1 Introduction

The comparison and clustering of different time series is an important topic in statistical data analysis and has various applications in fields like economics, marketing, medicine and physics, among many others. Examples are the grouping of stocks in several categories for portfolio selection in finance or the identification of similar birth and death rates in population studies. One approach to identify similarities or dissimilarities between two stationary processes is to compare the spectral densities of both time series, which directly yields to the testing problem for equality of spectral densities in multivariate time series data. This problem has found considerable interest in the literature [see for example Jenkins, (1961) or De Souza and Thomson, (1982) for some early results], but in the nonparametric situation nearly all proposed procedures are only reasoned by simulation studys or heuristic proofs, see Coates and Diggle, (1986), Pötscher and Reschenhofer, (1988), Diggle and Fisher, (1991) and Maharaj, (2002) among many others. Most recently Eichler, (2008), Dette and Paparoditis, (2009), Dette et al., (2011), Jentsch and Pauly, (2011) and Dette and Hildebrandt, (2011) provided mathematical details for the above testing problem using different -type statistics, but nevertheless in all mentioned articles it is always required that the different time series have the same length, which is typically not the case in practice. Caiado and Pena, (2009) considered different metrics for the comparison of time series with unequal sample sizes in a simulation study and Jentsch and Pauly, (2012) provided a theoretical result, which however does not yield a consistent test as it was also pointed out by the authors.

This paper generalizes the approach of Dette et al., (2011) to the case of unequal sample sizes and yields a consistent test for the equalness of spectral densities for time series with different length. Although the limiting distribution will be the same as in Dette et al., (2011) note that our proof is completely different. This is due to the fact that one essential part in the proofs of Dette et al., (2011) is that the different processes have the same Fourier coefficents which is not given if the observed time series have different sample sizes. For the sake of brevity we will focus on the case of two (not necessarily independent) stationary processes, but the results can be easily extended to the case of an dimensional process.

Our aim throughout this paper is to estimate the -distance , where and are the spectral densities of the first and the second process respectively. Under the null hypothesis

|

|

|

(1.1) |

the distance equals zero while it is strictly positive if for , where is a subset of with positive Lebesgue measure. We will estimate by sums of the (squared) periodogram, where the sum goes over the Fourier coefficents of the smaller time series. Asymptotic normality both under the null and the alternative will be derived and since the variance terms can be easily estimated also under the alternative, asymptotic confidence intervalls and a precise hypothesis test can be constructed next to the test for (1.1) [see Remark 2.2]. Furthermore our approach has much wider application like testing for zero correlation, discriminant analysis or clustering of time series with unequal length [see Remark 2.3–2.4], and a simulation study will indicate that some of our assumptions are in fact not necessary (for example our method seems to work also for Long Memory processes).

2 The test statistic

Let with and consider the two stationary time series

|

|

|

|

|

(2.1) |

where the are independent and identically standard normal distributed for and

|

|

|

(2.2) |

where and . This roughly speaking means that changes in the time series with less observations influence the more frequently observed series but not vice versa, which is for example the case if interest rates and stock returns are compared. Throughout the paper we also assume that the technical condition

|

|

|

(2.3) |

is satisfied for an (). Note that the assumption of Gaussianity is only imposed to simplify technical arguments [see Remark 2.5]. Furthermore innovations with variances different to can be included by choosing other coefficents . We define the spectral densities () through

|

|

|

An unbiased (but not consistent) estimator for is given by the periodogram

|

|

|

(2.4) |

and although the periodogram does not estimate the spectral density consistently, a Riemann-sum over the Fourier coefficents of an exponentiated periodogram is (up to a constant) a consistent estimator for the corresponding integral over the exponentiated spectral density. For example, Theorem 2.1 in Dette et al., (2011) yields

|

|

|

(2.5) |

where () are the Fourier coefficents of the smaller time series . If we can show that

|

|

|

|

(2.6) |

|

|

|

|

(2.7) |

we can construct an consistent estimator for through .

Although (2.6) looks very much like (2.5), note that the convergence in (2.6) is different since the coefficents are not necessarily the Fourier coefficents of the time series . This implies that the proof of (2.6) has to be done in a completely different way than the proof of (2.5) in Dette et al., (2011). We now obtain the following main theorem.

Theorem 2.1

If , and are Hölder continuous of order and

|

|

|

(2.8) |

for a , then as

|

|

|

with

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Although condition (2.8) imposes some restrictions on the growth rate of and , it is not very restrictive, since in practice there usually occur situations where even holds for a (if for example daily data are compared with monthly data) and on the other hand this condition needs only to be satisfied in the limit. From Theorem 2.1 it now follows by a straightforward application of the Delta-Method that , where , which becomes under . To obtain a consistent estimator for the variance under the null hypothesis we define

|

|

|

|

and analogous to the proof of Theorem 2.1 it can be shown that

|

|

|

Therefore an asymptotic niveau--test for (1.1) is given by: reject (1.1) if

|

|

|

(2.9) |

where denotes the quantile of the standard normal distribution. This test has asymptotic power where is the distribution function of the standard normal distribution. This yields that the test (2.9) has asymptotic power one for all alternatives with .

Remark 2.2

It is straightforward to construct an estimator , which converges to the variance also under the alternative. This enables us to construct asymptotic confidence intervals for . The same statement holds, if we consider the normalized measure ,which can be estimated by .

From Theorem 2.1 and a straightforward application of the delta method, it follows that

|

|

|

(2.10) |

where can be easily calculated. By considering a consistent estimator for (which can be constructed through the corresponding Riemann sums of the periodogram), (2.10) provides an asymptotic level test for the so called precise hypothesis

|

|

|

(2.11) |

where [see Berger and Delampady, (1987)]. This hypothesis is of interest, because spectral densities of time series in real-world applications are usually never exactly equal and a more realistic question is then to ask, if the processes have approximately the same spectral measure. An asymptotic level test for (2.11) is obtained by rejecting the null hypothesis, whenever .

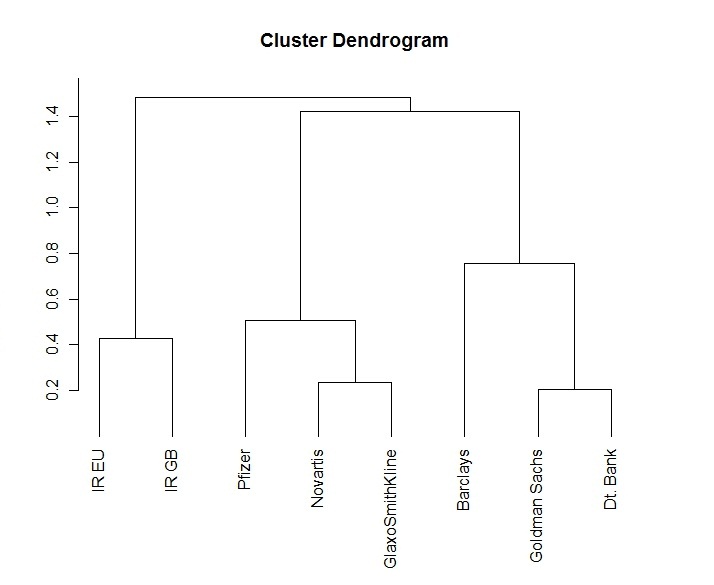

Remark 2.3

Theorem 2.1 can also be employed for a cluster and a discriminant analysis of time series data with different length, since it yields an estimator for the distance measure , where

|

|

|

|

|

which can take values between 0 and 1. A value close to 0 indicates some kind of similarities between two processes, whereas a value close to 1 exhibits dissimilarities in the second-order structure. The distance measure can be estimated by

|

|

|

|

|

(2.12) |

where the maximum is necessary, because the term might be negative.

Remark 2.4

The main ideas of the proof of Theorem 2.1 can be furthermore employed to construct tests for various other hypothesis. For example a test for zero correlation can be derived by testing for which can be done by estimating . An estimator for this quantity is easily derived using the above approach and furthermore the calculation of the variance is straightforward, which we omit for the sake of brevity.

Remark 2.5

Although we only considered the bivariate case, our method can be easily extended to an dimensional process. Moreover, a cumbersome but straightforward examination yields that our test also has asymptotic level , if we skip the assumption of Gaussianity since (under the null hypothesis) all terms which consist the fourth cumulants of the processes cancel out. A similar phenomenon can be observed for the tests proposed by Eichler, (2008), Dette et al., (2011), Dette and Hildebrandt, (2011) and Dette et al., (2011).

4 Appendix: Technical details

Proof of Theorem 2.1: By using the Cramer-Wold device, we have to show that

|

|

|

for all vectors . For the sake of brevity, we restrict ourselve to the case since the more general follows with exactly the same arguments. Therefore we show and we do that by using the method of cumulants, which is described in chapter 2.3. of Brillinger, (1981) (and whose notations we will make heavy use of), i.e. in the following it is proved that

|

|

|

|

(4.1) |

|

|

|

|

(4.2) |

which will yield the assertion.

Proof of (4.1) for the case : Because of the symmetry of the periodogram, it is

|

|

|

|

|

|

|

|

|

|

and because of the standard normality of the innovations we obtain

|

|

|

|

|

|

|

|

which yields that (without the -term) can be divided into the sums of three terms which are called , and respectively. For the first term we obtain the conditions (all others cases are equal to zero). This results in

|

|

|

|

|

|

|

|

|

|

where the last equality follows from

|

|

|

(4.3) |

with , where (2.3) was used. It now follows by the Hölder continuity condition that equals . If we consider the summand , we obtain the conditions ,

which yields

|

|

|

|

|

|

|

|

|

|

If we now employ the identity

|

|

|

(4.4) |

it follows with (2.8) that if is chosen there are only finitely many which yields a non-zero summand. Therefore we obtain that

and with the same arguments it can be shown that .

Proof of (4.2): It is

|

|

|

|

and the assertion follows if we show that

|

|

|

|

|

(4.5) |

|

|

|

|

|

(4.6) |

We present a detailed proof of (4.5) and then comment briefly on (4.6) since it is proved analogously. Employing the symmetry of the periodogram again, we get

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where the sum goes over all indecomposable partitions of

|

|

|

with (we only have to consider partitions with two elements in each set, because of the Gaussianity of the innovations; in the non-Gaussian case we would get an additional term containing the fourth cumulant). Every chosen partition will imply conditions for the choice of as in the calculation of the expectation. For some partitions there will not be a in the exponent of after inserting the conditions and for other partitions there will still remain one. Let us take an example of the latter one and consider the partition which corresponds to . We name the corresponding term of this partition in (4) with and obtain the conditions , , , which yields

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where the last equality again follows with (4.3). Now as in the handling of in the calculation of the expectation, (4.4) implies that .

Every other indecomposable partition is treated in exactly the same way and there are only three partitions which corresponding term in (4) does not vanish in the limit. These partitions correspond to one of the following three terms:

|

|

|

|

|

|

|

|

|

We will exemplarily present the calculation concerning the partition and denote the corresponding sum in (4) with . We get that equals

|

|

|

|

|

|

|

|

|

|

by using (4.3). Now the Hölder continuity condition implies and since the partitions and yield the same result, we have shown (4.5).

With the same arguments as in the proof of (4.5) it can be seen that

|

|

|

|

|

|

|

|

|

|

|

|

and it is shown completely analogously to the proof of (4.5) that

|

|

|

both converge to , which yields (4.6).

Proof of (4.1) for the case : Since the proof is done by combining standard cumulants methods with the arguments that are used in the previous proof, we will restrict ourselve to a brief explanation of the main ideas. We obtain

|

|

|

|

|

|

|

|

|

|

|

|

and if we now take a indecomposable partition of

|

|

|

which consists only of sets with two elements (again this suffices because of the Gaussianity of the innovations), it follows directly that at most of the variables (, ) are free to choose. By using the same arguments as in the calculation of the variance and the expectation it then follows by the indecomposability of the partition that in fact only of the remaining variables are free to choose. This implies which yields the assertion.