MULTIVARIATE RISK MEASURES: A CONSTRUCTIVE APPROACH BASED ON

SELECTIONS

††The authors are grateful to Leonid Hanin for his advice on duality

results in Lipschitz spaces. IM acknowledges the hospitality of the

University Carlos III de Madrid. IM has benefited from discussions

with Qiyu Li, Michael Schmutz and Irina Sikharulidze at various stages

of this work. The second version of this preprint was greatly inspired

by insightful comments of Birgit Rudloff concerning her recent work on

multivariate risk measures. The authors are grateful to the Associate

Editor and the referees for thoughtful comments and encouragement that

led to a greatly improved paper.

This version corrects Lemma 7.1 and

Lemma 7.2 in Section 7.

Ignacio Cascos

Universidad Carlos III de Madrid

Ilya Molchanov

University of Bern

††IC supported by the Spanish Ministry of

Science and Innovation Grants No. MTM2011-22993 and

ECO2011-25706. IM supported by the

Chair of Excellence Programme of the Universidad Carlos III de

Madrid and Banco Santander and the Swiss National Foundation Grant

No. 200021-137527.

††Address correspondence to Ilya Molchanov, Institute of

Mathematical Statistics and Actuarial Science, University of Bern,

Sidlerstrasse 5, 3012 Bern, Switzerland; e-mail:

ilya.molchanov@stat.unibe.ch.

Since risky positions in multivariate portfolios can be offset by various choices of capital requirements that depend on the exchange rules and related transaction costs, it is natural to assume that the risk measures of random vectors are set-valued. Furthermore, it is reasonable to include the exchange rules in the argument of the risk measure and so consider risk measures of set-valued portfolios. This situation includes the classical Kabanov’s transaction costs model, where the set-valued portfolio is given by the sum of a random vector and an exchange cone, but also a number of further cases of additional liquidity constraints.

We suggest a definition of the risk measure based on calling a set-valued portfolio acceptable if it possesses a selection with all individually acceptable marginals. The obtained selection risk measure is coherent (or convex), law invariant and has values being upper convex closed sets. We describe the dual representation of the selection risk measure and suggest efficient ways of approximating it from below and from above. In the case of Kabanov’s exchange cone model, it is shown how the selection risk measure relates to the set-valued risk measures considered by Kulikov (2008), Hamel and Heyde (2010), and Hamel, Heyde and Rudloff (2013).

Key Words: exchange cone, random set, selection, set-valued portfolio, set-valued risk measure, transaction costs.

1 Introduction

Since the seminal papers by Artzner, Delbaen, Eber, and Heath (1999) and Delbaen (2002), most studies of risk measures deal with the univariate case, where the gains or liabilities are expressed by a random variable. We refer to Föllmer and Schied (2004) and McNeil, Frey, and Embrechts (2005) for a thorough treatment of univariate risk measures and to Acciaio and Penner (2011) for a recent survey of the dynamic univariate setting.

Multiasset portfolios in practice are often represented by their total monetary value in a fixed currency with the subsequent calculation of univariate risk measures that can be used to determine the overall capital requirements. The main emphasis is put on the dependency structure of the various components of the portfolio, see Burgert and Rüschendorf (2006); Embrechts and Puccetti (2006). Numerical risk measures for a multivariate portfolio have been also studied in Ekeland, Galichon, and Henry (2012) and Rüschendorf (2006). The key idea is to consider the expected scalar product of with a random vector and take supremum over all random vectors that share the same distribution with and possibly over a family of random vectors . Farkas, Koch-Medina, and Munari (2014) defined the scalar risk as the infimum of the payoff associated with a random vector that being added to the portfolio renders it acceptable. A vector-valued variant of the value-at-risk has been suggested in Cousin and Di Bernardino (2013).

However, in many natural applications it is necessary to assess the risk of a vector in whose components represent different currencies or gains from various business lines, where profits/losses from one line or currency cannot be used directly to offset the position in a different one. Even in the absence of transaction costs, the exchange rates fluctuate and so may influence the overall risk assessment. Also the regulatory requirements may be very different for different lines (e.g. in the case of several states within the same currency area), and moving assets may be subject to transaction costs, taxes or other restrictions. For such cases, it is important to determine the necessary reserves that should be allocated in each line (currency or component) of in order to make the overall position acceptable. The simplest solution would be to treat each component separately and allocate reserves accordingly, which is not in the interest of (financial) agents who might want to use profits from one line to compensate for eventual losses in other ones. Thus, in addition of assessing the risk of the original vector , one can also evaluate the risk of any other portfolio that may be obtained from by allowed transactions. In view of this, it is natural to assume that the acceptability may be achieved by several (and not directly comparable) choices of capital requirements that form a set of possible values for the risk measure. This suggests the idea of working with set-valued risk measures.

Since the first work on multivariate risk measures (Jouini, Meddeb, and Touzi, 2004), by now it is accepted that multiasset risk measures can be naturally considered as taking values in the space of sets, see Ben Tahar and Lépinette (2013); Cascos and Molchanov (2007); Hamel and Heyde (2010); Hamel, Heyde, and Rudloff (2011); Kulikov (2008). The risk measures of random vectors are mostly considered in relation to Kabanov’s transaction costs model, whose main ingredient is a cone of portfolios available at price zero at the chosen time horizon (also called the exchange cone), while the central symmetric variant of is a solvency cone. If is the terminal gain, then each random vector with values in is possible to obtain by converting following the rules determined by . In other words, instead of measuring the risk of we consider the whole family of random vectors taking values in . In relation to this, note that families of random vectors representing attainable gains are often considered in the financial studies of transaction costs models, see e.g. Schachermayer (2004).

The set-valued portfolios framework can be related to the classical setting by replacing a univariate random gain with half-line and measuring risks of all random variables dominated by . The monotonicity property of a chosen risk measure implies that all these risks build the set . If is subadditive, then . Furthermore, if and only if contains the origin. While in the univariate case this construction leads to half-lines, in the multivariate situation it naturally gives rise to so-called upper convex sets, see Hamel and Heyde (2010); Hamel et al. (2011); Kulikov (2008). A portfolio is acceptable if its risk measure contains the origin and the value of the risk measure is the set of all such that the portfolio becomes acceptable if capital is added to it.

Note that in the setting of real-valued risk measures adapted in Ekeland et al. (2012), the family of all that make acceptable is a half-space, which apparently only partially reflects the nature of cone-based transaction costs models. Farkas et al. (2014) establish relation between families of real-valued risks and set-valued risks from Hamel et al. (2011). The setting of Riesz spaces (partially ordered linear spaces), in particular Fréchet lattices and Orlicz spaces, has become already common in the theory of risk measures, see Biagini and Fritelli (2008); Cheridito and Li (2009). However, these spaces are mostly used to describe the arguments of risk measures whose values belong to the (extended) real line. Furthermore, the space of sets is no longer a Riesz space — while the addition is well defined, the matching subtraction does not exist. The recent study of risk preferences (Drapeau and Kupper, 2013) also concentrates on the case of vector spaces for arguments of risk measures.

The dual representation for risk measures of random vectors in the case of a deterministic exchange cone is obtained in Hamel and Heyde (2010) and for the random case in Hamel et al. (2011), see also Kulikov (2008) who considers both deterministic and random exchange cones. However in the case of a random exchange cone, it does not produce law-invariant risk measures — the risk measure in Hamel and Heyde (2010); Hamel et al. (2011, 2013); Kulikov (2008) is defined as a function of a random vector representing the gain, while identically distributed gains might exhibit different properties in relation to the random exchange cone. Although the dual representations from Hamel and Heyde (2010); Hamel et al. (2011); Kulikov (2008) are general, they are rather difficult to use in order to calculate risks for given portfolios, since they are given as intersections of half-spaces determined by a rather rich family of random vectors from the dual space. Recent advances in vector optimisation have led to a substantial progress in computation of set-valued risk measures, see Hamel et al. (2013). However, the dual approximation also does not explicitly yield the relevant trading (or exchange) strategy that determines transactions suitable to compensate for risks. The construction of set-valued risk measures from Cascos and Molchanov (2007) is based on the concept of the depth-trimmed region, and their values are easy to calculate numerically or analytically, but it only applies for deterministic exchange cones and often results in marginalised risks (so that the risk measure is a translate of the solvency cone).

In order to come up with a law invariant risk measure and also cover the case of random exchange cones, we assume that the argument of a risk measure is a random closed set that consists of all attainable portfolios. This random set may be the sum of a random vector and the exchange cone (which has been the most important example so far) or may be defined otherwise. For instance, if only a linear space of portfolios is available for compensation, then the set of attainable portfolios is the intersection of with . In any such case we speak about a set-valued portfolio . This guiding idea makes it possible to work out the law-invariance property of risk measures and naturally arrive at set-valued risks.

In this paper we suggest a rather simple and intuitive way to measure risks for set-valued portfolios based on considering the family of all terminal gains that may be attained after some exchanges are performed. The crucial step is to consider all random vectors taking values in a random set (selections of ) as possible gains and regard the random set acceptable if it possesses a selection with all acceptable components. In view of this, we do not only determine the necessary capital reserves, but also the way of converting the terminal value of the portfolio into an acceptable one.

In the case of exchange cones, we relate our construction to the dual representation from Hamel and Heyde (2010) and Kulikov (2008). Throughout the paper we concentrate on the coherent case and one-period setting, but occasionally comment on non-coherent generalisations. Feinstein and Rudloff (2014a) thoroughly analyse and compare various approaches, including one from this paper, in view of defining multiperiod set-valued risks, see also Feinstein and Rudloff (2014b).

Example 1.1.

Let represent terminal gains on two business lines expressed in two different currencies. Assume that and are i.i.d. normally distributed with mean and variance . Assume that the exchanges between currencies are free from transaction costs with the initial exchange rate (number of units of the second currency to buy one unit of the first one), the terminal exchange rate is lognormal with mean and volatility , and is independent of . The set-valued portfolio is a half-plane with the boundary passing through and normal .

Assume that necessary capital reserves are determined using the expected shortfall at level , see Acerbi and Tasche (2002). If compensation between business lines is not allowed, the necessary capital reserves at time zero are given by (all numbers are given in the units of the first currency). If the terminal gains are transferred to one currency, then the needed reserves are given by and respectively in the case of transfers to the first and the second currency. These values correspond to evaluating the risks of selections of located at the points of intersection of the boundary of with coordinate axes.

However, it is possible to choose a selection that further reduces the required capital requirements. After transferring to the second asset units of the first currency, we arrive at the selection of given by

| (1) |

obtained by projecting the origin onto the boundary of . In this case the needed reserves are . The situation of random frictionless exchanges is also considered analytically in Example 5.1 and numerically in Examples 8.3 and 8.4.

Assume that now liquidity restrictions are imposed meaning that at most one unit of each currency may be obtained after conversion from the other. This framework corresponds to dealing with a non-conical set-valued portfolio . A reasonable strategy would be to use selection from (1) if and and otherwise choose the nearest point to from the extreme points of . The corresponding selection is given by

| (2) |

and the needed reserves are , which is higher than those corresponding to the choice of in view of imposed liquidity restrictions.

Before describing the structure of the paper, we would like to point out that our approach is constructive in the sense that instead of starting with an axiomatic definition of a set-valued risk measure we explicitly construct one based on selections of a random portfolio and univariate marginal risk measures. Then we show that the constructed risk measure indeed satisfies the desired properties of set-valued risk measures, in particular, the coherency and the Fatou properties, instead of imposing them. We show how to approximate the values of the risk measure from below (which is the aim of the market regulator) and from above (as the agent would aim to do). The suggested bounds provide a feasible alternative to exact calculations of risk. Furthermore, the computational burden is passed to the agent who aims to increase the family of selections in order to obtain a tighter approximation from above and so reduce the capital requirements, quite differently to the dual constructions of Hamel et al. (2011) and Kulikov (2008), where the market regulator faces the task of making the acceptance criterion more stringent by approximating from below the exact value of the risk measure. It should be noted our approach constitutes just one possible way to construct multivariate risk measures (and the corresponding acceptance sets) that satisfy the axioms of set-valued coherent risk measures from Hamel et al. (2011).

Section 2 introduces the concept of set-valued portfolios and the definition of set-valued risk measures for set-valued portfolios adapted from Hamel et al. (2011), where the conical setting was considered. Section 3 defines the selection risk measure, which relies on univariate risk measures applied to the components of selections for a set-valued portfolio. In particular, the coherency of the selection risk measure is established in Theorem 3.4. While throughout the paper we work with coherent risk measures defined on spaces with , the construction can be also based on convex non-coherent and non-convex univariate risk measures, so that it yields their non-coherent set-valued analogues, such as the value-at-risk.

Section 4 derives lower and upper bounds for risk measures. Section 5 is devoted to the setting of exchange cones (or conical market models) that has been in the centre of attention in all other works on multiasset risks. It is shown that, for the exchange cones setting, the lower bound corresponds to the dual representation of risk measures from Hamel and Heyde (2010); Hamel et al. (2011) and Kulikov (2008). For deterministic exchange cones the bounds become even simpler and in the case of comonotonic portfolios the risk measure admits an easy expression.

We briefly comment on scalarisation issues in Section 6, i.e. explain relationships to univariate risk measures constructed for set-valued portfolios, which in the case of a deterministic exchange cone are related to those considered in Ekeland et al. (2012); Rüschendorf (2006) and Farkas et al. (2014).

Section 7 establishes the dual representation of the selection risk measures. While the idea is to handle set-valued portfolios through their support functions, the key difficulty consists in dealing with possibly unbounded values of the support functions. For this, we introduce the Lipschitz space of random sets and specify the weak-star convergence in this space in order to come up with a general dual representation for set-valued risk measures with the Fatou property. Theorems 7.4, 7.5, and 7.7 establish the Fatou property of the selection risk measure under some conditions and so yield the closedness of its values and the validity of the dual representation. In the deterministic exchange cone model and for random exchange cones with , the selection risk measure has the same dual representation as in Hamel and Heyde (2010); Kulikov (2008).

Section 8 presents several numerical examples of set-valued risk measures covering the exchange cone setting, the frictionless case, and liquidity restrictions. The algorithms used to approximate risk measures are transparent and easy to implement in comparison with a considerably more sophisticated set-optimisation approach from Löhne (2011) used in Hamel et al. (2013) in order to come up with exact values of set-valued risk measures in conical models. A particular computational advantage is due to the use of the primal representation of selection risk measures in order to compute upper bounds, while utilising the dual representation to arrive at lower bounds.

2 Set-valued portfolios and risk measures

2.1 Operations with sets

In order to handle set-valued portfolios, we need to define several important operations with sets in . The closure of a set is denoted by . Further,

denotes the centrally symmetric set to . The sum of two (deterministic) sets and in a linear space is defined as the set . If one of the summands is compact and the other is closed, the set of pairwise sums is also closed. In particular, the sum of a point and a set is given by . For instance, is the set of points dominated by , where . Denote .

The norm of a set is defined as , where is the Euclidean norm of . A set is said to be upper, if and imply that , where all inequalities between vectors are understood coordinatewisely. Inclusions of sets are always understood in the non-strict sense, i.e. allows for the equality .

The -envelope of a closed set is defined as the set of all points such that the distance between and the nearest point of is at most . The Hausdorff distance between two closed sets and in is the smallest such that and . The Hausdorff distance metrises the family of compact sets, while it can be infinite for unbounded sets.

The support function (see (Schneider, 1993, Sec. 1.7)) of a set in is defined as

where denotes the scalar product. The support function may take infinite values if is not bounded. Denote by

the effective domain of the support function of . The set is always a convex cone in . If is a cone in , then equals the dual cone to defined as

| (3) |

2.2 Set-valued portfolios

Let be an almost surely non-empty random closed convex set in (shortly called random set) that represents all feasible terminal gains on assets expressed in physical units. The random set is called set-valued portfolio. Assume that is defined on a complete non-atomic probability space . Any attainable terminal gain is a random vector that almost surely takes values from , i.e. a.s., and such is called a selection of . We refer to Molchanov (2005) for the modern mathematical theory of random sets.

Since the free disposal of assets is allowed, with each point , the set also contains all points dominated by coordinatewisely and so is a lower set in . The efficient part of is the set of all points such that no other point of dominates in the coordinatewise order. While itself is never bounded, is called quasi-bounded if is a.s. bounded.

Fix and consider the space of -integrable random vectors in defined on . The reciprocal is defined from . The -norm of is denoted by . Furthermore, the family of -integrable selections of is denoted by , and is the family of all essentially bounded selections.

In the following we assume that is -integrable, i.e. possesses at least one -integrable selection. A random closed set is called -integrably bounded if its norm if -integrable (a.s. bounded if ). In the case of set-valued portfolios, this property is considered for .

The closed sum is defined as the random set being the closure of for . It is shown in (Hiai and Umegaki, 1977, Th. 1.4) (see also (Molchanov, 2005, Prop. 2.1.4)) that the set of -integrable selections of coincides with the norm closure of if . If , then is a norm closed set that contains the closed sum .

2.3 Examples of set-valued portfolios

Example 2.1 (Univariate portfolios).

If , then is a half-line and the monotonicity of risks implies that it suffices to consider only its upper bound as in the classical theory of risk measures.

Example 2.2 (Exchange cones).

Let represent gains from assets. Furthermore, let be a convex (distinct from the whole space and possibly random) exchange cone representing the family of portfolios available at price zero. Its symmetric variant is the solvency cone, while the dual cone contains all consistent price systems, see Kabanov and Safarian (2009); Schachermayer (2004). Formally, is a random closed set with values being cones. Define , so that selections of correspond to portfolios that are possible to obtain from following the exchange rules determined by .

If does not contain any line (and is called a proper cone), then the market has an efficient friction. Otherwise, some exchanges are free from transaction costs. In this case different random vectors yield the same portfolio , which is also an argument in favour of working directly with set-valued portfolios. The cone is a half-space if and only if all exchanges do not involve transaction costs. In difference to Ben Tahar and Lépinette (2013), our setting does not require that the exchange cone is proper.

If is deterministic, then we denote it by . If , no exchanges are allowed.

Example 2.3 (Cones generated by bid-ask matrix).

In the case of currencies, the cone is usually generated by a bid-ask matrix, as in Kabanov’s transaction costs model, see Kabanov (1999); Schachermayer (2004). Let be a (possibly random) matrix of exchange rates, so that is the number of units of currency needed to buy one unit of currency . It is assumed that the elements of are positive, the diagonal elements are all one and meaning that a direct exchange is always cheaper than a chain of exchanges. The cone describes the family of portfolios available at price zero, so that is spanned by vectors and for , where are standard basis vectors in . If the gain contains derivatives drawn on the exchange rates, then we arrive at the situation when and the exchange cone are dependent.

Example 2.4 (Conical setting with constraints).

It is possible to modify the conical setting by requiring that all positions acquired after trading are subject to some linear or other constraints, see e.g. Farkas et al. (2014). This amounts to considering the intersection of with a linear subspace or a more general subset of , that (if a.s. non-empty) results in a possibly non-conical set-valued portfolio and provides another motivation for working with set-valued portfolios.

Pennanen and Penner (2010) study in depth not necessarily conical transaction costs models in view of the no-arbitrage property, see also Kaval and Molchanov (2006). One of the most important examples is the model of currency markets with liquidity costs or exchange constraints.

The following examples describe several non-conical models that yield quasi-bounded set-valued portfolios. Despite the fact that some of them are generated by random vectors, it is essential to treat these portfolios as random sets, e.g. for possible diversification effects. The latter means that a sum of such set-valued portfolios is not necessarily equal to the set-valued portfolio generated by the sum of the generating random vectors.

Example 2.5 (Restricted liquidity).

Let , where . Then the exchanges up to the unit volume are at the unit rate free from transaction costs while other exchanges are not allowed. A similar example with transaction costs and a random exchange cone can be constructed as for some . A more general variant from (Pennanen and Penner, 2010, Ex. 2.4) models liquidity costs depending on the transaction’s volume.

Example 2.6.

Let be random vectors in that represent terminal gains in lines (e.g. currencies) of investments. The random set is defined as the set of all points in dominated by at least one convex combination of the gains. In other words, is the sum of and the convex hull of .

If and for and a bivariate random vector , then describes an arbitrary profit allocation between two different lines without transaction costs up to the amount .

Example 2.7.

Assume that , where is the ball of fixed radius centred at the origin. This model corresponds to the case, when infinitesimally small transactions are free to exchange at the rate that depends on the balance between the portfolio components.

Example 2.8 (Transactions maintaining solvency).

Let be an exchange cone from Example 2.2 and let be the value of a portfolio. Define to be the set of points coordinatewisely dominated by a point from if belongs to the solvency cone , and if . In this case no transactions are allowed in the non-solvent case and otherwise all transactions should maintain the solvency of the portfolio.

2.4 Set-valued risk measure

The following definition is adapted from Hamel and Heyde (2010); Hamel et al. (2011) and Kulikov (2008), where it appears in the exchange cones setting.

Definition 2.9.

A function defined on -integrable set-valued portfolios is called a set-valued coherent risk measure if it takes values being upper convex sets and satisfies the following conditions.

-

1.

for all (cash invariance).

-

2.

If a.s., then (monotonicity).

-

3.

for all (homogeneity).

-

4.

(subadditivity).

The risk measure is said to be closed-valued if its values are closed sets. Furthermore, is said to be a convex set-valued risk measure if the homogeneity and subadditivity conditions are replaced by

The names for the subadditivity and convexity properties are justified by the fact that sets can be ordered by the reverse inclusion; we follow Hamel and Heyde (2010); Hamel et al. (2011) in this respect. Definition 2.9 appears in Kulikov (2008) and Hamel and Heyde (2010); Hamel et al. (2011), with the argument of being a random vector and for a fixed exchange cone , which in our formulation means that the argument of is the random set .

The set-valued portfolio is acceptable if . The subadditivity of means that the acceptability of and entails the acceptability of , as in the classical case of coherent risk measures. In the univariate case, and for a coherent risk measure , so that is acceptable if and only if . If a.s., then is acceptable under any closed-valued coherent risk measure. Indeed, then , while contains the origin by the homogeneity and subadditivity properties and the closedness of the values for . For a non-coherent , it is sensible to extra impose the normalisation condition for each deterministic exchange cone .

Example 2.3 (cont.) (Capital requirements in the exchange cones setting).

The value of the risk measure determines capital amounts that make acceptable. The necessary capital should be allocated at time zero, when the exchange rules are determined by a non-random exchange cone . Thus, the initial capital should be chosen so that intersects , and

is the family of all possible initial capital requirements. Optimal capital requirements are given by the extremal points from in the order generated by the cone . If is not random, . If is a half-space, meaning that the initial exchanges are free from transaction costs, then is a half-space too. In this case, the sensible initial capital is given by the tangent point to in direction of the normal to , see Example 1.1.

If is the whole space, which might be the case, for instance, if and are two different half-spaces, then it is possible to release an infinite capital from the position, and this situation should be excluded for the modelling purposes.

3 Selection risk measure for set-valued portfolios

3.1 Acceptability of set-valued portfolios

Below we explicitly construct set-valued risk measures based on selections of . Let be law invariant coherent risk measures defined on the space with values in . Furthermore, assume that each satisfies the Fatou property, which for follows from the law invariance (Jouini et al., 2006) and for is always the case if takes only finite values, see (Kaina and Rüschendorf, 2009, Th. 3.1). For a random vector write

Random vector is said to be acceptable if , i.e. for all . This is exactly the case if portfolio is acceptable with respect to the set-valued measure

It is a special case of the regulator risk measure considered in (Hamel et al., 2013). The following definition suggests a possible acceptability criterion for set-valued portfolios that leads to a risk measure satisfying the axioms from Definition 2.9.

Definition 3.1.

A -integrable set-valued portfolio is said to be selection acceptable (in the following simply called acceptable) if for at least one selection .

The monotonicity property of univariate risk measures implies that is acceptable if and only if its efficient part admits an acceptable selection.

Example 2.3 (cont.).

The acceptability of means that it is possible to transfer the assets given by the components of according to the exchange rules determined by , so that the resulting random vector with has all acceptable components.

Remark 3.2 (Generalisations).

The acceptability of selections can be judged using any other multivariate coherent risk measure, e.g. considered in Hamel et al. (2011), that are not necessarily of point plus cone type, or numerical multivariate risk measures from Burgert and Rüschendorf (2006); Ekeland et al. (2012) and Farkas et al. (2014). Furthermore, it is possible to consider acceptability of a general convex subset of that might not be interpreted as the family of selections of a set-valued portfolio. This may be of advantage in the dynamic setting (Feinstein and Rudloff, 2014a) or for considering uncertainty models as in (Bion-Nadal and Kervarec, 2012).

3.2 Coherency of selection risk measure

Definition 3.3.

The selection risk measure of is defined as the set of deterministic portfolios that make acceptable, i.e.

| (4) |

Its closed-valued variant is .

Theorem 3.4.

The selection risk measure defined by (4) and its closed-valued variant are law invariant set-valued coherent risk measures, and

| (5) |

Proof.

We show first that is an upper set. Let and . If is acceptable for some , then also is acceptable because of the monotonicity of the components of . Hence . If and , then for a sequence . Consider any , then for sufficiently large , so that . Letting decrease to yields that , so that is an upper set.

In order to confirm the convexity of , assume that with and and take any . The subadditivity of components of implies that

It remains to note that is a selection of in view of the convexity of . Then is convex as the closure of a convex set.

The law invariance property is not immediate, since identically distributed random closed sets might have rather different families of selections, see (Molchanov, 2005, p. 32). Denote by the -algebra generated by the random closed set , see (Molchanov, 2005, Def. 1.2.4). If is acceptable, then for some . The dilatation monotonicity of law invariant numerical coherent risk measures on a non-atomic probability space (see Cherny and Grigoriev (2007)) implies that

Therefore, the conditional expectation is also acceptable. The convexity of implies that is a -integrable -measurable selection of . Therefore, is acceptable if and only if it has an acceptable -measurable selection. It remains to note that two identically distributed random sets have the same families of selections which are measurable with respect to the minimal -algebras generated by these sets, see (Molchanov, 2005, Prop. 1.2.18). In particular, the intersections of these families with are identical. Thus, and are law invariant.

Representation (5) follows from the fact that is the union of for .

The first two properties of coherent risk measures follow directly from the definition of . The homogeneity and subadditivity follow from the fact that all acceptable random sets build a cone. Indeed, if is acceptable, then is an acceptable selection of and so is acceptable. If and are acceptable, then is acceptable because the components of are coherent risk measures and so contains an acceptable random vector. Thus, and by passing to the closure we arrive at the subadditivity property of . ∎

Representation (5) was used in Hamel et al. (2013) to define the market extension of a regulator risk measure in the conical models setting.

Remark 3.5 (Eligible portfolios).

In order to simplify the presentation it is assumed throughout that all portfolios can be used to offset the risk. Following the setting of Hamel and Heyde (2010); Hamel et al. (2011, 2013), it is possible to assume that the set of eligible portfolios is a proper linear subspace of . The corresponding set-valued risk measure is , which equals the union of for all .

3.3 Properties of selection risk measures

Conditions for closedness of set-valued risk measures in the exchange cone setting were obtained in Feinstein and Rudloff (2014b). The following result establishes the closedness of for portfolios with -integrably bounded essential part. Further results concerning closedness of are presented in Corollary 7.6 and Corollary 7.8.

Theorem 3.6.

If is -integrably bounded, then the selection risk measure is closed.

Proof.

Let be acceptable and . Note that is weak compact for by (Molchanov, 2005, Th. 2.1.19) and for by its boundedness in view of the reflexivity of . By passing to subsequences we can assume that weakly converges to in . The dual representation of coherent risk measures yields that for a random variable , equals the supremum of over a family of random variables in . If weakly converges to in , then , so that . Applying this argument to the components of we obtain that

| (6) |

whence . If , then are uniformly bounded and so have a subsequence that converges in distribution and so can be realised on the same probability space as an almost surely convergent sequence. The Fatou property of the components of yields (6). ∎

Theorem 3.7 (Lipschitz property).

Assume that all components of take finite values on . Then there exists a constant such that for all -integrable set-valued portfolios and .

Proof.

Example 3.8 (Selection expectation).

If is the expectation of , then

where is the selection expectation of , i.e. the closure of the set of expectations for all integrable selections , see (Molchanov, 2005, Sec. 2.1). Thus, the selection risk measure yields a subadditive generalisation of the selection expectation.

Example 3.9.

Assume that and all components of are given by . Then is acceptable if and only if is almost surely non-empty, and is the set of points that belong to with probability one.

Example 3.10.

If is an exchange cone, then is a deterministic convex cone that contains . If is deterministic, then .

Remark 3.11.

Selection risk measures have a number of further properties.

I. Assume that has all identical components. If is acceptable, then its orthogonal projection on the linear subspace of generated by any is also acceptable, and so the risk of the projected contains the projection of .

II. The conditional expectation of random set with respect to a -algebra is defined as the closure of the set of conditional expectations for all its integrable selections, see (Molchanov, 2005, Sec. 2.1.6). The dilatation monotonicity property of components of implies that if is acceptable, then is acceptable. Therefore, is also dilatation monotone meaning that

In particular, . Therefore, the integrability of the support function for at least one provides an easy condition that guarantees that is not equal to the whole space.

Remark 3.12.

In the setting of Example 2.2, written as a function of only becomes a centrally symmetric variant of the coherent utility function considered in (Kulikov, 2008, Def. 2.1). It should be noted that the utility function from Kulikov (2008) and risk measures from Hamel et al. (2011) depend on both and and on the dependency structure between them and so are not law invariant as function of only, if is random.

If the components of are convex risk measures, so that the homogeneity assumption is dropped, then is a convex set-valued risk measure, which is not necessarily homogeneous. If the components of are not law invariant, then is a possibly not law invariant set-valued risk measure. The following two examples mention non-convex risk measures, which are also defined using selections.

Example 3.13.

Assume that the components of are general cash invariant risk measures without imposing any convexity properties, e.g. values-at-risk at the level , bearing in mind that the resulting selection risk measure is no longer coherent and not necessarily law invariant. Then is acceptable if and only if there exists a selection of such that for all .

Example 3.14.

Let be a deterministic exchange cone and fix some acceptance level . Call random vector acceptable if and note that this condition differs from requiring that for all . Then a set-valued portfolio is acceptable if and only if . If and , then is sometimes termed a multivariate quantile or the value-at-risk of , see Embrechts and Puccetti (2006) and Hamel and Heyde (2010).

4 Bounds for selection risk measures

4.1 Upper bound

The family of selections of a random set is typically very rich. An upper bound for can be obtained by restricting the choice of possible selections. The convexity property of implies that it contains the convex hull of the union of for the chosen selections . This convex hull corresponds to the case of a higher risk than . Making the upper bound tighter by considering a larger family of selections is in the interest of the agent in order to reduce the capital requirements.

At first, it is possible to consider deterministic selections, also called fixed points of , i.e. the points which belong to with probability one. If a.s., then . However, this set of fixed points is typically rather poor to reflect essential features related to the variability of .

Another possibility would be to consider selections of of the form for a fixed random vector and a deterministic . If for a deterministic set (which always can be chosen to be convex in view of the convexity of ), then

| (7) |

It is possible to tighten the bound by taking the convex hull for the union of the right-hand side for several . The inclusion in (7) can be strict even if , since taking random selections of makes it possible to offset the risks as the following example shows.

Example 4.1.

Let , where is the unit ball and is the standard bivariate normal vector. Consider the risk measure with two identical components being expected shortfalls at level . Then is the upper set generated by the ball of radius one centred at . Consider the selection of given by . By numerical calculation of the risks, it is easily seen that , which does not belong to .

4.2 Lower bound

Below we describe a lower bound for , which is a superset of and is also a set-valued coherent risk measure itself. For , (resp. ) denote the vectors composed of pairwise products (resp. ratios) of the coordinates of and . If is a set in , then . By agreement, let and .

Let be a non-empty family of non-negative -integrable random vectors in . Recall that denotes the selection expectation of with the coordinates scaled according to the components of , see Example 3.8. It exists, since is assumed to possess at least one -integrable selection and so . Define the set-valued risk measure

| (8) |

which is similar to the classical dual representation of coherent risk measures, see Delbaen (2002) and also corresponds to the -representation of risk measure in conical models from (Hamel et al., 2011, Th. 4.2) that is similar to (9) from the following theorem.

Theorem 4.2.

Assume that is a non-empty family of non-negative -integrable random vectors. The functional is a closed-valued coherent risk measure, and

| (9) |

Proof.

The closedness and convexity of follow from the fact that it is intersection of half-spaces; it is an upper set since the normals to these half-spaces belong to . It is evident that is monotonic, cash invariant and homogeneous. In order to check the subadditivity, note that

Recall that the support function of the expectation of a set equals the expected value of the support function. Since is an upper set,

and we arrive at (9) by replacing with . ∎

The components of admit the dual representations

| (10) |

where, for each , is the dual cone to the family of random variables such that , i.e. consists of non-negative -integrable random variables such that for all with , see Delbaen (2002); Föllmer and Schied (2004). Note that are the maximal families that provide the dual representation (10). Despite contains a.s. vanishing random variables, letting ensures the validity of (10).

Theorem 4.3.

Assume that the components of admit the dual representations (10). Then for any family of -integrable random vectors such that , .

Proof.

Corollary 4.4.

The selection risk measure is not equal to the whole space if is integrable for some and with , .

It should be noted that the acceptability of under the risk measure does not necessarily imply the existence of a selection with all acceptable marginals.

Remark 4.5.

The risk measure is not law invariant in general. It is possible to construct a law invariant (and also tighter) lower bound for the selection risk measure by extending to , so that, with each , the family contains all random vectors that share the distribution with .

Proposition 4.6.

Let all components of be identical univariate risk measures whose dual representation (10) involves the same family of a.s. non-negative random variables. Consider the family that consists of all for all . Then

| (11) |

where if with positive probability.

Proof.

The bounds for selection measures for set-valued portfolios determined by exchange cones are considered in the subsequent sections. Below we illustrate Proposition 4.6 on two examples of quasi-bounded portfolios.

Example 4.7.

Consider portfolio with being the segment in the plane with end-points and . Then

Example 4.8.

Consider portfolio from Example 2.7. If all components of are identical, then

5 Conical market models

5.1 Random exchange cones

Let for and a (possibly random) exchange cone , see Example 2.2. Then

| (12) |

where the first inclusion relation is due to the subadditivity of and the second one follows from the dilatation monotonicity of law invariant risk measures. If and are independent, the lower bound becomes .

Since is infinite unless almost surely belongs to the dual cone and for , the lower bound (9) turns into

| (13) |

The right-hand side of (13) corresponds to the dual representation for set-valued risk measures from Kulikov (2008) and Hamel et al. (2011), where it is written as function of only.

Consider now the frictionless case, where is a random half-space, so that for a random direction . Then

where is a family of non-negative -integrable random variables such that for all .

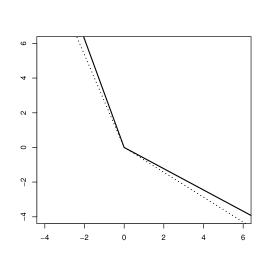

Example 5.1 (Bivariate frictionless random exchanges).

Consider two currencies exchangeable at random rate without transaction costs, see Example 2.3, so that the exchange cone is the half-plane with normal . Assume that for two identical -risk measures. The selection risk measure of is the closure of the set of for and , see Example 8.3 for a numerical illustration.

The value of is useful to bound the selection risk measure of , see (12). Assume that both and are -integrable. For the purpose of computation of it suffices to consider selections of the form , where . Furthermore, it suffices to consider separately almost surely positive and almost surely negative . Then is a cone in bounded by the two half-lines with slopes

The canonical choices and yield that

where the maximal and minimal elements above are obtained after applying the Jensen inequality to the dual representation of a univariate risk measure (observe that is convex on the positive half-line). Therefore, contains the cone with slopes given by and .

A lower bound for relies on a lower bound for and an upper bound for . Using the dual representation of as for a family of random variables with positive expectation, for (positive) we have

where the inequality follows from setting . Then

If is the expected shortfall , so that consists of all random variables taking value with probability and otherwise, and if has continuous distribution with a convex support, then

where denotes the value-at-risk. With a similar argument,

see Figure 3 for the corresponding lower and upper bounds. For any the upper bound for is not greater than the lower bound for meaning that is distinct from the whole space.

Proposition 5.2.

Let . Consider the selection measure generated by with all components being expected shortfalls at level . If , where is a half-plane with normal such that , has convex support, and and are independent, then is distinct from the whole plane.

5.2 Deterministic exchange cones

Assume that for a deterministic exchange cone and a -integrable random vector . Since , (12) yields that

Proposition 5.3.

Assume that has all identical components being . Then

| (14) |

Proof.

The result follows from Proposition 4.6 and the fact that if and otherwise the support function is infinite. ∎

A risk measure of for a deterministic cone is said to marginalise if its values are translates of for all . The coherency of implies that the intersection in (14) can be taken over all being extreme elements of , which in dimension 2, yields that is a translate of cone . In general dimension, if is a Riesz cone (i.e. with the order generated by is a Riesz space), then with being the supremum of in the order generated by . Similar risk measures were proposed in (Cascos and Molchanov, 2007, Ex. 6.6), where instead of a depth-trimmed region was considered.

Example 5.4.

Let all components of be univariate expected shortfalls at level , so that is the family of indicator random variables for all measurable with for some fixed . Then becomes the vector-valued worst conditional expectation (WCE) of introduced in (Jouini et al., 2004, Ex. 2.5). Furthermore, (14) yields the set-valued expected shortfall (ES) defined as

Its explicit expression if is a Riesz cone is given in (Cascos and Molchanov, 2007, eq. (7.1)) — in that case is a translate of . Since the univariate ES and WCE coincide for non-atomic random variables, their multivariate versions coincide by Proposition 4.6 if has a non-atomic distribution. It should be noted that is only a lower bound for the selection risk measure defined by applying to the individual components of selections of . In particular, the acceptability of under does not necessarily imply the existence of an acceptable selection of .

The following result deals with the comonotonic case, see Föllmer and Schied (2004) for the definition of comonotonicity and comonotically additive risk measures.

Theorem 5.5.

Assume that has all identical comonotonic additive components . If the components of are comonotonic and is a deterministic exchange cone, then .

Proof.

Since is comonotonic additive and is comonotonic, for any . Then

and consequently . ∎

Notice that is solely determined by the marginal distributions of . Consequently, if is a comonotonic rearrangement of (i.e. a random vector with the same marginal distributions and comonotonic coordinates), then

The following result shows that does not change if instead of all selections of one uses only those being deterministic functions of .

Theorem 5.6.

Set-valued portfolio is acceptable if and only if for a selection , which is a deterministic function of .

Proof.

If , then is acceptable. For the reverse implication, the dilatation monotonicity of the components of yields that

It remains to note that the conditional expectation is a function of taking values from , since is a deterministic convex cone. ∎

Example 5.7 (Frictionless market with deterministic exchange rates).

Consider a vector of terminal gains on currencies that can be exchanged without transaction costs, so that is a half-space with normal , where is the number of units of currency needed to by one unit of currency one, see Example 2.3.

Let with possibly different components whose maximal dual representations involve families of -integrable random variables from (10). It will be shown later on in Corollary 7.8 that for some family satisfying the condition of Theorem 4.3.

Then if and only if , , for a random variable from . The family determines the coherent risk measure called the convex convolution of , see Delbaen (2012). Then is acceptable under if and only if and

If all components of represent the same currency, but the regulator requirements applied to each component are different, e.g. because they represent gains in different countries, then and is acceptable if and only if .

While the above examples and Theorem 5.5 provide of the marginalised form , this is not always the case, as Example 8.1 confirms.

The calculation of for and can be facilitated by using the following result. It shows that coincides with its upper bound sufficiently far away from the origin.

Proposition 5.8.

Assume that and has all identical components . If for a deterministic cone and an essentially bounded random vector in dimension , then for all with sufficiently large norm, implies that .

Proof.

In dimension 2, we can always assume that the cone is generated by a bid-ask matrix (see Example 2.3), so that and its dual are given by

where

By Proposition 5.3 and by the coherence of ,

| (15) |

In order to obtain a point lying on the boundaries of both and , consider the positive random variable

Then

has the first a.s. deterministic coordinate. Since is a.s. non-negative, is a selection of . Define

The fact that guarantees that . Since and the first component of is constant,

| (16) |

where the last equality holds because and are orthogonal. Because of (15) and (16), lies on the supporting line of which is normal to , whence it lies on the boundaries of and .

By a similar argument,

lies on the supporting line of which is normal to , so on the boundaries of and .

Let be the radius of a closed ball centred at the origin and containing the triangle with vertices at , , and the vertex of cone . If with , then clearly for some , which by the convexity of and the fact that guarantees that . ∎

6 Numerical risk measures for set-valued portfolios

The set-valued risk measure gives rise to several numerical coherent risk measures, i.e. functionals with values in that satisfy the following properties.

-

1.

There exists such that for all .

-

2.

If , then .

-

3.

for all .

-

4.

.

The canonical scalarisation construction relies on the support function of . Namely,

is a law invariant coherent risk measure for each . Furthermore, is acceptable under , i.e. , if and only if is acceptable under for all . If the exchange cone is trivial, i.e. , then is given by a linear combination of the marginal risks.

Let . The max-correlation risk measure of -integrable random vector is defined as

where the supremum is taken over all random vectors distributed as , see Burgert and Rüschendorf (2006); Rüschendorf (2006). A general coherent numerical risk measure of can be represented as the supremum of over a family . Then the set of that make acceptable is given by

which is given by (13).

In the spirit of (Farkas et al., 2014), it is possible to define the numerical risk of as infimum of the payoffs for eligible portfolios , such that is acceptable, i.e. contains a selection with all acceptable components. In the conical market model and selection risk measures setting, this can be rephrased as infimum of for from , where is the subset of that consists of random vectors with all individually acceptable components.

7 Dual representation

The representation of the selection risk measure by (5) can be regarded as its primal representation. In this section we arrive at the dual representations of the selection risk measure and also general set-valued coherent risk measures of set-valued portfolios.

7.1 Lipschitz space of random sets

In general, the support function at a deterministic may be infinite with a positive probability. In order to handle this situation, we identify a random set-valued portfolio with its support function evaluated at random directions and consider some special families of set-valued portfolios.

Fix a (possibly random) closed convex cone , define . Since is compact, all its selections are bounded. Note that is endowed with the -metric. Let be the family of all functions such that is uniformly -integrable on and is Lipschitz with -integrable Lipschitz constant . The Lipschitz space is with the norm defined as the maximum of the -norm of and the -norm of the supremum of over all .

A set-valued portfolio is said to belong to the space if the effective domain of its support function is , and belongs to the space . Since

provides a linear embedding of such set-valued portfolios into .

Lemma 7.1.

Assume that , where is a convex cone and is a random closed set with the -integrable norm . Then belongs to , where is the dual cone to and is at most the -norm of .

Proof.

The domain of the support function of is , and for all . It is known that the support function of a compact set is Lipschitz with the Lipschitz constant being the norm of this set, see (Molchanov, 2005, Th. F.1). Thus, both the Lipschitz constant of and the supremum of for are bounded by . ∎

A quasi-bounded portfolio belongs to if is -integrably bounded. If , then does not belong to , no matter what is.

Example 2.3 (cont.).

The random set for an exchange cone with an efficient friction belongs to if is -integrable, and is bounded by the -norm of . In the case of some frictionless exchanges the choice of is not unique, and the above statement holds with chosen from the intersection of and the linear hull of .

Considering portfolios of the form from the space means that all of them share the same exchange cone . This is reasonable, since the diversification effects affect only the portfolio components, while the (possibly random) exchange cone remains the same for all portfolios. This setting also corresponds to one adapted in Hamel et al. (2011); Kulikov (2008) by assuming that the conical models share the same exchange cone.

Consider linear functionals acting on as

| (17) |

where is a random signed measure with -integrable weights assigned to its atoms and any . Note that (17) does not change if is a signed measure attaching weights or to , . These functionals form a linear space and build a complete family, in particular, the values of uniquely identify the distribution of . Indeed, by the Cramér–Wold device, it suffices to take with atoms located at selections of scaled by -integrable random variables in order to determine the joint distribution of the values of at these selections.

7.2 Weak-star convergence and dual representation

It is known (Johnson, 1970, Th. 4.3) that a sequence of functions from a

Lipschitz space with values in a Banach space weak-star converges

if and only if the norms of the functions are uniformly bounded and

their values at each given argument weak-star converge in . Note

that the weak convergence in Lipschitz spaces has not yet been

characterised, see Hanin (1997). In our case . Thus, the

sequence weak-star converges to if and only if

i) are uniformly bounded in ;

ii) for each , converges to

weakly in if and in probability

if .

Lemma 7.2.

Let and , , belong to the Lipschitz space . If weak-star converges to in , then the Hausdorff distance converges to zero in probability and a.s. for a deterministic compact set and all .

Proof.

The weak-star convergence yields the uniform boundedness for the -norms of , so that is bounded by a constant for all , meaning that is a subset of for a deterministic set . Furthermore, the Lipschitz constant of is bounded by . Let be a (random) -net in . Then

It suffices to note that converges in probability to for each . ∎

Consider a general set-valued coherent risk measure from Definition 2.9. If the family

of acceptable set-valued portfolios is weak-star closed, the risk measure is said to satisfy the Fatou property. In view of the cash invariance property, this formulation of the Fatou property is equivalent to if weak-star converges to in , cf. Kulikov (2008). Recall that the upper limit of is the set of limits for all convergent subsequences of , where , , see (Molchanov, 2005, Def. B.4).

Theorem 7.3 (Dual representation).

A function on random sets from with values being convex closed upper sets is a set-valued coherent risk measure with the Fatou property if and only if given by (9) for a certain family .

Proof.

Necessity. Note first that (9) can be equivalently written as

| (18) |

for being the family of counting measures with atoms from .

The dual cone to is the family of signed measures on with -integrable total variation such that for all . Since is acceptable for each random compact convex set containing the origin, each is non-negative. By the bipolar theorem, is the dual cone to .

Sufficiency. By Theorem 4.2, is a set-valued coherent risk measure. By an application of the dominated convergence theorem and noticing that the weak-star convergence implies the uniform boundedness of the norms, its acceptance set is weak-star closed. ∎

Example 2.3 (cont.).

If for a random exchange cone and -integrable random vector , then with and for all . If , then the weak-star convergence of to implies that weakly converges to in for and in probability if for all . Furthermore, the weak convergence of implies the boundedness of their -norms and so the uniform boundedness of . In case , the uniform boundedness of the norms follows from the weak-star convergence of to . Thus, weak-star converges to . In the case of (partially) frictionless models the random vectors and should be chosen appropriately from the intersections of the corresponding set-valued portfolios with the linear hull of . By Theorem 7.3, set-valued coherent risk measures defined on portfolios and satisfying the Fatou property can be represented by (9), which is exactly the dual representation Kulikov (2008) for and from Hamel et al. (2011) for a general .

7.3 Fatou property of selection risk measure

Since the selection risk measure is a special case of a general set-valued coherent risk measure, for a suitable (and possibly non-unique) family provided satisfies the Fatou property. Note that the Fatou property of is weaker than the Fatou property of , which is established in the following theorems. Even for the simplest selection risk measure being the selection expectation (see Example 3.8), the Fatou property is a rather delicate result proved in Balder and Hess (1995).

Theorem 7.4.

Assume that a.s. and imply that a.s. If , then the selection risk measure satisfies the Fatou property on random sets from .

Proof.

By the cash invariance property, it suffices to assume that for , with the aim to show that . Without loss of generality assume that for , .

Assume first that . Then there is a subsequence that weakly converges to in . For each and ,

| (19) |

In view of the weak-star convergence of to , and passing to the limits as , we have

Thus, a.s. meaning that is a selection of .

The -weak lower semicontinuity of the risk measure (see (Kaina and Rüschendorf, 2009, Th. 3.1)) yields that

where the lower limit is understood coordinatewisely, meaning that is acceptable.

Now assume that . The normalised sequence is -bounded and so admits a weakly convergent subsequence and so we assume without loss of generality that weakly converges in to . Then is acceptable since

By (19), for all and . Thus, a.s., so that and . This contradicts the imposed condition, since and so is not zero with a positive probability. ∎

The condition of Theorem 7.4 holds if the interior of almost surely contains a deterministic point and has all identical components such that for any non-trivial non-positive . Indeed, then is strictly negative for contrary to .

Theorem 7.5.

For , the selection risk measure satisfies the Fatou property on quasi-bounded set-valued portfolios.

Proof.

If necessary by passing to a subsequence, assume that and . Then, for all there exists such that .

The weak-star convergence of in implies that for a constant and all , . Thus, , , are all subsets of a fixed compact set , and the Hausdorff distance converges to zero in probability as . By (Molchanov, 2005, Th. 1.6.21), converges to in probability as random closed sets. The convergence in probability implies the weak convergence of random closed sets, see (Molchanov, 2005, Cor. 1.6.22), so that weakly converges to because the map is continuous on quasi-bounded portfolios. Since the family of convex subsets of a compact set is compact in the Hausdorff metric and , it is possible to find a subsequence of that weakly converges to . Pass to the chosen subsequence and realise the pairs on the same probability space, so that in the Hausdorff metric and a.s. with a.s.

Since the components of satisfy the Fatou property and are uniformly bounded,

Thus, . ∎

Recall that denote the subsets of that yield the maximal dual representations of the components of , see (10).

Corollary 7.6.

The selection risk measure on set-valued portfolios from for (under conditions of Theorem 7.4) and on quasi-bounded portfolios for equals and admits representation as for a family such that each satisfies for all .

Proof.

Consider the sequence , . Then the Fatou property of established in Theorems 7.4 and 7.5 implies that the upper limit of (being the closure of ) is a subset of , so that is closed.

Consider any with . Then is an acceptable set-valued portfolio, so that . By (9), this is the case if and only if for all . In turn, this is equivalent to for all such that and being the th component of . Since provides the maximal dual representation of , it necessarily contains . ∎

The following result establishes the Fatou property for the selection risk measure for and portfolios obtained as for a deterministic exchange cone .

Theorem 7.7.

For , the selection risk measure satisfies the Fatou property on the family of portfolios obtained as for an essentially bounded random vector and a fixed deterministic exchange cone .

Proof.

The weak-star convergence of implies that the Hausdorff distance between and converges to zero in probability and for a constant and all . Since there exists such that for all , we have that for some and a compact set . If does not contain any line and , this means that is uniformly bounded and converges to in probability, where . If contains a line, then and can be chosen to satisfy this requirement, say by letting be the intersection of the largest affine space contained in with the linear hull of .

For each , the numerical risk measure defined as a function of a random vector is law invariant and coherent, so that it satisfies the Fatou property by (Ekeland and Schachermayer, 2011, Th. 2.6) which also applies if the cash invariance property is relaxed as in Burgert and Rüschendorf (2006). Thus, if converges to in probability and a.s. for all , then

If , then for a certain sequence . Therefore,

Thus,

so that contains the upper limit of . ∎

Corollary 7.8.

If , the selection risk measure for set-valued portfolios with a fixed deterministic exchange cone has closed values and is equal to for a certain family of integrable random vectors such that each satisfies for all .

Proof.

It should be noted that not all risk measures are selection risk measures, and so the acceptability of under does not immediately imply the existence of an acceptable selection and so does not guarantee the existence of a trading strategy that eliminates the risk. While the calculation of the risk measure may be rather complicated, its primal representation (5) as the selection risk measure opens a possibility for an approximation of its values from above by exploring selections of .

8 Computation and approximation of risk measures

The evaluation of involves calculation of for all selections . The family of such selections is immense, and in application only several possible selections can be considered. A wider choice of selections is in the interest of the agent in order to better approximate from above and so reduce the required capital reserves. For lower bounds, one can use the risk measure or its superset obtained by restricting the family , e.g. if has all identical components.

In view of (5) and the convexity of its values, contains the convex hull of the union of for any collection of selections . It should be noted that this convex hull is not subadditive in general (unless the family of selections builds a cone) and so itself cannot be used as a risk measure, while providing a reasonable approximation for it. It is possible to start with some “natural” selections and and consider all their convex combinations or combine them as for events .

For the deterministic exchange cone model , it is sensible to consider selections for all and a selection taking values from the boundary of . By Theorem 5.6, it suffices to work with selections of which are functions of , and write them as . Since the aim is to minimise the risk, it is natural to choose which is a sort of “countermonotonic” with respect to , while choosing comonotonic and does not yield any gain in risk for their sum.

Assume that the components of are expected shortfalls at level . Then in order to approximate , it is possible to use a “favourable” selection constructed by projecting onto following the two-step procedure. First, is translated by subtracting the vector of univariate -quantiles in order to obtain random vector whose univariate -quantiles are zero. Then is projected onto the boundary of the solvency cone and is defined as the opposite of such projection. If belongs to the centrally symmetric cone to , it is mapped to the origin and no compensation will be applied in this case. Consider all selections of the form for . With this choice, the components of assuming small values are partially compensated by the remaining components.

An alternative procedure is to modify the projection rule, so that only some part of the boundary of the solvency cone is used for compensation. In dimension , and are defined by projecting onto either one of the two half-lines that form the boundary of .

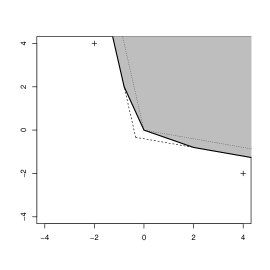

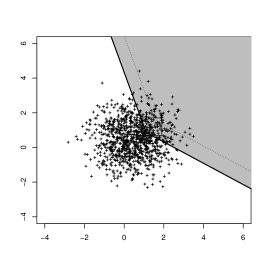

Example 8.1.

Consider the random vector taking values and with equal probabilities. Let be the cone with the points and on its boundary, so the corresponding bid-ask matrix has entries , see Example 2.3. Assume that consists of two identical components being the expected shortfall at level . Observe that and for

we obtain and .

By Theorem 5.6, the boundary of is given by with belonging to the boundary of . In order to compensate the risks of it is natural to choose as function of such that or and or for . The minimisation problem over and can be easily solved analytically (or numerically) and yields the boundary of . In Figure 1, the boundary of is shown as dashed line, the boundary of is dotted line, while is the shaded region.

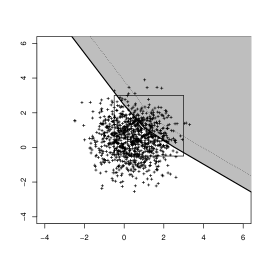

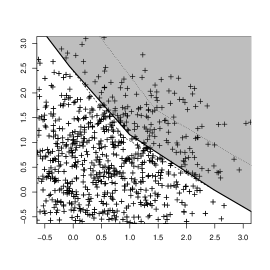

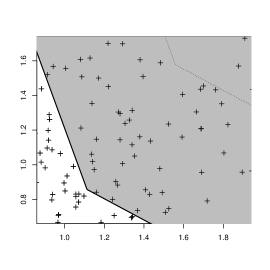

Example 8.2.

Consider the cone with the points and on its boundary, so the corresponding bid-ask matrix has entries . Let consist of two identical components. Let follow the empirical distribution for a sample of observations from the bivariate normal distribution with i.i.d. components of mean and variance .

In order to approximate from above (i.e. construct a subset of ), we first determine the set consisting of for the selections of obtained as , , and , for and , , described above using projection on and the two half-lines from its boundary. Then we determine the convex hull of and the points and described in the proof to Proposition 5.8 and finally add to this convex hull.

Figure 2(a) shows a sample of observations of a standard bivariate normal distribution and the approximation to the true value of described above, on the right panel a detail of the same plot is presented. The constructed approximation to is the shaded region, the boundary of obtained as described in Proposition 5.3 is plotted as dashed line, and the boundary of is plotted as dotted line.

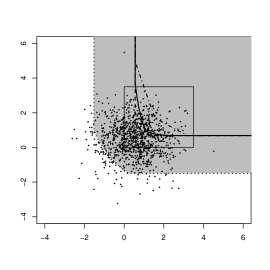

Example 8.3.

Consider the random frictionless exchange of two currencies described in Examples 1.1 and 5.1. Transactions that diminish the risk of can be constructed by projecting onto the boundary line to half-plane with normal and then subtracting the scaled projection from . This leads to the family of selections for and given by

| (20) |

Assume that the exchange rate is log-normally distributed with mean being the initial exchange rate and volatility . We approximate the risk of with having a bivariate standard normal distribution and independent of (equivalently independent of ) for with two identical components being . Observe that and , where is the cumulative distribution function of a standard normal random variable and its quantile function.

Fix , and the volatility . The bounds on are given by two cones and whose boundaries are determined in Example 5.1, see Figure 3. Namely is bounded by half-lines with slopes and , while the half-lines determining have slopes and , see Example 5.1.

In order to approximate the risk of , we take a sample of observations of . Denote by a random vector whose distribution is the empirical distribution of the sample of and by a random half-space with normal . Note that the empirical distribution of the exchange rate is bounded away from the origin and infinity.

Figure 4(a) shows a sample of observations of a standard bivariate normal distribution and an approximation to the true value of obtained as the sum of the convex hull of the risks of the selections of described in (20) and (solid line). The boundary of is shown as dotted line. The tip of the solid cone is approximately at , where is the selection from (1). Since the tip of the cone is the tangent point to in direction , it yields the minimal initial capital requirement of units of the first currency, as mentioned in Example 1.1.

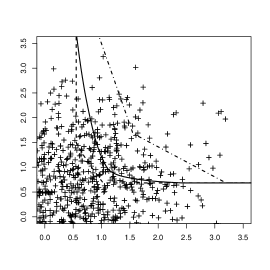

Example 8.4.

Consider the restricted liquidity situation from Example 2.5. Let , where follows a bivariate standard normal distribution and is the half-plane as in Examples 1.1 and 8.3. Assume that . Transactions that diminish the risk of can be constructed by projecting onto the boundary line to half-plane with normal and then subtracting the projection from . If the obtained point lies out of the line segment with end-points and , we take the nearest of the two end-points. This leads to a selection of given by (2). Other relevant selections of are and .

In order to approximate the risk of , we take a sample of observations of . Denote by a random vector whose distribution is the empirical distribution of the sample, by a random half-space with normal , and let .

Figure 5(a) shows a sample of observations of and an approximation to the true value of obtained by calculating risks of all convex combinations of the selection of defined by (2) and the selections , . The shaded region with boundary plotted as a dotted line is , the reflected selection expectation of . The boundary of is plotted as a dashed line, and the boundary of as a dash-dot line. The point belongs to the solid line and yields the capital reserves of mentioned in Example 1.1.

References

- Acciaio and Penner (2011) Acciaio, B. and I. Penner (2011): Dynamic risk measures. In Advanced mathematical methods for finance, 1–34. Heidelberg: Springer.

- Acerbi and Tasche (2002) Acerbi, C. and D. Tasche (2002): On the coherence of expected shortfall. J. Banking Finance 26, 1487–1503.

- Artzner et al. (1999) Artzner, P., F. Delbaen, J.-M. Eber, and D. Heath (1999): Coherent measures of risk. Math. Finance 9, 203–228.

- Balder and Hess (1995) Balder, E. J. and C. Hess (1995): Fatou’s lemma for multifunctions with unbounded values. Math. Oper. Res. 20, 175–188.

- Ben Tahar and Lépinette (2013) Ben Tahar, I. and E. Lépinette (2013): Vector-valued risk measure processes. Technical report, Université Paris-Dauphine, Paris. http://dx.doi.org/10.2139/ssrn.2241027.

- Biagini and Fritelli (2008) Biagini, S. and M. Fritelli (2008): A unified framework for utility maximization problems: an Orlicz space approach. Ann. Appl. Probab. 18, 929–966.

- Bion-Nadal and Kervarec (2012) Bion-Nadal, J. and M. Kervarec (2012): Risk measuring under model uncertainty. Ann. Appl. Probab. 22, 213–238.

- Burgert and Rüschendorf (2006) Burgert, C. and L. Rüschendorf (2006): Consistent risk measures for portfolio vectors. Insurance Math. Econom. 38, 289–297.

- Cascos and Molchanov (2007) Cascos, I. and I. Molchanov (2007): Multivariate risks and depth-trimmed regions. Finance and Stochastics 11, 373–397.

- Cheridito and Li (2009) Cheridito, P. and T. Li (2009): Risk measures on Orlicz hearts. Math. Finance 19, 189–214.

- Cherny and Grigoriev (2007) Cherny, A. S. and P. G. Grigoriev (2007): Dilatation monotone risk measures are law invariant. Finance and Stochastics 11, 291–298.

- Cousin and Di Bernardino (2013) Cousin, A. and E. Di Bernardino (2013): On multivariate extension of Value-at-Risk. J. Multivariate Anal. 119, 32–46.

- Delbaen (2002) Delbaen, F. (2002): Coherent risk measures on general probability spaces. In Advances in Finance and Stochastics, eds. K. Sandmann and P. J. Schönbucher, 1–37. Berlin: Springer.

- Delbaen (2012) Delbaen, F. (2012): Monetary Utility Functions. Osaka: Osaka University Press.

- Drapeau and Kupper (2013) Drapeau, S. and M. Kupper (2013): Risk preferences and their robust representation. Math. Oper. Res. 38, 28–62.

- Ekeland et al. (2012) Ekeland, I., A. Galichon, and M. Henry (2012): Comonotonic measures of multivariate risks. Math. Finance 22, 109–132.

- Ekeland and Schachermayer (2011) Ekeland, I. and W. Schachermayer (2011): Law invariant risk measures on . Statist. Risk Modeling 28, 195–225.

- Embrechts and Puccetti (2006) Embrechts, P. and G. Puccetti (2006): Bounds for functions of multivariate risks. J. Multivariate Anal. 97, 526–547.

- Farkas et al. (2014) Farkas, W., P. Koch-Medina, and C.-A. Munari (2014): Measuring risk with multiple eligible assets. Technical report, arXiv:1308.3331v2 [q-fin.RM].

- Feinstein and Rudloff (2014a) Feinstein, Z. and B. Rudloff (2014a): A comparison of techniques for dymanic risk measures with transaction costs. In Set Optimization and Applications in Finance, eds. A. Hamel, F. Heyde, C. Löhne, and C. Schrage. Springer. To appear, arXiv:1305.2151v1 [q-fin.RM].

- Feinstein and Rudloff (2014b) Feinstein, Z. and B. Rudloff (2014b): Multi-portfolio time consistency for set-valued convex and coherent risk measures. Finance and Stochastics To appear, arXiv:1212.5563v1 [q-fin.RM].

- Föllmer and Schied (2004) Föllmer, H. and A. Schied (2004): Stochastic Finance. An Introduction in Discrete Time. Berlin: De Gruyter, 2nd edition.

- Hamel and Heyde (2010) Hamel, A. H. and F. Heyde (2010): Duality for set-valued measures of risk. SIAM J. Financial Math. 1, 66–95.

- Hamel et al. (2011) Hamel, A. H., F. Heyde, and B. Rudloff (2011): Set-valued risk measures for conical market models. Math. Finan. Economics 5, 1–28.

- Hamel et al. (2013) Hamel, A. H., B. Rudloff, and M. Yankova (2013): Set-valued average value at risk and its computation. Math. Finan. Economics 7, 229–246.

- Hanin (1997) Hanin, L. G. (1997): Duality for general Lipschitz classes and applications. Proc. London Math. Soc. 75, 134–156.