Non stationary multifractality in stock returns

Abstract

We perform an extensive empirical analysis of scaling properties of equity returns, suggesting that financial data show time varying multifractal properties. This is obtained by comparing empirical observations of the weighted generalised Hurst exponent (wGHE) with time series simulated via Multifractal Random Walk (MRW) by Bacry et al. [E.Bacry, J.Delour and J.Muzy, Phys.Rev.E 64 026103, 2001]. While dynamical wGHE computed on synthetic MRW series is consistent with a scenario where multifractality is constant over time, fluctuations in the dynamical wGHE observed in empirical data are not in agreement with a MRW with constant intermittency parameter. We test these hypotheses of constant multifractality considering different specifications of MRW model with fatter tails: in all cases considered, although the thickness of the tails accounts for most of anomalous fluctuations of multifractality, still cannot fully explain the observed fluctuations.

keywords:

Multifractality, Generalized Hurst exponent, Multifractal models.1 Introduction

The concept of multifractality in the context of finance has received much attention in the econophysics literature [1] over the last two decades. Many empirical studies have investigated financial data scaling behaviour [2, 3, 4, 5, 6, 7, 8, 9, 10] and several models have been proposed to account for the observed multifractal features [11, 12, 13, 14, 15, 16, 17, 18, 19].

Multifractal behaviour has become a downright stylised fact of financial market data [20, 21], being observed across several classes of assets: from daily stock prices to foreign exchange rates and composite indices [6, 3, 22, 23, 24].

Multifractality is also particularly appealing for modelling financial markets as it offers a simple behavioural interpretation: looking at the volatility at different time scales is a very natural way to assess the impact of heterogeneous agents in the market and therefore any measure of scaling behaviour can convey information about the efficiency of a given market [21]. In this regard some authors have suggested, and confirmed through extensive empirical studies, that scaling exponents can be representative of the stage of development of a market [22, 3]. The same works have convincingly shown that, through a hierarchy of scaling exponents, it is possible to classify markets according to their degree of development with emerging markets exhibiting scaling exponents significantly larger than those observed in developed markets.

Let us recall that a process with stationary increments is called multifractal if the following scaling law is observed

| (1) |

where is a constant and is a non-linear function of , called the scaling function. The departure of from linearity is what distinguishes multifractal processes from uni-scaling processes and the degree of non-linearity of the scaling function is accounted for by the intermittency coefficient, defined as [11]. Note that the last definition requires the scaling function to have a second derivative well defined in in order for the intermittency coefficient to be defined. (In practice, it is extremely difficult to estimate this coefficient from empirical measures.) For multifractal processes, the scaling in equation (1) holds for small , with , where is some larger scale called the integral scale [11]. This means that if the integral scale of the process is not large enough compared to the resolution of the increments, although the scaling may in principle hold, the definition doesn’t hold any longer.

In order to estimate the scaling function from real data one resorts to the scaling of the empirical moments

| (2) |

where we denote the log-return at time and scale , with the asset price at time , the empirical scaling function and the length of the time series. It is well known [25, 26] that the empirically estimated is significant only for small values of and one therefore needs to be careful in interpreting the scaling beyond a certain . When the scaling (2) is observed, one defines the generalised Hurst exponent (GHE) via

| (3) |

The exponent is non-linear in for multi-scaling processes, whereas it reduces to a constant if the process is uni-scaling.

The time evolution of the scaling function, measured via the GHE, can be useful to track time varying properties of the market. For this reason has also been studied dynamically via the time dependent (or local) Hurst exponent [27, 28, 5]. In a recent publication [29] the authors have observed large fluctuations in multifractality measured via the generalised Hurst exponent in empirical daily data across different stock sectors. Specifically, the authors considered as a measure of multifractal behaviour the quantity

| (4) |

where is the weighted generalized Hurst exponent (wGHE) [29]. The weighting procedure incrementally damps effects from past return fluctuations. The dynamical evolution of (which we shall label ) is useful to track changes in multifractality occurring over time.

When facing the task of ascertaining the nature of dynamical fluctuations in these quantities, the subtle issue is being able to distinguish between spurious statistical fluctuations, which are due to the finiteness of the sample and noise, and true structural changes in the underlying multifractal process. In this paper we study the problem of validating dynamical fluctuations of the scaling functions, performing an empirical analysis of stock returns and comparing their properties with those of synthetic multifractal series.

Among all existing models we focus on the Multifractal Random Walk (MRW) introduced by Bacry et al. [11] because of its parsimonious formulation and its success in the econophysics literature.

This paper is organised as follows: in Section 2 we review the main properties of the MRW and establish the connection with the generalised Hurst exponent. In Section 3, after introducing the statistical testing procedure, we report the main findings on the varying multifractality of empirical stock returns data. A summary and conclusive remarks are drawn in Section 4.

2 Generalities on Multifractal random walk

The multifractal random walk (MRW) [11] can be viewed as a stochastic volatility model constructed by taking the limit for of the process

| (5) |

with a Gaussian white noise with variance and a stochastic volatility uncorrelated with . By taking as a stationary Gaussian process, we have log-normal volatility components. What distinguishes the limit of from a Brownian motion is the choice of the auto covariance structure of the process , which is chosen, according to cascade-like processes [30], as

| (6) |

The logarithmic decay with lag of the auto covariance creates long memory in the process. This specification implicitly defines the integral scale and the intermittency coefficient . In order for the process to have finite variance in the limit , one should impose [11]. can be shown to obey self similarity exactly, i.e. for a time scale contraction ()

| (7) |

with a Gaussian random variable of variance [31]. From equation (7) one can show that [32]

| (8) |

with a q-dependent factor and a non linear function of , i.e. the process is multi-scaling. It should be understood that the scaling (8) is exact only in the continuous time limit . Nonetheless for one can recover good approximations of the scaling even when considering the discretized version .

The main appeal of this model for describing stock returns evolution lies in its ability to reproduce faithfully the most common stylised facts of financial markets: the hyperbolic decay of the volatility auto covariance function (6) as well as the heavy tails of the process increments. Indeed, as shown in [31], the probability of observing increments larger than a certain value decays as a power law for large :

| (9) |

The parameter controls therefore also the thickness of the tails of the returns distribution. The stationarity and the causal structure of this model make it also preferable to other multifractal models [33]. One of the most important features though, is that the multi-fractal spectrum of this model can be computed exactly to be [11]

| (10) |

The scaling function is therefore a parabola whose constant concavity only depends on .

Let us here start to look at the theoretical relation between the intermittency coefficient and the GHE that can be established from the identity . Since the scaling exponents are computed from the scaling of the empirical moments, one has for the log-normal MRW that is bounded from above by [25]

| (11) |

Hence and must be chosen jointly in such a way that the last inequality holds. As shown in Section 3, typical values of obtained for financial data analysed in this study very rarely exceed the value of , which is well within the bound of equation (11). By considering the scaling relation for the MRW (using equation (10)) reads

| (12) |

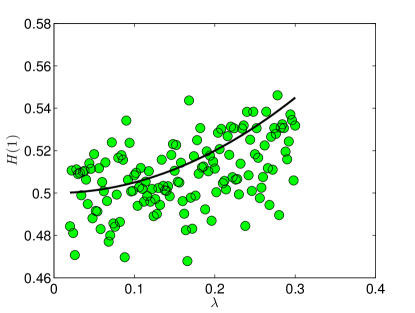

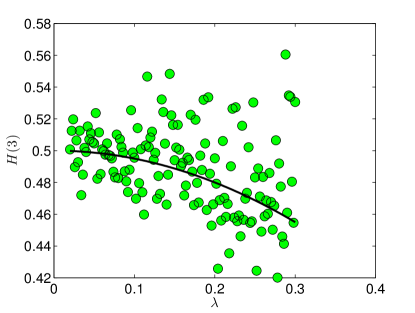

Values of the expressions (12) for different ’s are reported in Table 1 for . We have performed the following statistical study in order to compare theoretical predictions with GHE’s computed on synthetic time series: for a given value of , we have simulated MRW series and computed the corresponding GHE’s for every synthetic series; then, assuming these GHE’s are i.i.d., which is quite reasonable since every MRW simulation is independent from the others, we have obtained a sample distribution for the GHE’s. From this distribution we have computed the -quantiles which give the range of fluctuation of the GHE beyond which any observation can be deemed anomalous. We have performed this study for , after having checked that the scaling doesn’t hold for larger ’s. Results of this analysis for and are reported in Table 2. By comparing these values with those expected from the MRW model in Table 1 we can conclude that all values computed via the equations given in (12) are compatible with the statistical confidence intervals computed on the synthetic time series. In Figure 1 we plot the scaling exponents and computed on synthetic MRW time series with intermittency together with the theoretical relations (12) (black solid lines). The measured scaling exponents are found to be fluctuating around the theoretical relations. Although in this figure we show only the cases , we have also verified that the case is consistent with the expected behaviour .

| H(1) | 0.52 | 0.53 | 0.54 |

| H(2) | 0.50 | 0.50 | 0.50 |

| H(3) | 0.48 | 0.47 | 0.45 |

| H(1) | H(2) | H(3) | ||

|---|---|---|---|---|

| T=1250 | ||||

| T=2500 | ||||

| T=1250 | ||||

| T=2500 | ||||

| T=1250 | ||||

| T=2500 | ||||

It has been shown that modifications of the log-normal model, where residuals are Gaussian, can account better for the fat tails observed in empirical data [25]. One may first consider residuals to be Student t distributed, that is (we drop the subscript for readability)

| (13) |

where is the number of degrees of freedom, is the Euler gamma function and the parameter is related to the variance via [20]. The Student t distribution is known to better fit stock returns tails, if one considers or [20]. In order to let the model have fatter tails one can also act on the unconditional distribution of the ; in [25] indeed, it was pointed out that a cascade model where follows a gamma law can account for empirical observations better than a normal law. The pdf of is given in this case by (again the subscript is dropped)

| (14) |

where and are respectively shape and scale parameters. We will use these two modifications of the log-normal MRW in Sections 3.3 and 3.4.

3 Analysis of empirical data: time-varying multifractality

3.1 Statistical testing procedure

The hypothesis we want to test in this paper is whether stock returns exhibit multifractal properties consistent with a multifractal model whose intermittency coefficient is constant. First of all one needs to check that the data analysed show indeed multifractal properties, a feature which is encoded in the concavity of the estimated scaling function . Once the scaling has been checked we have performed the following statistical testing procedure: after having estimated the MRW parameters from the empirical data we simulated 1000 MRW synthetic series of length with the parameters obtained from the empirical time series (details in Section 3.2). On each of these synthetic series we have computed the multifractality proxy

| (15) |

via the weighted generalised Hurst exponent method [34] with damping coefficient equal to days, chosen in agreement with previous analysis carried out in [29, 35]. The scaling exponents and have been computed as average of several fits of equation (2) with the scale , with varied between and . Computing the scaling exponents for each of the simulated series we have obtained a distribution of the measured ’s. We have then computed dynamically on days rolling windows, on the empirical time series and compared its fluctuations in time with the extreme quantiles of the distributions obtained from synthetic series. We have then looked at the percentage of fluctuations falling outside of the confidence intervals provided by the extreme quantiles. A high quantile-exceedance rate of the empirical would suggest that the fluctuation in multifractality envisaged by the model are smaller than those observed on empirical data. If this is the case, these findings would suggest that a time-varying intermittency coefficient may be responsible for this feature observed in financial time series.

3.2 Empirical analysis

The statistical test described in Section 3.1 has been performed on a set of daily stock prices quoted in the NYSE in the period ranging from 01-01-1995 to 22-10-2012. The data were provided by Bloomberg. We have first of all verified that the scaling functions of the data are indeed not linear in . As an example, we plot in Figure 2 the scaling function of the daily stock returns of Microsoft Corp compared to that of a fractional Brownian motion with Hurst parameter .111The choice of is arbitrary, as the linear scaling is expected for all . This scaling has been checked to hold for the whole set of stocks analysed.

The parameters of the MRW can be extracted from the empirical data through the behaviour of the log-volatility auto covariance function. By identifying empirical returns with the increments of the MRW, using equation (5) one can write

| (16) |

It has been shown [4] that for financial time series, the function

| (17) |

exhibits a slow decay with the lag . By putting together the last two equations we see that is proportional to the log-volatility auto covariance function plus a term uncorrelated in the lag , i.e.

| (18) |

The intermittency coefficient and the integral scale can therefore be estimated from linear fits of equation (18) in log-linear scale. As already established in previous studies [32], the estimation of through this method yields much more reliable results than an estimation based on the variogram of the as a function of the scale (see [32] for details and comparison of the two methods). In the whole procedure we fix the return scale at day. These simulations of MRW synthetic series have been performed using a Fast Fourier Transform of the auto covariance function (6).

| T (days) | Quantiles | Exceedances percentage | |||

| Boeing Corp | 0.1228 | 1260 | 1.0651 | 8 % | |

| Microsoft Corp | 0.1342 | 739 | 0.021 | 33 % | |

| PNC Financials | 0.1418 | 28201 | 0.025 | 7 % | |

| Sara Lee Corp | 0.1335 | 3746 | 0.019 | 31.5% | |

| Rowan Cos INC | 0.2046 | 1080 | 0.7992 | 11.4% | |

| IBM Corp | 0.2363 | 816 | 1.7811 | 14% | |

| Wells Fargo | 0.3010 | 631 | 0.5923 | 15% | |

| American Express | 0.1340 | 1520 | 0.8356 | 29% | |

| General Motors Corp | 0.1727 | 440 | 1.0291 | 41% | |

| Citigroup | 0.2196 | 568 | 6.4585 | 39% | |

| JPMorgan Chase | 0.2950 | 534 | 0.9792 | 27 % | |

| Dominion Resources INC | 0.1738 | 754 | 0.013 | 10 % | |

| Morgan Stanley | 0.2528 | 538 | 1.1185 | 14 % |

We have estimated the MRW parameters for each empirical time series. Then, for each set of parameter we have simulated 1000 MRW synthetic series of 1250 time steps and on each series computed . The distribution of these for each set of parameters is used to estimate the -quantiles. Values of the parameters obtained for different stocks together with the corresponding quantiles obtained from the distributions of the ’s obtained from the simulated MRW series are reported in Table 3. In Table 3 we also report the percentage of empirical computed on rolling windows of length exceeding the quantiles, defined as

| (19) |

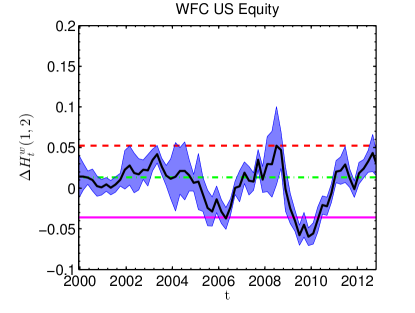

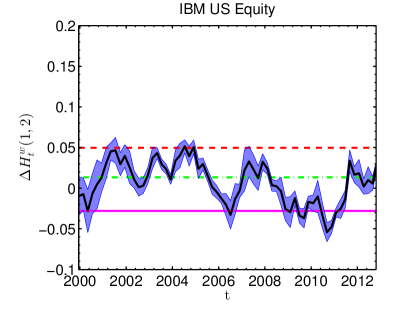

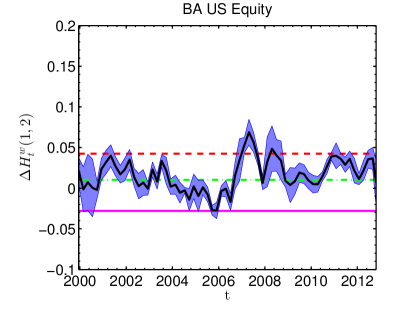

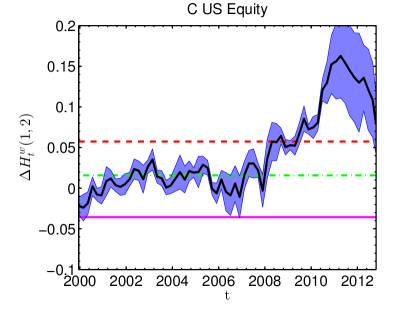

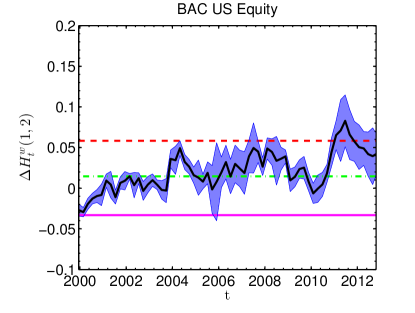

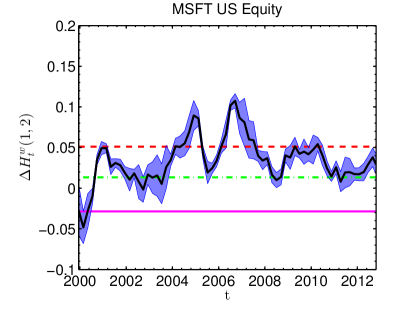

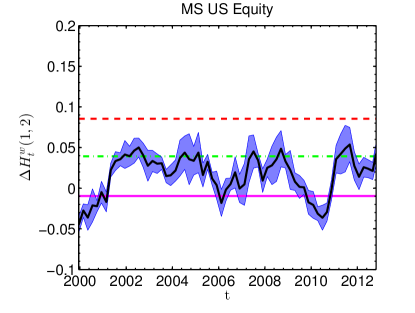

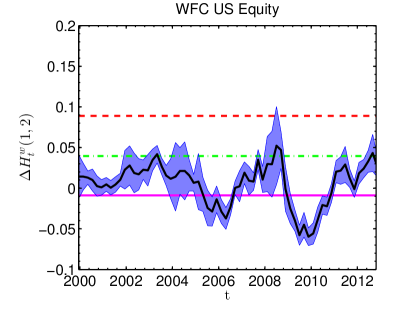

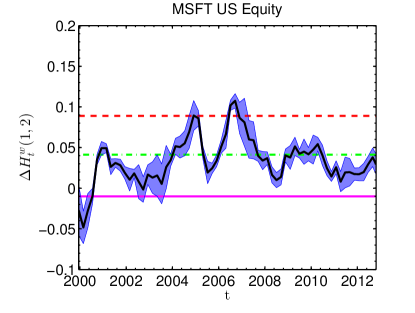

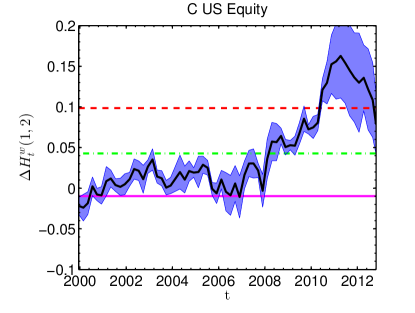

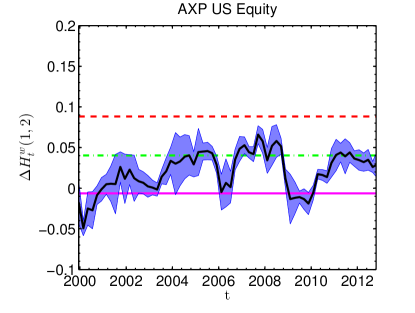

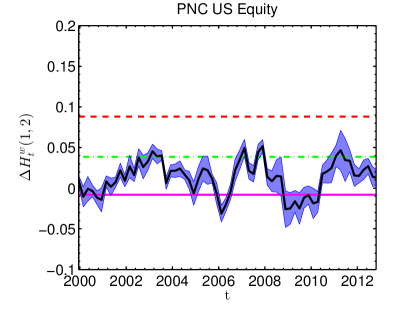

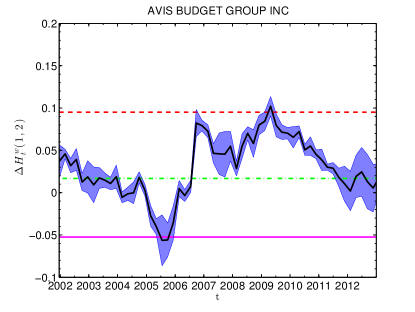

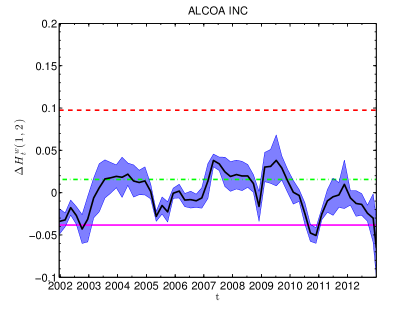

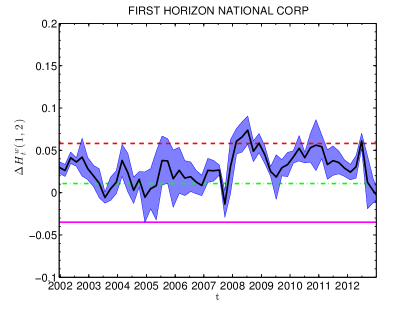

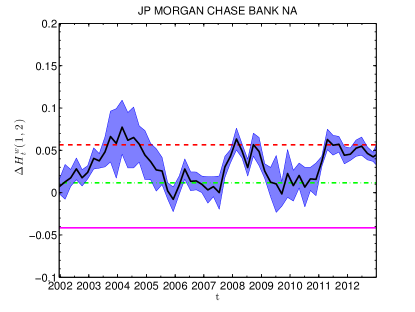

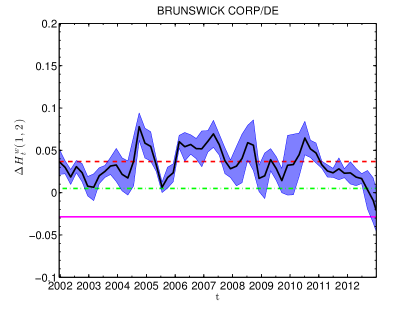

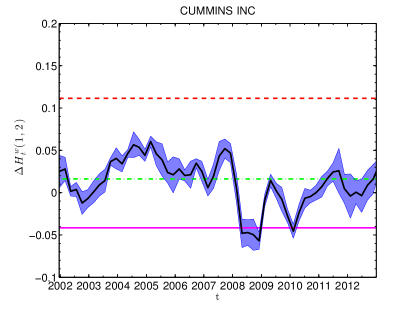

where is the number of time windows, and are respectively the and quantiles of the distribution and is the indicator function which is if the condition is enforced and otherwise. The rather high number of points falling outside the confidence intervals confirm systematically that empirical data do not agree with the hypothesis of constant multifractality. As one can appreciate from the quantiles reported in Table 3, there is no correlation between the number of quantile-exceeding and . This fact tells us that a simple underestimation of is unlikely to be the cause of the high quantile exceedance rate. In Figure 3 we show the results of this study for several daily stock prices, where is shown to exceed the quantiles many times.

|

|

|

|

|

|

We must remark that the values obtained for the correlation lengths T are very large compared to the time series lengths, a feature which is nonetheless commonly observed in multi-timescale volatility models [19].

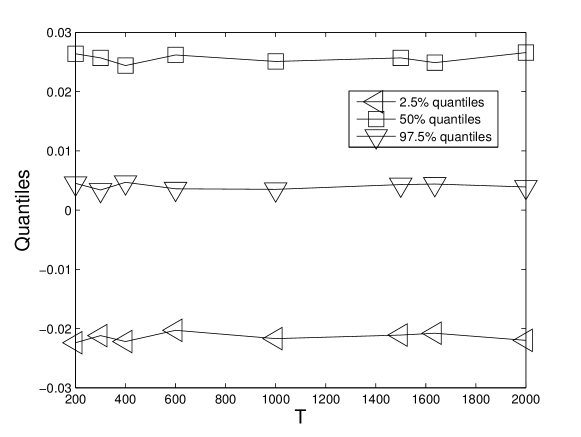

However, multifractality is expected to be proportional only to and thus the values of that we have measured should not be affected by the true of the series. This has been checked by computing the quantiles of the distributions of simulated with a fixed and varying the integral scale . As one can appreciate in Figure 4 the quantiles do not vary when the integral scale of the simulated series is changed but is kept constant.

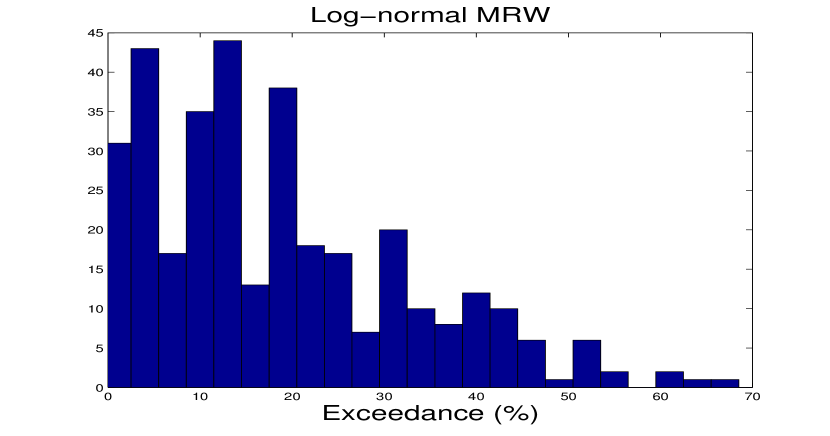

We have performed this statistical test for the set of 340 stocks listed in the NYSE. In particular, for each empirical time series, we have compared the fluctuations of empirical with the confidence intervals obtained from the MRW series simulated with the parameters estimated from the corresponding stock. The histogram in Figure 5 shows the distribution of the observed percentage of exceedances on this data set. It is remarkable that a conspicuous number of stocks shows a relevant number of ’s falling outside the confidence interval: the majority of stocks exhibits quantile crossings above and we find even some percentages above . This histogram shows that globally the hypothesis of a log-normal MRW model with constant intermittency looks like a poor approximation of empirical time series behaviour.

The conclusion one draws from these observations is that our proxy of multifractality appears to defy the hypothesis of a constant multifractal behaviour, as in the setup of the MRW model, as the majority of stocks shows time variations of which are not in agreement with the null hypothesis of constant multifractal behaviour. As discussed above, a time varying multifractality requires, through equation (3) and (10), a time varying . The observations reported here suggest that the scaling properties of financial time series may vary over time because of the reflection of complex and varying economic constraints. However, one needs to pay attention to the fact that the log-normal MRW with Gaussian residual may be a poor approximation for the empirical observations of the return distribution tails. In the next two sections we show how the same analysis performs if we consider a model with thicker tails.

3.3 The effect of Student t residuals

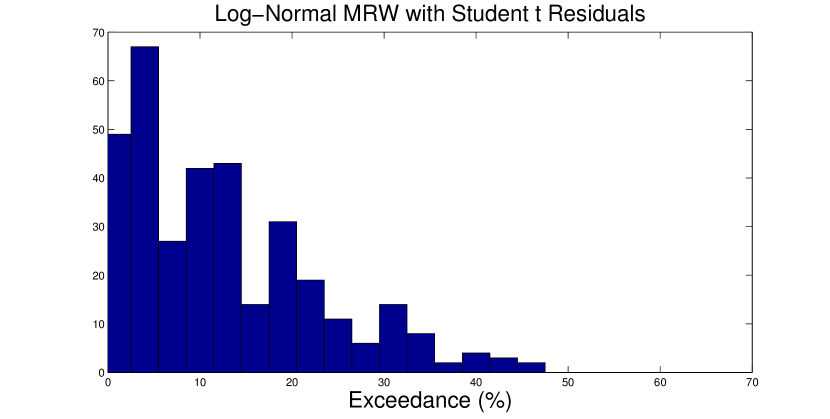

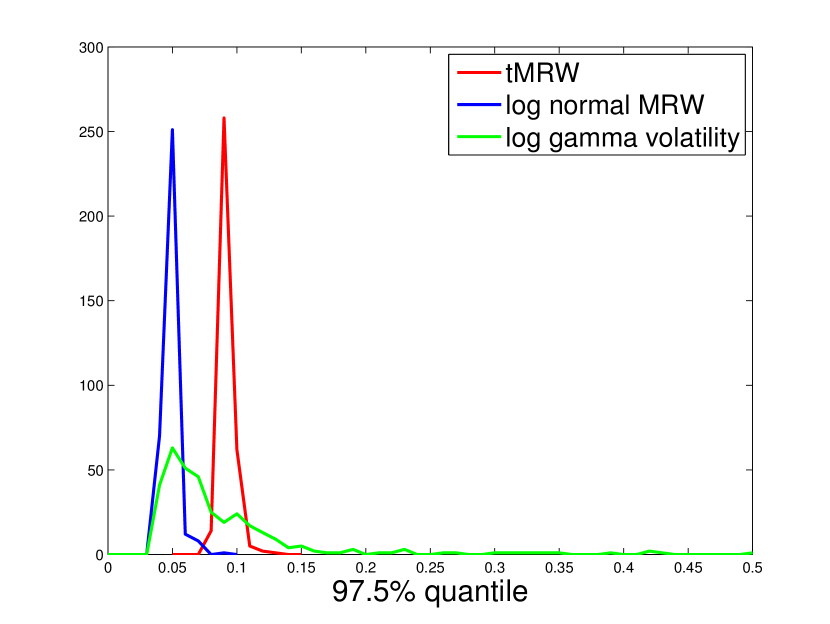

We have carried out the same analysis performed in the previous section for the complete set of 340 stocks, this time taking the residuals to be Student t distributed. MRW time series with Student t residuals (tMRW) have tails fatter than those observed in the log-normal case. We have simulated 1000 realisations of tMRW and computed the proxy of multifractality along with the corresponding quantiles. We plot in Figure 6 the observed for a selection of stocks together with the quantiles of the distribution of computed from the 1000 tMRW simulations. We also show in the top plot of Figure 9 the observed percentage of quantile-overpassing for all stocks analysed. As this plot shows, we still retrieve a significant fraction of the observations overpassing the extreme quantiles, with many still overpassing the quantiles more than of the time. The rate of quantile-crossing is nonetheless reduced with respect to the case in which residuals are Gaussian. The overall multifractal properties of the simulated time series are very much influenced by the Student t residuals: we observe indeed a systematic shift upwards of the sample distributions of the ’s. As shown in Figure 7, the median, corresponding to the quantile, is now peaked around , whereas the median retrieved from the log-normal case is peaked around . This tells us that, for a fixed intermittency, the thickness of the tails dramatically rebounds on the multifractal properties of the simulated series, which have now a higher degree of multifractality. This effect, which has also been reported in [7], clearly distinguishes different components of the measured multifractal property of the process: on the one hand the non-linear temporal dependence of the series, on the other hand the thickness of the tails of the unconditional distribution. Both aspects contribute to the measured multifractality and, by thickening the tails of the returns distribution, one can account for most of the anomalous fluctuations observed in the scaling exponents. Nonetheless the remaining multifractality still appears to defy the hypothesis of constant volatility covariance. In other words, the presence of more extreme fluctuations in the return process cannot fully account for the anomalous fluctuations observed in the empirical .

|

|

|

|

|

|

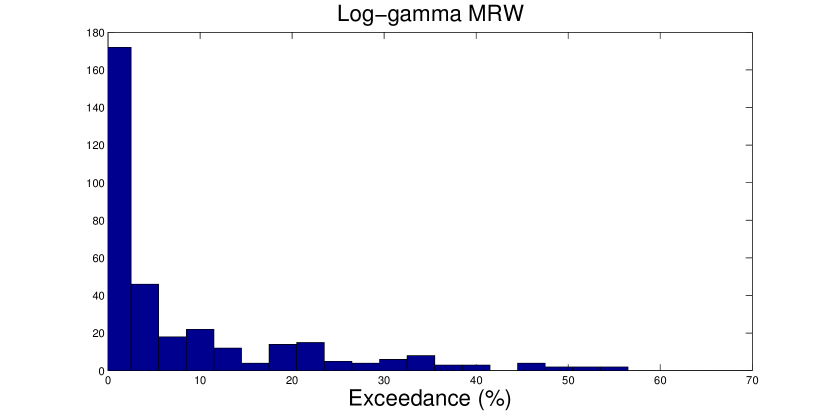

3.4 The effect of log-gamma volatility

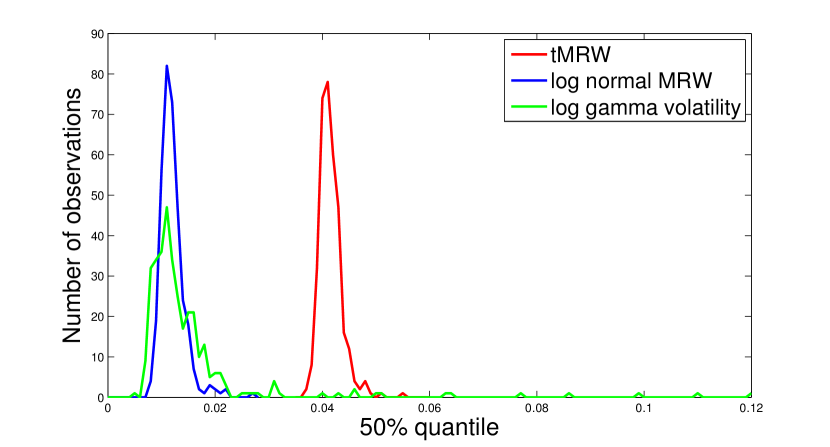

Another possible modification of the standard log-normal MRW in order to account for fatter tails is to consider the volatility to be log-gamma distributed. It has been shown in [25] that such a specification can reproduce the fat tails observed in the empirical distribution of stock returns better than the log-normal MRW. Synthetic time series with log-gamma volatility components are obtained replacing the normal distribution with the law given in (14) for . We have repeated the same testing procedure: after having estimated the model parameters we have computed the confidence intervals and, for each stock, we have compared the fluctuations of with the corresponding confidence interval. Examples of for a set of stocks compared with quantiles obtained with this specification of the volatility are shown in Figure 8. We also show in the histogram in bottom of Figure 9 the percentage of quantile-crossing observed on the complete data set. The histogram shows a dramatic reduction of quantile exceedances, with most of the anomalous fluctuations now falling below and therefore in agreement with what envisaged by the log-gamma MRW. As shown in Figure 7, the median of the distribution, although showing some large values, is distributed around the same values observed for the log-normal MRW. What is remarkably more broadly distributed than in the two previous cases is the quantile, whose observed distribution on the whole data set is shown in Figure 10, compared with those retrieved for log-normal MRW and tMRW. This confirms that the log-gamma volatility provides a framework in which very large fluctuations of the measured multifractality are much more likely than in the other two cases inspected but, as Figure 9 shows, some stocks still show fluctuations of which not even the log-gamma MRW can explain.

|

|

|

|

|

|

|

|

Overall we can say that both modifications of the log-normal MRW model confirm that beefing up the tails of the distribution of synthetic time series has a sizeable impact on multifractal properties, with the percentage of anomalous fluctuations being drastically reduced. Nonetheless, we still observe some stocks systematically overpassing the confidence intervals that do not allow to accept globally the hypothesis of constant multifractality.

4 Conclusive discussion

Main scope of this paper has been to measure and validate variations of multifractality on a set of stock returns. As a benchmark we have considered the MRW model, a parsimonious multifractal model that is able to reproduce faithfully many features commonly observed in stock returns. Since the dynamical estimations of multifractality are made on relatively small samples, to validate the observed fluctuations in the degree of multifractality as truly significant, we have shown that the fluctuations observed in empirical data are truly crossing the extreme quantiles expected from a MRW with constant intermittency coefficient. Confidence intervals have been computed by estimating a proxy of multifractality on different realisations of MRW’s simulated with parameters obtained from each empirical time series. We can conclude that the tails of the unconditional distribution of stock returns contribute significantly to the observed fluctuations of multifractality, but cannot fully explain the totality of the quantile crossings. Thus the disagreement between model and data could be possibly explained assuming the intermittency parameter to be time varying, which corresponds to having a breakdown in the serial dependence of the volatility. A possible time varying nature of the intermittency would also affect the tails of the distribution, which depend critically on . We have also shown that increasing the intermittency coefficient makes, as indeed expected, the tails of the GHE distribution computed on the synthetic series thicker, while we found no relevant dependence with . Our analysis thus suggests that a varying intermittency coefficient may be the correct guess towards the inclusion of the observed empirical facts into future multifractal modelling.

A natural extension, which we are investigating at the present, is the possibility of identifying switching points between multifractality regimes, as suggested by research contributions in regime switching for dynamical correlation [36, 37]. As with cross-correlation, one could model the temporal correlation of the volatility to be switching between different regimes of stationarity, although the association of the switching points with realistic economic triggers is yet to be established.

Starting from these results, our main future aim is the development of a realistic model for stock dynamics which incorporate these empirical findings, possibly backed by a plausible economic ground about what triggers multifractality to change over time.

Acknowledgments

The authors warmly thank Jean-Philippe Bouchaud for helpful discussions. We also thank Bloomberg for providing the data. TDM acknowledges support by COST ACTION TD1210.

References

- [1] R.N. Mantegna and H.E. Stanley. An introduction to econophysics: correlations and complexity in finance. Cambridge Univ Pr, 2000.

- [2] J.W. Kantelhardt, S.A. Zschiegner, E. Koscielny-Bunde, S. Havlin, A. Bunde, and H.E. Stanley. Multifractal detrended fluctuation analysis of nonstationary time series. Physica A, 316(1):87–114, 2002.

- [3] T. Di Matteo, T. Aste, and M.M. Dacorogna. Long-term memories of developed and emerging markets: Using the scaling analysis to characterize their stage of development. Journal of Banking & Finance, 29(4):827–851, 2005.

- [4] J.-F. Muzy, J. Delour, and E. Bacry. Modelling fluctuations of financial time series: from cascade process to stochastic volatility model. The European Physical Journal B, 17(3):537–548, 2000.

- [5] J. Barunik and L. Kristoufek. On hurst exponent estimation under heavy-tailed distributions. Physica A, 389(18):3844–3855, 2010.

- [6] T. Di Matteo. Multi-scaling in finance. Quantitative Finance, 7(1):21–36, 2007.

- [7] J. Barunik, T. Aste, T. Di Matteo, and R. Liu. Understanding the source of multifractality in financial markets. Physica A, 391:4234–4251, 2012.

- [8] L. Kristoufek. Multifractal height cross-correlation analysis: A new method for analyzing long-range cross-correlations. Europhysics Letters, 95:68001, 2011.

- [9] Z.-Q.-Q. Jiang and W.-X. Zhou. Multifractality in stock indexes: Fact or fiction? Physica A: Statistical Mechanics and its Applications, 387(14):3605–3614, 2008.

- [10] Z.-Q. Jiang and W.-X. Zhou. Multifractal analysis of chinese stock volatilities based on the partition function approach. Physica A: Statistical Mechanics and its Applications, 387(19):4881–4888, 2008.

- [11] E. Bacry, J. Delour, and J.-F. Muzy. Multifractal random walk. Physical Review E, 64(2):026103, 2001.

- [12] J.-P. Bouchaud, M. Potters, and M. Meyer. Apparent multifractality in financial time series. The European Physical Journal B, 13(3):595–599, 2000.

- [13] R. Liu, T.D. Matteo, and T. Lux. Multifractality and long-range dependence of asset returns: The scaling behaviour of the markov-switching multifractal model with lognormal volatility components. Advances in Complex Systems, 11(5):669–684, 2008.

- [14] L. Calvet and A. Fisher. Multifractality in asset returns: theory and evidence. Review of Economics and Statistics, 84(3):381–406, 2002.

- [15] R. Liu, T. Di Matteo, and T. Lux. True and apparent scaling: The proximity of the markov-switching multifractal model to long-range dependence. Physica A, 383(1):35–42, 2007.

- [16] B.B. Mandelbrot, A. Fisher, and L. Calvet. The multifractal model of asset returns. Cowles Foundation discussion paper no. 1164, Yale University, 1997.

- [17] T. Lux. The markov-switching multifractal model of asset returns. Journal of business & economic statistics, 26(2):194–210, 2008.

- [18] Z. Ding, C.W.J. Granger, and R.F. Engle. A long memory property of stock market returns and a new model. Journal of empirical finance, 1(1):83–106, 1993.

- [19] L. Borland and J.-P. Bouchaud. On a multi-timescale statistical feedback model for volatility fluctuations. arXiv:physics.soc-ph/0507073, 2005.

- [20] J.-P. Bouchaud and M. Potters. Theory of financial risk and derivative pricing: from statistical physics to risk management. Cambridge Univ Pr, 2003.

- [21] M.M. Dacorogna. An introduction to high-frequency finance. Academic Pr, 2001.

- [22] T. Di Matteo, T. Aste, and M.M. Dacorogna. Scaling behaviors in differently developed markets. Physica A, 324(1):183–188, 2003.

- [23] M. Bartolozzi, C. Mellen, T. Di Matteo, and T. Aste. Multi-scale correlations in different futures markets. The European Physical Journal B, 58(2):207–220, 2007.

- [24] W.-X. Zhou. The components of empirical multifractality in financial returns. EPL, 88(2):28004, 2009.

- [25] J.-F. Muzy, E. Bacry, and A. Kozhemyak. Extreme values and fat tails of multifractal fluctuations. Physical Review E, 73(6):066114, 2006.

- [26] J.-F. Muzy, E. Bacry, R. Baile, and P. Poggi. Uncovering latent singularities from multifractal scaling laws in mixed asymptotic regime. application to turbulence. EPL (Europhysics Letters), 82(6):60007, 2008.

- [27] A. Carbone, G. Castelli, and HE Stanley. Time-dependent hurst exponent in financial time series. Physica A, 344(1):267–271, 2004.

- [28] D. Grech and G. Pamuła. The local hurst exponent of the financial time series in the vicinity of crashes on the polish stock exchange market. Physica A, 387(16):4299–4308, 2008.

- [29] R. Morales, T. Di Matteo, R. Gramatica, and T. Aste. Dynamical generalized hurst exponent as a tool to monitor unstable periods in financial time series. Physica A, 391:3180–3189, 2012.

- [30] A. Arneodo, E. Bacry, S. Manneville, and J.-F. Muzy. Analysis of random cascades using space-scale correlation functions. Physical Review Letters, 80(4):708–711, 1998.

- [31] E. Bacry, A. Kozhemyak, and J.-F. Muzy. Continuous cascade models for asset returns. Journal of Economic Dynamics and Control, 32(1):156–199, 2008.

- [32] J.-F. Muzy, R. Baïle, and P. Poggi. Intermittency of surface-layer wind velocity series in the mesoscale range. Physical Review E, 81(5):056308, 2010.

- [33] L. Borland, J.-P. Bouchaud, J.-F. Muzy, and G. Zumbach. The dynamics of financial marketsmandelbrots multifractal cascades. Wilmott Magazine, page p 86, 2005.

- [34] T. Aste. https://www.mathworks.com/matlabcentral/fileexchange/36487-weighted-generalized-hurst-exponent.

- [35] F. Pozzi, T. Di Matteo, and T. Aste. Exponential smoothing weighted correlations. The European Physical Journal B, 85:175, 2012.

- [36] D. Pelletier. Regime switching for dynamic correlations. Journal of Econometrics, 131(1):445–473, 2006.

- [37] J.D. Hamilton. Analysis of time series subject to changes in regime. Journal of Econometrics, 45(1):39–70, 1990.