Estimation of extreme risk regions under multivariate regular variation

Juan-Juan Cailabel=e1]j.cai@tilburguniversity.edu

[John H. J. Einmahllabel=e2]j.h.j.einmahl@tilburguniversity.edu

[Laurens de Haanlabel=e3]ldehaan@ese.eur.nl

[

Tilburg University, Tilburg University and Lisbon University

Department of Econometrics & OR and CentER

Tilburg University

P.O. Box 90153

5000 LE Tilburg

The Netherlands

E-mail: e2

E-mail: e3

(2011; 7 2010; 3 2011)

Abstract

When considering

possibly dependent random variables, one is often interested in extreme risk

regions, with very small probability . We consider

risk regions of the form , where is the joint density

and a small number. Estimation of such an extreme risk region is difficult since it

contains hardly any or no data. Using extreme value theory, we

construct a natural estimator of an extreme risk region and prove a

refined form of consistency, given a random sample of multivariate

regularly varying random vectors. In a detailed simulation and

comparison study, the good performance of the procedure is

demonstrated. We also apply our estimator to financial data.

62G32,

62G05,

62G07,

60G70,

60F05,

Extremes,

level set,

multivariate quantile,

rare event,

spectral density,

tail dependence,

doi:

10.1214/11-AOS891

keywords:

[class=AMS]

.

keywords:

.

††volume: 39††issue: 3

,

and

aut1Supported in part by FCT/PTDC/MAT/112770/2009.

1 Introduction

A two-dimensional normal density or Student -density is constant on

boundaries of certain ellipses. Outside such an ellipse the density is

lower than inside. It is straightforward to find such an outer region

and its contour (line), for a given small probability. We can consider

such contour as a natural multidimensional extension of a

(one-dimensional) quantile. Even for extreme sets, that is, very low

density levels, the calculations are straightforward.

In this paper we consider, much more general, multivariate

regularly varying distributions [for a review, see Jessen and Mikosch (2006)]. We consider the latter distributions,

since we want to explore in particular extreme sets, that is, sets far

removed from the origin.

A random vector is multivariate regularly varying if

there exist

a constant , the index and an arbitrary probability measure

on , the unit

hypersphere, such that

(1)

for every and Borel set in with , with the -norm of ; see

Rvačeva

(1962).

An equivalent statement is

(2)

and there exists a measure such that

(3)

for every Borel set on that is bounded away from

the origin and satisfies ; here . Note that is homogeneous,

that is, for all

,

(4)

Clearly, on , is a probability measure.

The limit relation in (3) is a multivariate analogue of the

“peaks-over-threshold” or “generalized Pareto limit” method in

one-dimensional extreme value theory. Particular cases of (1)

are distributions in the sum-domain of attraction of -stable

distributions and heavy tailed elliptical distributions such as

multivariate -distributions [see Hashorva (2006)].

We require the convergence in (2) and (3) at the density

level: {longlist}[(a)]

Suppose that the distribution of has a continuous

and positive density and that for some positive function and

some positive function regularly varying at infinity with negative

index , we have

(5)

and

(6)

Then is continuous on and

for all and

.

Throughout, we can and will take (see Lemma 1, Section 5).

From Lemma 1, it follows that doing so (3) holds with .

The extreme region will be of the form

where is the probability density of the random vector ; is determined in such a way that the probability of is equal to a

given very small number , like ,.

It is the purpose of this paper to estimate based on i.i.d. copies of . Note that the shape of is

not predetermined, it depends on the density . For the estimation of

, we will use an approximation of based on the density of . The values of we consider are typically of order . This

means that the number of data points that fall in is small and can

even be zero, that is, we are extrapolating outside the sample. This

lack of relevant data points makes estimation difficult. The estimation

of is a multivariate analogue of the estimation of extreme

quantiles in the univariate setting; see, for example, de Haan and

Ferreira (2006), Chapter 4. The multivariate case

is much more complicated, however, since we have to estimate a whole

set instead of only one value.

Having an estimate of can be important in various settings. It can

be used as an alarm system in risk management: if a new observation

falls in the estimated it is a signal of extreme risk. See

Einmahl, Li and Liu (2009) for an application to aviation safety along

these lines.

In a financial or insurance setting, points on the boundary of the

estimate of can be used for stress testing. The estimate of can

also be used to rank extreme observations (see Remark 3,

Section 2).

For the “central” part of the distribution, that is, is

fixed (and “not too small”), nonparametric estimation of density

level sets has been studied in depth in the literature. Two approaches

are used, the plug-in approach using density estimation [see

Baíllo, Cuesta-Albertos and

Cuevas (2001) and Rigollet and Vert (2009)], and the excess

mass approach [see Müller and Sawitzki (1991),

Polonik (1995) and Tsybakov (1997)]. Our estimation problem

and (hence) our approach are quite different from these.

This paper is organized as follows. In Section 2, we derive our

estimator and show a refined form of consistency. A simulation and

comparison study is presented in Section 3 and a financial application

is given in Section 4. Section 5 contains the proof of the main result.

2 Main result

Consider a random sample with

, for ; their common

probability measure on is denoted with . Write

for the

radius and for the direction

of

. We wish to

estimate an extreme risk region of the form

where is such that , where , as .

This means that and depend on , that is, and

. We shall

connect to a fixed set not depending on , defined by

It will

turn out that can be approximated by a properly inflated version

of . In fact, it follows from (6) that the risk regions

are asymptotically homothetic as a function of , for small values of .

Define

and

. Note that is regularly varying at

infinity with index .

We will approximate in two steps by a (deterministic) region

. This approximation satisfies

(7)

( denotes “symmetric difference”) and is based on the

above limit relations. The region can therefore be

estimated using extreme value theory.

The first step is to establish an approximation of . Let

{longlist}[(b)]

be a sequence of positive

integers such that and .

The region is approximated by

Next, we approximate by a further region defined in

terms of the limit density rather than :

(8)

Indeed, and this approximation of are homothetic.

Write

for a Borel set on . Clearly,

and hence

The relation between the spectral measure and is [cf. (1) and (3)]

for

a Borel set . Recall that the spectral measure is a

probability measure.

The existence of a density of implies the existence of a density

of , that is,

where is the Hausdorff measure (surface area) on

and

Next, we write and in terms of the spectral

density:

and hence

To estimate , we need estimators for

and . From the above expressions

for and , we see that this means that we have to estimate

,

and . First, we define

[the th order statistic of the , ].

Since the tail of the distribution function of

is regularly varying with index , we can use one of

the well-known estimators of the extreme value index ,

based on

the ; see, for example, Hill (1975), Smith (1987) and

Dekkers, Einmahl and

de Haan (1989). It remains to estimate .

Let be a continuous and

nonincreasing (kernel) function with and .

For

, define an estimator of by

For estimating it suffices to estimate , see

(7). Hence, in view of (8), we define

(9)

with

and

In the definition of the set , the choice of the value 1 was not

motivated. We could have taken any number instead.

Such an alternative definition of would lead to exactly the same

estimator , which shows that the value 1 plays no role.

Assume

(c)

Note that this simple condition is weaker than the usual second order

condition with negative second order parameter [see, e.g.,

Theorem 4.3.8 in de Haan and Ferreira (2006)]; indeed,

there exist functions with that satisfy condition (c).

Theorem 1

Let as .

Assume conditions (a), (b), (c) hold and that is

such that

.

Also assume that , and

, as .

Then we have

(10)

and hence

Remark 1.

The tuning parameter is used in the estimators of and . It is important to be able to choose three

different values for , denoted with and ,

respectively. (Note that “good” values of and are

determined by the tail of —the distribution function of —whereas a good is determined by the conditional distribution

of , given that , for large .) If we adapt the

conditions of the theorem, in particular if (b) holds for and if , and , then (10) remains true for the generalized estimator that

allows for the aforementioned different -values. We will use this

generalized estimator in the simulation study and the real data

application.

The actual choice of these -values is a notorious problem in extreme

value theory. A solution of this problem is far beyond the scope of the

present paper. We will only give heuristic guidelines here. First,

consider the estimation of . Plot as a

function of . Now

find the first stable, that is, approximately constant, region in the

graph of this function. This vertical level is the final estimate of

. It is also possible to use (complicated) asymptotically

optimal procedures; see, for example, Danielsson et al. (2001). Once the

estimate is fixed, we plot

against and we search for the first stable part in this graph. The

vertical level is now the estimate of the constant in condition

(c). Observe that is a building block of

, so we do not need to estimate

separately. Also

observe that we do not (need to) determine and , but

only a

region of good values. Finally, using again the already fixed , we

plot as a function of and again we search for

the first stable region; we take to be the midpoint of this

region of -values.

Remark 2.

The class of multivariate regularly varying distributions is quite

large. It contains, for example, all elliptical distributions with a heavy

tailed radial distribution and all distributions in the domain of a

sum-attraction of a multivariate (nonnormal) stable distribution. It

seems natural, however, to try to extend the assumption of multivariate

regular variation to the case of nonequal tail indices . It is

an important feature of the present model that all directions are

equally important: the marginal distributions do not play a special

role. An extension to nonequal tail indices would be possible in

principle, but it will be of limited value since it only works if

marginal transformations lead to the present model. Also note

that basically all linear combinations of the components inherit the

lowest of the marginal tail indices: the tail index is not a smooth

function of the direction (if it is not constant). Moreover, the

statistical theory that will be needed will be challenging and will

lead to a new and different project.

Remark 3.

Note that the estimated extreme risk region

depends on in a continuous way and has the property that

implies . Hence, we can

find the smallest

such that an observation is on the boundary of . The

corresponding observation can be considered the largest one and we

know its “-value.” This is helpful in deciding whether some

observation is the most extreme or if it is an outlier. Also, by

continuing this procedure we can rank the larger observations.

3 Simulation study

In this section, a detailed simulation study is performed in order to

investigate the finite sample performance of our estimator [with

estimated using the moment estimator of Dekkers, Einmahl and

de Haan (1989) and with ].

We consider five multivariate distributions.

•

The bivariate Cauchy distribution with

density

(11)

This is a very heavy tailed density, with and

, for .

•

The trivariate Cauchy distribution with

density

(12)

This is also a very heavy tailed density, with

and , for .

•

A bivariate elliptical distribution with density ()

(13)

It is less heavy tailed. We have and

, with

.

•

A bivariate “clover” distribution with density ()

(14)

We have , again, and

.

•

A bivariate asymmetric shifted distribution with density

[, ]

(15)

This distribution is not symmetric and the “center” is not the origin,

but ; and

, if , and

, if ,

.

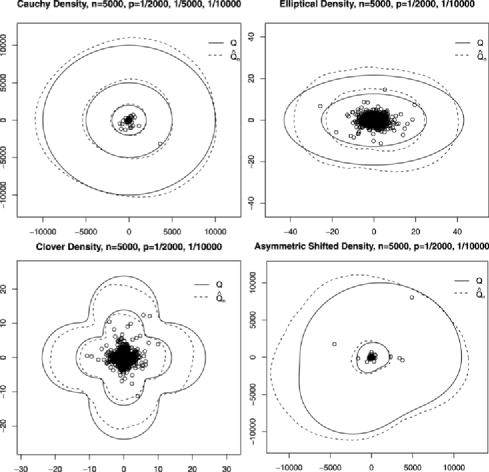

First, we simulated single data sets of size 5,000 of the bivariate

Cauchy distribution, the elliptical distribution in (13), the

clover distribution in (14) and the asymmetric shifted

distribution in (15). We computed the true and estimated risk regions

for , 15,000 or . This is depicted in Figure 1. We see that the estimated regions are relatively close to the

true risk regions. It is interesting to note that the -value (see

Remark 3) of the largest observation for the Cauchy sample is

0.000209, which is about . This shows that this observation is a

typical one. (Looking at the data only, one might want to conclude that

this observation is an outlier.) Also note that for the bivariate

Cauchy distribution, for, for example, , the density at the

boundary of the true risk region is less than . This

emphasizes that we are estimating in an “almost empty” part of the

plane and that a fully nonparametric procedure could not work here.

Figure 1: True and estimated risk regions based on

one sample of size 5,000 from the bivariate Cauchy distribution, the

elliptical distribution in (13), the clover distribution in

(14) and the asymmetric shifted distribution in (15).

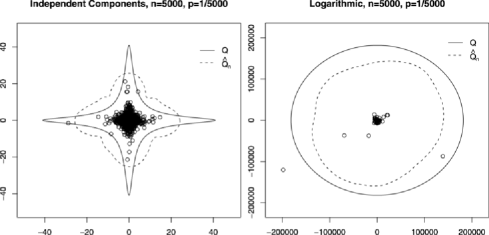

In addition, we simulated one sample of the bivariate distribution with

independent -components. This distribution does not

satisfy condition (a), since the spectral measure is discrete and

concentrated on the intersection of the coordinate axes with the unit

circle. We also simulated one sample of a bivariate “logarithmic”

distribution with and uniform spectral measure, but where

the radial distribution satisfies tends to a constant

and hence as , that is, this

distribution does not satisfy condition (c). Although both

distributions do not satisfy our conditions, we see nevertheless

satisfactory behavior of the estimator in Figure 2. In the

left panel, the estimated region has about the right size and the

difficult shape is approximated reasonably well; in the right panel, we

see that both the shape and the size are approximated quite well.

Figure 2: True and estimated risk regions based on

one sample of size from the bivariate distribution with

independent -components and the “logarithmic” distribution.

After this visual assessment of our estimator based on one sample at a

time, we now investigate its performance based on 100 simulated samples

of size 5,000. We will compare our estimator (denoted EVT) to a

nonparametric and to a more parametric estimator. The nonparametric

estimator is only defined in case and tries to mimic the

largest order statistic as an estimator of the th quantile in

the univariate case. It aims at elliptical level sets. It is defined as

follows. First, calculate the smallest ellipsoid containing half of the

data, the so-called MVE. Then inflate this ellipsoid, such that the

“largest” observation lies on its boundary. Now the region

outside this ellipsoid is the estimator.

For , the more parametric estimator is defined similarly to

in (9), but (only) the estimation of is done parametrically. Therefore, this estimator has the same size

as , but a different shape. (Note that the fully parametric

estimator based on multivariate normality would have a very bad

performance.) Take the observations with radius

and consider the transformed data

. In line with the limit result in (1), assume that these

data have a “distribution” , where

depends on a parameter . To be precise, we assume for the density

(Here a point on the unit circle is represented by its angle .) Now and are estimated by maximum

likelihood; observe that this yields the Hill estimator for .

Table 1: Median of the relative errors

of the three estimators, for (p1) and (p2)Figure 3: Boxplots of

for the here

proposed estimator and for the parametric and the nonparametric

estimator, based on

simulated data sets of size 5,000 from the five presented

densities for (p1) and (p2).

Table 1 shows for the three different estimators the median

of the 100 relative errors for

(p1)

and (p2).

In Figure 3, boxplots are shown of the relative error

for (p1) and

(p2). From

this table and figure, we see a good performance of our estimator. Its

behavior does not change much if changes from to .

The parametric estimator performs reasonably well, but it is

outperformed by our estimator, in particular for the elliptical and

clover densities. Recall that this estimator can be seen as a

modification of our estimator, since it uses the same estimated

inflation factor, but the shape is estimated differently. We see a

moderate performance of the nonparametric estimator; also, it cannot be

adapted to . Given that the estimation of these extreme

risk regions is a statistically difficult problem, we see decent

behavior of the three estimation methods. Obviously the parametric and

the nonparametric estimator do not perform well if the parametric part

of the model is not adequate or if the shape of the region is not

elliptical, respectively. The EVT estimator, presented in this paper,

does not suffer from these shortcomings and performs well for many

multivariate distributions.

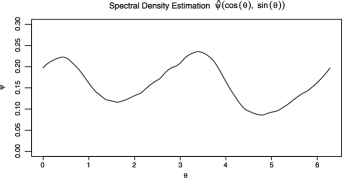

Figure 4: Estimator of of bivariate exchange rate

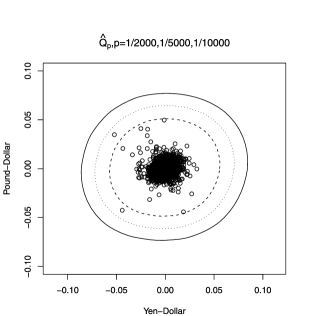

returns.Figure 5: Estimated extreme risk regions of exchange rate

returns.

4 Application

In this section, an application of our method to foreign exchange rate

data is presented. The data

are the daily exchange rates of Yen-Dollar and Pound-Dollar from

January 4, 1999 to July 31, 2009. Consider the daily log returns given

by

,

with , , and is the daily

exchange rate of the Yen to the Dollar and of the Pound to

the Dollar.

First, we check the equality of the extreme value indices (the

reciprocals of the tail indices) of the right and left tails of both

marginal distributions and that of the radius. This yields 5 extreme

value indices; the 5 estimates in increasing order are: 0.141, 0.191,

0.223, 0.242, 0.256. Hence, the maximal difference is 0.115. Based on

the asymptotic normality of the moment estimator of the extreme value

index, we compute an approximate upper bound for the maximal difference

of the 5 estimators under the null hypothesis of equality: 0.264.

Hence, there is no evidence that the 5 extreme value indices are

different. Other exchange rate data sets share this property. There are

also economic arguments supporting this claim. Therefore, we estimate

based on the radius and find .

As a next step, we estimate the density of the spectral

measure. The estimate

is depicted in Figure 4;

it is almost periodic with period . This yields that the boundary

of the

estimated extreme risk region is not like a circle, but more like an

ellipse. The location of the maxima of correspond to

the major axis of the region. We estimate the extreme risk regions for

and ,; see Figure 5. For risk management of financial institutions in the U.S., it is

important to know which extreme exchange rate returns w.r.t. the Pound

and the Yen can occur and which returns essentially never occur. Our

estimate answers this question.

More specifically,

points on the boundary of the estimated extreme risk region can be used

as multivariate stress test scenarios.

A scenario on the intersection of the major axis of the

ellipse-like boundary of the extreme risk region and the boundary

itself corresponds to a larger shock than a scenario on the

intersection of the minor axis of the ellipse-like boundary and the

boundary itself, but our method shows

that their “extremeness” is about the same.

5 Proofs

For the proof of the theorem, we need several lemmas and propositions.

We assume throughout that the conditions of the theorem are in force.

We start with a lemma on regular

variation in .

Lemma 1

Write . For any ,

(16)

Moreover

(17)

for any Borel set bounded away from the origin.

Define . Then

(18)

Let be the density of , then

(19)

{pf}

For any

[cf. Theorem 2.1 in de Haan and Resnick (1987)],

Let a Borel set be such that

, for some . Then

for and sufficiently large ,

is bounded by .

Hence, (17) holds by Lebesgue’s dominated convergence

theorem.

By taking derivatives, (16) and the homogeneity of , we obtain

\upqed

We now see that (5) and (6) hold with . From

now on, we will make the choice and hence .

Note that with this choice the relations (3) [with ] and (4) readily

follow from (17).

Corollary 1.

For all Borel sets with

positive distance from the origin,

(20)

and

(21)

{pf}

From and (3), we

obtain (20). It

follows from (c)

that

Note that . Observe that

or , hence

. By Lemma 3 and Corollary 1,

for any and large

Thus, .

Similarly, we have .

Hence,, that

is, .

In the same way, it follows from Lemmas 3 and 4 that

Hence,

.

The following proposition shows uniform consistency of and

might be of independent interest. There is an abundant literature on

density estimation for directional data. In particular, uniform

consistency of density estimators for directional data has been

established in Bai, Rao and Zhao (1988). Here, however, the data do

not have a fixed probability density on : the

density is defined via a limit relation. Hence, is only

an approximate model for the directional data. As a consequence, a more

general result is required.

Proposition 2

As ,

{pf}

It is easy to see that, for any , there exists a function

with and

, such that

Write , , and denote the corresponding order

statistics with . Let be the probability

measure on

corresponding to and let

be the

empirical

measure of the .

Define

By (26), for small enough the first term is

less than , with probability tending to one, uniformly in

. Also,

(29)

From (5), (5) and (27), we see

that for a proof of

(23) it remains to show that

It can be shown that there exists a constant and

finitely many , such that

as , and for every and

Hence for ,

The latter probability tends to , so it suffices to consider

the sum of the probabilities. Write . Fix and define

,

. Define the

conditional probability measure

on

and let be the corresponding empirical measure,

based on

observations. We have

(30)

Note that the first probability of the second sum in the

right

side of (5) is equal to 0.

From Bennett’s inequality [cf. Shorack and Wellner (1986), page 851],

it follows that for some constant

Hence, since ,

To complete the proof of (23), we need to consider

the first sum in the right side of (5). For the

first probability in there, we use Corollary 2.9 in Alexander (1984), a

good probability bound for empirical processes on VC classes.

We obtain as an upper bound

Using , we find for some constant

Next, we show (24). From (27) and

(26), we obtain for small enough,

with probability tending to one.

It remains to prove (25). It is readily seen that

.

Hence, for small enough

\upqed

From Proposition 2 and the consistency of , we obtain

immediately, as ,

and, for ,

(31)

Proposition 3

As ,

{pf}

Note that as , we have

Combining these three limit relations, we obtain

This and (31) yields

that with probability tending to one, as ,

Proof of Theorem 1

The result follows from

Propositions 1 and 3.

Acknowledgments

We thank two referees for many insightful comments that led to an

improved version of the paper. We are grateful to Kees Koedijk, Roger

Laeven, Ronald Mahieu and Chen Zhou for discussions of the financial

application.

References

Alexander (1984){barticle}[mr]

\bauthor\bsnmAlexander, \bfnmKenneth S.\binitsK. S.

(\byear1984).

\btitleProbability inequalities for empirical processes and a law of the

iterated logarithm.

\bjournalAnn. Probab.

\bvolume12

\bpages1041–1067.

\bnote[Corr.: 15 (1987) 428–430.]

\bidissn=0091-1798, mr=0757769

\bptnotecheck related

\endbibitem

Bai, Rao and Zhao (1988){barticle}[mr]

\bauthor\bsnmBai, \bfnmZ. D.\binitsZ. D.,

\bauthor\bsnmRao, \bfnmC. Radhakrishna\binitsC. R. and \bauthor\bsnmZhao, \bfnmL. C.\binitsL. C.

(\byear1988).

\btitleKernel estimators of density function of directional data.

\bjournalJ. Multivariate Anal.

\bvolume27

\bpages24–39.

\biddoi=10.1016/0047-259X(88)90113-3, issn=0047-259X, mr=0971170

\endbibitem

Baíllo, Cuesta-Albertos and

Cuevas (2001){barticle}[mr]

\bauthor\bsnmBaíllo, \bfnmAmparo\binitsA.,

\bauthor\bsnmCuesta-Albertos, \bfnmJuan A.\binitsJ. A. and \bauthor\bsnmCuevas, \bfnmAntonio\binitsA.

(\byear2001).

\btitleConvergence rates in nonparametric estimation of level sets.

\bjournalStatist. Probab. Lett.

\bvolume53

\bpages27–35.

\biddoi=10.1016/S0167-7152(01)00006-2, issn=0167-7152, mr=1843338

\endbibitem

Danielsson et al. (2001){barticle}[mr]

\bauthor\bsnmDanielsson, \bfnmJ.\binitsJ., \bauthor\bparticlede

\bsnmHaan, \bfnmL.\binitsL.,

\bauthor\bsnmPeng, \bfnmL.\binitsL. and \bauthor\bparticlede

\bsnmVries, \bfnmC. G.\binitsC. G.

(\byear2001).

\btitleUsing a bootstrap method to choose the sample fraction in tail index

estimation.

\bjournalJ. Multivariate Anal.

\bvolume76

\bpages226–248.

\biddoi=10.1006/jmva.2000.1903, issn=0047-259X, mr=1821820

\endbibitem

de Haan and Ferreira (2006){bbook}[mr]

\bauthor\bparticlede \bsnmHaan, \bfnmLaurens\binitsL.

and \bauthor\bsnmFerreira, \bfnmAna\binitsA.

(\byear2006).

\btitleExtreme Value Theory: An Introduction.

\bpublisherSpringer, \baddressNew York.

\bidmr=2234156

\endbibitem

de Haan and Resnick (1987){barticle}[mr]

\bauthor\bparticlede \bsnmHaan, \bfnmL.\binitsL. and \bauthor\bsnmResnick, \bfnmS.\binitsS.

(\byear1987).

\btitleOn regular variation of probability densities.

\bjournalStochastic Process. Appl.

\bvolume25

\bpages83–93.

\biddoi=10.1016/0304-4149(87)90191-8, issn=0304-4149, mr=0904266

\endbibitem

Dekkers, Einmahl and

de Haan (1989){barticle}[mr]

\bauthor\bsnmDekkers, \bfnmA. L. M.\binitsA. L. M.,

\bauthor\bsnmEinmahl, \bfnmJ. H. J.\binitsJ. H. J. and \bauthor\bparticlede \bsnmHaan, \bfnmL.\binitsL.

(\byear1989).

\btitleA moment estimator for the index of an extreme-value distribution.

\bjournalAnn. Statist.

\bvolume17

\bpages1833–1855.

\biddoi=10.1214/aos/1176347397, issn=0090-5364, mr=1026315

\endbibitem

Einmahl, Li and Liu (2009){barticle}[mr]

\bauthor\bsnmEinmahl, \bfnmJohn H. J.\binitsJ. H. J.,

\bauthor\bsnmLi, \bfnmJun\binitsJ. and \bauthor\bsnmLiu, \bfnmRegina Y.\binitsR. Y.

(\byear2009).

\btitleThresholding events of extreme in simultaneous monitoring of multiple

risks.

\bjournalJ. Amer. Statist. Assoc.

\bvolume104

\bpages982–992.

\biddoi=10.1198/jasa.2009.ap08329, issn=0162-1459, mr=2562001

\endbibitem

Hall, Watson and

Cabrera (1987){barticle}[mr]

\bauthor\bsnmHall, \bfnmPeter\binitsP.,

\bauthor\bsnmWatson, \bfnmG. S.\binitsG. S. and \bauthor\bsnmCabrera, \bfnmJavier\binitsJ.

(\byear1987).

\btitleKernel density estimation with spherical data.

\bjournalBiometrika

\bvolume74

\bpages751–762.

\biddoi=10.1093/biomet/74.4.751, issn=0006-3444, mr=0919843

\endbibitem

Hashorva (2006){barticle}[mr]

\bauthor\bsnmHashorva, \bfnmEnkelejd\binitsE.

(\byear2006).

\btitleOn the regular variation of elliptical random vectors.

\bjournalStatist. Probab. Lett.

\bvolume76

\bpages1427–1434.

\biddoi=10.1016/j.spl.2006.02.014, issn=0167-7152, mr=2245561

\endbibitem

Hill (1975){barticle}[mr]

\bauthor\bsnmHill, \bfnmBruce M.\binitsB. M.

(\byear1975).

\btitleA simple general approach to inference about the tail of a

distribution.

\bjournalAnn. Statist.

\bvolume3

\bpages1163–1174.

\bidissn=0090-5364, mr=0378204

\endbibitem

Jessen and Mikosch (2006){barticle}[mr]

\bauthor\bsnmJessen, \bfnmAnders Hedegaard\binitsA. H. and \bauthor\bsnmMikosch, \bfnmThomas\binitsT.

(\byear2006).

\btitleRegularly varying functions.

\bjournalPubl. Inst. Math. (Beograd) (N.S.)

\bvolume80(94)

\bpages171–192.

\biddoi=10.2298/PIM0694171J, issn=0350-1302, mr=2281913

\endbibitem

Müller and Sawitzki (1991){barticle}[mr]

\bauthor\bsnmMüller, \bfnmD. W.\binitsD. W. and \bauthor\bsnmSawitzki, \bfnmG.\binitsG.

(\byear1991).

\btitleExcess mass estimates and tests for multimodality.

\bjournalJ. Amer. Statist. Assoc.

\bvolume86

\bpages738–746.

\bidissn=0162-1459, mr=1147099

\endbibitem

Polonik (1995){barticle}[mr]

\bauthor\bsnmPolonik, \bfnmWolfgang\binitsW.

(\byear1995).

\btitleMeasuring mass concentrations and estimating density contour

clusters—an excess mass approach.

\bjournalAnn. Statist.

\bvolume23

\bpages855–881.

\biddoi=10.1214/aos/1176324626, issn=0090-5364, mr=1345204

\endbibitem

Rigollet and Vert (2009){barticle}[mr]

\bauthor\bsnmRigollet, \bfnmPhilippe\binitsP. and \bauthor\bsnmVert, \bfnmRégis\binitsR.

(\byear2009).

\btitleOptimal rates for plug-in estimators of density level sets.

\bjournalBernoulli

\bvolume15

\bpages1154–1178.

\biddoi=10.3150/09-BEJ184, issn=1350-7265, mr=2597587

\endbibitem

Rvačeva (1962){barticle}[mr]

\bauthor\bsnmRvačeva, \bfnmE. L.\binitsE. L.

(\byear1962).

\btitleOn domains of attraction of multi-dimensional distributions.

\bjournalSelect. Transl. Math. Statist. Probab.

\bvolume2

\bpages183–205.

\bidmr=0150795

\endbibitem

Shorack and Wellner (1986){bbook}[mr]

\bauthor\bsnmShorack, \bfnmGalen R.\binitsG. R. and \bauthor\bsnmWellner, \bfnmJon A.\binitsJ. A.

(\byear1986).

\btitleEmpirical Processes with Applications to Statistics.

\bpublisherWiley, \baddressNew York.

\bidmr=0838963

\endbibitem

Smith (1987){barticle}[mr]

\bauthor\bsnmSmith, \bfnmRichard L.\binitsR. L.

(\byear1987).

\btitleEstimating tails of probability distributions.

\bjournalAnn. Statist.

\bvolume15

\bpages1174–1207.

\biddoi=10.1214/aos/1176350499, issn=0090-5364, mr=0902252

\endbibitem

Tsybakov (1997){barticle}[mr]

\bauthor\bsnmTsybakov, \bfnmA. B.\binitsA. B.

(\byear1997).

\btitleOn nonparametric estimation of density level sets.

\bjournalAnn. Statist.

\bvolume25

\bpages948–969.

\biddoi=10.1214/aos/1069362732, issn=0090-5364, mr=1447735

\endbibitem