Toward Optimal Stratification for Stratified Monte-Carlo Integration

Abstract

We consider the problem of adaptive stratified sampling for Monte Carlo integration of a noisy function, given a finite budget of noisy evaluations to the function. We tackle in this paper the problem of adapting to the function at the same time the number of samples into each stratum and the partition itself. More precisely, it is interesting to refine the partition of the domain in area where the noise to the function, or where the variations of the function, are very heterogeneous. On the other hand, having a (too) refined stratification is not optimal. Indeed, the more refined the stratification, the more difficult it is to adjust the allocation of the samples to the stratification, i.e. sample more points where the noise or variations of the function are larger. We provide in this paper an algorithm that selects online, among a large class of partitions, the partition that provides the optimal trade-off, and allocates the samples almost optimally on this partition.

1 Introduction

The objective of this paper is to provide an efficient strategy for integrating a noisy function . The learner can sample times the function. If it samples the function at a time in a point of the domain that it can choose to its convenience, it obtains the noisy sample , where is drawn independently at random from some distribution , where is a probability distribution that depends on .

If the variations of the function are known to the learner, an efficient strategy is to sample more points in parts of the domain where the variations of are larger. This intuition is explained more formally in the setting of Stratified Sampling (see e.g. (Rubinstein and Kroese, 2008)).

More precisely, assume that the domain is divided in regions (according to the usual terminology of stratified sampling, we refer to these regions as strata) that form a partition of . It is optimal (for an oracle) to allocate a number of points in each stratum proportional to the measure of the stratum times a quantity depending of the variations of in the stratum (see Subsection 5.5 of (Rubinstein and Kroese, 2008)). We refer to this strategy as optimal oracle strategy for partition .

The problem is that the variations of the function in each stratum of are unknown to the learner.

In the papers (Etoré and Jourdain, 2010; Grover, 2009; Carpentier and Munos, 2011a), the authors expose the problem of, at the same time, estimating the variations of in each stratum, and allocating the samples optimally among the strata according to these estimates.

Up to some variation in efficiency or assumptions, these papers provide learners that are indeed able to learn about the variations of the function and allocate optimally the samples in the strata, up to a negligible term. However, all these papers make explicit in the theoretical bounds, or at least intuitively, the existence of a natural trade-off in terms of the refinement of the partition. The more refined the partition (especially if it gets more refined where variations of are larger), the smaller the variance of the estimate outputted by the optimal oracle strategy. However, the larger the error of an adaptive strategy with respect to this optimal oracle strategy, since the more strata there are, the harder it is to adapt to each stratum.

It is thus important to adapt also the partition to the function, and refine more the strata where variations of the function are larger, while at the same time limiting the number of strata.

As a matter of fact, a good partition of the domain is such that, inside each stratum, the values taken by are as homogeneous as possible (see Subsection 5.5 of (Rubinstein and Kroese, 2008)), while at the same time the number of strata is not too large.

There are some recent papers on how to stratify efficiently the space, e.g. (Glasserman et al., 1999; Kawai, 2010; Etoré et al., 2011; Carpentier and Munos, 2012a, b). More specifically, in the recent paper (Etoré et al., 2011), the authors propose an algorithm for performing this task online and efficiently. They do not provide proofs of convergence for their algorithm, but they give some properties of optimal stratified estimate when the number of strata goes to infinity, notably convergence results under the optimal allocation. They also give some intuitions on how to split efficiently the strata. Having an asymptotic vision of this problem prevents them however from giving clear directions on how exactly to adapt the strata, as well as from providing theoretical guarantees. In paper (Carpentier and Munos, 2012a), the authors propose to stratify the domain according to some preliminary knowledge on the class of smoothness of the function. They however fix the partition before sampling and thus do not consider online adaptation of the partition to the function. Finally, although considering online adaptation of the partition to the function, the paper (Carpentier and Munos, 2012b) considers the specific and somehow very different111In this setting where the function is noiseless and very regular, efficient strategies share ideas with quasi Monte-Carlo strategies, and the number of strata should be almost equal to the budget . setting where the noise to the function is null, and where is differentiable according to .

Contributions:

We consider in this paper the problem of designing efficiently and according to the function a partition of the space, and of allocating the samples efficiently on this partition. More precisely, our aim is to build an algorithm that allocates the samples almost in an oracle way on the best possible partition (adaptive to the function , i.e. that solves the trade-off that we named before) in a large class of partitions. We consider in this paper the class of partition to be the set of partitions defined by a hierarchical partitioning of the domain (as for instance what was considered in (bubeck2008online) for function optimization).

-

•

We provide new, to the best of our knowledge, ideas for sampling a domain very homogeneously, i.e. such that the samples are well scattered. The sampling schemes we introduce share ideas with low discrepancy schemes (see e.g. (Niederreiter, 2010)), and provide some theoretic guarantees for their efficiency.

-

•

We provide an algorithm, called Monte-Carlo Upper Lower Confidence band. We prove that it manages to at the same time select an optimal partition of the hierarchical partitioning and then to allocate the samples in this partition almost as an oracle would do. More precisely, we prove that its pseudo-risk is smaller, up to a constant, than the pseudo-risk of MC-UCB on any partition of the hierarchical partitioning.

The rest of the paper is organised as follows. In Section 2 we formalise the problem and introduce the notations used throughout the paper. We also remind the problem independent bound for algorithm MC-UCB. Section 3 presents algorithm MC-ULCB, and its bound on the pseudo-risk. After a technical part on notations, we introduce what we call Balanced Sampling Scheme (BSS) and a variant of it, BSS-A. These are sampling schemes for allocating samples in a random yet almost low discrepancy way, on a domain. Algorithm MC-ULCB that we present afterwards relies heavily on them. We also discuss the results, and finally conclude the paper.

2 Preliminaries

2.1 The function

Consider a noisy function .

In this definition, is the domain on which the learner can choose in which point to sample, and is a space on which the noise to the function is defined. We define for any the distribution of noise conditional to as . We also define a finite measure on corresponding to a algebra whose sets belong to . Without loss of generality, we assume that ( is a probability measure).

The objective of the learner is to sample the domain in order to build an efficient estimate of the integral of the noisy function according to the measure , that is to say . The learner can sample sequentially the function times, and observe noisy samples. When sampling the function at time in , it observes a noisy sample . The noise conditional to is independent of the previous samples .

For any point , define

We state the following Assumption on the function

Assumption 1

We assume that both and are bounded in absolute value by a constant . Let (if , set ). We assume that such that ,

, and

Assumption 1 means that the variations coming from the noise in , although potentially unbounded, are not too large222This assumption implies that the variations induced by the noise are sub-Gaussian. It is actually slightly stronger than the usual sub-Gaussian assumption. Nevertheless, e.g. bounded random variables and Gaussian random variables satisfy it.. We believe that it is rather general. In particular, it is satisfied if is bounded, or also for e.g. a bounded function perturbed by an additive, heterocedastic, (sub-)Gaussian noise.

2.2 Notations for a hierarchical partitioning

The strategies that we are going to consider for integration are allowed to choose where to sample the domain. In order to do that, the strategies we consider will partition the domain into strata and sample randomly in the strata. In theory the stratification is at the discretion of the strategy and can be arbitrary. However in practice, we will consider strategies that rely on given hierarchical partitioning.

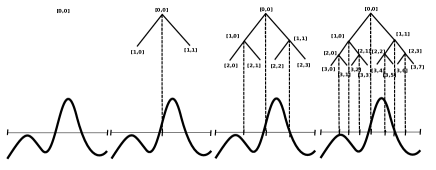

Define a dyadic hierarchical partitioning of the domain . More precisely, we consider a set of partitions of at every depth : for any integer , is partitioned into a set of strata , where . This partitioning can be represented by a dyadic tree structure, where each stratum corresponds to a node of the tree (indexed by its depth and index ). Each node has children nodes and . In addition, the strata of the children form a sub-partition of the parents stratum . The root of the tree corresponds to the whole domain .

We state the following assumption on the measurability and on the measure of any stratum of the hierarchical partitioning.

Assumption 2

, the stratum is measurable according to the algebra on which the probability measure is defined.

We write the measure of stratum , i.e. . We also assume that the hierarchical partitioning is such that all the strata of a given depth have same measure, i.e. .

Assumption 3

, the children strata of are such that .

If for example , a hierarchical partitioning that satisfies the previous assumptions with the Lebesgue measure is illustrated in Figure 1.

We write mean and variance of stratum the mean and variance of a sample of the function , collected in the point , where is drawn at random according to conditioned to stratum . We write

the mean and

the variance (we remind that and are defined in Assumption 1).

2.3 Pseudo-performance of an algorithm and optimal static strategies

We denote by an algorithm that allocates the budget and returns a partition included in the hierarchical partitioning of the domain. In each node of , algorithm allocates uniformly random samples. We write these samples, and we write the empirical mean built with these samples. We estimate the integral of on by . This is the estimate returned by the algorithm.

If is fixed as well as the number of samples in each stratum, and if the samples are independent and chosen uniformly according to the measure restricted to each stratum , we have

and also

where the expectations and variance are computed with respect to the samples collected in the strata.

For a given algorithm , we denote by pseudo-risk the quantity

| (1) |

This measure of performance is discussed more in depths in papers (Grover, 2009; Carpentier and Munos, 2011b). In particular, paper (Carpentier and Munos, 2011b) links it with the mean squared error.

Note that if, for a given partition , an algorithm would have access the variances of the strata in , it could allocate the budget in order to minimise the pseudo-risk, by choosing to pick in each stratum (up to rounding issues) samples. The pseudo risk for this oracle strategy is then

| (2) |

where we write . We also refer, in the sequel, as optimal allocation (for a partition ), to . Even when the optimal allocation is not realizable because of rounding issues, it can still be used as a benchmark since the quantity is a lower bound on the variance of the estimate outputted by any oracle strategy.

2.4 Main result for algorithm MC-UCB and point of comparison

Let us consider a fixed partition of the domain, and write for the number of strata it contains. We first recall (and slightly adapt) one of the main results of paper (Carpentier and Munos, 2011b) (Theorem 2). It provides a result on the pseudo-risk of an algorithm called MC-UCB. This algorithm takes some parameters linked to upper bounds on the variability of the function333It is needed that the function is bounded and that the noise to the function is sub-Gaussian., a small probability , and the partition . MC-UCB builds, for each stratum in the fixed444It is very important to note that the partition is fixed for this algorithm and that it only adapts the allocation to the function. partition , an upper confidence band (UCB) on it’s standard deviation, and allocates the samples proportionnal to the measure of each stratum times this UCB. Its pseudo-risk is bounded in high probability by . This theorem holds also in our setting. The fact that the measure is finite together with Assumptions 2 and 1 imply that the distribution of the samples obtained by sampling in the strata are sub-Gaussian (as a bounded mixture of sub-Gaussian random variables). We remind and slightly improve this theorem.

Theorem 1

The bound in this Theorem is slightly sharper than in the original paper. The (improved) proof is in the Supplementary Material, see Appendix C.2

We will use in the sequel the bound in this Theorem as a benchmark for the efficiency of any algorithm that adapts the partition. The aim will be to construct a strategy whose pseudo-regret is almost as small as the minimum of this bound over a large class of partitions (e.g. the partitions defined by the hierarchical partitioning). In paper (Carpentier and Munos, 2012a), it was proved that this bound is minimax optimal which makes it a sensible benchmark.

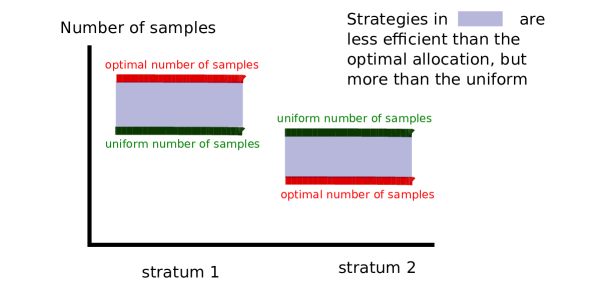

The bound in this Theorem depends on two terms. The first, , which is the oracle optimal variance of the estimate on partition , decreases with the number of strata, and more specifically if the strata are “well-shaped” (i.e. more strata where the variations of and are larger). On the other hand, the second term, , increases when the partition is more refined. There are however two extremal situations for this term, leading to two very different behaviours with the number of strata. If the strata have all the same measure where is the number of strata in partition , then . Now if the partition is very localised (i.e. exponential decrease of the measure of the strata), then whatever the number of strata, is of order , and the number of strata has no more influence than a constant.

These two facts enlighten the importance of adapting the shape of the partition to the function by having potentially strata of heterogeneous measure.

3 Algorithm MC-ULCB

3.1 Additional definitions for algorithm MC-ULCB

Let . We first define where and are chosen such that they satisfy Assumption 1. Set also for any , .

Let be a node of the hierarchical partitioning.

Assume that the children of node have received at least samples (and stratum has received at least samples). The standard deviations (for ) are computed using the first samples only:

| (3) |

where is the -th sample in stratum . We also introduce another estimate for the standard deviation , namely , which is computed with the first samples in stratum (and not with the first samples as ):

| (4) |

We use this estimate for technical purposes only.

We now define by induction the value for any stratum . We initialise the when there is enough points i.e. at least points in stratum , by . Assume that is defined. Whenever there are at least points in strata for , we define the value for (and the other) as

| (5) | |||

where , . It is either a (proportional) upper, or a (proportional) lower confidence bound on . It is a (proportional) upper confidence bound for the stratum that has the smallest empirical standard deviation, and a (proportional) lower confidence bound for the other. If the quantities and are too close, we set the same value to both sub-strata. The quantities are key elements in algorithm MC-ULCB, and they account for the name of the algorithm (Monte Carlo Upper Lower Confidence Bound).

Additional to that, we define the technical quantities , and .

3.2 Sampling Schemes

The algorithm MC-ULCB that we will consider in the next Subsection works by updating a partition of the domain, refining it more where it seems necessary (i.e. where the algorithms detects that or have large variations). In order to do that, the algorithm needs to split some nodes in their children nodes. We thus need guarantees on the number of samples in each child node and , when there are samples in . More precisely, we would like to have, up to rounding issues, samples in each child node.

The problem is that usual sampling procedures do not guarantee that. In particular, if one chooses the naive idea for sampling stratum , i.e. collect samples independently at random according to , then there is no guarantees on the exact numbers of samples in and . However, we would like that the sampling scheme that we use conserve the nice properties of sampling according to , i.e. that the empirical mean built on the samples remains an unbiased estimate of and that it has a variance smaller than or equal to .

This is one of the reasons why we need alternative sampling schemes

The Balanced Sampling Scheme

We first describe what we call Balanced Sampling Scheme (BSS).

We design this sampling scheme in order to be able to divide at any time each stratum, so that at any time, the number of points in each sub-stratum is proportional to the measure of the sub-stratum (up to one sample of difference).

The proposed methodology is the following recursive procedure. Consider a stratum , indexed by node and that has already been sampled according to the BSS times. It has two children in the hierarchical partitioning, namely and . If they have been sampled a different number of times, e.g. , we choose the child that contains the smallest number of points, e.g. , and apply BSS to this child. If the number of points in each of these nodes is equal, i.e. , we choose uniformly at random one of these two children, and apply BSS to this child. Then we iterate the procedure in this node, until for some depth and node , one has . Then when , sample randomly a point in stratum , according to . This provides the th sample.

We provide in Figure 2 the pseudo-code of this recursive procedure.

BSS if then return BSS else if then return BSS else return endif

An immediate property is that if stratum is sampled times according to the BSS, any descendant stratum of is such that .

We also provide the following Lemma providing properties of an estimate of the empirical mean when sampling with the BSS.

Lemma 1

Let be a stratum where one samples times according to the BSS. Then the empirical mean of the samples is such that

The proof of this Lemma is in the Supplementary Material (Appendix B). This Lemma also holds for the children nodes of (for a descendant , it holds with samples, since the procedure is recursive).

A variant of the BSS: the BSS-A procedure

We now define a variant of the BSS: the BSS-A sampling scheme.

The reason why we need also this variant is that it is crucial, if two children of a node have obviously very different variances, to allocate more samples in the node that has higher variance. Indeed, the number of samples that one allocates to a node is directly linked to the amount of exploration that one can do of this node, and thus to the local refinement of the partitioning taht one may consider. But it is also necessary to be careful and have an allocation that is more efficient than uniform allocation, as it is not sure that it is a good idea to split the parent-node. In order to do that, we construct a scheme that uses upper confidence bounds for the less variating node, and lower confidence bounds for the most variating node: we use the that were defined for this purpose. We assume that these are defined in some sub-tree of the hierarchical partitioning, and undefined outside. Using such an allocation is naturally less efficient than the optimal oracle allocation, but however more efficient than uniform allocation. We illustrate this concept in Figure 3 and provide the pseudo-code in Figure 4.

BSS-A if then return BSS-A else return endif

3.3 Algorithm Monte-Carlo Upper-Lower Confidence Bound

We describe now the algorithm Monte-Carlo Upper-Lower Confidence Bound. It is decomposed in two main phases, a first Exploration Phase, and then an Exploitation Phase.

The Exploration Phase uses Upper and Lower Confidence bounds for allocating correctly the samples. During this phase, we update an Exploration partition, that we write , and that is included in the hierarchical partitioning. When, in a stratum , there are more than samples (also if the standard deviation of teh stratum is large enough), we update by setting : we divide in its two children strata, and compute the corresponding to the children strata. The points are then allocated in the strata according to : a point is allocated in stratum if . All the points are allocated inside each stratum according to the BSS procedure.

The Exploration Phase stops at time , when every node is such that . We write the tree that is composed of all the nodes in and of their ancestors. The algorithm selects in this tree a partition, that we write , and that is an empirical minimiser (over all partitions in ) of the upper bound on the regret of algorithm MC-UCB.

Finally, we perform the Exploitation Phase which is very similar to launching algorithm MC-UCB on . We pull the samples in the strata of according to the BSS-A sampling scheme (described in Figure 4). We compute the final estimate of as a stratified estimate with respect to the deepest partition of , i.e. :

| (6) |

where is the empirical mean of all the samples in stratum .

We now provide the pseudo-code of algorithm MC-ULCB in Figure 5.

Input: , and . Initialization: Pull samples by BSS(). Set . Exploration Phase: while do Take a sample in BSS(). if then Compute and end if end while Select such that Exploitation Phase: for do Compute for any Choose a leaf such that Pick a point according to BSS-A() end for Output:

3.4 Main result

We are now going to provide the main result for the pseudo-risk of algorithm MC-ULCB.

Theorem 2

The proof of this result is in the Supplementary Material (Appendix D).

A first remark on this result is that even the first inequality (i.e. ) is not trivial since the algorithm does not sample at random according to in the strata , but according the BSS-A. It was necessary to do that since in order to select wisely , one should have explored the tree , and thus it was necessary to allocate the points in order to allow splitting of the nodes and adequate exploration.

Assume that is lower bounded, e.g. the function is noisy (i.e. the function is not almost surely equal to ). Then a second remark is that the second term in the final bound, namely , is negligible when compared to the second term, namely . Indeed, since is bounded by Assumption 1 by , we know that is smaller than , which implies that for one of the partitions that realises this minimum, we have , which is negligible when compared to and thus in particular .

3.5 Discussion

Algorithm MC-ULCB does almost as well as MC-UCB on the best partition: The result in Theorem 2 states that algorithm MC-ULCB selects adaptively a partition that is almost a minimiser of the upper bound on the pseudo-risk of algorithm MC-UCB. It then allocates almost optimally the samples in this partition. Its upper bound on the regret is thus smaller, up to additional multiplicative term contained in , than the upper bound on the regret of algorithm MC-UCB launched on an optimal partition of the hierarchical partitioning. The issue is that is bigger than the constant for MC-UCB. More precisely, we have , where is a constant depending of and (see bound on in Theorem 2). This additional dependency in is not an artifact of the proof and appears since we perform some model selection for selecting the partition . We do not know whether it is possible or not to get rid of it. Note however that a factors already appears in the bound of MC-UCB, and that the question of whether it is or not needed remains open.

The final partition : Algorithm MC-ULCB refines more the partition in parts of the domain where splitting a stratum in a sub-partition is such that is large. Note that this corresponds, by definition of the , to parts of the domain where and have large variations. We do not refine the partition in regions of the domain where this is not the case, since it is more efficient to have also as few strata as possible.

The sampling schemes: The key-points in this paper are the sampling schemes. Indeed, we construct and use a sampling technique, the BSS, that is such that the samples are collected in a way that reminds low discrepancy sampling schemes666Although the samples are chosen randomly, the sampling scheme is such that we know in a deterministic and exact way the number of samples in each not too small part of the domain. on the domain, and provide an estimate such that its variance is smaller than the one of crude Monte-Carlo. We also build another sampling scheme, BSS-A. This sampling scheme ensures that, with high probability, if two children strata have very different variances, then the one with higher variance is more sampled. At the same time, it ensures that if finally the decision of splitting a stratum is not taken, then the allocation in the stratum is still better than or as efficient as random allocation according to restricted to the stratum.

Evaluation of the precision of the estimate and confidence intervals: An important question that one can ask here is on the prssibility of constructing a confidence interval around the estimate that we obtain. What we would suggest in this case is to upper bound the pseudo-risk of the estimate by , and construct a confidence interval considering this as a bound on the variance or the estimate, using e.g. Bennett’s inequality. If e.g. the noise is symmetric, then the pseudo-risk equals the mean squared error, and the confidence interval is valid, and in particular asymptotically valid (see (Carpentier and Munos, 2011b)). Also it is less wide (up to a negligible term) than the smallest valid confidence interval on the best (oracle) stratified estimate on the hierarchical partitioning (and then in particular than the one for the crude MC estimate). Indeed, the oracle variance of such estimate is which is by definition of larger or equal up to a negligible term to , and this equals up to a negligible term to the upper bound on the pseudo-risk we used to construct the confidence interval.

Conclusion

In this paper, we presented an algorithm, MC-ULCB, that aims at integrating a function in an efficient way.

MC-ULCB improves the performances of Deep-MC-UCB and returns an estimate whose pseudo-risk is smaller, up to a constant, than the minimal pseudo-risk of MC-UCB run on any partition of the hierarchical partitioning. The algorithm adapts the partition to the function and noise on it, i.e. it refines more the domain where and have large variations. We believe that this result is interesting since the class of hierarchical partitioning is very rich and can approximate many partition.

Acknoledgements:

The research leading to these results has received funding from the European Community’s Seventh Framework Programme (FP7/2007-2013) under grant agreement n° 270327.

References

- Carpentier and Munos (2011a) A. Carpentier and R. Munos. Finite-time analysis of stratified sampling for monte carlo. In In Neural Information Processing Systems (NIPS), 2011a.

- Carpentier and Munos (2012a) A. Carpentier and R. Munos. Minimax number of strata for online stratified sampling given noisy samples. Algorithmic Learning Theory, 2012a.

- Carpentier and Munos (2012b) A. Carpentier and R. Munos. Adaptive stratified sampling for monte-carlo integration of differentiable functions. In Advances in Neural Information Processing Systems 25, 2012b.

- Carpentier and Munos (2011b) A. Carpentier and R. Munos. Finite-time analysis of stratified sampling for monte carlo. Technical report, INRIA-00636924, 2011b.

- Etoré and Jourdain (2010) Pierre Etoré and Benjamin Jourdain. Adaptive optimal allocation in stratified sampling methods. Methodol. Comput. Appl. Probab., 12(3):335–360, September 2010.

- Etoré et al. (2011) Pierre Etoré, Gersende Fort, Benjamin Jourdain, and Éric Moulines. On adaptive stratification. Ann. Oper. Res., 2011. to appear.

- Glasserman et al. (1999) P. Glasserman, P. Heidelberger, and P. Shahabuddin. Asymptotically optimal importance sampling and stratification for pricing path-dependent options. Mathematical Finance, 9(2):117–152, 1999.

- Grover (2009) V. Grover. Active learning and its application to heteroscedastic problems. Department of Computing Science, Univ. of Alberta, MSc thesis, 2009.

- Kawai (2010) R. Kawai. Asymptotically optimal allocation of stratified sampling with adaptive variance reduction by strata. ACM Transactions on Modeling and Computer Simulation (TOMACS), 20(2):1–17, 2010. ISSN 1049-3301.

- Niederreiter (2010) H. Niederreiter. Quasi-Monte Carlo Methods. Wiley Online Library, 2010.

- Rubinstein and Kroese (2008) R.Y. Rubinstein and D.P. Kroese. Simulation and the Monte Carlo method. Wiley-interscience, 2008. ISBN 0470177942.

[

Supplementary Material for paper: ”Toward Optimal Stratification for Stratified Monte-Carlo Integration”

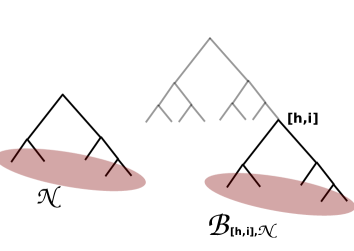

We first introduce the following natation. We write , where is a cut of a dyadic tree, the sub-partition given by the leafs of the tree issued from and with leaves (we branch partition on leaves ). We illustrate this in Figure 6.

Similarly and by a slight abuse of notations, we write for any integer the sub-tree as the sub-tree ussyed from node and extended until depth .

Appendix A Numerical experiments

We consider the pricing problem of an Asian option introduced in (Glasserman et al., 1999) and later considered in (Kawai, 2010; Etoré and Jourdain, 2010). This uses a Black-Scholes model with strike and maturity . Let be a Brownian motion. The discounted payoff of the Asian option is defined as a function of , by:

where , , and are constants.

We want to estimate the price by Monte-Carlo simulations (by sampling on ). In order to reduce the variance of the estimated price, we stratify as suggested in (Glasserman et al., 1999; Kawai, 2010) the space of according to the quantiles of , i.e. the quantiles of a normal distribution . In other words, we re-write where is the quantile that corresponds to . In this context, the noise comes from the directions along which we do not stratify, namely . After having sampled according to the algorithm for stratified Monte-Carlo (e.g. MC-ULCB), we simulate the rest of the Brownian motion by a Brownian Bridge (concretely, we discretize this Brownian motion in order to be able to simulate it in values). We choose the same numerical values as (Kawai, 2010): , , , and . We choose a strike .

By studying the range of the , we set the (meta-)parameters of the algorithm MC-ULCB to and (the other parameters adjust automatically with these two meta-parameters). Our main competitor is the algorithm described in (Etoré et al., 2011), to which we refer to as A-SSAA, and which also perform adaptive allocation and stratification.

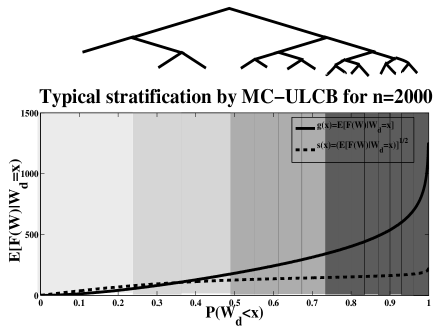

We first observe the behaviour of MC-ULCB with a budget of . On a typical run, algorithm MC-ULCB divides the domain in approximately strata that form partition , and the partition is more refined where and vary more. We illustrate this in Figure 7.

In Figure 1, we display the (averaged over runs) performances of algorithms MC-ULCB, A-SSAA, and MC-UCB (launched on some partitions in hypercubes of same measure). Note first that trough the performances of MC-UCB launched on partitions with varying number of strata, we observe the optimal number of strata increases with . We observe that MC-ULCB is more efficient than algorithm MC-UCB launched on any of these partitions in strata. This is not very surprising since we only consider MC-UCB launched on partitions where all strata have the same size, i.e. these partitions are not adapted to the function . We would probably observe slightly better results for MC-UCB if we launched it on an oracle partition with respect to , but such a partition is not easy to build, even when the function is known. Also, MC-ULCB is more efficient than A-SSAA, and that for any sample size. It is not very surprising since the price model for Asian option happens to verify Assumption 1, which is more restrictive than the assumptions made in paper (Etoré et al., 2011). This Assumption is used to tune the algorithm. In paper (Etoré et al., 2011), since they do not make this sub-Gaussian assumption, they can not calibrate the length of the exploration phase with respect to the properties of the distribution, and thus fit the exploration/exploitation to the problem.

| Budget | |||

|---|---|---|---|

| Crude MC | |||

| MC-UCB, | |||

| MC-UCB, | |||

| MC-UCB, | |||

| MC-UCB, | |||

| A-SSAA | |||

| MC-ULCB |

Appendix B Proof of Lemma 1

Assume that stratum has been sampled times according to the BSS. Let be the (uniquely defined) decomposition in basis of , i.e. and . This implies by Assumption 3 and by definition of , that . We denote by the set of the samples in stratum .

By construction of the BSS, there are at most two and at least one element of in each stratum of . For all , we write the first sample in stratum . Conditionally to the number of samples, each of these samples is pulled randomly in stratum according to .

Let us now consider the largest such that . Let us consider . By construction of the BSS, conditionally to the knowledge that there is a re-numeration of the samples such that (and thus conditionally only to the number of samples since the fact that there is a re-numeration such that follows deterministically from the budget ), there are at most two and at least one element of in each stratum of . We note the first sample. By construction of the BSS and conditionally to the number of samples, each of these samples is pulled randomly in stratum according to .

We can continue this induction for every such that . We have, at the end of the induction, relabeled (trough the relabeling that we presented) every sample (in ) by . We know that conditional to the number of samples, , and , and also that these relabeled samples are all independent of each other (although the relabeling of each sample is random and is not independent of the other samples).

The empirical mean on stratum thus satisfies

Since by construction , the empirical estimate of the mean thus satisfies

Note now that the variance of this estimate is such that

Appendix C Preliminary results

C.1 An interesting large probability event

Lemma 2

For a stratum of the hierarchical partition, write the samples collected by BSS in stratum (or by BSS in a stratum of smaller depth). Consider the event

| (7) |

where and . Then .

Note also that for , we have

-

Proof

Probability of the event

Let be a stratum of the hierarchical partitioning such that and . Let . By definition of the BSS, we know that for , sample , conditionally to the other samples, is sampled uniformly inside the strata that contain no samples, and independent of the other samples.

Using the results from Lemma 13, we know that with probability , the estimate of the standard deviation computed with the first samples satisfies

By the definition of , we know that there are less than strata in the hierarchical partitioning of depth smaller than . Because of the definition of , we have .

Characterisation of the strata of depth bigger than

Consider a node of depth . As both and are bounded by (see Assumption 1), then

As , we have . From that we deduce that for ,

C.2 Rate for the algorithm MC-UCB

We first prove the following result.

Proposition 1

- Proof

Step 1. Properties of the algorithm. For a node , we first recall the definition of used in the MC-UCB algorithm

Using the definition of and the fact that if node is in , then , it follows that, on

| (8) |

Let be the time at which an arm is pulled for the last time, that is . Note that there is at least one arm such that this happens as . Since at arm is chosen, then for any other arm , we have

| (9) |

From Equation 28 and , and also since by construction of the algorithm , we obtain on

| (10) |

Furthermore, since , then on

| (11) |

Combining Equations 29–11, we obtain on

Summing over all such that the previous Equation is satisfied, i.e. such that , on both sides, we obtain on

This implies

| (12) |

Step 2. Lower bound. Equation 12 implies

on , since (as ). Finally, if , we obtain on the following bound

| (13) |

Step 2bis. Lower bound on the number of pulls. By using Equation 13 and the fact that one gets

where .

This concludes the proof.

Appendix D Proof of Theorem 2

D.1 Some preliminary bounds

Let . Note that .

Let be a stratum that is explored during the Exploration Phase, and split in its to children.

This implies that . By definition, for

where is the complementary of in . Note that the three indicators used in the definition of form a partition of the domain.

Lemma 3

If on a node has two children and that have been explored by the algorithm, then .

-

Proof

Note first that (by definition of and , and also because of the properties of the empirical variance).

The result follows from the definition of as for , .

Lemma 4

For any stratum , if of depth smaller than is defined then on

-

Proof

The proof is done by induction. Note first that . The result is thus satisfied for node .

Assume that the property of Lemma 4 is satisfied for a given on .

Assume that the children of this node are opened. This implies that , i.e.

(14)

Let . Note first that (by definition of and , and also because of the properties of the empirical variance), and that on , as a node is open only if there are enough samples in it, i.e. if there are more than samples. This together with Equation 14 implies that

| (15) |

as . In the same way

| (16) |

Assume that . Then . It implies that, by Equation 17

| (19) |

Assume that . Then . It implies that, by by Equation 18

| (20) |

From Equations 17 and 19, from the definition of , and from the fact that , we deduce that

and finish the induction for the left-hand-side on .

In the same way, by combining Equations 18 and 20, we finish the induction for the right-hand-side on .

Corollary 1

For any stratum , if is defined then on

-

Proof

This is straightforward from Lemma 4, by the definition of and as .

Lemma 5

For any stratum , if is defined then on

- Proof

Let be a node.

Assume that the children of this node are explored at time . This implies that , and then by Lemma 4, on , (as ).

as . This implies as that

| (21) |

D.2 Study of the Exploration Phase

Lemma 6

On , the Exploration phase ends at and all the nodes of partition are such that and .

-

Proof

Let be the time at which the exploration phase ends (if it does not end, write ).

One needs to pull a node in at a time if and only if

We thus know that the last time stratum is sampled during the Exploration Phase (and thus at the end of the Exploration Phase)

If stratum is not sampled during the Exploration Phase after having been opened, then

Note that by Lemma 5, on . From that we deduce that

and from that together with the fact that we only sample a node at time if , we deduce the second part of the Lemma, i.e. that on , .

Note now that : it is straightforward by Lemma 3. This directly leads to:

This directly implies that , which leads to the desired result, i.e. that the Exploration Phase ends before all the budget has been used. This implies that on , .

Lemma 7

Let be a node such that and also such that, for all its parents, .

Then on , at the end of the Exploration phase phase, node is open, i.e. , which also implies .

-

Proof

The result is proven by induction. Assume that there is a node that satisfies the Assumptions of Lemma 7. Then . Note first that after the Initialization, i.e. at the time when , i.e. when the decision of opening or not the node is made, we have on that

The node is thus opened on .

Assume now that an ancestor of node is open. By Lemma 1, we now that on

By Lemma 7, we know that at the end of the Exploration Phase, with on , we have . As , we have by using the previous result that . By the definition of and the fact that , we know also that , which implies that . This, together with the fact that on , implies that node is open and split in its too children.

We have thus proved the result of the Lemma by induction.

Lemma 8

Let be the end of the Exploration Phase, and let . Then on ,

-

Proof

Let be the end of the exploration phase.

D.3 Characterization of the

The algorithm selects a partition such that

with and .

Note that for every partition , as all the nodes of are such that by the structure of the algorithm. One thus has on , for any partition included in , that

because by construction every node of has depth smaller than .

We thus have for the selected partition that, on ,

| (24) |

Let be the set of all nodes such that all their ancestors are such that . This implies because is positive, and because that

| (25) |

where is the minimum over all the partitions in the entire hierarchical partitioning.

Lemma 7 states that on , . This implies that

| (26) |

D.4 Study of the Exploitation phase

Lemma 9

At the end of the Exploitation phase (end of the algorithm) one has

where .

- Proof

Step 1. Lower Bound in each node Let us first note that by Lemma 6, we know that on , at the end of the Exploration Phase, we have . There is still a budget of at least pulls left for the Exploitation phase.Note first that as a node is opened only when there are points in it, so .

Step 2. Properties of the algorithm. We first recall the definition of used in the MC-UCB algorithm for a node

Using the definition of together with the fact that, by construction, at a time of the Exploration Phase, , it follows that, on

| (28) |

Let be the time at which an arm is pulled for the last time, that is . Note that there is at least one arm such that this happens as by Lemma 6. Since at arm is chosen, then for any other arm , we have

| (29) |

From Equation 28 and , we obtain on

| (30) |

Furthermore, since , then on

| (31) |

Combining Equations 29–31, we obtain on that if at least one sample is collected from stratum after the Exploration Phase, then

| (32) |

Step 3: The Exploration Phase has not deteriorate the performances of the algorithm.

If , then samples are pulled from after the Exploration Phase. By summing over these nodes on Equation 32, we obtain that, on , for any ,

| (33) |

where . The passage from line to line come from the fact that .

Lemma 8 states that on , for all

Note also that by Step 1, on , . We thus have from these two results that on , for any ,

| (34) |

By combining Equations 33 and Equation 34, we obtain for every that on

where we use the fact that and for for passing from line to line . We finally have

| (35) |

where .

Step 4. Lower bound on the number of pulls. By using Equation 35 and the fact that one gets

Lemma 10

Let . Let be an open grand-child of , and and be its two children. Then

where .

- Proof

We consider such that : otherwise it has no grand-children.

By Lemma 8, we know that for any grand-child of , we have . Note that at the moment of a node’s opening, the number of points in the node is smaller than . As the Exploration stops sampling in a stratum when , we know that at the end of the Exploration Phase, we have .

We prove by induction that for any grand-child of , and that for its two children and , we have .

By Lemma 4, we know that as , we have on

By combining this result with Lemma 9 and also with the definition of , we have on

because by definition, , and also because .

Let and be the two children of . Note first that at the end of the Exploration Phase, by Lemma 6, we have , where . By Lemma 3, we know that . This means that as , then then a sample will be pulled again in one of the two nodes after the Exploration Phase. Assume without risk of generality that it is node that is pulled.

Note also that . By summing, we get that

We thus have

If a sample is also collected from stratum , then the same result applies also for . Otherwise, it means that , and as one sample is collected in , we have , so we have in any case

The recursion continues in the same way for any child of such that (otherwise it has no children). Indeed, the budget in the terminal nodes of the Exploration partition does satisfy this property.

Lemma 11

Let be a node of . Let be the sub-partition of nodes in that cover the domain of . One has on :

-

Proof

The result of the Lemma follows by induction.

Let us consider a node , and let be the sub-partition of nodes in that cover the domain of .

Let and be two nodes of that have the same father-node . Assume without risk of generality that .

Lemma 10 states that

As , we have by the previous Equation

In the same way, we obtain

(36) and

(37) From that we deduce that if , then .

If , this implies that , and the last sample is pulled at random between the two strata. From that we deduce that , in the same way that in Lemma 1.

Assume now that . Note now that on , because of the definition of , we have on

By combining that with Equation 36, we get on

which leads to

| (38) |

In the same way, as on

we have

| (39) |

We deduce from Equations 38 and 39 that on

From that, together with the fact that and , we deduce because of variance properties that

and note that as and are terminal nodes of , then correspond to the variance of the stratified estimate on these nodes.

In the same way, by induction, for any child of that is in , we also have

which is the desired result in the specific case where .

D.5 Regret of the algorithm

Appendix E Large deviation inequalities for independent sub-Gaussian random variables

We first state Bernstein inequality for large deviations of independent random variables around their mean.

Lemma 12

Let be independent random variables of mean and of variance . Assume that there exists such that for any , for any , it holds that . Then with probability

-

Proof

If the assumptions of Lemma 12 are satisfied, then

By setting we obtain

By an union bound we obtain

This means that with probability ,

We also state the following Lemma on large deviations for the variance of independent random variables.

Lemma 13

Let be independent random variables of mean and of variance . Assume that there exists such that for any , for any , it holds that and also .

Let be the variance of a sample chosen uniformly at random among the distributions, and the corresponding empirical variance. Then with probability ,

| (40) |

-

Proof

By decomposing the estimate of the empirical variance in bias and variance, we obtain with probability

We then have by the definition of that with probability

(41)

If the assumptions of Lemma 13 are satisfied, we have with probability

If we take we obtain with probability

| (42) |

By a union bound we get with probability that

This means that with probability ,

| (43) |

Finally, by combining Equations 41 and 43 with Lemma 12, we obtain with probability

when and because .

This implies with probability that

On the other hand, we have also with probability

Finally, we have with probability

| (44) |

]