Dual regression

Abstract.

We propose dual regression as an alternative to the quantile regression process for the global estimation of conditional distribution functions under minimal assumptions. Dual regression provides all the interpretational power of the quantile regression process while avoiding the need for repairing the intersecting conditional quantile surfaces that quantile regression often produces in practice. Our approach introduces a mathematical programming characterization of conditional distribution functions which, in its simplest form, is the dual program of a simultaneous estimator for linear location-scale models. We apply our general characterization to the specification and estimation of a flexible class of conditional distribution functions, and present asymptotic theory for the corresponding empirical dual regression process.

keywords: Conditional distribution; Duality; Monotonicity; Quantile regression; Method of moments; Mathematical programming; Convex approximation.

1. Introduction

Let be a continuously distributed random variable and a random vector. Then the conditional distribution function of given , written , has three properties: is standard uniform, is independent of , and is strictly increasing in for any value of . We will refer to these three properties as uniformity, independence and monotonicity. For some specified mean zero and unit variance distribution function with support the real line and inverse function , define . Then satisfies independence and monotonicity, has distribution , and is transformed to uniformity by taking .

If we have a sample of points drawn from the joint distribution , how might we estimate the values using only the requirement that the estimate displays independence and monotonicity, and has distribution ? We explore this question by formulating a sequence of mathematical programming problems that embodies these requirements, with each element of this sequence providing an asymptotically valid characterization of an increasingly flexible class of conditional distribution functions.

The use of dual is thus motivated by the general observation that the estimation problem for a conditional distribution function indexed by a parameter is usually formulated in terms of a procedure that obtains directly and as a byproduct that follows from a calculation from the representation evaluated at a specific value of . A classical example is the linear location shift model , for which the parameter vector needs to be estimated in order to obtain the values . Here we turn that process around, obtaining first (from a mathematical programming problem) and backing out afterwards, if at all.

In its simplest form, dual regression augments the median regression dual programming problem (Koenker & Bassett, 1978) with global second moment orthogonality constraints, while expanding the support of parameter values from the unit interval to the real line. Adding further global orthogonality constraints gives rise to a sequence of augmented, generalized dual regression programs. Although each of these programs seeks only to find the values , their first-order conditions show that the assignment of these values corresponds to a sequence of augmented location-scale representations, the simplest element of which is a linear heteroscedastic model. Moreover, their second-order conditions are equivalent to monotonicity, so optimal dual regression solutions are free of quantile-crossing problems.

To each element of the sequence of dual programs corresponds a convex primal problem, both nontrivial to determine and difficult to implement, the convexity of which guarantees uniqueness of optimal dual regression solutions. For a given specification of , the first-order conditions of the corresponding primal problem also describe necessary and sufficient conditions for independence of the associated dual solutions. Thus our dual formulation reveals a sequence of convex optimization problems, gives a feasible and direct implementation of each of them, and uniquely characterizes the family of associated globally monotone representations, which can then be used as complete estimates of a flexible class of conditional distribution functions.

2. Basics

2.1. The dual regression problem

We introduce the basic principles underlying our general method by first providing a new characterization of the conditional distribution function associated with the linear location-scale model

| (2.1) |

where is a vector of explanatory variables including an intercept, and a mean zero and unit variance cumulative distribution function over the real line.

Suppose that we observe a sample of identically and independently distributed realizations generated according to model (2.1). The primary population target of our analysis is

knowledge of which is equivalent to knowledge of the values up to the monotone transformation .

Let and satisfy the system of equations and inequality constraints

| (2.2) |

where further satisfies the orthogonality conditions and . Since includes an intercept, the sample moments of and are and , and and are orthogonal to each column of the matrix of explanatory variables. We propose a characterization of the sequence of vectors that satisfy representation (2.2) and the associated orthogonality constraints for each . The corresponding sequence of empirical distribution functions then provides an asymptotically valid characterization of the conditional distribution function corresponding to the data-generating process (2.1). As a by-product of this approach, we simultaneously obtain a characterization of the parameter vector in (2.2), which then provides a consistent estimator of the population parameter in (2.1).

For each , with the scale function , is an increasing function of , and to representation (2.2) corresponds a convex function

and whose quadratic form corresponds to a location-scale representation for . Letting be the vector of dependent variable values, and assuming knowledge of and , we consider assigning a value to each observation in the sample by maximizing the correlation between and subject to a constraint that embodies the properties of :

| (2.3) |

Problem (2.3) describes the assignment of values to values in a sample generated according to a location-scale model, and it admits as its only solution. Since and are unknown, the assignment problem (2.3) is infeasible: we thus introduce the equivalent, feasible formulation

the dual regression program.

2.2. Solving the dual program

The solution to (D) is easily found from the Lagrangian

Differentiating with respect to we obtain first-order conditions:

Upon rearranging we obtain the closed-form solution

which is of the location-scale form , with and linear in .

Another view is obtained by writing the first-order conditions as

| (2.4) |

a linear location-scale representation, with corresponding quantile regression representation

| (2.5) |

Program (D) thus provides a complete characterization of linear representations of the form (2.4) and (2.5), as they arise from its first-order conditions. Moreover, the parameters of these representations are the Lagrange multipliers and of an optimization problem with solution .

The quantile regression representation of the first-order conditions of (D) sheds additional light on the monotonicity property of dual regression solutions, when there are no repeated values. For , , the no-crossing property of conditional quantiles requires

which is satisfied if is strictly positive for each , and coincides with the second-order conditions of program (D):

Therefore, an optimal solution that violates the monotonicity property is ruled out by the requirement that for an observation with value , the ordering of the values and must correspond to the ordering of the values. Hence the correlation criterion of system (D) suffices to impose monotonicity, with optimality of a solution then being equivalent to monotonicity at the sample points. Dual regression is thus able to incorporate this property in the estimation procedure, which facilitates extrapolation beyond the empirical support of , and yields significant finite-sample improvements in the estimation of conditional quantile functions as illustrated by our simulations in 5.2.

2.3. Formal duality

By Lagrangian duality arguments (Boyd & Vandenberghe, 2004, Chapter 5), the objective function of the dual of problem (D) is

defined for all , where , with and . Under the conditions of Theorem 1 below, has a closed-form expression, is strictly convex over , and minimizing over is equivalent to solving (D). Given a vector , we let denote the diagonal matrix with diagonal elements .

Condition 1.

The random variable is continuously distributed conditional on , with conditional density bounded away from .

Condition 2.

For a specified vector , the matrix is nonsingular and the matrix is finite, positive definite, and has rank .

Condition 3.

There exists such that with for some constant , and and .

Theorem 1 summarizes our finite-sample analysis of dual regression. The proofs of all formal results in the paper are given in the Supplementary Material.

Theorem 1.

If Conditions 1–3 hold with , for all , then problem (2.3) admits the equivalent feasible formulation (D), with solution and multipliers and , respectively. Moreover, for program (D) the following holds:

(i) Primal problem: the dual of (D) is

the primal dual regression problem, with solution .

(ii) First-order conditions: program (D) admits the method-of-moments representation

| (2.6) |

the first-order conditions of (P).

(iii) With probability 1: (a) uniqueness: the pair is the unique optimal solution to (P) and (D), and ; (b) strong duality: the value of (D) equals the value of (P).

Theorem 1 establishes formal duality of our initial assignment problem under first and second moment orthogonality constraints and the global -estimation problem (P). Convexity of (P) guarantees that to a unique assignment of values corresponds a unique linear representation of the form (2.2). Uniqueness further implies that if satisfies independence, then the orthogonality conditions in (2.6) are both necessary and sufficient for the dual solution to satisfy independence.

The primal problem (P) is a locally heteroscedastic generalization of a simultaneous location-scale estimator proposed by Huber (1981) and further analyzed in Owen (2001). The linear heteroscedastic model of equation (2.4) has been previously encountered in the quantile regression literature: see Koenker & Zhao (1994) and He (1997). The former consider the efficient estimation of (2.4) via -estimation while the latter develops a restricted quantile regression method that prevents quantile crossing. Compared to these quantile-based methods, dual regression trades local estimation and the convenient linear programming formulation of quantile regression for simultaneous estimation of location and scale parameters.

2.4. Connection with the dual formulation of quantile regression

The dual problem of the linear quantile regression of on is (cf., Koenker, 2005, p. 87, equation 3.12):

| (2.7) |

The solution to problem (2.7) produces values of that are largely 0 and 1, with sample points being assigned values that are neither 0 nor 1. The points that are assigned 1 fall above the median quantile regression; the points receiving 0’s fall below; and the remaining points fall on the median quantile regression plane. One direction of extension of (2.7) is to replace the 1/2 with values that fall between 0 and 1 to obtain the quantile regression.

Another extension is to augment problem (2.7) by adding more constraints:

| (2.8) |

It is apparent that the solution to (2.7) does not satisfy (2.8): the variance of around 0 in the solution to (2.7) is approximately , not . To satisfy program (2.8), the ’s have to be moved off and . Since contains an intercept, the sample moments of and will be and ; and will be orthogonal to the columns of the matrix , relations that are necessary but not sufficient for uniformity and independence.

Both systems (2.7) and (2.8) demand monotonicity by maximally correlating and . A violation of monotonicity requires there to be two observations that share the same values but have different values, with the lower of the two values having the weakly higher value of . However, a solution characterized by such a violation could be improved upon by exchanging the assignments. Thus violation of monotonicity in program (2.7) arises because the set of admissible exchanges in assignments is overly restricted: (2.7) is dual to a linear program well-known to have solutions at which observations are interpolated when parameters are being estimated, i.e., the hyperplanes obtained by regression quantiles must interpolate observations.

By reformulating program (2.8) into a constrained optimization problem over , program (D) further expands the set of admissible exchanges in assignments, since is restricted to . Doing this, the problem corresponding to (2.8) becomes the dual regression program (D), where can take on any real value. It is then natural to take the empirical cumulative distribution function of the dual regression solution , thereby imposing uniformity to high precision even at small .

3. Generalization

3.1. Infeasible generalized dual regression

The dual regression characterization of location-scale conditional distribution functions via the monotonicity element, the objective, and the independence element, the constraints, can be exploited to characterize more flexible representations. Similarly to the approach introduced in 2, we first analyze the infeasible assignment problem for a general representation of the stochastic structure of conditional on :

| (3.1) |

where is a specified cumulative distribution function with support the real line, and for each value of , the derivative of is strictly positive. Representation (3.1) always exists with defined as the composition of the conditional quantile function of given and the distribution function .

To each monotone function also corresponds a convex function defined as

The monotonicity of guarantees the convexity of . The slope of this function gives the value of corresponding to a value of at . Thus corresponds to a collection of convex functions, with one element of this collection for each value of together with a single random variable whose distribution is common to all the convex functions.

Equipped with , suppose we are tasked with assigning a value to each of the realizations . Then, for , solving the infeasible problem

generates the correct assignment: writing the Lagrangian

the associated first-order conditions are

| (3.2) |

and convexity of then guarantees that (3.2) is uniquely satisfied by , with . This demonstrates that maximizing generally suffices to match ’s to ’s, regardless of the form of in (3.1).

Theorem 2.

Theorem 2 shows that problem (IGD) fully characterizes the assignment problem: given and , solving (IGD) assigns a value to each sample point , and this value is the corresponding value up to a specified transformation . If is specified to be a known distribution, the values are then also known. If is specified to be an unknown distribution, as in our application below, the empirical distribution of then provides an asymptotically valid estimator for . Knowledge of and can thus be incorporated into a mathematical programming problem which delivers the values of at the sample points.

3.2. Generalized dual regression representations: definition and characterization

Problem (IGD) is infeasible because neither nor is known. However, Theorem 2 motivates a feasible approach once and are specified. Denote the components of without the intercept by , so that . Without loss of generality, let be centered, denoted , and let . With and , we specify by a linear combination of basis functions , the coefficients of which depend on :

| (3.3) |

and we assume that is linear in and set:

| (3.4) |

Finally, we specify a zero mean and unit variance distribution for by imposing and , and setting for , in (3.4).

With , our normalization and (3.3)–(3.4) together yield the augmented, generalized dual regression model

| (3.5) |

Equation (3.5) admits of the following interpretation. When and , so that is just a re-scaled version of the distribution of at . Since is independent of , transformations of this shape of must suffice to produce at other values of . The first two transformations, and , are translations of location and scale which do not essentially affect the shape of ’s response to changes in at all. The additional terms achieve that end.

Suppose that we observe a sample of identically and independently distributed realizations generated according to model (3.5). Define for , and for , and let and satisfy the system of equations and inequality constraints

| (3.6) |

where further satisfies , with , , and . These relations reduce to the linear heteroscedastic representation of 2 for , and impose that be a zero mean and unit variance vector satisfying the augmented set of orthogonality conditions . The sequence of vectors that satisfies the generalized dual regression representation (3.6) as well as the associated orthogonality constraints for each then provides an asymptotically valid characterization of the data-generating process (3.5).

Each element of this sequence is characterized by the assignment problem

| (3.7) |

where , and , with for , and for . Since and are unknown, problem (3.7) is infeasible; we thus formulate an equivalent, feasible implementation of problem (IGD):

the generalized dual regression program. (GD) then uniquely characterizes representation (3.6).

In order to state the properties of (GD) formally, we define the parameter space , which specifies parameter values compatible with monotone representations:

with . For , let denote the inverse function of , which is well-defined for each . We assume that the basis functions and the pair satisfy the following conditions.

Condition 4.

There exists a finite constant such that , and the matrix is finite and nonsingular for each and all .

Condition 5.

There exists such that and , for and some constant , and satisfies , for .

Let . Theorem 3 summarizes our finite-sample analysis of generalized dual regression.

Theorem 3.

If Conditions 1, 2, 4 and 5 hold with , for all , then problem (IGD) admits the equivalent feasible formulation (GD), with solution and multipliers and , respectively. Moreover, for program (GD) the following holds:

(i) Primal problem: the dual of (GD) is

the primal generalized dual regression problem, with solution .

(ii) First-order conditions: program (GD) admits the method-of-moments representation

| (3.8) |

the first-order conditions of (GP).

(iii) With probability 1: (a) uniqueness: the pair is the unique optimal solution to (GP) and (GD), and ; (b) strong duality: the value of (GD) equals the value of (GP).

Problem (GD) augments the set of orthogonality constraints in (D) and generates increasingly flexible representations of the form (3.6). For each element of this sequence, (GD) then provides a feasible formulation of the generalized assignment problem (IGD) with optimality condition equivalent to monotonicity. Theorem 3 also states the form of the corresponding primal problem, whose convexity guarantees that (GD) and (GP) uniquely and equivalently characterize representation (3.5). Uniqueness further implies that if satisfies independence, then the orthogonality conditions in (B.9) are both necessary and sufficient for the dual solution to satisfy independence as well. Theorem 3 thus characterizes and establishes the duality between specification of orthogonality constraints on and specification of a globally monotone representation for conditional on .

Formally, (GP) is the restriction of the dual of (GD) to . The existence Condition 5 and the form of (GD) optimality conditions together ensure that (GD) does not admit a global maximum with associated multipliers outside . Implementing (GP) thus requires the imposition of inequality constraints with only implicitly defined in the specification of (GP) for , and problem (GD) therefore provides a greatly simplified dual implementation. The special case of dual regression corresponds to , and imposing , for , is a normalization. The simple basis is obviously impoverished for the space of all convex functions, although quite practical for many applications once the flexibility in the distribution of is taken into account.

3.3. Connection with optimal transport formulation of quantile regression

An alternative approach is to specify to a known distribution, and alter representation (3.5) and the corresponding problem accordingly. If is specified to be the standard uniform distribution, then (2.8) in 2.4 can be generalized as

| (3.9) |

For , let , with . With denoting the Kronecker product, the large-sample form of program (3.9) is

| (3.10) |

Letting increase, both the distributional and the orthogonality constraints get strengthened. Because includes an intercept, the distribution of approaches uniformity, while simultaneously satisfying an increasing sequence of orthogonality constraints. In the limit, a uniformly distributed random variable satisfying the full set of orthogonality constraints is thus specified. Since for all is equivalent to the mean-independence property and the uniformity constraint , in the large limit program (3.10) coincides with the scalar quantile regression problem proposed in independent work by Carlier et al. (2016) (cf., equation 19, p. 1180)

| (3.11) |

which provides an optimal transport formulation of quantile regression (we are grateful to an anonymous referee for highlighting this connection). Program (3.11) is directly amenable to a linear programming implementation which maintains and exploits the full specification of the marginal distribution of to a known distribution, whereas (3.10) provides a sequential nonlinear programming characterization of which relaxes uniformity for finite and .

For , let . The large-sample form of program (GD) is

| (3.12) |

Program (3.12) relaxes the support constraint in (3.9) and only specifies first and second moments of , while the centering of ensures that this is sufficient for to be uniquely determined. The empirical distribution of solutions of the finite-sample analog (GD) of (3.12) then provides an asymptotically valid characterization of the distribution of .

4. Asymptotic Properties

We apply our framework to the estimation of a –term generalized dual regression model of the form (3.5). Denote the support of by , and, for some finite constant , define . Letting denote the space of continuously differentiable functions on , define the space of strictly increasing functions indexed by values, . The large-sample analog of is then the space of vectors in such that there exists a corresponding optimal generalized dual regression representation:

For any , denote in such that by .

Condition 6.

For some and some mean zero and unit variance cumulative distribution function , the representation holds with probability one, with and , for , and for some constant .

Condition 7.

The matrix defined in Condition 2 satisfies , a positive definite matrix of rank , and for all the matrix is nonsingular.

Condition 8.

(i) Let , and ; (ii) let , and .

These conditions are used to establish existence and consistency of dual regression solutions, and Condition 8(ii) is needed for asymptotic normality of estimates of . In view of uniqueness stated in part (iii) of Theorem 3, these properties are shared by and , which we denote by for notational simplicity. We also denote both and indirect estimates , constructed after solving (GP), by , with empirical distribution function , . Furthermore, part (ii) of Theorem 3 shows that while the solution is obtained directly by solving the mathematical program (GD), knowledge that the solution obeys representation (3.6) can be exploited to write estimating equations for in the form of system (B.9). The computation of the asymptotic distribution of follows from this characterization.

Theorem 5.

Knowledge of the statistical properties of can be used to establish the limiting behaviour of the empirical distribution of . Define the empirical dual regression process

Theorem 6 establishes weak convergence of the empirical distribution of and the limiting behaviour of , accounting for its dependence on the distribution of .

Theorem 6.

If the conditions of Theorem 5 hold, and, uniformly in over , is uniformly continuous in , bounded and, for some finite constant and all , satisfies , then (i) converges in probability to zero, and (ii) converges weakly to a zero-mean Gaussian process with covariance function defined in (5.11) in the Supplementary Material.

Theorems 5 and 6 together establish that the pair provides an asymptotically valid characterization of the generalized dual regression representation specified in Condition 6. When is independent of , Theorem 6 further implies that the empirical distribution of provides an asymptotically valid estimator of the conditional distribution of given . For , estimates of the coefficients in quantile regression form can then be constructed as , exploiting the structure of the conditional quantile function of given implied by representation (3.5). Theorem 6 also establishes asymptotic normality of the empirical dual regression process. The form of the covariance function of reflects the influence of imposing sample orthogonality constraints in (GD) on the empirical distribution of , or equivalently, of sample variability of parameter estimates on the empirical distribution of , as expected from the classical result of Durbin (1973).

Theorem 6 can be applied to perform pointwise inference on the conditional distribution function of conditional on . However, simultaneous inference over regions of the joint support of and is typically of interest in practice. Several approaches for uniform inference in the presence of non-pivotal limit processes have been considered in the literature (e.g., Koenker & Xiao, 2002, and Parker, 2013), including simulation methods (Chernozhukov et al., 2013). Extension of existing results to dual regression is beyond the scope of this paper but they provide a natural direction for future study of uniform inference on the empirical dual regression process.

5. Engel’s Data Revisited

5.1. Empirical analysis

The classical dataset collected by Engel consists of food expenditure and income measurements for 235 households, and has been studied by means of quantile regression methods (Koenker, 2005). We illustrate dual regression methods by estimating the statistical relationship between food expenditure and income, with household income as a single regressor and food expenditure as the outcome of interest.

We specify the vector of basis functions by means of trigonometric series. Alternative choices such as splines and shape-preserving wavelets (e.g., DeVore, 1977, and Cosma et al., 2007). In order to choose , we first implement program (GD) for , which we then augment sequentially adding one pair of cosine and sine basis at a time, up to a representation of order . At each step, we compute a Schwarz Information Criterion (Schwarz, 1978) applied to the primal generalized dual regression problem, exploiting the strong duality result of Theorem 3 in order to compute its value as . Our procedure selects the location-scale representation . In the Supplementary Material, we describe the procedure and report results from the augmented specifications, which show that our results are robust to the number of terms included. In order to test for the validity of the selected model, a complementary procedure that should be explored in future research is to test for independence of dual regression solutions and explanatory variables. The test for multivariate independence proposed by Genest et al. (2007) constitutes an interesting starting point for such a development.

All computational procedures can be implemented in the software R (R Development Core Team, 2017) using open source software packages for nonlinear optimization such as Ipopt or Nlopt, and their R interface Ipoptr and Nloptr developed by Jelmer Ypma. Quantile regression procedures in the package quantreg have been used to carry our comparisons.

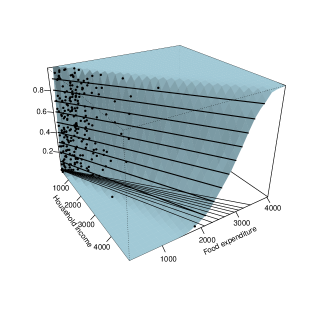

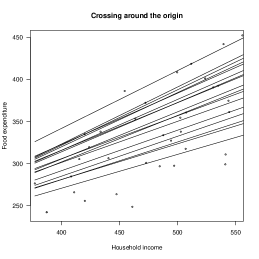

Figure 5.1 illustrates our results and plots the estimated distribution of food expenditure conditional on household income. Estimates , where , are used in order to plot each observation in the -space with predicted coordinates , and the solid lines give the -level sets for a grid of values . Although nonstandard, this representation relates to standard quantile regression plots since the levels of the distribution function give the conditional quantiles of food expenditure for each value of income. These are the plotted shadow solid lines corresponding for each to dual regression estimates of conditional quantile functions of food expenditure given household income.

Figure 5.1 shows that the predicted conditional distribution function obtained by dual regression is indeed endowed with all desired properties. Of particular interest is the fact that the estimated function is monotone in food expenditure. Also, our estimates satisfy some basic smoothness requirements across probability levels, in the food expenditure values. This feature does not typically characterize estimates of the conditional quantile process by quantile regression methods, as conditional quantile functions are then estimated sequentially and independently of each other. The decreasing slope of the distribution function across values of income provides evidence that the data indeed follow a heteroscedastic generating process. This is the distributional counterpart of quantile functions having increasing slope across probability levels, a feature characterizing the conditional quantile functions on the plane and signalling increasing dispersion in food expenditure across household income values.

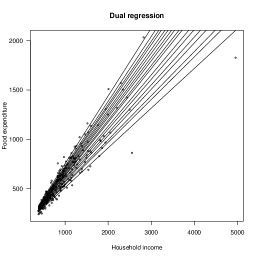

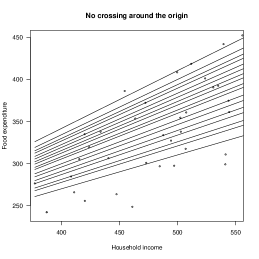

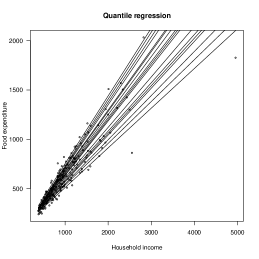

Figure 5.2 gives the more familiar quantile regression plots. The plots presented show scatterplots of Engel’s data as well as conditional quantile functions obtained by dual and quantile regression methods. The rescaled plots in the right panels of Fig. 5.2 highlight some features of the two procedures. The fitted lines obtained from dual regression are not subject to crossing in this example, whereas several of the fitted quantile regression lines actually cross for small values of household income. Last, the more evenly spread dual regression conditional quantile functions illustrate the effect of specifying a functional form for the quantile regression coefficients, while preserving asymmetry in the conditional distribution of food expenditure.

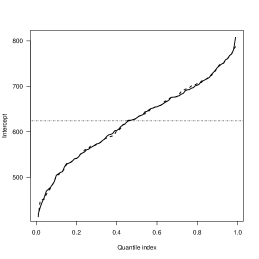

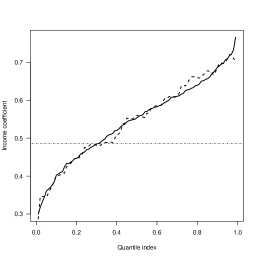

Figure 5.3 compares our estimates of intercept and income coefficients in quantile regression form, with estimates obtained by quantile regression. For interpretational purposes, we follow Koenker (2005) and estimate the functional coefficients after having recentered household income. This avoids having to interpret the intercept as food expenditure for households with zero income. After centering, the intercept coefficient can be interpreted as the -th quantile of food expenditure for households with mean income. Fig. 5.3 shows the estimated quantile regression coefficients as a function of . It illustrates the fact that the flexible structure imposed by dual regression yields estimates that are indeed smoother than their quantile regression counterpart, the latter having a somewhat erratic behaviour around our estimates.

5.2. Simulations

We give a brief summary of the results of a Monte Carlo simulation in order to assess the finite-sample properties dual regression. The data-generating process is

| (5.1) |

with parameter values calibrated to the empirical application, from which samples are simulated. As a benchmark, we compare generalized dual regression estimates of the values , to those obtained by applying the inversion procedure of Chernozhukov et al. (2010) to the quantile regression process. For each simulation, the estimation and selection procedures are identical to those implemented in the empirical application.

Table 1 reports a first set of results regarding the accuracy of conditional distribution function estimates. We report average estimation errors across simulations of dual regression and quantile regression estimators, respectively, and their ratio in percentage terms. Estimation errors are measured in norms , for , and , where for , , and are computed with the solutions to the selected generalized dual regression program. Correct model selection ranges from of the simulations for to for , providing encouraging evidence about the validity of the proposed criterion. The results show that for this setup our estimates systematically outperform quantile regression-based estimates, with the spread in performance increasing with sample size. Whereas the reduction in average estimation error is between and , depending on the norm, for , estimation error is reduced up to when . The larger reduction in average errors in norm reflects the higher accuracy in estimation of extreme parts of the distribution.

| Sample size | ||||||

|---|---|---|---|---|---|---|

In the Supplementary Material, we describe the experiment in detail, and report results on estimation of quantile regression coefficients and the distribution of selected models across simulations. We also include additional simulations that illustrate the empirical performance of dual regression with multiple covariates and show that it performs well relative to the noncrossing quantile regression method proposed by Bondell et al. (2010).

6. Discussion

If we designate problems such as (D) and (GD) as already dual, then their solutions reveal a corresponding primal. Typically, the Lagrange multipliers of the dual appear as parameters in the primal, and the primal has an interpretation as a data-generating process. So perhaps not surprisingly the constraints on the construction of the stochastic elements have shadow values that are parameters of a data-generating representation. In this way the relation between identification and estimation is made perspicuous: a parameter of the data-generating process is the Lagrange multiplier of a specific constraint on the construction of the stochastic element, so to specify that some parameters are non-zero and others are zero is to say that some constraints are in the large-sample limit binding and others are not.

Another way of expressing this is to say that when a primal corresponds to the data-generating process, additional moment conditions are superfluous: they will in the limit attract Lagrange multiplier values of zero and consequently not affect the value of the program nor the solution. In a sense, this is obvious: the parameters of the primal can typically be identified and estimated through an –estimation problem that will generate equations to be solved for the unknown parameters. Nonetheless, the recognition that the only moment conditions that contribute to enforcing the independence requirement are those whose imposition simultaneously reduces the objective function while providing multipliers that are coefficients in the stochastic representation of suggests the futility of portmanteau approaches (e.g., those based on characteristic functions) to imposing independence. The dual formulation reveals that to specify the binding moment conditions is to specify an approximating data-generating process representation, which then can be extrapolated to provide estimates of objects of interest beyond the explicitly estimated values of that characterize the sample and the definition of the mathematical program.

As is well understood in mathematical programming, dual solutions provide lower bounds on the values obtained by primal problems. In the generic form of the problems we have considered here there is no gap between the primal and dual values; hence in econometrics these problems are said to display point identification. We conjecture that the problems without point identification do have gaps between their dual and primal values, and that this characterization will enhance our understanding.

Appendix A Proof of Theorem 2

For , the Lagrangian of the infeasible problem (IGD) is

By definition of and continuous differentiability of , for each , the Fundamental Theorem of Calculus implies the first-order conditions

| (A.1) |

The second-order conditions

| (A.2) |

are satisfied if and only if , since is strictly positive for each . Since cannot hold under Condition 1, with probability one, (A.1) rules out . Moreover, for , (A.2) implies that the map is strictly convex over the real line, since for each , and hence unbounded above. Therefore we only need to show that the pair is the unique pair in that satisfies (A.1).

By strict monotonicity of , the inverse function is well-defined, for each , and a solution to (A.1) is . Substituting into the constraint of (IGD) yields

| (A.3) |

By Lemma 1 below, is the unique solution to (A.3) such that . Since for , strict concavity of for implied by (A.2) shows that is the unique pair in that satisfies (A.1).

Lemma 1.

Under the conditions of Theorem 2, is the unique solution to the equation

| (A.4) |

such that .

Proof.

We first show that Equation (A.4) is the first-order condition of the infeasible generalized dual regression primal problem , where

and then show that admits as its unique minimum.

Step 1. Define the Lagrange dual function (Boyd & Vandenberghe, 2004, Chapter 5) , for . In order to derive , we show that the maximum of the map is attained and is unique, and evaluate at this value.

For and , consider the level sets of . These sets are compact. Given , let and , so that and . Thus, by definition of , a second-order Taylor expansion of around yields, for some on the line connecting and ,

where the last inequality follows from and the uniform lower bound on for each which implies that is positive definite. For , the above inequality implies that is bounded and therefore is bounded. Since is continuous over , is also closed. It then follows from the Weierstrass theorem that there exists .

Since the Hessian matrix of the map is negative definite for all , is strictly concave with unique maximum , for all . Upon using first-order conditions (A.1), direct substitution yields , the maximum of the map , for all .

Step 2. The function is strictly convex for : since is continuously differentiable for each by assumption, by the inverse function theorem is continuously differentiable for each , and there are the following derivatives:

| (A.5) | ||||

| (A.6) |

for every , and . Upon using (A.5) and (A.6), has first-order conditions (A.4), and the second-order conditions

are satisfied for all since for each . Therefore, is strictly convex for all and admits at most one minimum. Since for , and by definition, is also feasible. The result follows.∎

Appendix B Proofs of Theorems 1 and 3

B.1. Proof of Theorem 1

Theorem 1 is a corollary of Theorem 3, upon substituting to and setting .

B.2. Preliminary lemmas

We establish the equivalence (IGD)–(GD) and convexity of (GP).

Lemma 2.

Proof.

Letting , the corresponding expression is

| (B.1) |

Given the form of , the constraint in (IGD) can be simplified using

by definition of in Theorem 2, expansion (B.1), and the properties of assumed in Condition 5. Therefore, the infeasible problem (IGD) becomes

with Lagrangian

for . For all , the map satisfies the conditions of Theorem 2, which implies that and , by application of Theorem 2 upon substituting for and for .

Adding to the choice variables of the optimization problem, we obtain the additional constraints

| (B.2) |

Equation (B.2) can be directly appended to the objective to obtain the optimization problem (GD) in which the Lagrange multiplier is . By part (iii) of Theorem 3, problem (GD) admits a unique optimal solution over . Since is a feasible solution by Condition 5, . It follows that (GD) and (IGD) are equivalent. ∎

Lemma 3.

Proof.

For , define , with defined as

| (B.3) |

and let , , . For and , the derivative of with respect to satisfies

upon substituting and by definition of . Using

and the definition of , for all we obtain

| (B.4) |

Letting and , upon using (B.4) the Hessian matrix is

Suppose is positive definite for all . Positive definiteness of then implies that is positive definite for all if and only if the Schur complement of in is positive definite (Boyd & Vandenberghe, 2004, Appendix A.5.5) for all , i.e., if and only if the determinant of is strictly positive, for all . Letting for all , is equal to

| (B.5) |

a positive semidefinite matrix, and equal to zero if and only if

| (B.6) |

this is an application of the Cauchy-Schwarz inequality for matrices stated in Tripathi (1999). Under Condition 4, system (B.6) cannot hold, with probability 1, for all .

B.3. Proof of Theorem 3

The equivalence result follows by Lemma 2. For , define the Lagrangian for (GD) as

with first-order conditions

| (B.8) |

and denote any vector in satisfying (B.8) by , and the th element of by .

Proof of part (i). Define the Lagrange dual function (Boyd & Vandenberghe, 2004, Chapter 5) for . In order to derive , we show that the maximum of the mapping is attained and is unique, and evaluate at this value.

Step 1. We show that the map admits at least one maximum in for all . Since , existence of a maximum then holds for all . For and , consider the level sets of . These sets are compact. Consider a sequence in such that as . Let , a bounded sequence with unit norm. By the Bolzano-Weierstrass theorem there exists a convergent subsequence , as , with limit , say. Then, using that , and is bounded, for

as , since as . Therefore grows unboundedly as , and is bounded. Since is continuous over for , is also closed. It then follows from the Weierstrass theorem and that there exists , for all .

Step 2. The Hessian matrix of the map is , and is thus negative definite for all . Therefore, is strictly concave with unique maximum for all . With defined in (B.3), and upon using first-order conditions (B.8), direct substitution yields , the maximum of the map for all , and the primal objective function.

Proof of part (ii). By Lemma 3, the first-order conditions of (GP) implied by (B.4) coincide with the system

| (B.9) |

Moreover, the first-order conditions (B.8) and the constraints of (GD) together yield the method-of-moments representation of (GD).

Proof of part (iii). (a) By Condition 5, there exists such that first-order conditions (B.9) are satisfied. By Lemma 3, is strictly convex over . Therefore, is the unique minimum of and uniquely solves (B.9).

By definition, a solution to (GD) with Lagrange multiplier satisfies first-order conditions (B.8). Suppose . By Step 2 in part (i), the map admits a unique maximizer , for all : each pair is well-defined and satisfies first-order conditions (B.8). Since uniquely solves (B.9) over , the pair is the unique pair satisfying system (B.9) in , where is the set of admissible optimal solutions to (GD). It follows that the pair is the unique pair satisfying system (B.9) in . Therefore, the pair uniquely solves (GP) and (GD) over .

Suppose . For , a pair (not necessarily unique) does not satisfy the second-order conditions of (GD). Thus a solution to (GD) with Lagrange multipliers is not a global maximum of (GD) over . Thus there is no solution to (GD) such that both and the value of (GD) is equal to or exceeds the optimal value of (GD) at . Therefore, the pair is the unique optimal solution to (GP) and (GD) over .

(b) By direct substitution and using that , at a solution the value of (GD) is . Using that , at a solution the value of (GP) is . Strong duality then follows from established in (a).

Appendix C Proof of Theorem 4

Proof.

Proof of part (i). Let satisfy and . Then:

for all . The first equality holds by iterated expectations, the second by mean independence, the third by linearity of the expectation, and the last by uniformity of and definition of .

In order to show the converse statement, suppose that does not hold. Following steps similar to the proof of Lemma 2.1 in Donald et al. (2003), and letting , for such that ,

as , which implies for all large enough, since

Now suppose that does not hold. Because includes an intercept, any random variable such that for all must also satisfy for all , and therefore . It follows that in the large limit.

Therefore, for all if and only if and , and the result follows.

Proof of part (ii). Let be a random variable with mean and variance satisfying . Then , for all , by iterated expectations and mean independence.

In order to show the converse statement, suppose that . Letting and such that , and following steps similar to the proof of Lemma 2.1 in Donald et al. (2003),

as , which implies as .

Therefore, a random variable with mean and variance satisfies for all large enough if and only if , and the result follows. ∎

Appendix D Asymptotic Theory

In this Section, denotes a generic constant whose value may vary from place to place.

D.1. Proof of Theorem 5

Letting for , by definition (B.3), can be decomposed as

| (D.1) |

Define , the population objective of the generalized primal problem.

Both existence and consistency of result from strict convexity of , and pointwise convergence of to , since strict convexity and pointwise convergence together imply uniform convergence, as in, for instance, Theorem 2.7 in Newey & Mc Fadden (1994). The asymptotic distribution of follows from the method-of-moments characterization of the estimates given in part (ii) of Theorem 3, and Theorem 3.4 in Newey & Mc Fadden (1994).

Proof of parts (i) and (ii).We verify the conditions of Theorem 2.7 in Newey & Mc Fadden (1994). We first show that is the unique minimizer of in , using the next result.

Lemma 4.

Proof.

We first show that for all . in (D.1) satisfies

| (D.2) |

which has finite expectation if and are bounded. Since and are bounded, in (D.1) satisfies

| (D.3) |

which has finite expectation if and are bounded. It follows that has finite expectation if .

The identity holds with probability one for , and bounded thus implies

| (D.4) |

Therefore,

Bounds (D.2) and (D.3) now imply and , for all since is bounded. Hence for all .

Bound (D.4) implies that . By Lemma 3, and , and . Bound (D.4) together with bounded, boundedness of and Holder’s inequality thus imply that under Condition 8(i). Lemma 3.6 in Newey & Mc Fadden (1994) then implies that is continuously differentiable and that the order of differentiation and integration can be interchanged for . ∎

By Lemma 4, is continuously differentiable and the order of differentiation and integration can be interchanged, for . Moreover, is differentiable for . Letting and , from the proof of Lemma 3,

Applying steps similar to those leading to the bound (D.4) in the proof of Lemma 4 and using that for all shows that has finite expectation for all under Condition 8(i). Therefore, boundedness of and , and Holder’s inequality imply that . It then follows from Lemma 3.6 in Newey & Mc Fadden (1994) that is continuously differentiable, and that the Hessian matrix of is , which is a finite positive definite matrix under the assumed conditions, by application of Lemma 3. Therefore, is strictly convex and is the unique minimizer of in , and Condition (i) of Newey and McFadden’s Theorem 2.7 is verified.

By Condition 6, is in the interior of , which is convex, and is convex with probability 1 by Lemma 3, and their Condition (ii) is verified. Finally, since the sample is independently and identically distributed by assumption, pointwise convergence of to follows from boundedness of , established in the proof of Lemma 4, and application of Khinchine’s law of large numbers. All conditions of Newey and McFadden’s Theorem 2.7 are therefore satisfied, and there exists with probability approaching one and converges in probability to .

Proof of part (iii). Define for , and for , and let , and . By part (ii) of Theorem 3, the Lagrange multiplier vector solves the equations system

| (D.5) |

System (D.5) can be equivalently viewed as minimizing

Asymptotic normality of the method-of-moments estimator then follows after verifying conditions of Theorem 3.4 in Newey & Mc Fadden (1994).

From the proof of Lemma 3, the derivative of with respect to is , for , and , for , which is continuous for all with probability one by definition of and . Thus the mapping is continuously differentiable in with probability one, and Newey and McFadden’s Condition (ii) is satisfied. By definition is independent of which implies that , and the first part of their Condition (iii) is satisfied. In addition, steps similar to the proof of Lemma 4 show that and are finite under Conditions 8, and their Conditions (iii)–(iv) are thus verified. Finally, their full rank condition on is satisfied under our conditions since is then positive definite. Therefore, converges in distribution to with

| (D.6) |

D.2. Proof of Theorem 6

Proof of part (i). Denote the cumulative distribution function of , by for all , and consider the decomposition

| (D.7) |

For the first term, convergence in probability of to 0 is implied by Glivenko-Cantelli (e.g., Theorem 19.1 in van der Vaart, 1998). For the second term, upon using that the events and are equivalent conditional on for , and in particular for , applying iterated expectations, a change of variable and a mean-value expansion, yields

where is on the line connecting and . Since and are uniformly bounded, it follows that

Consistency of and finite then imply convergence in probability of to 0. The result follows from combining the two uniform convergence results.

Proof of part (ii). For , let and , and define the class of functions . Following van der Vaart & Wellner (2007), the empirical dual regression process admits the following decomposition:

| (D.8) |

The proof thus proceeds by (i) establishing that the first term on the right in (D.8) converges in probability to zero, (ii) using the fact that the second term converges in distribution to a mean zero Gaussian process, and (iii) expanding the last term uniformly in .

Step 1. Stochastic equicontinuity. By Theorem 2.1 in van der Vaart & Wellner (2007), since by part (i) of Theorem 5, converges in probability to holds if the class of functions is Donsker and if the pseudometric satisfies converges in probability to 0.

We first show that the class of functions is Donsker. Define the parametric class of functions . For all , a mean-value expansion and Cauchy-Schwarz inequality yield

where is on the line joining and . Steps similar to those in the proof of Theorem 5 show that is bounded under Condition 8, so that is Donsker by Example 19.7 in van der Vaart (1998). Therefore, is Donsker, by monotonicity of the indicator function, with unit envelope.

We now show that converges in probability to . Since the events and are equivalent conditional on for , the law of iterated expectations, a mean-value expansion and Cauchy-Schwarz inequality yield:

where is on the line joining and . Convergence in probability of to zero now follows from finite and consistency of .

Step 2. Expansion. Letting , , we show that the following expansion is valid uniformly in :

| (D.9) |

Steps similar to above yield:

where is on the line joining and . We obtain

uniformly in , by uniform continuity of the mapping , uniformly in over , consistency of , and since , are bounded and is finite. Hence (D.9) holds by definition of , uniformly in .

Finally, the method-of-moments representation of dual regression implies that the dual regression estimator is asymptotically linear with influence function

| (D.10) |

Thus (D.8)–(D.10) together imply that uniformly in

where

Therefore, the empirical dual regression process weakly converges to the zero-mean Gaussian process , where has covariance function

| (D.11) |

Appendix E Numerical Illustrations

E.1. Implementation of generalized dual regression

Define the criterion

where solves , denoted . For such that holds for each , using the strong duality result of Theorem 3, the value of the criterion can be computed as , with the solution of the corresponding dual problem. We then select an even value of according to the following alogorithm:

Step 1. For each in the grid :

Step 1.1. Run program (GD) with basis functions specified as

for , and even. Denote the solution by , with corresponding multipliers .

Step 1.2. Compute .

Step 2. Select the value of that minimizes , denoted .

Results in the empirical application are robust to using a larger grid for . The grid specified above is also used in all simulations. Although the proposed algorithm provides a convenient semi-automated method for the specification of a generalized dual regression representation, it is also instructive to examine the solutions obtained for greater than two. Fig. E.1 plots the solutions , and obtained in Step 1.1. against the selected solution in Step 2. We also plot the solution obtained for a location model, denoted and obtained as . Visual inspection then confirms that although the dual regression solution differs significantly from the location solution , our results are robust to the addition of extra terms in the representation.

E.2. Design and implementation of the numerical simulations

We generate datasets of size according to the model with and , calibrated to Engel’s data. The value of is set to the value of estimates obtained by the method suggested in Koenker & Xiao (2002): for a grid of quantile indices , are estimated by quantile regression, and and are set equal to the estimates obtained from linear regression of on , where is the inverse standard normal distribution. We set and . Thus the quantile regression parameters are and , and . As a benchmark, is also estimated by applying the inversion procedure of Chernozhukov et al. (2010) to the quantile regression process, as , with . Dual regression multipliers yield functional coefficients estimates and , where is the empirical quantile function of and , and with the transformed intercept coefficients accounting for the centering of in the implementation of (GD).

| Sample size | ||||||

|---|---|---|---|---|---|---|

| Sample size | ||||||

| Sample size | ||||||

| Intercept | |||||

| Sample size | Method | Ave. | |||

|---|---|---|---|---|---|

| GDR | |||||

| QR | |||||

| GDR | |||||

| QR | |||||

| GDR | |||||

| QR | |||||

| GDR | |||||

| QR | |||||

| coefficient | |||||

| GDR | |||||

| QR | |||||

| GDR | |||||

| QR | |||||

| GDR | |||||

| QR | |||||

| GDR | |||||

| QR | |||||

Table 2 shows the distribution of selected models across simulations. The 2 and 4 terms representations are selected in most simulations, wth the proportion of incorrect selections decreasing from to as sample size increases. For completeness, Table 3 reports average estimation errors of conditional distribution function estimates across simulations for and terms generalized dual regression and quantile regression-based estimators, respectively, and their ratio in percentage terms. The performance of dual regression estimates in the simulations is robust to incorrect choice of , with only a small loss in accuracy caused by misspecification. For the 8 terms representation, the gains over quantile regression-based estimates remain significant, ranging from to depending on the norm and sample size.

Table 4 summarizes the results corresponding to the accuracy of functional intercept and covariate coefficients estimates across simulations. Estimates are based on the selected model in each simulation. For each coefficient, we compute the root mean absolute error of estimates, by computing errors for quantile indices in for each replication, and then computing the summary statistic. We also report average root mean absolute error over the grid of quantile indices. In all cases selected generalized dual regression estimates have lower root mean absolute error, which corroborates results shown in Table 1 in the main text for the conditional distribution function.

E.3. Additional Simulations

We provide additional simulations comparing dual regression to the noncrossing quantile regression method introduced by Bondell et al. (2010), replicating the experiments they propose. In their simulation study they consider three examples which are special cases of the linear heteroscedastic model

where each component of satisfies , , and with . Their method imposes noncrossing constraints on the quantile regressions estimated, and they show that it outperforms both linear quantile regression and the method of He (1997) in their proposed experiments. The three examples are:

Example 1. , , and .

Example 2. , , and .

Example 3. , , and .

| Example 1 | ||||

|---|---|---|---|---|

| GDR | ||||

| NCRQ | ||||

| GDR (2): Ratio | ||||

| GDR (4): Ratio | ||||

| GDR (6): Ratio | ||||

| GDR (8): Ratio | ||||

| GDR | ||||

| NCRQ | ||||

| GDR (2): Ratio | ||||

| GDR (4): Ratio | ||||

| GDR (6): Ratio | ||||

| GDR (8): Ratio | ||||

| GDR | ||||

| NCRQ | ||||

| GDR (2): Ratio | ||||

| GDR (4): Ratio | ||||

| GDR (6): Ratio | ||||

| GDR (8): Ratio |

| Example 2 | ||||

|---|---|---|---|---|

| GDR | ||||

| NCRQ | ||||

| GDR (2): Ratio | ||||

| GDR (4): Ratio | ||||

| GDR (6): Ratio | ||||

| GDR (8): Ratio | ||||

| GDR | ||||

| NCRQ | ||||

| GDR (2): Ratio | ||||

| GDR (4): Ratio | ||||

| GDR (6): Ratio | ||||

| GDR (8): Ratio | ||||

| GDR | ||||

| NCRQ | ||||

| GDR (2): Ratio | ||||

| GDR (4): Ratio | ||||

| GDR (6): Ratio | ||||

| GDR (8): Ratio |

For each example, 500 datasets of size 100, 200 and 500 are simulated. For the method of Bondell et al. (2010), six quantile curves are fitted to the data for each example, . We also implemented the noncrossing quantile regression method by fitting eleven quantile curves for the larger sequence , the results are similar and are thus omitted.

Tables 5–7 show the average root mean integrated squared errors over the 500 datasets along with their estimated standard errors, for each sample size, and for each of . For each simulation, the empirical root mean integrated squared error is calculated as , where and are the estimated and true vector of quantile regression coefficients, respectively. The results for the other quantiles are similar, and are thus omitted.

In all three examples the location-scale structure, , is selected by the Schwartz criterion for each simulation and our proposed estimator significantly outperforms the noncrossing quantiles method for all quantiles and all sample sizes, except for and in Example 2. The good relative performance of dual regression results from the selected location-scale structure, which adds further smoothness and stability across quantile curves, beyond the noncrossing constraints imposed by noncrossing quantile regression. This improvement is greater in the tails, as dual regression solutions are estimated globally whereas the local nature of quantile regression affects estimation of extreme quantiles.

We also report the relative performance of non-selected dual regression estimates. Apart from Examples 2 and 3 with , the results are similar for all to the selected model . For , results for Example 2, and to a lesser extent Example 3, show that the relative performance of dual regression deteriorates, especially for . These results are driven by a few simulations where the solver was unable to find an optimal solution, 7 instances for Example 2 and 5 for Example 3. Since for Example 2 and the number of parameters is for 100 observations, this is not unexpected. Compared to the simulations calibrated to the Engel data example, the fact that representations with greater 2 are never selected for Examples 1–3 suggest that the presence of multiple covariates provides useful information effectively accounted for by the proposed model selection procedure.

| Example 3 | ||||

|---|---|---|---|---|

| GDR | ||||

| NCRQ | ||||

| GDR (2): Ratio | ||||

| GDR (4): Ratio | ||||

| GDR (6): Ratio | ||||

| GDR (8): Ratio | ||||

| GDR | ||||

| NCRQ | ||||

| GDR (2): Ratio | ||||

| GDR (4): Ratio | ||||

| GDR (6): Ratio | ||||

| GDR (8): Ratio | ||||

| GDR | ||||

| NCRQ | ||||

| GDR (2): Ratio | ||||

| GDR (4): Ratio | ||||

| GDR (6): Ratio | ||||

| GDR (8): Ratio |

References

- Bondell et al. (2010) Bondell, H., Reich, B. and Wang, H. (2010). Noncrossing quantile regression curve estimation. Biometrika 97, 825–838.

- Boyd & Vandenberghe (2004) Boyd, S. P. and Vandenberghe, L. (2004). Convex Optimization. Cambridge University Press.

- Carlier et al. (2016) Carlier, G., Chernozhukov, V., & Galichon, A. (2016). Vector quantile regression: an optimal transport approach. Annals of Statistics 44, 1165–1192.

- Cosma et al. (2007) Cosma, A., Scaillet, O., & Von Sachs, R. (2007). Multivariate wavelet-based shape-preserving estimation for dependent observations. Bernouilli 13, 301–329.

- Chernozhukov et al. (2010) Chernozhukov, V., Fernandez-Val, I. & Galichon, A. (2010). Quantile and probability curves without crossing. Econometrica 78, 1093–1125.

- Chernozhukov et al. (2013) Chernozhukov, V., Fernandez-Val, I. & Melly, B. (2013). Inference on Counterfactual Distributions. Econometrica 81, 2205–2268.

- DeVore (1977) De Vore, R. (1977). Monotone approximation by splines. SIAM Journal on Mathematical Analysis 8, 891–905.

- Donald et al. (2003) Donald, S.G., Imbens, G.W. and Newey W.K. (2003). Empirical likelihood estimation and consistent tests with conditional moment restrictions. Journal of Econometrics, 117, 55–93.

- Durbin (1973) Durbin, J. (1973). Weak convergence of the sample distribution function when parameters are estimated. Annals of Statistics, 1, 279–290.

- Genest et al. (2007) Genest, C., Quessy, J.-F., & Remillard, B. (2007). Asymptotic local efficiency of Cramer–von Mises tests for multivariate independence. Annals of Statistics 35, 166–191.

- He (1997) He, X. (1997). Quantile Curves without Crossing. The American Statistician 51, 186–192.

- Huber (1981) Huber, P. (1981). Robust Statistics. Wiley, New York.

- Koenker (2005) Koenker, R. (2005). Quantile Regression. Cambridge University Press.

- Koenker & Bassett (1978) Koenker, R. & Bassett, G. (1978). Regression quantiles . Econometrica 46, 33–50.

- Koenker & Xiao (2002) Koenker, R. & Xiao, Z. (2002). Inference on the quantile regression process. Econometrica 70, 1583–1612.

- Koenker & Zhao (1994) Koenker, R. & Zhao, Q. (1994). L-estimation for linear heteroscedastic models. Nonparametric Statistics 3, 223–235.

- Newey & Mc Fadden (1994) Newey, W. & Mc Fadden, D. (1994). Large sample estimation and hypothesis testing. In Handbook of Econometrics, vol. 4, ch. 36, 1st ed., pp. 2111–2245. Amsterdam: Elsevier.

- Owen (2001) Owen, A. B. (2001). Empirical Likelihood. Chapman&Hall/CRC, Boca Raton, USA.

- Parker (2013) Parker, T. (2013). A comparison of alternative approaches to supremum-norm goodness-of-fit tests with estimated parameters. Econometric Theory 29, 969–1008.

- R Development Core Team (2017) R Development Core Team (2017). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing. Vienna, Austria. ISBN 3-900051-07-0. http://www.R-project.org.

- Schwarz (1978) Schwarz, G. (1978). Estimating the dimension of a model. The Annals of Statistics 6, 461–464.

- Tripathi (1999) Tripathi, G. (2006). A matrix extension of the Cauchy-Schwarz inequality. Economics Letters 63, 1–3.

- van der Vaart (1998) van der Vaart, A.W. (1998). Asymptotic Statistics. Cambridge University Press.

- van der Vaart & Wellner (2007) van der Vaart, A.W. and Wellner, J. (2007). Empirical processes indexed by estimated functions. Lecture Notes-Monograph Series, 234–252.