A note on nonparametric testing for Gaussian innovations in AR-ARCH models

Abstract

In this paper we consider autoregressive models with conditional autoregressive variance, including the case of homoscedastic AR-models and the case of ARCH models. Our aim is to test the hypothesis of normality for the innovations in a completely nonparametric way, i. e. without imposing parametric assumptions on the conditional mean and volatility functions. To this end the Cramér-von Mises test based on the empirical distribution function of nonparametrically estimated residuals is shown to be asymptotically distribution-free. We demonstrate its good performance for finite sample sizes in a simulation study.

AMS 2010 Classification: Primary 62M10, Secondary 62G10

Keywords and Phrases: autoregression, conditional heteroscedasticity, empirical distribution function, kernel estimation, nonparametric CHARN model, time series

1 Introduction

Nonlinear AR-ARCH models, i. e. models with an autoregressive conditional mean function and an autoregressive conditional variance function which are both not assumed linear, have become increasingly popular. They are also called CHARN (conditional heteroscedastic autoregressive nonlinear) models. In this paper we assume an AR-ARCH model of order one. Our aim is to test for Gaussian distribution of the innovations, which constitutes a typical assumption in the modelling of time series data. Under the normality assumption, asymptotic results often simplify. For instance, then no fourth moments appear in the asymptotic variance matrix of the empirical autocovariances of linear processes, see e. g. Brockwell & Davis (2006), Proposition 7.3.3. Further, the lack-of-fit test for ARCH models by Horváth, Kokozka & Teyssière (2004) strongly depends on the assumption of Gaussian innovations. Araveeporn (2011) uses the assumption of Gaussian innovations in order to estimate the conditional mean and volatility functions. Furthermore, estimation of conditional quantiles is of great importance in the context of financial time series. Starting from a nonparametric AR-ARCH model, however, the quantiles of the innovation distribution need to be estimated, or better be known (see Franke, Kreiß & Mammen (2009), section 4). Moreover, under Gaussianity of the innovations one can derive asymptotically distribution-free versions of other specification tests; see the discussion below.

We suggest a completely nonparametric test, which does not assume any parametric assumption on either mean or volatility function, but applies kernel estimators for those functions (see Doukhan & Ghindès (1983), Robinson (1983), Masry & Tjstheim (1995), Härdle & Tsybakov (1997), among others, for estimation procedures in nonparametric AR-ARCH models). Relatedly, in a homoscedastic nonparametric AR model Müller, Schick & Wefelmeyer (2009), who prove an asymptotic expansion of the empirical process of estimated innovations, mention the possibility to use their result for testing goodness-of-fit of the innovation distributions. They do not present the asymptotic distribution of the test statistics, nor finite sample properties. On the other hand, goodness-of-fit tests for the innovation distribution in parametric time series are suggested by Koul & Ling (2006) in AR-ARCH models and by Klar, Lindner & Meintanis (2011) for GARCH models, for instance. Ducharme & Lafaye de Micheaux (2004) test for normality of the innovations in standard ARMA models.

Our test statistic for Gaussianity of the innovations is the Cramér-von Mises distance of a weighted empirical distribution function of estimated innovations and the standard normal distribution. Though the mean and volatility functions are not specified in any way, the test statistic is shown to be asymptotically distribution-free. The test and its asymptotic distribution are presented in section 2.1. We treat the special cases of nonparametric AR and nonparametric ARCH models in detail in sections 2.2 and 2.3. In a small simulation study we demonstrate the good performance of the test for moderate sample sizes in section 3. We further discuss briefly how the test can be generalized to AR-ARCH models of higher order or to models with additional covariates.

As already mentioned, under Gaussianity of the innovations other testing procedures based on the residual empirical process will be asymptotically distribution-free. Then bootstrap procedures (for which asymptotic validity often is not investigated rigorously in the literature) can be avoided. As example for an asymptotically distribution-free specification test under the normality assumption we present a lack-of-fit test for standard AR(1) models in section 4. Further we reconsider the test for multiplicative structure by Dette, Pardo-Fernández & Van Keilegom (2009) under the normality assumption.

Finally, technical assumptions are listed in appendix A.

2 Main results

2.1 AR-ARCH model

Assume we have observed , where is a real valued stationary -mixing stochastic process following the AR-ARCH model of order one, i, e.

| (2.1) |

Here the innovations , , are assumed independent and identically distributed with unknown distribution function . Moreover, the innovations are centered with unit variance and is independent of the past , , .

Our aim is to test the null hypothesis of standard normal innovations against a general alternative . To this end we define kernel estimators for the conditional mean and conditional variance function as

| (2.2) |

where denotes a kernel function and a sequence of positive bandwidths. Technical assumptions are listed in the appendix. Now we estimate the innovations as residuals

and consider a weighted empirical distribution function, i. e.

| (2.3) |

as estimator for the innovation distribution. Here we define

while denotes some weight function fulfilling assumption (W) in the appendix. Selk & Neumeyer (2012) showed (see (A.1), (A.3) and the arguments following in the proof of Th. 3.1 in that paper) that under the assumptions stated in the appendix,

uniformly with respect to , where denotes the innovation density. Further in the aforementioned paper it is shown that

| (2.5) | |||||

| (2.6) |

(see (A.5)–(A.7) in the cited paper). Thus,

| (2.7) |

and the stochastic process

converges weakly to a centered Gaussian process with

Now let and denote distribution and density function of the standard normal distribution, respectively, and denote by a centered Gaussian process with covariance structure

Then we have the following result for the Cramér-von Mises test statistic.

Theorem 2.1

Under model (2.1) and the assumptions stated in the appendix under the null hypothesis of Gaussian innovations the test statistic

converges in distribution to .

Proof. A calculation of the covariance of in the case gives

because for standard normally distributed one easily calculates , and one has , . From the continuous mapping theorem it follows that converges in distribution to

while has the same distribution as . This finishes the proof.

Remark 2.2

It follows from Stephens (1976) that is also the weak limit of some process such that is the limit of

where are iid with known variance and unknown expectation and where denotes the normal distribution function with expectation and variance . That the limits of and coincide in distribution might be suprising because in our AR-ARCH model the variance is unknown and has to be estimated. However, as can be seen from the proof, in the asymptotic covariance of under exactly those terms cancel that arise from the estimation of the variance function (cf. (2.6)). Quantiles of and thus critical values for are tabled in Stephens (1976) and restated in Table 1 for convenience. We obtain an asymptotically distribution-free test by rejecting for asymptotic level whenever is larger than the critical value . Consistency can be deduced from uniform convergence of to in probability, which follows from (2.7).

| nominal level | |||||

|---|---|---|---|---|---|

| critical value |

Remark 2.3

The results for the nonparametric AR-ARCH model (2.1) can be extended to models of the form where is a stationary time series and may include covariates as well as a finite number of past values while , . Here denotes the sigma-field generated by . We conjecture that applying local polynomial estimators for and and assuming enough smoothness of those functions the expansion (2.7) stays valid. A thorough treatment is beyond the scope of the paper. Note also that asymptotic properties of estimators for the innovation distribution in such nonparametric AR()/regression models have not yet been treated in the literature. However, in the case of independent observations Neumeyer & Van Keilegom (2010) showed validity of an expansion like (2.7) for the empirical distribution of residuals in multiple nonparametric regression models (they obtain the same expansion as in the case of one-dimensional covariates, see Akritas & Van Keilegom (2001)). Thus we believe that Theorem 2.1 stays valid in the more general model under suitable regularity conditions and the same test for Gaussianity of the innovation distribution can be applied.

2.2 AR model

In this section we consider a nonparametric AR model of order one, i. e.

| (2.8) |

where the innovations , , are iid and centered and is independent of the past , . Thus we have model (2.1) with for the unknown (constant) variance . Our aim is to test the null hypothesis of normal innovations, i. e.

The constant variance is estimated by

where is the kernel estimator defined in (2.2). In this case we define the residuals as

and consider as defined in (2.3) as estimator for the distribution of the standardized innovations . Let again and denote distribution and density function of , respectively. Then is equivalent to and we have the following results.

Lemma 2.4

Under the assumptions stated in the appendix we have the expansion

uniformly with respect to .

Proof. First we consider the variance estimator, for which one obtains

by Lemmata B.2 and B.3 in Selk & Neumeyer (2012). Further

and

(see also (A.4) in Selk & Neumeyer (2012)) and thus

| (2.9) |

Now note that

and with arguments analogous to the proof of Theorem 3.1 in Selk & Neumeyer (2012) which leads to (2.1) (see also the proof of Lemma 1 in Dette, Pardo-Fernández & Van Keilegom (2009) or the proof of Theorem 3.1 in Müller, Schick & Wefelmeyer (2009)) one obtains that

uniformly with respect to . The assertion follows from (2.5) and (2.9).

Corollary 2.5

2.3 ARCH model

In this section we consider a nonparametric ARCH model of order one, i. e.

| (2.10) |

where the innovations , , are iid and centered with unit variance and is independent of the past , . Thus we have model (2.1) with conditional mean . Our aim is to test the null hypothesis of normal innovations. To this end let be estimated by the kernel estimator

and the residuals be defined as

whereas is as in (2.3). Let again denote the standard normal distribution function and let denote a standard Brownian bridge on . Then we obtain the following result.

Theorem 2.6

Under the assumptions stated in the appendix under the null hypothesis of Gaussian innovations in the ARCH model (2.10) the test statistic

converges in distribution to .

Proof. In the expansion (2.1) the estimation of is not present while (2.6) stays valid for the new estimator . Thus it follows that

and the stochastic process

converges weakly to a centered Gaussian process with

As the innovations are standard normally distributed we have , and . Hence,

The assertion follows by the continuous mapping theorem noting that is a standard Brownian bridge.

For convenient reference we state the critical values for the test in Table 2. Here is the ()-quantile of , see Shorack & Wellner (1986), p. 147.

| nominal level | |||||

|---|---|---|---|---|---|

| critical value |

3 Simulations

To examine the performance of the test on small samples we consider AR(1) models and ARCH(1) models, for which we compare the results under the assumption of an AR-ARCH model like (2.1) and under the assumption of an AR model like (2.8) (respectively ARCH like (2.10)).

For the AR(1) case we consider the models

where denotes the skew-normal distribution with location parameter

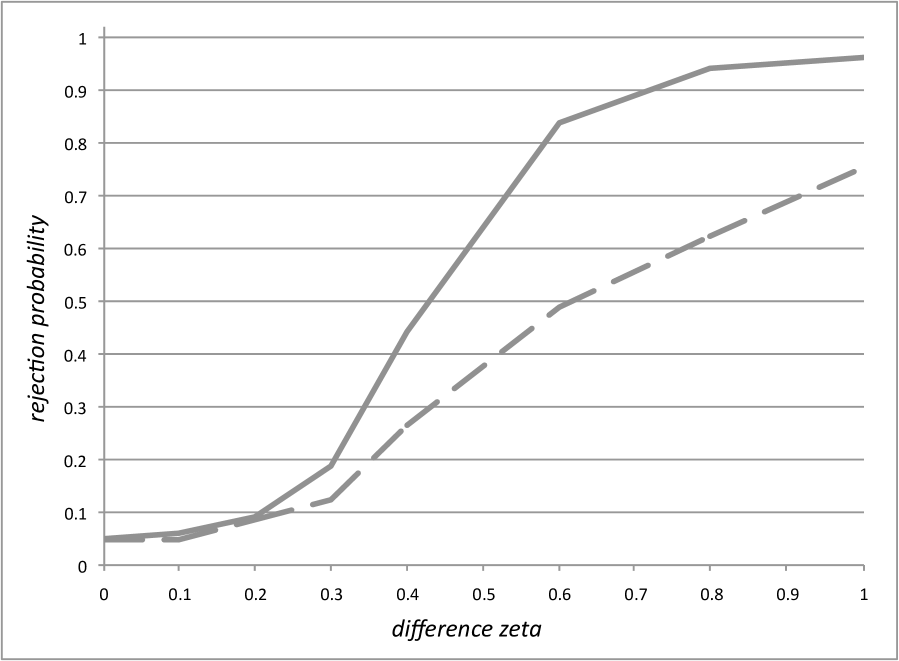

scale parameter and shape parameter for different values of . For this is the standard normal distribution. The rejection probabilities for 500 repetitions and level 5% are displayed in Table 3 and Figure 1 for the AR-ARCH model (2.1) and the AR model (2.8) respectively. It can be seen that the level is approximated well and the power increases for increasing parameter as well as for increasing sample size .

| AR-ARCH | ||||||||

|---|---|---|---|---|---|---|---|---|

| AR | ||||||||

We also examine ARCH(1) models with the same innovation distribution,

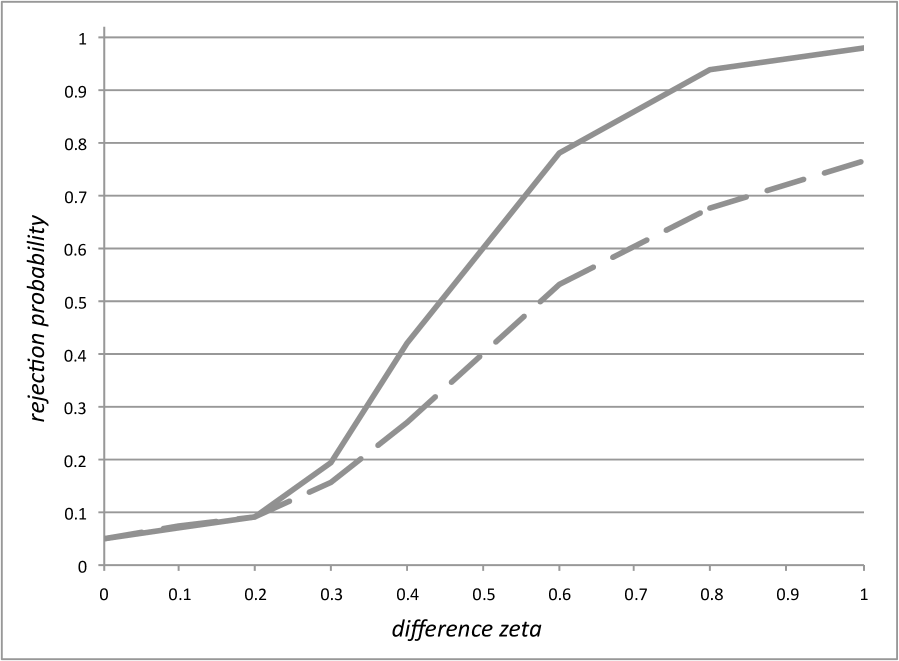

for different values of . The rejection probabilities for 500 repetitions and level 5% are shown in Table 4 and Figure 2 for the AR-ARCH model (2.1) and the ARCH model (2.10) respectively. The asymptotic level is approximated well and the power increases with increasing as well as with increasing . For the ARCH model the increase with for small is not as pronounced as for the models considered before, therefore we additionally examined this model with sample size for which an increase comparable to those before can be observed.

| AR-ARCH | ||||||||

|---|---|---|---|---|---|---|---|---|

| ARCH | ||||||||

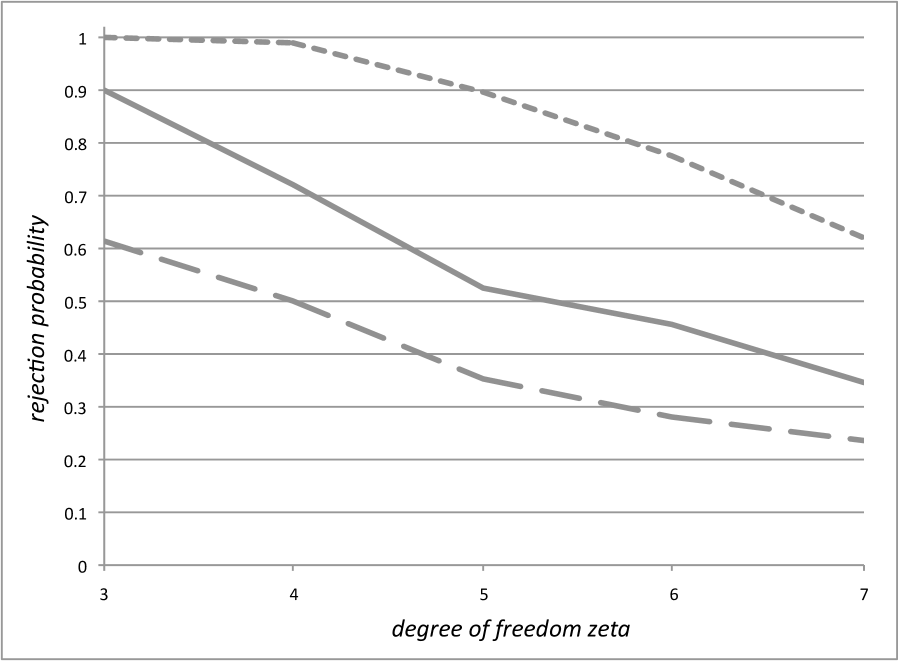

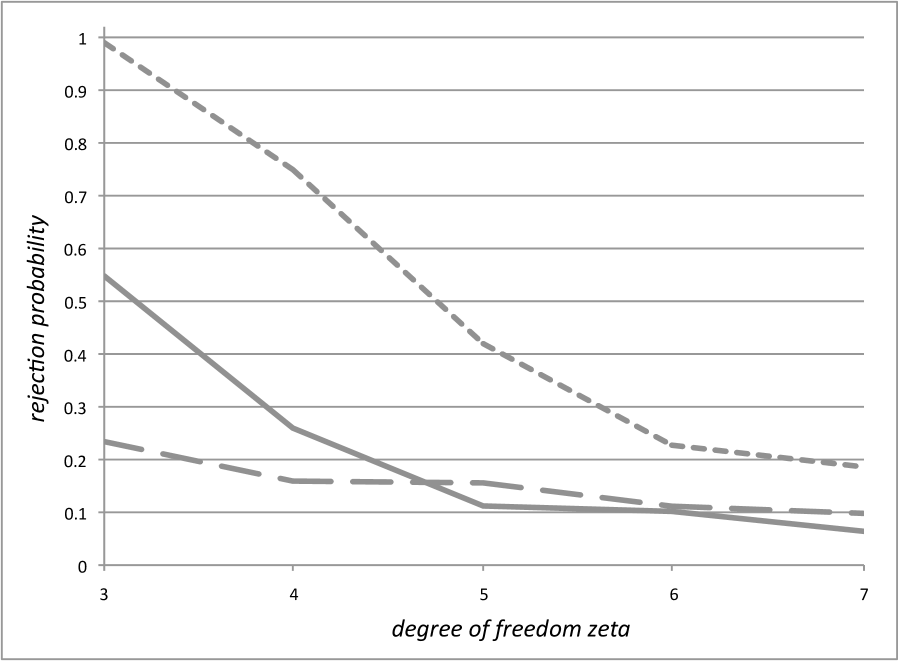

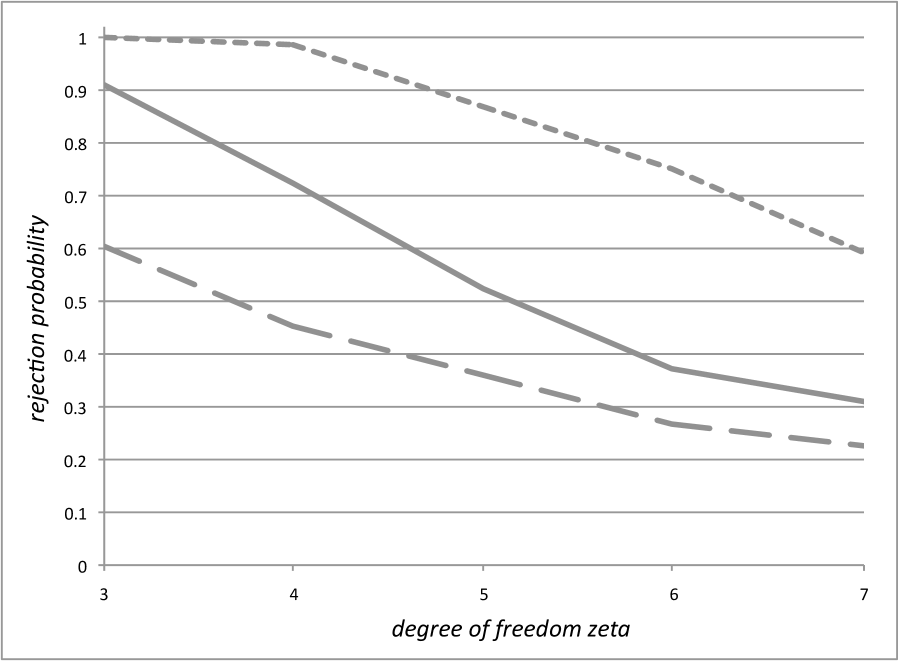

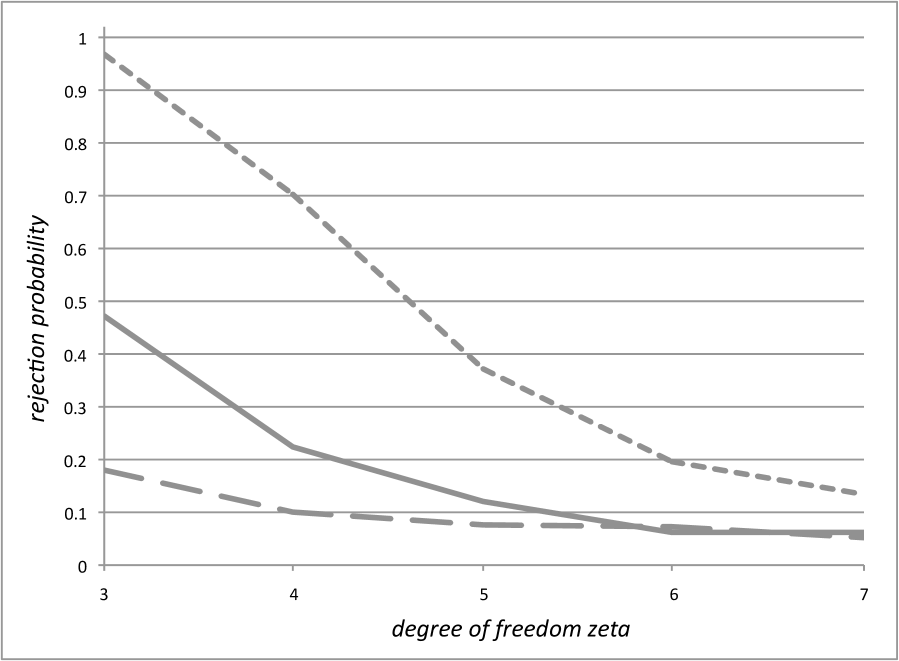

To further study the power of the testing procedure, we examine the same models with Student-t distributed innovations with different degrees of freedom. Due to the fact that Var has to be one for all , the Student-t distribution was standardized. The models are AR(1)

and ARCH(1)

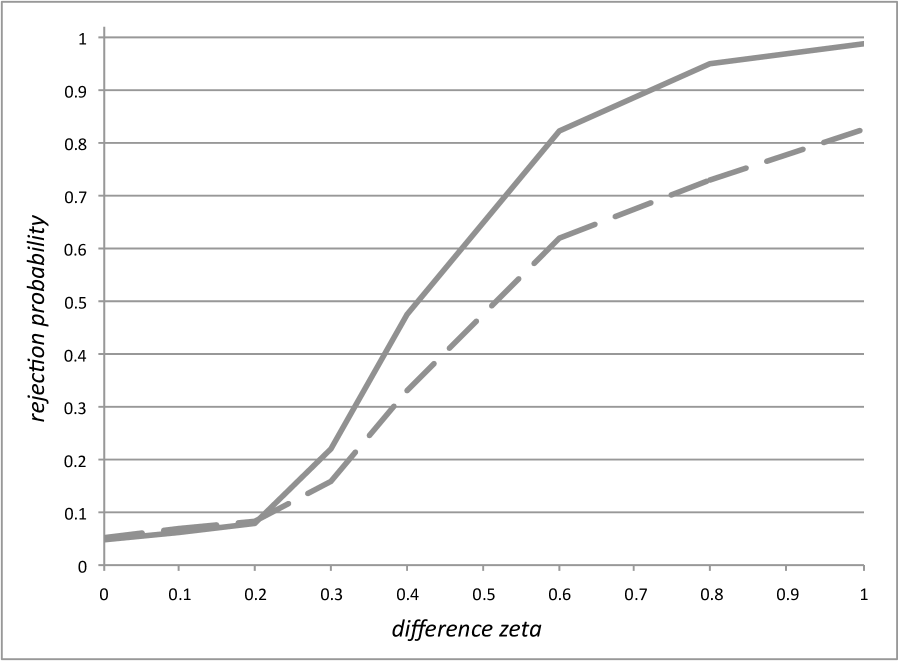

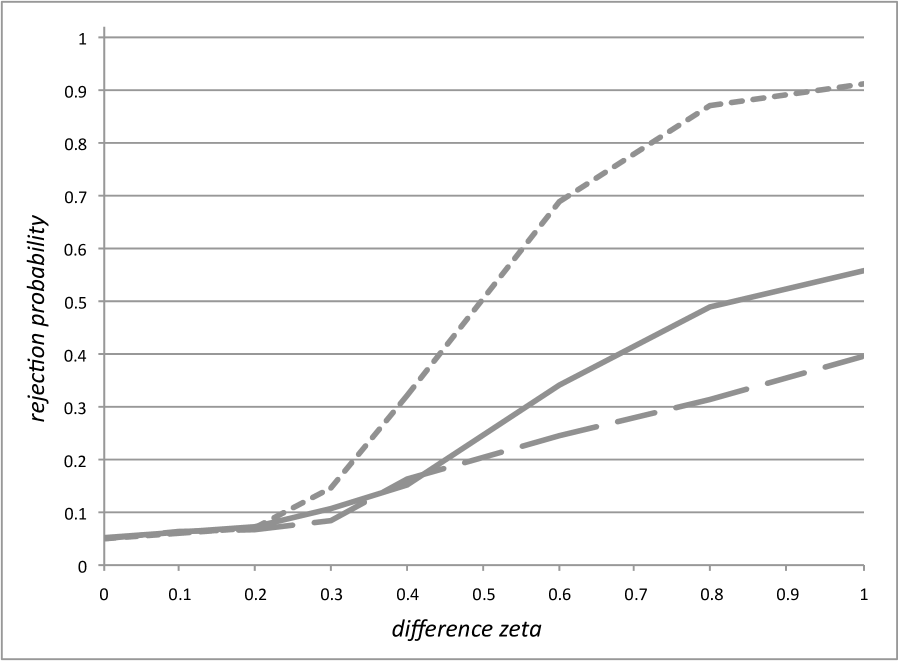

for different values of . The rejection probabilities for 500 repetitions and level 5% are displayed in Table 5, Figure 3 (AR(1) model) and Figure 4 (ARCH(1) model). As before we compare the results under the assumption of an AR-ARCH model like (2.1) and under the assumption of an AR model like (2.8) (respectively ARCH like (2.10)). It can be seen that the power is good and increases for increasing sample size while it decreases for increasing parameter , because the Student-t distribution converges to the standard normal distribution for increasing degree of freedom.

| AR-ARCH | ||||||||||

| AR/ARCH | ||||||||||

Simulation setting.

For each simulation observations were generated. For the test the last observations were used. This was done to ensure that the process is in balance.

The empirical processes were built with weight function .

The Nadaraya-Watson estimators and were calculated with Gaussian kernel. This is not compatible with all assumptions, e. g. the support of the kernel is not compact. However this has negligible effect on the simulations because the Gaussian kernel decreases exponentially fast at the tails. The bandwidth was chosen according to the assumptions by a rule of thumb as with .

4 Further examples

4.1 Testing for linear AR(1)

As was mentioned in the introduction other distribution-free specification tests for the AR-ARCH model can be derived once the Gaussianity of the errors has been established. In this section we will study in detail a lack-of-fit test for the linear AR(1) model. For the method compare Van Keilegom, González Manteiga, & Sánchez Sellero (2008) in a nonparametric regression model with independent observations. Similarly one can derive tests, e. g., for parametric ARCH models.

For simplicity here we assume that as this is a typical assumption in AR models. We consider the model

| (4.1) |

where the innovations , , are iid standard normal and is an unknown positive constant. Further, is independent of the past , . Our aim is to test the null hypothesis

See Hong-zhi & Bing (1991) or Koul & Stute (1999) for other procedures to test for .

Let denote any (under ) -consistent estimator for , e. g. the Yule-Walker or ordinary least squares estimator under suitable regularity assumptions. Now define residuals under the null as

with , and

Let further be defined as in section 2.2. Then we have the following result.

Theorem 4.1

Under the assumptions stated in the appendix for model (4.1) with Gaussian innovations we have under that

converges in distribution to a -distributed random variable.

Proof. Let denote the ‘true’ parameter under . Similar to the proof of Lemma 2.4 we have for standard Gaussian that

uniformly with respect to . Note that for the defined here the last equality in (2.6) also holds. Further,

because is ergodic due to its mixing property (see e.g. Doukhan (1994)). Thus with the -consistency of we obtain

uniformly with respect to . Now from Lemma 2.4 we have

which converges in distribution to with a standard normally distributed . Thus converges in distribution to

which is -distributed.

An asymptotically distribution-free level- test is obtained by rejecting the null hypothesis of a standard AR(1)-model whenever is larger than the -quantile of the -distribution.

4.2 Testing for multiplicative structure

Under the assumption of Gaussian innovations the test for multiplicative models by Dette, Pardo-Fernández & Van Keilegom (2009) simplifies. Here the null hypothesis to be tested for model (2.1) is

This condition connects ARCH models of the form to model (2.1) by setting with and .

Note that under the constant can be estimated -consistently by a least-squares estimator defined by Dette, Pardo-Fernández & Van Keilegom (2009). Its asymptotic expansion under and under our assumptions is

| (4.2) |

see Theorem 5 in the aforementioned paper, but note that under our assumptions given in the appendix the influence of the weight function vanishes asymptotically. Now define

with residuals

where is as in (2.2). Let for ,

and . Finally, let be defined as in (2.3). Then we have the following result.

Theorem 4.2

Under the assumptions stated in the appendix for model (2.1) with Gaussian innovations we have under that

converges in distribution a -distributed random variable.

Proof. We only sketch the main differences to the proof in Dette, Pardo-Fernández & Van Keilegom (2009) due to slightly different assumptions (under which in particular the influence of the weight function is asymptotically negligible). We have

uniformly with respect to (compare to (2.1)). From this and (4.2), (2.1), (2.6) one obtains

which by Th. 2.21 in Fan & Yao (2003) converges in distribution to , where is centered normally distributed with variance with

Finally the assertion follows because consistently estimates because consistently estimates and inherits the mixing property of and is therefore ergodic as well. Thus converges in distribution to

which is -distributed.

One obtains an asymptotically distribution-free test for and thus avoids to implement bootstrap procedures. Note that it is not obvious which kind of bootstrap procedure should be applied here in the context of arbitrary innovation distributions.

Appendix A Technical assumptions

The assumptions are similar to those in Selk & Neumeyer (2012) and required for their Theorem 3.1 which we use.

- (K)

-

The kernel is a three times differentiable density with compact support and , . Moreover and .

- (C)

-

The sequence of bandwidths fulfills

- (I)

-

For the interval some exists, such that . Moreover , where denotes the density of .

- (W)

-

The weight function fulfills for and for for some independent of and is three times differentiable such that for .

- (F)

-

The innovations , , are independent and standard normally distributed.

- (E)

-

Some exists such that .

- (X)

-

The observation process is -mixing with mixing-coefficient for some

Their density is bounded and four times differentiable with bounded derivatives. The density is also bounded away from zero on compact intervals and some exists, such that .

- (Z)

-

It holds that

and there exists some such that

is valid for all , for , with .

- (M)

-

The regression function and the scale function are four times differentiable and there exist some and , with , , and , where , , , .

Remark A.1

Note that the mixing condition in (X) is weaker than the one in Selk & Neumeyer (2012). This is due to the nonsequential case that is examined here for which the proof of Lemma B.3 in the aforementioned paper can be simplified. Further note that the assumptions above are formulated under the null hypothesis of Gaussian innovations. To obtain consistency of the testing procedures one needs to replace assumption (F) by

- (F’)

-

The innovations , , are independent and identically distributed with distribution function . Their density is continuously differentiable and as well as . Further, for from assumption (E).

For AR model (2.8) with some conditions in (Z) and (M) are redundant because is a constant function. A similar remark holds for the ARCH model (2.10) where .

References

-

Akritas, M. & Van Keilegom, I. (2001). Nonparametric estimation of the residual distribution. Scand. J. Statist. 28, 549-567.

-

Araveeporn, A. (2011). Developing Nonparametric Conditional Heteroscedastic Autoregressive Nonlinear Model by Using Maximum Likelihood Method. Chiang Mai J. Sci. 38, 331-345.

-

Brockwell, P. J. & Davis, R. A. (2006). Time Series: Theory and Methods. Springer, New York.

-

Dette, H., Pardo-Fernández, J. C. & Van Keilegom, I. (2009). Goodness-of-Fit Tests for Multiplicative Models with Dependent Data. Scand. J. Statist. 36, 782-799.

-

Doukhan, P. (1994). Mixing, Properties and Examples. Springer, New York.

-

Doukhan, P. & Ghindès, M. (1983). Estimation de la transition de probabilité d’une chaîne de Markov Doëblin-récurrente. Étude du cas du processus autorégressif général d’ordre 1. Stochastic Process. Appl. 15, 271-293.

-

Ducharme, G. & Lafaye de Micheaux, P. (2004). Goodness-of-fit tests of normality for the innovations in ARMA models. J. Time Ser. Anal. 25, 373-395

-

Franke, J., Kreiß, J.-P. & Mammen, E. (2009). Nonparametric modelling of financial time series. T. G. Andersen (ed) et al, Handbook of Financial Time Series. Springer, Berlin, 927-952.

-

Härdle, W. & Tsybakov, A. (1997). Local polynomial estimators of the volatility function in nonparametric autoregression. J. Econometrics 81, 223-242.

-

Härdle, W. & Vieu P. (1991). Kernel regression smoothing of time series. J. Time Ser. Anal. 13, 209-232.

-

Hong-zhi, A. & Bing, C. (1991). A Kolmogorov-Smirnov type statistic with application to test for nonlinearity in time series. Internat. Statist. Rev. 59, 287-307.

-

Horváth, L., Kokoszka, P. & Teyssière, G. (2004). Bootstrap misspecification tests for ARCH based on the empirical process of squared residuals. J. Stat. Comput. Simul. 74 , 469-485.

-

Klar, B., Lindner, F. & Meintanis, S. G. (2011). Specification tests for the error distribution in GARCH models. Comput. Statist. Data Anal., to appear. preprint available at http://www.math.kit.edu/stoch/ klar/seite/veroeffentlichungen/de

-

Koul, H. L. & Ling, S. (2006). Fitting an error distribution in some heteroscedastic time series models. Ann. Statist. 34, 994-1012.

-

Koul, H. L. & Stute, W. (1999). Nonparametric model checks for time series. Ann. Statist. 27, 204-236.

-

Masry, E. & Tjstheim, D. (1995). Nonparametric estimation and identification of nonlinear ARCH time series. Econometric Theory 11, 258-289.

-

Müller, U. U., Schick, A. & Wefelmeyer, W. (2009). Estimating the innovation distribution in nonparametric autoregression. Probab. Theory Relat. Fields 144, 53-77.

-

Neumeyer, N. & Van Keilegom, I. (2010). Estimating the error distribution in nonparametric multiple regression with applications to model testing. J. Multiv. Anal. 101, 1067-1078.

-

Robinson, P. M. (1983). Nonparametric estimators for time series. J. Time Ser. Anal. 4, 185-207.

-

Selk, L. & Neumeyer, N. (2012). Testing for a change of the innovation distribution in nonparametric autoregression - the sequential empirical process approach. Preprint available at http://preprint.math.uni-hamburg.de/public/ims.html

-

Shorack, G. R. & Wellner, J. A. (1986). Empirical Processes with Applications ot Statistics. Wiley, New York.

-

Stephens, M. A. (1976). Asymptotic Results for Goodness-of-Fit Statistics with Unknown Parameters. Ann. Statist. 4, 357-369.

-

Van Keilegom, I., González Manteiga, W. & Sánchez Sellero, C. (2008). Goodness-of-fit tests in parametric regression based on the estimation of the error distribution. TEST, 17, 401-415.