High-dimensionality effects in the Markowitz problem and other quadratic programs with linear constraints: Risk underestimation

Abstract

We first study the properties of solutions of quadratic programs with linear equality constraints whose parameters are estimated from data in the high-dimensional setting where , the number of variables in the problem, is of the same order of magnitude as , the number of observations used to estimate the parameters. The Markowitz problem in Finance is a subcase of our study. Assuming normality and independence of the observations we relate the efficient frontier computed empirically to the “true” efficient frontier. Our computations show that there is a separation of the errors induced by estimating the mean of the observations and estimating the covariance matrix. In particular, the price paid for estimating the covariance matrix is an underestimation of the variance by a factor roughly equal to . Therefore the risk of the optimal population solution is underestimated when we estimate it by solving a similar quadratic program with estimated parameters.

We also characterize the statistical behavior of linear functionals of the empirical optimal vector and show that they are biased estimators of the corresponding population quantities.

We investigate the robustness of our Gaussian results by extending the study to certain elliptical models and models where our observations are correlated (in “time”). We show a lack of robustness of the Gaussian results, but are still able to get results concerning first order properties of the quantities of interest, even in the case of relatively heavy-tailed data (we require two moments). Risk underestimation is still present in the elliptical case and more pronounced than in the Gaussian case.

We discuss properties of the nonparametric and parametric bootstrap in this context. We show several results, including the interesting fact that standard applications of the bootstrap generally yield inconsistent estimates of bias.

We propose some strategies to correct these problems and practically validate them in some simulations. Throughout this paper, we will assume that , and tend to infinity, and .

Finally, we extend our study to the case of problems with more general linear constraints, including, in particular, inequality constraints.

doi:

10.1214/10-AOS795keywords:

[class=AMS] .keywords:

.T1Supported by the France–Berkeley Fund, a Sloan research Fellowship and NSF Grants DMS-06-05169 and DMS-08-47647 (CAREER).

1 Introduction

Many statistical estimation problems are now formulated, implicitly or explicitly, as solutions of certain optimization problems. Naturally, the parameters of these problems tend to be estimated from data and it is therefore important that we understand the relationship between the solutions of two types of optimization problems: those which use the population parameters and those which use the estimated parameters. This question is particularly relevant in high-dimensional inference where one suspects that the differences between the two solutions might be considerable. The aim of this paper is to contribute to this understanding by focusing on quadratic programs with linear constraints. An important example of such a program where our questions are very natural is the celebrated Markowitz optimization problem in Finance which will serve as a supporting example throughout the paper.

The Markowitz problem (Markowitz, 1952) is a classic portfolio optimization problem in Finance, where investors choose to invest according to the following framework: one picks assets in such a way that the portfolio guarantees a certain level of expected returns but minimizes the “risk” associated with them. In the standard framework, this risk is measured the variance of the portfolio.

Markowitz’s paper was highly influential and much work has followed. It is now part of the standard textbook literature on these issues [Ruppert (2006), Campbell, Lo and MacKinlay (1996)]. Let us recall the setup of the Markowitz problem.

-

•

We have the opportunity to invest in assets, .

-

•

In the ideal situation, the mean returns are known and represented by a -dimensional vector, .

-

•

Also, the covariance between the returns is known; we denote it by .

-

•

We want to create a portfolio, with guaranteed mean return , and minimize its risk, as measured by variance.

-

•

The question is how should items be weighted in portfolio? What are weights ?

We note that is positive semi-definite and hence is in particular symmetric. In the ideal (or population) solution, the covariance and the mean are known. The mathematical formulation is then the following simple quadratic program. We wish to find the weights that solve the following problem:

Here is a -dimensional vector with 1 in every entry. If is invertible, the solution is known explicitly (see Section 2). If we call the solution of this problem, the curve , seen as a function of , is called the efficient frontier.

Of course, in practice, we do not know and and we need to estimate them. An interesting question is therefore to know what happens in the Markowitz problem when we replace population quantities by corresponding estimators.

Naturally, we can ask a similar question for general quadratic programs with linear constraints [see below or Boyd and Vandenberghe (2004) for a definition], the Markowitz problem being a particular instance of such a problem. This paper provides an answer to these questions under certain distributional assumptions on the data. Hence our paper is really about the impact of estimation error on certain high-dimensional -estimation problems.

It has been observed by many that there are problems in practice when replacing population quantities by standard estimators [see Lai and Xing (2008), Section 3.5], and alternatives have been proposed. A famous one is the Black–Litterman model [Black and Litterman (1990), Meucci (2005) and, e.g., Meucci (2008)]. Adjustments to the standard estimators have also been proposed: Ledoit and Wolf (2004), partly motivated by portfolio optimization problems, proposed to “shrink” the sample covariance matrix toward another positive definite matrix (often the identity matrix properly scaled), while Michaud (1998) proposed to use the bootstrap and to average bootstrap weights to find better-behaved weights for the portfolio. As noted in Lai and Xing (2008), there is a dearth of theoretical studies regarding, in particular, the behavior of bootstrap estimators.

An aspect of the problem that is of particular interest to us is the study of large-dimensional portfolios (or quadratic programs with linear constraints). To make matters clear, we focus on a portfolio with assets. If we use a year of daily data to estimate , the covariance between the daily returns of the assets, we have observations at our disposal. In modern statistical parlance, we are therefore in a “large , large ” setting, and we know from random matrix theory that the sample covariance matrix is a poor estimator of , especially when it comes to spectral properties of . There is now a developing statistical literature on properties of sample covariance matrices when and are both large, and it is now understood that, though is unbiased for , the eigenvalues and eigenvectors of behave very differently from those of . We refer the interested reader to Johnstone (2001), El Karoui (2007, 2008, 2009a), Bickel and Levina (2008a), Rothman et al. (2008) for a partial introduction to these problems. We wish with this study to make clear that the “large , large ” character of the problem has an important impact of the empirical solution of the problem. By contrast, standard but thorough discussions of these problems (Meucci, 2005) give only a cursory treatment of dimensionality issues (e.g., one page out of a whole book).

Another interesting aspect of this problem is that the high-dimensional setting does not allow, by contrast to the classical “small , large ” setting, a perturbative approach to go through. In the “small , large ” setting, the paper Jobson and Korkie (1980) is concerned, in the Gaussian case, with issues similar to the ones we will be investigating.

The “large , large ” setting is the one with which random matrix theory is concerned—and the high-dimensional Markowitz problem has therefore been of interest to random matrix theorists for some time now. We note in particular the paper Laloux et al. (2000), where a random matrix-inspired (shrinkage) approach to improved estimation of the sample covariance matrix is proposed in the context of the Markowitz problem.

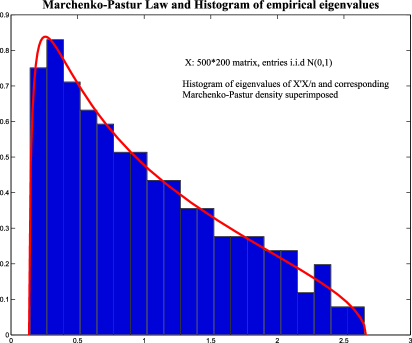

Let us now remind the reader of some basic facts of random matrix theory that suggest that serious problems may arise if one solves naively the high-dimensional Markowitz problem or other quadratic programs with linear equality constraints. A key result in random matrix theory is the Marčenko–Pastur equation (Marčenko and Pastur, 1967) which characterizes the limiting distribution of the eigenvalues of the sample covariance matrix and relates it to the spectral distribution of the population covariance matrix. We give only in this introduction its simplest form and refer the reader to Marčenko and Pastur (1967), Wachter (1978), Silverstein (1995), Bai (1999) and, for example, El Karoui (2009a) for a more thorough introduction and very recent developments, as well as potential geometric and statistical limitations of the models usually considered in random matrix theory.

In the simplest setting, we consider data , which are -dimensional. In a financial context, these vectors would be vectors of (log)-returns of assets, the portfolio consisting of assets. To simplify the exposition, let us assume that the ’s are i.i.d. with distribution . We call the matrix whose th row is the vector . Let us consider the sample covariance matrix

where is a matrix whose rows are all equal to the column mean of . Now let us call the spectral distribution of , that is, the probability distribution that puts mass at each of the eigenvalues of . A graphical representation of this probability distribution is naturally the histogram of eigenvalues of . A consequence of the main result of the very profound paper Marčenko and Pastur (1967) is that , though a random measure, is asymptotically nonrandom, and its limit, in the sense of weak convergence of distributions, has a density (when ) that can be computed. depends on in the following manner: if , the density of is

where and . Figure 1 presents a graphical illustration of this result.

What is striking about this result is that it implies that the largest eigenvalue of , , will be overestimated by the largest eigenvalue of . Also, the smallest eigenvalue of , , will be underestimated by the smallest eigenvalue of , . As a matter of fact, in the model described above, has all its eigenvalues equal to 1, so , while will asymptotically be larger or equal to and smaller or equal to (in the Gaussian case and several others, and converge to those limits). We note that the result of Marčenko and Pastur (1967) is not limited to the case where is identity, as presented here, but holds for general covariance ( has of course a different limit then).

Perhaps more concretely, let us consider a projection of the data along a vector , with , where is the Euclidian norm of . Here it is clear that, if , , for all , since . However, if we do not know and estimate it by , a naive (and wrong) reasoning suggests that we can find direction of lower variance than 1, namely those corresponding to eigenvectors of associated with eigenvalues that are less than 1. In particular, if is the eigenvector associated with , the smallest eigenvalue of , by naively estimating, for independent of , the variance in the direction of , , by the empirical version , one would commit a severe mistake: the variance in any direction is 1, but it would be estimated by something roughly equal to in the direction of .

In a portfolio optimization context, this suggests that by using standard estimators, such as the sample covariance matrix, when solving the high-dimensional Markowitz problem, one might underestimate the variance of certain portfolios (or “optimal” vectors of weights). As a matter of fact, in the previous toy example, thinking (wrongly) that there is low variance in the direction , one might (numerically) “load” this direction more than warranted, given that the true variance is the same in all directions.

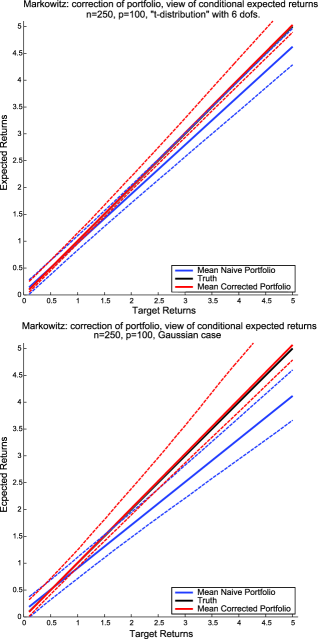

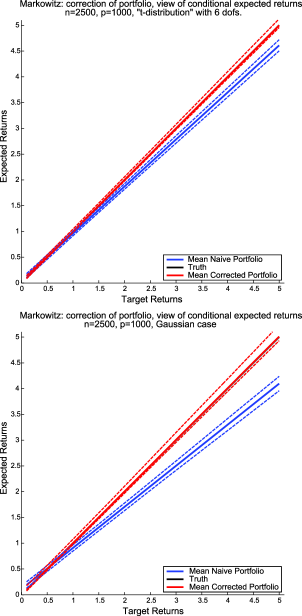

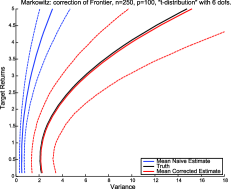

This simple argument suggests that severe problems might arise in the high-dimensional Markowitz problem and other quadratic programs with linear constraints, and in particular, risk might be underestimated. While this heuristic argument is probably clear to specialists of random matrix theory, the problem had not been investigated at a mathematical level of rigor in that literature before this paper was submitted [the paper Bai, Liu and Wong (2009) has appeared while this paper was being refereed. It is concerned with different models than the ones we will be investigating and our results do not overlap]. It has received some attention at a physical level of rigor [see, e.g., Pafka and Kondor (2003), where the authors treat only the Gaussian case, and do not investigate the effect of the mean, which as we show below creates problems of its own]. In this paper, we propose a theoretical analysis of the problem in a Gaussian and elliptical framework for general quadratic programs with linear constraints, one of them involving the parameter . Our results and contributions are several-fold. We relate the empirical efficient frontier to the theoretical efficient frontier that is key to the Markowitz theory, in a variety of theoretical settings. We show that the empirical frontier generally yields an underestimation of the risk of the portfolio and that Gaussian analysis gives an over-optimistic view of this problem. We show that the expected returns of the naive “optimal” portfolio are poorly estimated by . We argue that the bootstrap will not solve the problems we are pointing out here. Beside new formulas, we also provide robust estimators of the various quantities we are interested in.

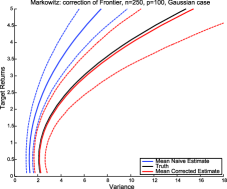

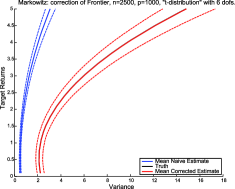

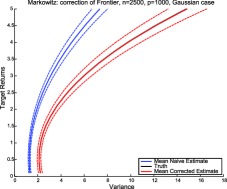

The paper is divided into four main parts and a conclusion. In Section 2, to make the paper self-contained, we discuss the solution of quadratic problems with linear equality constraints—a focus of this paper. In Section 3, we study the impact of parameter estimation on the solution of these problems when the observed data is i.i.d. Gaussian and obtain some exact distributional results for fixed and . In Section 4, we obtain results in the case where the data is elliptically distributed. This allows us also to understand the impact of correlation between observations in the Gaussian case and to get information about the behavior of the nonparametric bootstrap. In Section 5, we apply the results of Section 4 to the quadratic programs at hand and compare the elliptical and the Gaussian cases. We show, among other things, that the Gaussian results are not robust in the class of elliptical distribution. In particular, two models may yield the same and but can have very different empirical behavior. In Section 5, we also propose various schemes to correct the problems we highlight (see pages 2, 3 and 4 for pictures) and study more general problems with linear constraints (see Section 5.6). The conclusion summarizes our findings and the Appendix contains various facts and proofs that did not naturally flow in the main text or were better highlighted by being stated separately.

Several times in the paper and will appear. Unless otherwise noted, when taking the inverse of a population matrix, we implicitly assume that it exists. The question of existence of inverse of sample covariance matrices is well understood in the statistics literature. Because our models will have a component with a continuous distribution, there are essentially no existence problems (unless we explicitly mention and treat them) as proofs similar to standard ones found in textbooks [e.g., Anderson (2003)] would show. Hence, we do not belabor this point any further in the rest of the paper as our focus is on things other than rather well-understood technical details, and the paper is already a bit long.

Finally, let us mention that while the Finance motivation for our study is important to us, we treat the problem in this paper as a high-dimensional -estimation question (which we think has practical relevance). We will not introduce particular modelization assumptions which might be relevant for practitioners of Finance but might make the paper less relevant in other fields. A companion paper (El Karoui, 2009b) deals with more “financial” issues and the important question of the realized risk of portfolios that are “plug-in” solutions of the Markowitz problem.

2 Quadratic programs with linear equality constraints

We discuss here the properties of the solution of quadratic programs with linear equality constraints as they lay the foundations for our analysis of similar problems involving estimated parameters (and of problems with inequality constraints). We included this section for the convenience of the reader to make the paper as self-contained as possible.

The problem we want to solve is the following:

| (QP-eqc) |

Here is a positive definite matrix of size , and . We have the following theorem:

Theorem 2.1

Let us call the matrix whose th column is , the dimensional vector whose th entry is and the matrix

We assume that the ’s are such that is invertible. The solution of the quadratic program with linear equality constraints (QP-eqc) is achieved for

and we have

Let us call a dimensional vector of Lagrange multipliers. The Lagrangian function is, in matrix notation,

This is clearly a (strictly) convex function in , since is positive definite by assumption. We have

So . Now we know that . So . Therefore,

We deduce immediately that

We now turn to another result which will prove to be useful later. It gives a compact representation of linear combinations of the weights of the optimal solution, and we will rely heavily on it in particular in the case of Gaussian data.

Lemma 2.2

Let us consider the solution of the optimization problem (QP-eqc). Let be a vector in . Let us call the matrix that is written in block form

Assume that is invertible. Then

| (1) |

The proof is a consequence of the results discussed in the Appen- dix concerning inverses of partitioned matrices [see Section A.1 and equation (A.4) there]. Let us write

where is , is naturally and is a scalar. With the same block notation, we have

Then, we know [see equation (A.4)] that but since is a scalar, equal to , we have

Now , so . Hence,

We note that here , as an application of equation (A.2) clearly shows.

3 QP with equality constraints: Impact of parameter estimation in the Gaussian case

From now on, we will assume that we are in the high-dimensional setting where and go to infinity. Our study will be divided into two. We will first consider the Gaussian setting (in this section) and then study an elliptical distribution setting (in Section 4). (We note that for the Markowitz problem, the assumption of Gaussianity would be satisfied if we worked under Black–Scholes diffusion assumptions for our assets and were considering log-returns as our observations.) Interestingly, we will show that the results are not robust against the assumption of Gaussianity, which is not (so) surprising in light of recent random matrix results [see El Karoui (2009a)]. We will also show that understanding the elliptical setting allows us to understand the impact of correlation between observations and to discuss bootstrap-related ideas. In particular, we will see that various problems arise with the bootstrap in high-dimension and that the results change when one deals with observations that are correlated (in time) or not.

We also address similar questions concerning inequality constrained problems in Section 5.6.

Before we proceed, we need to set up some notations: we call the -dimensional vector whose entries are all equal to 1. We call , as above, the matrix containing all of our constraint vectors, which we may have to estimate (for instance, if for a certain ). We call the matrix of estimated constraint vectors.

The template question for all our investigations will be the following (Markowitz) question: what can be said of the statistical properties of the solution of

compared to the solution of the population version

We will solve the problem at a much greater degree of generality, by considering first quadratic programs with linear equality constraints (see Section 5.6 for inequality constraints) and comparing the solutions of

| (QP-eqc-Emp) |

and

| (QP-eqc-Pop) |

Here and will be estimated from the data. We call the vector that yields a solution of problem (QP-eqc-Emp) and the vector that yields a solution of problem (QP-eqc-Pop).

We call the matrix containing and , and its population counterpart, which contains and . We assume that are deterministic and known (just like the vector in the Markowitz problem). In our analysis, will be held fixed. (The th column of will contain in general or our estimator of .)

As should be clear from Theorem 2.1, the properties of the entries of the matrix as compared to those of the matrix will be key to our understanding of this question. In what follows, we assume that the vectors are either deterministic or equal to . The extension to linear combinations of a deterministic vector and is straightforward. We also note that in the Gaussian case, we could just assume that the are (deterministic) functions of (because and are independent in this case). On the other hand, the vector is assumed to be deterministic.

Before we proceed, let us mention that after our study was completed, we learned of similar results (restricted to the Markowitz case and not dealing with general quadratic programs with linear equality constraints) by Kan and Smith (2008). We stress the fact that our work was independent of theirs and is more general which is why it is included in the paper.

3.1 Efficient frontier problems

We first study questions concerning the efficient frontier and then turn to information we can get about linear functionals of the empirical weights.

Theorem 3.1

Let us assume that we observe data , for . Here is and . Suppose we estimate with the sample covariance matrix , and with the sample mean . Suppose we wish to solve the problem

| (QP-eqc-Pop) |

where are deterministic, are deterministic and given for and . Assume that we use as a proxy for the previous problem the empirical version with plugged-in parameters. Let us consider the solution of the problem

| (QP-eqc-Emp) |

Now for and , for a given deterministic function . Let us call the corresponding “weight” vector. The plug-in estimate of is . Let us call the optimal solution of the quadratic program obtained under the assumption that is given, but is not and is estimated by . Finally, we assume that .

Then we have

| (2) |

where is random (because is) but is statistically independent of . Also,

The previous theorem means that the cost of not knowing the covariance matrix and estimating it is the apparition of the . In the high-dimensional setting when and are of the same order of magnitude and is large, this terms is approximately . Hence, the theorem quantifies the random matrix intuition that having to estimate the high-dimensional covariance matrix at stake here leads to risk underestimation, by the factor . In other words, using plug-in procedures leads to over-optimistic conclusions in this situation.

We also note that the previous theorem shows that, in the Gaussian setting under study here, the effect of estimating the mean and the covariance on the solution of the quadratic program are “separable”: the effect of the mean estimation is in the oracle term, while the effect of estimating the covariance is in the term. To show risk underestimation, it will therefore be necessary to relate to . We do it in Proposition 3.2 but first give a proof of Theorem 3.1.

Proof of Theorem 3.1 The crux of the proof is the following result, which is well known by statisticians, concerning (essentially) blocks of the inverse of a Wishart matrix: if , that is, is a Wishart matrix with degree of freedoms and covariance , and is , deterministic matrix, then, when ,

We refer to Eaton [(1983), Proposition 8.9, page 312] for a proof, and to Mardia, Kent and Bibby [(1979), pages 70–73] for related results.

Another important remark is the well-known fact that, in the situation we are considering, is and independent of . Finally, it is also well known that if and is a -dimensional deterministic vector, then .

Now . Therefore, since is a function of , we have, by independence of and ,

Therefore,

Because the right-hand side does not depend on , we have established the independence of

Hence, we conclude that

and the two terms are independent. Now the term is the estimate we would get for the solution of problem (QP-eqc-Pop), if were known and were estimated by . In other words, it is the “oracle” solution described above.

3.1.1 Some remarks on the oracle solution

Theorem 3.1 sheds light on the separate effects of mean and covariance estimation on the problem considered above. To understand further the problem of risk estimation, we need to better understand the role the estimation of the mean might play. This is what we do now.

Proposition 3.2.

Suppose that the last column of is . Let us call the dimensional matrix whose th column is , which are known deterministic vectors. Suppose that . Suppose further that , where is the smallest eigenvalue of the matrix .

Further, call and call the canonical basis vectors in . Finally, call .

Then, when , asymptotically,

Let us discuss a little bit this result before we provide a proof. In the asymptotics we have in mind and are considering, and therefore . So if , when the above analysis applies, the impact of the estimation of by will be risk underestimation, just as is the case for the case of the covariance matrix. Here, we can also quantify the impact of this estimation of by : it leads to risk underestimation by the amount .

Proof of Proposition 3.2 Let us write , where . Clearly, , where is . We have, using block notations,

Replacing by its value, we have . By the same token, we can also get that

Our assumption that implies that and . Therefore,

Hence, since ,

Our assumptions guarantee that , and therefore. In other respects, let be a matrix such that and be a matrix such that . Recall that for symmetric matrices, [see, e.g., Weyl’s theorem, Horn and Johnson (1994), page 185]. So in this situation, . Let us now consider the implications of this remark on the difference of and . We claim that . By the first resolvent identity, ; our previous remark implies that and the result follows. Applying the results of this discussion to and , we have

We can now use well-known results concerning inverses of rank-1 perturbation of matrices, namely

This allows us to conclude that

This is the result announced in the theorem and the proof is complete.

We can now combine the results of Theorem 3.1 and Proposition 3.2 to obtain the following corollary.

Corollary 3.3.

The corollary shows that the effects of both covariance and mean estimation are to underestimate the risk, and the empirical frontier is asymptotically deterministic.

3.2 On the optimal weights

Our matrix characterization of the empirical optimal weights (Lemma 2.2) allows us to give a precise characterization of the statistical properties of linear functionals of these weights. We give here some exact results, concerning distributions and expectations of those functionals. A longer discussion, including robustness and more detailed bias issues can be found in Section 5.

Proposition 3.4.

Assume that the assumptions of Theorem 3.1 hold and in particular are i.i.d. . Let be a fixed -dimensional vector. Let us call the matrix whose first columns are those of . Let and be a matrix with distribution (conditional on ). Then,

In particular,

We note, somewhat heuristically, that when is estimated by , since , , when , and are all large (we refer again to Section 5 for a more precise statement). Hence is a not a consistent estimator of . As we will see in Section 5.2 and as can be expected from the previous proposition, this will also imply bias for linear combinations of empirical optimal weights. We will show in particular that returns are overestimated when using as an estimator for .

Another interesting aspect of the previous proposition is that it allows us to understand the fluctuation behavior of when is large: as a matter of fact, the limiting fluctuation behavior of the entries of a (fixed-dimensional) Wishart matrix with large number of degrees of freedom is well known [see, e.g., Anderson (2003), Theorem 3.4.4, page 87] and the -method can be applied to get the information—conditional on .

For instance, if we assume that, conditional on , the matrix converges to a matrix , which possibly depends on , we see that calling the last column , is asymptotically normal (all statements are conditional on ), if goes to infinity when and go to infinity. Furthermore we know the limiting covariance of (after scaling by ), using Theorem 3.4.4 in Anderson (2003). Let us call it and let us call the limit of —which we assume exists.

If we assume that is not 0, Slutsky’s lemma and the -method give us through simple computations that

where .

We know the distribution of , so we could get (limiting) unconditional results for . This is not hard but a bit tedious if we want explicit expressions, and because our focus is mostly on first-order properties in this paper, we do not state the result.

Proof of Proposition 3.4 The proof follows from the representation we gave in Lemma 2.2, that is,

and the fact that, by the same arguments as before, conditional on ,

We conclude that

This shows the fist part of the proposition.

The second part follows from the following observation. Suppose the matrix is . If and are -dimensional, orthogonal vectors, let us consider

We can, of course, write , where are i.i.d. . In other respects, and are clearly independent normal random variables, since their covariance is , and they are normal. So

because the quantity whose expectation we are taking is a linear combination of mean 0 independent normal random variables. Hence, also,

Now, when is not orthogonal to , we write , where is orthogonal to . We immediately deduce that in general,

Furthermore, when is , because we can write , where , we finally have

In the case of interest to us, we have , and . Applying the previous formula gives us the second part of the proposition.

We now turn to the question of understanding the robustness properties of the Gaussian results we just obtained. We will do so by studying the same problems under more general distributional assumptions, and specifically we will now assume that the observations are elliptically distributed.

4 Solutions of quadratic programs when the data is elliptically distributed

In Section 3, we studied the properties of the “plug-in” solution of problem (QP-eqc-Pop) under the assumption that the data was normally distributed. While this allowed us to shed light on the statistical properties of the solution of problem (QP-eqc-Emp), it is naturally extremely important to understand how robust the results are to our normality assumptions.

In this section, we will consider elliptical models, that is, models such that the data can be expressed as

where is a random variable and are i.i.d. entries. and are assumed to be independent, and to lift the indeterminacy between and , we assume that . Under this assumption, we clearly have . We note that this is not the standard definition of elliptical models, which generally replaces with a vector uniformly distributed on the sphere in , but it captures the essence of the problem. We refer the interested reader to Anderson (2003) and Fang, Kotz and Ng (1990) for extensive discussions of elliptical distributions.

Our motivation for undertaking this study comes also from the fact that for certain types of data, such as financial data, it is sometimes argued that elliptical models are more reasonable than Gaussian ones, for instance, because they can capture nontrivial tail dependence [see Frahm and Jaekel (2005) where such models are advocated for high-dimensional modelization of financial returns, Meucci (2005) for a discussion of their relevance for certain financial markets, Biroli, Bouchaud and Potters (2007) for modelization considerations quite similar to Frahm and Jaekel (2005) and McNeil, Frey and Embrechts (2005) for a thorough discussion of tail dependence]. From a theoretical standpoint, considering elliptical models will also help in several other ways: the results will yield alternative proofs to some of the results we obtained in the Gaussian case, they will allow us to deal with some situations where the data are not independent and they will also allow us to understand the properties of the bootstrap.

We also want to point out that elliptical distributions allow us to not fall into the geometric “trap” of standard random matrix models highlighted in El Karoui (2009a): the fact that data vectors drawn from standard random matrix models are essentially assumed to be almost orthogonal to one another and that their norm (after renormalization by ) is almost constant. In a sense, studying elliptical models will allow us to understand what is the impact of the implicit geometric assumptions made about the data when assuming normality. (We purposely do so not under minimal assumptions but under assumptions that capture the essence of the problem while allowing us to show in the proofs the key stochastic phenomena at play.) This part of the article can therefore be viewed as a continuation of the investigation we started in El Karoui (2009a) where we showed a lack of robustness of random matrix models (contradicting claims of “universality”) by thoroughly investigating limiting spectral distribution properties of high-dimensional covariance matrices when the data is drawn according to elliptical models and generalizations. We show here that the theoretical problems we highlighted in El Karoui (2009a) have important practical consequences. [For more references on elliptical models in a random matrix context, we refer the reader to El Karoui (2009a) where an extended bibliography can be found.]

We now turn to the problem of understanding the solution of problem (QP-eqc-Emp) in the setting where the data is elliptically distributed. We will limit ourselves to the case where the matrix is full of known and deterministic vectors, except possibly for the sample mean. In this section we restrict ourselves to convergence in probability results. It is clear from Section 2 that to tackle the problems we are considering we need to understand at least three types of quantities: for a deterministic with unit norm, and .

Here is a brief overview of our findings. When we consider elliptical models, our results say that roughly speaking, under certain assumptions given precisely later:

-

[3.]

-

1.

, where satisfies, if is the limit law of the empirical distribution of the and , .

-

2.

If , .

-

3.

If , .

All these convergence results are to be understood in probability. They naturally allow us—under certain conditions on the population parameters—to conclude about the convergence in probability of the matrix . The results mentioned above are stated in all details in Theorems 4.1 and 4.6.

In the situation where are i.i.d., the results above hold when have a second moment and they do not put too much mass near 0. This is interesting in practice because it tells us that our results hold for heavy-tailed data, which are of particular interest in some financial applications.

The bootstrap situation corresponds basically to being Poisson(1), which we denote by . Also in the statement above for , one should replace by in the bootstrap case. This is explained in Theorem 4.12 and Section 4.4.4. Finally, in the case of Gaussian data with “temporal” correlation, that is, when the data can be written in matrix form , where is not diagonal (and is an -dimensional vector with only 1’s in its entries), one should replace by the limiting spectral distribution of . The question of convergence of is then more involved. We refer to Proposition 4.8 for details about this situation.

Though we are taking a fundamentally random matrix theoretic approach, our presentation purposely avoids borrowing too many techniques from random matrix theory in the hope of making clear(er) the phenomena that yield the results we will obtain. A more general but considerably more technically complicated (for non-specialists of random matrix theory) approach is being developed in our study of a connected problem and will appear in another paper.

This section is divided into four subsections. The first two are devoted to the main technical issues arising in the study of the problem when the data is elliptically distributed. The third discusses the impact of correlation between observations when the data is Gaussian, as it can be recast as a variant of elliptical problems. The last subsection discusses questions related to the (nonparametric) bootstrap.

4.1 On quadratic forms of the type

The focus of this subsection is on understanding statistics of the type , where is a deterministic vector. We will prove the following important theorem.

Theorem 4.1

Suppose we observe observations , where has the form , with and is independent of . is deterministic and .

We call and assume that .

We use the notation and assume that the empirical distribution, , of converges weakly in probability to a deterministic limit . We also assume that for all .

If is the th largest , we assume that we can find a random variable and positive real numbers and such that

| (Assumption-BB) |

Under these assumptions, if is a (sequence of) deterministic vector,

where satisfies

| (4) |

A few comments are in order before we turn to the proof. First, the assumption that for all could be dispensed of, as long as all assumptions stated above hold when is understood to denote the number of nonzero ’s. Second, (Assumption-BB) concerning and will generally hold as soon as does not put too much mass at 0, the only problem-specific question remaining being how much mass is put at 0 by compared to , the limit of .

In particular, in the case where the ’s are i.i.d., if there exists and such that , and if is the empirical distribution of the ’s, if , we see, using, for example, Lemma 2.2 in van der Vaart (1998), that

So picking will guarantee that we have, if in probability, and, of course, . Hence, in checking whether the theorem applies, we just need to see whether stays bounded away from 1.

In the simpler case when all the are bounded away from 0, the conditions on and apply directly by taking . Finally, let us say that (Assumption-BB) is needed in the proof to guarantee that the smallest eigenvalues of stay bounded away from 0 with high-probability.

We now briefly compare the Gaussian and elliptical cases. A simple convexity argument [relying on the fact that is a convex function of for and Jensen’s inequality] shows that, if is the mean of ,

In the case of Gaussian data, , that is, it is a point mass at 1 and we have . In other respects, for to have covariance , we need . When the ’s are i.i.d., with having distribution , , and we know that in probability. Therefore, in the class of elliptical distributions considered here, risk underestimation, which is essentially measured by (see Theorem 2.1 and Section 5) will be least severe in the Gaussian case. In other words, the Gaussian results lead to over-optimistic conclusions (in terms of proximity between sample and population solutions of the quadratic programs we are considering) within the class of elliptical distributions.

We go back to these questions in more detail in Section 5 and now turn to the proof of Theorem 4.1. The proof could be carried out in at least two ways. We take one that is not standard but we feel best explains the phenomenon that is occurring.

Proof of Theorem 4.1 The proof is easier to carry out when we write the problem in matrix form. Because we focus on , we can assume without loss of generality (wlog) that . Let us consider the data matrix whose th row is . Similarly, we denote by the data matrix whose th row is . Let us call the diagonal matrix with th diagonal entry and , where is an -dimensional vector whose entries are all equal to 1. Note that . With these notations, we have, since we assume that ,

Therefore, , and

Let us call the matrix . Note that is a rank matrix with probability 1, if we assume that (recall that all the entries of are nonzero). Hence, is invertible with probability 1. Therefore,

Finally, we have

where is a vector of norm 1.

We now make all of our statements conditional on . Because of the independence of and , we can therefore treat the ’s as if they were constant and the ’s as i.i.d. random variables. is now assumed to be in the set of matrices , defined just below, for which we have control of the smallest eigenvalue of . In the steps that follow that are conditional on , we therefore consider that we control the smallest eigenvalue of . We note that if is in , is lower bounded. Because is a function of the ’s and hence of , we write all the results conditionally on , but the reader should keep in mind that this conditioning constrains also the possible values of .

The set .

In Lemma B.1 in the Appendix, we prove the following result: when is such that , if [see (Assumption-BB) and Lemma B.1 for definitions] and is the smallest eigenvalue of , we have, if denotes probability conditional on ,

Let us call the set of matrices such that and . Under (Assumption-BB), for a bounded away from 0 (e.g., , since we need a bound on that holds with probability going to 1), . In other respects, if ,

Getting results conditionally on .

If is an orthogonal matrix, , because is full of i.i.d. random variables and is therefore invariant (in law) by left and right rotation. Therefore the eigenvalues and eigenvectors of are independent and its matrix of eigenvectors is uniformly (i.e., Haar) distributed on the orthogonal group [see also Chikuse (2003), page 40, equation (2.4.4)]. Let us write a spectral decomposition of

We know that a.s. for all , so

We claim that

To see this, note that because is uniformly distributed on the unit sphere when (the matrix containing the ) is Haar distributed on the orthogonal group. Hence, given the independence between and ,

Now let us call the vector with , and the vector with th entry . Clearly, since , . By symmetry it is clear that and if . Further, since the matrix containing the vectors is Haar distributed on the orthogonal group, we can assume without loss of generality that for all the computations at stake. As a matter of fact, if is an orthogonal matrix such that , then where the matrix is again Haar distributed on the orthogonal group.

So from now on, we assume (without loss of generality) that , and we therefore simply need to understand the correlation between and . Now, the first row of an orthogonal matrix uniformly distributed on the orthogonal group is a unit vector uniformly distributed on the unit sphere, because if is Haar distributed, so is . We now recall the fact that a vector uniformly distributed on the unit sphere, can be generated by drawing at random a random vector and normalizing it. In other words, if , .

So our task has now been considerably simplified, and it consists in understanding the covariance between 2 random variables, and such that, if are i.i.d. ,

Now, by symmetry, for all and . In other words,

We can therefore conclude that

Hence, . On the other hand,

since , and , for [see, e.g., Mardia, Kent and Bibby (1979), page 487]. Applying these results with yields the above result as soon as , by using the fact that . We therefore have

Since, for instance by symmetry, , and , we conclude that

We have therefore established the fact that

On the other hand, since , we have

Now using the (standard) fact that, for symmetric matrices , if is the largest singular value of ,

[it can easily be proved using, for instance, Theorems 5.6.6 and 5.6.9 in Horn and Johnson (1994), or Geršgorin’s theorem (Theorem 6.1.1 in the same reference)] we have

The first term in the previous bound comes from the contribution of the diagonal and the second term is the sum over the off-diagonal elements on a given row of the upper-bound we had on each such element, that is, for some .

Let us now return to our initial question which was to show that the conditional variance of interest to us was going to zero. Recall that is a vector whose th entry is . Since

and , we have, for a constant, and if denotes the operator norm (or largest singular value) of the matrix ,

Now given the assumptions we made on , according to the arguments given at the beginning of this proof and Lemma B.1 in the Appendix, , where , with high ()-probability. So we conclude that all the ’s are bounded away [uniformly for in and with high ()-probability] from 0, and when this is the case,

Therefore,

Let us now show that this implies convergence in probability to 0 (conditional on only) of . Let us call . For to be determined later, we have

On the other hand,

Because is a function of the ’s and ,

But when , under our assumptions and their consequences on the ’s mentioned above [i.e., with high probability], we have , so taking , we have and of course, . Hence, for any ,

Let us now turn to the question of identifying the limit.

About .

The Stieltjes transform of the spectral distribution of is

The quantity is therefore and we are interested in its limit, if it exists, which would correspond to .

Recall the Marčenko–Pastur equation, from Marčenko and Pastur (1967), Wachter (1978) and Silverstein (1995): if is has i.i.d. entries with mean 0 and variance 1 and is positive semidefinite, has limiting spectral distribution and is independent of , if , and if is the Stieltjes transform of the spectral distribution of , then tends (in probability) to for all in and satisfies

| (5) |

Note that, if , we have

Therefore, according to Marčenko and Pastur (1967), Wachter (1978) and Silverstein (1995), we know that converges for to a nonrandom quantity , in probability. Note that satisfies, in light of equation (5),

Here, because we know using our assumptions (see the end of the proof) that are bounded away from 0 with probability going to 1, we can also conclude that with probability going to 1, because of the weak convergence (in probability) of spectral distributions that pointwise convergence of Stieltjes transforms implies (as a test function, we can use a function that coincides with except in a interval near 0 where we are guaranteed that there are no eigenvalues asymptotically). We also know that is continuous (and actually analytic) at in this situation since the is the Stieltjes transform of a measure who has support bounded away from 0. So the previous equation holds for , and we have

Multiplying both sides by , we get, after we recall that is a probability measure,

Calling , we have the result we announced, conditionally on . Now, here is the limiting spectral distribution of , but because this matrix is a rank one perturbation of , these two matrices have the same limiting spectral distribution. This concludes this part of the proof.

Getting results unconditionally on .

All the statements above were made conditional on . If we can show that our probability bounds and our characterization of the limit hold uniformly in , we will have an unconditional statement, as we seek.

The fact that the limit does not depend on is essentially obvious from its description: all that matters is the limiting spectral distribution, which is the same for all . Let us consider the question of uniform probability bounds. All we need to do is show that we control uniformly in . At this point, it is helpful to recall that can be viewed as a function of .

Recall also that if ,

Hence, when , if , , where tends to 0 as tends to infinity. In other words, we have now established that if , and , for any ,

Using the fact that , we conclude that as tends to infinity for any and the proof is complete.

As a consequence of Theorem 4.1, we have the following practically useful result.

Lemma 4.2

We assume that the assumptions of Theorem 4.1 hold and that is such that is not .

Suppose that and are deterministic vectors such that

are bounded away from 0. Then under the assumptions of Theorem 4.1,

In other respects, suppose that , while and stay bounded away from . Then, under the assumptions of Theorem 4.1,

The proof of the first part of the lemma is an immediate consequence of Theorem 4.1, after writing

For the proof of the second part, we note that Theorem 4.1 implies that

Note that since for , is assumed to stay bounded, the same is true of , where . Now we write

Our previous remark and the assumption of boundedness of implies that, when ,

4.2 On quadratic forms involving and

As is clear from the solutions of problems (QP-eqc) and (QP-eqc-Emp), when appears in the matrix , its influence on the solution of our quadratic program will manifest itself in the form of quantities of the type and . It is therefore important that we get a good understanding of those quantities.

Compared to the Gaussian case, in the elliptical case, is not independent of anymore, which generates some complications. They are fully addressed in Theorem 4.6, but as a stepping stone to that result (the main of this subsection), we need the following theorem, which essentially takes care of the problem of understanding for the class of elliptical distributions we consider when the population mean is 0.

Theorem 4.3

Suppose is an matrix whose rows are the vectors , which are i.i.d. .

Suppose is a diagonal matrix whose th entry is , which is possibly random and is independent of . Call . We assume that for all and

| (Assumption-BLa) |

If is the th largest , we assume that we can find a random variable and positive real numbers and such that

| (Assumption-BB) |

Let us call and . We assume that . We call

Then we have

If the data matrix is written , and if is the vector of column means of , and if is the sample covariance matrix computed from , we have

Some comments on this theorem are in order. First, is unchanged if we rescale all the ’s by the same constant. So it appears we could assume that they are all less than 1, for instance, and dispense entirely with (Assumption-BLa). However, that would potentially violate the conditions of (Assumption-BB) which appear to guarantee that has variance going to zero. We also note that because the ’s have a continuous distribution and we know that all the ’s are different from 0, the existence of is guaranteed with probability 1.

Some practical clarifications are also in order concerning the condition

When the ’s are i.i.d., this condition is satisfied (almost surely and hence in probability) if for, instance, the ’s have finite second moment according to the Marcinkiewicz–Zygmund law of large numbers [see Chow and Teicher (1997), page 125]. This is very interesting from a practical standpoint as it basically means that we only require our random variables to have a second moment for the theorem to hold. We note that if there were no variance, the premises of the problem would be essentially flawed (after all the quadratic form we are optimizing involves a proxy for the population covariance, and, in the absence of a second moment for the ’s, the population covariance would not exist), and hence we require minimal conditions from the point of view of the practical problem at stake.

Finally, and remarkably, the limit of does not depend on the empirical distribution of the ’s. In particular, in the class of elliptical distributions (satisfying the assumptions of Theorem 4.3), the limit of is always the same: .

We now turn to proving Theorem 4.3. The proof will be facilitated by the following lemma, which essentially gives us .

Lemma 4.4

Let be an random matrix, with with, for instance, independent rows, . Assume that have symmetric distributions, that is, . Let be an diagonal matrix with possibly random entries. Let be a random projection matrix. is assumed to be independent of and and are assumed to be such that exists with probability 1. Then,

In particular, the result applies when are normally distributed, and is such that (Assumption-BB) holds, and is defined with probability one. {pf*}Proof of lemma 4.4 Let us note that . Now, conditional on , . However, , if . As a matter of fact,

Hence, conditional on , . Now is an orthogonal projection matrix, , so all its entries are less than 1 in absolute value, the operator norm of . In particular, all the entries have an expectation. Since, if , has a symmetric distribution (conditional on ), we conclude that

Note that the same arguments would apply if were replaced by , so we really have

Therefore,

since has rank and is a projection matrix.

The same results hold when we take expectations over by similar arguments.

To prove Theorem 4.3, all we have to do (in light of Lemma 4.4) is to show that we control the variance of

We are going to do this now by using rank 1 perturbation arguments, in connection with the Efron–Stein inequality. {pf*}Proof of Theorem 4.3 As before, we first work conditionally on . We assume until further notice that , a set of matrices which is defined at the end of the proof, will have measure going to 1 asymptotically, and is such that all the technical issues appearing in the proof can be taken care of. (The arguments are not circular.)

We will use the notation

Note that is symmetric and positive semi-definite. Naturally, in matrix form we can write and , where is the same matrix as , except that . Our aim is to approximate

by a random variable involving only , that is, not involving . Using classic matrix perturbation results [see Horn and Johnson (1990), page 19], we have

Of course, if is the th canonical basis vector in ,

Let us now call and . We have

| (6) |

Similarly,

This is, in some sense, the key expansion in this proof. Now let us call and . We have

Now let us call . Clearly, does not depend on . Now, it is easily verified that

We finally conclude that

| (8) |

We now recall the Efron–Stein inequality, as formulated in Theorem 9 of Lugosi (2006): if , where the ’s are independent, and is a measurable function of , then

In particular, for us, it means that

If we now use equation (8) and the fact that , we have

Moreover, conditional on (and since all our arguments at this point are made conditional on ), is when the ’s are , because . Therefore,

Almost by definition, we have , since the vector has norm 1 and is a projection matrix (recall that and ). So we would be done if we had uniform control on . Let us now go around this difficulty.

Regularization interlude.

Let us consider, for , , where . Clearly, , because in the positive-semidefinite ordering. In other respects, the decomposition in equation (8) is still valid if we replace by and by everywhere. However, . We therefore have

So applying the previous analysis and using the fact that , we conclude that

So under our assumptions, can be approximated, in probability, at least conditionally on , by . If we write the singular value decomposition of , where , we have , , and therefore

To get the inequality above, we used the fact that the are orthonormal in , and can therefore be completed to form an orthonormal basis of this vector space. The quantities are naturally the coefficients of in this basis, and we know that their sum of squares should be the squared norm of , which is .

Let us now call the set of matrices such that and . Under our assumptions, for a bounded away from 0 (e.g., ), . Let us pick such a . If , according to Lemma B.1 and the proof of Theorem 4.1, if denotes probability conditional on ,

Hence, when , we can find, for any , an ,

where, as , for fixed .

On the other hand, our conditional variance computations have established that, for any , converges in probability (conditional on ) to 0 if tends to 0. We note that and that the same is true for . Therefore, and goes to zero, since

In other words, we also have, if , for any ,

Hence, if and , goes to zero as goes to infinity, and we conclude that, since ,

Deconditioning on .

Let us call the set of matrices such that . Our previous computations clearly show that we can find a function , with as , such that, for any , when , , and hence we have the “uniform bound,” if ,

Now under our assumptions, goes to 1 for any given , so we conclude, using the fact that

that

This last statement is now understood of course unconditionally on and this proves the first part of the theorem.

Proof of the second part of the theorem.

We now focus on the part of the theorem. Let us call . Then, . Therefore,

Hence,

Since in probability with , we have the result announced in the theorem.

Now that we have proved Theorem 4.3, we need to turn to results that will allow us to handle the case of nonzero population mean, as well as questions such as the convergence of , for deterministic .

4.2.1 On quantities of the type

Recall that the key quantity in the solution of problem (QP-eqc-Emp), the problem of main interest in this paper, is of the form . Therefore, it is important for us to understand quantities of the type

for a fixed vector . At this point, we focus on the particular case where . To do so, we will need to study, if ,

for a fixed vector . As it turns out, this random variable goes to zero in probability when for instance .

Theorem 4.5

Suppose is a deterministic vector, with . Suppose the assumptions stated in Theorem 4.3 hold and also that

| (Assumption-BLb) |

Consider

where . Then

Before giving the proof, we note that if the ’s are i.i.d. and have a second moment, the “extra” condition on introduced in this theorem (as compared to Theorem 4.3) is clearly satisfied by the law of large numbers.

Proof of Theorem 4.5 The proof is quite similar to the proof of Theorem 4.3 above. We start by conditioning on .

Let us call the quantity obtained when we replace by in the definition of . Note that since is symmetric, , conditionally on , by arguments similar to those given in the proof of Lemma 4.4. Now clearly has an expectation (conditional on ), because , for , so . Now recall equation (6): with the notations used there,

Let us now call , and . Clearly, if is the random variable obtained by excluding from the computation of (e.g., by replacing by 0), we have

We remark that and recall that . Using the fact that , and the remarks we made in the proof of Theorem 4.3, we get that , , where and . We also have

Hence, simply using the fact that , we get

We conclude by the Efron–Stein inequality that, when is such that , for any ,

As before, let us call the set of matrices such that and . Recall that under our assumptions, for bounded away from 0 (e.g., ), .

As we saw before, when , is bounded with high-probability (conditional on ), so we conclude that, for any , we can find a such that

We also notice that conditionally on , and hence, . We recall that , and since

we conclude that with high-probability (conditional on ), for any , and finally,

Now along the same lines as what was done in the proof of Theorem 4.3, we can make all these probability bounds uniform in when is in a set of matrices such as and when we also have bounds on and . Under our assumptions, the set of for which these conditions hold has measure going to 1, so we can finally conclude—along the same lines (omitted here) as in the proof of Theorem 4.3—that, unconditionally on ,

After these preliminaries, we can finally state the theorem of main interest. Recall that under the assumptions of Theorem 4.1, if is deterministic,

where is defined in equation (4).

Theorem 4.6

Suppose that , where are i.i.d. and are random variables, independent of . Let be a deterministic vector. Suppose that has a finite nonzero limit, and that .

We call . We assume that for all as well as

| (Assumption-BL) |

If is the th largest , we assume that we can find a random variable and positive real numbers and such that

| (Assumption-BB) |

We also assume that the empirical distribution of ’s converges weakly in probability to a deterministic limit .

We call the diagonal matrix with , the matrix whose th row is , and . Finally, we use the notation , .

Then, we have, for defined as in equation (4),

| (9) |

the second statement holding if, for instance, and are such that the first set of conditions in Lemma 4.2 are met.

Also,

| (10) |

and we recall that and .

To be able to exploit equation (10) in practice, we make the following remarks. We can consider three cases, having to do with the size of :

-

[3.]

-

1.

If , then, .

-

2.

If , then .

-

3.

Finally, if stays bounded away from 0 and infinity,

A noticeable feature of these results is that the “extra bias” , which comes essentially from mis-estimation of , is constant within the class of elliptical distributions considered here. This should be contrasted with the “scaling,” , which strongly depends on the empirical distribution of the ’s.

We now give a brief proof of Theorem 4.6. {pf*}Proof of Theorem 4.6 We first note that in the notation of Theorem 4.3. Also, . Finally,

Proof of equation (10). By writing , we clearly have

We have already seen in Theorem 4.3 that the third term tends to . On the other hand, half of the middle term is equal to

Since , we have

and we deduce the result of equation (10). We now remark that is equal to the quantity in Theorem 4.3. The fact that follows from applying Theorem 4.5 with .

4.3 On the effect of correlation between observations

It is clear that in financial practice and other applied settings, the assumption that the returns (or observed data vectors) are independent is often questionable. So for quadratic programs with linear equality constraints (including the Markowitz problem but also going beyond it), it is natural to ask what is the impact of correlation in our observations on the empirical solution of the problem. In our notation, this means that the vectors and are correlated; we refer to this situation as the correlated case or as the case of temporal correlation.

Our work on the elliptical case comes in handy here and allows us to also draw conclusions concerning the correlated case. We consider a particular model, namely we assume that the data matrix is given by

where is a deterministic but not necessarily a diagonal matrix, and is a matrix with i.i.d. entries. We assume throughout that is full rank. The model we consider now is more general than the one we looked at before, since if , we get the i.i.d. Gaussian case, and if is diagonal we are back in an “elliptical” case (where the ellipticity parameters are assumed to be deterministic, which amounts to doing computations conditional on ). But when is not diagonal, and might be correlated. [In all the situations where is deterministic, the marginal distribution of is , where is the norm of the th row of .]

Because we want to focus here on robustness questions arising when going from independent Gaussian random variables to correlated ones, we will assume throughout that is deterministic. (Allowing to be random simply requires some minor technical modifications but would make the exposition a bit less clear.) Our main results in this subsection can be interpreted as saying that that the Gaussian analysis of Section 3, carried out in the setting of independent observations, is not robust against these independence assumptions. The results change quite significantly when the vectors of observations are correlated.

In general, we write the singular value decomposition of the matrix as [see Horn and Johnson (1990), page 414], where and are orthogonal, and is diagonal. Therefore, , and

So we are almost back in the elliptical case. The key difference now is that what will matter in our analysis are not the diagonal entries of , but rather its eigenvalues (see Proposition 4.7). Also, we will see (in Proposition 4.8) that the results change quite significantly when we look at quantities like .

4.3.1 On quadratic forms involving

As a counterpart to Theorem 4.1, we have the following proposition.

Proposition 4.7.

Suppose the data matrix (whose th row is the th vector of observations) can be written as

where is a deterministic but not necessarily diagonal matrix. Suppose that the eigenvalues of satisfy (Assumption-BB) with a deterministic and that the spectral distribution of converges weakly to a probability distribution . Suppose also that . Call the classical sample covariance matrix, that is,

Then, if is a deterministic vector, we have

where satisfies, if is the limiting spectral distribution

The proposition shows that Theorem 4.1 essentially applies again; however, now what matters, unsurprisingly, are the singular values of and not its diagonal entries. The proof of Proposition 4.7, or rather the adjustments needed to make the proof of Theorem 4.1 go through, are given in the Appendix, Section C.1.

4.3.2 On quadratic forms involving and

This is the situation where the results are most different from that of the uncorrelated case. Once again, here we will be content to just state the results; a detailed justification of our claims is in the Appendix, Section C.2.

As before, the most complicated aspect of the problem is to understand quantities of the type , in the situation where . In this setting, we have the following result.

Proposition 4.8.

Suppose the data matrix is such that, for an matrix with i.i.d. entries, and a deterministic matrix,

We assume that (Assumption-BB) holds for the eigenvalues of , for a deterministic sequence . We write the singular value decomposition of as .

We call and , that is, the sample mean of the columns of . We denote by the diagonal elements of , and . We also call

If we call , and , we have, if and ,

where

Further,

Essentially the previous proposition tells us that when dealing with correlated variables, the new replaces the old . We note that there are no inconsistencies with our previous results as and in the “elliptical” case (i.e., diagonal), , so the previous proposition is consistent with the results we have obtained in the elliptical case. We also remark that , since is orthogonal.

Finally, in the case where the ’s have a limiting spectral distribution and satisfy (Assumption-BB), further computations show that . However, this does not help (in general) in getting a simpler expression for .

4.4 On the bootstrap

An interesting aspect of the analysis of elliptical models is that it also shed lights on the properties of the bootstrap in this context. As a matter of fact, the nonparametric bootstrap yields covariance matrices that have a structure similar to those computed from elliptical distributions: if we call the diagonal matrix whose th diagonal entry is the number of times observation appears in our bootstrap sample, we have, if is the bootstrapped covariance matrix,

where is our original data matrix, and is the sample mean of our bootstrap sample, which can also be written . Unless otherwise noted, we assume in the discussion that follows that the population mean is 0. Since the covariance matrix is shift-invariant, we can make this assumption without loss of generality. We call

As we will see shortly, understanding the properties of boils down to understanding those of so we will focus on this slightly more convenient object in this short discussion.

We note that if is Gaussian, can be thought of as a “covariance matrix” computed from the elliptical data . The same remark applies when is elliptical, that is, for us, : all we need to do is change the “ellipticity parameter” to . The same remark is also applicable to the case of correlated observations, that is, , where is not diagonal anymore. Studying the bootstrap properties of such a model is the same as studying that of the model where we replace by . We therefore would like to apply directly all the results we have obtained above in our study of elliptical models to better understand the bootstrap. For quantities of the form , we will see that we can essentially do it, but differences will appear when dealing with , which yields statistics that are not exactly analogous to corresponding statistics appearing in the elliptical case.

Our focus will be on bias properties of bootstrapped replications, so we will aim for convergence in probability results and not fluctuation behavior. Our overall strategy here is to show convergence in probability of the quantities we are interested in as functions of both the ’s and ’s. We will derive the convergence properties of our bootstrapped statistics by then conditioning on the data and arguing that with high probability (over the ’s), this does not change the results much. We first give some needed background on the bootstrap in Sections 4.4.1 and 4.4.2, then turn to properties of quantities like (in Section 4.4.3) and finally study (in Section 4.4.4), where we will see (in Proposition 4.13) some key differences with the elliptical case. We conclude this subsection with a brief discussion of the parametric bootstrap and the conclusions that can be reached about it through our results.

4.4.1 A remark on needed convergence properties

Making statements about bootstrapped statistics requires us to make statements that are conditional on the observed data. This is not a trivial matter for the statistics we deal with since they cannot be easily described in terms of simple formulas involving the original observations. However, we can take a roundabout way: by showing joint convergence in probability (joint here refers to the “new” data being the vectors of bootstrapped weights and observations), we can obtain interesting conclusions conditional on the data. Though this is not difficult to show, we give full arguments here for the sake of completeness.

We will look at our statistics as functions of the number of times an observation appears in the sample and also, of course, of our observations. In other words, the original statistic, can be written

and, the bootstrapped version is, if observation appears times in the bootstrap sample,

The following simple proposition is used repeatedly in our bootstrap work.

Proposition 4.9.

Let us consider a statistic , where is the number of times appears in our sample. Suppose that the vector of weights, , is independent of the data matrix . Denote by the joint probability distribution of the ’s, the joint probability distribution of the ’s and the probability distribution of .

Suppose we have established that tends in -probability to , a deterministic object, as .

Then we have, with -probability going to 1 as ,

In other words, calling , for all , if , as tends to infinity.

In the case where the weights are obtained by standard bootstrapping, is multinomial(). Then, has the distribution of the usual bootstrap quantity . We will focus on this case more specifically later. {pf*}Proof of Proposition 4.9 The proof and the statement are almost obvious but we include them for the sake of completeness. Let us call and . By assumption, in probability. Hence,

Let us call . Clearly, and, so for any ,

We now investigate the case of the classical bootstrap, that is, the situation in which is multinomial.

4.4.2 Empirical distribution of bootstrap weights

As we saw in Theorem 4.1, the empirical distribution of the ellipticity parameters affect crucially statistics of the type , so to understand the effect of bootstrapping, we need to understand the empirical distribution of the bootstrap weights. This question has surely been investigated, but we did not find a good reference, so we provide the result and a simple proof for the convenience of the reader.

Proposition 4.10.

Let the vector be distributed according to a multinomial distribution. Call the empirical distribution of the vector . Then

where is the Poisson distribution with parameter 1.

Let us first start by an elementary remark: suppose are i.i.d. with distribution . Call . Then

This result is a simple application of Bayes’s rule and the fact that .

Let us now show that if is bounded and continuous, and if ,

To do so, we note that and therefore its marginal distribution is asymptotically . Therefore,

Now all we need to do is therefore to show that goes to zero. Clearly, by independence of the ’s,

because is bounded. But our first remark implies that

Now,

Since has distribution, . Hence,

and the result is established.

We will also need later to use on the following (coarse) fact:

Fact 4.11.

Let the vector be distributed according to a multinomial distribution. Then

In particular, this probability goes to 0 faster than any , .

The proof of the fact is elementary, and relies on the representation used above for the vector , a simple union bound, the fact that and the fact that which is easy to see by writing explicitly the probability we are trying to compute.

With these preliminaries behind us, we are now ready to tackle the question of understanding the (first-order) bootstrap properties of the statistics appearing in the study of quadratic programs with linear equality constraints.

4.4.3 On inverse covariance matrices computed from bootstrapped data

Our aim in this subsubsection and the next is to find analogs to Theorems 4.1 and Theorems 4.6. Our first result along these lines is an analog of Theorem 4.1.

We present the result in the case of Gaussian data, where we can get a somewhat explicit expression for the quantity we care about, and discuss possible extensions below.

Theorem 4.12

Suppose we observe i.i.d. observations , where are i.i.d. in with distribution . Call and assume that . Call the covariance matrix computed after bootstrapping the ’s. Call the joint distribution of the ’s.

If is a (sequence of) deterministic vectors, then conditional on , with high probability,

where satisfies, if is a distribution

| (11) |

As before, we call the law of the bootstrap weights [i.e., multinomial] and . Without loss of generality, we can assume that . Let us call the diagonal matrix containing the bootstrap weights. We have . Also, it is true that

Since , we also have

Because is of the form under our assumptions, we see that

| (12) |

If we call , we have because the sum of the bootstrap weights is . Therefore, . Also, (like ) is a projection matrix and a rank 1 perturbation of .

The situation is therefore very similar to the question we studied in Theorem 4.1, except that is replaced by . All the arguments given there hold provided we can show that (Assumption-BB) is satisfied for the bootstrap weights in the situation we have here.

Now let us call the number of nonzero bootstrap weights. In the notation of Theorem 4.1, and . So clearly, . So is a possibility. Also, in probability, so has a limit in probability and this limit is bounded away from 1 because of our assumption that . Finally, we can pick .

So the proof of Theorem 4.1 applies [it is easy to see here that the assumption that can be dispensed of, because we know that the nonzero ’s are large enough for our arguments to go through, and there are enough of them that we do not have problems (at least in probability) with not being defined], and we have the announced result.

The previous theorems settled the question of understanding the impact of the nonparametric bootstrap on statistics of the form in the situation where the original data were Gaussian. A similar analysis could be carried out in the case of elliptical data, when we assume that the “ellipticity” parameters, , are such (Assumption-BB) is satisfied for the “new weights” . The result would then depend on the limiting distribution of (if it exists), where is the bootstrap weight given to observation .

4.4.4 Bootstrap analogs of Theorems 4.5 and 4.6

An important piece of our analysis of quadratic programs with linear equality constraints when the data are elliptically distributed was the study of quadratic forms of the type . It is natural to ask what happens to them when we bootstrap the data. In the elliptical case, we saw that the key statistic was of the form, when and ,

However, in the bootstrap case, if is the diagonal matrix containing the bootstrap weights, we have , but , so the key statistic is going to be of the form

This creates complications because the matrix is not a projection matrix, and hence some of our previous analysis cannot be applied directly. However, this statistic can be rewritten, if we denote , as

where is now a projection matrix. As before its off-diagonal elements have mean 0 (conditional on ), but now we also need to understand and not only . A detailed analysis of the former quantity is done in Appendix C.3.