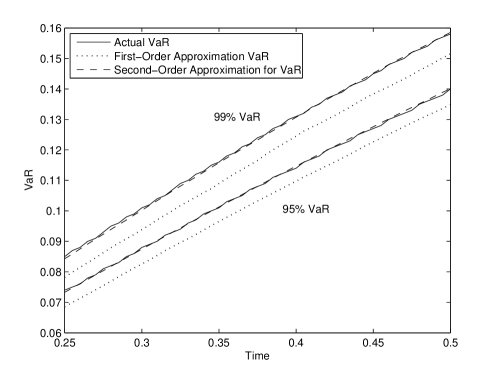

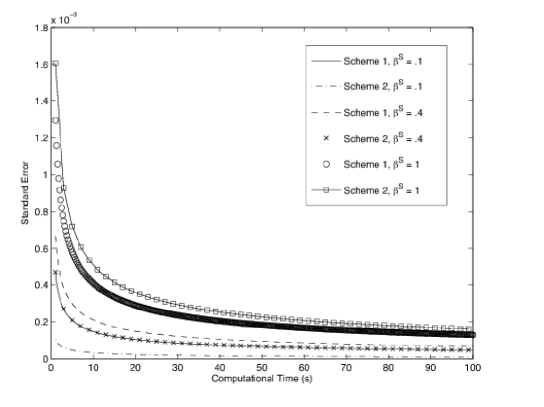

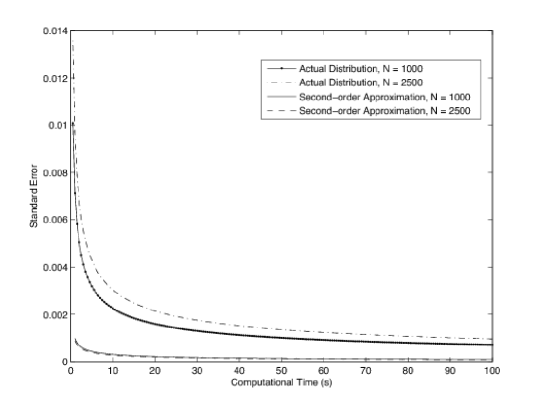

The fluctuation analysis leads to a second-order approximation to the loss distribution that can be significantly more accurate than an approximation obtained from just the LLN. Our numerical results, which are based on a method of moments for solving the stochastic evolution equation governing the fluctuation limit, confirm that the second-order approximation is much more accurate. The second-order approximation is even accurate for relatively small portfolios in the order of hundreds of names or when the influence of the systematic risk process X is relatively low. The second-order approximation also improves the accuracy in the tails. The effort of computing the second-order approximation exceeds that of computing the first-order approximation, but is still much lower than directly simulating the pool.

Prior research has established various weak convergence results for interacting particle systems represented by reduced-form models of correlated default timing. \citeasnoundaipra-etal and \citeasnoundaipra-tolotti study mean-field models in which an intensity is a function of the portfolio loss. In a model with local interaction, \citeasnoungiesecke-weber take the intensity of a name as a function of the state of the names in a specified neighborhood of that name. In these formulations, the impact of a default on the dynamics of the surviving constituent names, a contagion effect, is permanent. In our mean-field model, an intensity depends on the path of the portfolio loss. Therefore, the impact of a default may be transient and fade away with time. There is a recovery effect. Moreover, the system which we analyze includes firm-specific sources of default risk and addresses an additional source of default clustering, namely the exposure of a name to a systematic risk factor process. This exposure generates a random limiting behavior for the LLN and leads to a fluctuation limit which is only conditionally Gaussian.

There are several other related articles. \citeasnounCMZ prove a LLN for a mean-field system with permanent default impact, taking an intensity as a function of an idiosyncratic risk factor, a systematic risk factor, and the portfolio loss rate. The risk factors follow diffusion processes whose coefficients may depend on the portfolio loss. \citeasnounhambly establish a LLN for a system in which defaults occur at first hitting times of correlated diffusion processes. Conditional on a correlating systematic risk factor governed by a Brownian motion, defaults occur independently of one another.

\citeasnounPapanicolaouSystemicRisk analyze large deviations in a system of diffusion processes that interact through their empirical mean and have a stabilizing force acting on each of them. \citeasnounfouque-ichiba study defaults and stability in an interacting diffusion model of inter-bank lending.

The rest of this paper is organized as follows. Section 2 describes the class of reduced-form models of correlated default timing which we analyze.

Section 3 reviews the law of large numbers proved by \citeasnounGieseckeSpiliopoulosSowersSirigano2012 for the portfolio loss in these models. Section 4 states our main weak convergence result for the fluctuation process, essentially a central limit theorem for the loss. Section 5 provides a numerical method for solving the stochastic evolution equation governing the fluctuation limit and provides numerical results. Sections 6-9 are devoted to the proof of the main result. There is an appendix.

2. Model and Assumptions

We analyze a class of reduced-form point process models of correlated default timing in a pool of firms (“names”). Models of this type have been studied by \citeasnounCMZ, \citeasnoundaipra-etal, \citeasnoundaipra-tolotti, \citeasnounGieseckeSpiliopoulosSowers2011, \citeasnounGieseckeSpiliopoulosSowersSirigano2012, and others. In these models, a default is governed by the first jump of a point process. The point process intensities follow a system of SDEs.

Fix a probability space . Let be a countable collection of independent standard Brownian motions. Let be an i.i.d. collection of standard exponential random variables which are independent of the ’s. Finally, let be a standard Brownian motion which is independent of the ’s and ’s. Each will represent a source of risk which is idiosyncratic to a specific name. Each will represent a normalized default time for a specific name. The process will drive a systematic risk factor process to which all names are exposed. Define and , where contains the -null sets. Lastly, we will denote by the conditional law given , where may represent , for example.

Fix , and consider the following system:

| (1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Here, is the indicator function. The initial value of is fixed. The are parameters.

The process is the fraction of names in default, which we loosely call the “loss rate” or simply the “loss.” The process represents the intensity, or conditional default rate, of the -th name in the pool. More precisely, is the density of the Doob-Meyer compensator to the default indicator , where . That is, a martingale is given by

The results in Section 3 of \citeasnounGieseckeSpiliopoulosSowers2011 imply that the system (1) has a unique solution such that for every , and . Thus, the model is well-posed.

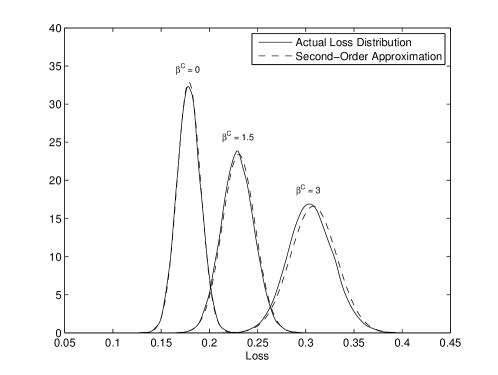

The default timing model (1) addresses several channels of default clustering. An intensity is influenced by an idiosyncratic source of risk represented by a Brownian motion , and a source of systematic risk common to all firms–the diffusion process . Movements in cause correlated changes in firms’ intensities and thus provide a channel for default clustering emphasized by \citeasnounddk for corporate defaults in the U.S. The sensitivity of to changes in is measured by the parameter . The second channel for default clustering is modeled through the feedback (“contagion”) term . A default causes a jump of size in the intensity , where . Due to the mean-reversion of , the impact of a default fades away with time, exponentially with rate . \citeasnounazizpour-giesecke-schwenkler have found self-exciting effects of this type to be an important channel for the clustering of defaults in the U.S., over and above any clustering caused by the exposure of firms to systematic risk factors.

Figure LABEL:fig:paths illustrates the behavior of the system when the systematic risk follows an OU process. It shows sample paths of the processes and for a pool with names. Between defaults, the intensities of the surviving names evolve as correlated diffusion processes, where the co-movement is driven by the systematic risk . At a default, the process associated with the defaulting name drops to 0. At the same time, the processes associated with the surviving names jump by , and the loss increases by .

We allow for a heterogeneous pool; the intensity dynamics of each name can be different. We capture these different dynamics by defining the parameter “types”

|

|

|

The ’s take values in parameter space . For each , define

|

|

|

for all and . Define . The vector represents a random environment that addresses the heterogeneity of the system.

Condition 2.1.

We assume that the are i.i.d. random variables with

common law and that has compact support in . In particular, and to avoid inessential complications, we assume that all elements of the random vector are bounded in absolute values by some , for all . Moreover, we assume that is independent of and .

This formulation of heterogeneity generalizes that of \citeasnounGieseckeSpiliopoulosSowersSirigano2012. They assume that and exist (in and , respectively). Their formulation is a special case of the one proposed here, where the law .

Condition 2.2.

We assume that for all .

3. Law of large numbers

Except for special cases of little practical interest, the distribution of the portfolio loss in the system (1) is difficult to compute. We are interested in an approximation to this distribution for the large portfolios common in practice, i.e., for the case that is large. \citeasnounGieseckeSpiliopoulosSowersSirigano2012 prove a law of large numbers (LLN) for the loss in the system (1) and use it for developing a first-order approximation. We first review this result and then extend it in Section 4 by analyzing the fluctuations of the loss around its LLN limit. The fluctuation analysis will allow us to construct a more accurate second-order approximation.

To outline the LLN, define

|

|

|

this is the empirical distribution of the type and intensity for those names which are still “alive.”

We note that is a sub-probability measure. Since

| (2) |

|

|

|

it suffices to study the limiting behavior of the measure-valued process for some fixed horizon .

Let be the collection of sub-probability measures (i.e., defective probability measures) on ; i.e., consists

of those Borel measures on such that .

Topologizing in the usual way (by projecting onto the one-point compactification of ; see Chapter 9.5 of \citeasnounMR90g:00004) we obtain that is a Polish space.

Thus, is an element of where is the Skorokhod space (i.e., is the set of RCLL processes on taking values in ).

Further, for where

and (the space of twice continuously differentiable, bounded functions), define, similarly to [GieseckeSpiliopoulosSowers2011], the operators

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Also define

|

|

|

The generator corresponds to the diffusive part of the

intensity with killing rate , and is the

macroscopic effect of contagion on the surviving intensities at any

given time. The operators and are related

to the exogenous systematic risk .

For a measure , we also specify the inner product

|

|

|

The law of large numbers of \citeasnounGieseckeSpiliopoulosSowersSirigano2012 states that weakly converges to in . To rigorously formulate the result we need to use the weak form (see also Lemma 8.3). In particular, for all , the evolution of

is governed by the measure evolution equation

| (3) |

|

|

|

The LLN suggests an approximation to the distribution of the loss in large pools by the large pool limit:

| (4) |

|

|

|

|

4. Main Result: Fluctuations Theorem

In order to improve the first-order approximation (4), we analyze the fluctuations of around its large pool limit .

As is indicated by the proof of Lemmas 8.4 and 8.5 (see also \citeasnounGieseckeSpiliopoulosSowersSirigano2012), for an appropriate metric, the sequence is stochastically bounded.

Hence, it is reasonable to define the scaled fluctuation process by

| (5) |

|

|

|

In Theorem 4.1 below we will show that the signed-measure-valued process weakly converges to a fluctuation limit process in an appropriate space.

The analysis of the limiting behavior of the fluctuation process (5) involves issues that do not occur in the treatment of the LLN.

In particular, even though the fluctuation process is a signed-measure-valued process, its limit process is distribution-valued in an appropriate space.

The space of signed measures endowed with the weak topology is not metrizable. The difficulty is then to identify a rich enough space, where tightness and uniqueness can be proven. It turns out that

we have to consider the convergence in weighted Sobolev spaces. Here, several technical challenges arise. These are mainly due to

the growth and degeneracies of the coefficients of the system (1), which make it difficult to identify the correct weights. The spaces that we consider are Hilbert spaces. For

the sake of clarity of presentation the appropriate Hilbert spaces will be defined in detail in Section 7. For the moment, we mention that the space in question is denoted by

, with and the appropriate weight functions, and will be its dual. A precise definition is given in Section 7.

We need to introduce several additional operators to state our weak convergence result. For and , we define

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The main result of this paper is the following theorem.

Theorem 4.1.

Let . For large enough (in particular for ) and for weight functions such that Condition 7.1 holds, the sequence is relatively compact in . For any subsequence of this sequence,

there exists a subsubsequence that converges in distribution with limit . Any accumulation point satisfies the stochastic evolution equation

| (6) |

|

|

|

for any , where is a distribution-valued martingale with predictable variation process

|

|

|

Moreover, conditional on the -algebra , is centered Gaussian with covariance function, for ,

given by

|

|

|

|

| (7) |

|

|

|

|

Finally, the limiting stochastic evolution equation (6) has a unique solution in and thus the limit accumulation point is unique.

The proof of Theorem 4.1 is developed in Sections 6 through 9. In Section 6, we identify the limiting equation and prove the convergence theorem based on the tightness and uniqueness results of Sections 8 and Section 9. In Section

7, we discuss the Sobolev spaces we are using. In Section 8,

we prove that the family is relatively compact in , see Lemma 8.8. In Section 9, we prove uniqueness of (6) in , see Theorem 9.7.

The fluctuation analysis leads to a second-order approximation to the distribution of the portfolio loss in large pools. The weak convergence established in Theorem 4.1 implies that

|

|

|

for large . Theorem 4.1 and its proof in Section 6 imply that weakly converges to . This motivates the approximation

|

|

|

which implies a second-order approximation for the portfolio loss:

| (8) |

|

|

|

The next section develops, implements and tests a numerical method for computing the distribution of , and numerically demonstrates the accuracy of the approximation (8).

6. Proof of Theorem 4.1

In this section we prove the fluctuation Theorem 4.1. The methodology of the proof goes as follows. After some preliminary computations,

we obtain a convenient formulation of the equation that satisfies, see (20). Some terms in this equation will vanish in the limit as

; this is Lemma 6.1. Based on tightness of the involved processes (the topic of Section 8) and continuity properties of the operators involved, we can then pass to the limit

and thus identify the limiting equation. The limit process satisfies in the weak form another stochastic evolution, which has a unique solution (proven in Section 9).

The difficulty is to identify a rich enough space where tightness and uniqueness can be simultaneously proven. This is not trivial in our case, because the coefficients are not bounded

and the equation degenerates (coefficients of the highest derivatives are not bounded away from zero). It turns out that the appopriate space in which one can prove both tightness and uniqueness

is a weighted Sobolev space, introduced in \citeasnounPurtukhia1984 and further generalized in \citeasnounGyongiKrylov1992 to study stochastic partial differential equations with unbounded coefficients,

and are briefly reviewed in Section 7.

An application of Itô’s formula shows that for ,

|

|

|

|

| (18) |

|

|

|

|

where

|

|

|

|

|

|

for all , and ,

|

|

|

and

|

|

|

By subtracting (3) from (18) we find that satisfies the equation

|

|

|

|

|

|

|

|

In order to simplify the calculations later on, for each , , and , we define the quantity

|

|

|

A simple computation shows that

| (19) |

|

|

|

We can rewrite the stochastic evolution equation that satisfies as follows:

| (20) |

|

|

|

|

|

|

|

|

|

|

where

|

|

|

|

|

|

|

|

|

|

|

|

The term turns out to vanish in the limit as the following lemma shows.

Lemma 6.1.

For any and any , there is a constant , independent of such that

|

|

|

and

|

|

|

Moreover, we have that

|

|

|

Lastly, regarding the conditional (on ) covariation of the martingale term we have

| (21) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

We continue with the proof of the theorem and defer the proof of Lemma 6.1 to the end of this section. Relative compactness of the sequences

and in follows by

Lemmas 8.7 and 8.8. Relative compactness of the sequence

in follows by Lemma 7.1 in \citeasnounGieseckeSpiliopoulosSowersSirigano2012.

These imply that the sequence

|

|

|

is relatively compact in . Let us denote by

|

|

|

a limit point of this sequence. We mention here that this is a limit in distribution, so the limit point may not be defined on the same probability space as the prelimit sequence,

but nevertheless (and thus ), have the same distribution both in the limit and in the prelimit. Then, by (20), Lemma 6.1 and the continuity of the operators

and we get that will satisfy, due to Theorem 5.5 in \citeasnounKurtzProtter, the stochastic evolution equation (6). By Lemma 6.1, the conditional covariation of the distribution valued martingale is given by (7).

Uniqueness follows by Theorem 9.7. This concludes the proof of the theorem.

We conclude this section with the proof of Lemma 6.1.

Proof of Lemma 6.1.

We start by recalling that Lemma 3.4 in \citeasnounGieseckeSpiliopoulosSowers2011 states that for each and ,

| (22) |

|

|

|

for some constant that is independent of . Along with (19), this implies that

|

|

|

|

|

|

|

|

|

|

|

|

for some nonnegative constant that is independent of . Then, the first statement of the lemma follows. The second statement follows similarly. In particular, using the martingale property, (19) and (22) we immediately obtain

|

|

|

for some constant . The statement regarding follows directly by the previous computations and Doob’s inequality. The statement involving the conditional covariation of the martingale term follows directly by the definition of

and the fact that jumps do not occur simultaneously.

∎

7. The appropriate weighted Sobolev space

In this section we discuss the Sobolev space in which the fluctuations theorem is stated. Similar weighted Sobolev spaces were introduced in \citeasnounPurtukhia1984 and further generalized in \citeasnounGyongiKrylov1992 to study stochastic partial differential equations with unbounded coefficients. These weighted spaces turn out to be convenient and well adapted to our case. See \citeasnounFernandezMeleard and \citeasnounKurtzXiong for the use of weighted Sobolev spaces in fluctuation analyses of other interacting particle systems.

Let and be smooth functions in with . Let be an integer and define by the weighted Sobolev space which is the closure of in the norm

|

|

|

For the weight functions and we impose the following condition, which guarantees that will be a Hilbert space, see Proposition 3.10 of \citeasnounGyongiKrylov1992.

Condition 7.1.

For every , the functions and are bounded.

The inner product in this space is

|

|

|

Moreover, we denote by , the dual space to equipped with the norm

|

|

|

For notational convenience we will sometimes write and in the place of

and respectively, if no confusion arises.

The coefficients of our operators have linear growth in the first order terms and quadratic growth in the second order terms. For example, we easily see that the choices and with satisfy the assumptions of Condition 7.1. We refer the interested reader to \citeasnounGyongiKrylov1992 for more examples on possible choices for the weight functions .

Lemma 7.2.

Let Condition 7.1 with in place of hold, and fix and such that .

Then the operator is a linear map from into and for all , there exists a constant such that

|

|

|

Moreover, the operator is a linear map from into and for all

|

|

|

Proof.

Recall the definition of and examine term by term. For the first term, Condition 7.1 gives us

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For the second term again Condition 7.1 gives us

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For the third term we have

|

|

|

|

|

|

|

|

|

|

For the fourth term we have

| (23) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The statement for follows analogously. This completes the proof of the lemma.

∎

Notice that if the weights are chosen as above, then the condition on of Lemma 7.2 is equivalent to assuming that has finite moments up to order .

8. Tightness and continuity properties of the limiting process

We first recall three key preliminary results from \citeasnounGieseckeSpiliopoulosSowers2011 and \citeasnounGieseckeSpiliopoulosSowersSirigano2012 that will be useful in the sequel.

Lemma 8.1.

[Lemma 3.4 in \citeasnounGieseckeSpiliopoulosSowers2011.] For each and , there is a constant , independent of such that

|

|

|

Lemma 8.2.

[Lemma 8.2 in \citeasnounGieseckeSpiliopoulosSowersSirigano2012.] Let be a reference Brownian motion. For each where , there is a unique pair

taking values in

such that

| (24) |

|

|

|

|

and

| (25) |

|

|

|

Lemma 8.3.

[Lemma 8.4 in \citeasnounGieseckeSpiliopoulosSowersSirigano2012.] For all and , satisfying (3) is given by

|

|

|

where is defined via (24)-(25). Therefore, for any ,

|

|

|

Let us now set

|

|

|

Notice that

|

|

|

We prove tightness based on a coupling argument. The role of the coupled intensities will be played by , defined as follows.

Define to be the solution to (1) when the loss process term in the equation for the intensities has

been replaced by . Let us also denote by the corresponding default time and by the corresponding loss process. It is easy to see that conditional on the systematic process , the for are independent. The related empirical distribution will be accordingly denoted by .

Let and define the stopping time

|

|

|

Notice that the estimate in Lemma 8.1 implies that for and

| (26) |

|

|

|

Thus, it is enough to prove tightness for .

The following lemma provides a key estimate for the tightness proof.

Lemma 8.4.

For large enough (in particular for ) and weights such that Condition 7.1 holds and for every , there is a constant independent of such that

|

|

|

Proof.

For notational convenience we shall write in place of . Let us denote by and let . For notational convenience we define the operator

|

|

|

After some term rearrangement, Itô’s formula gives us, via the representations of Lemmas 8.2-8.3,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Using the bounds of Lemma 6.1, Itô’s formula and the fact that common jumps occur with probability zero, we have

|

|

|

|

|

|

|

|

|

|

where the term originates from the martingales and from Lemma 6.1. Next we apply Young’s inequality to get

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Let us next bound the term on the last line of the previous equation. It is easy to see that

|

|

|

is a discrete time martingale with respect to .

Thus, by Theorem 3.2 of \citeasnounBurkholder, we have that

|

|

|

where, maintaining the notation of \citeasnounBurkholder,

|

|

|

Therefore, recalling the bound from Lemma 8.1 we obtain

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This bound implies that

|

|

|

For large enough , Proposition 3.15 of \citeasnounGyongiKrylov1992 and Theorem 6.53 of \citeasnounAdams1978 immediately imply that the embedding is of Hilbert-Schmidt type. So, by Lemma 1 and Theorem 2 in Chapter 2.2 of \citeasnounGelfandVilenkin1964, if is a complete orthonormal basis for , then .

Hence, if is a complete orthonormal basis for we obtain that

|

|

|

|

|

|

|

|

Summing over we then obtain

|

|

|

Then as in Lemma 9.6 we get that

|

|

|

So,

|

|

|

Finally, an application of Gronwall’s lemma concludes the proof.

∎

The following lemma provides a uniform bound for the fluctuation process.

Lemma 8.5.

Let and weights such that Condition 7.1 holds. For every , there is a constant independent of such that

|

|

|

Proof.

Clearly .

Notice now that by Lemmas 8.2 and 8.3

|

|

|

is a discrete time martingale, which in turn implies via Theorem 3.2 of \citeasnounBurkholder and Proposition 3.15 of \citeasnounGyongiKrylov1992 (similarly to the proof of Lemma 8.4) that

|

|

|

Therefore, if is a complete orthonormal basis for with , Parseval’s identity gives (similarly to Lemma 8.4)

| (27) |

|

|

|

Since,

|

|

|

summing over we then obtain

|

|

|

which by Lemma 8.4 (obviously ) and (27) yields the statement of the lemma.

∎

Next we discuss relative compactness for . In particular, we have the following lemma.

Lemma 8.6.

Let and let and weights such that Condition 7.1 holds. The process is a valued martingale such that

|

|

|

Furthermore, it is relatively compact in

.

Proof.

Clearly, it is enough to prove tightness for . Let us define

|

|

|

Each one of the terms in the last display can be bounded by above similarly to the derivation of the upper bound for the term in (23). The bound from

Lemma 8.1 is then used in order to treat the integrals of the weight functions with respect to . It then follows that there exists a constant such that

|

|

|

Therefore, if is a complete orthonormal basis for with , we obtain

| (28) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As in the proof of Lemma 8.4, the restriction implies that . Similarly, we can also show that there exists a constant such that

|

|

|

|

|

Moreover, due to the inequality , the inequality (28) implies that

|

|

|

which obviously goes to zero as . The last two displays give relative compactness of in (Theorem 8.6 of Chapter 3 of \citeasnounMR88a:60130 and page 35 of \citeasnounJoffeMetivier1986).

The uniform bound of the lemma follows by the fact that as , see (26).

∎

Regarding the convergence of the martingale we have the following lemma.

Lemma 8.7.

Let and weights such that Condition 7.1 holds. The sequence

is relatively compact in . Moreover, it converges towards a distribution

valued martingale with conditional (on the algebra ) covariance function, defined, for , by (7). The martingale is conditionally on the algebra , Gaussian.

Proof.

Relative compactness follows by Lemma 8.6. Due to continuous dependence of (21) on and on the weak convergence of

by \citeasnounGieseckeSpiliopoulosSowersSirigano2012, we obtain that any limit point of as , , will satisfy (7).

Conditionally on , the limiting is a continuous square integrable martingale and its predictable variation is deterministic. Thus, by Theorem 7.1.4 in \citeasnounMR88a:60130, it is conditionally Gaussian.

This concludes the proof.

∎

Next we discuss relative compactness of the process .

Lemma 8.8.

Let , and weights such that Condition 7.1 holds. The process is relatively compact in .

Proof.

It is enough to prove tightness for

. For , the bound from Lemma 8.5 holds, i.e.,

| (29) |

|

|

|

Let be a complete orthonormal basis for with . By (20) we have

| (30) |

|

|

|

Next, we consider the mapping from into defined by

|

|

|

and we notice that

|

|

|

|

|

|

|

|

|

|

|

|

where the second inequality is due to Lemma 7.2 and the third inequality because .

Hence, by Parseval’s identity we have

|

|

|

|

Thus, by (29) we get

|

|

|

|

|

|

|

|

Similarly we also obtain that

|

|

|

The last estimates, the uniform bound from Lemma 8.5, Lemma 8.6 for and Lemma 6.1 for the remainder term imply the statement of the lemma. We follow the same steps as in the proof of Lemma 8.6 and thus the details are omitted.

∎

We end this section by proving a continuity result.

Lemma 8.9.

Any limit point of and is continuous, i.e., it takes values in , with .

Proof.

In order to prove that any limit point of takes values in , it is sufficient to show that

|

|

|

Let be a complete orthonormal basis for . Then, by definition, we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Clearly, is continuous, so we only need to consider the first two terms. The first term is bounded by , see (19), whereas for the second we immediately get

|

|

|

So, as in Proposition 3.15 of \citeasnounGyongiKrylov1992, we get that

|

|

|

Thus,

|

|

|

|

|

|

|

|

Since , we certainly have , and then as in Lemma 8.4, , which implies that after taking the limit as , the right hand side of the last display goes to zero. This concludes the proof of continuity of the limit point trajectories of .

Next we consider continuity of the trajectories of the limit points of . It follows directly by (30) and Lemma 6.1 that and have the same discontinuities. Thus, the continuity of any limit point of implies the continuity of any limit point of , which concludes the proof of the lemma.

∎

9. Uniqueness

In this section we prove uniqueness of the stochastic evolution equation (6). Let be two solutions of (6) and let us define . Then, will satisfy the stochastic evolution equation

|

|

|

|

|

|

|

|

Notice that this is a linear equation. In order to prove uniqueness, it is enough

to show that

|

|

|

Let be a complete orthonormal basis for . By Itô’s formula we get that

|

|

|

|

|

|

|

|

|

|

|

|

Then, summing over and taking expected value (due to Lemma 7.2, the expected value of the stochastic integral is zero) we have

| (31) |

|

|

|

Hence, if we prove that there is a constant such that

|

|

|

then we can conclude by Gronwall inequality that a.s.

Let us recall now that

|

|

|

and set

|

|

|

|

|

|

|

|

|

|

and for i=1,2.

Moreover, for simplicity in presentation and without loss of generality, we shall consider from now on only the case of a homogeneous portfolio, i.e, set . This is done without loss of generality, since the operators involve differentiation only with respect to . The proof for the general heterogeneous case, is identical with heavier notation.

Before a term by term examination, we gather some straightforward results in the following lemma.

Lemma 9.1.

Let and and assume Condition 7.1. Then, up to a multiplicative constant for the term , that may be different from line to line, we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proof.

It follows directly by integration by parts using Condition 7.1 and the assumption that and its derivatives are compactly supported.

∎

Then we bound each term on the right hand side of (31).

First, we notice that, by Riesz representation theorem, for there exists a unique such that

|

|

|

By a density argument we may assume that and obtain

|

|

|

which is true since by Lemma 7.2, .

Lemma 9.2.

For such that we have

|

|

|

|

|

|

|

|

|

|

Since , the integrals on the right hand side are well defined and bounded.

Proof.

We recall that

|

|

|

and that

|

|

|

Hence we bound each of the three terms separately. Using the statements of Lemma 9.1 we have for

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Similarly, for we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lastly, for the third term, , we have

|

|

|

|

|

|

|

|

|

|

Hence, putting all the estimates together, we conclude the proof of the lemma.

∎

Lemma 9.3.

Let us assume that is such that . For such that we have

|

|

|

Proof.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

which concludes the proof of the lemma.

∎

Lemma 9.5.

For such that we have

|

|

|

Since the integral on the right hand side is well defined and bounded.

Proof.

|

|

|

By the definition of the operator we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The first inequality follows from integration by parts on the second integral and the second and third inequality by Cauchy-Schwartz using Condition 7.1. Therefore, by canceling the term and then taking the square of the resulting expression, the statement of the lemma follows.

∎

Collecting the statements of Lemma 9.2 and Lemma 9.3 we obtain the following lemma.

Lemma 9.6.

For we have

|

|

|

Then we are in position to prove uniqueness for the limiting stochastic evolution equation.

Theorem 9.7.

Let us assume that . Then, the solution to the stochastic evolution equation (6) is unique in .

Proof.

Equation (31) gives, via Lemma 9.6,

|

|

|

|

|

|

|

|

|

|

Therefore, by applying Gronwall inequality we get that , which concludes the proof of the theorem.

∎