A partial least squares algorithm handling ordinal variables

also in presence of a small number of categories

![[Uncaptioned image]](/html/1212.5049/assets/x1.png)

A Partial Least Squares Algorithm

Handling Ordinal Variables also in Presence

of a Small Number of Categories

Gabriele Cantaluppi

Dipartimento di Scienze statistiche

Università Cattolica del Sacro Cuore

Largo A. Gemelli, 1, 20123 Milano, Italy

gabriele.cantaluppi@unicatt.it

Abstract: The partial least squares (PLS) is a popular modeling technique commonly used in social sciences. The traditional PLS algorithm deals with variables measured on interval scales while data are often collected on ordinal scales: a reformulation of the algorithm, named ordinal PLS (OPLS), is introduced, which properly deals with ordinal variables. An application to customer satisfaction data and some simulations are also presented. The technique seems to perform better than the traditional PLS when the number of categories of the items in the questionnaire is small (4 or 5) which is typical in the most common practical situations.

Keywords: Ordinal Variables, Partial Least Squares, Path Analysis, Polychoric Correlation Matrix, Structural Equation Models with Latent Variables

1 Introduction

The partial least squares (PLS) technique is largely used in socio-economic studies where path analysis is performed with reference to the so-called structural equation models with latent variables (SEM-LV).

Furthermore, it often happens that data are measured on ordinal scales; a typical example concerns customer satisfaction surveys, where responses given to a questionnaire are on Likert type scales assuming a unique common finite set of possible categories.

In several research and applied works, averages, linear transformations, covariances and Pearson correlation coefficients are conventionally computed also on the ordinal variables coming from surveys. This practice can be theoretically justified by invoking the pragmatic approach to statistical measurement (Hand, 2009). Namely according to this approach ’the precise property being measured is defined simultaneously with the procedure for measuring it’ (Hand, 2012), so when defining a construct, e.g. the overall customer satisfaction, the measuring instrument is also defined, and ’in a sense this makes the scale type the choice of the researcher’ (Hand, 2009).

A more traditional approach (see Stevens, 1946) would require appropriate procedures to be adopted in order to handle manifest indicators of the ordinal type. Within the well-known covariance-based framework, several approaches are suggested in order to appropriately estimate a SEM-LV model; in particular, Muthén (1984), Jöreskog (2005) and Bollen (1989) make the assumption that to each manifest indicator there corresponds an underlying continuous latent variable, see Section 3.

Other approaches have been proposed to deal with ordinal variables within the Partial Least Squares (PLS) framework for SEM-LV: Jakobowicz & Derquenne (2007) base their procedure on the use of generalized linear models; Nappo (2009) and Lauro et al. (2011) on Optimal Scaling and Alternating Least Squares; Russolillo & Lauro (2011) on the Hayashi first quantification method (Hayashi, 1952).

As observed by Russolillo & Lauro (2011) in the procedure by Jakobowicz & Derquenne (2007) a value is assigned to the impact of each explanatory variable on each category of the response, while the researcher may be interested in the impact of each explanatory variable on the response as a whole. The same issue characterizes the techniques illustrated in the Chapter 5 by Lohmöller (1989). The present proposal goes in this direction: a reformulation of the PLS path modeling algorithm is introduced, see Section 6, allowing us to deal with variables of the ordinal type in a manner analogous to the covariance based procedures.

In this way we recall the traditional psychometric approach, by applying a method for treating ordinal measures according to the well-known Thurstone (1959) scaling procedure, that is assuming the presence of a continuous underlying variable for each ordinal indicator. The polychoric correlation matrix can be defined. We show that by using this matrix one can obtain parameter estimates also within the PLS framework.

When the number of points of the scale is sufficiently high the value of the polychoric correlation between two variables is usually quite close to that of the Pearson correlation; in these situations there would be no need to have recourse to polychoric correlations and the traditional PLS algorithm may be applied. However, to make the response of interviewed people easier, it is common practice to administer questionnaires whose items are measured on at most 4 or 5 point alternatives: in these circumstances the proposed modification of the PLS algorithm seems to be appropriate.

An application to customer satisfaction data and some simulations conclude the paper.

2 The Structural Equation Model with latent variables

A linear SEM-LV consists of two sets of equations (see Bollen, 1989): the structural or inner model describing the path of the relationships among the latent variables, and the measurement or outer model, representing the relationships linking the latent variables, which cannot be directly observed, to appropriate corresponding manifest variables.

The inner model

The structural model is represented by the following linear relation

| (1) |

where is an vector of latent endogenous random variables (dependent variables); is an vector of latent exogenous random variables; is an vector of error components, zero mean random variables. and are respectively and matrices containing the so-called structural parameters. In particular the matrix contains information concerning the linear relationships among the latent endogenous variables: their elements represent the direct casual effect on each of the remaining . The matrix contains the coefficients explaining the relationships among the latent exogenous and the endogenous variables: their elements represent the direct causal effects of the components on the variables.

When the matrix is lower triangular or can be recast as lower triangular by changing the order of the elements in (which is possible if has all zero eigenvalues (see e.g. Faliva, 1992)) and is diagonal, then the model (1) is said to be causal or of the recursive type, which excludes feedback effects. In the sequel we will assume to be lower triangular.

The outer model

We consider only measurement models of the reflective type, which are adopted (see Diamantopoulos et al., 2008) when the latent variables ’determine’ their manifest indicators, and are defined according to the following linear relationships

| (2) | |||

| (3) |

where the vector random variables and represent the indicators for the latent variables and , respectively. Each latent construct in and in is characterized by a set of indicators, for and for .

The assumption of uncorrelation among the error components and uncorrelation between the errors and the independent variables in relationships (1)-(3) is made. All latent variables and errors are usually assumed to be multivariate distributed according to a Normal random variable.

Measurement models of the formative and of the MIMIC type may also be defined (see Esposito Vinzi et al., 2010) but are not considered here.

It often happens that the indicators are measured on ordinal scales, e.g. the responses given by the respondents to a questionnaire are on Likert type scales that assume a unique common finite set of possible categories. In this instance appropriate procedures are adopted for parameter estimation in SEM-LV in order to treat manifest indicators of the ordinal type. In Muthén (1984), Jöreskog (2005) Bollen (1989) and Bollen & Maydeu-Olivares (2007) estimation procedures within a covariance-based framework are presented, which are based on the assumption that for each manifest indicator there corresponds a further underlying continuous latent variable, whose definition is here described in Section 3.

The PLS specification

Observe that the structural relationship (1) can be re-written in matrix notation as

| (4) |

and the reflective measurement model (2)-(3) as

In the initial works on PLS (Wold, 1985; Lohmöller, 1989) the same notation is used for endogenous and exogenous entities; thus the above relationships are re-written as

| (5) | |||

| (6) |

by having (re-)defined

The sub-matrix , corresponding to the matrix which appears in (1), is assumed to be lower triangular. The so-called Wold predictor specification, , is made, giving rise to structural equation models of the causal type.

The measurement model of the reflective type is named ’Mode A’ in the PLS terminology.

3 Assumptions on the genesis of ordinal categorical observed variables

The set of responses are assumed to be expressed on a conventional ordinal scale. This type of scale requires, according to the classical psychometric approach, appropriate methods to be applied. Here we propose to adopt a traditional psychometric approach, by considering the existence of an underlying continuous unobservable latent variable for each observed ordinal manifest variable.

Following the PLS notation (5) and (6) for structural equation models with latent variables, the set of responses gives rise to a -dimensional random categorical variable, say , whose components may assume, for simplicity, the same ordered categories, denoted by the conventional integer values . is the dimension of in (6), corresponding to in (2)-(3), the sum of the dimensions of and .

Let , with , be the corresponding marginal probabilities and let

| (7) |

be the probability of observing a conventional value for not greater than . Furthermore assume that to each categorical variable there corresponds an unobservable latent variable , which is represented on an interval scale with a continuous distribution function . The distribution for the continuous -dimensional latent random variable is usually assumed to be multinormal. Each observed ordinal indicator is related to the corresponding latent continuous by means of a non linear monotone function (see Bollen, 1989; Muthén, 1984; Jöreskog, 2005), of the type

| (8) |

where are marginal threshold values defined as , being the cumulative distribution function of a specific random variable, usually the standard Normal, Jöreskog (2005); denotes the number of categories effectively used by the respondents; when each category has been chosen by at least one respondent.

We also set and and set to or 4 threshold values respectively lower than or larger than 4.

4 Appropriate covariance matrix in presence of ordinal categorical variables

We remember that covariance-based estimation procedures look for the parameter values minimizing the distance between the covariance matrix of the manifest variables, specified as a function of the parameters, and its sample counterpart. Since, in case of ordinal variables it is not possible to compute the covariance matrix, we have recourse to the polychoric correlation matrix or the polychoric covariance matrix (see Bollen, 1989).

For two generic ordinal categorical variables and , , the polychoric correlation is defined (see Drasgow, 1986; Olsson, 1979), as the value of maximizing the loglikelihood typically conditional on the marginal threshold estimates

where is the number of observations for the categories th of and th of ,

being the standard bivariate Normal distribution function with correlation conditional on the threshold values, , for and , respectively estimated by having recourse e.g. to the two marginal latent standard Normal variates according to the usual two step computation, and .

Later on we will assume that , that is each category has been chosen by at least one respondent, possibly substituting a negligible quantity, e.g. , to the zero s.

By considering the polychoric coefficients for each pairs and , we can obtain the polychoric correlation matrix (and also the covariance matrix, if appropriate location and scale values are assigned to the underlying latent variables (Jöreskog, 2005)), which, according to the covariance-based approach, is necessary for the parameter estimation of a structural model with manifest indicators of the ordinal type.

In case of manifest variables of generic type appropriate correlations should be computed (see Drasgow, 1986); in particular: a) polychoric correlation coefficients for pairs of ordinal variables, b) polyserial correlation coefficients between an ordinal variable and one defined on an interval or ratio scale, and c) Pearson correlation coefficients between variables defined on interval or ratio scales. However we will assume, later on, that only variables on ordinal scales are present.

5 Application within the PLS framework

In presence of manifest indicators of the ordinal type, we suggest a slightly modified version of model (5)-(6), where the manifest variables in relationship (6) are in a certain sense ’replaced’ by the underlying unobservable latent variables .

We do not write explicitly the dependence between and , since for the subject the real point value for each indicator is not known: we only assume that it belongs to the interval defined by the threshold values in (8) having as image the observed category .

It will be possible to obtain point estimates for the parameters in and , while only estimates of the threshold values will be directly predicted with regard to the scores of the latent variables .

The PLS algorithm structure typically adopted to obtain the PLS estimates in presence of standardized latent variables is briefly presented. Mode A (reflective outer model) is considered for outer estimation of latent variables and the centroid scheme for the inner estimation (Tenenhaus et al., 2005; Lohmöller, 1989).

Some linear algebra restatement of the algorithm is necessary, which renders the usual procedure apt to be applied with minor changes also in presence of manifest variables of the ordinal type.

5.1 The PLS algorithm

The PLS procedure obtaining the estimates of the parameters in (5)-(6) consists of a first iterative phase which produces the latent score estimates; subsequently the values of the vector , containing all the unknown parameters in the model (, etc.), are estimated, by applying the Ordinary Least Squares method to all the linear multiple regression sub-problems into which the inner and outer models are decomposed.

Remember that the whole set of true latent variables (always measured as differences from their respective average values) is summarized by the vector

being the first elements of the exogenous type and the remaining endogenous. Observe that, since we are in presence of models of the causal type, the generic endogenous variable , , may only depend on the exogenous variables and on a subset of its preceding endogenous latent variables.

With reference to the inner model, a square matrix , of order , indicating the structural relationships among latent variables may be defined:

| (9) |

The generic element of is given unit value if the endogenous is directly linked to ; is null otherwise. Then may be defined as the indicator matrix of in (5) by having set to 0 the elements on the main diagonal.

The PLS algorithm follows an iterative procedure, which defines, at the th generic step, the scores of each latent variable , according the so-called ’outer approximation’, as a standardized linear combination of the manifest variables corresponding to

| (10) |

with appropriate weights summing up to 1 (see Lohmöller, 1989).

In the PLS framework each latent variable is thus defined as a ’composite’ of its manifest indicators.

Step 0. The starting step of the algorithm uses an arbitrarily defined weighting system that, for the sake of simplicity, may be set to

| (11) |

The initial scores of the latent variables , , are defined as linear combinations of the centered values of the corresponding manifest variables , ; thus for the generic subject , , we have:

| (12) |

where , , denote the mean of the manifest variables associated to the latent variable . Observe that at step 0 the weights sum up to 1 by definition.

The scores are then standardized

| (13) |

where

is an estimate of the variance of , being the number of available observations.

We then set

| (14) |

Iterative phases of the PLS algorithm

Step 1. Define for each latent variable an instrumental variable as a linear combination of the estimates of the latent variables directly linked to

| (15) |

where

| (16) |

(remember that is the generic element of the matrix , used to specify the relationships in the inner model: if the latent variable is connected with in the path model representation, otherwise, see (9)) and

| (17) |

having zero mean.

Step 2. In case of the so-called Mode A (reflective outer model), at every stage of the iteration () update the vectors of the weights as

| (18) |

where

| (19) | |||

| (20) |

being

Looping. Loop step 1 to step 3 until the following convergence stop criterion is attained

where is an appropriately chosen positive convergence tolerance value.

Ending phase of the PLS algorithm

Carry out the ordinary least squares estimation of the coefficients linking to (for every inner submodel), the parameters (outer models, Mode A), specifying the linear relations between the latent and the corresponding manifest and the residual variances (having standardized the involved variables).

6 An equivalent formulation of the PLS algorithm and its implementation with ordinal variables

We now rewrite the PLS algorithm, by making extensive use of linear algebra notations, in order to avoid the reconstruction, at each step, of the latent scores. The procedure will be based on the covariance matrix of the observed manifest variables or the polychoric correlation matrix in case of manifest variables of the ordinal type.

Namely, in presence of ordinal indicators we substitute the categorical variables with the underlying latent variables , see (8), that are standardized and thus centered. Note that the components of are not observable, but in the algorithm we will only make use of variances and covariances defined on their linear transformations.

These variances and covariances can be derived as a function of , the covariance matrix of the vector random variable containing all the manifest indicators , of the metric/interval type, or their counterparts when the indicators are ordinal; in the latter case is the polychoric correlation matrix defined across the ordered categorical variables.

Step 0. The outer approximation for the generic variable is formally defined, see (10), as

Later on we will omit the symbol, here (0), specifying the iteration step of the algorithm.

Relationship (10) may be written in matrix form as

| (22) |

where are the centered manifest variables that, in presence of ordinal indicators, are set to .

It is now possible to define the matrix containing the outer approximation values of the latent variables for the subjects as

being the matrix of the deviations of the manifest variables from their means, and the square matrix containing the vectors as columns.

Thus the covariance (17) between and can be expressed as

| (23) |

and the variance covariance matrix of the random vector as

| (24) |

The standardized version (13) of is

where is the Hadamard element by element product, the identity matrix, and

| (25) |

is a transformation of the original weights , which for each group of manifest indicators sum up to 1, into a set of weights allowing the latent variables to be on a standardized scale. We then set

The covariance matrix across standardized can be re-defined as

| (26) |

so becoming a correlation matrix.

Iterative phases of the PLS algorithm

Step 1. The instrumental variables , see (15), which are defined for each latent variable as a linear combination of the estimates of the latent variables linked to in the path diagram may be expressed as

| (44) | |||||

| (48) |

where is the th column of the matrix with generic element defined, according to (15), as

| (49) |

being the elements of equal to 0 or 1.

With reference to the matrix of observable data the matrix containing the values of the instrumental variables for the subjects may be obtained as

Step 2. The covariance (19) between and is defined as

| (53) | |||||

| (68) | |||||

| (83) |

and the covariance matrix between all the manifest variables and the instrumental variables as

| (84) |

The covariance between and is

| (85) |

and the covariance matrix between all the manifest variables and the composites can be obtained as

| (86) |

Now define a matrix by the Hadamard product of the indicator matrix of the matrix and the covariance matrix between and

| (87) |

it results in a block diagonal matrix with generic block

The matrix with the updated weights is obtained from

| (88) |

where is the unitary vector, is the operator transforming a vector in a diagonal matrix and is the vector defined as

| (89) |

Finally transformation (25) may be applied to obtain the standardizing weights .

We resume the sequence of steps defining the reformulation of the PLS algorithm, which has the characteristic of avoiding the determination, at each step, of the composites scores and of the instrumental variables scores . Ending phases of the PLS algorithm will be described later (see Sections 6.1 and 6.2).

Compute (in case of ordinal items the polychoric correlation matrix)

Define the starting weights

Iterative phase

Set

Compute:

Update the weights

Obtain

Check if

6.1 Ending phase of the PLS algorithm with manifest variables of the interval type

After convergence of the weights in the score values can be determined as

and OLS regressions carried out (on standardized variables) to obtain the estimates of the parameters in and and the variances of the error components as the residual variances of the corresponding regression models.

6.2 Parameter Estimation of the inner and outer relationships in presence of ordinal manifest variables

The estimates in the inner and outer regression models can also be obtained without having to reconstruct the score values , that cannot be estimated in presence of manifest variables of the ordinal type: their prediction may be obtained according to one of the procedures illustrated in Section 6.3.

The parameter estimates make reference to the following linear regression models, defined on standardized variables,

| (90) |

where and is a subset of defined according to the th equation in (5).

The estimate of the vector , which contains the unknown elements of the row of matrix in (5), may be computed as

| (91) |

where is the matrix obtained by extracting from , the correlation matrix of , see (26), the rows and columns pertaining to the independent variables in the linear model (90) and is the vector obtained by extracting from the th column of the elements corresponding to correlations between and its covariates, according to relationship (90).

Let now be the correlation matrix between the manifest indicators and the composites , which can be derived from (86). The estimate of parameter in the outer model

is given by the correlation coefficient between and .

The ending phase of the PLS algorithm, in presence of manifest variables of the ordinal type, can be then resumed in the following way:

is equal to the correlation coefficient between and .

In presence of manifest variables of the interval type the procedure gives, by having recourse to Pearson’s correlations, the same results as the ending phase of the usual PLS algorithm presented in Section 6.1.

Only the ’covariance’ or ’correlation’ matrix of the manifest variables is needed in order to determine the final weights and the inner and outer model parameter estimates. In presence of manifest indicators of the ordinal type we propose to use the polychoric correlation matrix. This is consistent with the so-called METRIC 1 option suggested by Lohmöller (1989) (see also Tenenhaus et al., 2005; Rigdon, 2012) performing the standardization of all manifest indicators.

Both polychoric covariance and correlation matrices must be invertible for the above procedure to work. However, constrained algorithms do exist whenever invertibility problems should arise for the polychoric correlation matrix. (For example the function hetcor, available in the R polycor package, makes it possible to require that the computed matrix of pairwise polychoric, polyserial, and Pearson correlations be positive-definite).

After having transformed the manifest variables according to (8) the threshold values related to the standard normal variables are available. In this case we have , that is the polychoric covariance matrix between the underlying latent variables coincides with the polychoric correlation matrix.

The algorithm we have presented for ordinal manifest variables will be denoted as Ordinal Partial Least Squares (OPLS) from now on.

6.3 Prediction of Latent Scores

A point estimate of the composite continuous (latent) cannot be determined in presence of ordinal variables for the generic subject; we can only establish an interval of possible values conditional on the threshold values pertaining the latent variables that underlie each ordinal manifest variable.

Since each underlying variable is assumed to be a standard Normal variate, the composite variable , defined by the outer approximation

will also be distributed according to a standard Normal variate.

A set of threshold values , , can be derived from the threshold values referred to the variables , , being the common number of categories assumed by the variables , as

Should some threshold values equal they have to be replaced with . Later we will also consider and .

For the generic subject expressing the values for the variables , linked to the generic , let us first define the sets of values images of all possible .

In case subject chooses the same category for all the manifest indicators of , that is with , the image will be of the type

which we will call ’homogeneous thresholds’.

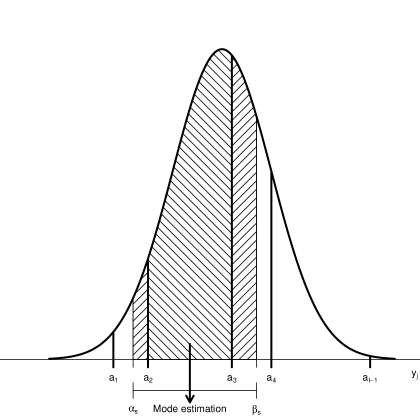

Otherwise, see Fig. 1, the set which is the image of all possible responses , will not correspond exactly to one subset . Let us denote this set with

where:

being and the threshold values corresponding to the category observed by subject , that is the values defining the interval for to have as image according to (8).

In order to assign a category to subject for the latent variable we can use one of the following options:

-

1.

Mode estimation. Compute, see Fig. 1, the probabilities for to overlap each set defined by the ’homogeneous thresholds’

(92) and, for subject , select the set with maximum probability. To the set corresponds the assignment of category as a score estimate for the latent variable .

Figure 1: Latent variable category assignment, see (92) -

2.

Median estimation. Compute the median of the variable over the interval

(93) the category pertaining the set to which belongs, is assigned to subject .

-

3.

Mean estimation. Compute the mean of the variable over the interval

(94) the category pertaining the set to which belongs, is assigned to subject .

6.4 Bias effects of the OPLS algorithm

Schneeweiss (1993) shows that parameter estimates obtained with the PLS algorithm are negatively biased for the inner model, (these estimates are related to the covariances or correlations across latent variables). The OPLS is based on the analysis of the polychoric correlation matrix, which is obtained by maximizing the correlation across the latent variables that generate, according to (8), the manifest variables. Especially in presence of items with a low number of categories, polychoric correlations are usually larger than the Pearson’s ones as was also observed by Coenders et al. (1997). Thus we may expect that the distribution of the inner model parameter estimates obtained with OPLS dominates stochastically that of the PLS algorithm, possibly reducing the negative bias of estimates based on Pearson’s correlations.

However, the reduction in the bias of the inner model parameter estimates for OPLS can have a drawback: a positive bias in the estimation of the parameters in the outer model. Fornell & Cha (1994) report, for the special case of identical correlation coefficients (say ) across all the manifest variables, the following relationship relating the bias of the PLS algorithm with respect to maximum likelihood estimates of the outer model parameters and the one referred to the common correlation across latent variables, upon which the inner model coefficients are obtained:

An high value for bias corresponds to a low value of bias; we have observed this issue in the illustration presented in Section 7.2.

Anyway, we have to observe that outer model parameters are not the most important target in a decision making procedure based on the PLS estimation of a structural equation model with latent variables: the main role is played by the inner model parameter estimates and by the weights see (10) and (22), defining each PLS latent variable as a ’composite’, that is a linear combination of its related manifest variables. The largest weights are related to the manifest variables which are supposed to have greater influence in driving the ’composite’; moreover, since the weights sum up to 1 they should not suffer of any dimensional bias problem.

6.5 Assessing reliability

Scale reliability can be assessed, for ordinal scales, by having recourse to methods based on the polychoric correlation matrix (see Zumbo et al., 2007; Gadermann et al., 2012) for Cronbach’s . The Dillon-Goldstein’s rho (Chin, 1998) and methods presented for covariance based models (Green & Yang, 2009; Raykov, 2002), which make reference to all relationships in the structural equation model (1)-(3), can also be implemented.

7 Illustrative examples

The Partial Least Squares algorithm has been successfully applied to estimate models aimed at measuring customer satisfaction, first at a national level (Fornell, 1996; Fornell et al., 1996) and then also in a business context (Johnson & Gustafsson, 2000; Johnson et al., 2001). A widespread literature on this field is available.

The OPLS methodology is here implemented in R (R Core Team, 2012) and applied to a well-known data set describing the measure of customer satisfaction in the mobile phone industry (Bayol et al., 2000; Tenenhaus et al., 2005). By means of this example we compare the behaviour of the PLS and OPLS in presence of a traditional questionnaire whose items are characterized by a high number of categories (say 10).

Some simulations are then reported to analyze the behaviour of the procedure when the number of points for each item is reduced.

The R procedures by Fox (2010) and Revelle (2012) are used to compute polychoric correlation matrices, with minor changes to allow polychoric correlations to be computed when the number of categories is larger than 8. We never needed the polychoric correlation matrix to be forced in order to comply with the positive definiteness condition.

7.1 The Mobile Phone Data Set

We applied the procedure to a classical example on mobile phone, presented in Bayol et al. (2000) and Tenenhaus et al. (2005). Data (250 observations) are available e.g. in Sanchez & Trinchera (2012). Data were collected on 24 ordered categorical variables with 10 categories; the observed variables are resumed by 7 latent variables.

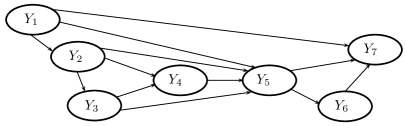

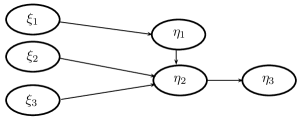

The customer satisfaction model underlying the mobile phone data refers to a version of the European Customer Satisfaction Index with 1 exogenous latent variable, the Image () with 5 manifest indicators, and 6 endogenous latent variables: Customer Expectations (), Perceived Quality (), Perceived Value (), Customer Satisfaction (), Loyalty () and Complaints (), with respectively and 3 manifest indicators. See Fig. 2 for the inner path model relationships. Table 1 in Tenenhaus et al. (2005) contains the structure of the questionnaire; it can be considered as a possible instrument for customer satisfaction measurement in the mobile phone industry.

Table 1 reports the parameter estimates obtained both with the standard PLS algorithm and with the OPLS algorithm.

| PLS | OPLS | ||||

|---|---|---|---|---|---|

| 0.491 | (0.000) | 0.584 | (0.000) | ||

| 0.545 | (0.000) | 0.612 | (0.000) | ||

| 0.067 | (0.281) | 0.037 | (0.563) | ||

| 0.540 | (0.000) | 0.596 | (0.000) | ||

| 0.153 | (0.006) | 0.199 | (0.001) | ||

| 0.035 | (0.431) | 0.035 | (0.423) | ||

| 0.544 | (0.000) | 0.517 | (0.000) | ||

| 0.201 | (0.000) | 0.198 | (0.000) | ||

| 0.541 | (0.000) | 0.563 | (0.000) | ||

| 0.212 | (0.001) | 0.261 | (0.000) | ||

| 0.466 | (0.000) | 0.493 | (0.000) | ||

| 0.051 | (0.376) | 0.043 | (0.417) | ||

Surprisingly, results are quite similar but not so close. When the number of categories is sufficiently high, Pearson correlation coefficients are good approximations for their polychoric counterparts, but responses in customer satisfaction surveys do usually have skewed distributions since respondents do not effectively choose, with a non-negligible frequency, all the available categories of the manifest variables. 6 over 24 manifest indicators had only 6 categories with at least 5 respondents. Thus differences between Pearson and polychoric correlations may be evident with effects on parameter estimates.

Coefficients computed with the OPLS algorithm, that are significantly different from 0, are larger (except for and ) than those obtained with the PLS algorithm which is known to underestimate the inner model parameters (see Schneeweiss, 1993) and it is also based on Pearson’s correlations which underestimate real correlations when the ordinal manifest variables are measured on scales with a small number of categories.

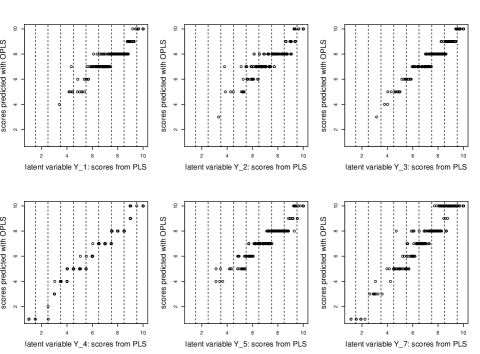

Figure 3 shows a comparison of the latent scores reconstructed with the two methodologies. Information about is not reported since the variable is identical to its unique manifest indicator.

Recall that according to the PLS algorithm the scores are weighted averages of the values expressed by the subjects on the proxies; the scores are thus generated on an interval scale. With the OPLS algorithm latent variable scores can only be predicted according to one of the procedures presented in Section 6.3 and their values are on the same ordinal scale common to the proxy variables (the procedure ’Mode estimation’ was adopted to produce the graph).

Table 2 shows the degree of coherency of the latent scores obtained with the traditional PLS algorithm and the 3 procedures presented in Section 6.3 for OPLS.

Having rounded scores obtained with the PLS algorithm to integer values, percentages of exact concordance are reported on the first three lines, while in the remaining lines are percentages of concordance with a difference between rounded values not larger than 1. We have at least 70% exact concordance (except for latent variable ); more than 90% of cases for all latent variables show a difference between rounded values lower than 1.

| Method | ||||||

|---|---|---|---|---|---|---|

| Mode estimationa | 70.0 | 71.6 | 79.2 | 84.4 | 71.6 | 49.2 |

| Median estimationa | 74.8 | 75.2 | 78.0 | 88.0 | 70.4 | 51.2 |

| Mean estimationa | 72.8 | 77.2 | 75.6 | 86.8 | 71.6 | 50.4 |

| Mode estimationb | 98.8 | 98.0 | 100.0 | 99.6 | 99.2 | 89.6 |

| Median estimationb | 99.2 | 98.4 | 100.0 | 100.0 | 99.2 | 94.0 |

| Mean estimationb | 99.2 | 98.4 | 100.0 | 99.6 | 99.6 | 90.0 |

a percentages of exact concordance after having rounded PLS scores to integer values

b percentages of concordance with a difference between rounded values not larger than 1

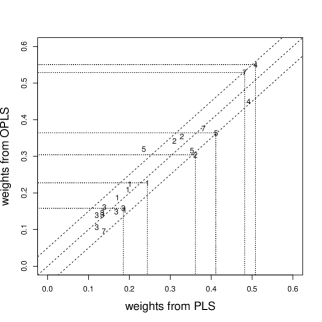

The weights , see relationships (18) or (88), play an important role in making decisions based on PLS estimation of structural equation model with latent variables. They establish which proxy variables drive a latent variable behaviour. Latent variables are defined as ’composite’ variables in the PLS algorithm, that is weighted averages of their manifest indicators with weights . Figure 4 shows the comparison of the weights for the 7 latent variables obtained with the two algorithms. Points with the same number identify the weights assigned by the two algorithms to the manifest indicators of each latent variable (values 6 do not appear since has only one indicator with unitary weight). Dashed bandwidths include pairs which differ, with the two methodologies, no more than 0.05. Only 2 values over the 23 weights are outside the bandwidths. We can conclude that the two methods construct composite variables in quite the same manner. Dotted lines give information for each latent variable about the indicator with the largest weight determined by the two algorithms: except for latent variables and the same proxy variable is identified as the most important in explaining each latent construct.

7.2 Some Simulations

To compare the performance of the classical PLS algorithm with the OPLS for different number of points in the scale of manifest variables we considered some simulations from the following model

see Figure 5.

Measurement models of the reflective type were assumed, with 3 manifest ordinal reflective indicators for each latent variable

In order to take into account the presence of asymmetric distributions, latent variables , were generated, in separate simulations, according both to the standard Normal distribution for all variables and Beta distributions with parameters for , for , for which were then standardized. Theoretical asymmetry indices , and correspond to the three Beta distributions. Values of the asymmetry indices for the mobile phone data analyzed in Section 7.1 are in the range except for one variable showing positive asymmetry. The model parameters were fixed to and . The coefficients of measurement models were set to . Both the variances of the error components in the inner model and those pertaining errors in the measurement models were set to values ensuring the latent indicators and the manifest variables and to have unit variance.

Manifest variables and were rescaled according to the following rules

with extrema computed over the sample realizations, being the desired number of points common to all items. Values were then rounded to obtain integer (ordinal) responses.

Simulations were performed by considering and 9 categories in the scales, which correspond to the situations commonly encountered in practice. We expect results from the PLS and the OPLS procedures to be quite similar in presence of 9 categories, since in this case polychoric correlations are close to their corresponding Pearson correlations.

500 replications for each instance, each with 250 observations were made.

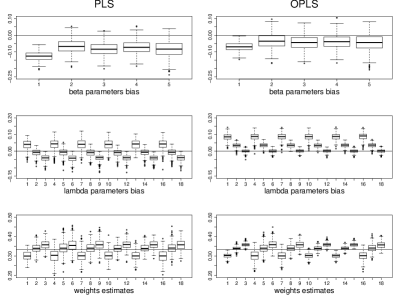

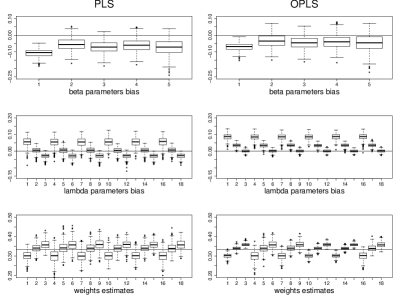

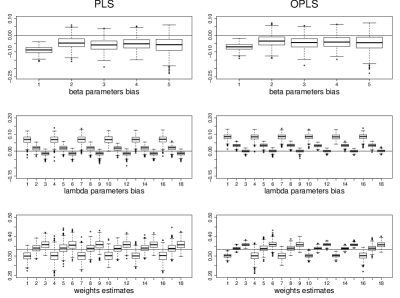

To compare the performance of the two procedures we considered the empirical distribution of the inner model parameter estimate biases, see Tables 3-10.

As expected (see Schneeweiss, 1993) estimates obtained with the traditional PLS algorithm are negatively biased. Only for scales with and 9 categories we can observe about 5% trials with a small or negligible positive bias for Normal distributed latent variables. The bias gets more evident with decreasing number of scale points. The behaviour is common both to Normal and Beta situations. With the OPLS about 10% simulations always present positive bias. Most percentage points of the bias distribution for the OPLS procedure are closer to 0 than with traditional PLS. Averages biases are again closer to 0 for the OPLS algorithm.

Percentage points and average values are very close for the two estimation procedures in case of a 9 point scale.

The ratio between the absolute biases observed in each trial with OPLS and the traditional PLS was considered, to better compare the two procedures. The distribution of the ratios is shown in the third sections of Tables 3-10 giving evidence that over 90% trials have an absolute bias of the OPLS lower than the traditional PLS, when scales are characterized by 4 and 5 points. By comparing the 5% and 95% percentage points for the distributions of ratios of absolute biases in case of the Normal assumption with 4 point scales, we can observe the better behaviour of the OPLS: for parameter we have 5% and 95% absolute ratios 0.0728 and 3.8032. According to the latter value 5% trials have an absolute bias in OPLS estimates larger more than 3.8 times that of traditional PLS. According to the former value 5% trials have an absolute bias of traditional PLS larger more than times than OPLS.

Geometric means have been computed to summarize ratios between absolute biases of OPLS and traditional PLS and in all situations (except for , 9 points, Beta distribution) they are lower than 1. Their values increase with increasing number of scale points and get close to 1 in presence of scales with 9 points and asymmetric Beta distribution of the latent variables.

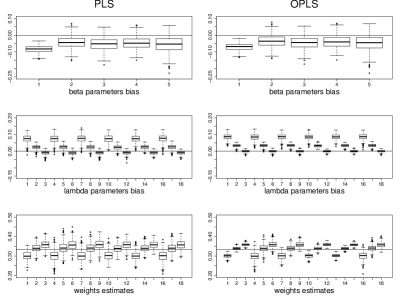

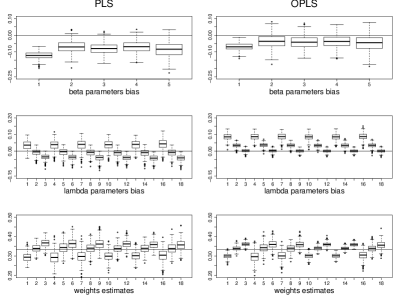

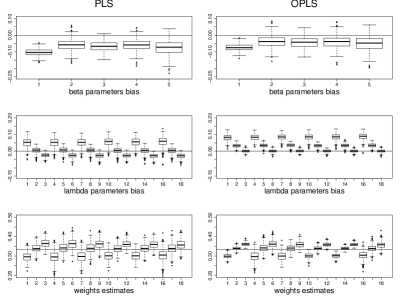

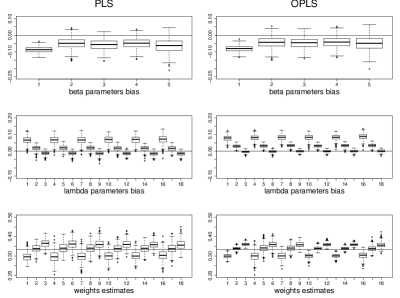

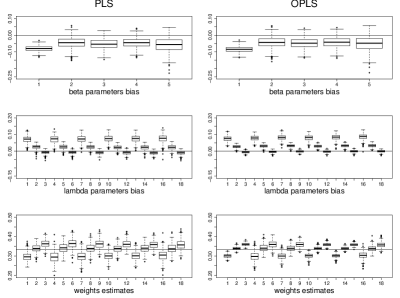

In Section 6.4 we reminded how the reduction in the bias attained by OPLS, pertaining the inner model parameter estimates, can have as a drawback an increase in the bias of the outer model parameter estimates. The bias is evident if we examine Figures 6-13 which report Box & Whiskers plots for the distribution of the bias of the coefficients estimates and from their theoretical values and the distribution of the weights under the Normal and Beta assumptions for scales with 4 and 9 points.

However, as we have already remarked, the role played by outer parameters is less important than that of the inner model parameters: when making decisions based on PLS results the weights are used instead of outer parameters; we remember that PLS define each latent variable as a ’composite’ of its manifest indicators, see (10) and (22), and the weights give information about the strength of the relationship of each ’composite’ across its manifest indicators. According to the Box & Whiskers Plots the estimates of the weights seem to be always characterized by a lower variability (interquartile range) when obtained with the OPLS algorithm.

| 5% | 10% | 25% | 50% | 75% | 90% | 95% | mean | sd | |

| PLS | |||||||||

| -0.166 | -0.158 | -0.144 | -0.125 | -0.107 | -0.094 | -0.087 | -0.126 | 0.025 | |

| -0.128 | -0.118 | -0.095 | -0.067 | -0.039 | -0.019 | -0.004 | -0.068 | 0.039 | |

| -0.147 | -0.131 | -0.110 | -0.084 | -0.056 | -0.033 | -0.021 | -0.083 | 0.038 | |

| -0.131 | -0.119 | -0.098 | -0.072 | -0.046 | -0.023 | -0.010 | -0.072 | 0.038 | |

| -0.164 | -0.149 | -0.115 | -0.083 | -0.050 | -0.022 | -0.006 | -0.084 | 0.049 | |

| OPLS | |||||||||

| -0.111 | -0.103 | -0.087 | -0.070 | -0.052 | -0.039 | -0.027 | -0.070 | 0.025 | |

| -0.101 | -0.090 | -0.065 | -0.036 | -0.004 | 0.019 | 0.035 | -0.035 | 0.042 | |

| -0.111 | -0.095 | -0.072 | -0.044 | -0.014 | 0.009 | 0.023 | -0.044 | 0.042 | |

| -0.103 | -0.091 | -0.067 | -0.039 | -0.011 | 0.016 | 0.031 | -0.039 | 0.042 | |

| -0.138 | -0.111 | -0.077 | -0.044 | -0.010 | 0.020 | 0.036 | -0.046 | 0.052 | |

| Ratio of absolute biases OPLS over PLS | geometric mean | ||||||||

| 0.329 | 0.392 | 0.465 | 0.557 | 0.613 | 0.666 | 0.693 | 0.522 | ||

| 0.073 | 0.166 | 0.376 | 0.594 | 0.755 | 1.090 | 3.803 | 0.531 | ||

| 0.113 | 0.182 | 0.385 | 0.577 | 0.697 | 0.792 | 0.982 | 0.483 | ||

| 0.100 | 0.207 | 0.414 | 0.621 | 0.747 | 0.914 | 2.559 | 0.543 | ||

| 0.112 | 0.244 | 0.436 | 0.606 | 0.736 | 0.911 | 3.437 | 0.575 | ||

| 5% | 10% | 25% | 50% | 75% | 90% | 95% | mean | sd | |

| PLS | |||||||||

| -0.145 | -0.136 | -0.123 | -0.105 | -0.092 | -0.078 | -0.070 | -0.107 | 0.023 | |

| -0.120 | -0.106 | -0.079 | -0.057 | -0.029 | -0.008 | 0.004 | -0.056 | 0.037 | |

| -0.126 | -0.111 | -0.095 | -0.071 | -0.046 | -0.027 | -0.015 | -0.071 | 0.035 | |

| -0.114 | -0.104 | -0.086 | -0.060 | -0.035 | -0.013 | 0.010 | -0.060 | 0.038 | |

| -0.150 | -0.134 | -0.103 | -0.071 | -0.039 | -0.011 | 0.007 | -0.072 | 0.048 | |

| OPLS | |||||||||

| -0.110 | -0.098 | -0.085 | -0.069 | -0.054 | -0.043 | -0.034 | -0.070 | 0.023 | |

| -0.100 | -0.088 | -0.060 | -0.035 | -0.005 | 0.018 | 0.027 | -0.034 | 0.039 | |

| -0.103 | -0.090 | -0.071 | -0.046 | -0.018 | 0.003 | 0.014 | -0.045 | 0.036 | |

| -0.095 | -0.085 | -0.066 | -0.040 | -0.013 | 0.010 | 0.036 | -0.038 | 0.040 | |

| -0.131 | -0.110 | -0.079 | -0.046 | -0.010 | 0.017 | 0.033 | -0.046 | 0.049 | |

| Ratio of absolute biases OPLS over PLS | geometric mean | ||||||||

| 0.459 | 0.511 | 0.590 | 0.651 | 0.704 | 0.751 | 0.772 | 0.629 | ||

| 0.107 | 0.220 | 0.509 | 0.700 | 0.823 | 1.670 | 4.287 | 0.641 | ||

| 0.164 | 0.262 | 0.499 | 0.667 | 0.764 | 0.848 | 0.945 | 0.585 | ||

| 0.147 | 0.270 | 0.531 | 0.704 | 0.815 | 0.925 | 2.136 | 0.628 | ||

| 0.165 | 0.250 | 0.527 | 0.703 | 0.817 | 1.676 | 3.410 | 0.670 | ||

| 5% | 10% | 25% | 50% | 75% | 90% | 95% | mean | sd | |

| PLS | |||||||||

| -0.128 | -0.117 | -0.105 | -0.089 | -0.074 | -0.063 | -0.055 | -0.090 | 0.022 | |

| -0.109 | -0.097 | -0.069 | -0.047 | -0.022 | -0.000 | 0.012 | -0.047 | 0.037 | |

| -0.115 | -0.103 | -0.084 | -0.059 | -0.035 | -0.013 | -0.002 | -0.059 | 0.035 | |

| -0.107 | -0.098 | -0.077 | -0.052 | -0.027 | -0.004 | 0.014 | -0.051 | 0.036 | |

| -0.140 | -0.118 | -0.091 | -0.057 | -0.025 | -0.001 | 0.012 | -0.059 | 0.048 | |

| OPLS | |||||||||

| -0.107 | -0.099 | -0.084 | -0.070 | -0.055 | -0.044 | -0.037 | -0.070 | 0.021 | |

| -0.098 | -0.088 | -0.059 | -0.035 | -0.010 | 0.012 | 0.025 | -0.035 | 0.038 | |

| -0.102 | -0.091 | -0.071 | -0.044 | -0.020 | 0.002 | 0.012 | -0.045 | 0.037 | |

| -0.095 | -0.089 | -0.066 | -0.041 | -0.014 | 0.007 | 0.027 | -0.040 | 0.037 | |

| -0.131 | -0.104 | -0.077 | -0.045 | -0.011 | 0.012 | 0.024 | -0.045 | 0.048 | |

| Ratio of absolute biases OPLS over PLS | geometric mean | ||||||||

| 0.617 | 0.667 | 0.725 | 0.779 | 0.824 | 0.867 | 0.889 | 0.764 | ||

| 0.296 | 0.436 | 0.664 | 0.813 | 0.915 | 1.393 | 2.320 | 0.789 | ||

| 0.277 | 0.443 | 0.657 | 0.794 | 0.877 | 0.959 | 1.635 | 0.733 | ||

| 0.283 | 0.420 | 0.683 | 0.845 | 0.904 | 1.242 | 1.785 | 0.767 | ||

| 0.272 | 0.462 | 0.679 | 0.827 | 0.910 | 1.761 | 3.156 | 0.840 | ||

| 5% | 10% | 25% | 50% | 75% | 90% | 95% | mean | sd | |

| PLS | |||||||||

| -0.119 | -0.112 | -0.098 | -0.082 | -0.069 | -0.057 | -0.050 | -0.084 | 0.021 | |

| -0.104 | -0.092 | -0.066 | -0.044 | -0.018 | 0.001 | 0.015 | -0.043 | 0.036 | |

| -0.113 | -0.104 | -0.079 | -0.052 | -0.027 | -0.009 | 0.005 | -0.054 | 0.037 | |

| -0.106 | -0.095 | -0.072 | -0.048 | -0.023 | -0.001 | 0.016 | -0.047 | 0.037 | |

| -0.133 | -0.117 | -0.087 | -0.053 | -0.021 | 0.003 | 0.015 | -0.056 | 0.046 | |

| OPLS | |||||||||

| -0.106 | -0.099 | -0.085 | -0.068 | -0.056 | -0.044 | -0.038 | -0.070 | 0.021 | |

| -0.099 | -0.085 | -0.060 | -0.036 | -0.011 | 0.009 | 0.024 | -0.036 | 0.037 | |

| -0.105 | -0.096 | -0.071 | -0.044 | -0.019 | 0.000 | 0.015 | -0.045 | 0.037 | |

| -0.100 | -0.088 | -0.066 | -0.040 | -0.013 | 0.008 | 0.025 | -0.040 | 0.038 | |

| -0.126 | -0.108 | -0.077 | -0.045 | -0.013 | 0.011 | 0.023 | -0.048 | 0.047 | |

| Ratio of absolute biases OPLS over PLS | geometric mean | ||||||||

| 0.688 | 0.739 | 0.789 | 0.844 | 0.894 | 0.936 | 0.956 | 0.832 | ||

| 0.316 | 0.508 | 0.754 | 0.884 | 0.971 | 1.205 | 1.672 | 0.837 | ||

| 0.293 | 0.539 | 0.731 | 0.867 | 0.939 | 1.025 | 1.439 | 0.809 | ||

| 0.305 | 0.491 | 0.753 | 0.889 | 0.955 | 1.149 | 1.560 | 0.833 | ||

| 0.370 | 0.535 | 0.784 | 0.884 | 0.957 | 1.410 | 2.006 | 0.867 | ||

| 5% | 10% | 25% | 50% | 75% | 90% | 95% | mean | sd | |

| PLS | |||||||||

| -0.160 | -0.151 | -0.135 | -0.122 | -0.107 | -0.094 | -0.088 | -0.122 | 0.022 | |

| -0.130 | -0.116 | -0.094 | -0.071 | -0.045 | -0.027 | -0.012 | -0.070 | 0.036 | |

| -0.136 | -0.125 | -0.103 | -0.080 | -0.059 | -0.038 | -0.025 | -0.081 | 0.034 | |

| -0.128 | -0.116 | -0.093 | -0.069 | -0.046 | -0.025 | -0.015 | -0.070 | 0.035 | |

| -0.152 | -0.139 | -0.117 | -0.084 | -0.055 | -0.030 | -0.013 | -0.086 | 0.044 | |

| OPLS | |||||||||

| -0.106 | -0.097 | -0.083 | -0.070 | -0.054 | -0.043 | -0.035 | -0.070 | 0.021 | |

| -0.102 | -0.089 | -0.064 | -0.037 | -0.008 | 0.011 | 0.023 | -0.038 | 0.040 | |

| -0.103 | -0.091 | -0.067 | -0.042 | -0.016 | 0.006 | 0.023 | -0.042 | 0.038 | |

| -0.099 | -0.088 | -0.062 | -0.037 | -0.012 | 0.015 | 0.026 | -0.038 | 0.038 | |

| -0.118 | -0.103 | -0.079 | -0.045 | -0.014 | 0.011 | 0.028 | -0.047 | 0.046 | |

| Ratio of absolute biases OPLS over PLS | geometric mean | ||||||||

| 0.371 | 0.426 | 0.501 | 0.575 | 0.629 | 0.681 | 0.704 | 0.549 | ||

| 0.075 | 0.142 | 0.357 | 0.598 | 0.738 | 0.850 | 2.108 | 0.488 | ||

| 0.101 | 0.189 | 0.384 | 0.559 | 0.692 | 0.781 | 0.888 | 0.454 | ||

| 0.127 | 0.213 | 0.415 | 0.598 | 0.741 | 0.842 | 1.621 | 0.522 | ||

| 0.099 | 0.226 | 0.397 | 0.590 | 0.720 | 0.828 | 2.197 | 0.503 | ||

| 5% | 10% | 25% | 50% | 75% | 90% | 95% | mean | sd | |

| PLS | |||||||||

| -0.135 | -0.126 | -0.116 | -0.104 | -0.089 | -0.079 | -0.072 | -0.103 | 0.019 | |

| -0.114 | -0.099 | -0.079 | -0.058 | -0.037 | -0.014 | 0.001 | -0.057 | 0.034 | |

| -0.118 | -0.107 | -0.088 | -0.067 | -0.047 | -0.028 | -0.017 | -0.067 | 0.031 | |

| -0.115 | -0.102 | -0.080 | -0.059 | -0.037 | -0.016 | 0.001 | -0.059 | 0.034 | |

| -0.145 | -0.131 | -0.103 | -0.072 | -0.045 | -0.013 | 0.000 | -0.073 | 0.044 | |

| OPLS | |||||||||

| -0.106 | -0.097 | -0.087 | -0.075 | -0.060 | -0.047 | -0.041 | -0.074 | 0.020 | |

| -0.099 | -0.084 | -0.061 | -0.038 | -0.015 | 0.010 | 0.025 | -0.038 | 0.037 | |

| -0.100 | -0.087 | -0.066 | -0.042 | -0.021 | -0.001 | 0.010 | -0.043 | 0.033 | |

| -0.099 | -0.086 | -0.065 | -0.038 | -0.017 | 0.007 | 0.022 | -0.039 | 0.037 | |

| -0.123 | -0.108 | -0.079 | -0.047 | -0.020 | 0.014 | 0.027 | -0.048 | 0.046 | |

| Ratio of absolute biases OPLS over PLS | geometric mean | ||||||||

| 0.537 | 0.581 | 0.653 | 0.722 | 0.780 | 0.827 | 0.857 | 0.704 | ||

| 0.199 | 0.325 | 0.558 | 0.724 | 0.851 | 0.987 | 2.509 | 0.686 | ||

| 0.146 | 0.259 | 0.502 | 0.664 | 0.789 | 0.856 | 0.926 | 0.564 | ||

| 0.236 | 0.353 | 0.546 | 0.719 | 0.832 | 0.962 | 2.579 | 0.687 | ||

| 0.221 | 0.367 | 0.560 | 0.720 | 0.824 | 1.124 | 3.351 | 0.706 | ||

| 5% | 10% | 25% | 50% | 75% | 90% | 95% | mean | sd | |

| PLS | |||||||||

| -0.117 | -0.111 | -0.099 | -0.087 | -0.075 | -0.066 | -0.061 | -0.088 | 0.017 | |

| -0.101 | -0.086 | -0.069 | -0.049 | -0.027 | -0.006 | 0.003 | -0.049 | 0.033 | |

| -0.107 | -0.095 | -0.080 | -0.056 | -0.035 | -0.019 | -0.009 | -0.057 | 0.031 | |

| -0.104 | -0.094 | -0.070 | -0.048 | -0.029 | -0.008 | 0.000 | -0.050 | 0.032 | |

| -0.135 | -0.122 | -0.091 | -0.063 | -0.035 | -0.005 | 0.010 | -0.063 | 0.044 | |

| OPLS | |||||||||

| -0.114 | -0.107 | -0.094 | -0.080 | -0.069 | -0.059 | -0.053 | -0.082 | 0.019 | |

| -0.099 | -0.082 | -0.065 | -0.043 | -0.021 | 0.003 | 0.013 | -0.042 | 0.034 | |

| -0.100 | -0.087 | -0.069 | -0.045 | -0.024 | -0.005 | 0.004 | -0.047 | 0.032 | |

| -0.098 | -0.087 | -0.063 | -0.041 | -0.020 | 0.000 | 0.010 | -0.042 | 0.033 | |

| -0.122 | -0.109 | -0.078 | -0.049 | -0.019 | 0.009 | 0.021 | -0.050 | 0.044 | |

| Ratio of absolute biases OPLS over PLS | geometric mean | ||||||||

| 0.781 | 0.816 | 0.868 | 0.932 | 0.997 | 1.048 | 1.098 | 0.926 | ||

| 0.415 | 0.585 | 0.792 | 0.908 | 1.018 | 1.186 | 1.778 | 0.876 | ||

| 0.293 | 0.463 | 0.700 | 0.831 | 0.919 | 1.013 | 1.154 | 0.751 | ||

| 0.351 | 0.456 | 0.729 | 0.872 | 0.971 | 1.125 | 2.057 | 0.835 | ||

| 0.353 | 0.502 | 0.701 | 0.826 | 0.901 | 1.078 | 2.075 | 0.817 | ||

| 5% | 10% | 25% | 50% | 75% | 90% | 95% | mean | sd | |

| PLS | |||||||||

| -0.107 | -0.101 | -0.091 | -0.080 | -0.070 | -0.059 | -0.053 | -0.080 | 0.016 | |

| -0.098 | -0.084 | -0.065 | -0.045 | -0.024 | -0.002 | 0.008 | -0.045 | 0.033 | |

| -0.102 | -0.092 | -0.073 | -0.054 | -0.031 | -0.011 | -0.004 | -0.053 | 0.030 | |

| -0.097 | -0.087 | -0.065 | -0.045 | -0.025 | -0.004 | 0.008 | -0.045 | 0.032 | |

| -0.127 | -0.116 | -0.086 | -0.056 | -0.028 | -0.004 | 0.014 | -0.058 | 0.043 | |

| OPLS | |||||||||

| -0.115 | -0.110 | -0.097 | -0.085 | -0.073 | -0.061 | -0.056 | -0.085 | 0.018 | |

| -0.095 | -0.086 | -0.064 | -0.044 | -0.021 | 0.001 | 0.014 | -0.043 | 0.034 | |

| -0.098 | -0.087 | -0.069 | -0.048 | -0.027 | -0.006 | 0.004 | -0.048 | 0.031 | |

| -0.097 | -0.085 | -0.064 | -0.042 | -0.021 | -0.001 | 0.010 | -0.042 | 0.032 | |

| -0.121 | -0.108 | -0.079 | -0.048 | -0.019 | 0.004 | 0.019 | -0.050 | 0.043 | |

| Ratio of absolute biases OPLS over PLS | geometric mean | ||||||||

| 0.885 | 0.926 | 0.984 | 1.061 | 1.132 | 1.205 | 1.244 | 1.056 | ||

| 0.561 | 0.699 | 0.856 | 0.986 | 1.097 | 1.332 | 1.709 | 0.973 | ||

| 0.470 | 0.658 | 0.823 | 0.922 | 1.028 | 1.202 | 1.763 | 0.914 | ||

| 0.467 | 0.661 | 0.829 | 0.945 | 1.070 | 1.286 | 1.747 | 0.918 | ||

| 0.381 | 0.569 | 0.778 | 0.884 | 0.949 | 1.084 | 1.463 | 0.833 | ||

8 Conclusions and Final Remarks

A PLS algorithm dealing with variables on ordinal scales has been presented. The algorithm, OPLS, is based on the use of the polychoric correlation matrix and seems to perform better than the traditional PLS algorithm in presence of ordinal scales with a small number of point alternatives, by reducing the bias of the inner model parameter estimates.

A basic feature of PLS is the so-called soft modelling, requiring no distributional assumptions on the variables appearing in the structural equation model. With the OPLS algorithm the continuous variables underlying the categorical manifest indicators are considered multinormally distributed. This can appear a strong assumption but, as Bartolomew (1996) observes, every distribution can be obtained as a transformation of the Normal one, which can suit most situations: for instance, in presence of a manifest variable with a negative asymmetric distribution, points on the right side of a scale will have the highest frequency and the underlying latent variable should also be of an asymmetric type, but transformation (8) will work anyway assigning larger intervals to the classes defined by the thresholds to which the highest points in the scale correspond.

Furthermore polychoric correlations are expected to overestimate real correlations when scales present some kind of asymmetry, but this can be regarded as a positive feature for the OPLS algorithm. This may represent a correction of the negative bias characterizing PLS algorithms with regard to the estimates of the inner model parameters (which are in some way linked to correlations across manifest variables).

The gain in the bias reduction is less evident for scales with an higher number of categories, for which polychoric correlation values are closer to Pearson’s correlations. In these cases ordinal scales can be considered as they were of the interval type, possibly according to the so-called pragmatic approach to measurement (Hand, 2009).

Increasing the number of the points of the scale can help the performance of the traditional PLS algorithm when the scale is interpreted as continuous, but it often happens that in presence of asymmetric distributions many points of the scale are characterized by a very low response frequency, since the number of points that respondents do effectively choose may be quite restricted. Thus the administered scale corresponds to a scale with a lower number of points and OPLS can anyway be useful in these situations.

Another important feature of the PLS predictive approach is the direct estimation of latent scores. With the OPLS algorithm we can estimate some thresholds for the latent variables, from which a ’category’ indication for the ordinal latent variable follows according to one of the 3 estimation methods presented in Section 6.3.

Simulations have been carried out to assess the properties of the algorithm also in presence of asymmetric distributions for latent variables and the bias characterizing the inner model parameter estimates obtained with the traditional PLS algorithm was reduced.

References

- Bartolomew (1996) Bartolomew, D. J. (1996). The Statistical Approach to Social Measurement. Academic Press.

- Bayol et al. (2000) Bayol, M. P., de la Foye, A., Tellier, C., & Tenenhaus, M. (2000). Use of the pls path modelling to estimate the european customer satisfaction index (ecsi) model. Statistica Applicata, 12(3), 361–375.

- Bollen (1989) Bollen, K. A. (1989). Structural Equations with Latent Variables. New York: John Wiley.

- Bollen & Maydeu-Olivares (2007) Bollen, K. A., & Maydeu-Olivares, A. (2007). A polychoric instrumental variable (piv) estimator for structural equaltion models with categorical variables. Psychometrika, 72, 309–326.

- Chin (1998) Chin, W. W. (1998). The partial least squares approach for structural equation modeling. In G. Marcoulides (Ed.), Modern methods for business research (pp. 295–336). London: Lawrence Erlbaum Associates.

- Coenders et al. (1997) Coenders, G., Satorra, A., & Saris, W. E. (1997). Alternative approaches to structural modeling of ordinal data: A monte carlo study. Structural Equation Modeling, 4(4), 261–282.

- Diamantopoulos et al. (2008) Diamantopoulos, A., Riefler, P., & Roth, K. P. (2008). Advancing formative measurement models. Journal of Business Research, 61, 1203–1218.

- Drasgow (1986) Drasgow, F. (1986). Polychoric and polyserial correlations. In S. Kotz, & N. Johnson (Eds.), The Encyclopedia of Statistics (pp. 68–74). John Wiley volume 7.

- Esposito Vinzi et al. (2010) Esposito Vinzi, V., Trinchera, L., & Amato, S. (2010). Pls path modeling: From foundations to recent developments and open issues for model assessment and improvement. In V. Esposito Vinzi, W. W. Chin, J. Henseler, & H. Wang (Eds.), Handbook of Partial Least Squares (pp. 47–82). Springer-Verlag.

- Faliva (1992) Faliva, M. (1992). Recursiveness vs. interdependence in econometric models: a comprehensive analysis for the linear case. Journal of the Italian Statistical Society, 1(3), 335–357.

- Fornell (1996) Fornell, C. (1996). A national customer satisfaction barometer: The swedish experience. Journal of Marketing, 56(1), 6–21.

- Fornell & Cha (1994) Fornell, C., & Cha, J. (1994). Partial least squares. In R. Bagozzi (Ed.), Advanced methods of marketing research (pp. 52–78). Blackwell.

- Fornell et al. (1996) Fornell, C., Johnson, M. D., Anderson, E. W., Cha, J., & Everitt Bryant, B. (1996). The american customer satisfaction index: Nature, purpose, and findings. Journal of Marketing, 60(4), 7–18.

- Fox (2010) Fox, J. (2010). polycor: Polychoric and Polyserial Correlations. R package version 0.7-8.

- Gadermann et al. (2012) Gadermann, A. M., Guhn, M., & Zumbo, B. D. (2012). Estimating ordinal reliability for likert-type and ordinal item response data: A conceptual, empirical, and practical guide. Practical Assessment, Research & Evaluation, 17(3), 1–13.

- Green & Yang (2009) Green, S. B., & Yang, Y. (2009). Reliability of summed item scores using structural equation modeling: an alternative to coefficient alpha. Psychometrika, 74, 155–167.

- Hand (2009) Hand, D. J. (2009). Measurement Theory and Practice: The World Through Quantification. New York: John Wiley.

- Hand (2012) Hand, D. J. (2012). Foreword. In R. S. Kenett, & S. Salini (Eds.), Modern Analysis of Customer Surveys: with applications using R (pp. xvii–xviii). John Wiley.

- Hayashi (1952) Hayashi, C. (1952). On the prediction of phenomena from qualitative data and the quantification of qualitative data from the mathematicostatistical point of view. Annals of the Institute of Statistical Mathematics, 3, 69–98.

- Jakobowicz & Derquenne (2007) Jakobowicz, E., & Derquenne, C. (2007). A modified pls path modeling algorithm handling reflective categorical variables and a new model building strategy. Computational Statistics & Data Analysis, 51, 3666–3678.

- Johnson & Gustafsson (2000) Johnson, M. D., & Gustafsson, A. (2000). Improving Customer Satisfaction, Loyalty and Profit: An Integrated Measurement and Management System. Jossey Bass.

- Johnson et al. (2001) Johnson, M. D., Gustafsson, A., Andreassen, T. W., Lervik, L., & Cha, J. (2001). The evolution and future of national customer satisfaction index models. Journal of Economic Psychology, 22, 217–245.

- Jöreskog (2005) Jöreskog, K. G. (2005). Structural Equation Modeling with Ordinal Variables using LISREL. Scientific Software International Inc. http://www.ssicentral.com/lisrel/techdocs/ordinal.pdf.

- Lauro et al. (2011) Lauro, C. N., Nappo, D., Grassia, M. G., & Miele, R. (2011). Method of quantification for qualitative variables and their use in the structural equations models. In B. Fichet, D. Piccolo, R. Verde, & M. Vichi (Eds.), Classification and Multivariate Analysis for Complex Data Structures. Studies in Classification, Data Analysis, and Knowledge Organization (pp. 325–333). Springer.

- Lohmöller (1989) Lohmöller, J. B. (1989). Latent Variable Path Modeling with Partial Least Squares. Physica-Verlag.

- Mair & de Leeuw (2010) Mair, P., & de Leeuw, J. (2010). A general framework for multivariate analysis with optimal scaling: The r package aspect. Journal of Statistical Software, 32, 1–23.

- Muthén (1984) Muthén, B. O. (1984). A general structural equation model with dichotomous, ordered, categorical, and continuous latent variable indicators. Psychometrika, 49, 115–132.

- Nappo (2009) Nappo, D. (2009). SEM with ordinal manifest variables. An Alternating Least Squares approach. Ph.D. thesis Università degli Studi di Napoli Federico II.

- Olsson (1979) Olsson, U. (1979). Maximum likelihood estimation of the polychoric correlation coefficient. Psychometrika, 44, 443–460.

- R Core Team (2012) R Core Team (2012). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing Vienna, Austria. ISBN 3-900051-07-0.

- Raykov (2002) Raykov, T. (2002). Analytic estimation of standard error and confidence interval for scale reliability. Multivariate Behavioral Research, 37(1), 89–103.

- Revelle (2012) Revelle, W. (2012). psych: Procedures for Psychological, Psychometric, and Personality Research. Northwestern University Evanston, Illinois. R package version 1.2.8.

- Rigdon (2012) Rigdon, E. E. (2012). Rethinking partial least squares path modeling: In praise of simple methods. Long Range Planning, 45, 341–358.

- Russolillo & Lauro (2011) Russolillo, G., & Lauro, C. N. (2011). A proposal for handling categorical predictors in pls regression framework. In B. Fichet, D. Piccolo, R. Verde, & M. Vichi (Eds.), Classification and Multivariate Analysis for Complex Data Structures. Studies in Classification, Data Analysis, and Knowledge Organization (pp. 343–350). Springer.

- Sanchez & Trinchera (2012) Sanchez, G., & Trinchera, L. (2012). plspm: Partial Least Squares Data Analysis Methods. R package version 0.2-2.

- Schneeweiss (1993) Schneeweiss, H. (1993). Consistency at large in models with latent variables. In K. Haagen, D. J. Bartholomew, & M. Deistler (Eds.), Statistical Modelling and Latent Variables (pp. 299–320). Elsevier.

- Stevens (1946) Stevens, S. S. (1946). On the theory of scales of measurement. Science, 103, 677–680.

- Tenenhaus et al. (2005) Tenenhaus, M., Esposito Vinzi, V., Chatelin, Y.-M., & Lauro, C. (2005). Pls path modeling. Computational Statistics & Data Analysis, 48, 159–205.

- Thurstone (1959) Thurstone, L. L. (1959). The measurement of Values. Chicago: University of Chicago Press.

- Wold (1985) Wold, H. (1985). Partial least squares. In S. Kotz, & N. L. Johnson (Eds.), Encyclopedia of Statistical Sciences (pp. 581–591). Wiley volume 6.

- Zumbo et al. (2007) Zumbo, B. D., Gadermann, A. M., & Zeisser, C. (2007). Ordinal versions of coefficients alpha and theta for likert rating scales. Journal of Modern Applied Statistical Methods, 6(1), 21–29.

Finito di stampare nel mese di Dicembre 2012

presso la Redazione e composizione stampati

Università Cattolica del Sacro Cuore

La Redazione ottempera agli obblighi previsti

dalla L. 106/2004 e dal DPR 252/2006