Detection of weak signals in high-dimensional complex-valued data

Alexei Onatski

University of Cambridge, ao319@cam.ac.uk.

Abstract

This paper considers the problem of detecting a few signals in

high-dimensional complex-valued Gaussian data satisfying Johnstone’s (2001)

spiked covariance model. We focus on the difficult case where

signals are weak in the sense that the sizes of the corresponding covariance

spikes are below the phase transition threshold studied in Baik et

al (2005). We derive a simple analytical expression for the maximal possible

asymptotic probability of correct detection holding the asymptotic

probability of false detection fixed. To accomplish this derivation, we

establish what we believe to be a new formula for the Harish-Chandra/Itzykson-Zuber (HCIZ) integral , where has a deficient rank . The formula links the

HCIZ integral over to an HCIZ integral over a

potentially much smaller unitary group . We

show that the formula generalizes to the integrals over orthogonal and

symplectic groups. In the most general form, it expresses the hypergeometric

function of two matrix arguments as a

repeated contour integral of the hypergeometric function of two matrix arguments.

Much contemporary research in statistics concerns with situations where the

dimensionality of data is large and comparable to the number of observations

(see special issues of the Philosophical Transactions of the Royal

Society (2009) 367 and Annals of Statistics (2008)

36). Often, the goal is to estimate or detect a few signals

contaminated by high-dimensional noise. One general conclusion that seems to

emerge from this research is that, in the absence of a priori

sparsity assumptions about signals, there is a lower limit for the

signal-to-noise ratio below which statistical inference about the signals

completely fails (Johnstone and Titterington, 2009, Nadakuditi and Edelman,

2008, Nadakuditi and Silverstein, 2010). This limit equals the phase

transition threshold studied in Baik et al (2005). In a recent paper,

Onatski et al (2012) show that not all is lost below the threshold. They

consider the case of a single non-sparse signal in high-dimensional noisy

data and establish sharp non-trivial limits for the asymptotic power, as

both the data dimensionality and the number of observations go to infinity,

of statistical tests for signal detection when the signal may be arbitrarily

weak.

This paper extends Onatski et al (2012) to the case of multiple non-sparse

arbitrarily weak signals when the data are complex-valued. Complex-valued

data are of interest in signal processing (Schreier and Scharf, 2010),

wireless communication (Telatar, 1999, Tulino and Verdu, 2004), and the

spectral analysis of economic and financial time series (Onatski, 2009).

Considering the case of multiple signals is important for applied work

because the constraint that there is no more than one signal can rarely be

justified in practice. We derive a simple analytical expression for the

maximal possible asymptotic probability of correct detection, based on the

sample covariance eigenvalues of the data, holding the asymptotic

probability of false detection fixed.

We find that the asymptotic probability of detection may be close to one

even in cases where the strength of all signals is substantially below the

phase transition threshold. This finding is, perhaps, surprising in light of

the fact (Péché, 2003) that in such cases, sometimes referred to as

the sub-critical regime, the asymptotic behavior of any finite number of the

largest sample covariance eigenvalues is not different from their behavior

when the data are pure noise. We show that in these difficult cases, the

detection power lies not in the different behavior of a few of the largest

eigenvalues, but in the small deviations of the empirical distribution of

all the eigenvalues from the Marchenko-Pasturlimit

(Marchenko and Pastur, 1967).

Let us discuss our findings in more detail. We assume that data consist of independent observations of -dimensional complex-valued Gaussian

vectors with mean zero and covariance matrix , where is the -dimensional

identity matrix, is a real scalar, is an real

diagonal matrix with elements along the diagonal, and is a

-dimensional complex parameter normalized so that . Such a spiked covariance model was

proposed by Johnstone (2001) as a simple model of a situation, often

observed in applications, where a few eigenvalues of the sample covariance

matrix, corresponding to signals, are relatively large, whereas the rest of

the eigenvalues are relatively small and tightly clustered. In our notation,

the size of the spikes is regulated by the values of and the signal

space is spanned by the columns of matrix .

Let be the ordered

eigenvalues of where ,

and let where . We are interested in the asymptotic power of

tests for signal detection based on the information contained in

when so that with .

Our null hypothesis is (no signals), and our

alternative is for some . The matrix is

left as an unspecified nuisance parameter. In this framework, signal

detection tests can also be interpreted as tests of sphericity.

We consider both cases of specified and unspecified . For the

purpose of brevity, in the introduction, we will discuss only the case of

specified . First, we study the likelihood ratio defined as the ratio of the densities of

corresponding to unrestricted and restricted , the densities being

evaluated at the observed value of . We show that can be represented in the form of the determinant of an matrix with entries equal to contour integrals of elementary

functions. We use Laplace approximations to these contour integrals to show

that for any such that with being

the value of the phase transition threshold, the sequence of log-likelihood

processes

converges weakly to a Gaussian process111Here the index in the notation is

used to distinguish the limiting log-likelihood process in the case of

specified from that in the case of unspecified which we denote by . under the null

hypothesis as . The limiting process has mean and autocovariance

function . The established weak convergence of

statistical experiments implies, via Le Cam’s first lemma (see van der Vaart

1998, p.88), that the joint distributions of the sample covariance

eigenvalues under the null and under alternatives associated with are mutually contiguous.

An asymptotic power envelope for eigenvalue-based tests of against can be constructed using the Neyman-Pearson lemma and Le Cam’s third

lemma. We show that, for tests of size the maximum achievable

asymptotic power against a point alternative equals where is the standard normal distribution function and . A preliminary analysis indicates that

the asymptotic power of the likelihood ratio test based on the information

contained in is close to the asymptotic power envelope. In

contrast, we find that the asymptotic powers of various previously proposed

tests are well below the envelope.

The central technical result of this paper is the contour integral

representation of the likelihood ratio. To derive such a representation, we

establish what we believe to be a novel formula for the hypergeometric

functions of two matrix arguments

where a matrix has rank so that, without loss of

generality, only its upper-left block is non-zero.

Such functions appear as a key term in the explicit expressions for the

joint density of the eigenvalues of Wishart matrices with spiked covariance

parameter. In Lemma 1, we show that

(1)

where is an

auxiliary matrix, and

is a simple function of and . This formula expresses the

hypergeometric function of high-dimensional arguments as a repeated contour

integral of a hypergeometric function of low-dimensional arguments, which is

convenient for analysis.

For the special case (1) reduces to the formula that has

been recently derived in Mo (2011) and, independently, in Wang (2012) and

Onatski et al (2012) (see also Forrester, 2011 for a short derivation). Our

method of proof is different from the methods used by these authors. It is

based on the orthogonality of Jack polynomials with respect to the torus

scalar product (Macdonald (1995), Chapter VI, §10).

Although our analysis of signal detection in complex data requires only the

formula for we establish (1) for all where is a positive integer.222For cases where is odd, we require that be even. For even such a requirement is not needed. The importance of finding

“serviceable approximations” to has been recently emphasized by Johnstone

(2007, p.322). Since in applications that rely on the spiked covariance

matrix framework is typically much smaller than , analyzing is much easier than

analyzing , and the established contour

integral representation of the latter may be of the welcomed service to

practitioners.

For and function has an integral representation where is the

orthogonal group for , the unitary group for , and the compact symplectic group for and where is the normalized Haar measure over . Such integrals have various important applications in

mathematics and physics, where they are referred to as

Harish-Chandra/Itzykson-Zuber (HCIZ) integrals (Zinn-Justin and Zuber,

2003). The HCIZ integrals with rank-deficient have been used in the

analysis of spin glasses (Marinari et al, 1994), wireless communication

systems (Muller et al, 2008), statistical tests for signal detection

(Bianchi et al, 2010, and Onatski et al, 2012), distribution of the largest

sample covariance eigenvalue (Mo, 2011, and Wang, 2012), and spiked Wishart -ensembles (Forrester, 2011). Their asymptotic behavior as has been studied in Guionnet and Maïda (2005) and

Collins and Śniady (2007). We hope that the reduction of HCIZ integrals

over large group to those over

smaller group that follows from (1) will be useful in a wide spectrum of applications.

The rest of this paper is organized as follows. In Section 2, we derive

explicit formulae for the likelihood ratios. Section 3 establishes

relationship (1). Section 4 uses (1) to derive

contour integral representations for the likelihood ratios. Section 5

applies Laplace approximations to the contour integrals in the derived

representation to obtain the asymptotics of the likelihood ratio process.

This asymptotics is then used along with the Neyman-Pearson lemma and Le

Cam’s third lemma to establish a simple analytical formula for the maximal

possible asymptotic probability of correct signal detection holding the

asymptotic probability of false detection fixed. Section 6 concludes. All

proofs are relegated to the Appendix.

2 Likelihood ratios

As mentioned above, we assume that data consist of independent

observations of -dimensional complex-valued Gaussian vectors . This means that , where denotes the imaginary unit, and the

joint density of at

equals (see, for example, Goodman, 1963).

Further, we assume that the covariance matrix equals where quantifies the sizes of the covariance spikes. Our

goal is to study the asymptotic power of tests of

against for some .

If is specified, the model is invariant with respect to

unitary transformations and the maximal invariant statistic is ,

the vector of the first eigenvalues of where . Therefore, we

consider tests based on . If is unspecified, the

model is invariant with respect to the unitary transformations and

multiplications by non-zero scalars, and the maximal invariant is the vector

of normalized eigenvalues

where .

Hence, we consider tests based on . Note that the distribution of does not depend on whereas if is specified,

we can always normalize dividing it by . Therefore,

in what follows, we will assume without loss of generality that .

Let , and let us denote the joint density

of as and that of as We have

(2)

where depends only on and ; ; is a diagonal

matrix, so that there are no zeros along the diagonal if ; is the set of all unitary matrices; and is the invariant measure on the unitary group normalized to make the total measure unity.

Formula (2) is a special case of the densities given in

James (1964, p.489) for and in Ratnarajah and Vaillancourt (2005)

for .

Let and let Note that the Jacobian of

the coordinate change from to equals Changing variables in (2) and integrating out, we obtain

(3)

where is

a diagonal matrix.

Consider the likelihood ratios: and . Formulae (2) and (3)

imply the following Proposition.

Proposition 1

Let be the set of all unitary matrices. Denote by the invariant measure on the unitary group normalized to make the total measure unity. Further, let and . Then

(4)

(5)

Our analysis of the asymptotic power of tests for signal detection is based

on a study of the asymptotic properties of the likelihood ratio processes and . First, we will focus on the key terms in the expressions (4) and (5), which are the integrals over the unitary group.

These integrals are special cases of the complex hypergeometric function where

and, possibly, are rank-deficient. In the next section, we derive a

formula for with rank-deficient

and that links this function to a hypergeometric functions of full-rank

matrix arguments of lower dimensions. We do not restrict attention to the

case because, as discussed in the introduction, other cases

constitute independent interest.

3 Contour integral representation for

Let us first provide a necessary background on hypergeometric functions. Let

and be Hermitian matrices over real, complex, or

quaternion division algebra. The eigenvalues of such matrices are real and

we will denote them as and . The hypergeometric function is defined as (see, for example, Koev and Edelman,

2006)

(6)

where and are normalized

Jack polynomials (Macdonald, 1995, chapter VI, §10), and the inner sum

runs over all partitions of that is over all non-increasing

sequences of non-negative integers such that The

normalization of is chosen so that

(7)

Note that depends on and

only through and Therefore, in what follows, without loss of

generality, we will consider only diagonal matrices and We will allow and to be complex,

thus extending definition (6) to complex diagonal matrices and .

As was mentioned in the introduction, for and

hypergeometric functions admit the

integral representation

(8)

where is the orthogonal group for the unitary group for and the compact symplectic group for . For real diagonal and such a representation follows from the fact that (see

Proposition 5.5 of Gross and Richards, 1987), and the fact that

which follows from (7). For complex diagonal and ,

the representation holds by the analytic continuation because both parts of

equality (8) are complex analytic functions of the

diagonal elements of and .

The main result of this section is as follows.

Lemma 1

Let and , where and are real or

complex numbers. Assume that for and

for , and denote the upper left block of as . Further, let where are complex

variables, and let be a contour in the complex plane that

encircles counter-clockwise. Finally, let where is a positive integer. Then, assuming that is an

even integer in cases where is odd, and without this additional

assumption in cases where is even, we have

(1)

where

The proposition reduces , a hypergeometric function with potentially high-dimensional

matrix arguments, to a repeated contour integral of , a

hypergeometric function with matrix arguments of possibly much lower

dimensions. In the special case where and (1) becomes

(9)

For this formula has been established by Mo (2011), who used it

to analyze the asymptotic behavior of the largest eigenvalue of a rank-one

perturbation of a real Wishart matrix. He gives two proofs of the formula.

One of the proofs uses Jack polynomial expansions and requires that be

an even integer (consistent with our requirement that is even). The

other proof, which Mo (2011) calls geometric, allows for odd .

Similar to the first proof of Mo, our proof of Lemma 1 uses Jack polynomial

expansions. In contrast to that proof, we do not rely on the simplification

of the Jack polynomials for top-order partitions, but use Jack polynomials’

orthogonality with respect to the torus scalar product (Macdonald, chapter

VI, §10). It is likely that our requirement that is even in cases

where is odd can be lifted without affecting relationship

(1). This would require a different proof of the

proposition, which is left for future research.

For and with even , formula (9) has been independently established by Wang (2012). He uses

the formula to study the asymptotic distribution of the largest eigenvalue

of the real, complex and quaternionic Wishart matrices perturbed by matrices

of rank one. Wang’s proof is similar to the first proof of Mo (2011) (see

Forrester, 2011, for an alternative proof). For formula (9) has also been independently established by Onatski et al

(2012). Their proof is based on the properties of the so-called Lauricella

function.

In contrast to (9), the general relationship (1) contains special functions on both left- and right-hand sides.

However, for it is possible to further simplify the right-hand

side of (1) using Harish-Chandra/Itzykson-Zuber formula

(see Harish-Chandra, 1957, and Itzykson and Zuber, 1980)

(10)

where and are the Vandermonde

determinants associated with the diagonal elements of and the diagonal elements of ,

respectively. Using (10) in (1), noting that

one of the terms in the definition of equals and applying

Andreief’s identity (Andreief, 1883)

we obtain the following Corollary.

Corollary 1

Under assumptions of Lemma 1,

(11)

An alternative way of deriving (11) is to apply l’Hôpital’s rule to the Harish-Chandra/Itzykson-Zuber determinantal formula

(12)

the right-hand side of which is degenerate because is rank-deficient. We

include a proof of (11) that uses this approach in the

Supplementary Appendix. The proof is elementary in the sense that it does

not rely on properties of Jack polynomials.

4 Likelihood ratios as contour integrals

Combining Proposition 1 and Corollary 1 leads to useful contour integral

representations of the likelihood ratios and . We now introduce new notation to express such

representations in a convenient form. For any let us

define a random variable

(13)

where is the cumulative

distribution function of the Marchenko-Pastur distribution with a point mass

of at zero, where and

density

(14)

where and . Further, let

(15)

(16)

Finally, for any permutation of the sequence and any vector , let

(17)

where

Proposition 2

Let the contour that encircles counter-clockwise be chosen so that for any , . Then

(18)

(19)

where denotes the imaginary unit, the summation in (19) is over all permutations of the sequence ,

In the next section, we perform the asymptotic analysis of and that relies on the Laplace

approximations of the contour integrals in (18) and (19) after the contours are suitably deformed without changing

the value of the integrals.

5 Asymptotic analysis

Consider contours with which are obtained by

deforming the contour defined in Proposition 2 so that passes through

Precisely, we define as where is the complex

conjugate of and with

It is possible to verify that, when , the derivative

of equals zero at . Therefore, choosing

contours of integration so they pass through allows us to use the

method of steepest descent in the asymptotic analysis of the corresponding

integrals in (18) and (19). The next

lemma shows that the change of contours in (18) and (19) does not lead to a change in the value of the

corresponding integrals.

Lemma 2

Suppose that the null hypothesis is true, and let be an arbitrary number such that . Suppose further that

for all . Then, as so that

Our next lemma establishes Laplace approximations to the contour integrals

in (18) and (19) after the change of the

contours. The lemma uses some new notation that we introduce now. When is analytic at let with

be the coefficients in the power series representation

(22)

When is not analytic at , let the

coefficients be arbitrary numbers for all .

Lemma 3

Under the conditions of Lemma 2,

(23)

(24)

where is uniform in and . The branch of the square root in

formulae (23) and (24) is chosen so that .

Using Lemma 3, we establish the following theorem.

Theorem 1

Suppose that the null hypothesis is true (). Let be any fixed number such that

and let be the space

of real-valued continuous functions on equipped with the supremum norm. Then, as so that we have

(25)

(26)

where the terms are uniform in . Furthermore,

and viewed as random

elements of , converge weakly

to and with Gaussian finite-dimensional distributions

such that, for any

(27)

(28)

(29)

(30)

Theorem 1 and Le Cam’s first lemma (van der Vaart (1998), p.88) imply that

the joint distributions of (as well as those

of ) under the null and under the alternative are

mutually contiguous for any . Along with

Le Cam’s third lemma (van der Vaart (1998), p.90), this can be used to study

the “local” powers of tests detecting

signals in noise.

Let and

be the asymptotic powers of the asymptotically most powerful - and

-based tests of size of the null against a point

alternative with . We have

Theorem 2

Let denote the standard normal distribution

function. Then,

(31)

(32)

The theorem implies in particular that detection of signals corresponding to

covariance spikes of sizes well below the phase transition threshold is

possible with high probability. Consider for example the case where the

number of observations equals the dimensionality of data so that the

number of signals under the alternative equals five, and the signals have

equal but rather weak strengths . Then the best

possible -based procedure for detecting such signals with the

asymptotic probability of false detection fixed at 0.05 has asymptotic

probability of correct detection .

Unfortunately, constructing testing procedures with uniformly optimal power

is hard because the log-likelihood process established in Theorem 1 is not

of the Gaussian shift type, so that the statistical experiments we study are

not locally asymptotically normal (LAN) ones. For the case of real-valued

data and Onatski et al (2012) use numerical simulations to show that

the asymptotic powers of the likelihood ratio (LR) tests based on

and on are close to the respective asymptotic power envelopes and . The - and -based LR tests of against the alternative reject the null if and only if , respectively,

and are sufficiently large. As grows,

it becomes increasingly difficult to find the asymptotic critical values for

the LR tests by simulation. This requires simulating an -dimensional

Gaussian random field with the covariance function and the mean function

described in Theorem 1, which, for relatively large , is computationally

expensive.

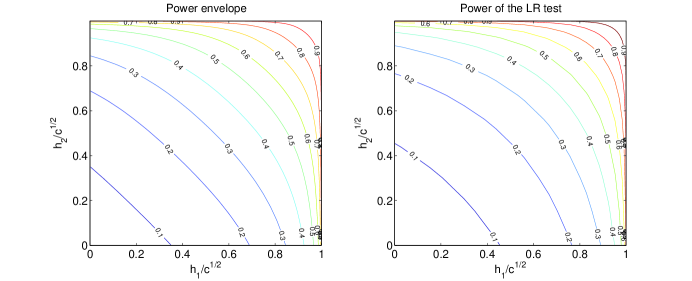

For Figure 2 shows the contour plots of the power

envelope (left panel) and of the

asymptotic power of the likelihood ratio test based on . We chose

parameter so that it is very close to the threshold ,

precisely We see that the contours of and of the asymptotic power of the -based LR test corresponding to the same value of these functions are

relatively close to each other, which suggests that the LR test has good

asymptotic power properties. More detailed analysis of the asymptotic and

finite sample power of the LR test is, however, beyond the scope of this

paper, and is left for future research.

Figure 2: The asymptotic power envelope and the asymptotic power

of the LR test based on ; asymptotic size is .

In contrast to the LR test, the popular signal detection procedures based on

the information in a few of the largest eigenvalues of

(see, for example, Krichman and Nadler (2009), Nadakuditi and Silverstein

(2010), Onatski (2009), Patterson et al (2006), Perry and Wolf (2010), and

Tracy and Widom (2009)), have trivial asymptotic power (that is, the

asymptotic power, which equals the asymptotic size) in the region . It is because the asymptotic behavior of any

finite number of the largest sample covariance eigenvalues when is not different from their behavior when the data

are pure noise (Péché, 2003).

As was mentioned above, signal detection tests can be interpreted as tests

of sphericity. Vice versa, previously proposed sphericity tests, can, in

principle, be used for signal detection. In the Supplementary Appendix, we

use Theorem 1 along with Le Cam’s third lemma to derive asymptotic powers of

several such tests against “spiked

covariance” alternatives. The derived asymptotic powers

turn out to be much lower than the asymptotic power envelopes and . However,

we feel that this comparison is somewhat unfair to the sphericity tests

because they are typically designed against general alternatives, as opposed

to “the spiked covariance” alternatives.

Therefore, and to save space, we do not report these results here.

6 Conclusion

This paper studies the asymptotic power of the signal detection tests in

complex-valued Gaussian data as both the number of observations and data

dimensionality go to infinity. Contrary to the conventional wisdom that

detection of signals becomes nearly impossible when their strength, measured

by the size of the covariance spikes, is below the phase transition

threshold, we find that detection of such signals may be possible with high

probability. The detection power lies not in the different behavior of a few

of the largest sample covariance eigenvalues under the null and the

alternative, which is exploited by the popular signal detection tests, but

in small deviations of the empirical distribution of all the eigenvalues

from the Marchenko-Pastur limit.

To derive our results, we consider the ratio of the densities of the sample

covariance eigenvalues under the null and under the alternative hypothesis.

We establish a contour integral representation of this likelihood ratio, and

use the Laplace approximation to derive its asymptotic limit. Our analysis

of the limiting log-likelihood ratio process shows that the sub-critical

region, where the sizes of the covariance spikes are below the phase

transition threshold, is the region of mutual contiguity of the joint

densities of the sample covariance eigenvalues under the null and the

alternative. We use the derived limiting log-likelihood process along with

Le Cam’s third lemma and the Neyman-Pearson lemma to obtain the asymptotic

power envelope for the signal detection tests. Preliminary analysis

indicates that the asymptotic power of the likelihood ratio test based on

the sample covariance eigenvalues is close to the asymptotic power envelope.

Our technical analysis is based on what we believe to be a novel

representation of the Harish-Chandra/Itzykson-Zuber integral with one of the

matrices being of reduced rank in the form of an

matrix of contour integrals. We obtain such a representation as a corollary

to a much more general result established in Lemma 1. This result expresses

the hypergeometric function of two matrix

arguments, one of which has rank , as a repeated contour integral of the

hypergeometric function of two matrix

arguments. As discussed in the introduction, the established dimension

reduction for the hypergeometric function may be important in various

applied and theoretical fields of study. In particular, for , it

can, potentially, be used to extend the analysis of this paper to the case

of real-valued data. Such an extension is currently under investigation.

7 Appendix

Proof of Lemma 1.

Let and be functions defined on the -dimensional torus Consider the scalar product, sometimes

called the torus scalar product,

(33)

where the contours of integration are the unit circles in the complex plane.

Our proof relies on the orthogonality property of Jack polynomials: for (Macdonald, chapter VI, §10).

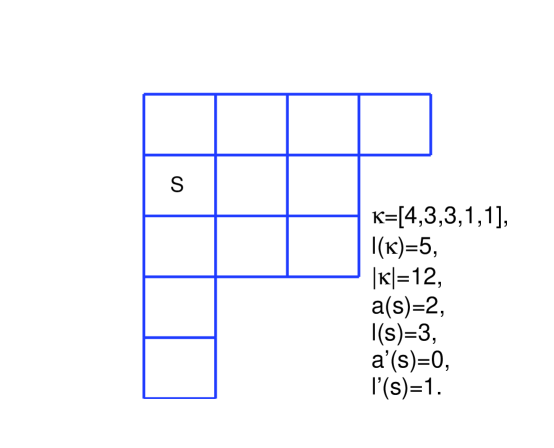

Figure 3: The Ferrers diagram of partition

.

Let us, first, introduce a few definitions (following Macdonald, 1995,

chapter I, §1, and Dumitriu et al, 2007): The non-zero in

the partition are

called the parts of . The number of parts is the length of denoted as The sum of the parts is the weight

of denoted as . We will identify

partition with its Ferrers diagram, defined as an arrangement of boxes in

left-justified rows, the number of boxes in row being the same as (see Figure 3). For each square in the Ferrers

diagram, let and

be respectively the numbers of squares in the diagram to the north, south,

east, and west of the square . Further, let and Finally, let , , and .

We will need the following lemmata.

Lemma A1. For the torus scalar product of with itself, we have

(34)

Proof: Macdonald (1995, Chapter VI, §10) establishes the

orthogonality of “” normalizations of

Jack polynomials, , with respect to the torus

scalar product. His formula (10.37) gives an explicit expression (up to a

constant that can be evaluated using (10.38)) for where (see (10.16)). On

the other hand,

(35)

(see, for example, Table 6 of Dumitriu et al, 2007). Substituting this

expression in Macdonald’s formulae, we get (34).

Lemma A2.Let where are

complex variables, and let be complex constants.

Then

(36)

The series on the right-hand side of this equality converges

uniformly over for any .

Proof: Macdonald (1995, Chapter VI, §10) shows that where . This result

together with (35) imply (36). The uniform

convergence in (36) follows from the fact that function

is analytic in an open region that includes .

We are now ready to prove Lemma 1. Consider the right-hand side of (1), which we will denote as RHS. We will assume that and that the contour is the unit circle in the complex plane. That these assumptions are

without loss of generality follows from the fact that the value of RHS does

not change under the transformation and where is any positive number, and under a deformation of

into the unit circle (because such a deformation leaves the contour in the

region of the analyticity of the integrand). With these assumptions, and

noting that the component of equals we can rewrite

RHS for where is any positive integer, in the

form of the torus scalar product

where

(37)

Substituting and in the above formula by their

expansions (6) and (36) in the series of Jack

polynomials, and interchanging the order of integration and summation, which

is possible because the series converge uniformly over the unit torus, we

obtain

But where denotes

partition . Note

that is well defined for where

is an even integer. If is an odd integer, we need to assume that is even. Therefore, using the orthogonality of the Jack

polynomials with respect to the torus scalar product, we have

Using Lemma A1, (37), and equality we get after some cancellations

(38)

where

In the above expression for substitute and by their explicit forms,

that can be obtained from a general formula

(39)

A variant of this formula, that uses the generalized Pochhammer symbol, can

be found, for example, in Dumitriu et al (2007, Table 5). Then, after

cancellations, we get

Now consider the last ratio of the products in the above expression. For the

product term in the numerator that corresponds to square in the position

in the diagram of there exists exactly the

same term in the denominator, which corresponds to square in the

position in the diagram of . Therefore, we can write

where is the partition that consists of identical parts

Finally, note that

Therefore, and the statement of the lemma

follows from (6) and (38).

Proof of Proposition 2

Proposition 1 and Corollary 1 directly imply (18) and the

following formula for

(40)

where is an matrix with

Let us write as

or equivalently as

(41)

Using this representation, we have

Since the contour is chosen so that for any , the

integrand in the above multiple integral is absolutely integrable on , and

Fubini’s theorem justifies the interchange of the order of the integrals, so

that

The lemma can be proven using arguments very similar to those in the proof

of Lemmas 4 and 6 in Onatski, Moreira and Hallin (2012) (OMH in what

follows), and we omit the proof to save space.

Proof of Lemma 3.

To save space, we will only establish (23), relegating a

conceptually similar but more technical proof of (24) to the

Supplementary Appendix. Lemma 5 in OMH implies that

(42)

where and is uniform in . A careful inspection of OMH’s proof of their Lemma 5 reveals

that a version of (42) remains valid for general functions that are analytic in the open ball with center at and radius with probability approaching 1 as . Precisely, for such general we have

(43)

with

(44)

(45)

(46)

where and are some positive constants, and is a

closed ball with center at and radius .

Now, let . Lemma A2 in OMH implies that uniformly in . Therefore, by (44) and (45),

(47)

Turning to the analysis of , note that by definition of and

(48)

For we have

and for any . Therefore, using (48), we get

On the other hand, for any for sufficiently large and and Indeed, using the definition of

and the fact, established in OMH’s Lemma 11, that we

have

The right hand side of this equality equals at and has a

non-negative derivative with respect to for all Therefore,

and thus, ,

uniformly in . Combining this with (43) and (47), we obtain (23).

Proof of Theorem 1

Proposition 2 and Lemma 3 imply that

As is shown in OMH (see their Lemma 11 and (A8))333Note that the expressions given in OMH are half times the expressions given

below because the equivalent of in the real-valued data case

considered by OMH is ., for ,

(49)

(50)

Moreover, by OMH’s Lemma A2, uniformly in . Using these facts and the definition of given in Proposition

2, we get after some algebra

Turning to the proof of (26), Proposition 2 and Lemma 3

imply that

(51)

Using the definition of and of we get

(52)

Further, using the definition of , the fact that equals the Vandermonde determinant we get

Substituting (52) and (7) into (51), and using (49) and (50) together with the fact that the branch of the

square root in is chosen so that we

get after some algebra

To establish the rest of the statements of Theorem 1 we will need the

following lemma.

Lemma A3. Suppose that our null hypothesis holds. Denote as Then, for any

fixed and and any as so that , the

vector converges in distribution to a Gaussian vector with

Proof: The proof of the lemma is similar to that of Lemma 12 in

OMH. The convergence to the Gaussian distribution follows from Theorem 1.1

of Bai and Silverstein (2004). The formulas for the means, variances and

covariances of and are obtained using Theorem 1.1 iii) of

Bai and Silverstein (2004) similarly to how the corresponding formulas in

Lemma 12 of OMH are obtained using Theorem 1.1 ii). Therefore, below we only

derive the formulae for the mean, variance, and covariances that involve . Variable does not appear in Lemma 12 of OMH because the

lemma does not study the asymptotics of

The fact that follows directly from Theorem 1.1 iii) of

Bai and Silverstein (2004). The same theorem implies that

(54)

where as

(55)

and

(56)

where

with given by (3.6) of OMH, where is replaced by

That is,

(57)

where the branch of the square root is chosen so that the real and the

imaginary parts of have the same signs

as the real and the imaginary parts of , respectively. The contours

of integration in (54)-(56) are closed,

oriented counterclockwise, enclose zero and the support of the

Marchenko-Pastur distribution with parameter , and do not enclose .

The above expressions can be simplified. Use formula 1.16 of Bai and

Silverstein (2004), to get

(58)

(59)

(60)

where

(61)

and the contours of integration over and in (58-60) are obtained from the contours of

integration over and in (54-56) by transformation Recall that by

assumption the contours over and intersect the real line to

the left of zero and in between the upper boundary of the support of the

Marchenko-Pastur distribution, , and Therefore, as can be shown using the definition (57) of , the -contour and -contour are clockwise oriented and intersect the real line in between and and to the right of zero.

In particular, both contours enclose and , but not and .

Assuming without loss of generality that -contour lies inside the -contour, from (A64) in the Supplementary appendix of OMH, we have

where the last equality follows from Cauchy’s residue theorem and the fact

that the contour is oriented clock-wise.

For we have

so that

by Cauchy’s theorem.

For we have

so that

by Cauchy’s theorem.

Lemma A3 and formulae (25) and (26) imply

the convergence of finite dimensional-distributions of the random fields and to the

Gaussian distributions with means and covariance matrices characterized by (27-30).

To complete the proof of Theorem 1, we need to establish the tightness of and , viewed as

random elements of the space as so that Formulae (25-26) and the facts that and that

for where are uniform in imply that for an arbitrarily small positive there must exist such that and for sufficiently large and Since, as

implied by Proposition 1, and are continuous functions on and so that the tightness of and follows.

Proof of theorem 2

To save space, we only derive the asymptotic power envelope for the

relatively more difficult case of real-valued data and -based tests.

According to the Neyman-Pearson lemma, the most powerful test of the null against a point alternative is the

test which rejects the null when is larger than

a critical value It follows from Theorem 1 that, for such a test to

have asymptotic size , must be

(63)

where

Now, according to Le Cam’s third lemma and Theorem 1, under

Therefore, the asymptotic power is (32).

References

[1] Andreief, C. (1883). “Note sur une relation les

intégrales définies des produits des fonctions”, Mém.de la Soc. Sci. Bordeaux 2.

[2] Bai, Z.D. and J.W. Silverstein (2004) “CLT

for Linear Spectral Statistics of Large-Dimensional Sample Covariance

Matrices”, Annals of Probability 32, 553-605.

[3] Baik, J., Ben Arous, G. and S. Péché. (2005)

“Phase transition of the largest eigenvalue for non-null

complex sample covariance matrices” Annals of

Probability 33, 1643–1697.

[4] Bianchi, P., M. Debbah, M. Maïda and J. Najim (2010)

“Performance of Statistical Tests for Single Source

Detection using Random Matrix Theory”, manuscript.

[5] Collins, B. and P. Śniady (2007), “New

scaling of Itzykson-Zuber integrals”, Annales de

l’IHP Prob. Stats. 43 (2), 139–146.

[6] Dumitriu, I., Edelman, A., and G. Shuman (2007)

“MOPS: Multivariate orthogonal polynomials

(symbolically)”, Journal of Symbolic Computation

42, 587–620

[7] Forrester, P.J. (2011), “Probability densities

and distributions for spiked Wishart -ensembles”,

ArXiv:1101.2261.v1

[8] Goodman, N. R. (1963) “Statistical analysis

based on a certain multivariate complex Gaussian distribution, (An

introduction).” Annals of Mathematical Statistics

34, 152-177.

[9] Gross, K.I., and Richards, D.S.P. (1987), “Special Functions of Matrix Argument.I: Algebraic Induction, Zonal

Polynomials, and Hypergeometric Functions”, Transactions of the American Mathematical Society 301 (2), 781-811

[10] Guionnet, A. and M. Maïda (2005), “A

Fourier view on the R-transform and related asymptotics of spherical

integrals”, Journal of Functional Analysis 222

(2), 435–490.

[11] Harish-Chandra (1957) “Differential

Operators on Semi-simple Lie Algebra”, American

journal of Mathematics 79, 87-120.

[12] Itzykson, C., and Zuber, J.B. (1980) “The

Planar Approximation. II”, Journal of Mathematical

Physics 21, 411-421.

[13] James, A. T. (1964) “Distributions of matrix

variates and latent roots derived from normal samples”, Annals of Mathematical Statistics 35, 475-501.

[14] Johnstone, I.M. (2001) “On the distribution of

the largest eigenvalue in principal components analysis.” Annals of Statistics 29, 295–327.

[15] Johnstone, I.M. (2007). “High dimensional

statistical inference and random matrices”, Proceedings of

the International Congress of Mathematicians, Madrid, Spain, 2006. European

Mathematical Society, 307-333.

[16] Johnstone, I.M., and D.M. Titterington (2009).

“Statistical challenges of high-dimensional

data”, Philosophical Transactions of Royal Society

A 367, 4237-4253

[17] Koev, P. and A. Edelman (2006). “The Efficient

Evaluation of the Hypergeometric Function of a matrix

Argument”, Mathematics of Computation 75 (254),

833-846

[18] Krichman, S., and Nadler, B. (2009) “Non-Parametric Detection of the Number of Signals: Hypothesis Testing and

Random Matrix Theory”, IEEE Transactions on Signal

Processing 57, 3930-3941.

[19] Macdonald, I. G. (1995) Symmetric functions and Hall

polynomials. Second edition. Oxford Mathematical Monographs. Oxford Science

Publications. The Clarendon Press, Oxford University Press, New York.

[20] Mo, M.Y. (2011) “The rank 1 real Wishart

spiked model”, arXiv:1101.5144v1

[21] Marchenko, V.A., and L.A. Pastur (1967) “Distribution of eigenvalues for some sets of random

matrices”, Math. USSR-Sbornik, vol. 1, no. 4, 457-483

[22] Marinari, E., Parisi, G., and Ritort, F. (1994),

“Replica field theory for deterministic models. II. A

non-random spin glass with glassy behavior”, J.

Phys. A 27 (23), 7647–7668.

[23] Muller, R.R., Guo, D., and Moustakas, A.L (2008)

“Vector precoding for wireless MIMO systems and its replica

analysis” IEEE Journal of Selected Areas in

Communications 26 (3), 530-540

[24] Nadakuditi, R.R. and A. Edelman (2008) “Sample

Eigenvalue Based Detection of High-Dimensional Signals in White Noise Using

Relatively Few Samples”, IEEE Transactions on

Signal Processing 56, 2625-2638

[25] Nadakuditi, R.R. and J.W. Silverstein (2010) “Fundamental Limit of Sample Generalized Eigenvalue Based Detection of

Signals in Noise Using Relatively Few Signal-Bearing and Noise-Only

Samples”, IEEE Journal of Selected Topics in

Signal Processing 4, 468-480.

[26] Onatski, A. (2009) “Testing Hypotheses About

the Number of Factors in Large Factor Models”, Econometrica 77, 1447-1479.

[27] Onatski, A., Moreira, M. J., and Hallin, M. (2012)

“Asymptotic Power of Sphericity Tests for High-dimensional

Data”, manuscript, Economics Faculty, University of

Cambridge.

[28] Patterson, N., A. L. Price, and D. Reich (2006)

“Population Structure and Eigenanalysis”,

PLoS Genetics 2 (12), 2074-2093

[29] Péché, S. (2003). “Universality of

local eigenvalue statistics for random sample covariance

matrices,” Ph.D. thesis, Ecole Polytechnique Fédérale de Lausanne.

[30] Perry, P.O. and P.J. Wolfe (2010) “Minimax

Rank Estimation for Subspace Tracking”, IEEE

Journal of Selected Topics in Signal Processing 4, 504-513

[31] Ratnarajah, T. and R. Vaillancourt (2005) “Complex Singular Wishart Matrices and Applications”,

Computers & Mathematics with Applications 50, 399–411.

[32] Schreier, P.J., and L. L. Scharf (2010), Statistical Signal

Processing of Complex-Valued Data: The Theory of Improper and Noncircular

Signals, Cambridge University Press.

[33] Telatar, E. (1999), “Capacity of Multi-antenna

Gaussian Channels”, European Transactions on

Telecommunications 10 (6), 585-595.

[34] Tracy, C.A., and Widom, H. (2009) “The

Distributions of Random Matrix Theory and their

Applications”, in V. Sidoravičius (ed.), New Trends in

Mathematical Physics, Springer Science + Business Media B.V., 753-765

[35] Tulino, A. and Verdú, S. (2004). Random Matrix Theory and

Wireless Communications. Foundations and Trends in Communications and

Information Theory 1. Now Publishers, Hanover, MA.

[36] van der Vaart, A.W. (1998) Asymptotic Statistics, Cambridge

University Press.

[37] Wang, D. (2010) “The largest eigenvalue of

real symmetric, Hermitian and Hermitian self-dual random matrix models with

rank one external source, part I.” arXiv:1012.4144

[38] Zinn-Justin, P. and J.-B. Zuber (2003) “On

some integrals over the U(N) unitary group and their large N

limit”, Journal of Physics A. 36 (12), 3173-3193