Abstract

In the following article we consider approximate Bayesian parameter inference for observation driven time series models.

Such statistical models appear in a wide variety of applications, including econometrics and applied mathematics.

This article considers the scenario where the likelihood function cannot be evaluated point-wise; in such cases,

one cannot perform exact statistical inference, including parameter estimation, which often requires advanced computational algorithms, such as Markov chain Monte Carlo (MCMC).

We introduce a new approximation based upon approximate Bayesian computation (ABC). Under some conditions, we show that

as , with the length of the time series, the ABC posterior has, almost surely, a maximum a posteriori (MAP) estimator of the parameters which is different from the true parameter.

However, a noisy ABC MAP, which perturbs the original data, asymptotically converges to the true parameter, almost surely. In order to draw statistical inference,

for the ABC approximation adopted, standard MCMC algorithms can have acceptance probabilities that fall at an exponential rate in

and slightly more advanced algorithms can mix poorly.

We develop a new and improved MCMC kernel, which is based upon an exact approximation of a marginal algorithm, whose cost per-iteration is random but the expected cost, for good performance, is

shown to be per-iteration.

We implement our new MCMC kernel for parameter inference from models in econometrics.

Key Words: Observation Driven Time Series Models, Approximate

Bayesian Computation, Asymptotic Consistency, Markov Chain Monte Carlo.

Approximate Inference for Observation Driven Time Series Models with Intractable Likelihoods

BY AJAY JASR, NIKOLAS KANTA, & ELENA EHRLIC

1Department of Statistics & Applied Probability,

National University of Singapore, Singapore, 117546, SG.

E-Mail: staja@nus.edu.sg

2Department of Statistical Science, University

College London, London, WC1E 6BT, UK.

E-Mail: n.kantas@ucl.ac.uk

3Department of Mathematics, Imperial College

London, London, SW7 2AZ, UK.

E-Mail: e.ehrlich05@imperial.ac.uk

1 Introduction

Observation driven time-series models, introduced by [4], has a wide variety of real applications, including econometrics (GARCH models) and applied mathematics (inferring initial conditions and parameters of ordinary differential equations). The model can be described as follows. We observe , which are associated to a dynamic system , which is potentially unknown. Define the process (with some arbitrary point on ) on a probability space , where, for every , is a probability measure. Denote by . The model is defined as, for

where , and for every , (the probabilities on ). Throughout, we assume that for any admits a density w.r.t. some finite measure , which we denote as . Next, we define a prior probability distribution on , with Lebesgue density . Thus, given observations the object of inference is the posterior distribution on :

| (1) |

where we have used the notation and is Lebesgue measure. In most applications of practical interest, one cannot compute the posterior point-wise and has to resort to numerical methods, such as MCMC, to draw inference on and/or .

In this article, we are not only interested in inferring the posterior distribution, but the scenario for which cannot be evaluated point-wise, nor do we have access to an unbiased estimate of it (it is assumed we can simulate from the associated distribution). In such a case, it is not possible to draw inference from the true posterior, even using numerical techniques. The common response in Bayesian statistics, is now to adopt an approximation of the posterior using the notion of approximate Bayesian computation (ABC); see [13] for a recent overview. ABC approximations of posteriors are based upon defining a probability distribution on an extended state-space, with the additional random variables lying on the data-space and usually distributed according the true likelihood. The closeness of the ABC posterior distribution is controlled by a tolerance parameter and often the approximation is exact as .

In this paper, we introduce a new ABC approximation of observation driven time-series models, which is closely associated to that developed in [8] for hidden Markov models (HMMs) and later for static parameter inference from HMMs [5]. This latter ABC approximation is particularly well behaved and a noisy variant (which pertrubs the data; see e.g. [5]) is shown under some assumptions to provide maximum-likelihood estimators (MLE) which asympotically in are the true parameters. The new ABC approximation that we develop is studied from a theoretical perspective. Relying on the recent work of [6] we show that, under some conditions, as , with the length of the time series, the ABC posterior has, almost surely, a MAP estimator of which is different from the true parameter say. However, a noisy ABC MAP of asymptotically converges to the true parameter, almost surely. These results establish that the particular approximation adopted is reasonably sensible.

The other main contribution of this article is a development of a new MCMC algorithm designed to sample from the ABC approximation of the posterior. Due to the nature of the ABC approximation it is easily seen that standard MCMC algorithms (e.g. [12]) will have an acceptance probability that will fall at an exponential rate in . In addition, more advanced ideas such as those based upon the ‘pseudo marginal’ [3], have recently been shown to perform rather poorly in theory; see [11]. These latter algorithms are based upon exact approximations of marginal algorithms [1, 2], which in our context is just sampling . We develop an MCMC kernel, related to recent work in [10], which is designed to have a random running time per-iteration, with the idea of improving the exploration ability of the Markov chain. We show that the expected cost per iteration of the algorithm, under some assumptions and for reasonable performance, is , which compares favourably with competing algorithms. We also show, empirically, that this new MCMC method out-performs standard pseudo marginal algorithms.

This paper is structured as follows. In Section 2 we introduce our ABC approximation and give our theoretical results on the MAP estimator. In Section 3, we give our new MCMC algorithm, along with some theoretical discussion about its computational cost and stability. In Section 4 our approximation and MCMC algorithm is illustrated on toy and real examples. In Section 5 we conclude the article with some discussion of future work. The proofs of our theoretical results are given in the appendix.

2 Approximate posteria using ABC approximations

2.1 ABC approximations and noisy ABC

As it was emphasised in Section 1, we are interested in performing inference when cannot be evaluated point-wise, nor do we have access to an unbiased estimate of it. We will instead assume it is possible to sample from . In such scenaria, one cannot use standard simulation based methods. For example, in a standard MCMC approach the Metropolis-Hastings acceptance ratio cannot be evaluated, even though it may be well-defined. Following the work in [5, 8] for hidden Markov models, we introduce an ABC approximation for the density of the posterior in (1) as follows:

| (2) |

with and

| (3) |

where we denote as the open ball centred at with radius and write . When is the Lebesgue measure, corresponds to the volume of the ball .

In general we will refer to ABC as the procedure of performing inference for the posterior in (2). In addition, we will call noisy ABC the inference procedure that uses instead of the original observation sequence a perturbed one, namely , where each is given by

with each is identically independently distributed (i.i.d.) uniformly on (shorthand ).

2.2 Consistency results for the MAP estimator

In this section we will investigate some interesting properties of the ABC posterior in (2). In particular, we will look at the asymptotic behaviour with of the resulting MAP estimators for . The properties of the MAP estimator reveal information about the mode of the posterior distribution as we obtain increasingly more data. To simplify the analysis in this section we will assume that:

-

(A1)

-

–

is fixed and known, i.e. , where denotes the Dirac delta measure on and is known.

-

–

is bounded and positive everywhere in .

-

–

the observations actually originated from the true model model for some , i.e. we look at a well-specified problem.

-

–

and do not depend upon . Thus we have the following model recursions for the true model:

(4) where we will denote associated expectations to as .

-

–

In addition, for this section we will introduce some extra notations: is a compact, complete and separable metric space and is a compact metric space, with . For two measures and of bounded variation denote the convolution . Let also be the probability law associated to the random sequence , where each is an i.i.d. sample from the uniform distribution defined on .

We proceed with some additional technical assumptions:

-

(A2)

is a stationary stochastic process, with strict sense stationary and ergodic, following (4).

-

(A3)

For every , is continuous. In addition, there exist such that for any , . Finally , for every .

-

(A4)

There exist a measurable , such that for every

-

(A5)

The following statements hold:

-

1.

if and only if

-

2.

If holds a.s., then .

-

1.

Assumptions (A(A2)-(A5)) and the compactness of are standard assumptions for maximum likelihood estimation (ML) and they can be used to show the uniqueness of the maximum likelihood estimator (MLE); see [6] for more details. Therefore, if the prior is bounded and positive everywhere on it is a simple corollary that the MAP estimator will correspond to the MLE. In the remaining part of this section we will adapt the analysis in [6] for MLE to the ABC setup.

In particular, we are to estimate using the log-likelihood function:

We define the ABC-MLE for an -long sequence as

We proceed with the following proposition:

The result establishes that the estimate will converge to a point, which is typically different to the true parameter. Hence there is an intrinsic asymptotic bias for the plain ABC procedure. To correct this bias, consider the noisy ABC procedure, of replacing the observations by where . The noisy ABC MLE estimator is then:

We have the following result:

The result shows that the noisy ABC MLE estimator is asymptotically unbiased. Therefore, given that in our setup the ABC MAP estimator corresponds to the ABC MLE we can conclude that the mode of the posterior distribution as we obtain increasingly more data is converging towards the true parameter. Finally we note that our assumptions indeed pose some restrictions, but these are shown to be realistic for a few interesting models in [6]. In addition, the main purpose of this result is to motivate the use of the approximate posterior in (2) when the observation sequence is long or its marginal likelihood is quite informative.

3 Computational Methodology

Recall that we formulated in the ABC posterior written in (5). One can rewrite the approximate posterior in (2):

with

Note we have just used Fubini’s theorem to rewritte the likehood as an integral of a product instead of a product of integrals shown in (2)-(3). In this paper we will focus only on MCMC algorithms and in particular on the Metropolis-Hastings (M-H) approach. In order to sample from the posterior one runs an ergodic Markov Chain with the invariant density being . Then after a few iterations when the chain has reached stationarity, one can treat the samples from the chain as approximate samples from . This is shown in Algorithm 1, where for convenience we denote . The one-step transition kernel of the MCMC chain is usually described as the M-H kernel and follows from Step 2 in Algorithm 1.

-

1.

(Initialisation) At sample .

-

2.

(M-H kernel) For :

-

•

Sample from a proposal with density .

-

•

Accept the proposed state and set with probability

otherwise set . Set and return to the start of 2.

-

•

Unfortunately is not available analytically and cannot be evaluated, so this rules out the possibility of using of traditional MCMC approaches like Algorithm 1. However, one can resort to the so called pseudo-marginal approach whereby unbiased estimates of are used instead within an MCMC algorithm. We will refer to this algorithm as ABC-MCMC. The resulting algorithm can be posed as one targeting a posterior defined on an extended state space, so that its marginal coincides with . We will use these ideas to present ABC-MCMC as a M-H algorithm which is an exact approximation to an appropriate marginal algorithm.

To illustrate an example of these ideas, we proceed by writing a posterior on an extended state-space as follows:

| (5) |

It is clear that (2) is the marginal of (5) and hence the similarity in the notation. As we will show later in this section, extending the target space in the posterior as in (5) is not the only and certainly not the best choice. We emphasise that the only essential requirement for each choice is that the marginal of the extended target is , but one should be cautious because the particular choice will affect the mixing properties and the efficiency of the MCMC scheme that will be used to sample from in (5) or another variant.

3.1 Standard approaches for ABC-MCMC

We will now look at two basic different choices for extending the ABC posterior while keeping the marginal fixed to . In the remainder of the paper we will denote as we did in Algorithm 1.

Initially consider the ABC approximation when be extended to the space :

Recall one cannot evaluate and is only able to simulate from it. In Algorithm (2) we present a natural M-H proposal that could be used to sample from instead of the one shown Step 2 at Algorithm 1. Note that this time the state of the MCMC chain is composed of . Here each assumes the role of an auxiliary variable to be eventually integrated out at the end of the MCMC procedure.

-

•

Sample from a proposal with density .

-

•

Sample from a distribution with joint density

-

•

Accept the proposed state with probability:

However, as increases, the M-H kernel in Algorithm 2 will have an acceptance probability that falls quickly with . In particular, for any fixed , the probability of obtaining such a sample will fall at an exponential rate in . This means that this basic ABC MCMC approach will be inefficient for a moderate value of .

This issue can be dealt with by using multiple trials, so that at each , some auxiliary variables (or pseudo-observations) are in the ball . This idea originates from [3, 12] and in fact augments the posterior to a larger state-space, , in order to target the following density:

Again, it is easy to show that the marginal of interest is preserved, i.e.

In Algorithm 3 we present an M-H kernel with invariant density . The state of the MCMC chain now is . We remark that as grows, one expects to recover the properties of the ideal M-H algorithm in Algorithm 1. Nevertheless, it has been shown in [11] that even the M-H kernel in Algorithm 3 does not always perform well. It can happen that the chain gets often stuck in regions of the state-space where

is small.

-

•

Sample from a proposal with density .

-

•

Sample from a distribution with joint density .

-

•

Accept the proposed state with probability:

3.2 A Metropolis-Hastings kernel for ABC with a random number of trials

We will address this shortfall detailed above, by proposing an alternative augmented target and corresponding M-H kernel. The basic idea is that a random number of trials is used based on the value of . Then it will be possible to use more computational effort when the chain is at regions where is low.

Consider an alternative extended target, for , , :

Standard results for negative binomial distrubutions (see [14, 15] for more details) imply that

| (6) |

holds and this can be used to deduce that

is an unbiased estimator for . In addition, from (6) it follows that the marginal w.r.t. is the one of interest:

In Algorithm 4 we present a M-H kernel with invariant density . The state of the MCMC chain this time is .

-

•

Sample from a proposal with density .

-

•

For repeat the following: sample with probability density until there are samples lying in ; the number of samples to achieve this (including the successful trial) is .

-

•

Accept with probability:

The potential benefit of this kernel is that one expects the probability of accepting a proposal is higher than the previous M-H kernel (for a given ). This comes at a computational cost which is both increased and random. The proposed kernel is based on the hit kernel of [10], which has been adapted here to account for the data being a sequence of observations resulting from a time series. Finally, it is important to mention that in Algorithms 3 and 4 generating multiple trials can be implemented very efficiently in parallel using appropriate computing hardware, such as multi-core processors or computing clusters.

3.2.1 On the choice of

To implement the proposed kernel, one needs to select . In practice to it is difficult to know a good value this a priori, so we present a theoretical result that can add some intuition on choosing . Let denote expectation w.r.t. given . We will also pose the assumption:

-

(A6)

For any fixed , , we have .

The the following result holds, whose proof can be found in the appendix.:

Proposition 3.1.

The result shows that one should set for the relative variance not to grow with , which is unsuprising, given the conditional independence structure of the . To get a better handle on the variance, suppose , then for fixed

For the new approach one can show

Not taking into account the computational cost, one prefers this new estimate with regards to variance if

which is likely to occur if is not too large (recall we want to be small, so that we have a good approximation of the true posterior) and is moderate - this is precisely the scenario in practice.

Remark 3.1.

It is easily shown that the relative variance associated to the estimate is

Note this quantity is not uniformly upper-bounded in unless , which may not occur. Conversely, Proposition 3.1 shows that the relative variance of the new estimator is uniformly upper-bounded in under minimal conditions. We suspect that this means in practice that the kernel with random number of trials may mix faster .

3.2.2 Computational considerations

As the cost per-iteration is random, we will investigate this further. We denote the proposal of as . Let be the initial distribution of the MCMC chain and the distribution of the state at time . In addition, denote by the proposed state for at iteration . Finally, we will write as the expectation of a random variable proposed by given the simulated state at time . We will assume that the observations are fixed and known. Then we have the following result:

Proposition 3.2.

Let , and suppose that there exists a constant such that for any we have , a.e.. Then it holds for any , , that:

The expected computational cost grows linearly with . Thus, coupled with the result in Proposition 3.1, one has a cost of per-iteration, which is comparable to many exact approximations of MCMC algorithms (e.g. [1]), albeit in a much simpler situation. Note also that the kernel in Algorithm 3 is expected to require a cost of per iteration for reasonable performance, although this cost here is deterministic. As mentioned above, one expects the approach with random number of trials to work better with regards to the mixing time, especially when the values of are not large. We attribute this to Algorithm 4 providing a more ‘targetted’ way to use the simulated auxiliary variables. This will be illustrated numerically in Section 4.

3.2.3 Relating the variance of the estimator or with the efficiency of ABC-MCMC

A comparison of our results with the interesting work in [7] seems relevant. There the authors deal with a more general context and show that we should choose as a particular asymptotic (in ) variance; the main point is that the (asymptotic) variance of the estimate of should be the same for each . We conjecture that in our set-up one should choose such that the actual variance of the estimate of is constant with respect to . In this scenario, on inspection of the proof of Proposition 3.1, for a given , one should set to be the solution of

for some desired (upper-bound on the) variance (whose optimal value would need to be obtained). This makes a random variable, in addition, but does not change the simulation mechanism. Unfortunately, one cannot do this in practice, as the are unknown. Taking into account Remark 3.1, this latter approach may not be so much of a concern in practice.

3.2.4 On the ergodicity of the sampler

We conclude this discussion by adding a related comment regarding the ergodicity of the proposed MCMC kernel. If there exists a constant such that

and the marginal MCMC kernel in Algorithm 1 is geometrically ergodic, then by [2, Propositions 7, 9] the MCMC kernel of Algorithm 4 is also geometrically ergodic.

4 Examples

4.1 Scalar normal means model

4.1.1 Model

For this example let each be a scalar real random variable and consider the model:

with and , where we denote the zero mean normal distribution with variance . The prior on is . This model is usually referred to as the standard normal means model in one dimension and the posterior is given by:

where Note that if , then the posterior on is consistent and concentrates around as .

The ABC approximation after marginalizing out the auxiliary variables has a likelihood given by:

where is the standard normal cumulative density function. Thus, this is a scenario where we can perform the marginal MCMC.

4.1.2 Simulation Results

Three data sets are generated from the model with and . In addition, for we perturb the data-sets in order to use them for noisy ABC. For the sake of comparison, we also generate a noisy ABC data-set for . We will also use a prior with .

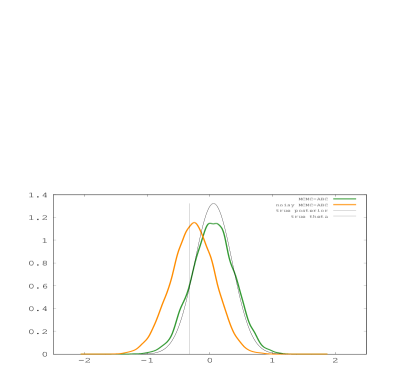

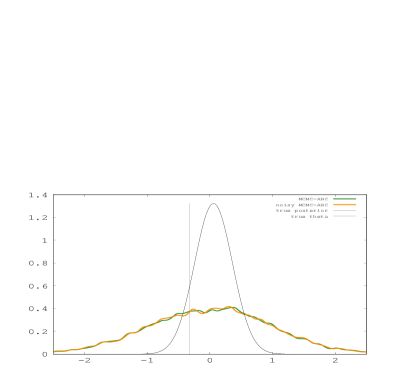

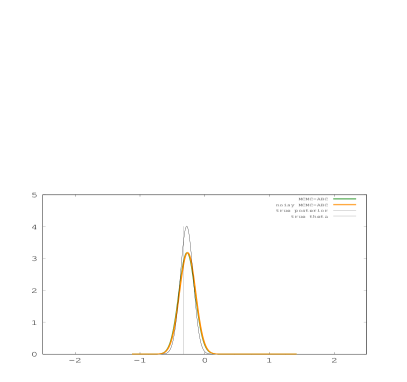

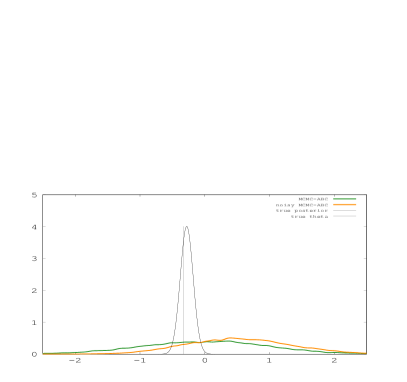

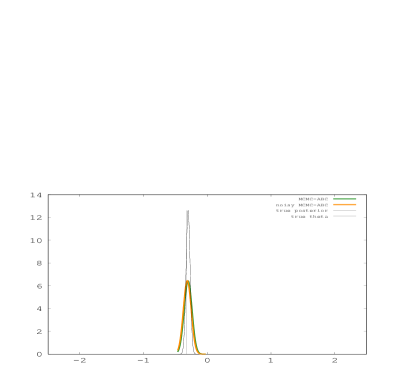

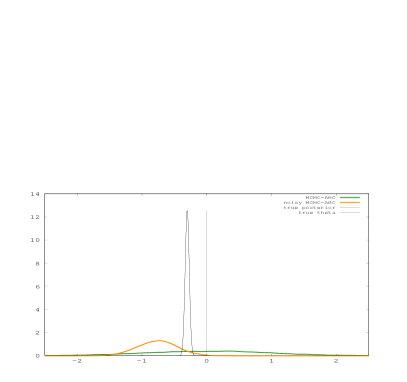

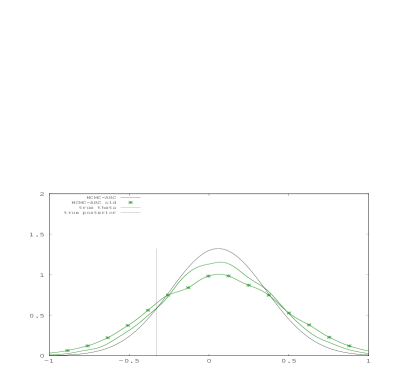

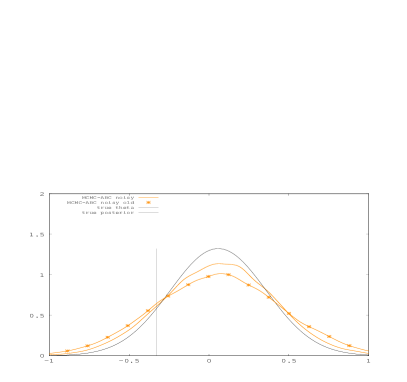

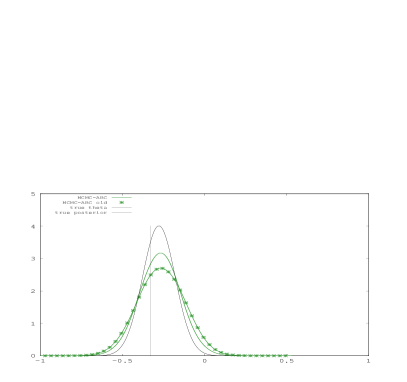

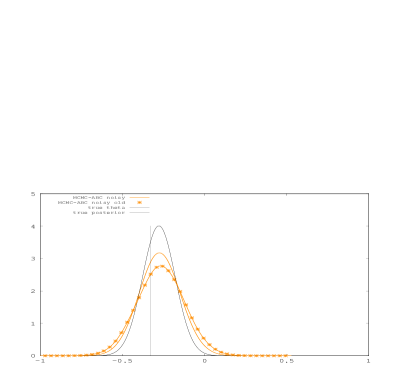

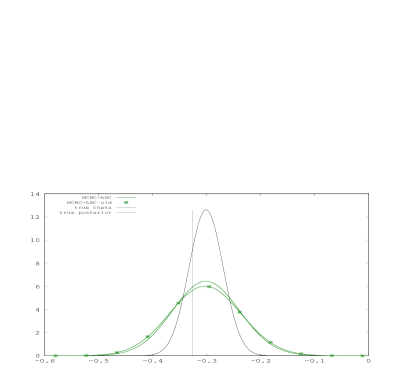

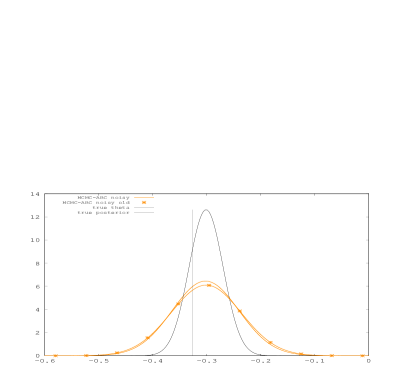

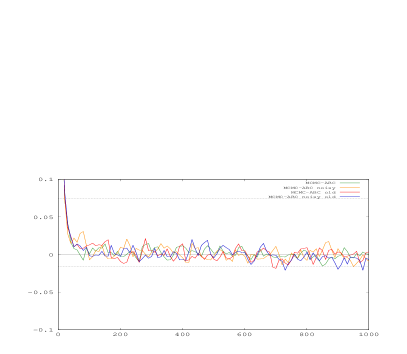

We run the new MCMC kernel (the proposal in Algorithm 4 - we will frequently use the expression ‘Algorithm’ to mean an MCMC kernel with the given proposal mechansim of the Algorithm), old MCMC kernel (Algorithm 3) and a Marginal MCMC algorithm which just samples on the parameter space (i.e. the posterior density is proportional to ). Each algorithm is run with a normal random walk proposal on the parameter space, with the same scaling. The scaling chosen yields an acceptance rate of around 0.25 for each run of the marginal MCMC algorithm. The new MCMC kernel is run with and the old with a slightly higher value of so that the computational times are about the same (so for example, the running time of the new kernel is not a problem in this example). The algorithms are run for 10000 iterations and the results can be found in Figures 1-3.

In Figure 1 the density plots for the posterior samples on , from the marginal MCMC can be seen for and each value of . When , we can observe that both ABC and noisy ABC both get closer to the true posterior as grows. For noisy ABC, this is the behavior that is predicted in Section 2.2. For the ABC approximation, following the proof of Theorem 1 in [8], one can see that the bias falls with ; hence, in this scenario there is not a substantial bias for the standard ABC approximation. When we make much larger a more pronounced difference between ABC and noisy ABC can be seen and it appears as grows that the noisy ABC approximation is slightly more accurate (relative to ABC).

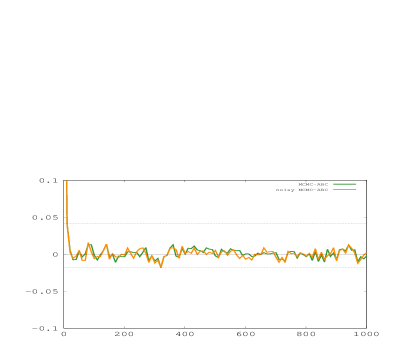

We now consider the similarity of the new and old MCMC kernels to the marginal algorithm (i.e. the kernel both procedures attempt to approximate), the results are in Figures 2-3. With regards to both the density plots (Figure 2) and auto-correlations (Figure 3) we can see that both MCMC kernels appear to be quite similar to the marginal MCMC. It is also noted that the acceptance rates of these latter kernels are also not far from that of the marginal algorithm (results not shown). These results are unsuprising, given the simplicity of the density that we target, but still reassuring; a more comprehensive comparison is given in the next example. Encouragingly, the new and old MCMC kernels do not seem to noticably worsen as grows; this shows that, at least for this example, the recommendation of is quite useful. We remark that whilst these results are for a single batch of data, the results are consistent with other data sets.

4.2 Real Data Example

4.2.1 Model

Set, for

where (i.e. a stable distribution, with location 0, scale and asymmetry and skewness parameters ). We set

where is a Gamma distribution with mean and . This is a GARCH(1,1) model with an intractable likelihood.

4.2.2 Simulation Results

We consider daily log-returns data from the S&P 500 index from 03/1/11 to 14/02/13, which constitutes 533 data-points. In the priors, we set and , which are not overly informative. In addition, and . We consider and only a noisy ABC approximation of the model. Algorithms 3 and 4 are to be compared. The MCMC proposals on the parameters are random-walks on the log-scale and for both algorithms we set . It should be noted that our results are fairly robust to changes in , which are the values we tested the algorithm with.

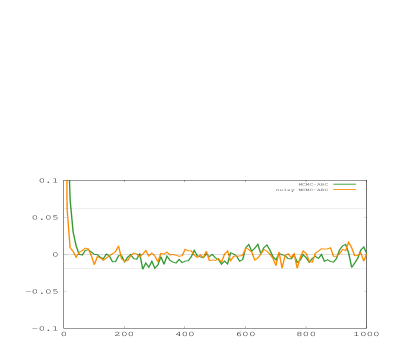

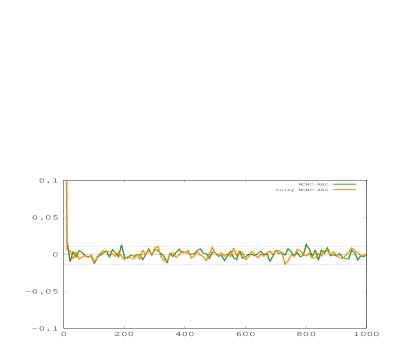

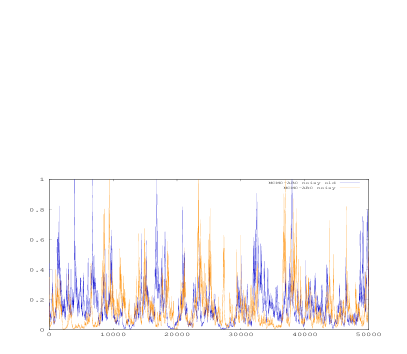

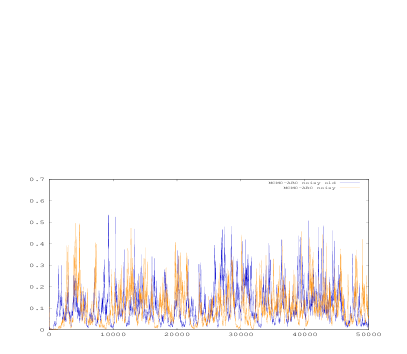

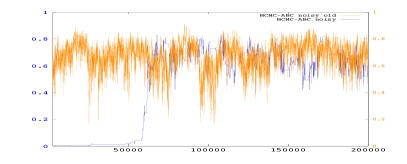

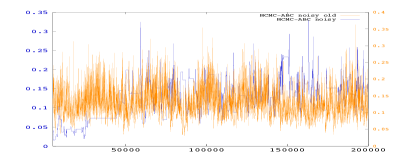

In Figure 4 we present the trace-plot of 50000 iterations of both MCMC kernels when . Algorithm 3 took about 0.30 seconds per iteration and Algorithm 4 took about 1.12 seconds per iteration We modified the proposal variances to yield an acceptance rate around 0.3. The plot shows that both algorithms appear to move across the state-space in a very reasonable way. The new algorithm takes much longer and in this situation does not appear to be required. This run is one of many we performed and we observed this behaviour in many of our runs.

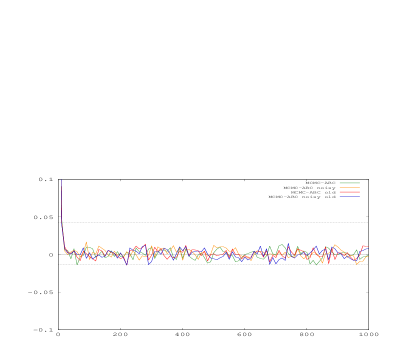

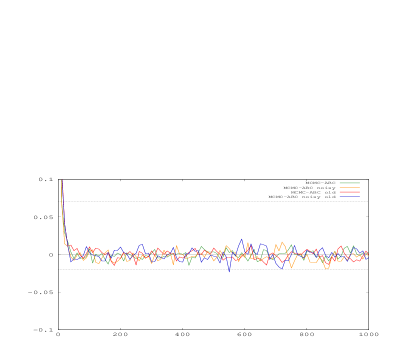

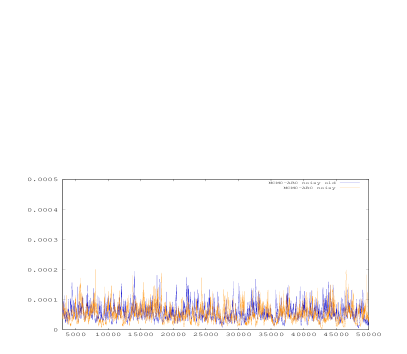

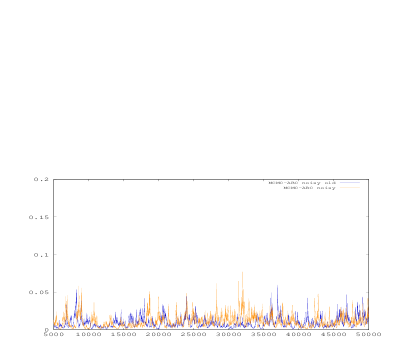

In Figure 5 we can observe the trace plots from a particular (typical) run when . In this case, both algorithms are run for 200000 iterations. Algorithm 3 took about 0.28 seconds per iteration and Algorithm 4 took about 2.06 seconds per iteration; this issue is discussed below. In this scenario, considerable effort was expended for Algorithm 3 to yield an acceptance rate around 0.3, but despite this, we were unable to make the algorithm traverse the state-space. In contrast, with less effort, Algorithm 4 appears to perform quite well and move around the parameter space (the acceptance rate was around 0.15 versus 0.01 for Algorithm 3). Whilst the computational time for Algorithm 4 is considerably more than Algorithm 3, in the same amount of computation time, it still moves more around the state space; algorithm runs of the same length are provided for presentational purposes. We remark that, whilst we do not claim that it is ‘impossible’ to make Algorithm 3 mix well in this example, we were unable to do so and, alternatively, for Algorithm 4 we expended considerably less effort for very reasonable performance. This example is typical of many runs of the algorithm and examples we have investigated and is consistent with the discussion in Section 3.2.2, where we stated that Algorithm 4 is likely to out-perform Algorithm 3 when the are not large, which is exactly the scenario in this example.

Turning to the cost of simulating Algorithm 4; for the case we simulated the data an average of 148000 times (per-iteration) and for this figure was 330000. In this example signifcant effort is expended in simulating the . This shows, at least in this example, that one can run the algorithm without it failing to sample the . The results here suggest that one should prefer Algorithm 4 only in challenging scenarios, as it can be very expensive in practice.

Finally, we remark that the MLE for a Gaussian Garch model, is . This differs to the posterior means, which may indicate that a stable distribution could be useful for modelling the observations for this class of models.

5 Conclusions

In this article we have considered approximate Bayesian inference from observation driven time series models. We looked at some consistency properties of the corresponding MAP estimators and also proposed an efficient ABC-MCMC algorithm to sample from these approximate posteriors. The performance of the latter was illustrated using numerical examples.

There are several interesting extensions to this work:

-

•

the asymptotic analysis of the ABC posterior in Section 2.2 can be further extended. For example, one may consider Bayesian consistency or Bernstein Von-Mises theorems, which could provide further justification to the approximation that was introduced here. Alternatively, one could look at the the asymptotic bias of the ABC posterior w.r.t. or the asymptotic loss in efficiency of the noisy ABC posterior w.r.t. similar to the work in [5] for hidden Markov models.

- •

-

•

an investigation to extend the ideas here for sequential Monte Carlo methods should be beneficial. This has been initiated in [9] in the context of particle filtering for a different class of models.

Acknowledgements

A. Jasra acknowledges support from the MOE Singapore and funding from Imperial College London. N. Kantas was kindly funded by EPSRC under grant EP/J01365X/1.

Appendix A Proofs for Section 2

Proof.

[Proof of Proposition 2.1] The proof of follows from [6, Theorem 21] if we can establish conditions (B1-3) for our perturbed ABC model. Clearly (B1) and part of (B2) holds. (B3-i) hold via [6, Lemma 21] via (A(A4)). We first need to show that for any that is continuous. Consider

Let , then, by (A(A3)) there exists a such that for

and hence for as above

which establishes (B2) of [6]. Now, for (B3-ii) of [6], we note that as (see (A(A3))) the function is Lipshitz and

for some that does not depend upon . Now

and

Thus, by (A(A4)) and the fact that (B3-i) of [6] holds:

Note, finally that (B3-iii) trivially follows by . Hence we have proved that

∎

Appendix B Proof for Section 3

Proof.

[Proof of Proposition 3.1] We have

and thus clearly

hence

| (7) |

Now the R.H.S.of (7) is equal to

| (8) |

Now, we will show

| (9) |

The proof is given when is odd. The case even follows by the proof as is odd and the additional term is negative. Now we have for that the sum of consecutive even and odd terms is equal to

which is negative as

Thus we have established (9). We will now show that

| (10) |

Following the same approach as above (i.e. is odd) the sum of consecutive even and odd terms is equal to

This is positive if

as and it follows that ; thus one can establish (10).

∎

Proof.

[Proof of Proposition 3.2] We have

where we have used the expectation of a negative-binomial random variable and applied , a.e. in the inequality ∎

References

- [1] Andrieu, C., Doucet, A. & Holenstein, R. (2010). Particle Markov chain Monte Carlo methods (with discussion). J. R. Statist. Soc. Ser. B, 72, 269–342.

- [2] Andrieu, C. & Vihola, M. (2012). Convergence properties of pseudo-marginal Markov chain Monte Carlo algorithms. arXiv:1210.1484 [math.PR]

- [3] Beaumont, M. A. (2003). Estimation of population growth or decline in genetically monitored populations. Genetics, 164, 1139.

- [4] Cox, D. R. (1981). Statistical analysis of time-series: some recent developments. Scand. J. Statist. 8, 93–115.

- [5] Dean, T. A., Singh, S. S., Jasra, A. & Peters G. W. (2010). Parameter estimation for Hidden Markov models with intractable likelihoods. arXiv:1103.5399 [math.ST]

- [6] Douc, R., Doukhan, P. & Moulines, E. (2012). Ergodicity of observation-driven time series models and consistency of the maximum likelihood estimator. arXiv:1210.4739 [math.ST].

- [7] Doucet, A., Pitt, M., & Kohn, R. (2012). Efficient implementation of Markov chain Monte Carlo when using an unbiased likelihood estimator. arXiv:1210.1871 [stat.ME].

- [8] Jasra, A., Singh, S. S., Martin, J. S. & McCoy, E. (2012). Filtering via approximate Bayesian computation. Statist. Comp., 22, 1223–1237.

- [9] Jasra, A., Lee, A., Yau, C. & Zhang, X. (2013). The alive particle filter. in preparation.

- [10] Lee, A. (2012). On the choice of MCMC kernels for approximate Bayesian computation with SMC samplers. In Proc. Winter Sim. Conf..

- [11] Lee, A. & Latuszynski, K. (2012). Variance bounding and geometric ergodicity of Markov chain Monte Carlo for approximate Bayesian computation. arXiv:1210.6703 [stat.ME].

- [12] Majoram, P., Molitor, J., Plagnol, V. & Tavare, S. (2003). Markov chain Monte Carlo without likelihoods. Proc. Nat. Acad. Sci., 100, 15324–15328.

- [13] Marin, J.-M., Pudlo, P., Robert, C.P. & Ryder, R. (2012). Approximate Bayesian computational methods. Statist. Comp., 22, 1167–1180.

- [14] Neuts, M. F. & Zacks, S. (1967). On mixtures of and distributions which yield distributions of the same family. Ann. Inst. Stat. Math., 19, 527–536.

- [15] Zacks, S. (1980). On some inverse moments of negative-binomial distributions and their application in estimation. J. Stat. Comp. & Sim., 10, 163-165.