Towards the full information chain theory: solution methods for optimal information acquisition problem

Abstract

When additional information sources are available in decision making problems that allow stochastic optimization formulations, an important question is how to optimally use the information the sources are capable of providing. A framework that relates information accuracy determined by the source’s knowledge structure to its relevance determined by the problem being solved was proposed in a companion paper. There, the problem of optimal information acquisition was formulated as that of minimization of the expected loss of the solution subject to constraints dictated by the information source knowledge structure and depth. Approximate solution methods for this problem are developed making use of probability metrics method and its application for scenario reduction in stochastic optimization.

pacs:

02.50.Cw, 02.50.Le, 89.70.CfI Introduction

In many practically important decision making problems where uncertainty about input data is present and optimization methods are appropriate, sources of additional information are in principle available. Often, information that such sources possess fails to be taken advantage of due to its perceived and factual imprecision and to the lack of methodology that allows doing this in a regular controlled fashion. Such methodology, if developed in a general setting, would form a branch of the science of information which is at present represented by the classical Information Theory and its extensions. Generalizing somewhat, one can say that Information Theory explores the implications of information quantity while abstracting from the information content and, in particular, its accuracy and relevance. Respectively, the classical Information Theory is predominantly a theory of information transmission and related activities (such as compression). On the other hand, if information is to be acquired and used for decision making, a quantitative framework describing these processes would be rather helpful.

A notion of full information chain was introduced in Perevalov and Grace (2012a, b) to schematically describe the typical path of information from acquisition to usage (see Fig. 1 for an illustration). In this context, the classical Information Theory is a theory of the middle link, while the methodology developed in Perevalov and Grace (2012a, b, c) and the present article concerns the basics of a general theory of the two end links. More specifically, the information acquisition link was addressed in Perevalov and Grace (2012a, b), and the basic framework for the information use link was proposed in Perevalov and Grace (2012c) resulting – after making a connection with the results of Perevalov and Grace (2012a, b) – in a formulation of the optimal information acquisition problem. This article builds on these results and proposes specific solution methods for the optimal information acquisition problem.

The proposed approach, as was mentioned earlier, can be looked upon as an attempt to initiate a process of extending the classical Information Theory to a theory of the whole information chain. The field of Information Theory, born from Shannon’s work on the theory of communications Shannon (1948), since have enjoyed great success in a number of fields that include, besides communication theory, statistical physics Jaynes (1957a, b), computer vision Viola (1995), climatology Mokhov and Smirnov (2006); Verdes (2005), physiology Katura et al. (2006) and neurophysiology Chávez et al. (2003). Generalized Information Theory (see e.g. Klir and Harmanec (1996), Maeda and Ichihashi (1993); Harmanec and Klir (1994)) addresses problems of characterizing uncertainty in frameworks that are more general than classical probability such as Dempster-Shafer theory Shafer (1976).

The approach developed here is based on a theory of information exchange between the agent and information source(s) that is developed in Perevalov and Grace (2012a, b). The latter can be thought of as a development of the general theory of inquiry that goes back to the work of Cox Cox (1946, 1961, 1979). This line of work received more attention recently resulting in a formulation of the calculus of inquiry Knuth (2005, 2007, 2008). The definition of questions adapted in Perevalov and Grace (2012a) corresponds to the particular subclass of questions – the partition questions – defined in Knuth (2005). It is also related to the measure-dependent notion of a question introduced in Caticha (2004). Our work in Perevalov and Grace (2012a, b) goes beyond that on the calculus of inquiry in that it introduces the concept of pseudoenergy as a measure of source specific difficulty of various questions to the given information source. One could say that it develops a quantitative theory of knowledge as opposed to the theory of information.

One of successful applications of the order-theoretic approach to fundamental physics is the recent derivation Knuth and Bahreyni (2010) of Lorentz transformations and Minkowski metric of special relativity directly from the consideration of the partial order of events in space-time.

Information Physics Caticha (2012a) is a relatively new branch of physical sciences that studies the role information plays in fundamental laws of nature. This line of research goes back to the defining work of Jaynes Jaynes (1957a, b) on the application of the Principle of Maximum Entropy (MaxEnt) to derive the fundamental laws of thermodynamics. It is related to the proposed framework in that it addresses information relevance in application to physical sciences. The main Information Physics hypothesis is that the laws of nature are essentially the laws of inductive inference correctly applied to respective systems. In order to correctly formulate them one needs to know the degrees of freedom and the relevant information necessary to completely specify the system state. Recently, this approach (in modified and extended form) was applied to derive the fundamental laws of classical Caticha and Cafaro (2007) and quantum Caticha (2011) mechanics, and also – very recently – relativistic quantum theory Caticha (2012b). A closely related line of research explores the ramifications of general order-theoretic relations. An interesting example of the latter is the derivation Knuth and Bahreyni (2010) of Lorentz transformations and Minkowski metric of special relativity directly from the consideration of the partial order of events in space-time.

The area of statistical decision making has dealt with the idea of improving solution quality by means of acquiring additional information. There have been applications to innovation adoption McCardle (1985), Jensen (1988), fashion decisions Fisher and Raman (1996) and vaccine composition decisions for flu immunization Kornish and Keeney (2008) can be mentioned in this regard. Some authors Fischer et al. (1996), Ellison and Fudenberg (1993) even introduced models (e.g. effective information model) for accounting for the actual, or effective, amount of information contained in the received observations. One could also mention the recent work on optimal decision making in the absence of the knowledge of the distribution shape and parameters Huh and Rusmevichientong (2009); Levi et al. (2007); Bassamboo and Zeevi (2009). The difference of the proposed approach is in that it explicitly describes and allows to optimize over not just the quantity of additional information but also its content and is based on explicit description of properties of information sources.

The related problem of optimal usage of information obtained from experts has been addressed in existing research literature mostly in the form of updating the agent’s beliefs given probability assessment from multiple experts French (1985); Genest and Zidek (1986); Clemen (1987); Clemen and Winkler (1999) and optimal combining of expert opinions, including experts with incoherent and missing outputs Predd et al. (2008). In the present and preceding papers, the emphasis is on optimizing on the particular type of information for the given expert(s) and decision making problem.

Methodologically, the present article borrows from the field of probability metrics and scenario reduction in stochastic optimization. More details, along with relevant references, can be found in Appendices.

The rest of the paper is organized as follows. In Section II, main results of Perevalov and Grace (2012a, b) that are necessary for the developments in this paper are reviewed. Section III reviews main results of Perevalov and Grace (2012c) where, in particular, the problem of additional information acquisition was formulated in the specific form that is used here. Section IV develops the main theoretical framework for the use of scenario reduction methods for optimization of additional information acquisition. Section V provides an example illustrating the use of methods developed in Section IV. Section VI contains a conclusion. Appendix A provides proofs for some of the results in the main text, Appendix B gives some background information on probability metrics in application to stochastic optimization, and Appendix C contains a very brief review of scenario reduction algorithms.

II Information Accuracy: Source Knowledge Structure

As was explained in Perevalov and Grace (2012c), the starting point of the whole discussion is a problem of the general form

| (1) |

where is the set of all feasible solutions, is a parameter space to which uncertain problem parameters belong, and is a fixed initial probability measure (with a suitable sigma-algebra assumed) on that describes the initial state of the uncertainty. The function : is assumed to be integrable on for each . For example, in the context of stochastic optimization, is the set of feasible first-stage solutions and is the best possible objective value for the first stage decision in case when the random outcome is observed.

Let be the expected loss corresponding to measure defined as follows.

| (2) |

where is a solution of (1) and is a solution of for the given .

The main goal is, as explained in Perevalov and Grace (2012c), for the given information source(s), to find the way of extracting information from it so that the resulting expected loss is minimized. The knowledge structure of the source determines the accuracy of source’s answers. The difference between the original loss (2) and the loss obtained with the help of the source’s answers serves as a measure of the information relevance.

The process of information exchange between an agent and an information source was described in Perevalov and Grace (2012a, b). Here we review the main results to make the presentation self-contained. The source is characterized by its knowledge structure encoded in the form the question difficulty functional described below. The agent poses questions for which the source provides answers.

Questions were identified in Perevalov and Grace (2012a) with partitions of the parameter space of the problem. Partitions were allowed to be incomplete, i.e. such that . The question difficulty functional was introduced to measure the degree of difficulty of the question to the given information source, so that the information source would be able to answer questions with lower values of the difficulty functional more accurately that those with higher values of difficulty. The specific form of the difficulty functional was determined in Perevalov and Grace (2012a) by demanding that it satisfy a system of reasonable postulates that, in particular, imposed the requirements of linearity and isotropy. The resulting form of the difficulty functional is given in the following theorem.

Theorem 1

Let the function where satisfy Postulates 1 through 6 (see Perevalov and Grace (2012a)). Then it has the form

where and : is an integrable nonnegative function on the parameter space .

One can see that the difficulty of the given question depends on, besides the initial probability measure , the function : on the parameter space . Using parallels with thermodynamics (see Perevalov and Grace (2012a) for more details), this function may be called the pseudotemperature. The question difficulty then can be interpreted as the amount of pseudoenergy associated with question .

Given a question , the information source can provide an answer that takes one of values in the set . A reception of the value has an effect of modifying the original probability measure on to a new (updated) measure . To ensure the the answer is in fact an answer to the (complete) question (and no more) the following condition is required to hold for the updated measures , :

| (3) |

where , , are nonnegative coefficients such that for .

The answer depth functional for the answer to question measures the amount of pseudoenergy that is conveyed by in response to question . The general form of can be established if certain reasonable requirements (postulates) it has to satisfy are imposed. A system of postulates proposed in Perevalov and Grace (2012b) that parallels the postulates for question difficulty and, in particular, imposes the requirements of linearity and isotropy. The following theorem was then proved in Perevalov and Grace (2012b).

Theorem 2

The answer depth functional has the form

where is the measure on updates by the reception of and and the function : is the same function that is used in the question difficulty functional .

It can be shown (see Perevalov and Grace (2012b) for details) that if is any answer to the question then with equality if and only if the answer is perfect, i.e. for .

As far as answers that are not perfect are concerned, it is convenient to consider the class of answers for which the degree of imperfection is described by a single error probability – the quasi-perfect answers Perevalov and Grace (2012b). For a quasi-perfect answer to a (complete) question , the coefficients have the form for and , and the updated measure is simply

for . Clearly, for a quasi-perfect answer to becomes a perfect one. It can be shown (see Perevalov and Grace (2012b)) that the answer depth functional for a quasi-perfect answer to question can be written as

which can be seen to reduce to for (when ) and vanish for .

An information source model provides a connection between questions and the corresponding answers. It was defined in Perevalov and Grace (2012b) as a function : such that

The simplest information source model considered in Perevalov and Grace (2012b) is the simple capacity model given by

| (4) |

which is fully characterized by the single parameter which has the meaning of the information source capacity. The most apparent drawback of model (4) is that, according to it, the source provides a perfect answer to any question with difficulty not exceeding the source capacity. The linear modified capacity model described by

| (5) |

removes this drawback at the expense of one extra parameter that has to be estimated. Several other models were proposed in Perevalov and Grace (2012b).

The values of model parameters as well as pseudotemperature functions for information sources can be estimated from the observed sources’ performance on sample questions. The corresponding estimation procedures were also discussed in Perevalov and Grace (2012b).

III Information Relevance: Loss Reduction

The basic framework for the information use link description was presented in Perevalov and Grace (2012c). We briefly summarizes the main points here to make a transition to the subject of this article in a self-contained manner.

Consider the set of all maps from into with a discrete image set. Any such map can be uniquely described by the corresponding partition of and the corresponding image set such that for all . Let be any probability measure on , let an arbitrary element of the solution space , and let be an arbitrary map from into . The suboptimality, loss and gain functionals are defined (Perevalov and Grace (2012c)) as follows.

| (6) |

| (7) |

and

| (8) |

respectively.

Moreover, it is convenient to introduce the corresponding functionals not just for a fixed measure , but also for the given question and a given answer , For example, for an arbitrary , the suboptimality of solution with respect to question (and initial measure ) is given by

| (9) |

and the suboptimality of with respect to answer to question (and initial measure ) reads

| (10) |

where for brevity. The loss and gain functionals for the given map and question and answer are defined analogously.

Note that each map from the set can be characterized by the corresponding loss with respect to the original measure and the value – the difficulty of the corresponding question. The efficient frontier in the Euclidean plane with coordinates can be found by solving the following parametric optimization problem

| (11) | ||||||

| subject to |

for all values of the parameter .

The maps that are solutions of (11) for various values of the parameter possess the property of having the smallest possible loss among the maps corresponding to questions whose difficulty does not exceed the given value . We denote by the subset of all maps in that are solutions of (11) and by the set of all subset-optimal maps, i.e. maps of the form , where is an optimal solution of problem (1) with measure replaced with the conditional measure . Then, as was shown in Perevalov and Grace (2012c),

| (12) |

i.e. if one is interested in finding Pareto-optimal maps in it is sufficient to consider subset-optimal maps only. We call a partition optimal if the corresponding map belongs to the set of Pareto-optimal maps. So the problem of finding maps in the set is equivalent to that of searching for optimal partitions of the parameter space .

Let us now address the optimal information acquisition problem (14): what question(s) need to be asked the given information source in order to obtain the minimum possible loss for (1). Given a question to an information source and its answer taking values in the set , we denote by , the minimum conditional expected loss given that and by the minimum expected loss that the agent can achieve given the answer . The latter can be found as

| (13) |

i.e. as an expectation over possible values of the answer .

If the agent poses a question to the information source and receives a particular value of answer , the original measure on gets updated to . Therefore, in order to minimize loss for the given value of answer , the agent needs to choose the solution – the solution minimizing the expectation over all (feasible) values of .

The next two propositions, proved in Perevalov and Grace (2012c), give the minimum expected loss achievable with a perfect and a general answer to question , respectively.

Proposition 1

Let be a complete question and be a corresponding subset optimal map. If the agent is given a perfect answer to then

Proposition 2

Let be a complete question and be a corresponding subset optimal map. If the agent is given a (generally imperfect) answer to then

The information acquisition optimization problem can then be written as

| (14) | ||||||

| subject to |

where the minimum expected loss is given by either Proposition 1 or Proposition 2. The source model function and the pseudotemperature function that enters the expressions for the question difficulty and answer depth in (14) are assumed to be known.

It’s easy to see that if a source is capable of providing perfect answers (for instance, in the simple linear model) solution of problem (14) reduces to finding the efficient frontier: if is the expression describing the efficient frontier (abstracting from its true discrete structure) and is the capacity of the information source, then the minimum in (14) is equal to and is achieved by the question lying on the efficient frontier such that .

If a source cannot provide perfect answers, questions with difficulty exceeding the source capacity need to be considered in order to minimize the expected loss. The search for an optimal question in this case becomes more complicated as the error structure for the source’s answers needs to be taken into account. If answers are assumed to be quasi-perfect, optimal question(s) can be found approximately provided the efficient frontier is already known.

IV Information Acquisition Optimization

As stated in the previous section, a solution of the optimal information acquisition problem (14) is greatly facilitated by the search for the efficient frontier in the set of all questions. To find the latter, one needs to determine optimal partitions of the parameter space . It turns out that the methods of measure (scenario) reduction developed previously for solving stochastic optimization problems can be also helpful for the task of searching for optimal partitions.

IV.1 Measure reduction and optimal partitions

In the following, we assume that the (initial) probability measure is supported at a discrete set :

| (15) |

where is a Dirac delta that puts a unit mass at . Points are usually referred to as scenarios. The scenario reduction methodology (see Appendix C) is often used in stochastic optimization to lower computational complexity of various practically important problems. In scenario reduction approach, the original discrete measure given by (15) is said to be reduced to another discrete measure given by

| (16) |

if the support of is a subset of .

For later convenience, we denote by the set of all scenario reduction maps from the set of measures of the form (15) supported at into the set of all measures of the form (16) supported at some subset of of cardinality satisfying the additional property that we call simplicity. A map is called simple if there exists a partition of the set of scenarios such that for all and . In such a case we write and for .

Additionally, if : is some symmetric cost function, we call a map -optimal if for . It is shown in Heitsch and Römisch (2003) that the Monge-Kantorovich functional (see Appendix B) is minimized for all measures supported at iff the corresponding simple scenario reduction map is -optimal.

In the following we call measures and -equivalent for some partition of if for all . It is easy to see that measures and are -equivalent for all possible partitions if and only if , but two distinct measures can easily be -equivalent for a specific partition . In particular, any two measures on are -equivalent if is the trivial partition .

Given a probability measure on and some measure that was obtained from by a reduction, let us denote by the virtual pseudoenergy content of measure relative to . It is defined as follows.

| (17) |

i.e. is the difference between the difficulties of exhaustive questions associated with measures and , respectively. One can think about the virtual pseudoenergy of relative to as an amount of pseudoenergy a source would need to supply in order to obtain a new state in which the hardest possible question has a difficulty equal to . Since no question is in fact answered in going from measure to the reduced measure , we call this pseudoenergy virtual.

We can now introduce the virtual difficulty of question for measure with respect to measure :

| (18) |

In particular, , i.e. the virtual difficulty of for measure relative to reduces just to the standard difficulty of .

It also turns out to be useful to introduce the relative expected loss for partitions of and measures obtained from the original measure by a (simple) scenario reduction operation. In other words, we assume that there exists for some value of such that . The relative (to measure ) expected loss of partition and measure is then defined as follows.

| (19) |

where is the subset-optimal map for partition and measure . In particular, if is the trivial partition , the loss of relative to is simply111Here and later we omit the trivial partition from the list of arguments of and . . If the measure coincides with , the loss relative to is just the standard expected loss of the corresponding subset-optimal map: .

Let us now consider the following construction. Reduce the original measure to that is supported at points: , where . Let and let the preimage of under map : for all . Then let be a partition of such that for . We say that the partition is generated by the map , or, equivalently by the reduction of measure to . Let be an arbitrary coarsening of .

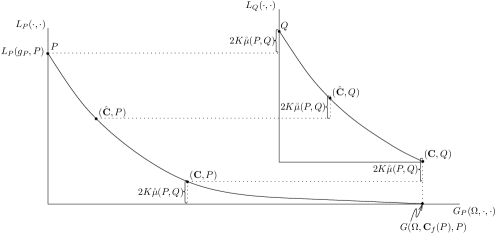

We are interested in the location of points , , , , and on the plane with coordinates . First of all, it is clear that and where is the EVPI of problem (1). Second, it is also clear that

| (20) |

since by construction of . In words, the virtual difficulty of the question for measure where the partition was generated by a reduction of the original measure to is equal to the difficulty of the exhaustive question for the original measure .

To obtain relationships between relative expected losses the following two auxiliary lemmas are needed.

Lemma 1

Let , be a symmetric matrix with elements satisfying the triangle inequality . Let be a probability distribution. Then

Proof: See Appendix A.

The second lemma states a useful probability metrics result. Let be a discrete support probability measure on and let be another such measure. Let be a Fortet-Mourier metric for some cost function : that satisfies conditions described in Appendix B. Finally, let be a partition of such that the measures and are -equivalent.

Lemma 2

Under assumptions described above,

1. , where .

2. If is generated by some map that is -optimal, where is the reduced cost function defined as in (30) then

.

Proof: See Appendix A.

Now, assume that the integrand in (1) is in class defined in Appendix B for some symmetric cost function : that satisfies the conditions described in Appendix B. The following proposition describes a relation between relative expected losses for measures and .

Proposition 3

Let be a partition of generated by a reduction of a measure with support at to by means of a -optimal map and let any coarsening of (including itself). Then

where is some constant that does not depend on measures and .

Proof: See Appendix A.

If we use the trivial partition (which is obviously a coarsening of any ) in Proposition 3 we can obtain an upper bound on the relative loss of with respect to which we formulate as a corollary.

Corollary 1

The loss of reduced measure relative to can be bounded from above as

where is the EVPI of the original problem (1).

The following proposition relates the expected loss of a subset-optimal map based on a partition generated by a reduction of the original measure to measure to the Fortet-Mourier distance between and .

Proposition 4

Let be a partition of generated by a reduction of a measure supported at the discrete set to measure by means of a -optimal map . Then

where is a constant.

Proof: See Appendix A.

Fig. 2 shows the locations of various points on coordinate plane.

Several useful observations can now be made.

-

•

The result of Proposition 4 suggests that good (near-optimal) partitions of can be generated by a reduction of the original measure to a measure that is (i) supported at a few points and (ii) has a low value of the Fortet-Mourier metric . The latter value of the Monge-Kantorovich functional with the reduced cost can be computed as that of a minimum-cost transportation problem.

-

•

For a wide class of linear multi-period two stage stochastic optimization problems, the relevant cost function is given by (see Appendix B) with where is the number of periods. The corresponding minimum cost transportation problem can easily be solved exactly for fixed support of measure and approximately if the support itself needs to be optimized (see Appendix C for details).

-

•

The optimality “price” one pays for scenario reduction from the original measure to a simpler measure – which can be thought of as adding information that’s minimally relevant to the problem in question without actually finding it – can be estimated by the amount . This implies, in particular, that one could do a scenario reduction before starting the search for the efficient frontier. In fact, scenario reduction and additional information acquisition are complementary to each other in the sense of information: scenario reduction, as already mentioned, can be thought of as an addition of information that’s minimally relevant as opposed to information acquisition optimization, where one looks for maximally relevant information.

It is now possible to formulate an efficient approximate algorithm for optimal partition determination.

IV.2 Efficient frontier algorithm

Proposition 4 provides a useful tool for approximating the efficient frontier. Specifically, one can use the following algorithm (here and later we assume that the original measure on has a support at a discrete set consisting of points).

-

1.

Choose an integer parameter .

-

2.

Choose an appropriate cost function : such that for all . Let be the corresponding reduced cost function.

-

3.

Reduce the original measure to measure supported at points in the set , i.e. find a -optimal map such that .

-

4.

Let be any partition of generated by the map .

-

5.

Let the map be a subset-optimal map corresponding to partition .

Varying the value of parameter from 2 upwards one can obtain a series of maps in the set that are (approximately) Pareto-optimal. Step 2 of the above algorithm is essential for its feasibility. For example, if the problem (1) is a linear multi-period stochastic optimization problem, the cost function of the form (34) can be used. In step 3, finding the measure supported at points that minimizes the value of Monge-Kantorovich functional is an NP-hard problem Heitsch and Römisch (2003) but approximate algorithm such as fast forward selection algorithm are available (see Appendix C).

Using the algorithm described above, one can obtain one approximately Pareto-optimal map for each value of the chosen integer parameter. If more Pareto-optimal maps are needed (especially in the region with lower values of pseudoenergy) additional heuristics can be used. For instance, one could begin with the algorithm described above for some relatively high value of and then merge some of the resulting subsets into one giving rise to a partition with a lower value of . Clearly, this can be done in ways, where is the -th Bell number which is just the number of all different partitions of a set consisting of elements and that can be found from the recursive relation and . (For example, the Bell number for the lower values of are , , , , , , .)

We see that if the original chosen value of is not very high this would lead to a manageable number of partitions. Additionally, scenario reduction can be used to reduce computational complexity of finding the values for subsets of resulting partitions. On the other hand, if the original value of makes evaluation of all maps that can be obtained this way computationally prohibitive, a heuristic algorithm described by the following pseudo-code can be used. It finds another partition, with a lower value of , so that the subset merging procedure can be applied.

The goal of the algorithm represented by the pseudo-code is to identify subsets which are locally compact but as far away from one another as possible. In each step , we find the average distance of each subset center remaining in the index set to only the other remaining centers. The center, and therefore the associated subset, with the largest average distance is chosen and removed from the set . The remaining subsets are then merged into a single set.

So far the pseudotemperature function has not been taken into account. It is clear, on the other hand, that it will in general affect the composition of the set of Pareto-optimal maps. In order to properly incorporate the pseudotemperature function into the heuristics described above, one could note that the questions difficultly is generally smaller when subsets with high pseudotemperature values have large measures as well. In other words, if one wishes to keep the question difficulty low, one should avoid creating subsets of small measure in regions of the parameter space characterized with high pseudotemperature values. To facilitate creation of such subsets, one could, for example modify the (reduced) cost function in the following way

| (21) |

where : is some increasing function of its arguments. The specific shape of can be determined experimentally, and several shapes can be tried for every given instance assuming computational resources are not a limiting factor.

V Example

Let us consider an example. The original problem is a that of two-stage linear stochastic optimization with simple recourse taken from a well-known textbook Birge and Louveaux (1997). The problem is for a farmer to allocate the appropriate amount of land between wheat, corn and sugar beets in order to maximize profits. The farmer knows that at least 200 tons of wheat and 240 tons of corn must be grown for cattle feed. If not enough is grown to satisfy this demand, both wheat and corn can be bought for $238 and $210 per ton, respectively. Any excess above the demand can be sold for $170 and $150 per ton of wheat and corn, respectively. It costs $150 per acre to plant the wheat and $230 per acre to plant the corn. The farmer can also grow sugar beets that sell for $36 per ton. However, there is a quota of 6000 tons and any amount grown above this may only be sold at $10 per ton. It costs $260 per acre to plant sugar beets. The farmer has 500 acres available.

The problem can be stated as:

| minimize | (FP) | |||

| subject to | ||||

where the second stage problem for a specific scenario can be written

| subject to | |||

where represents the yield of crop for wheat, corn, and sugar beets, respectively, under scenario ; are the acres of land to devote to each crop ; , are tons of wheat and corn, respectively, purchased to meet cattle feed requirements; are tons of wheat, corn, sugar beets below quota, and sugar beets above quota, respectively, sold for profit.

The problem has been modified in order to create the illustrative example used below. In this example, only wheat and sugar beet yields are uncertain. Each is allowed to take five different values of yields resulting in 25 scenarios. For the sake of convenience, we assume that the corn yield is non-random and is equal to 3 tons per acre, while for both wheat and beets the average yield equal to 2.5 and 20, respectively, has a probability of 0.30. The yield for both of these cultures can be either higher or lower than average by 20% with probability 0.20 and also can be higher or lower than average by 30% with probability 0.15. The yields for wheat and beets are assumed to be independent.

The resulting uncertain yields are summarized below:

| wheat | [1.75, 2.00, 2.50, 3.00, 3.25] | w.p. (0.15,0.20,0.30,0.20,0.15) |

| corn | [3] | w.p. (1) |

| beets | [14, 16, 20, 24, 26] | w.p. (0.15,0.20,0.30,0.20,0.15) |

Also, let us assume that the pseudotemperature function is given as

| (22) |

where are the indices referencing the uncertain yields of wheat and sugar beets, respectively (where the smallest value of the uncertain yield corresponds to () and the largest yield corresponds to ()). The pseudotemperature function is then normalized so that . Fig. 3 shows a plot of the pseudotemperature function.

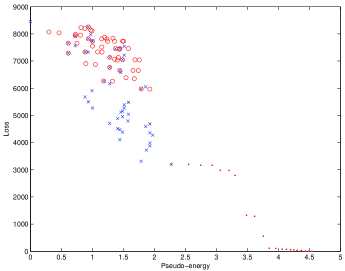

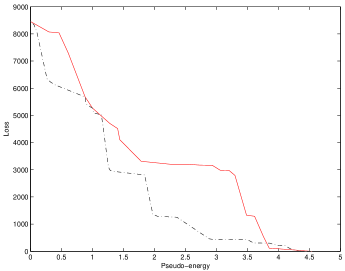

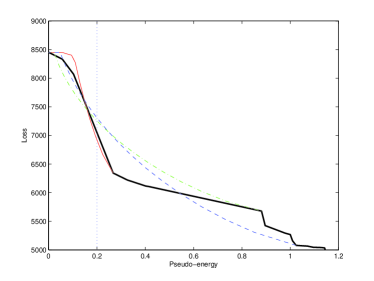

The efficient frontier can be approximated by using the scenario reduction based algorithm described in the previous section together with subset merging heuristics. The resulting maps are shown in Fig. 4 for the case of constant pseudotemperature. The resulting approximate efficient frontier both for constant pseudotemperature function and for the pseudotemperature given shown in Fig. 3 are shown in Fig. 5.

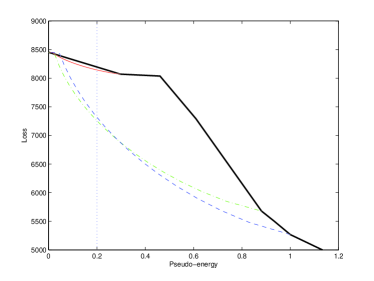

Now consider an information source described by the modified linear model with parameters and (which is a rather modest capacity value). We would like to find out how much the original loss can be reduced by optimally using such an information source. In other words, we want to solve problem (14). For this purpose one can take questions on the (approximate) efficient frontier and plot parametric curves

where is given by Proposition 2. The question yielding the lowest point of intersection of such a curve with the vertical line will give an approximate solution of problem (14).

Results for the case of constant pseudotemperature are shown in Fig. 6. The parametric curves for three questions (all three with ) are produced. We can see that the lowest value of the expected loss that can be obtained this way is equal to 7250 which constitutes a reduction of about 14%.

For the case of non-constant pseudotemperature are shown in Fig. 7. Analogously, three questions were chosen on the approximate efficient frontier and the corresponding parametric curves plotted. The best curve is observed to intersect the vertical line at the value of vertical coordinate equal to about 6900 which represents a reduction of about 18% compared to the EVPI of 8450 of the original problem.

VI Conclusion

The main subject of this work is the development of approximate methods for solving the problem of optimizing additional information acquisition in decision making problems with uncertainty that are typically solved using stochastic optimization techniques. It represents a logical continuation of the developments presented in Perevalov and Grace (2012c). The main problem that was formulated Perevalov and Grace (2012c) is that of finding the efficient frontier in the space of questions to the given information source and determining optimal question(s) that allow for the loss reduction maximization for the problem the agent is interested in solving.

The solution methods proposed in here are based on the method of probability metrics and their application for scenario reduction in stochastic optimization (see appendices). The main idea is that, informally speaking, optimal scenario reduction on one hand and optimal information acquisition on the other hand are complementary processes. More specifically, in scenario reduction, the goal is to reproduce the overall shape of the original probability distribution as faithfully as possible with a probability measure of a smaller support – one strives to keep the “overall shape” of the distribution while leaving out the “small details”. From the informational point of view, this corresponds to searching for the least relevant information and adding it (updating the measure accordingly) – without finding it. In information acquisition, on the contrary, the goal is to find the most relevant information that, at the same time, is relatively easy (so that the question requesting it has sufficiently low difficulty) for the information source to supply – and, hence, it ends up being accurate. Therefore, if one has a method for finding the least relevant information, the same method can likely be made to work for finding the most relevant information.

This observation provides for a means of development of simple approximate algorithms for determining the efficient frontier and for finding optimal questions for the given information source. The methods described here work for the class of linear multi-period two stage stochastic optimization problems and should generalize relatively easily to other problem classes for which scenario reduction based on probability metrics was shown to be possible, including chance constrained and two-stage integer stochastic optimization problems.

Appendix A Proofs

A.1 Proof of Lemma 1

Let (so that ). Then we can write

where (a) follows from the triangle inequality satisfied by the elements and (b) follows from the definition of .

A.2 Proof of Lemma 2:

The first statement actually holds true for any measures (see Appendix 1 for the definition of ). Indeed, let be the function that achieves the maximum of

Let be the restriction of to . Clearly, . We can write

where (a) follows from the definition of conditional measures and , (b) follows from the definition of functions , and (c) follows from that and definition of .

To prove the second statement, we can use the duality result (27) together with (32) that relates the values of Kantorovich-Rubinstein and Monge-Kantorovich functionals. Let be the map that generates partition , and let for all . Note also that , . We can write

where (a) and (d) follow from (27) and (32), (b) follows from that is supported at a single point , (c) follows from the way measure was constructed as a reduction of the measure with a -optimal map .

A.3 Proof of Proposition 3:

Let be the measure of subsets in and let and be the corresponding subset measures.

where (a) follows from the definition of , (b) follows from the definition of the optimal objective values and , (c) follows from that the integrand is in and definition (26) of Fortet-Mourier metric , and (d) follows from Lemma 2.

A.4 Proof of Proposition 4:

Let , be measures of subsets in and let and be the corresponding subset measures.

where for , (a) follows from the definition of optimal values and , (b) follows from the upper bound (33), (c) follows from the duality relation (27) and from the relation (32) between the Kantorovich-Rubinstein and Monge-Kantorovich functionals, (d) follows from Lemma 1 (since is a metric and is a probability distribution), (e) follows from that , where is -optimal, and (f) follows from Lemma 2.

Appendix B Probability metrics and stability in stochastic optimization

Consider the problem (1). Let be the set of all Borel probability measures on and define

and

to be the optimal value and optimal solution set of (1), respectively.

Let’s also define (as in, for example, Römisch and Wets (2007))

and

where is the closed unit ball in .

Then the probability distance of the form

| (23) |

can be defined on . This distance is called Zolotarev’s pseudometric with -structure Zolotarev (1983); Rachev and Römisch (2002); Rachev and Rüschendorf (1998, 1998). The pseudometric (23) would become a metric if the class were rich enough so that implies .

Theorem 2 in Dupačová et al. (2003) states that if , is nonempty and bounded then there exist and such that

| (24) |

is valid for all such that .

The distance in (24) is typically difficult to handle since the class of functions is determined by the specific integrand for the given instance of problem (1). The main idea underlying the use of the probability metrics method for the study of stability and for scenario reduction in stochastic programming is to suitably enlarge the class so that it still shares its main analytical properties with functions . Such properly enlarged classes are sometimes referred to as canonical classes and the corresponding metrics are sometimes called canonical metrics.

Consider, for instance the class of continuous functions defined as

| (25) |

where : is a continuous symmetric function such that if and only if . Then the corresponding (pseudo-) metric has the form

| (26) |

and is known as Fortet-Mourier metric. If the cost function satisfies additional boundedness and continuity conditions:

-

•

for some : mapping bounded sets into bounded sets,

-

•

as for each , where is the -ball centered at ,

the Fortet-Mourier metric (26) admits a dual representation as the Kantorovich-Rubinstein functional Rachev and Shortt (1990):

| (27) |

where and denote projections on first and second components, respectively. It is straightforward to show that the Kantorovich-Rubinstein functional (27) can be upper-bounded by the Monge-Kantorovich functional:

| (28) |

and that the bounds becomes tight, (i.e. ) if the cost function is a metric on Levin (1975). The problem of finding the minimum in (28) is known the Monge-Kantorovich mass transportation problem.

Note that if measures and are discrete ( and ), the Monge-Kantorovich functional (28) takes the following form:

| (29) |

Given the cost function one can define the reduced cost on by

| (30) |

In can easily be shown that the reduced cost function is a metric (since it satisfies the triangle inequality) on and that with the inequality being tight when is also a metric.

It can also be shown (see Rachev and Rüschendorf (1998), chapter 4) that if is compact with analytic sublevel sets then the Kantorovich-Rubinstein functional (27) with the reduced cost function coincides with the Kantorovich-Rubinstein functional with the original cost function (the result referred to as the reduction theorem):

| (31) |

Since the reduced cost is a metric on we have and, comparing with (31) we conclude that, for compact parameter spaces with analytic sublevel sets, the equality

| (32) |

holds true.

We thus arrive at the following useful stability result. If the integrand in problem (1) belongs to class for all for some cost function satisfying additional boundedness and continuity conditions described earlier in the appendix, then the estimate

| (33) |

is valid for Borel measures and in on compact characterized with analytic sublevel sets. (Here for some .)

The particular function that plays an important role in the context of convex stochastic optimization has the form

| (34) |

for some . The corresponding metric is referred to as the -th order Fortet-Mourier metric.

To give an example of a class of problems for which the -th order Fortet-Mourier metric is relevant, consider linear multi-period stochastic optimization problems of the form

| (35) |

where are polyhedral sets. Problem (35) can be written in the form (1) with the integrand given by

where the function is defined recursively:

for and .

It is shown in Römisch and Wets (2007) that if for all pairs (relatively complete recourse) and for (where denotes the horizon cone222The horizon cone for the convex set is defined as the set of all elements such that for all and all . In particular, if is bounded. of ) then there exists a constant such that

| (36) |

for all , and . This implies that for all , and .

It is now straightforward to obtain the following result (Römisch and Wets (2007)). Let be the optimal value of problem (35). Assume that the relatively complete recourse condition for (35) is satisfied and that for . Then there exists a constant such that the estimate

| (37) |

is valid for any , . (Here denotes the set of Borel measures on with finite -th order moments.)

Appendix C Scenario reduction algorithms

The goal of scenario reduction algorithms is, given a stochastic optimization problem of the form (1) characterized by a discrete measure find the discrete measure such that and the difference in the optimal objective values is as small as possible.

If the stochastic optimization problem has the form (35) of a linear multi-period problem then, as discussed earlier in this section, under relatively complete recourse assumption, the upper bound (38) can be shown to hold. This motivates searching for discrete measures that minimize the distance (or ).

Thus the optimal scenario reduction problem based on the method of probability metrics can be formulated as follows Dupačová et al. (2003). Let and consider the measure supported at points , . The measure is said to be reduced from by deleting scenarios , and by assigning new probabilities to the remaining scenarios. The optimal reduction concept proposed in Dupačová et al. (2003) seeks the minimum value of the functional

| (39) |

It is shown in Dupačová et al. (2003) that, for set fixed, the optimal weights are straightforward to find:

| (40) |

where and for each . The corresponding minimum of the functional is

On the other hand, the optimal choice of the set of given cardinality

is a combinatorial problem, and it is unlikely that efficient solution algorithms for arbitrary value of are available. However cases and are easy to solve to optimality and they can be used to formulate heuristic algorithms for other values of . The fast forward scenario reduction algorithms proposed in Heitsch and Römisch (2003) proceeds as follows.

Fast forward selection algorithm:

Step 1: ,

,

.

Step : ,

,

.

Step : Redistribution by (40).

References

- Perevalov and Grace (2012a) E. Perevalov and D. Grace, “Towards the full information chain theory: question difficulty,” (2012a), submitted to Physical Review E, arXiv:1212.2696[physics.data-an].

- Perevalov and Grace (2012b) E. Perevalov and D. Grace, “Towards the full information chain theory: answer depth and source models,” (2012b), submitted to Physical Review E, arXiv:1212.2693[physics.data-an].

- Perevalov and Grace (2012c) E. Perevalov and D. Grace, “Optimization of additional information acquisition in decision making problems: main framework,” (2012c), submitted to European Journal of Operational Research.

- Shannon (1948) C. E. Shannon, Bell Systems Technical Journal 27, 379 (1948).

- Jaynes (1957a) E. T. Jaynes, Phys. Rev. 106, 620 (1957a).

- Jaynes (1957b) E. T. Jaynes, Phys. Rev. 108, 171 (1957b).

- Viola (1995) P. A. Viola, Alignment by maximization of mutual information, A.I. Technical Report 1548 (Massachusetts Institute of Technology, 1995).

- Mokhov and Smirnov (2006) I. I. Mokhov and D. A. Smirnov, Geophys. Res. Lett. 33 (2006), l03708.

- Verdes (2005) P. F. Verdes, Phys. Rev. E 72 (2005), 026222.

- Katura et al. (2006) T. Katura, N. Tanaka, A. Obata, H. Sato, and A. Maki, NeuroImage 31, 1592 (2006).

- Chávez et al. (2003) M. Chávez, J. Martinerie, and M. Le Van Quyen, J. of Neurosci. Methods 124, 113 (2003).

- Klir and Harmanec (1996) G. J. Klir and D. Harmanec, Kybernetes 25, 50 (1996).

- Maeda and Ichihashi (1993) Y. Maeda and H. Ichihashi, Int. J. Gen. Syst. 21, 379 (1993).

- Harmanec and Klir (1994) D. Harmanec and G. J. Klir, Int. J. Gen. Syst. 22, 405 (1994).

- Shafer (1976) G. Shafer, A Mathematical Theory of Evidence (Princeton University Press, Princeton, NJ, 1976).

- Cox (1946) R. T. Cox, Am. J. Phys. 14, 1 (1946).

- Cox (1961) R. T. Cox, The Algebra of Probable Inference (Johns Hopkins Press, Baltimore, 1961).

- Cox (1979) R. T. Cox, in The Maximum Entropy Formalism, edited by R. Levine and M. Tribus (MIT Press, Cambridge, MA, 1979) pp. 119-167.

- Knuth (2005) K. H. Knuth, Neurocomputing 67, 245 274 (2005).

- Knuth (2007) K. H. Knuth, in Bayesian Inference and Maximum Entropy Methods in Science and Engineering, AIP Conf. Proc., Vol. 954, edited by K. Knuth et al. (2007) pp. 23–36.

- Knuth (2008) K. H. Knuth, in Bayesian Inference and Maximum Entropy Methods in Science and Engineering, Sao Paolo, Brazil (2008) pp. 24–31.

- Caticha (2004) A. Caticha, in Bayesian Inference and Maximum Entropy Methods in Science and Engineering, AIP Conf. Proc., Vol. 735, edited by R. Fischer et al. (2004) p. 429.

- Knuth and Bahreyni (2010) K. H. Knuth and N. Bahreyni, “A derivation of special relativity from causal sets,” arXiv:1005.4172v1[math-ph] (2010).

- Caticha (2012a) A. Caticha, Entropic Inference and the Foundations of Physics (11th Brazilian Meeting on Bayesian Statistics, São Paolo, Brazil, 2012).

- Caticha and Cafaro (2007) A. Caticha and C. Cafaro, in Bayesian Inference and Maximum Entropy Methods in Science and Engineering, AIP Conf. Proc., Vol. 954, edited by K. Knuth et al. (2007) p. 165.

- Caticha (2011) A. Caticha, J. Phys. A 44, 225303 (2011).

- Caticha (2012b) A. Caticha, in MaxEnt 2012, The 32nd International Workshop on Bayesian Inference and Maximum Entropy Methods in Science and Engineering (2012) arXiv:1212.6946.

- McCardle (1985) K. F. McCardle, Management Sci. 31, 1372 (1985).

- Jensen (1988) R. Jensen, Management Sci. 34, 230 (1988).

- Fisher and Raman (1996) M. L. Fisher and A. Raman, Oper. Res. 44, 87 (1996).

- Kornish and Keeney (2008) L. J. Kornish and R. L. Keeney, Oper. Res. 56, 527 (2008).

- Fischer et al. (1996) A. J. Fischer, A. J. Arnold, and M. Gibbs, Amer. J. Agr. Econ. 78, 1073 (1996).

- Ellison and Fudenberg (1993) G. Ellison and D. Fudenberg, J. Political Econom. 101, 612 (1993).

- Huh and Rusmevichientong (2009) W. T. Huh and P. Rusmevichientong, MOOR 34, 103 (2009).

- Levi et al. (2007) R. Levi, R. O. Roundy, and D. B. Shmoys, MOOR 32, 821 (2007).

- Bassamboo and Zeevi (2009) A. Bassamboo and A. Zeevi, OR 57, 514 (2009).

- French (1985) S. French, Bayesian Statist. 2, 183 (1985).

- Genest and Zidek (1986) C. Genest and J. V. Zidek, Statist. Sci. 1, 114 (1986).

- Clemen (1987) R. Clemen, Management Sci. 33, 373 (1987).

- Clemen and Winkler (1999) R. Clemen and R. Winkler, Risk Anal. 19, 187 (1999).

- Predd et al. (2008) J. B. Predd, D. N. Osherson, S. R. Kulkarni, and H. V. Poor, Decision Anal. 5, 177 (2008).

- Heitsch and Römisch (2003) H. Heitsch and W. Römisch, Computational Optimization and Applications 24, 187 (2003).

- Note (1) Here and later we omit the trivial partition from the list of arguments of and .

- Birge and Louveaux (1997) J. R. Birge and F. Louveaux, Introduction to Stochastic Programming (Springer-Verlag, New York, NY, 1997).

- Römisch and Wets (2007) W. Römisch and R. J.-B. Wets, SIOPT 18, 961 (2007).

- Zolotarev (1983) V. M. Zolotarev, Theory of Probability and its Applications 28, 264 (1983).

- Rachev and Römisch (2002) S. T. Rachev and W. Römisch, Math. Oper. Res. 27, 792 (2002).

- Rachev and Rüschendorf (1998) S. T. Rachev and L. Rüschendorf, Mass Transportation Problems, Volume I: Theory (Springer-Verlag, New York, 1998).

- Rachev and Rüschendorf (1998) S. T. Rachev and L. Rüschendorf, Mass Transportation Problems, Volume II: Applications (Springer-Verlag, New York, 1998).

- Dupačová et al. (2003) J. Dupačová, N. Gröwe-Kuska, and W. Römisch, Math. Programming, Ser. A 95, 493 (2003).

- Rachev and Shortt (1990) S. T. Rachev and R. M. Shortt, Dissertationes Mathematicae 299, 647 (1990).

- Levin (1975) V. L. Levin, Sov. Math. Dokl. 16, 1349 (1975).

- Note (2) The horizon cone for the convex set is defined as the set of all elements such that for all and all . In particular, if is bounded.