Three-dimensional Brownian motion and the golden ratio rule

Abstract

Let be a transient diffusion process in with the diffusion coefficient and the scale function such that as , let denote its running minimum for , and let denote the time of its ultimate minimum . Setting we show that the stopping time

minimizes over all stopping times of (with finite mean) where the optimal boundary can be characterized as the minimal solution to

staying strictly above the curve for . In particular, when is the radial part of three-dimensional Brownian motion, we find that

where is the golden ratio. The derived results are applied to problems of optimal trading in the presence of bubbles where we show that the golden ratio rule offers a rigorous optimality argument for the choice of the well-known golden retracement in technical analysis of asset prices.

doi:

10.1214/12-AAP859keywords:

[class=AMS] .keywords:

., and

1 Introduction

The golden ratio has fascinated people of diverse interests for at least 2400 years (see, e.g., Li ). In mathematics (and the arts) two quantities and are in the golden ratio if the ratio of the sum of the quantities to the larger quantity is equal to the ratio of the larger quantity to the smaller quantity . This amounts to setting and solving which yields Apart from being abundant in nature, and finding diverse applications ranging from architecture to music, the golden ratio has also found more recent uses in technical analysis of asset prices (in strategies such as Fibonacci retracement representing an ad-hoc method for determining support and resistance levels). Despite its universal presence and canonical role in diverse applied areas, we are not aware of any more exact connections between the golden ratio and stochastic processes (including any proofs of optimality in particular).

One of the aims of the present paper is to disclose the appearance of the golden ratio in an optimal stopping strategy related to the radial part of three-dimensional Brownian motion. More specifically, denoting the radial part by it is well known that is transient in the sense that as . After starting at some , the ultimate minimum of will therefore be attained at some time that is not predictable through the sequential observation of (in the sense that it is only revealed at the end of time). The question we are addressing is to determine a (predictable) stopping time of that is as close as possible to . We answer this question by showing that the time at which the excursion of away from the running minimum and the running minimum itself form the golden ratio is as close as possible to in a normalized mean deviation sense. We consider this problem by embedding it into transient Bessel processes of dimension and in this context we derive similar optimal stopping rules. We also disclose further/deeper extensions of these results to transient diffusion processes. The relevance of these questions in financial applications is motivated by the problem of optimal trading in the presence of bubbles. In this context we show that the golden ratio rule offers a rigorous optimality argument for the choice of the well-known golden retracement in technical analysis of asset prices. To our knowledge this is the first time that such an argument has been found/given in the literature.

The problem considered in the present paper belongs to the class of optimal prediction problems (within optimal stopping). Similar optimal prediction problems have been studied in recent years by many authors (see, e.g., BDP , Coh , DP-1 , DP-2 , DP-3 , DPS , ET , GPS , NS , Ped-2 , Sh-3 , Sh-4 , Ur ). Once the “unknown” future is projected to the “known” present, we find that the resulting optimal stopping problem takes a novel integral form that has not been studied before. The appearance of the minimum process in this context makes the problem related to optimal stopping problems for the maximum process that were initially studied and solved in important special cases of diffusion processes in DS , DSS and Ja . The general solution to problems of this kind was derived in the form of the maximality principle in Pe-1 ; see also Section 13 and Chapter V in PS and the other references therein. More recent contributions and studies of related problems include CHO , Ga-1 , Ga-2 , GZ , Ho , Ob-1 , Ob-2 , Ped-1 . Close three-dimensional relatives of these problems also appear in the recent papers DGM and Zi where the problems were effectively solved by guessing and finding the optimal stopping boundary in a closed form. The maximality principle has been extended to three-dimensional problems in the recent paper Pe-4 .

Although the structure of the present problem is similar to some of these problems, it turns out that none of these results is applicable in the present setting. Governed by these particular features in this paper we show how the problem can be solved when (i) no closed-form solution for the candidate stopping boundary is available and (ii) the loss function takes an integral form where the integrand is a functional of both the process and its running minimum . This is done by extending the arguments associated with the maximality principle to the setting of the present problem and disclosing the general form of the solution that is valid in all particular cases. The key novel ingredient revealed in the solution is the replacement of the diagonal and its role in the maximality principle by a nonlinear curve in the two-dimensional state space of and . We believe that this methodology is of general interest and the arguments developed in the proof should be applicable in similar two/multi-dimensional integral settings.

2 Optimal prediction problem

1. We consider a nonnegative diffusion process solving

| (1) |

where and are continuous functions satisfying (4) and (5) below, and is a standard Brownian motion. By we denote the probability measure under which the process starts at . Recalling that the scale function of is given by

| (2) |

and the speed measure of is given by

| (3) |

we assume that the following conditions are satisfied:

| (4) | |||||

| (5) |

From (4) we read that is a transient diffusion process in the sense that -a.s. as , and from (5) we read that is an entrance boundary point for in the sense that the process could start at but will never return to it (implying also that will never visit after starting at ).

2. The main example we have in mind is the -dimensional Bessel process solving

| (6) |

where . Recalling that the scale function is determined up to an affine transformation we can choose the scale function (2) and hence the speed measure (3) to read

| (7) | |||||

| (8) |

for . It is well known that when one can realize as the radial part of -dimensional standard Brownian motion. Similar interpretations of (6) are also valid when (with an addition of the local time at zero) and but is not transient in these cases (but recurrent), and hence the problem considered below will have a trivial solution. Other examples of (1) are obtained by composing Bessel processes solving (6) with strictly decreasing and smooth functions. This is of interest in financial applications and will be discussed below. There are also many other examples of transient diffusion processes solving (1) that are not related to Bessel processes.

3. To formulate the problem to be studied below consider the diffusion process solving (1), and introduce its running minimum process by setting

| (9) |

for . Due to the facts that is transient (converging to ) and is an entrance boundary point for , we see that the ultimate infimum is attained at some random time in the sense that

| (10) |

with -probability one for given and fixed (the case being trivial and therefore excluded). It is well known that is unique up to a set of -probability zero (cf. Wi , Theorem 2.4). The random time is clearly unknown at any given time and cannot be detected through sequential observations of the sample path for . In many applied situations of this kind, we want to devise sequential strategies which will enable us to come as “close” as possible to . Most notably, the main example we have in mind is the problem of optimal trading in the presence of bubbles to be addressed below. In mathematical terms this amounts to finding a stopping time of that is as “close” as possible to . A first step toward this goal is provided by the following lemma. We recall that stopping times of refer to stopping times with respect to the natural filtration of that is defined by for .

Lemma 1

We have

| (11) |

for all stopping (random) times of .

The identity is well known (see, e.g., PS , page 450) and can be derived by noting that

for all stopping (random) times of as claimed.

4. Taking on both sides in (11) yields a nontrivial measure of error (from to ) as long as for given and fixed. The latter condition, however, may not always be fulfilled. For example, when is a transient Bessel process of dimension it is known (see Sh , Lemma 1) that as . Hence we see that if and only if or equivalently . It is clear from (11), however, that the pointwise minimization of the Euclidean distance on the left-hand side is equivalent to the pointwise minimization of the integral on the right-hand side. To preserve the generality we therefore “normalize” on the left-hand side by subtracting from it. After taking on both sides of the resulting identity, we obtain

| (13) |

for all stopping times of (for which the right-hand side is well defined). The optimal prediction problem therefore becomes

| (14) |

where the infimum is taken over all stopping times of (with finite mean) and is given and fixed. Note that the problem (14) is equivalent to the problem of minimizing over all stopping times of (with finite mean) whenever . To tackle the problem (14) we first focus on the right-hand side in (13) above.

Lemma 2

We have

| (15) |

for all stopping times of (with finite mean) and all .

Using a well-known argument (see, e.g., PS , page 450), we find that

for any stopping time of (with finite mean) and any given and fixed. Setting and recalling that , we find by the Markov property that

for . To compute the latter probability we recall that is a continuous local martingale and note that if and only if where . This shows that the set coincides with the set which in turn can be expressed as where . Taking we see that the continuous local martingale is bounded above by and bounded below by with under . It follows therefore that is a uniformly integrable martingale and hence by the optional sampling theorem we find that

upon using that -a.s. on . Combining (2) with the previous conclusions we obtain

| (19) |

for in . From (2) and (19) we see that

| (20) |

for all and (for the underlying three-dimensional law, see CFS , Theorem A). Inserting this expression back into (2) we obtain (15) and the proof is complete.

5. From (13) and (15) we see that the problem (14) is equivalent to

| (21) |

where the infimum is taken over all stopping times of (with finite mean) and is given and fixed. Passing from the initial diffusion process to the scaled diffusion process we see that there is no loss of generality in assuming that in (1) or equivalently that for (with -a.s. as ). Note that the time of the ultimate minimum is the same for both and since is strictly increasing. Note also that is a stopping time of if and only if is a stopping time of . To keep the track of the general formulas throughout we will continue with considering the general case (when is not necessarily zero and is not necessarily the identity function). This problem will be tackled in the next section below.

6. For future reference we recall that the infinitesimal generator of equals

| (22) |

for . Throughout we denote and set for in . It is well known that

| (23) |

for in . The Green function of is given by

If is a measurable function, then it is well known that

| (25) |

for in . This identity holds in the sense that if one of the integrals exists, so does the other one, and they are equal.

3 Optimal stopping problem

It was shown in the previous section that the optimal prediction problem (14) is equivalent to the optimal stopping problem (21). The purpose of this section is to present the solution to the latter problem. Using the fact that the two problems are equivalent this also leads to the solution of the former problem.

In the setting of (1)–(5) consider the optimal stopping problem (21). This problem is two-dimensional and the underlying Markov process equals . Setting for enables to start at under for in , and we will denote the resulting probability measure on the canonical space by . Thus under the canonical process starts at . The problem (21) then extends as follows:

| (26) |

for in where the infimum is taken over all stopping times of (with finite mean). In addition to and from (1) and (2) above, let us set

| (27) |

for in . The main result of this section may then be stated as follows.

Theorem 3

The optimal stopping time in problem (26) is given by

| (28) |

where the optimal boundary can be characterized as the minimal solution to

| (29) |

staying strictly above the curve for (in the sense that if the minimal solution does not exist, then there is no optimal stopping time). The value function is given by

| (30) |

for and for with .

1. It is evident from the integrand in (26) that the excursions of away from the running minimum play a key role in the analysis of the problem. In particular, recalling definition (27), we see from (26) that the process can never be optimally stopped in the set where we let denote the state space of the process . Indeed, if is given and fixed, then the first exit time of from a sufficiently small ball with the centre at (on which is strictly negative) will produce a value strictly smaller than (the value corresponding to stopping at once). Defining

| (31) |

for we see that for and for whenever in are given and fixed. Note that the mapping is increasing and continuous as well as that for with and . This shows that . Note in particular that contains the diagonal in the state space.

2. Before we formalize further conclusions, let us recall that the general theory of optimal stopping for Markov processes (see PS , Chapter 1) implies that the continuation set in the problem (26) equals , and the stopping set equals . It means that the first entry time of into is optimal in problem (26) whenever well defined. It follows therefore that is contained in , and the central question becomes to determine the remainder of the set . Since -a.s. as it follows that -a.s. as so that the integrand in (26) becomes strictly positive eventually, and this reduces the incentive to continue (given also that the “favorable” set becomes more and more distant). This indicates that there should exist a point at or above which the process should be optimally stopped under where in are given and fixed. This yields the following candidate:

| (32) |

for an optimal stopping time in (26) where the function is to be determined.

3. Free-boundary problem. To compute the value function and determine the optimal function , we are led to formulate the free-boundary problem

| (33) | |||||

| (34) | |||||

| (35) | |||||

| (36) |

for , where is the infinitesimal generator of given in (22) above. For the rationale and further details regarding free-boundary problems of this kind, we refer to PS , Section 13, and the references therein (we note, in addition, that the condition of normal reflection (34) dates back to GSG ).

4. Nonlinear differential equation. To solve the free-boundary problem (33)–(36) consider the stopping time defined in (32) and (formally) the resulting function

| (37) |

for in given and fixed. Applying the strong Markov property of at and using (23)–(25), we find that

| (38) |

It follows from (38) that

Using (35) and (36) we find after dividing and multiplying with that

| (40) |

Moreover, it is easily seen by (2) that

| (41) | |||

| (42) |

Inserting this back into (38) and using (2) and (25), we conclude that

| (43) |

for in . Finally, using (34) we find that

for . Recalling that is contained in , we see that there is no restriction to assume that each candidate function solving (3) satisfies for all . In addition we will also show below that all points belong to for so that (at least in principle) there would be no restriction to assume that each candidate function solving (3) also satisfies for all . These candidate functions will be referred to as admissible. We will also see below, however, that solutions to (3) “starting” at play a crucial role in finding/describing the solution.

Summarizing the preceding considerations, we can conclude that to each candidate function solving (3), there corresponds the function (43) solving the free-boundary problem (33)–(36) as is easily verified by direct calculation. Note, however, that this function does not necessarily admit the stochastic representation (37) (even though it was formally derived from this representation). The central question then becomes how to select the optimal boundary among all admissible candidates solving (3). To answer this question we will invoke the subharmonic characterization of the value function (see PS , Chapter 1) for the three-dimensional Markov process where for . Fuller details of this argument will become clearer as we progress below. It should be noted that among all admissible candidate functions solving (3) only the optimal boundary will have the power of securing the stochastic representation (37) for the corresponding function (43). This is a subtle point showing the full power of the method (as well as disclosing limitations of the optimal stopping problem itself).

5. The minimal solution. Motivated by the previous question we note from (43) that is decreasing over admissible solutions to (3). This suggests to select the candidate function among admissible solutions to (3) that is as far as possible from . The subharmonic characterization of the value function suggests to proceed in the opposite direction, and this is the lead that we will follow in the sequel.

To address the existence and uniqueness of solutions to (3), denote the right-hand side of (3) by . From the general theory of nonlinear differential equations, we know that if the direction field is (locally) continuous and (locally) Lipschitz in the second variable, then the equation (3) admits a (locally) unique solution. For instance, this will be the case if, along a (local) continuity of , we also have a (local) continuity of . In particular, we see from the structure of that equation (3) admits a (locally) unique solution whenever is (locally) continuously differentiable. It is important to realize that the preceding arguments apply only away from since each point is a singularity point of equation (3) in the sense that when due to for . In this case it is also important to note that the preceding arguments can be applied to the equivalent equation for the inverse of since this singularity gets removed (the derivative of the inverse being zero).

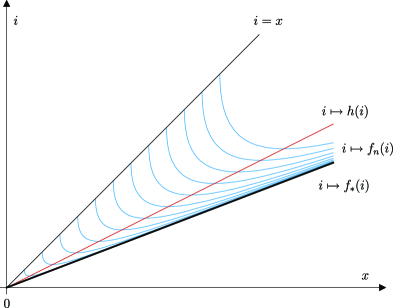

To construct the minimal solution to (3) staying strictly above , we can proceed as follows (see Figure 1). For any such that as , let denote the solution to (3) on such that . Note that is singular at and that passing to the equivalent equation for the inverse of , this singularity gets removed as explained above. (Note that the solution to the equivalent equation for the inverse can be continued below as well until hitting the diagonal at some strictly positive point at which the derivative is . This yields another solution to (3) staying below and providing its “physical” link to the diagonal. We will not make use of this part of the solution in the sequel.) Note that the right-hand side of equation (3) is positive for so that is strictly increasing on . By the uniqueness of the solution we know that the two curves and cannot intersect for , and hence we see that is increasing. It follows therefore that exists on . Passing to an integral equation equivalent to (3) it is easily verified that solves (3) wherever finite. This represents the minimal solution to (3) staying strictly above the curve on . We will first consider the case when is finite valued on .

6. Stochastic representation. We show that the function (43) associated with the minimal solution admits the stochastic representation (37). For this, let be the solution to (3) on such that for with as . Consider the function defined by (43) for and with given and fixed. Recall that solves the free-boundary problem (33)–(36) for . Consider the stopping time where and . Applying Itô’s formula and using (33), we find that

where we also use (34) to conclude that the integral with respect to is equal to zero and is a continuous local martingale for .

Since the process remains in the compact set up to time under , and both and are continuous (and thus bounded) on this set, we see that is a uniformly integrable martingale, and hence by the optional sampling theorem we have . Taking on both sides of (3), we therefore obtain

since on and on . Using that we find by (42), (23) and (31) that

| (47) | |||

as since and , so that , due to (5) above. Hence letting in (3) and using that by the monotone convergence theorem, as well as that since and , we find noting that and using the dominated convergence theorem that

| (48) |

for all in as claimed.

7. Nonpositivity. We show that for every solution to (3) such that on and the function defined by (43) above, we have

| (49) |

for all in . Clearly, since for in (43), it is enough to prove (49) for and with . For this, consider the stopping time and note that . Hence by the strong Markov property of applied at we find using (48) that

where the final inequality follows from the facts that for all and due to upon recalling (43) as already indicated above. This completes the proof of (49).

8. Optimality of the minimal solution. We will begin by disclosing the subharmonic characterization of the value function (26) in terms of the solutions to (3) staying strictly above . For this, let be any solution to (3) satisfying for all . Consider the function defined by (43) for in and set for in . Let in be given and fixed. Due to the “double-deck” structure of , we can apply the change-of-variable formula from Pe-2 that in view of (36) reduces to standard Itô’s formula and gives

where we also use (34) to conclude that the integral with respect to is equal to zero. The process defined by

| (52) |

is a continuous local martingale. Introducing the increasing process by setting

| (53) |

and using the fact that the set of all for which equals is of Lebesque measure zero, we see by (33) that (3) can be rewritten as follows:

| (54) |

From this representation we see that the process is a local submartingale for .

Let be any stopping time of (with finite mean). Choose a localization sequence of bounded stopping times for . Then by (49) and (54) we can conclude using the optional sampling theorem that

Letting and using the dominated convergence theorem (upon recalling that as already used above) we find that

| (56) |

Taking first the infimum over all , and then the supremum over all , we conclude that

| (57) |

upon recalling that is decreasing over so that the supremum is attained at . Combining (57) with (48) we see that (28) and (30) hold as claimed.

Note that (3) implies that the function is subharmonic for the Markov process where for . Recalling that is decreasing over , and that for all in by (49) above, we see that selecting the minimal solution staying strictly above is equivalent to invoking the subharmonic characterization of the value function (according to which the value function is the largest subharmonic function lying below the loss function). For more details on the latter characterization in a general setting we refer to PS , Chapter 1. It is also useful to know that the subharmonic characterization of the value function represents the dual problem to the primal problem (26) (for more details on the meaning of this claim including connections to the Legendre transform see Pe-3 ).

Consider finally the case when is not finite valued on . Since is increasing we see that there is such that for all when and for all with when . If , then the proof above can be applied in exactly the same way to show that (28) and (30) hold as claimed under for all in with . If with when , then the same proof shows that (30) still holds with in place of , however, the stopping time (28) can no longer be optimal in (26). This is easily seen by noting that the value in (30) is nonpositive (it could also be ) for any for instance, while the -probability for hitting before drifting away to is strictly smaller than so that the -expectation over this set in (26) equals (since the integrand tends to as tends to ) showing that the stopping time (28) cannot be optimal. The proof above shows that the optimality of (30) in this case is obtained through which play the role of approximate stopping times (obtained by passing to the limit when tends to in (3) above). This completes the proof of the theorem.

4 The golden ratio rule

In this section we show that the minimal solution to (29) admits a simple closed-form expression when is a transient Bessel process (Theorem 4). In the case when is the radial part of three-dimensional Brownian motion this leads to the golden ratio rule (Corollary 5). We also show that stopped according to the golden ratio rule has what we refer to as the golden ratio distribution (Corollary 8).

In the setting of (6)–(8) consider the optimal prediction problem (14). Recall that this problem is equivalent to the optimal stopping problem (21) which further extends as (26). The main result of this section can now be stated as follows.

Theorem 4

By the result of Theorem 3 we know that the optimal stopping time is given by (28) above where the optimal boundary can be characterized as the minimal solution to (29) staying strictly above the curve for . Using (7) and (27) it can be verified that (29) reads as follows:

and for . Hence it is enough to show that is the minimal solution to (4) staying strictly above the curve for .

To show that is a solution to (4) staying strictly above , insert into (4) with to be determined. Multiplying both sides of the resulting identity by (to be able to derive the factorization (64) below) it is easy to see that this yields the equation where we set

for . After some algebraic manipulations we find that

| (64) |

for and . Hence we see that the equation has two roots and where . It is easy to check that and showing that has a local maximum at and has a local minimum at . Noting that , and this shows that (i) is strictly increasing on with and ; (ii) is strictly decreasing on with and ; and (iii) is strictly increasing on with . It follows therefore that the equation has exactly three roots where and . Setting this shows that is a solution to (4) staying strictly above the curve for as claimed.

To show that is the minimal solution satisfying this property, set and note that (4) can then be rewritten as follows:

| (65) |

for . Since for we see from (65) that is increasing for . Noting that (65) implies that

| (66) |

it follows therefore that the integrand on the left-hand side is bounded by a constant (not dependent on ) as long as for with any given and fixed. Letting then in (66) we see that the left-hand side remains bounded while the right-hand side tends to leading to a contradiction. Noting that if and only if , we can therefore conclude that there is no solution to (4) satisfying for . Thus is the minimal solution to (4) staying strictly above and the proof is complete.

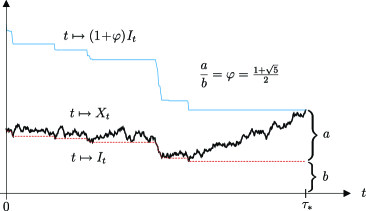

Corollary 5 ((The golden ratio rule))

If is the radial part of three-dimensional Brownian motion, then the optimal stopping time in (14) is given by

| (67) |

where is the golden

ratio (see Figure 2).

In this case and equation (59) reads

| (68) |

for . Solving the latter quadratic equation and choosing the root strictly greater than , we find that where is the golden ratio. The optimality of (67) then follows from (58) and the proof is complete.

Returning to the result of Theorem 3 above we now determine the law of the transient diffusion process stopped at the optimal stopping time (for related results on the Skorokhod embedding problem see RY , pages 269–277, and the references therein).

Proposition 6

Note that

where we set , and for . Let be given and fixed. For set where is a continuously differentiable function with bounded support. Using the fact that when it is easily verified by Itô’s formula that the process defined by

| (71) |

is a continuous local martingale. Moreover, since is continuous and has bounded support, we see that is bounded and therefore uniformly integrable. By the optional sampling theorem we thus find that

where we set and denotes the distribution function of under . Since (4) holds for all functions of this kind, it follows that

| (73) |

for with . Solving (73) under this boundary condition we find that

| (74) |

for . Recalling that and substituting it follows that

for in . Hence we find that

for with . This completes the proof.

Specializing this result to the -dimensional Bessel process of Theorem 4 we obtain the following consequence.

Corollary 7

In this case for where is the unique solution to either (59) when or (60) when and is given by (7). Inserting these expressions into the right-hand side of (69) it is easily verified that this yields (77).

Specializing this further to the radial part of three-dimensional Brownian motion in Corollary 5 we obtain the following conclusion.

Corollary 8 ((The golden ratio distribution))

Note from (78) that the density function of under is given by

| (79) |

for with and equals zero otherwise. We refer to (78) and (79) as the golden ratio distribution. It is easy to see that

| (80) |

for . The fact that this number is strictly greater than (the initial point corresponding to stopping at once) is not surprising since is a submartingale. It needs to be recalled moreover that the aim of applying the golden ratio rule is to be as close as possible to the time at which the ultimate minimum is attained. We will see in the next section that the golden ratio distribution provides insight as to what extent the golden ratio rule has the power of capturing the ultimate maximum of a strict local martingale.

5 Applications in optimal trading

In this section we present some applications of the previous results in problems of optimal trading. We also outline some remarkable connections between such problems and the practice of technical analysis. These applications and connections rest on three basic ingredients that we describe first.

1. Fibonnaci retracement. We begin by explaining a few technical terms from the field of applied finance. Technical analysis is a financial term used to describe methods and techniques for forecasting the direction of asset prices through the study of past market data (primarily prices themselves plus the volume of their trade). Support and resistance are concepts in technical analysis associated with the expectation that the movement of the asset price will tend to cease and reverse its trend of decrease/increase at certain predetermined price levels. A support/resistance level is a price level at which the price will tend to find support/resistance when moving down/up. This means that the price is more likely to bounce off this level rather than break through it. One may also think of these levels as turning points of the prices. Fibonacci retracement is a method of technical analysis for determining support and resistance levels. The name comes after its use of Fibonacci numbers for with and . Fibonacci retracement is based on the idea that after reversing the trend at a support/resistance level, the price will retrace a predictable portion of the past downward/upward move by advancing in the opposite direction until finding a new resistance/support level, after which it will return to the initial trend of moving downwards/upwards. Fibonacci retracement is created by taking two extreme points on a chart showing the asset price as a function of time and dividing the vertical distance between them by the key Fibonacci ratios ranging from (start of the retracement) to (end of the retracement representing a complete reversal to the original trend). The other key Fibonacci ratios are (shallow retracement), (moderate retracement) and (golden retracement). They are obtained by formulas , and , respectively (see the next paragraph). These retracement levels serve as alert points for a potential reversal at which traders may employ other methods of technical analysis to identify and confirm a reversal. Despite its widespread use in technical analysis of asset prices, there appears to be no (rigorous) explanation of any kind as to why the Fibonacci ratios should be used to this effect. We will show below that the golden ratio rule derived in the previous section offers a rigorous optimality argument for the choice of the golden retracement (). To our knowledge this is the first time that such an argument has been found/given in the literature.

2. Golden ratio and Fibonacci numbers. The link between the two is well known and is expressed by Binet’s formula

| (81) |

where and . It follows that

| (82) |

This fact is used in the description of Fibonacci retracement above.

3. The CEV model. One of the simplest/tractable models for asset price movements that is capable of reproducing the implied volatility smile/frown effect and the (inverse) leverage effect (both observed in the empirical data) is the Constant Elasticity of Variance (CEV) model in which the (nonnegative) asset price process solves

| (83) |

where is the appreciation rate, is the volatility coefficient, and is the elasticity parameter. If then is a geometric Brownian motion which was initially considered in Os and Sa . For this model was firstly considered in Cox for and then in EM for . Due to its predictive power and tractability, the CEV model is widely used by practitioners in the financial industry, especially for modeling prices of equities and commodities. If then the model embodies the leverage effect (commonly observed in equity markets) where the volatility of the asset price increases as its price decreases. If then the model embodies the inverse leverage effect (often observed in commodity markets) where the volatility of the asset price increases when its price increases. For example, it is reported in GS that the elasticity coefficient for Gold on the London Bullion Market in the period from 2000 to 2007 was approximately 0.49. Similar elasticity coefficients have also been observed for other precious metals (such as Copper for instance).

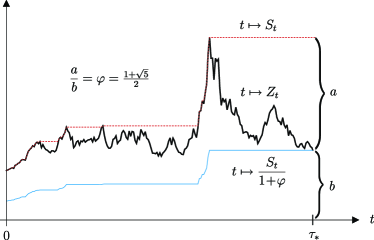

In the remainder of this section we focus on the case when and . It is well known (cf. EM ) that solving (83) is a strict local martingale (a local martingale which is not a true martingale) in this case due to the fact that is strictly decreasing on for any . This also implies that does not admit an equivalent martingale measure so that the CEV model may admit arbitrage opportunities. One way of looking at the models of this type is to associate them with asset price bubbles (see HLW ). After soaring to a finite ultimate maximum (bubble) at a finite time, the asset price will tend to zero as time goes to infinity, and the central question for a holder of the asset becomes when to sell so as to be as close as possible to the time at which the ultimate maximum is attained. More precisely, introducing the running maximum process associated with by setting

| (84) |

and recalling that as , we see that the ultimate supremum is attained at some random time in the sense that

| (85) |

with -probability one for given and fixed. The optimal selling problem addressed above then becomes the optimal prediction problem

| (86) |

where the infimum is taken over all stopping times of (with finite mean) and is given and fixed. We will now show that due to the well-known connection between CEV and Bessel processes (dating back to similar transformations in Cox and EM ) the problem (86) can be reduced to the problem (14) solved above.

4. The golden ratio rule for the CEV process. For given and fixed consider the -dimensional Bessel process solving (6) under with . Recall that the scale function is given by (7) and set for with given and fixed. Then the process defined by

| (87) |

is on natural scale and Itô’s formula shows that solves

| (88) |

where and is a standard Brownian motion. Note that equation (88) coincides with equation (83) for and . By the uniqueness in law for this equation (among positive solutions) it follows that is a CEV process. From the properties of it follows that after starting at , the process stays strictly positive (without exploding at a finite time) and with -probability one as . This shows that in (85) is well defined. Moreover, due to the reciprocal relationship (87) we see that the time of the ultimate maximum for in (85) coincides with the time of the ultimate minimum for in (10), and hence the problem (86) has the same solution as the problem (14) (note also that the natural filtrations of and coincide so that is a stopping time of if and only if is a stopping time of ). Since if and only if it follows from (58) in Theorem 4 that the optimal stopping time in (86) is given by

| (89) |

where is the unique solution to either (59) or (60) belonging to . In particular, if then we know from (68) that so that (89) reads

| (90) |

This is the golden ratio rule for the CEV process where is the radial part of three-dimensional Brownian motion (see Figure 3).

To relate the golden ratio rule (90) to Fibonacci retracement discussed above, let denote the larger quantity and let denote the smaller quantity in the golden ratio rule. To determine the percentage of in we need to calculate

Multiplying this expression by gives and this is exactly the golden retracement discussed above. In view of the optimality of (90) in (86) we see that the golden retracement of for the CEV process (starting close to zero) where is the radial part of three-dimensional Brownian motion can be seen as a rational support level (in the sense that rational investors who aim at selling the asset at the time of the ultimate maximum will sell the asset at the time of the golden retracement, and therefore the asset price could be expected to raise afterwards). To our knowledge this is the first time that such a rational optimality argument for the golden retracement has been established.

References

- (1) {barticle}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmBernyk, \bfnmV.\binitsV., \bauthor\bsnmDalang, \bfnmR. C.\binitsR. C. and \bauthor\bsnmPeskir, \bfnmG.\binitsG. (\byear2011). \btitlePredicting the ultimate supremum of a stable Lévy process with no negative jumps. \bjournalAnn. Probab. \bvolume39 \bpages2385–2423. \bptokimsref \endbibitem

- (2) {barticle}[mr] \bauthor\bsnmCohen, \bfnmAlbert\binitsA. (\byear2010). \btitleExamples of optimal prediction in the infinite horizon case. \bjournalStatist. Probab. Lett. \bvolume80 \bpages950–957. \biddoi=10.1016/j.spl.2010.02.006, issn=0167-7152, mr=2638963 \bptokimsref \endbibitem

- (3) {barticle}[mr] \bauthor\bsnmCox, \bfnmA. M. G.\binitsA. M. G., \bauthor\bsnmHobson, \bfnmDavid\binitsD. and \bauthor\bsnmObłój, \bfnmJan\binitsJ. (\byear2008). \btitlePathwise inequalities for local time: Applications to Skorokhod embeddings and optimal stopping. \bjournalAnn. Appl. Probab. \bvolume18 \bpages1870–1896. \biddoi=10.1214/07-AAP507, issn=1050-5164, mr=2462552 \bptokimsref \endbibitem

- (4) {bmisc}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmCox, \bfnmJ.\binitsJ. (\byear1975). \bhowpublishedNotes on option pricing I: Constant elasticity of diffusions. Working paper, Stanford Univ. \bptokimsref \endbibitem

- (5) {barticle}[mr] \bauthor\bsnmCsáki, \bfnmEndre\binitsE., \bauthor\bsnmFöldes, \bfnmAntónia\binitsA. and \bauthor\bsnmSalminen, \bfnmPaavo\binitsP. (\byear1987). \btitleOn the joint distribution of the maximum and its location for a linear diffusion. \bjournalAnn. Inst. Henri Poincaré Probab. Stat. \bvolume23 \bpages179–194. \bidissn=0246-0203, mr=0891709 \bptokimsref \endbibitem

- (6) {barticle}[mr] \bauthor\bparticleDu \bsnmToit, \bfnmJ.\binitsJ. and \bauthor\bsnmPeskir, \bfnmG.\binitsG. (\byear2007). \btitleThe trap of complacency in predicting the maximum. \bjournalAnn. Probab. \bvolume35 \bpages340–365. \biddoi=10.1214/009117906000000638, issn=0091-1798, mr=2303953 \bptokimsref \endbibitem

- (7) {bincollection}[mr] \bauthor\bparticleDu \bsnmToit, \bfnmJacques\binitsJ. and \bauthor\bsnmPeskir, \bfnmGoran\binitsG. (\byear2008). \btitlePredicting the time of the ultimate maximum for Brownian motion with drift. In \bbooktitleMathematical Control Theory and Finance \bpages95–112. \bpublisherSpringer, \baddressBerlin. \biddoi=10.1007/978-3-540-69532-5_6, mr=2484106 \bptokimsref \endbibitem

- (8) {barticle}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmDu Toit, \bfnmJ.\binitsJ. and \bauthor\bsnmPeskir, \bfnmG.\binitsG. (\byear2009). \btitleSelling a stock at the ultimate maximum. \bjournalAnn. Appl. Probab. \bvolume19 \bpages983–1014. \bptokimsref \endbibitem

- (9) {barticle}[mr] \bauthor\bparticleDu \bsnmToit, \bfnmJ.\binitsJ., \bauthor\bsnmPeskir, \bfnmG.\binitsG. and \bauthor\bsnmShiryaev, \bfnmA. N.\binitsA. N. (\byear2008). \btitlePredicting the last zero of Brownian motion with drift. \bjournalStochastics \bvolume80 \bpages229–245. \biddoi=10.1080/17442500701840950, issn=1744-2508, mr=2402166 \bptokimsref \endbibitem

- (10) {barticle}[mr] \bauthor\bsnmDubins, \bfnmLester E.\binitsL. E., \bauthor\bsnmGilat, \bfnmDavid\binitsD. and \bauthor\bsnmMeilijson, \bfnmIsaac\binitsI. (\byear2009). \btitleOn the expected diameter of an -bounded martingale. \bjournalAnn. Probab. \bvolume37 \bpages393–402. \biddoi=10.1214/08-AOP406, issn=0091-1798, mr=2489169 \bptokimsref \endbibitem

- (11) {barticle}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmDubins, \bfnmL. E.\binitsL. E. and \bauthor\bsnmSchwarz, \bfnmG.\binitsG. (\byear1988). \btitleA sharp inequality for sub-martingales and stopping times. \bjournalAstérisque \bvolume157-158 \bpages129–145. \bptokimsref \endbibitem

- (12) {barticle}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmDubins, \bfnmL. E.\binitsL. E., \bauthor\bsnmShepp, \bfnmL. A.\binitsL. A. and \bauthor\bsnmShiryaev, \bfnmA. N.\binitsA. N. (\byear1993). \btitleOptimal stopping rules and maximal inequalities for Bessel processes. \bjournalTheory Probab. Appl. \bvolume38 \bpages226–261. \bptokimsref \endbibitem

- (13) {barticle}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmEmanuel, \bfnmD. C.\binitsD. C. and \bauthor\bsnmMacBeth, \bfnmJ. D.\binitsJ. D. (\byear1982). \btitleFurther results on the constant elasticity of variance call option pricing model. \bjournalJ. Financial Quant. Anal. \bvolume17 \bpages533–554. \bptokimsref \endbibitem

- (14) {bmisc}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmEspinosa, \bfnmG. E.\binitsG. E. and \bauthor\bsnmTouzi, \bfnmN.\binitsN. (\byear2010). \bhowpublishedDetecting the maximum of a mean-reverting scalar diffusion. Working paper, Univ. Paris-Dauphine. \bptokimsref \endbibitem

- (15) {barticle}[mr] \bauthor\bsnmGapeev, \bfnmPavel V.\binitsP. V. (\byear2006). \btitleDiscounted optimal stopping for maxima in diffusion models with finite horizon. \bjournalElectron. J. Probab. \bvolume11 \bpages1031–1048 (electronic). \biddoi=10.1214/EJP.v11-367, issn=1083-6489, mr=2268535 \bptokimsref \endbibitem

- (16) {barticle}[mr] \bauthor\bsnmGapeev, \bfnmPavel V.\binitsP. V. (\byear2007). \btitleDiscounted optimal stopping for maxima of some jump-diffusion processes. \bjournalJ. Appl. Probab. \bvolume44 \bpages713–731. \biddoi=10.1239/jap/1189717540, issn=0021-9002, mr=2355587 \bptokimsref \endbibitem

- (17) {barticle}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmGeman, \bfnmH.\binitsH. and \bauthor\bsnmShih, \bfnmY. F.\binitsY. F. (\byear2009). \btitleModelling commodity prices under the CEV model. \bjournalJ. Alternative Investments \bvolume11 \bpages65–84. \bptokimsref \endbibitem

- (18) {barticle}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmGoldman, \bfnmM. B.\binitsM. B., \bauthor\bsnmSosin, \bfnmH. B.\binitsH. B. and \bauthor\bsnmGatto, \bfnmM. A.\binitsM. A. (\byear1979). \btitlePath dependent options: “Buy at the low, sell at the high.” \bjournalJ. Finance \bvolume34 \bpages1111–1127. \bptokimsref \endbibitem

- (19) {barticle}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmGraversen, \bfnmS. E.\binitsS. E., \bauthor\bsnmPeskir, \bfnmG.\binitsG. and \bauthor\bsnmShiryaev, \bfnmA. N.\binitsA. N. (\byear2001). \btitleStopping Brownian motion without anticipation as close as possible to its ulimate maximum. \bjournalTheory Probab. Appl. \bvolume45 \bpages41–50. \bptokimsref \endbibitem

- (20) {barticle}[mr] \bauthor\bsnmGuo, \bfnmXin\binitsX. and \bauthor\bsnmZervos, \bfnmMihail\binitsM. (\byear2010). \btitle options. \bjournalStochastic Process. Appl. \bvolume120 \bpages1033–1059. \biddoi=10.1016/j.spa.2010.02.008, issn=0304-4149, mr=2639737 \bptokimsref \endbibitem

- (21) {barticle}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmHeston, \bfnmS. L.\binitsS. L., \bauthor\bsnmLoewenstein, \bfnmM.\binitsM. and \bauthor\bsnmWillard, \bfnmG. A.\binitsG. A. (\byear2007). \btitleOptions and bubbles. \bjournalRev. Financial Studies \bvolume20 \bpages359–390. \bptokimsref \endbibitem

- (22) {barticle}[mr] \bauthor\bsnmHobson, \bfnmDavid\binitsD. (\byear2007). \btitleOptimal stopping of the maximum process: A converse to the results of Peskir. \bjournalStochastics \bvolume79 \bpages85–102. \biddoi=10.1080/17442500601111429, issn=1744-2508, mr=2290399 \bptokimsref \endbibitem

- (23) {barticle}[mr] \bauthor\bsnmJacka, \bfnmS. D.\binitsS. D. (\byear1991). \btitleOptimal stopping and best constants for Doob-like inequalities. I. The case . \bjournalAnn. Probab. \bvolume19 \bpages1798–1821. \bidissn=0091-1798, mr=1127729 \bptokimsref \endbibitem

- (24) {bbook}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmLivio, \bfnmM.\binitsM. (\byear2002). \btitleThe Golden Ratio: The Story of Phi, The World’s Most Astonishing Number. \bpublisherBroadway Books, \baddressNew York. \bptokimsref \endbibitem

- (25) {barticle}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmNovikov, \bfnmA. A.\binitsA. A. and \bauthor\bsnmShiryaev, \bfnmA. N.\binitsA. N. (\byear2008). \btitleOn a stochastic version of the trading rule “buy and hold.” \bjournalStatist. Decisions \bvolume26 \bpages289–302. \bptokimsref \endbibitem

- (26) {barticle}[mr] \bauthor\bsnmObłój, \bfnmJan\binitsJ. (\byear2004). \btitleThe Skorokhod embedding problem and its offspring. \bjournalProbab. Surv. \bvolume1 \bpages321–390. \biddoi=10.1214/154957804100000060, issn=1549-5787, mr=2068476 \bptokimsref \endbibitem

- (27) {bincollection}[mr] \bauthor\bsnmObłój, \bfnmJan\binitsJ. (\byear2007). \btitleThe maximality principle revisited: On certain optimal stopping problems. In \bbooktitleSéminaire de Probabilités XL. \bseriesLecture Notes in Math. \bvolume1899 \bpages309–328. \bpublisherSpringer, \baddressBerlin. \biddoi=10.1007/978-3-540-71189-6_16, mr=2409013 \bptokimsref \endbibitem

- (28) {barticle}[mr] \bauthor\bsnmOsborne, \bfnmM. F. M.\binitsM. F. M. (\byear1959). \btitleBrownian motion in the stock market. \bjournalOper. Res. \bvolume7 \bpages145–173. \bidissn=0030-364X, mr=0104513 \bptokimsref \endbibitem

- (29) {barticle}[mr] \bauthor\bsnmPedersen, \bfnmJesper Lund\binitsJ. L. (\byear2000). \btitleDiscounted optimal stopping problems for the maximum process. \bjournalJ. Appl. Probab. \bvolume37 \bpages972–983. \bidissn=0021-9002, mr=1808862 \bptokimsref \endbibitem

- (30) {barticle}[mr] \bauthor\bsnmPedersen, \bfnmJesper Lund\binitsJ. L. (\byear2003). \btitleOptimal prediction of the ultimate maximum of Brownian motion. \bjournalStoch. Stoch. Rep. \bvolume75 \bpages205–219. \biddoi=10.1080/1045112031000118994, issn=1045-1129, mr=1994906 \bptokimsref \endbibitem

- (31) {barticle}[mr] \bauthor\bsnmPeskir, \bfnmGoran\binitsG. (\byear1998). \btitleOptimal stopping of the maximum process: The maximality principle. \bjournalAnn. Probab. \bvolume26 \bpages1614–1640. \biddoi=10.1214/aop/1022855875, issn=0091-1798, mr=1675047 \bptokimsref \endbibitem

- (32) {bincollection}[mr] \bauthor\bsnmPeskir, \bfnmGoran\binitsG. (\byear2007). \btitleA change-of-variable formula with local time on surfaces. In \bbooktitleSéminaire de Probabilités XL. \bseriesLecture Notes in Math. \bvolume1899 \bpages69–96. \bpublisherSpringer, \baddressBerlin. \bidmr=2408999 \bptokimsref \endbibitem

- (33) {bmisc}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmPeskir, \bfnmG.\binitsG. (\byear2012). \bhowpublishedA duality principle for the Legendre transform. J. Convex Anal. 19 609–630. \bptokimsref \endbibitem

- (34) {bmisc}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmPeskir, \bfnmG.\binitsG. (\byear2010). \bhowpublishedQuickest detection of a hidden target and extremal surfaces. Research Report No. 23, Probab. Statist. Group Manchester (25 pp.). \bptokimsref \endbibitem

- (35) {bbook}[mr] \bauthor\bsnmPeskir, \bfnmGoran\binitsG. and \bauthor\bsnmShiryaev, \bfnmAlbert\binitsA. (\byear2006). \btitleOptimal Stopping and Free-boundary Problems. \bpublisherBirkhäuser, \baddressBasel. \bidmr=2256030 \bptokimsref \endbibitem

- (36) {bbook}[mr] \bauthor\bsnmRevuz, \bfnmDaniel\binitsD. and \bauthor\bsnmYor, \bfnmMarc\binitsM. (\byear1999). \btitleContinuous Martingales and Brownian Motion. \bpublisherSpringer, \baddressBerlin. \bptokimsref \endbibitem

- (37) {barticle}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmSamuelson, \bfnmP.\binitsP. (\byear1965). \btitleRational theory of warrant pricing. \bjournalIndustrial Management Review \bvolume6 \bpages13–32. \bptokimsref \endbibitem

- (38) {bincollection}[mr] \bauthor\bsnmShi, \bfnmZhan\binitsZ. (\byear1996). \btitleHow long does it take a transient Bessel process to reach its future infimum? In \bbooktitleSéminaire de Probabilités, XXX. \bseriesLecture Notes in Math. \bvolume1626 \bpages207–217. \bpublisherSpringer, \baddressBerlin. \biddoi=10.1007/BFb0094649, mr=1459484 \bptokimsref \endbibitem

- (39) {bincollection}[mr] \bauthor\bsnmShiryaev, \bfnmAlbert N.\binitsA. N. (\byear2002). \btitleQuickest detection problems in the technical analysis of the financial data. In \bbooktitleMathematical Finance—Bachelier Congress, 2000 (Paris). \bseriesSpringer Finance \bpages487–521. \bpublisherSpringer, \baddressBerlin. \bidmr=1960576 \bptokimsref \endbibitem

- (40) {barticle}[auto:STB—2012/04/30—08:06:40] \bauthor\bsnmShiryaev, \bfnmA. N.\binitsA. N. (\byear2009). \btitleOn conditional-extremal problems of the quickest detection of nonpredictable times of the observable Brownian motion. \bjournalTheory Probab. Appl. \bvolume53 \bpages663–678. \bptokimsref \endbibitem

- (41) {barticle}[mr] \bauthor\bsnmUrusov, \bfnmM. A.\binitsM. A. (\byear2005). \btitleOn a property of the time of attaining the maximum by Brownian motion and some optimal stopping problems. \bjournalTheory Probab. Appl. \bvolume49 \bpages169–176. \bptokimsref \endbibitem

- (42) {barticle}[mr] \bauthor\bsnmWilliams, \bfnmDavid\binitsD. (\byear1974). \btitlePath decomposition and continuity of local time for one-dimensional diffusions. I. \bjournalProc. Lond. Math. Soc. (3) \bvolume28 \bpages738–768. \bidissn=0024-6115, mr=0350881 \bptokimsref \endbibitem

- (43) {barticle}[mr] \bauthor\bsnmZhitlukhin, \bfnmMikhail\binitsM. (\byear2009). \btitleA maximal inequality for skew Brownian motion. \bjournalStatist. Decisions \bvolume27 \bpages261–280. \biddoi=10.1524/stnd.2009.1061, issn=0721-2631, mr=2732522 \bptokimsref \endbibitem