Inventory Control for Spectrally Positive Lévy Demand Processes

Abstract.

A new approach to solve the continuous-time stochastic inventory problem using the fluctuation theory of Lévy processes is developed. This approach involves the recent developments of the scale function that is capable of expressing many fluctuation identities of spectrally one-sided Lévy processes. For the case with a fixed cost and a general spectrally positive Lévy demand process, we show the optimality of an -policy. The optimal policy and the value function are concisely expressed via the scale function. Numerical examples under a Lévy process in the -family with jumps of infinite activity are provided to confirm the analytical results.

Furthermore, the case with no fixed ordering costs is studied.

AMS 2010 Subject Classifications: 60G51, 93E20, 49J40

Key words: inventory models; impulse control; -policy;

spectrally one-sided Lévy processes; scale functions

1. Introduction

In this study, we introduce the fluctuation theory of Lévy processes to solve inventory control problems. In the continuous-time model, the majority of existing studies use a certain type of Lévy process as a demand process; typically it is modeled by Brownian motion, a compound Poisson process, or a mixture of the two. Pursuing the connections between the inventory theory and the Lévy-process theory is naturally of great importance. However, recent advances on Lévy processes have not been used to study inventory models. Therefore, our objective in the current study is to fill this void. Toward this end, we introduce the so-called scale function to inventory control, which plays a key role in the fluctuation theory of Lévy processes. We demonstrate both analytically and numerically that it is in fact a powerful tool to solve inventory control problems.

The common aim of inventory control is to derive the optimal replenishment policy to minimize both inventory and ordering costs. This study focuses on the discounted continuous-time model with fixed and proportional costs. We assume that the order quantity is continuous and back-orders are allowed. Furthermore, we assume the absence of lead time, perishability, and lost sales. This setting is the same as that in the seminal study by [9] where they solved (complementing [12]) the case where the demand arrives as a combination of Brownian motion and a compound Poisson process. In the current study, a scale-function-based approach is used to solve the problem for any choice of spectrally positive Lévy demand process i.e. a Lévy process with only upward jumps.

To our best knowledge, this is the first study on inventory models where the theory of scale functions is applied to derive the optimal solution. We focus on the aforementioned simple setting and demonstrate that the existing known properties of the scale function can be efficiently used to follow the classical guess and verify procedure in a straightforward fashion. Of course, applying the same technique in other inventory models can be of great importance. We expect that this study can potentially serve as a guide on how to tackle these open problems using the theory of scale functions. For a detailed review of inventory control problems, we refer the readers to [12, 13, 43] and the recent book by Bensoussan [10].

Over the last decade or two, significant developments in the fluctuation theory of Lévy processes have been presented (see, e.g., the textbooks by Bertoin [14], Doney [18], and Kyprianou [31]). Whereas the majority of Lévy processes still remain to be analytically tractable, numerous computations have been made possible when it comes to the spectrally one-sided Lévy process (a Lévy process with only upward or downward jumps) because of the development of the scale function.

For every spectrally one-sided Lévy process, the corresponding scale function, which is concisely defined in terms of the Laplace exponent, plays a great role. Without specifying a particular process type, it can efficiently express, e.g., hitting time probabilities, resolvent (potential) measures, and overshoot/undershoot distributions. It has gradually come into use in several stochastic models. In particular, it is now considered as a key tool in insurance mathematics; the classical formulation that models the surplus of an insurance company using a compound Poisson process is now being replaced by the spectrally negative Lévy model. Other stochastic models where the scale function plays a key role include, e.g., optimal stopping [20, 32, 36, 41, 47], stochastic games [4, 5, 19, 26], and mathematical finance [34, 46].

In this study, we begin with the same formulation as in [12] and solve for the general spectrally positive Lévy process. We have no difficulty in conjecturing that the form of an optimal policy is again of the -type, i.e., bringing the inventory level up to whenever it goes below is optimal. However, the scale-function-based approach is worth studying for various reasons. Here we summarize its advantages over the classical approach that involves solutions to integro-differential equations (IDEs).

Generalization of the demand process: Essentially, all existing Lévy-based inventory models employ the Lévy processes with upward jumps of finite activity [as defined in (3.20)], i.e., the demand arrives as a (drifted) compound Poisson process with or without a Brownian motion. The set of these Lévy processes excludes those with infinite activity/variation. In other words, the existing models do not cover well-known processes such as the (spectrally positive versions of) variance gamma, CGMY, and normal inverse Gaussian processes as well as classical ones as the gamma process and a subset of stable processes. For these processes, the IDE involves integration with respect to infinite measures, and hence, the IDE-based approach can become intractable. On the other hand, the approach that uses the scale function can accommodate these processes without any additional work.

Lévy processes of infinite activity/variation have been applied in the field of finance and insurance. Empirical evidence shows that asset prices can be more precisely modeled by jumps of infinite activity as opposed to being modeled by Brownian motion (see the introduction in [16]). Because the demand is closely linked to the price of an item, modeling inventory systems using these processes also makes sense. This reason motivates us to work on the inventory control problem for a general spectrally positive Lévy demand process.

Conciseness of arguments: The scale function can explicitly express the expected total costs under the -policy. Using this function, the optimal solution can be derived in a straightforward manner. As typically conducted in solving stochastic control problems, the optimal solution is first “guessed,” and its optimality is then confirmed by “verification” arguments. The known properties of the scale function help one achieve these objectives.

The first guessing step is reduced to choosing the pair by imposing the following two conditions on the expected cost function as follows:

-

(1)

The continuous (resp. smooth) fit condition at the lower threshold when the demand process is of bounded (resp. unbounded) variation,

-

(2)

The condition at the upper threshold such that the slope at is equal to the negative of the unit proportional cost.

Because of the (semi-)analytical expression of the expected costs under the -policy, these two conditions can be concisely rewritten by the scale function. For the results in this study, become the zeros of the function defined in (4.6) and that of its derivative with respect to the second argument. Using this graphical interpretation and taking advantage again of the certain known properties of the scale function, the existence of such can be confirmed.

The second verification step reduces to indicating that the candidate value function is sufficiently smooth and satisfies the quasi-variational inequalities (QVIs). The former can be easily confirmed because of the known smoothness/continuity properties of the scale function that depend on the path variation of the process. Unfortunately, part of the latter can become difficult to verify. However, in this study, the optimality in fact holds because of several known facts on the scale function and the results obtained in [9].

Computability: The derived optimal thresholds and the associated optimal value function are concisely written via the scale function. Hence, the computation of these factors is essentially equivalent to that of the scale function. Because the scale function is defined by its Laplace transform written in terms of the Laplace exponent, the Laplace transform needs to be inverted either analytically or numerically to compute it.

Fortunately, some important classes of Lévy processes have rational forms of Laplace exponents. For these processes, analytical forms of scale functions can be easily obtained by partial fraction decomposition. In Section 3.2, we show examples of such processes. Among others, the phase-type Lévy process of [2] is of great interest both in analytical and numerical aspects. It admits a rational form of Laplace exponent and is known to be dense in the set of all Lévy processes. This means that, it has an explicit form of scale function, and, more importantly, any scale function can be approximated by the scale function of this form. Egami and Yamazaki [22] conducted a sequence of numerical experiments to confirm the accuracy of this approximation.

Alternatively, the scale function can always be directly computed via numerical Laplace inversion. As discussed in Kuznetsov et al. [29], a scale function can be written as the difference between an exponential function (whose parameter is defined by in the current paper) and the resolvent (potential) term [see the third equation in (3.19) below]. Hence, the computation is reduced to that of the resolvent term. It is a bounded function that asymptotically converges to zero, and hence, numerical Laplace inversion can be quickly and accurately conducted. For more details, we refer the readers to Section 5 of [29].

To confirm the analytical results obtained in this study, we provide numerical examples with a quadratic inventory cost and a demand process in the -family in [28] with jumps of infinite activity. We can see that the optimal levels and the value function can be instantaneously computed.

Sensitivity analysis: Because of the analytical expressions of optimal thresholds and the value function, sensitivity analysis can be more directly conducted.

The sensitivity with respect to the parameter of the underlying Lévy process is equivalent to that of the scale function. For example, the smoothness of the optimal value function is directly linked to the asymptotic behavior of the scale function near zero. In our numerical results, we consider the cases where the diffusion coefficient is zero and positive, and analyze how the optimal solutions differ.

Furthermore, the sensitivity with respect to the fixed and unit proportional costs is of great interest. In particular, the forms of the optimal solutions are different depending on the existence of a fixed ordering cost. The distance between the optimal thresholds and is expected to shrink as the fixed cost decreases. In this study, we also consider the case with no fixed ordering cost and show that the optimal policy is of the barrier type. Using the fluctuation theory of reflected Lévy processes as in [3] and [42], the value function can again be written using the scale function. We numerically confirm that, as the fixed cost decreases to zero, the optimal -policy converges to the optimal barrier strategy.

Before closing the introduction, we briefly review the scale-function approach used in other stochastic control problems and discuss the similarities and differences with the results of this study.

The most relevant factor is the optimal dividend problem (de Finetti’s problem) in insurance mathematics. After the development of the fluctuation theory of reflected Lévy processes, many authors have applied the results in the spectrally negative Lévy model of de Finetti’s problems [33, 37, 38, 39] (see also [7, 8, 49] for the spectrally positive Lévy models). The main difference with our inventory control problem is that whereas our problem has an infinite time horizon, de Finetti’s problem is terminated at the ruin time (or the first time the controlled process goes below the zero level). In our problem, the absence of a ruin makes the problem both easier and more difficult. Whereas in de Finetti’s problem the optimality holds only for a subset of Lévy processes (see [37]), it holds for any spectrally positive demand process in our problem (except that the Lévy measure needs to have a light tail). On the other hand, without the ruin, the value function becomes unbounded (even not Lipschitz continuous), and the verification arguments become significantly more difficult (see the proof of Theorem 7.1).

In our problem, with a fixed cost, two threshold levels for the optimal -policy need to be found, which is different from the optimal stopping and de Finetti’s problems (with the exceptions of [8] and [39]), where only one parameter describes the optimal policy. In general, choosing two parameters is significantly more difficult. However the scale function helps one achieve this objective. Whereas this technique remains to be established, similar arguments can be found in stochastic games [19, 26] where two parameters characterize the equilibrium between two players.

The rest of this study is organized as follows. Section 2 presents a mathematical model of the problem. Section 3 reviews spectrally one-sided Lévy processes and scale functions. Section 4 presents the computation of the expected total costs under the -policy via the scale function. Section 5 obtains a candidate policy via the continuous/smooth fit principle and shows its existence. Section 6 verifies its optimality. Section 7 studies the case without a fixed ordering cost. Section 8 presents numerical results and Section 9 concludes this study.

Throughout this study, and are used to indicate the right- and left-hand limits, respectively. Superscripts , , , and are used to indicate positive and negative parts. Finally, we let , for any right-continuous process .

2. Inventory Models

Let be a probability space on which a stochastic process with , which represents the demand of a single item, is defined. Under the conditional probability , the initial level of inventory is given by (in particular, we let ). Hence, the inventory in the absence of control follows the stochastic process

| (2.1) |

We shall consider the case where is a spectrally positive Lévy process, or equivalently is a spectrally negative Lévy process; we will define these processes formally in the next section. Let be the filtration generated by (or equivalently by ).

An (ordering) policy is given in the form of an impulse control with and , , where is an increasing sequence of -stopping times and , for , is an -measurable random variable. Corresponding to every policy , the (controlled) inventory process is given by where and

We assume that the order quantity is continuous and backorders are allowed. In addition, we assume that there is no lead time, perishability, and lost sales.

The problem is to compute, for a given discount factor , the total expected costs given by

and to obtain an admissible policy that minimizes it, if such a policy exists. We shall additionally assume that an admissible policy is such that and are both well-defined and finite -a.s.

Here, corresponds to the cost of holding and shortage when and , respectively. Regarding , we assume

| (2.2) |

for some unit (proportional) cost of the item and fixed ordering cost . We shall study the case separately in Section 7. As in [9, 12], we assume the following.

Assumption 2.1.

-

(1)

is continuous and piecewise continuously differentiable with , and grows (or decreases) at most polynomially (that is to say, there exist and such that for all such that ).

-

(2)

For some ,

(2.3) is decreasing and convex on and increasing on .

-

(3)

For some and , we have for a.e. .

As in [9, 12], this is a crucial assumption for our analysis, and in particular will be used to verify the existence of the optimal policy.

Finally, the (optimal) value function is written as

| (2.4) |

where is the set of all admissible policies. If the infimum is attained by some admissible policy , then we call an optimal policy.

3. Spectrally Negative Lévy Processes and Scale Functions

Throughout this paper, we assume that the demand process is a spectrally positive Lévy process. Equivalently, the process as in (2.1) is a spectrally negative Lévy process. By the Lévy-Khintchine formula (see e.g. Bertoin [14]), any Lévy process can be characterized by its Laplace exponent. Here, Assumption 3.1 we shall assume below allows us to write the Laplace exponent of as

| (3.1) |

where is a Lévy measure with the support that satisfies the integrability condition .

A Lévy process has paths of bounded variation a.s. or otherwise it has paths of unbounded variation a.s. The former holds if and only if and ; in this case, the expression (3.1) can be simplified to

with . We exclude the case in which is the negative of a subordinator (i.e., is monotonically decreasing a.s.). This assumption implies that when is of bounded variation.

Regarding the Lévy measure , we make the same assumption as Assumption 3.2 of [12] so that has a finite moment for some small .

Assumption 3.1.

We assume that there exists a such that

This guarantees that

| (3.2) |

is well-defined and finite.

For the rest of this section, we briefly review the fluctuation theory of the spectrally negative Lévy process and the scale function, which will play significant roles in solving the problem. Note that, unless otherwise stated, Assumption 3.1 is not required for the results in the next subsection to hold.

3.1. Scale functions

Fix . For any spectrally negative Lévy process, there exists a function called the -scale function

which is zero on , continuous and strictly increasing on , and is characterized by the Laplace transform:

| (3.3) |

where

Here, the Laplace exponent in (3.1) is known to be zero at the origin and convex on ; therefore is well-defined and is strictly positive as . We also define, for ,

Because for , we have

| (3.4) |

The most well-known application of the scale function can be found in the two-sided exit problem. Let us define the first down- and up-crossing times, respectively, of by

| (3.5) |

Then, for any and ,

| (3.6) | ||||

The continuity and smoothness of the scale function depend on the path variation of . First, regarding the behaviors around zero, as in Lemmas 3.1 and 3.2 of [29],

| (3.9) | ||||

| (3.13) |

These properties are particularly useful in applying the continuous/smooth fit principle in stochastic control problems. In this paper, we use this to obtain the candidate thresholds of the optimal policy; see Section 5.1 below.

Regarding the smoothness on , we have the following; see [17] for more comprehensive results.

Remark 3.1.

If is of unbounded variation or the Lévy measure does not have an atom, then it is known that is . Hence,

-

(1)

is and for the bounded variation case, while it is and for the unbounded variation case,

-

(2)

is and for the bounded variation case, while it is and for the unbounded variation case.

These smoothness results are important in order to apply the Itô formula where the (candidate) value function must be (resp. ) for the case of unbounded (resp. bounded) variation.

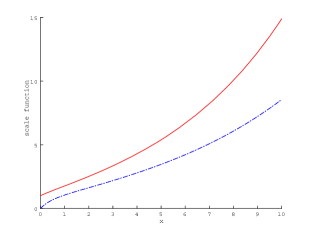

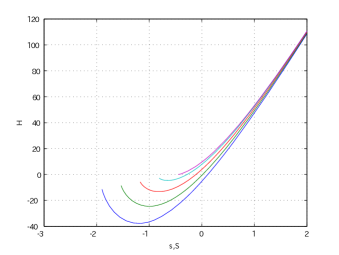

In Figure 1, we show sample plots of the scale function on . As reviewed in (3.9), the behaviors around zero depend on the path variation of the process.

|

3.1.1. Change of measures

Fix and define as the Laplace exponent of under with the change of measure

| (3.14) |

see page 213 of [31]. Suppose and are the scale functions associated with under (or equivalently with ). Then, by Lemma 8.4 of [31], , , which is well-defined even for by Lemmas 8.3 and 8.5 of [31]. In particular, we define

| (3.15) |

which is known to be an increasing function.

By this change of measure (3.14), one can express the expectation for using the scale function. Using this, we can compute the (discounted) moments; for example, by taking the derivative with respect to and then a limit, we have under (3.2)

| (3.16) |

see Proposition 2 of [3] for more detailed computation.

3.1.2. Martingale properties

3.1.3. -resolvent (potential) measure

The scale function can express concisely the -resolvent (potential) density. As summarized in Theorem 8.7 and Corollaries 8.8 and 8.9 of [31] (see also Bertoin [15], Emery [23], and Suprun [45]), we have

| (3.19) | ||||

It is clear that these can be used in the computation of inventory costs (see (4.11)).

The same identities can be obtained when the process is replaced with the running infimum process , . In particular, by Corollary 2.2 of [29], for Borel subsets in the nonnegative half-line,

where is the measure such that (see [31, (8.20)]) and is the Dirac measure at zero. Here, for all ,

We shall use this function and

later in the paper. Here the positivity of holds because for and that of holds because it is the integral of . Their positivity will be important in deriving the existence of the optimal solution and the verification of optimality. See the proofs of Proposition 5.2 and Lemma 5.3 below.

3.2. Examples of scale functions

We shall conclude this section with concrete examples of scale functions. We refer the readers to, e.g., [27, 29] for other examples.

3.2.1. Brownian motion

3.2.2. -stable processes

The spectrally negative stable process with index has the Laplace exponent . As in Example 8.2 of [31], its scale function is given by

where is the Mittag-Leffler function of parameter (which is a generalization of the exponential function).

3.2.3. Phase-type Lévy processes [2]

A spectrally negative Lévy process with a finite Lévy measure admits a decomposition

| (3.20) |

for some , , standard Brownian motion , a Poisson process with arrival rate and a sequence of i.i.d. random variables . These processes are assumed to be mutually independent.

The spectrally negative phase-type Lévy process is a special case where is phase-type distributed; a distribution on is of phase-type if it is the distribution of the absorption time in a finite state continuous-time Markov chain consisting of one absorbing state and transient states. If the phase-type distributed random variable is given by a Markov chain with intensity matrix over all transient states and the initial distribution , then the Laplace exponent (3.1) becomes

which can be extended to except at the negative of eigenvalues of .

Suppose is the set of the (possibly complex-valued) roots of the equality with negative real parts, and if these are assumed distinct, then the scale function can be written

| (3.21) |

3.2.4. Meromorphic Lévy processes [30]

As a variant of the phase-type Lévy process, the meromorphic Lévy process [30] is a type of Lévy process whose Lévy measure admits a density of the form

for some . Examples include Lévy processes in the -family as we use for numerical results in Section 8 below. The equation has a countable number of negative real-valued roots that satisfy the interlacing condition:

As discussed in [29], the scale function can be written as

| (3.22) |

4. The -policy

In this paper, we aim to prove that the -policy is optimal for some . For arbitrary , an -policy, , brings the level of the inventory process up to whenever it goes below .

This process can be defined recursively as follows. First, it moves like the original process until the first time it goes below :

This is immediately pushed up to (and hence ) by adding , and then follows

where is the first time after the pre-controlled process

| (4.1) |

goes below .

The process after can be constructed in the same way. The stopping time , for each , corresponds to the jump of ; the -measurable random variable

is the corresponding jump size. Clearly, this strategy is admissible: it can be written

The process is a strong Markov process. To see this, the Markov property is clear because, from the construction, the distribution of only depends on and the increment , where the latter is independent of . This can be strengthened to the strong Markov property by the right-continuity of the path of (see, e.g., the proof of Exercise 3.2 of [31], which shows the strong Markov property of a reflected Lévy process).

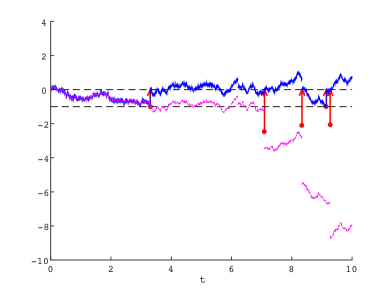

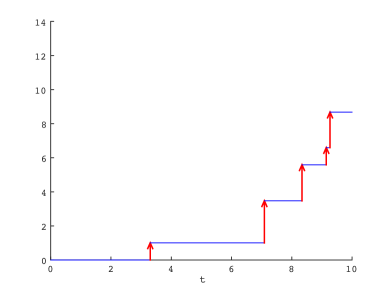

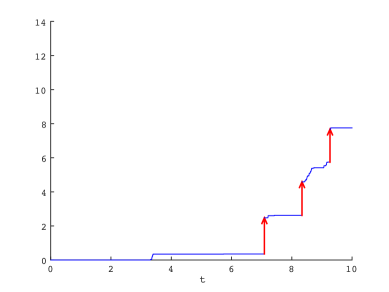

In Figure 2, we show sample paths of the controlled process and its corresponding control process for , when the starting value is . Due to the negative jumps, the process as in (4.1) can jump to a level strictly below (and is then immediately pushed to ). In the figure, the red arrows show the corresponding impulse control: each time the process goes below , it pushes up to by adding . At the same time, the process increases by the same amount.

|

|

Our objective in this section is to compute the expected total costs under the -policy, denoted by

| (4.2) |

Toward this end, we compute that of its “tilted version” (with respect to the unit proportional cost )

| (4.3) |

As has been already seen in, e.g., [9, 12], the computation in the following arguments becomes simpler if we deal with (4.3) rather than (4.2). The reason will be clear in later arguments. In particular, for , the slope of is and hence that of is . Accordingly, we use instead of . To see this, note in the verification of optimality that we need to show the positivity of , and we have .

Proposition 4.1.

For all ,

| (4.4) | ||||

where we define

| (4.5) | ||||

| (4.6) |

For the rest of the paper, we define , and analogously to (4.5). Analytical properties (as in, e.g., Lemma 5.1) of these functions are important in deriving the results of this paper. In particular, for the limiting case as we study in Section 7 below, the optimal threshold is given by the root of (see Lemma 5.1).

Remark 4.1.

By Assumption 2.1(1), the functions , , and are finite for any .

4.1. Proof of Proposition 4.1

Recall the down-crossing time as in (3.5). Notice from the construction that, -a.s., for and on . By these, (2.2), and the strong Markov property of , the expectation (4.2) must satisfy, for every ,

| (4.7) |

Define

| (4.8) |

Then, using (3.6) and (4.3), we can write (4.7) as

| (4.9) | ||||

where

| (4.10) |

Here (4.10) holds by solving (4.9) for . Hence, once we identify the expression for , we can compute and consequently the whole function (4.3) as well.

The proof consists of evaluating the three expectations in (4.8). The first expectation can be obtained directly by (3.19). We have for ,

| (4.11) |

which is well-defined by Remark 4.1.

Here, by the following lemma, we can write (4.5) and the integral interchangeably for and .

Lemma 4.1.

For , we have

Proof.

See Appendix A.1. ∎

In (4.8), substituting (3.6) (with replaced with ), (4.12), and (4.13), we have the expression

Substituting this in (4.10) shows the first equation of (4.4). The second equation is immediate by (4.9).

Remark 4.2.

The same technique can be used to compute the expected costs under the four parameter band policy for an extension of the problem with a two-sided control; see the note by Yamazaki [48].

5. Candidate policies

In the previous section, we computed for arbitrary as in (4.4). Here two different functions for and are pasted together at the point , and hence the continuity/smoothness of the function does not necessarily hold at the point . The principle of smooth/continuous fit chooses the parameters so that the function becomes continuous/smooth at . In our problem, as we need to identify two parameters , we use one additional condition described below.

In this section, we obtain the candidates of for the optimal policy. Toward this end, we choose such that (1) is continuous (resp. differentiable) at the lower threshold when is of bounded (resp. unbounded) variation, and (2) the slope of at the upper threshold equals the negative of the unit proportional cost. We rewrite these two conditions, via the scale function, as and where is defined as in (4.6) and is the derivative of with respect to the second argument, i.e.,

| (5.1) |

We shall then show the existence of the pair that simultaneously satisfy these two equations.

5.1. Continuous/smooth fit

We will see that the condition is equivalent to the so-called continuous/smooth fit condition at . It is well-known, in the existence of a diffusion component, that smooth fit holds for impulse control problems; see, e.g., [24]. On the other hand, for a Lévy process of bounded variation, continuous fit may be used alternatively. This is well-studied particularly for optimal stopping problems; see, e.g., [21, 34]. Here we apply continuous fit for the case is of bounded variation and smooth fit for the case it is of unbounded variation.

Once is satisfied, then the second condition turns out to be equivalent to the condition that the slope of the value function at equals the negative of the proportional cost , i.e., the slope of at is zero. Note that this condition is commonly used in impulse control to identify optimal -policies.

For all , the function (5.1) can be written

where the last equality holds because integration by parts gives

| (5.2) |

and

| (5.3) |

Proposition 5.1.

Suppose are such that . Then,

-

(1)

is continuous (resp. differentiable) at when is of bounded (resp. unbounded) variation,

-

(2)

.

Proof.

The proof of Proposition 5.1 can be carried out by a straightforward differentiation of the scale function and its asymptotic behavior near zero as in (3.9) and (3.13).

By taking in the second equality of (4.4) and because

| (5.4) |

we have

Note that if and only if is of unbounded variation in view of (3.9). Hence, the continuity at holds if and only if for the case of bounded variation while it holds automatically for the unbounded variation case.

For the case of unbounded variation, we further pursue the differentiability at . Differentiating (4.4),

| (5.5) |

Because for the case of unbounded variation by (3.13) and , we see that the differentiability holds if and only if as well.

We now turn our attention to the slope at . If we impose in (5.5), we have . Hence if and only if . This completes the proof.∎

5.2. Existence of

We shall now show that there indeed exists a pair such that ; in the next section we show that this requirement is sufficient to prove the optimality of the -policy. We refer the readers to the stochastic games [19] and [26] where similar arguments are used to identify a pair of parameters that describe the optimal policy.

Recall , , as in Assumption 2.1 and that is equivalent to (4.23) of [12] (times a positive constant). By Assumption 2.1, this satisfies the following. These results are due to Proposition 5.1 of [12] and hence the proof is omitted. Regarding the connection between and the function , see our later discussion in Section 7.

Lemma 5.1.

-

(1)

There exists a unique number such that , if and if .

-

(2)

for .

-

(3)

for .

With defined above, we show that the desired pair exists, and in particular lies on the left-hand side and lies on the right-hand side of .

Proposition 5.2.

There exist and such that

| (5.6) |

with where is defined to be any value of such that is minimized.

Proof of Proposition 5.2.

Lemma 5.2.

We have

Proof.

See Appendix A.2. ∎

Second, we obtain the asymptotic behavior of as follows.

Lemma 5.3.

-

(1)

For every fixed , .

-

(2)

For every fixed , .

Proof.

See Appendix A.3. ∎

We are now ready to show the existence of . While this is shown analytically below, numerical plots of and in Figure 4 of Section 8 are certainly helpful in understanding the proof.

First we recall the definition of as in Lemma 5.1(1) and show that we can focus on smaller than . To see this, for any , Lemmas 5.1(1) and 5.2 and the positivity of imply that uniformly; this together with (5.4) implies that the function starts at (at ) and increases monotonically as while never touching the x-axis.

Let us now start at and consider decreasing the value of toward . Fix . By Lemma 5.3(1), there exists a global minimizer . In addition, for any , and hence , which also means that a local minimum is attained at (hence ).

Regarding the function on , we have the following three properties:

-

(1)

It decreases as decreases. Indeed, , which is positive for by Lemma 5.1(1). Hence for any , .

-

(2)

It is continuous thanks to the continuity of with respect to both variables.

-

(3)

Lemma 5.3(2) implies, for sufficiently small , that .

By these three properties, there must exist such that (5.6) holds and . Note that while is unique by construction, may not be unique in the sense that the infimum of can possibly be attained at multiple values. Moreover, by construction, and (because is negative for ). This completes the proof of Proposition 5.2. ∎

6. Verification of optimality

With the obtained in Proposition 5.2, we shall show that the -policy is optimal. By substituting in (4.4),

| (6.1) | ||||

| (6.2) |

Substituting this and by the definition of as in (4.6),

| (6.3) |

The function can be recovered by (4.3). By Lemma 4.1, we can also write

| (6.4) | ||||

Notice that (6.2), (6.3) and (6.4) hold also for by (3.4) and because for .

We state the main result of the paper for the case .

Theorem 6.1.

Remark 6.1.

6.1. Proof of Theorem 6.1

In order to show Theorem 6.1, it suffices to show that the function as in (6.4) satisfies the QVI (quasi-variational inequalities):

| (6.5) | ||||

see [11, 12] and also the proof of verification for the no fixed cost case as in Section 7. Here one needs to apply an appropriate version of the Itô formula since the value function is not smooth enough at to apply the usual version. For the case is of unbounded variation, because is differentiable with absolutely continuous first derivatives, we apply Theorem 71 of Protter [44], which is written in terms of the semimartingale local time (for its definition and existence, see page 216 of [44]). For the case of bounded variation, we apply the Meyer-Itô formula as in Theorem 70 of [44]. In this case, because is again of bounded variation, the semimartingale local time process is identically zero. Hence the extra term due to the discontinuity of vanishes and has no effects after all.

We first show the first part of the QVI, which can be shown easily thanks to the martingale property as reviewed in Section 3.1.2 of the scale function and the fact that is linear below .

Lemma 6.1.

-

(1)

for ,

-

(2)

for .

Proof.

(1) First, by (3.18), for any . On the other hand, as in the proof of Lemma 4.5 of [20], . Hence in view of (6.4), (1) is proved.

(2) Because for and by (5.3) and (6.1),

This is positive by Assumption 2.1(2) and Lemma 5.1(1), recalling that .

∎

The second part of the QVI is given as follows.

Proposition 6.1.

For every , we have . This inequality holds with equality for .

It is clear that showing Proposition 6.1 is equivalent to showing

| (6.6) |

Toward this end, we use the following lemma.

Lemma 6.2.

The following holds true.

-

(1)

.

-

(2)

is decreasing on .

-

(3)

.

Proof.

For , Proposition 6.1 holds immediately by Lemma 6.2(1) and because . For , it also holds by Lemma 6.2(2).

Proof of Proposition 6.1 for .

The proof for is the most difficult part of the verification. However, thanks to Lemmas 6.1(1) and 6.2(3), we can follow the same arguments as the proof of Theorem 1(iii) of Benkherouf and Bensoussan [9], where they show that (6.6) holds also for .

While they assume that the demand process is a mixture of a Wiener process and a compound Poisson process, only a slight (mostly notational) modification is needed to show that it is also valid for a general spectrally positive Lévy demand process. Here we illustrate briefly how this is so.

The proof of Theorem 1 of [9] uses a contradiction argument to show the claim. The first step is to assume that (6.6) does not hold so that is finite, and then construct the points such that the following properties hold:

-

(1)

such that [or equivalently in their paper] attains local minima at and and local maximum at ,

-

(2)

is the smallest minimizer of over ,

-

(3)

is the smallest maximizer of over ,

-

(4)

is the smallest minimizer of over ,

-

(5)

, and for all .

The only requirements for these are that is continuously differentiable on (which holds by Remark 6.1) and it tends to (which is verified in Lemma 6.2). Hence, we can construct these points with the same properties in exactly the same way.

Using constructed above and the IDE

| (6.7) |

satisfied on (which holds by Lemma 6.1(1)), a contradiction is derived. In particular, if (resp. if ), it is derived by comparing (6.7) for and (resp. and ). Hence, in doing so, the only difference with [9] is that the form of the generator is more general (and contains the cutoff function inside the integral).

However, local maxima/minima are attained at , and hence the first derivatives vanish and the cutoff function in the integral of vanishes. In turn, for ,

Consequently, we end up having the same expression, and the same results hold.

∎

7. The Case with No Fixed Ordering Costs

In this section, we study a variant of the problem with . Here, we widen the set of admissible policies to accommodate also the processes containing diffuse increments; we consider the set of given by a nondecreasing, right-continuous, and -adapted process such that . With , , the problem is to compute the total costs:

for some and to obtain an admissible policy that minimizes it, if such a policy exists. For , we again impose Assumption 2.1. In addition, an admissible policy is such that and are both well-defined and finite -a.s.

From the results in the previous section, the optimal policy is easily conjectured. We have seen, for the case , that the -policy is optimal for some . In addition, because are such that and, for all , , the distance between and is expected to shrink as decreases. Hence it is a reasonable conjecture for the case that a barrier policy with the lower barrier is optimal. We shall show that it is indeed so.

|

. . |

Define, for ,

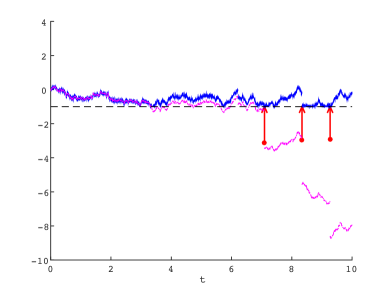

The corresponding inventory process becomes a reflected Lévy process that always stays at or above . Figure 3 shows sample paths of these processes using the same realization of as in Figure 2; differently from Figure 2, the process can increase both continuously and discontinuously.

Our objective is to show that for all where

| (7.1) |

and is the set of all admissible policies.

The fluctuation theory of the reflected Lévy process has been well-studied as in, e.g., [3, 42]. The expression (7.1) can be computed easily via the scale function.

Lemma 7.1.

-

(1)

We have for any .

-

(2)

We have for any .

Proof.

See Appendix A.4. ∎

Combining the two results above, we can now write

| (7.2) | ||||

which holds also for by (3.4). Here, by Lemma 4.1, (5.3), and the definition of such that ,

For the rest of this section, we show the following.

Theorem 7.1.

The barrier policy is optimal and the value function is given by as in (7.2).

Remark 7.1.

Recently, Baurdoux and Yamazaki [6] study an extension of this problem where the control is two-sided and in particular show the optimality of a double barrier policy when is convex. In another direction, Hernández-Hernández et al. [25] consider a version under the condition that is absolutely continuous with respect to the Lévy measure.

Remark 3.1 guarantees that is continuous on and is (resp. ) for the case is of bounded (resp. unbounded) variation. It turns out that our choice of guarantees the smoothness of (7.2) (or equivalently (7.3)) at (that is even stronger than the case as in Section 5).

Because (5.2) gives , we have

| (7.4) |

Lemma 7.2.

The function is (resp. ) for the case is of bounded (resp. unbounded) variation.

Proof.

For the proof of Theorem 7.1, we shall show the following variational inequalities: for all ,

| (7.5) | ||||

Here, by Lemma 7.2 and because the integral part is well-defined and finite by Assumption 3.1 and the linearity of below , we confirm that makes sense for all .

Lemma 7.3.

-

(1)

for ,

-

(2)

for .

Proof.

Lemma 7.4.

We have for every and for every .

Proof.

Recall (7.4). When , it is clear that . When , because for every , the claim holds in view of the definition of as in (4.5).

Now suppose . Using as in (3.15), we write

where the last inequality holds because, for a.e. where , whereas, for a.e. where , .

Finally, because for a.e. ,

This completes the proof.

∎

7.1. Proof of Theorem 7.1

Lemmas 7.3 and 7.4 show the variational inequalities (7.5). We shall now give the rest of the proof of Theorem 7.1.

Lemma 7.5.

For any , .

Proof.

See Appendix A.5. ∎

Now, we are ready to prove Theorem 7.1. Fix any admissible policy such that is finite. Using the standard martingale arguments as in Section 5 of [40] (recall the smoothness of as in Lemma 7.2), we obtain

| (7.6) |

where we define .

By Lemma 7.5, we have that . Hence, the strong Markov property gives

| (7.7) |

Here, for all ,

where the first inequality holds because is decreasing and increasing by Assumption 2.1(2) and . Hence, integration by parts gives

This together with (7.6) and (7.7) gives a bound:

On the right hand side, the finiteness of can be shown in the same way as the proof for the finiteness of in Lemma 7.5. Hence, by taking , the claim holds.

8. Numerical Results

In this section, we conduct numerical experiments using, for , the spectrally negative Lévy process in the -family introduced by [28]. The following definition is due to Definition 4 of [28].

Definition 8.1.

A spectrally negative Lévy process is said to be in the -family if (3.1) is written

for some , , , , and the beta function .

The -family is a subclass of the meromorphic Lévy process and hence the scale function can be computed by the formula (3.22). This process has been receiving much attention recently due to many analytical properties that make many computations possible. In particular, it can approximate tempered stable (or CGMY) processes and is hence suitable to model the price of an asset. As we discussed in the introduction, the demand is a main determinant of the price; hence it is a reasonable choice for our inventory process .

We suppose , , , and . With this specification, the process has infinitely many jumps in a finite time interval (and has paths of bounded variation), which is not covered in the framework of [12]. We consider and so as to study both the bounded and unbounded variation cases.

We let , and, for the inventory cost, we consider the quadratic case , . By straightforward calculation, , ,

and for

where we define for , and .

8.1. Results

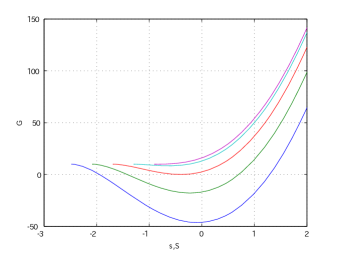

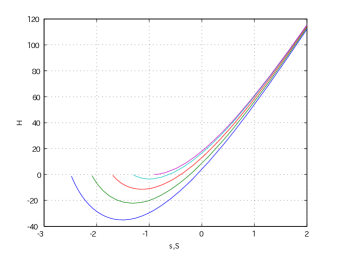

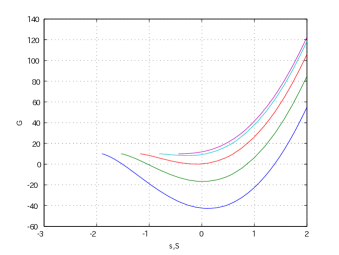

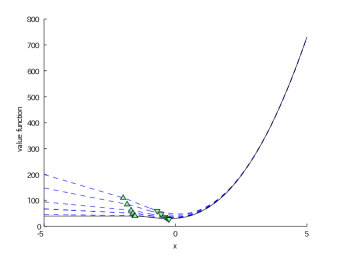

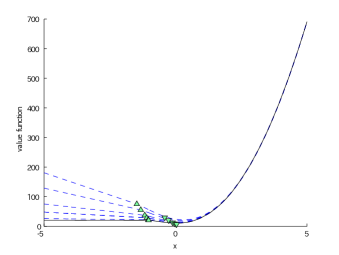

For the case , the first step is to obtain the pair as in Proposition 5.2. As is discussed in Section 5.2, starting at and as we decrease the value of , we arrive at the desired that makes the function tangent to the x-axis at . Figure 4 plots and for . The lines in red correspond to the desired curve; the starting point becomes and the point touching zero becomes . Here we assume . As it turns out, appears to be strictly convex in this example. Moreover, as is already clear analytically, it starts at zero (for the unbounded variation case) or below zero (for the bounded variation case). Hence has a unique global minimum over , which is confirmed to be increasing in (see the item (1) in the discussion following Lemma 5.3). Hence, we apply a bisection method to obtain and .

|

|

| unbounded variation case () | |

|

|

| bounded variation case () | |

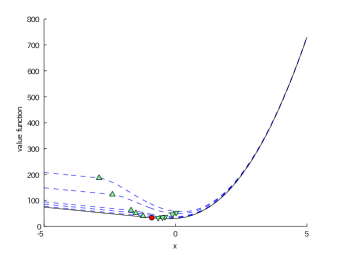

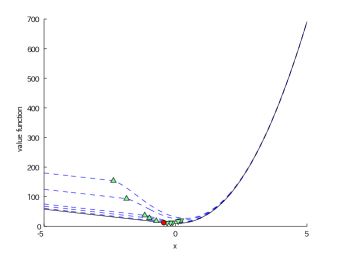

With computed instantaneously using the technique addressed above, the value function is computed using (6.3). In Figure 5, we first plot it against the initial value for the unit proportional cost with the common fixed cost . The triangle signs indicate the points and for each choice of . It can be confirmed that the value function is increasing in uniformly in . Moreover, tends to increase as decreases. This is consistent with our intuition that one is more eager to replenish as the ordering cost decreases. We also see in this plot that also tends to increase as decreases.

|

|

| unbounded variation case () | bounded variation case () |

|

|

| unbounded variation case () | bounded variation case () |

We now consider decreasing the value of the fixed cost and confirm the convergence to the case as studied in Section 7. In Figure 6, we plot the value functions for (dotted) along with that for the no-fixed cost case given by (7.2) (solid) with the common proportional cost . The circle signs indicate . We can confirm that, as the value of decreases, the value function converges decreasingly to the one for . The convergence of the points to is also confirmed. Regarding the smoothness of the value function, it appears indeed that it is continuous at for the case of bounded variation while it is differentiable for the case of unbounded variation. Furthermore, the smaller the value of is, the smoother the value function gets. This is consistent with Lemma 7.2 where the smoothness holds in a higher order for .

9. Conclusions

We have studied the inventory control problem for a general spectrally positive Lévy demand process. We considered both the cases with and without fixed ordering costs. By using the recently developed fluctuation theories of spectrally one-sided Lévy processes, the problem can be solved efficiently and the value function can be written concisely via the scale function. Our numerical experiments show that the computation is fast and accurate; this is a powerful alternative to the existing IDE-based numerical methods, which tend to be difficult when the underlying process has jumps of infinite activity/variation.

Our approach can potentially be used in other inventory models, and in particular it is of great interest to incorporate, e.g., lead time, perishability and lost sales. The demand for realistic inventory models can potentially contribute to the theory of scale functions. As insurance problems contributed to the development of the theory of scale functions (see [1, 35]), it is expected that pursuing realistic inventory systems will open up new questions on the theory of scale functions and Lévy processes.

Appendix A Proofs

A.1. Proof of Lemma 4.1

The first claim holds by integration by parts. For the second claim, we have

as desired.

A.2. Proof of Lemma 5.2

We shall show the equation for for because it is clear that for . The equation for , , is then immediate because it is simply a derivative of .

A.3. Proof of Lemma 5.3

(1) By Lemmas 5.1(3) and 5.2, for any ,

The claim is now immediate because, for and sufficiently large ,

where the inequality holds because is positive and monotonically increasing.

(2) Similarly, if we choose , we have, for any ,

By Lemma 5.1(1) and (2) and because , we have, for any and sufficiently small ,

A.4. Proof of Lemma 7.1

(1) As in the proof of Theorem 1 of [3], if we define for ,

with . From Exercise 8.5 of [31] and l’Hôpital’s rule, as . This together with the monotone convergence theorem gives

By shifting the initial position of , the proof is complete.

(2) By Theorem 1(i) of [42], for every

Thanks to Assumption 2.1(1), the boundedness of in view of (3.6) and because is increasing, the integrand of the right hand side is bounded uniformly in by an integrable function. Hence, the dominated convergence theorem along with the convergence (by Exercise 8.5 of [31]) yields the result for . The same result holds for . Because both are finite by Assumption 2.1(1), after summing up these, we have the desired results.

A.5. Proof of Lemma 7.5

We shall first prove that

| (A.1) |

where and are defined as in (3.5). We have

where, in the second equality, we used dominated convergence for the limit of the first expectation (because is bounded on ) and monotone convergence for the second expectation.

By the definition of as in (7.1) and Assumption 2.1(1), grows at most polynomially as while it is linear below . To see the former, if is the reflected Lévy process that starts at , it is easy to verify that for all and a.s.

Hence, for (A.1), it suffices to show

| (A.2) |

for any . The latter holds trivially because does not have positive jumps (and hence on if ) and , for , by Theorem 3.12 of [31].

By Assumption 3.1, we can take a sufficiently small such that and where is the Laplace exponent of the dual process . Then, as in page 78 of [31], is a martingale. This means that, for any fixed , , is a nonnegative supermartingale. This together with Fatou’s lemma gives, upon taking , .

Now, for any sufficiently large , we have , , and hence

By taking , we see that the first claim of (A.2) holds and consequently (A.1) holds.

Here, we notice that this limit is well-defined and finite. Indeed, for any , by the arguments similar to the above, there exist a sufficiently small (such that ) and large , such that, for any , . Hence,

Similarly, we can show that there exists some such that . By Assumption 2.1(1), is indeed well-defined and finite.

Acknowledgements

The author thanks Alain Bensoussan as well as the anonymous referees for their insightful comments that help improve the presentation of this paper. K. Yamazaki is in part supported by MEXT KAKENHI grant numbers 22710143 and 26800092, JSPS KAKENHI grant number 23310103, the Inamori foundation research grant, and the Kansai University subsidy for supporting young scholars 2014.

References

- [1] H. Albrecher, J.-F. Renaud, and X. Zhou. A Lévy insurance risk process with tax. J. Appl. Probab., 45(2):293–586, 2008.

- [2] S. Asmussen, F. Avram, and M. R. Pistorius. Russian and American put options under exponential phase-type Lévy models. Stochastic Process. Appl., 109(1):79–111, 2004.

- [3] F. Avram, Z. Palmowski, and M. R. Pistorius. On the optimal dividend problem for a spectrally negative Lévy process. Ann. Appl. Probab., 17(1):156–180, 2007.

- [4] E. Baurdoux and A. E. Kyprianou. The McKean stochastic game driven by a spectrally negative Lévy process. Electron. J. Probab., 13:no. 8, 173–197, 2008.

- [5] E. J. Baurdoux, A. E. Kyprianou, and J. C. Pardo. The Gapeev-Kühn stochastic game driven by a spectrally positive Lévy process. Stochastic Process. Appl., 121(6):1266–1289, 2008.

- [6] E. J. Baurdoux and K. Yamazaki. Optimality of doubly reflected Lévy processes in singular control. Stochastic Process. Appl., 125(7):2727–2751, 2015.

- [7] E. Bayraktar, A. E. Kyprianou, and K. Yamazaki. On optimal dividends in the dual model. Astin Bull., 43(3):359–372, 2013.

- [8] E. Bayraktar, A. E. Kyprianou, and K. Yamazaki. Optimal dividends in the dual model under transaction costs. Insurance: Math. Econom., 54:133–143, 2014.

- [9] L. Benkherouf and A. Bensoussan. Optimality of an policy with compound Poisson and diffusion demands: a quasi-variational inequalities approach. SIAM J. Control Optim., 48(2):756–762, 2009.

- [10] A. Bensoussan. Dynamic programming and inventory control, volume 3 of Studies in Probability, Optimization and Statistics. IOS Press, Amsterdam, 2011.

- [11] A. Bensoussan and J.-L. Lions. Impulse control and quasi-variational inequalities. John Wiley & Sons Ltd, 1984.

- [12] A. Bensoussan, R. H. Liu, and S. P. Sethi. Optimality of an policy with compound Poisson and diffusion demands: a quasi-variational inequalities approach. SIAM J. Control Optim., 44(5):1650–1676 (electronic), 2005.

- [13] A. Bensoussan and C. S. Tapiero. Impulsive control in management: prospects and applications. J. Optim. Theory Appl., 37(4):419–442, 1982.

- [14] J. Bertoin. Lévy processes, volume 121 of Cambridge Tracts in Mathematics. Cambridge University Press, Cambridge, 1996.

- [15] J. Bertoin. Exponential decay and ergodicity of completely asymmetric Lévy processes in a finite interval. Ann. Appl. Probab., 7(1):156–169, 1997.

- [16] P. Carr, H. Geman, D. Madan, and M. Yor. The fine structure of asset returns: An empirical investigation. J. Bus., 75(2):305–333, 2002.

- [17] T. Chan, A. E. Kyprianou, and M. Savov. Smoothness of scale functions for spectrally negative Lévy processes. Probab. Theory Relat. Fields, 150:691–708, 2011.

- [18] R. A. Doney. Fluctuation theory for Lévy processes, volume 1897 of Lecture Notes in Mathematics. Springer, Berlin, 2007.

- [19] M. Egami, T. Leung, and K. Yamazaki. Default swap games driven by spectrally negative Lévy processes. Stochastic Process. Appl., 123(2):347–384, 2013.

- [20] M. Egami and K. Yamazaki. Precautional measures for credit risk management in jump models. Stochastics, 85(1):111–143, 2013.

- [21] M. Egami and K. Yamazaki. On the continuous and smooth fit principle for optimal stopping problems in spectrally negative Lévy models. Adv. in Appl. Probab., 46(1):139–167, 2014.

- [22] M. Egami and K. Yamazaki. Phase-type fitting of scale functions for spectrally negative Lévy processes. J. Comput. Appl. Math., 264:1–22, 2014.

- [23] D. J. Emery. Exit problem for a spectrally positive process. Adv. in Appl. Probab., 5:498–520, 1973.

- [24] X. Guo and G. Wu. Smooth fit principle for impulse control of mutidimensional diffusion processes. SIAM J. Control Optim., 48(2):594–617, 2009.

- [25] D. Hernández-Hernández, J.-L. Pérez, and K. Yamazaki. Optimality of refraction strategies for spectrally negative Lévy processes. SIAM J. Control Optim., Forthcoming.

- [26] D. Hernández-Hernández and K. Yamazaki. Games of singular control and stopping driven by spectrally one-sided Lévy processes. Stochastic Process. Appl., 125(1):1–38, 2015.

- [27] F. Hubalek and E. Kyprianou. Old and new examples of scale functions for spectrally negative Lévy processes. In Seminar on Stochastic Analysis, Random Fields and Applications VI, volume 63 of Progr. Probab., pages 119–145. Birkhäuser/Springer Basel AG, Basel, 2011.

- [28] A. Kuznetsov. Wiener-Hopf factorization and distribution of extrema for a family of Lévy processes. Ann. Appl. Probab., 2009.

- [29] A. Kuznetsov, A. Kyprianou, and V. Rivero. The theory of scale functions for spectrally negative Lévy processes. Springer Lecture Notes in Mathematics, 2061:97–186, 2013.

- [30] A. Kuznetsov, A. E. Kyprianou, and J. C. Pardo. Meromorphic Lévy processes and their fluctuation identities. Ann. Appl. Probab., 22(3):1101–1135, 2012.

- [31] A. E. Kyprianou. Introductory lectures on fluctuations of Lévy processes with applications. Universitext. Springer-Verlag, Berlin, 2006.

- [32] A. E. Kyprianou and C. Ott. A capped optimal stopping problem for the maximum process. Acta Appl. Math., 129(147–174), 2014.

- [33] A. E. Kyprianou and Z. Palmowski. Distributional study of de Finetti’s dividend problem for a general Lévy insurance risk process. J. Appl. Probab., 44(2):428–443, 2007.

- [34] A. E. Kyprianou and B. A. Surya. Principles of smooth and continuous fit in the determination of endogenous bankruptcy levels. Finance Stoch., 11(1):131–152, 2007.

- [35] A. E. Kyprianou and X. Zhou. General tax structures and the Lévy insurance risk model. J. Appl. Probab., 46(4):1146–1156, 2009.

- [36] T. Leung and K. Yamazaki. American step-up and step-down credit default swaps under levy models. Quant. Finance, 13(1):137–157, 2013.

- [37] R. L. Loeffen. On optimality of the barrier strategy in de Finetti’s dividend problem for spectrally negative Lévy processes. Ann. Appl. Probab., 18(5):1669–1680, 2008.

- [38] R. L. Loeffen. An optimal dividends problem with a terminal value for spectrally negative Lévy processes with a completely monotone jump density. J. Appl. Probab., 46(1):85–98, 2009.

- [39] R. L. Loeffen. An optimal dividends problem with transaction costs for spectrally negative Lévy processes. Insurance Math. Econom., 45(1):41–48, 2009.

- [40] B. Øksendal and A. Sulem. Applied stochastic control of jump diffusions. Universitext. Springer, Berlin, second edition, 2007.

- [41] C. Ott. Optimal stopping problems for the maximum process with upper and lower caps. Ann. Appl. Probab., 23(6):2327–2356, 2013.

- [42] M. R. Pistorius. On exit and ergodicity of the spectrally one-sided Lévy process reflected at its infimum. J. Theoret. Probab., 17(1):183–220, 2004.

- [43] E. Presman and S. P. Sethi. Inventory models with continuous and Poisson demands and discounted and average costs. Prod. Oper. Manag., 15(2):279–293, 2006.

- [44] P. E. Protter. Stochastic integration and differential equations, volume 21 of Stochastic Modelling and Applied Probability. Springer-Verlag, Berlin, 2005. Second edition. Version 2.1, Corrected third printing.

- [45] V. Suprun. Problem of destruction and resolvent of terminating process with independent increments. Ukrainian Math. J., 28:39–45, 1976.

- [46] B. A. Surya and K. Yamazaki. Optimal capital structure with scale effects under spectrally negative Lévy models. Int. J. Theor. Appl. Finance, 17(2):1450013, 2014.

- [47] K. Yamazaki. Contraction options and optimal multiple-stopping in spectrally negative Lévy models. Appl. Math. Optim., 72(1):147–185, 2014.

- [48] K. Yamazaki. Cash management and control band policies for spectrally one-sided Lévy processes. Proceedings of the TMU Finance Workshop 2014, forthcoming.

- [49] C. Yin and Y. Wen. Optimal dividend problem with a terminal value for spectrally positive Lévy processes. Insurance Math. Econom., 53(3):769—773, 2013.