Statistics of transitions for Markov chains with periodic forcing.111supported by Conseil Regional de Bourgogne (contracts no. 2012-9201AAO047S01283 and no. 2012-9201AAO049S02781)

Abstract

The influence of a time-periodic forcing on stochastic processes can essentially be emphasized in the large time behaviour of their paths. The statistics of transition in a simple Markov chain model permits to quantify this influence. In particular the first Floquet multiplier of the associated generating function can be explicitly computed and related to the equilibrium probability measure of an associated process in higher dimension. An application to the stochastic resonance is presented.

Key words and phrases: Markov chain, Floquet multipliers, ergodicity, large time asymptotic, stochastic resonance.

2000 AMS subject classifications: primary 60J27; secondary: 60F05, 34C25

Introduction

The description of natural phenomenon sometimes requires to introduce stochastic models with periodic forcing. The simplest model used to interpret for instance the abrupt changes between cold and warm ages in paleoclimatic data is a one-dimensional diffusion process with time-periodic drift [3]. This periodic forcing is directly related to the variation of the solar constant (Milankovitch cycles). In the neuroscience framework, such periodic forced model is also of prime importance: the firing of a single neuron stimulated by a periodic input signal can be represented by the first passage time of a periodically driven Ornstein-Uhlenbeck process [12] or other extended models [9]. Moreover let us note that seasonal autoregressive moving average models have been introduced in order to analyse and forecast statistical times series with periodic forcing. Recently the time dependence of the volatility in financial time series leaded to emphasize periodic autoregressive conditional heteroscedastic models. Whereas several statistical models permit to deal with time series, the influence of periodic forcing on time-continuous stochastic processes concerns only few mathematical studies. Let us note a nice reference in the physics literature dealing with this research subject [8].

Therefore we propose to study a simple Markov chain model evolving in a time-periodic environment (already introduced in the stochastic resonance context [7] and [6]) and in particular to focus our attention to its large time asymptotic behaviour. Since the dynamics of the Markov chain is not time-homogeneous, the classical convergence towards the invariant measure and the related convergence rate cannot be used. One essential tool is to increase the dimension of the state space in order to construct an appropriate homogeneous Markov chain and to apply classical ergodic results.

Description of the model. Let us consider a time-continuous Markov chain evolving in the state space whose transition rates correspond to respectively , the exit rate of the state resp. . We assume that and we perturb this initial process by a periodic forcing of period ; it means that the transition rates are increased using two additional non negative periodic functions . The obtained Markov chain is denoted by and its infinitesimal generator is given by

| (0.1) |

where are -periodic functions. In order to describe precisely the paths of the chain , we define transitions statistics: corresponds to the number of switching from state to up to time . The law of the random process at a fixed time is characterized by its moment generating function:

| (0.2) |

Main result. Let us first note that, in the higher dimensional space , we can define a Markov process which is time-homogeneous and admits a unique invariant measure . The main result can then be stated. The periodic forcing implies the use of Floquet’s theory to obtain a precise description of the moment generating function: there exist two time-periodic functions with such that

| (0.3) |

where is a positive function, and

| (0.4) |

This result implies in particular that, if the observed time-interval is increased by adding a period, the associated function is multiplied by a parameter which becomes close to

as becomes large.

Application. The explicit expression (0.4) of the first Floquet exponent permits to deal with particular optimization problems appearing in the stochastic resonance framework (see, for instance, [5]). Let us consider a family of periodic forcing having all the same period and being parametrized by a variable , then it is possible to choose in this family the perturbation which has the most influence on the stochastic process, just by minimizing the following quality measure:

In Section 3 we shall compare this quality measure (already introduced in [13]) to other measures usually used in the physics literature [7].

1 Periodic stationary measure for Markov chains

Before focusing our attention to the paths behaviour of the Markov chain, we describe, in this preliminary section, the fixed time distribution of the random process and, in particular, analyse the existence of a so-called periodic stationary probability measure – PSPM (we shall precise this terminology in the following).

The distribution of the Markov chain starting from the initial distribution and evolving in the state space is characterized by

This probability measure (the symbol stands for the transpose) constitutes a solution to the following ode:

| (1.1) |

where the generator is defined in (0.1).

Floquet’s theory dealing with linear differential equation with periodic coefficients can thus be applied. In particular we shall prove that converges exponentially fast towards a periodic solution of (1.1), the convergence rate being related to the Floquet multipliers (see Section 2.4 in [2]).

Definition 1.1.

Any -periodic solution of (1.1) is called a periodic stationary probability measure – PSPM iif and both for all .

The following statement points out the long time asymptotics of the Markov chain.

Proposition 1.2.

In the large time limit, the probability distribution converges towards the unique PSPM defined by and

| (1.2) |

where

| (1.3) |

More precisely:

| (1.4) |

where stands for the second Floquet exponent:

| (1.5) |

Remark 1.3.

It is possible to transform into a time-homogeneous Markov process just by increasing the space dimension. By this procedure becomes the invariant probability measure of .

Proof.

1. First we study the existence of a unique PSPM. Let be a probability measure thus . If satisfies (1.1) then we obtain, by substitution, the differential equation:

This equation can be solved using the variation of the constant. The procedure yields to (1.2). The periodicity of the solution requires and leads to (1.3).

2. The system (1.1) admits two Floquet multipliers and . Since there exists a periodic solution, one of the multipliers (let’s say ) is equal to and we can compute the other one using the relation between the product and the trace of :

The explicit expression of the trace leads to (1.5). Let us just note that we can link to both Floquet multipliers and the so-called Floquet exponents and defined (not uniquely) by

3. Since the Floquet multipliers are different, each multiplier is associated with a particular solution of (1.1). (i.e. ) corresponds to the PSPM since for all . For the Floquet exponent , we consider the solution of (1.1) with initial condition . Combining both equations of (1.1), we obtain

| (1.6) |

We deduce

and we can easily check that .

The solution of (1.1) with any initial condition is therefore a linear combination of and , the solutions corresponding to the Floquet multipliers. Writing in the basis yields

with (equal to in the particular probability measure case) and

Then, if the initial condition is a probability, we obtain (1.5) since

∎

2 Statistics of transitions

In the previous section, the study of the process points out how fast its distribution converges towards a periodic stationary distribution (in the sense that and are identically distributed). The aim now is to improve this result, which is just related to the position of the chain at some fixed time , by analysing the paths behaviour in the large time scale, especially the statistics of the transitions between the two states namely and . That’s why we introduce the moment generating function

| (2.1) |

associated with , the number of transitions from state to state up to time . We can decompose this generating function into two parts:

Then the vector satisfies the ode:

| (2.2) |

Since (2.2) is a differential equation with periodic coefficients, Floquet’s theory can be applied and, in this way, the Floquet multipliers describe the large time behaviour of any solution to the equation (2.2), in particular the generating function. That’s why we shall compute explicitly these multipliers. In Section 1 the system of ode considered has been reduced to a one-dimensional equation, here it is not the case so that we need to introduce an other procedure: a time-discretization approach.

2.1 The discrete-time counterpart of the chain

We consider a non-homogeneous Markov chain in discrete time defined on the space state . The associated transition matrix is given by

where are periodic sequences of period . Let us introduce different quantities related to :

| (2.3) |

For notational simplicity, the index shall voluntarily be removed when there is no ambiguity. Let us now consider usual properties of the discrete-time Markov chain: existence of periodic stationary probability measure, uniqueness and ergodic properties.

Proposition 2.1.

The Markov chain admits a unique stationary probability measure given by

| (2.4) |

and

| (2.5) |

Remark 2.2.

Since the PSPM is a probability, we compute and deduce .

Proof.

Let us define the probability that the chain is in the state at time . The chain is initialized through . Then applying the matrix , the distribution of satisfies The same argument yields the distribution of :

By induction, we obtain the general formula:

which can be rewritten by use of the quantities as follows:

| (2.6) |

Since the Markov chain is positive and recurrent, there exists a unique stationary probability measure . This measure is obtained by setting and solving . This leads immediately to the value of and in the sequel for any using (2.6). ∎

Theorem 2.3.

Let be the number of transitions from state to state performed by the Markov chain up to time (included). We denote by its moment generating function:

| (2.7) |

The following asymptotic behaviour holds:

| (2.8) |

where is the stationary distribution of the Markov chain defined in Proposition 2.1.

Proof.

Step. 1 Let us prove that for any

| (2.9) |

The second equality in (2.8) is then immediate. We obtain (2.9) by induction: for , we easily have

We assume that (2.9) is satisfied for some , then

This leads to (2.9) with replaced by . Formula (2.9) is therefore satisfied for all especially for .

Step 2. The ergodic theorem is the essential tool for studying the long time behaviour. First of all we construct a new -valued Markov chain defined by

The associated transition matrix depends on and ; moreover it is -periodic. To deal with an homogeneous chain, it suffices to consider . Suppose that the law of is the invariant periodic measure describe in Proposition 2.1 then is also in the invariant regime: for all , we have

In the previous expression, both terms constituting the right hand side are -periodic. Hence is periodic. Let us therefore define the following measure :

Let us just observe that is a positive invariant measure for the homogeneous Markov chain . It suffices to normalize the measure in order to obtain an invariant probability: . Let us now consider the moment generating function associated with the number of transitions . By construction, is also the number of time the non-homogeneous Markov chain visits the state or finally the number of times the homogeneous Markov chain visits the set

Since the homogeneous chain is recurrent positive and aperiodic, the ergodic theorem implies

More precisely the law of the iterated logarithm implies the existence of a constant such that

| (2.11) |

Let us then define the event : the set of all paths satisfying

Hence, for , we obtain the associated decomposition

Using Lebesgue’s dominated convergence theorem and (2.11), the second term converges to when tends to infinity. Moreover

and by symmetry

Since converges to as , the combination of both previous inequalities leads to

In order to conclude the proof, it suffices to compute the explicit expression of . ∎

In a similar way to Section 1, the asymptotic behaviour of the moment generating function is related to the eigenvalues of a suitable matrix. Indeed, if we decompose the generating function as follows

| (2.12) |

then the vector satisfies the recurrence relation:

| (2.13) |

Let us define the product of matrices

| (2.14) |

We thus obtain . We observe in the following statement the link between the asymptotic behaviour of the moment generating function and the eigenvalues of the monodromy matrix.

Corollary 2.4.

Let . The eigenvalues of the monodromy matrix satisfy: and

| (2.15) |

Proof.

The matrix is directly related to the fundamental solution of equation (2.13). In fact its coefficients correspond to

These coefficients are all positive: the matrix thus admits two distinct real eigenvalues, denoted by and ( corresponds to the largest one), and is diagonalizable. We denote by , the associated eigenvectors. Hence can be expressed in this basis: there exists and such that . We immediately deduce

| (2.16) |

Let us prove that . If we compute the determinant of , we obtain:

We recall that is defined in (2.3). Since ,

| (2.17) |

Due to the assumption , (2.17) leads to . Suppose that (consequently ), then according to (2.16), is a bounded sequence. Of course, this is a nonsense since is the generating function (associated with ) of a growing process which a.s. tends to infinity. Consequently , and . Finally we deduce the large time asymptotic behaviour:

| (2.18) |

Remark 2.5.

It is also possible to compute the second eigenvalue of the monodromy matrix . Indeed, by (2.17), we get:

2.2 On the convergence from discrete to continuous time

In the previous section, the asymptotic behaviour of a periodic discrete-time Markov chain was emphasized. The study of such Markov chain was a first step in the analysis of continuous-time Markov chain. We shall now describe how all previous results can have a continuous counterpart.

In this section, we especially prove that the Markov chain , the expression defined by (2.3), the probability measures defined by (2.4) and (2.5) and finally the moment generating function

converge as becomes large.

Let us assume that the transition probabilities of the Markov chain are small with respect to :

| (2.19) |

where and are piecewise continuous functions defined in (0.1).

Lemma 2.6.

Proof.

For notational simplicity, we set . By definition for . Using (2.19), we obtain for ,

Using the Taylor expansion, we get

To conclude it suffices to use the uniform convergence of the Riemann series theorem on one side and to prove that the error term converges uniformly towards . The details are left to the reader. ∎

Since we have a link between the transition probabilities of the discrete-time Markov chain (through ) and the transition probabilities of the continuous one , we shall compare the processes themselves. First we investigate the comparison of the stationary measures and secondly we point out the convergence in law of the processes.

Let us define the time-continuous process associated with the discrete Markov chain

as follows

| (2.21) |

Let us note that is a piecewise constant and càdlàg process.

Proposition 2.7.

The stationary probability measure associated with the process converges to the stationary distribution of the Markov chain . This convergence holds uniformly w.r.t. the time variable .

Remark 2.8.

We shall use the following result : if converges uniformly to on and if is piecewise continuous on , then the following convergence holds uniformly

Proof of Proposition 2.7. We first focus our attention to the convergence of given by (2.5). The assumption (2.19) leads to

| (2.22) |

which converges uniformly (Lemma 2.6) towards

| (2.23) |

Let us just recall that has been defined in (1.3). Using (2.5), (2.22), (2.23) and the identity , leads to

| (2.24) |

Using similar arguments, we prove the convergence of defined by (2.4). Let and two real numbers such that . We define and by and . We observe the following uniform convergences:

| (2.25) |

and

| (2.26) |

By (2.24), (2.25) and (2.26) applied to (2.4), the uniform limit holds:

| (2.27) |

The right hand term corresponds to the expression of , see (1.2).

Proposition 2.9.

The process , defined by (2.21), converges in distribution towards the Markov chain .

Proof.

The proof is divided into three parts. First we prove the convergence of the conditional distribution of successive jumps. In the second part, we prove the convergence of the process on any bounded interval. Finally, we point out that converges in distribution to .

Step 1. Convergence of successive jumps.

We set .

We set and we define the successive transition times for the chain as

and for the chain the associated transition times are denoted by . For (resp. ), we set (resp. ). We study the transition times from to : by (2.19) we get

By similar arguments as those developed in Lemma 2.6, we obtain

| (2.28) |

For transitions from to , that is typically given , we obtain the same result, just replacing by .

Step 2. Let us prove now the convergence of the Markov chain on any compact set. Wet set the time interval , it is straightforward to generalize to any compact set.

Let us define the counting process of all transitions of the chain on the interval :

| (2.29) |

and the counting process associated with the chain . We prove that the distribution sequence of the processes is tight (see for instance Theorem 13.3 p.141 in [1]). The theorem requires two conditions. The first one is

| (2.30) |

Let us define . Then

Thus we obtain

which corresponds to the first condition (2.30). For the second condition, let . We have to prove that, for any , there exist and such that

| (2.31) |

where is the modulus of continuity defined by

Let us observe that takes either the value or the value . Hence, for all , we define . Therefore

| (2.32) |

We set where is defined by the following probability

Introducing , we obtain the lower-bound

Consequently

and, by induction, the following lower-bound holds

| (2.33) |

Let us now use the bounds (2.33) and (2.2) in order to prove (2.31). Since converges in distribution to (see Step 1) as , there exist and such that

Choose small enough such that permits to deduce from (2.33). In particular, there exist and such that ,

and therefore (2.2) leads to (2.31). Both conditions needed in Theorem 13.3 [1] are satisfied, we conlude that the distribution of the process is tight.

Step 3. The two first steps (convergence of marginals and tightness) imply that converges in distribution towards as becomes large. Let us now deduce the convergence of towards . It suffices to use the function which is continuous with respect to the Skorohod topology:

The convergence of is then immediate. ∎

Remark 2.10.

The statement of Proposition 2.9 can be improved: not only the process converges to , the couple (Markov chain and associated counting process) also converges in distribution to .

Since both the periodic stationary probability measure and the distribution of the periodic discrete-time Markov chain converges, we can obtain the large time asymptotic behaviour of the statistics of transitions for the time-continuous Markov chain via the discretization procedure. The main result announced in the introduction is an adaptation of the following statement which is a consequence of Theorem 2.3.

Let us recall that (resp. ) is the moment generating function of the transitions (from state to ) for the discrete-time Markov chain (resp. the continuous-time one).

Theorem 2.11.

1. For all , the statistics of transitions converge in distribution as : the moment generating functions satisfy

| (2.34) |

2. The eigenvalues of the matrix defined in (2.13) and (2.14) satisfy and the largest one is given by

| (2.35) |

Here denotes the PSPM defined by (1.2). The long time asymptotic behaviour of the generating function is given by

Proof.

By Proposition 2.9, the process converges in distribution to . The convergence of the generating function is an immediate consequence. In particular,

| (2.36) |

We deduce that the four coefficients of the monodromy matrix converge to

Using the equation , the limit matrix is in fact the monodromy matrix of the ode (2.2). Both eigenvalues of converge to the eigenvalues of . Hence, according to equation (2.15)

which converges to

Since , the inequality holds. By similar arguments as those presented in the proof of Corollary 2.4, we obtain and we can write the moment generating function in the Floquet basis as follows: with . Hence . In order to obtain the large time asymptotics, let us note that, for any , there exists such that and consequently

Both bounds tend to .

Finally let us note that can easily be expressed as the mean number of transitions during one period and starting with the PSPM. This identity remains true in the large limit. Indeed it suffices to use the convergence of the generating functions to deduce that the family of random variables is uniformly integrable. Therefore applying Vallée-Poussin’s theorem (see for instance Theorem T22 in [10]) to the function with . We thus obtain the convergence of the average number of transitions starting from any initial distribution and in particular starting from the PSPM. So we deduce:

∎

3 Two examples in the stochastic resonance framework

We seek to describe the phenomenon of stochastic resonance. The continuous-time Markov chain oscillates between two values according to a T-periodic infinitesimal generator . Then by varying the period, we observe that the behaviour of the chain changes and adopts more or less periodic paths. The aim in each example is to find the optimal period such that the behaviour of the paths looks like the most periodic as possible. That’s why we shall introduce a criterion which measures the periodicity of any random path. We propose to use a criterion associated with the largest Floquet exponent of the generating function. The interesting tunings correspond to situations where this exponent is close to the value . Such a criterion was already presented in [13].

3.1 An infinitesimal generator constant on each half period

In this first example, we consider T-periodic rates given by

| (3.1) |

where et , . This Markov model is often used in the stochastic resonance framework (see for instance [11]). Here we can compute explicitly the invariant measure (see also [11] Proposition 4.1.2 p.34)

Lemma 3.1.

The periodic stationary probability measure PSPM is given by:

| (3.2) |

and , .

Proof.

An immediate consequence of Theorem 2.11 and Lemma 3.1 leads to the explicit computation of the largest Floquet exponent (the details of the proof are left to the reader).

Proposition 3.2.

We are interested in the phenomenon of stochastic resonance associated to continuous-time process . This process essentially depends on two parameters: a parameter describing the intensity of the transition rates between both states (some small corresponds to a frozen situation: the Markov chain remains in the same state for a long while) and a second parameter , the period of the process dynamics. By considering the normalized process , especially its paths on a fixed interval , we observe the following phenomenon (for fixed ): if is small then there are very few transitions of : the process tends to remain in its original state. If is large, behaves in a chaotic way: lots of transitions are observed. For some intermediate values of , the random paths of are close to deterministic periodic functions (one transition in each direction per period). Let us note that this phenomenon can also be observed by freezing the period length and varying the intensity of the rates.

The aim is therefore to point out the best relationship (tuning) between and which makes the process the most periodic as possible. If the process is close to a periodic function then the number of transition from state to sate is close to per period, which leads to find the tuning corresponding to the Floquet exponent equal to . By Proposition 3.2, it is then sufficient to find the best relation between and such that

| (3.5) |

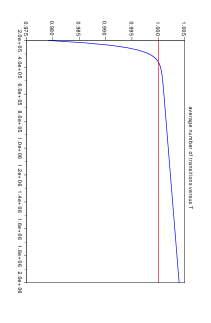

In Figure 1, we set , , , and let vary. We compute numerically the average number of transitions per period. We can clearly observe that there is one and only one period corresponding to the condition (3.5).

Proposition 3.3.

Let be the period which provides an average number of transitions per period equal to . The following asymptotic behaviour holds, as tends to ,

| (3.6) |

Proof.

The condition (3.5) combined with Proposition 3.2 leads to the equation

The aim is to solve it and let tend to . The left member in the previous equation is an increasing function of . We introduce the change of variable . We first prove that increases as decreases. satisfies with

Both functions and decrease for small and large enough. It follows that increases when decreases and tends to . Let us assume in the limit . Then which contradicts the identity . We deduce that when . Now let us set and . With these new parameters can be written like

Let us define then , we obtain that tends to when and the previous equation becomes:

Thus, when , we have

If with and , we obtain the limit when and therefore

We recall which leads to the result set. ∎

In [11], several quality measures have been proposed to point out the optimal tuning of : the spectral power amplification (SPA), the SPA to noise intensity ratio (SPN), the energy (En), the energy to noise intensity ratio (ENR), the out-of-phase measure which describes the time spent in the most attractive state, the entropy or relative entropy. In his PhD report, I. Pavlyukevich computes for each measure the optimal relation between and , the length of the period, in the small limit, we adopt a similar procedure in Proposition 3.3. So we can now gather these quality measures into three families:

-

•

for the first family, the optimal tuning satisfies where is given by (3.6). The associated Markov chain has an average number of transitions from to strictly smaller than . This family contains in particular the SPN.

-

•

The second family concerns . The Markov chain has then more than one transition per period on average. This family contains most of the measures: SPA, En, Out-of-phase, the entropy and relative entropy.

-

•

Finally in the third family and are comparable, this is namely the case for ENR.

3.2 Infinitesimal generator with constant trace

Let us finally present a second example of periodic forcing in the stochastic resonance framework. This model was introduced by Eckmann and Thomas [4]. The aim in this paragraph is to find the optimal tuning between the noise intensity in the system and the period length in order to reach an average number of transitions during one period close to . This approach is different from the study prensented in [4].

The model consists in a continuous-time Markov chain with periodic forcing: the transition rates are given by

| (3.7) |

The period satisfies . In this particular case, the trace of the infinitesimal generator, defined by (0.1), is a constant function. It is then quite simple to compute explicitely the periodic stationary probability measure and the Floquet multipliers associated with the moment generating function of the statistics of transitions.

Lemma 3.4.

The periodic stationary probability measure of the periodic forced Markov chain is given by

| (3.8) |

Proof.

Using Proposition 1.2, we obtain

Hence

Setting , we obtain and consequently the announced statement. ∎

An application of Theorem 2.11 permits to describe the large time asymptotics for the moment generating function of the transitions from state to state . It suffices to compute explicitely . The result is described in the following statement while the proof is left to the reader.

Proposition 3.5.

The largest Floquet exponent associated with the statistics of transitions (the moment generating function) is equal to with

| (3.9) |

and given by (3.8).

Let us now discuss the suitable choice of the period such that . We then need to solve

| (3.10) |

It is obvious that is of the order , we set and look for the best choice of the parameter . Considering (3.10), the optimal value is in fact a real root of the following polynomial function

It is straightforward to prove that this polynomial function has a single positive root since it is increasing and verifies . Using the Cardan formula, we can obtain an explicit expression of which depends of course on the coefficient , this dependence is asymptotically linear as becomes large.

Acknowledgements

We are very grateful to Mihai Gradinaru for interesting conceptual and scientific discussions on the problem of stochastic resonance associated to the two-states Markov chain. His availability was greatly appreciated.

References

- [1] P. Billingsley. Convergence of probability measures. Wiley Series in Probability and Statistics: Probability and Statistics. John Wiley & Sons Inc., New York, second edition, 1999. A Wiley-Interscience Publication.

- [2] C. Chicone. Ordinary differential equations with applications, volume 34 of Texts in Applied Mathematics. Springer-Verlag, New York, 1999.

- [3] P. D. Ditlevsen. Extension of stochastic resonance in the dynamics of ice ages. Chemical Physics, 375(2-3):403 – 409, 2010. Stochastic processes in Physics and Chemistry (in honor of Peter Hänggi).

- [4] J P Eckmann and L E Thomas. Remarks on stochastic resonances. Journal of Physics A: Mathematical and General, 15(6):L261, 1982.

- [5] L. Gammaitoni, P. Hänggi, P. Jung, and F. Marchesoni. Stochastic resonance. Reviews of Modern Physics, 70(1):223–287, 1998.

- [6] S. Herrmann and P. Imkeller. The exit problem for diffusions with time-periodic drift and stochastic resonance. Ann. Appl. Probab., 15(1A):39–68, 2005.

- [7] P. Imkeller and I. Pavlyukevich. Stochastic resonance in two-state Markov chains. Arch. Math. (Basel), 77(1):107–115, 2001. Festschrift: Erich Lamprecht.

- [8] P. Jung. Periodically Driven Stochastic Systems. Physics reports. North-Holland, 1993.

- [9] A. Longtin. Stochastic resonance in neuron models. Journal of Statistical Physics, 70:309–327, 1993.

- [10] P.-A. Meyer. Probability and potentials. Blaisdell Publishing Co. Ginn and Co., Waltham, Mass.-Toronto, Ont.-London, 1966.

- [11] I. Pavlyukevich. Stochastic Resonance. Logos Verlag Berlin, 2002.

- [12] H.E. Plesser and S. Tanaka. Stochastic resonance in a model neuron with reset. Physics Letters A, 225(4-6):228 – 234, 1997.

- [13] P. Talkner. Statistics of entrance times. Phys. A, 325(1-2):124–135, 2003. Stochastic systems: from randomness to complexity (Erice, 2002).