Technical Report

Risk-neutral density recovery via spectral analysis

Abstract

In this paper, we propose a new method for estimating the conditional risk-neutral density (RND) directly from a cross-section of put option bid-ask quotes. More precisely, we propose to view the RND recovery problem as an inverse problem. We first show that it is possible to define restricted put and call operators that admit a singular value decomposition (SVD), which we compute explicitly. We subsequently show that this new framework allows us to devise a simple and fast quadratic programming method to recover the smoothest RND whose corresponding put prices lie inside the bid-ask quotes. This method is termed the spectral recovery method (SRM). Interestingly, the SVD of the restricted put and call operators sheds some new light on the RND recovery problem. The SRM improves on other RND recovery methods in the sense that 1) it is fast and simple to implement since it requires solution of a single quadratic program, while being fully nonparametric; 2) it takes the bid ask quotes as sole input and does not require any sort of calibration, smoothing or preprocessing of the data; 3) it is robust to the paucity of price quotes; 4) it returns the smoothest density giving rise to prices that lie inside the bid ask quotes. The estimated RND is therefore as well-behaved as can be; 5) it returns a closed form estimate of the RND on the interval of the positive real line, where is a positive constant that can be chosen arbitrarily. We thus obtain both the middle part of the RND together with its full left tail and part of its right tail. We confront this method to both real and simulated data and observe that it fares well in practice. The SRM is thus found to be a promising alternative to other RND recovery methods.

key words:

Risk-neutral density; Nonparametric estimation;

Singular value decomposition; Spectral analysis; Quadratic programming.

AMS subject classifications:

91G70, 91G80, 45Q05, 62G05

1 Introduction

1.1 The setting

Over the last four decades, the no-arbitrage assumption has proved to be a fruitful starting point that paved the way for the elaboration of a rich theoretical framework for derivatives pricing known today as arbitrage pricing theory. Among its numerous achievements, the arbitrage pricing theory has set forth two fundamental theorems. The First Fundamental Theorem of Asset Pricing (see [21, p.72]) proves that a market is arbitrage-free if and only if there exists a measure equivalent to the historical (or statistical) measure , which turns the underlying price process into a martingale. is therefore referred to as a martingale measure. The Second Fundamental Theorem of Asset Pricing (see [21, p.73]) proves in turn that this martingale measure is unique if and only if the market is complete (see [21, p.300] for terminology). Let us denote by the positive valued price of the underlying at a deterministic future date and by the payoff of a contingent claim maturing at time . Let us moreover denote by the marginal density of under with respect to the Lebesgue measure on the positive real line, assuming that it exists. As initially proved in [10], the arbitrage price of this derivative security writes as its discounted expected payoff under , that is,

where stands for the continuously compounded risk-free rate. It is

a widely acknowledged fact that financial markets are

incomplete, if only due to the presence of jumps in the

underlying price process. In such a setting, and as described above,

there exist possibly very many s, and therefore, very many

corresponding systems of arbitrage-free prices. Let us denote by

the corresponding set of valid densities . The elements of

are most often referred

to as risk-neutral densities (RNDs) and we will stick to this

terminology in the sequel.

RNDs are of crucial interest for Central Banks and, in fact, most institutions

and people concerned with financial markets

since they represent the market sentiment about a given

underlying price process at a future point in time (see

[3]). They are also of crucial interest to the financial

derivatives industry since the knowledge of allows to price

new derivative securities in an arbitrage-free way with respect to

traded ones. For these reasons, the literature related to

risk-neutral density estimation is very extensive, the bulk of it

dating back to the late 90’s and early 2k’s. It is not our purpose

here to present an exhaustive review of this literature. Excellent and

up-to-date reviews can in fact be found in [14, 17]. Older but still relevant ones can be found in [9, 3].

Among derivative securities, call and put options play a very

particular role since they are actively traded in the market and thus believed to be

efficiently priced. Let us recall that a call of strike and maturity

gives its holder the right to buy the underlying security at

maturity time at price . It is an insurance against a rise

in the price of the underlying. Its payoff writes , where we have written for . Conversely, a put option gives

the right to sell the underlying security. It is an insurance against

a fall in the underlying price and its payoff writes . Here and in what follows, we denote the strike

price by and not by , which will stand for a

running index in .

According to the celebrated Breeden-Litzenberger formula, the second derivative of put and call prices with respect to their strike price both equal the discounted RND (see [6]). Therefore, if a continuum of put or call prices were available in the market, we would have direct access to the RND by the latter formula. However, this is not the case and only a few strike prices around the forward price are quoted and actively traded at each maturity date. Depending on the market, we overall reckon from to quotes at a given maturity date . To complicate the matter even more, quotes do not appear as a single price. Dealers quote in fact a bid price, at which they offer to buy the security, and an ask price, at which they offer to sell the security. The difference between both prices is referred to as the bid-ask spread. For an interesting insight into the nature of option quotes and sources of error in them, the reader is referred to, say, [16, p.786].

1.2 The problem and brief literature review

As detailed above, if traded puts and calls at a given maturity are arbitrage free, they

must write as their expected discounted

payoff with respect to a single RND drawn from the set . Given the paucity of quoted option prices at a given

maturity and the presence of a

bid-ask spread, it is clear that many RNDs could in fact be hidden

behind quoted option prices. Therefore, the RND quest is not that much about

estimating the true RND that is used by the market for pricing

purpose, since the nature of the quotes does not allow to identify it

uniquely. It is rather more about recovering a valid RND, meaning an

actual density function, to be chosen according to a criterion

typically related to its smoothness or

information content. Historically, three main routes have been used to

recover a RND from quoted option prices: parametric methods,

nonparametric methods and models of the underlying price

process. Each of them have their pros and cons. Parametric methods are

well adapted to small data sets and always recover a

density. However, they constrain the RND to belong to a given

parametric family. On the other hand, models of the underlying price process have been

the first great success of arbitrage pricing theory with the

celebrated geometric Brownian motion (see [4, 20]). However, the limitation of the log-normal

distribution is now widely acknowledged and no satisfying stochastic

process has yet been proposed that both reproduce accurately the dynamics of

the underlying price process and be analytically

tractable. Nonparametric methods circumvent both of these problems in the

sense that they do not require any stringent assumption on the process

generating the data (they are model-free) and can recover all

possible densities. As a main drawback, these methods are often data intensive.

Let us briefly come back on some contributions to the nonparametric literature which are relevant to the present paper. We can classify nonparametric methods as follows.

-

•

The expansion methods. It includes the Edgeworth (see [19]) and cumulant expansions (see [22]), which allow to estimate a finite number of RND cumulants. It also includes orthonormal basis methods such as Hermite polynomials (see [1]), which rely on well known Hilbert space techniques and give access to the middle part of the RND.

-

•

The kernel regression methods. As a recent example, [2] have introduced a shape constrained local polynomial estimator of the RND. Notice that it performs estimation on the average quoted prices (that is, the average of the bid-ask quotes) and requires therefore to pre-process them in order to make them arbitrage-free. Moreover, the returned RND depends on the kernel chosen and it is not clear how it relates to the other valid RNDs in term of information content or smoothness.

-

•

The maximum entropy method. It is introduced in [8, 23], where the RND is obtained via the maximization of an entropy criterion. According to [9, p.19], this method often gives bumpy (multimodals) estimates since it imposes no smoothness restriction on the estimated density. In addition, it is claimed in [18, p.1620], that this method presents convergence issues.

-

•

Other methods, which do not belong to any of the three categories above. Among them, we can refer to the positive convolution approximation (PCA) of [5]. In practice, it fits a finite (but large) convex linear combination of normal densities to the average quoted put prices and approximates the RND by the weights of the linear combination. It thus presents similarities with [18], since it ultimately fits a discrete set of probabilities to the average quoted prices. We can also refer to the smoothed implied volatility smile method (SML) as in [14]. This method uses the Black-Scholes formula as a non-linear transform. It consists in fitting a polynomial through the implied volatilities obtained from average quoted prices, and using the continuum of option prices obtained in that way to get the RND via the Breeden-Litzenberger formula. [14] refines this method by taking the bid-ask quotes into account at the implied volatility fit stage. The SML method gives access to the middle part of the RND. [14] proposes in addition a method for appending generalized extreme value (GEV) tail distributions to it. The SML method is cumbersome and can seem a bit odd since it requires going from price space to implied volatility space, back and forth. It is claimed that it is outperformed in term of accuracy and stability by simpler parametric methods in [7].

1.3 Our results

In this paper, we propose to view the RND recovery problem as an

inverse problem. We first show that it is possible to define

restricted put and call operators that admit a singular value decomposition (SVD),

which we compute explicitly. We subsequently show that this new framework

allows to devise a simple and fast quadratic programming method to recover the smoothest

RND that is consistent with market bid-ask quotes.

To be more precise, let us denote by the segment of the positive real line. We define the restricted put and call operators, denoted by and , from into itself (see 2.1 and 2.2 below) and show that they are conjugates of one another. We prove that the resulting self-adjoint operator is compact. As a consequence of the spectral theorem (see [15]), admits a singular value decomposition with positive decreasing singular values. We prove that the corresponding singular bases are complete in (see Theorem 3.1, item 3)) and compute them explicitly together with their singular values (see 1).

To fix notations, we will write and the two orthonormal families of such that , , where is a positive decreasing sequence of singular values. Precisely, we obtain explicitly,

where

and, for all , is the smallest positive solution of the following fixed point equation in ,

Interestingly, the positive sequence decreases exponentially fast toward zero as detailed in Lemma 6.3. Therefore, the sequence of singular values tends asymptotically toward zero at a rate of order . The RND recovery problem is therefore said to be mildly ill-posed with a degree of ill-posedness equal to (see [13, p.40]). Furthermore, for all , we obtain,

where the coefficients are such that,

Based on this new framework, we propose a spectral approach to RND

recovery. It is fully nonparametric and can recover the

restriction of any density to the interval . To that end, we

notice that the singular bases functions and are in

fact oscillations at frequency carried by the exponential

trend (see 6.2 and 6.1 for

notations). Conveniently, smooth densities

are therefore essentially captured by low singular spaces. The idea of

recovering the smoothest density among the valid ones was initially

suggested in [18]. Subsequently, [9]

correctly pointed out that the smoothness criterion can be debated as

it is difficult to give it an economic or even information theoretic

meaning. Our spectral

approach sheds some new light on this issue and makes it clear that

the smoothness criterion is justified by the fact

that the restricted call and put operators behave as low-pass frequency

filters. It is therefore

illusory to look for high frequency information about the

RND in a set of quoted options prices, since this information has been drastically

attenuated by the operator. The smoothness criterion

arises therefore as a by-product of the spectral nature of the

restricted put and call operators and might well not be an intrinsic

property of the true RND. Interestingly, smooth densities are also

easier to recover by nonparametric means.

In what follows, we exploit the rich framework offered by the SVD of the restricted put and call operators to recover the smoothest RND that is compatible with market quotes. As detailed in 7.1 below, the discounted restricted put operator coincides with the put price function (as a function of the strike) on . We therefore propose to recover the smoothest RND such that its image by the discounted restricted put operator lies in-between the bid-ask quotes (see 7.1). Conveniently, the singular bases present the property of being image of one another by second derivation modulo a multiplication by the corresponding singular value of (see Theorem 6.1). This allows us to characterize the smoothness of the estimated RND directly in term of a quadratic form of the coefficients of the estimated put price function, which depends on the singular values of the restricted put operator (see Proposition 7.1). This crucial feature allows to recover the smoothest RND as the solution of a simple quadratic program, which takes the bid ask quotes as sole input. Our estimation method improves on existing ones in several ways, which we sum up here.

-

•

It is fast and simple to implement since it only requires solution of a single quadratic program, while being fully nonparametric.

-

•

It is robust to the paucity of price quotes since the smaller the number of quotes, the less constrained the quadratic program and thus the easier to solve.

-

•

It takes the bid ask quotes as sole input and does not require any sort of smoothing or preprocessing of the data.

-

•

It returns the smoothest density giving rise to price quotes that lie inside the bid ask quotes. The estimated RND is therefore as well-behaved as can be.

-

•

It returns a closed form estimate of the RND on . We thus obtain both the middle part of the RND together with its left tail and part of its right tail. Interestingly, the left tail contains crucial information about market sentiments relative to a potential forthcoming market crash.

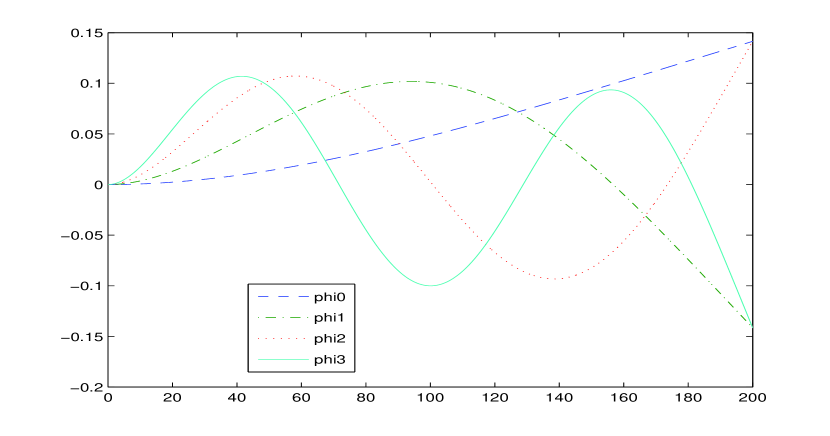

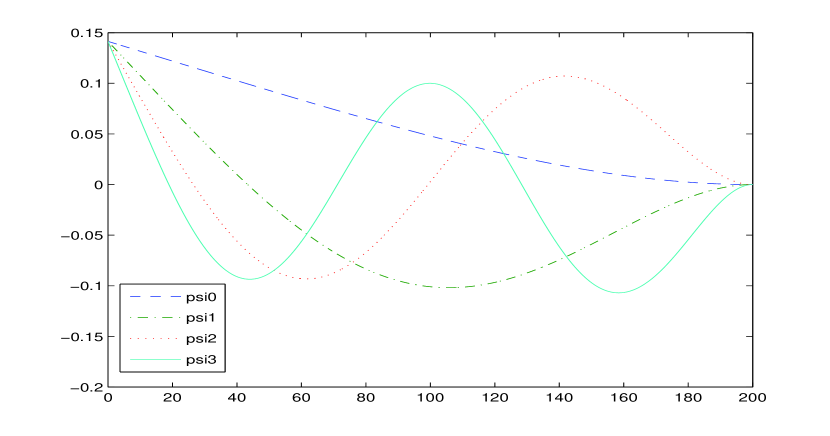

It is noteworthy that the singular vectors and

corresponding to the largest singular value of

and look themselves very much like cross sections of put

and call prices, respectively (see 1). In that sense, they will be able to

capture the bulk of the shape of a cross section of option prices,

while the subsequent singular vectors will add corrections to this general

behavior. This is a crucial feature of this SVD that leads us

to think that the singular bases of the restricted pricing operators are

appropriate tools to recover the RND . Interestingly, the

performance of our quadratic programming algorithm on real data

is indeed quite convincing (see 8 for details).

Readers interested in appending a full right tail to this estimated RND are

referred to [14], who proposes a simple method for

smooth pasting of parametric GEV tail distributions to an estimated

RND.

Here is the paper layout. We introduce the restricted call and put operators, and , and operators derived therefrom in 2. We detail the properties of operators and on the one hand, and and on the other hand, in 3 and 4, respectively. Other results relative to these four operators are reported in 5. 6 gives explicit expressions for the , and . The spectral recovery method (SRM) is detailed in 7. Finally, we run a simulation study in 8. An Appendix regroups some additional useful results.

2 Definitions and setting

Let us define the restricted call operator on the interval as the operator from into such that,

| (2.1) | |||||

It is a trivial fact that belongs indeed to . Let’s denote by the usual scalar product on and by the associated norm. Now, it is enough to notice that for all , and apply Cauchy-Schwartz inequality to obtain,

The adjoint operator of is such that, for all ,

Hence

| (2.2) | |||||

So that is nothing but the restricted put operator on the interval . In particular, we can write

| (2.3) | |||||

| (2.4) |

where

and

Let us now turn to the detailed inspection of these operators.

3 Results relative to and

Let us denote by the range of an operator of and by its null space (see [12, p.23]). Obviously both and are self-adjoint. This translates into the fact that their kernels are symmetric (meaning ). In addition, both and are continuous on the bounded square . Therefore, the associated operators are compact (see [12, Ex. 4.8.4, p.172]). As such, they verify the spectral theorem (see [12, Th. 4.10.1, 4.10.2, p.187-189]).

Theorem 3.1.

Given the operators and defined in 2.3 and 2.4 above, we have the following results.

-

1)

The operators and are compact and self-adjoint. As such, they admit countable families of orthonormal eigenvectors and associated to the same positive decreasing sequence of eigenvalues , which are complete in and , respectively.

-

2)

Besides, we have

where stands for the set of four times differentiable functions on .

-

3)

Furthermore, the orthonormal families and are complete in . In other words, they are both orthonormal bases of . In fact, we can write

where stands for the closure of in (see [12, p.16]) and for the set of (potentially infinite) linear combinations of elements .

-

4)

Therefore, and are both invertible and admit the fourth order differential operator as an inverse (see [12, p.155] for terminology). More precisely, we have got

and idem for .

-

5)

Finally, we have the following spectral decompositions,

and

Proof.

As detailed above, 1) follows directly from the spectral theorem. 2) follows directly from the kernel representations in 2.3 and 2.4. It can also be seen from the fact that, for any , both and are twice differentiable, which follows by simple inspection of 2.1 and 2.2. 3) follows directly from Proposition 5.1 below. 4) is a direct consequence of Lemma 8.1 below. Finally, 5) follows directly from 1) and 3). ∎

4 Results relative to and

The following theorem details the properties of the restricted put and call operators. It builds upon Theorem 3.1 above.

Theorem 4.1.

Given operators and defined in 2.1 and 2.2 above, we have the following results.

-

1)

Consider the sequence of positive decreasing singular values and singular vectors and defined in Theorem 3.1 above. The restricted put and call operators and are such that, for all ,

-

2)

Besides, we have

where stands for the set of two times differentiable functions on .

-

3)

In addition, we have . So that both and are invertible and admit the second order partial differential operator as an inverse. In particular, we obtain

(4.1) So that the knowledge of or/and allows to recover directly as their second derivative. This is nothing but the so-called Breeden-Litzenberger formula restricted to the interval .

-

4)

We have furthermore the following spectral decompositions,

and

-

5)

Finally, we have a put-call parity on the interval that can be written as follows

where we have defined .

Proof.

The proof of 1) follows directly from [13, p.37]. 2) follows by simple inspection of 2.2 and 2.1. The first part of 3) follows from the facts that and (see 1) above) and Theorem 3.1, item 3). The second part of 3) follows partly from Lemma 8.1 below (see Appendix) and partly from the obvious fact that for all (idem for ). 4) follows directly from 1) and 3). Finally, 5) follows immediately from the following obvious computations,

∎

We regroup other results relative to the above operators in the following section.

5 Other results relative to , , and

We prove here that both orthonormal families and are complete in . Other interesting results are to be found in the Appendix. Some of them are purely technical, while some others are of more general interest.

Proposition 5.1.

We have got,

where stands for the closure of in (see [12, p.16]) and for the set of (potentially infinite) linear combinations of elements .

Proof.

We know from [13, §2.3.] that,

Therefore, it is enough to show that both null-spaces reduce to the zero element. The kernel of is constituted by the functions that are solutions of

Deriving four times with respect to and applying Lemma 8.1 (see Appendix) leads to . So that . Now it is enough to notice that . However, we know from Lemma 8.2 that if and only if (see 8.1 for notation). Therefore , where by , we mean . ∎

6 Explicit computation of , and

6.1 Main result

In this section, we give explicit expressions for the singular bases and singular vectors of the restricted call and put operators. The results are gathered below in Theorem 6.1. Let us write

where

| (6.1) |

and, for all , is the smallest positive solution of the following fixed point equation in ,

Interestingly, the positive sequence decreases exponentially fast toward zero as detailed in Lemma 6.3. In addition, we write,

| (6.2) |

where the coefficients are such that,

Then, we have the following theorem.

Theorem 6.1.

Proof.

Notice readily that 6.6, 6.7 and the fact that both and are unit normed are straightforward consequences of 6.3. In addition, 6.4 is a repetition of Theorem 4.1, item 1). So that we are in fact left with proving 6.3 and 6.5. Each eigenvector of associated to the eigenvalue is solution of the problem,

| (6.8) |

for some and . After differentiating four times the latter equation with respect to (assuming that ) and applying Lemma 8.1, we obtain that the solutions of 6.8 are also solutions of the following fourth order ordinary differential equation,

where stands for the fourth order ordinary differential operator. Its characteristic polynomial admits four roots and . Consequently, the real solutions of the above ordinary differential equation are of the form

| (6.9) |

The s are thus of this form. Plugging this generic solution back into 6.8 leads in turn, after tedious but straightforward computations, to

| (6.10) |

where is a vector such that and is the matrix defined by

| (6.11) |

There exists a non-trivial solution to 6.10 if and only

if is such that the determinant of cancels, that is

. As detailed in Proposition

6.1, the roots of are exactly the

where is defined in 6.16. In

addition, we prove in Proposition 6.2 that the system

admits the unique solution . Reading off

6.9, we obtain that the eigenvector of

associated to eigenvalue writes as where both and are defined in

6.15. Now, it is enough to notice that, given the

properties of the sequence detailed in Proposition 6.3, and , . In addition, we

know from Lemma 6.1 that . This allows us to conclude that the eigenvalues of

are, without redundancy, the , , defined in

6.5 and the associated eigenspaces are unit-dimensional

and respectively spanned by the eigenvectors , , defined in 6.3.

Computing leads, after tedious but straightforward

computations to and concludes the proof.

∎

6.2 Additional results

This section contains a series of results that are used throughout the proof of Theorem 6.1 above. In this section we make use of the map such that for all .

Proposition 6.1.

Proof.

It follows from straightforward computations that,

| (6.14) |

Let us write and notice that if , then so that we must have for 6.10 to admit a non-trivial solution. To be more specific reduces to where . However the roots of are given by

Henceforth, cancels if and only if is solution of anyone of the two following fixed point equations,

The proof follows now directly from Proposition 6.3. ∎

Proposition 6.2.

Proof.

Lemma 6.1.

Proof.

It follows from straightforward computations using the fact that . ∎

Proposition 6.3.

Let us define the map such that for . Let us write

and consider the fixed point equations and . The set of corresponding solutions is exhausted by the sequence

| (6.16) |

where is defined in Lemma 6.3. In particular, notice that and for all such that . Notice in addition that, by construction, is solution of

This latter result, together with the fact that (see 6.14), leads straightforwardly to the following relationships,

Proof.

Consider the fixed point equation . Given the properties of detailed in Proposition 6.4, two cases arise depending

whether is positive or negative. In the case where is

positive, the exponential map meets at points of the form

for and some small but positive s. A direct application of Lemma 6.2 shows that the negative

solutions are exactly the .

The second fixed point equation can be rewritten

as . The positive solutions are of the form . And, from Lemma 6.2 again, the

corresponding negative solutions are the .

Let us write . It is clear that and for . In particular, is solution of

| (6.17) |

Let us define the map such that for all . We define such that , that is and , . By construction, exhausts the set of solutions of both fixed point equations and . In fact, is solution of

∎

Proposition 6.4.

Notice readily that , so that it is enough to study the properties of alone. We have the following results,

-

1.

is defined on the domain ;

-

2.

is periodic and such that, for all , ;

-

3.

Finally, is strictly increasing on and such that,

where we write (resp. ) to mean the limit from the above (resp. below).

-

4.

Notice that (resp. ) corresponds exactly to the set of all the zeros of (resp. ). Thus is the subset of containing all the points where both and are well defined and different from zero.

Proof.

Let us first focus on the domain of . It is defined on . However, can be extended by continuity to be worth zero at points . Notice indeed that for any small positive and , one has got

With a slight abuse of notations, we denote the latter extension by . So that is actually defined on . The other properties are straightforward. ∎

Lemma 6.2.

Recall that and are defined in Proposition 6.4. Notice first that is symmetric, meaning that if , then . For any , we have the following results,

-

1.

If is solution of the fixed point equation , then is also a solution.

-

2.

If is solution of the fixed point equation , then is also a solution.

Proof.

Notice first that we have the identity for any . Its proof is immediate. And therefore, for any solution of , we obtain . And idem for the solutions of . ∎

Lemma 6.3.

The sequence is such that, for all , is the smallest positive solution of the following fixed point equation in ,

In addition, the approximation holds true with a large degree of accuracy from onward.

Proof.

Let us write , for some small but positive such that is solution of 6.17. Notice that

So that 6.17 reduces to

Plugging-in the Taylor expansions above, we obtain

which can be rewritten as

| (6.18) |

It can be verified numerically that is a very good approximation of as soon as in the sense that 6.17 holds true with a very large degree of accuracy. ∎

7 The spectral recovery method (SRM)

In this Section, we first describe how and relate to the bid-ask quotes. We then show that the SVD of the restricted pricing operators described above can be used to design a simple quadratic program that recovers the smoothest RND compatible with market quotes.

7.1 From and to call and put prices

Let us denote by and the put and call prices at strike and by the corresponding risk neutral density. Let us furthermore write . We assume that the restriction to the interval of is in . For all , the following relationships are immediate.

| (7.1) | ||||

| (7.2) |

where we have defined,

Notice in particular that

7.1 shows that put prices directly relate to the restricted put operator. From an estimation perspective, this is a crucial feature that will allow us to recover the RND directly from market put quotes. Unfortunately, the situation is slightly different for call prices. As shown from 7.2, call prices relate to the restricted call operator via and , which are both unknown. Although, they could be estimated and give rise to an estimator of the RND based on quoted call prices, we wont pursue this route here, but rather focus on the simpler relation given by 7.1.

7.2 A refresher on no-arbitrage constraints

For a detailed review of model-free no-arbitrage constraints, the reader is referred to [21, p.32, § 1.8] and [11]. Let us denote by the price today of the underlying stock. Let us moreover assume that it pays a continuous dividend yield . Let us denote by the continuously compounded short rate and by the time to maturity. Let us recall first that, by no-arbitrage, put and call prices are related by the put-call parity.

| (7.3) |

Besides and . Let us now focus on put prices. We have,

| (7.4) | ||||

| (7.5) | ||||

| (7.6) |

Assume we are given an increasing sequence of strikes and a set of corresponding put prices . As described in [2], the above no-arbitrage relationships translate into a finite set of affine constraints on the latter put prices. These constraints can in fact be written in matrix form as , where stands for a matrix, is the vector such that and is a vector. More precisely, 7.6 translates into constraints as,

Moreover, the left-hand-side of 7.4 is fully captured in-sample by adding the following additional constraints,

| (7.7) |

The right-hand-side of 7.4 need not be taken into account at this stage. It is indeed less stringent than the upper-bound constraints we will impose in the next section. Finally, given the first constraints, 7.5 reduces to two additional constraints,

Finally, let us recall that if the forward price of the underlying stock is observable today, then, by no-arbitrage, it must be equal to .

7.3 Bid-ask spread constraints

Let us assume that the market provides us with an increasing sequence of strike prices , where typically ranges from to depending on the underlying. In addition, the market provides us with a corresponding sequence of bid ask quotes for put options. Let us denote them by and . We want the corresponding fitted put prices to lie inside the bid ask quotes. This corresponds to the following affine constraints,

| (7.8) |

The quoted strikes might possibly span a very small portion of the segment on which we want to recover the RND. In order to improve the quality of our estimator, we can constrain it to verify the above no-arbitrage constraints on a denser set of strikes than the quoted ones. Let us denote by this new set of strike prices, such that , and including the initial quoted strikes. For later reference, we denote by the subset of corresponding to the indexes of the initial quoted strikes. We know that, in any case, we must have , so that we can define . Furthermore, we know from 7.5 that cannot grow at a rate faster than , so that we can define to be the corresponding linear extrapolation of the right-most market quote , meaning . In summary, the requirement that the s fall in-between the bid-ask quotes translates into additional constraints, which we can write as follows

| (7.9) | |||||

| (7.10) |

All previously mentioned constraints are summarized in 2.

7.4 The quadratic program

Fix . The choice of will be discussed in the next Section. Let us denote by the estimator of the put price on built upon the ’s up to level and by the corresponding inverse image by . We have explicitly, from 7.1 and Theorem 4.1, item 4),

for some . Furthermore for a given matrix , we will denote by the sub-matrix obtained by extracting the rows of at indexes in and the columns of at indexes in . When extracting all the columns, we will write , and similarly for the rows. And we will naturally write in the case where is a vector. The SRM estimator is obtained as a solution of a quadratic program. It corresponds (modulo rescaling by the s and the discount factor) to the coefficients of the smoothest density that verifies the no-arbitrage and bid-ask constraints above. To that end, notice that the -norm of the second derivative of , namely , quantifies its smoothness. is often used as a smoothness penalty and has been widely used in the context of smooth RND recovery. Obviously, the smoother , the smaller . As detailed in Proposition 7.1, can be directly expressed as a quadratic form of involving the first eigenvalues of the restricted put operator . As a consequence, is solution of,

| (P1’) | subject to |

where, with a slight abuse of notations, we have written , stands for

the vector of initial put bid quotes and

stands for the vector of initial put ask quotes augmented with the no

arbitrage bounds and . Notice that we have added the

constraint , which does not arise as a natural property of

the s.

Denote by and,

similarly, write . Then we have and , where is defined below in Proposition

7.1. Let us finally

denote by the matrix whose rows are constituted by the

, and write . With these notations,

P1’ can be rewritten in canonical form as

| (P1) | subject to |

which is nothing but a quadratic program in . This result is due to the following Proposition.

Proposition 7.1.

Let us write and

| (7.11) |

which stands for the diagonal matrix whose diagonal entries are the for . Then

Proof.

Notice indeed that . However, as demonstrated above in Theorem 6.1, . Hence, using the property that the s constitute an orthonormal basis of , we obtain

∎

7.5 Properties of P1 and choice of the spectral-cutoff

A first question that arises is whether this quadratic program eventually

admits a solution? In that perspective, it is straightforward to

notice that P1 admits a solution if and only if

admits an element which satisfies the

constraints. Let us denote by the subset of which

satisfies the constraints described in P1’ and assume

that . Obviously, P1 admits a

solution as soon as is large enough, since is complete

in (see Proposition 5.1). On the other hand, it

admits no solution when , that is when the

constraints are incompatible. This latter situation might result from

the presence of spurious data, since the presence of an arbitrage in the

bid-ask quotes corresponds to a real arbitrage in the market, which

would certainly be arbitraged away by practitioners.

A second natural question that arises, is how to choose the spectral

cutoff ? As detailed in P1, we aim at recovering the

smoothest density built upon compatible

with price quotes. As described in Theorem 6.1,

is constituted of a periodic component oscillating

at frequency around an exponential trend , where

grows roughly speaking like . It is therefore natural to

think that the smaller , the smoother the singular basis functions

and thus the smoother the density built upon them (although this needs

not be the case, rigorously speaking). This intuitive observation, is

justified through simulations (see 5,

bottom graph). In practice, we therefore suggest to choose to be the smallest

such that P1 admits a solution. This is what we

actually do in the forthcoming simulation study.

Finally, let us point out that we could

have chosen to impose a positivity constraint on at each point

of the underlying dense grid , as an alternative

to the in-sample convexity

constraints on the s described in P1. However, we have

noticed via numerical simulations that results obtained in that way are less satisfying than

with the convexity constraints on the s. We therefore opted for

the convexity constraints.

8 Simulation study

We run a simulation study both on real and simulated data. The purpose of the

estimation on simulated data is mostly to show that the SRM returns a

valid RND estimator in extreme cases, when as little as

market quotes are available.

Recall from Lemma 6.3 that, from onward, we can write

in 6.1 above.

This approximation is not valid for . In that case, however, we can solve

6.17 numerically to obtain . This is the

value of we use in the following simulation study.

| Strike price | 500 | 550 | 600 | 700 | 750 | 800 | 825 | 850 | 900 | 925 |

|---|---|---|---|---|---|---|---|---|---|---|

| Best bid | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.10 | 0.00 | 0.00 | 0.00 | 0.20 |

| Best offer | 0.05 | 0.05 | 0.05 | 0.10 | 0.15 | 0.20 | 0.25 | 0.50 | 0.50 | 0.70 |

| Strike price | 950 | 975 | 995 | 1005 | 1025 | 1050 | 1075 | 1100 | 1125 | 1150 |

| Best bid | 0.50 | 0.85 | 1.30 | 1.50 | 2.05 | 3.00 | 4.50 | 6.80 | 10.10 | 15.60 |

| Best offer | 1.00 | 1.35 | 1.80 | 2.00 | 2.75 | 3.50 | 5.30 | 7.80 | 11.50 | 17.20 |

| Strike price | 1170 | 1175 | 1180 | 1190 | 1200 | 1205 | 1210 | 1215 | 1220 | 1225 |

| Best bid | 21.70 | 23.50 | 25.60 | 30.30 | 35.60 | 38.40 | 41.40 | 44.60 | 47.70 | 51.40 |

| Best offer | 23.70 | 25.50 | 27.60 | 32.30 | 37.60 | 40.40 | 43.40 | 46.60 | 49.70 | 53.40 |

| Strike price | 1250 | 1275 | 1300 | 1325 | 1350 | |||||

| Best bid | 70.70 | 92.80 | 116.40 | 140.80 | 165.50 | |||||

| Best offer | 72.70 | 94.80 | 118.40 | 142.80 | 167.50 |

8.1 Real data

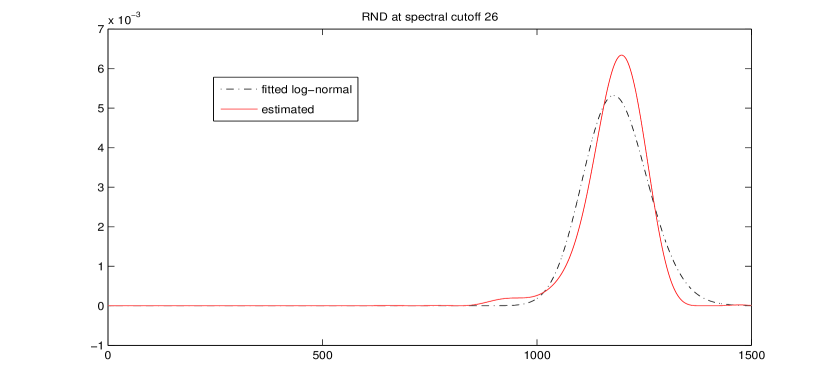

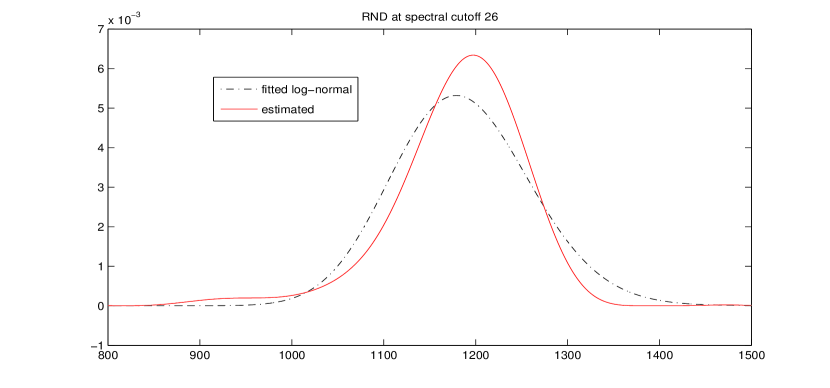

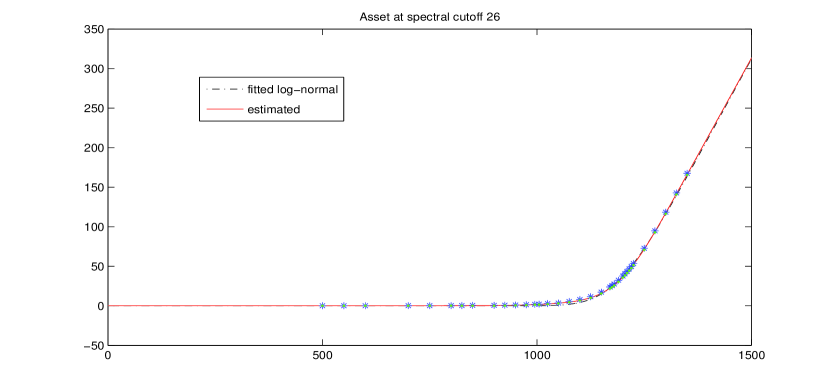

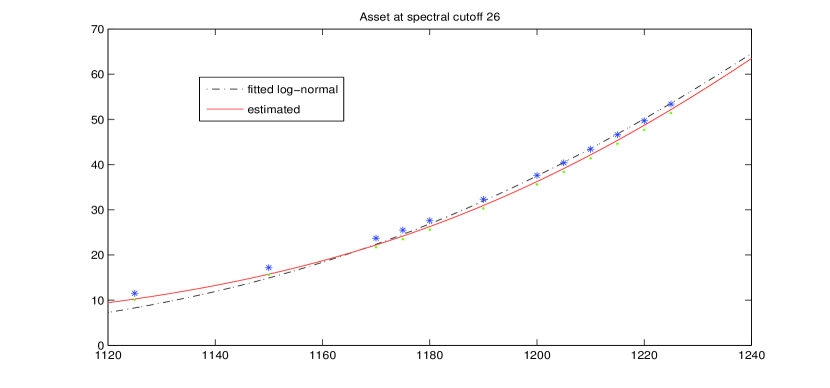

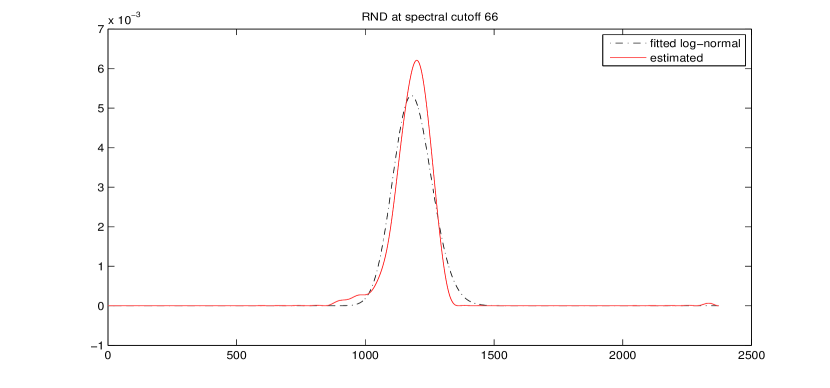

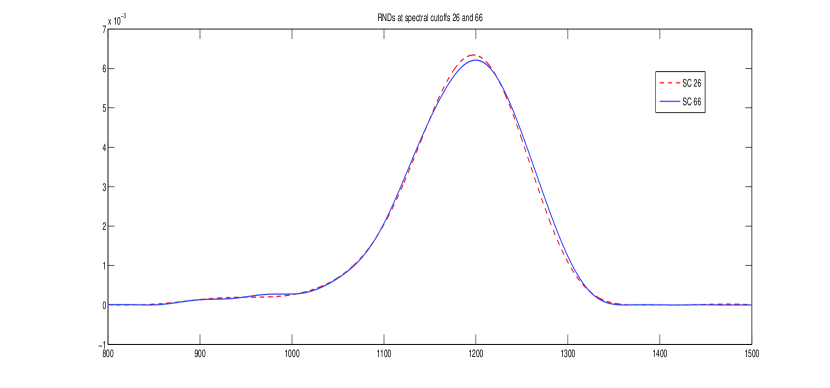

We use the bid ask quotes reported in [14, Table 1] for put options on the S&P 500 Index on January 5, 2005. For completeness, we reproduce the table here in 1. We choose , which corresponds to two times the Forward price on the underlying stock. This choice is arbitrary and produces an interval , which is symmetric around the forward price. We observe from our simulation that the result is largely independent of the choice of . However, the higher , the higher we will need to go into the spectrum of , since the smoothest RND that fits the data will be more and more concentrated around the center of the interval . As regards the constraints, we choose the grid to be such that and if , we add . Of course, this grid contains the initial quoted strike prices since they are integer valued. With the above choice of , the quadratic program given in P1 finds a feasible solution from spectral cutoff onward. We report below in 5. For the sake of comparison, we plot on the same figure the log-normal distribution obtained by least-square fit to the put prices obtained as average of the bid-ask quotes. The only parameter of the log-normal distribution that must be fitted is (see Proposition 8.1), and we find . Interestingly, displays a small bump at the beginning of its left-tail, which does not appear in [14, Fig. 8] and could hardly be accounted for by parametric methods. Notice the small blip next to in 5. This boundary effect is due to the fact that all the s and their first derivative are worth in . In order to show that the choice of has very little impact, we compute the RND estimator for . Results are reported in 3. As was expected, first feasible points appear at much lower spectral cutoffs, namely from spectral cutoff onward. Therefore, we plot . As can be seen from 4, the put prices arising from P1 lie inside the bid ask quotes, while the ones produced by the fitted log-normal density lie outside.

8.2 Simulated data

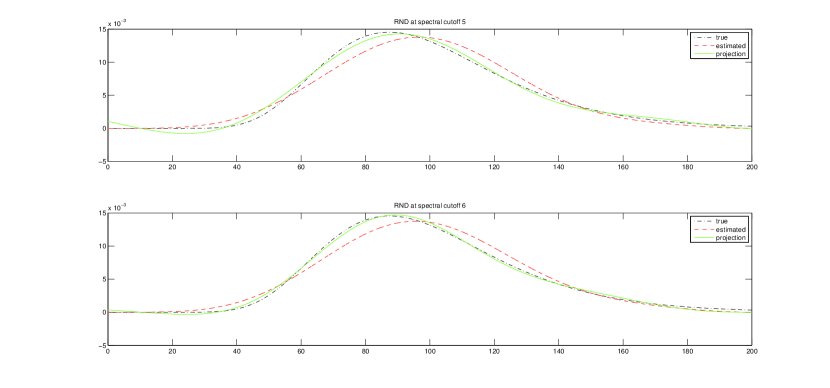

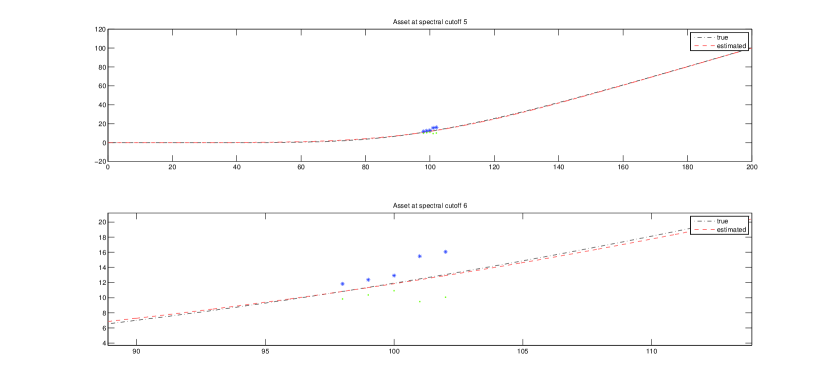

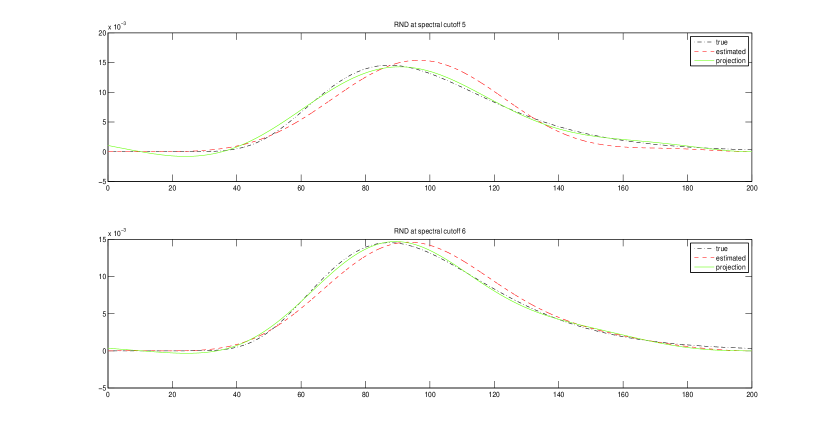

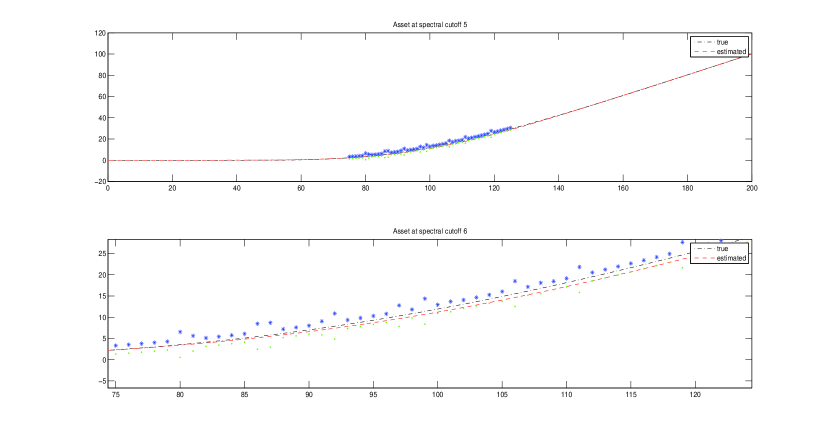

As regards the simulated data, we work in the Black-Scholes setting. In that context the price of a put option admits a closed form solution and the RND is log-normal (see Proposition 8.1). We model the bid-ask spread as a random noise around the true price given by the Black-Scholes formula. More precisely, for a given set of quoted strikes and corresponding put prices , we write and , where , the ’s are iid standard normal random variables and . The bounds and are chosen by analogy with the real data quotes in 1. Of course, the bid-ask quotes we obtain in that way are not arbitrage free. However, they contain the true put price , which, given the nature of the quadratic program described in P1 above, is all that matters to approximate the true RND. For the sake of simplicity, we choose , , , , and and . In addition we set a first strike price at and spread the others on its left and right sides at unit length distance away from each other until we obtain strikes. More precisely, the second strike would be , the third , the fourth and so on and so forth. We plot the results for the first two spectral cutoffs at which a feasible point is found below in 6 in the case where there are as little as bid ask quotes and in 7 in the case where there are as many as of them. In any case, we can see that we obtain a smooth density that resembles the log-normal density generating the initial quoted prices and that the estimate is stable from one spectral cutoff to another. Of course, the more strikes we have, the better the fit. Besides, we observe as expected from an other simulation not reported here that, the smaller the bid-ask spread, the better the fit. Notice once again that the fitted right-tail reaches zero in , while the true one is strictly positive at that point. As before, this is due to the fact that .

Appendix

Refresher on the Black-Scholes model

This is a well-known result of mathematical finance.

Proposition 8.1.

Let us denote by the price today of a stock paying dividends continuously over time at a constant rate and by the continuously compounded risk-free rate. The arbitrage price today of a put option on that stock maturing at time is given by the following closed form formula,

with

where stands for the volatility of the stock and for the standard normal cumulative distribution. In addition, the RND is log-normal and writes as

Proof.

These results can be found in see [21, p.117], for example. ∎

Additional results relative to and

We now present three results relative to and , which are either used in the core of the paper or of interest in their own right.

Proposition 8.2.

The operators and admit no eigenvectors.

Proof.

Suppose is an eigenvector of associated to eigenvalue , then denote by

| (8.1) |

and notice that for all , a direct application of Lemma 8.2 allows to write

Thus must be an eigenvector of . However, it is well known that admits no eigenvalue since, for any ,

defines a homogeneous Volterra equation in , whose unique trivial solution is (see [12, p.239, Th. 5.5.2]). ∎

Finally, let us point out the two following useful lemmas.

Lemma 8.1.

Let us denote by the order partial differential operator with respect to . Then, for any , we have the following results.

Proof.

Notice indeed that

Therefore, we obtain immediately

The remaining of the proof follows directly from these first results. Notice indeed that,

which concludes the proof. ∎

Lemma 8.2.

For any and , we have (see 8.1 for notations).

Proof.

Perform the change of variable to obtain

∎

Relation between the s and the s

We believe that and could be readily estimated from the data, so that 7.2 could be used to construct a second estimator of the RND based on the restricted call operator. This second estimator could eventually be combined with the one obtained from the SRM above. To that end, and for the sake of completeness, we compute the scalar products between elements of the two singular bases. Results are reported in the following proposition.

Proposition 8.3.

Let us write

Then, we have the following relationships,

On the way, we obtain,

Proof.

Recall that, for all , we have defined

Besides, we have that

Therefore, we obtain the following relationships,

Which leads to

Now, it remains to compute and . The results follow from lengthy and tedious but straightforward computations and are therefore not reported here. ∎

From the RND of to the density of

Some authors have chosen to focus on the estimation of the density of rather than on the density of itself. Both densities relate by a simple transformation, as described in the following proposition. In our case, this transformation can be readily applied since the SRM returns an analytic expression for the estimated RND.

Proposition 8.4.

If admits for density on , then admits for density on . Conversely, if admits for density on , then admits for density on .

Acknowledgments

The author is deeply grateful to Peter Tankov for his careful reading of this manuscript and for his constructive and insightful comments, which greatly contributed to improve its clarity and content. The author is of course solely responsible for any eventual remaining error. Finally, the author would like to acknowledge interesting conversations with Gérard Kerkyacharian and Dominique Picard.

References

- [1] Peter A. Abken, Dilip B. Madan, and Sailesh Ramamurtie, Estimation of risk-neutral densities by Hermite polynomial approximation: with an application to eurodollar futures options, Federal Reserve Bank of Atlanta, working paper no. 96-5, (1996).

- [2] Yacine Aït-Sahalia and Jefferson Duarte, Nonparametric option pricing under shape restrictions, J. Econometrics, 116 (2003), pp. 9–47.

- [3] Bhupinder Bahra, Implied risk-neutral probability density functions from option prices: theory and application, Bank of England, working paper no. 1368-5562, (1997).

- [4] Fischer Black and Myron Scholes, The pricing of options and corporate liabilities, J. Polit. Econ., 81 (1973), pp. 637–654.

- [5] Oleg Bondarenko, Estimation of risk-neutral densities using positive convolution approximation, J. Econometrics, 116 (2003), pp. 85–112.

- [6] Douglas T. Breeden and Robert H. Litzenberger, Prices of state-contingent claims implicit in option prices, J. Bus., 51 (1978), pp. 621–651.

- [7] Ruijun Bu and Kaddour Hadri, Estimating option implied risk-neutral densities using spline and hypergeometric functions, Econometrics J., 10 (2007), pp. 216–244.

- [8] Peter W. Buchen and Michael Kelly, The maximum entropy distribution of an asset inferred from option prices, J. Finan. Quant. Anal., 31 (1996), pp. 143–159.

- [9] Rama Cont, Beyond implied volatility: extracting information from option prices, in Econophysics: an emergent science, J. Kertész and I. Kondor, eds., Dordrecht, Kluwer, 1997.

- [10] John C. Cox and Stephen A. Ross, The valuation of options for alternative stochastic processes, Journal of Financial Economics, 3 (1976), pp. 145–146.

- [11] Mark H. A. Davis and David G. Hobson, The range of traded option prices, Math. Finance, 17 (2007), pp. 1–14.

- [12] Lokenath Debnath and Piotr Mikusiński, Introduction to Hilbert spaces with applications, Academic Press, 1990.

- [13] Heinz W. Engl, Martin Hanke, and Andreas Neubauer, Regularization of inverse problems, Kluwer Academic Publishers, 1996.

- [14] Stephen Figlewski, Estimating the implied risk neutral density for the U.S. market portfolio, in Volatility and time series econometrics: essays in honor of Robert F. Engle, Tim Bollerslev, Jeffrey R. Russel, and Mark Watson, eds., Oxford University Press, 2008.

- [15] Paul R. Halmos, What does the spectral theorem say?, Am. Math. Mon., 70 (1963), pp. 241–247.

- [16] Ludger Hentschel, Errors in implied volatility estimation, J. Finan. Quant. Anal., 38 (2003), pp. 779–810.

- [17] Jens Carsten Jackwerth, Option-implied risk neutral distributions and risk aversion, Research Foundation of AIMR (CFA Institute), 2004.

- [18] Jens Carsten Jackwerth and Mark Rubinstein, Recovering probability distributions from option prices, J. Finance, 51 (1996), pp. 1611–1631.

- [19] Robert Jarrow and Andrew Rudd, Approximate option valuation for arbitrary stochastic processes, J. Finan. Econ., 10 (1982), pp. 347–369.

- [20] Robert C. Merton, Theory of rational option pricing, Bell J. Econ. Manag. Sci., 4 (1973), pp. 141–183.

- [21] Marek Musiela and Marek Rutkowski, Martingale methods in financial modeling, ed., Springer-Verlag, 2008.

- [22] Marc Potters, Rama Cont, and Jean-Philippe Bouchaud, Financial markets as adaptive systems, Europhys. Lett., 41 (1998), pp. 239–244.

- [23] Michael Stutzer, A simple approach to derivative security valuation, J. Finance, 51 (1996), pp. 1633–1652.