sectioning ection]subsection \setkomafontcaptionlabel

Simplified Pair Copula Constructions — Limits and Extensions

Abstract

So called pair copula constructions (PCCs), specifying multivariate distributions only in terms of bivariate building blocks (pair copulas), constitute a flexible class of dependence models. To keep them tractable for inference and model selection, the simplifying assumption that copulas of conditional distributions do not depend on the values of the variables which they are conditioned on is popular. In this paper, we show for which classes of distributions such a simplification is applicable, significantly extending the discussion of \shortciteNhaff2010b. In particular, we show that the only Archimedean copula in dimension which is of the simplified type is that based on the gamma Laplace transform or its extension, while the Student-t copula is the only one arising from a scale mixture of Normals. Further, we illustrate how PCCs can be adapted for situations where conditional copulas depend on values which are conditioned on.

Keywords: archimedean copula; elliptical copula; pair copula construction; conditional distribution

1 Introduction

Growing capabilities to store large data sets and increasing computing power for their computational analysis substantially increased the demand to develop statistical methodology for many dependent variables over the last years. The properties of high-dimensional distributions in general, however, remain hard to understand intuitively. Given that, the early focus was on the multivariate Normal distribution, which allows to describe the whole dependence structure by specifying bivariate correlations. These linear dependencies between just two variables remain easy to understand and communicate. But more recent developments, in particular in econometrics (c.f. \citeNlongin2001, \citeNang2002b), showed that many data sets in higher dimensions exhibit more complex dependence structures.

To deal with these challenging structures and keeping the model understandable at the same time, a popular technique is to sequentially decompose the joint distributions into bivariate building blocks by conditioning. These are then modeled using bivariate copulas of which many parametric families are well studied, see for example the monographs by \citeNJoe and \citeNNelsen. Distributions arising from such a decomposition are called pair copula constructions (PCCs). The question for which classes of multivariate models and under which assumptions such a sequential conditioning is possible, however, remained unsolved. The only publication in this direction is \shortciteNhaff2010b, providing first illustrative examples.

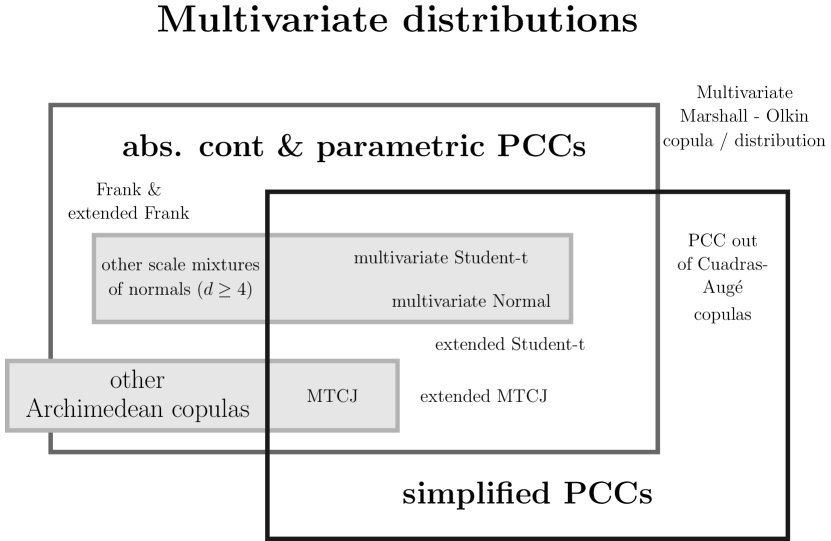

In this paper, we fill in this gap by classifying multivariate distributions in terms of the dependence properties of their conditional distributions (see Figure 1). Special attention will be paid to the simplifying assumption that the copulas corresponding to conditional distributions are constant irrespective of the values of variables that they are conditioned on. This assumption is usually made to keep model selection and inference tractable, and we will show for which multivariate distributions it holds. Furthermore, we discuss how constructions based on simplified PCCs can be extended when the simplifying assumption is not applicable.

The remainder is structured as follows. Section 2 introduces PCCs. In Section 3 and 4, we demonstrate which Archimedean and elliptical copulas are simplified PCCs. Section 5 provides the remaining examples for the classification in Figure 1 and considers the increased flexibility gained by weakening the simplifying assumption. Section 6 concludes with an outlook to areas of future research.

2 Pair copula constructions

A copula is defined as the cumulative distribution function (cdf) of a multivariate distribution with uniform margins. These have become of great importance in multidimensional dependence modeling, since the theorem of \citeNsklar allows to separate the specification of a -dimensional distribution into specifying the univariate marginal distribution functions , , and a copula , i.e., to find such that

Here, we use the abbreviation for . In particular bivariate copula families are well studied, and every multivariate distributions can be constructed from marginal distributions and two-dimensional copulas by sequential conditioning, a so-called pair-copula construction. While different principles for PCCs such as regular vines (R-vines) (\citeANPbedford2001 2001; 2002) or non-Gaussian directed acyclic graphs (DAGs) Bauer et al. (2011) have been investigated over the years, the underlying basic idea is always that of Joe (1996):

Let us consider three random variables (rvs) , and with corresponding cumulative distribution functions (cdfs) and , then we can first construct a joint distribution of and of by assigning copula functions and , respectively:

| (1) |

These bivariate distributions can be combined to a three-dimensional distribution by assigning a conditional copula ,

| (2) |

For every cdf , Sklar’s theorem implies the existence of a bivariate copula that couples and for every . The generalization of this principle to arbitrary dimensions is obvious and the conditional copulas corresponding to such a construction can be determined for every multivariate distribution (c.f. Patton (2006) for a discussion of conditional copulas).

To make PCCs tractable for inference and model selection however, further assumptions regarding the conditional copulas have to be made.

We will call a multivariate distribution an absolutely continuous and parametric PCC if all bivariate copula families occurring in the construction have densities with a parameter vector. In this case, it will be possible to express the likelihood function of the joint copula model in terms of the bivariate densities and to make inference about the finite-dimensional parameter based on this expression.

One example for this would be the decomposition of a -dimensional density with marginal densities , , as a C-vine copula (see \shortciteNaas2009): with univariate parameters and copula parameters , and ,

The above multivariate density is valid for a simplified PCC because all bivariate copulas occurring in the constructions do not depend on the variables that are conditioned on, e.g.,

This simplifying assumption reduces the specification of a PCC to choosing bivariate copula families and their parameters. This means that the potentially complex dependence between variables that are conditioned on and the copula functions can be neglected, and model selection can be performed more easily. Also other techniques for PCCs such as for R-vines (stepwise estimation in Hobæk Haff (2012) and \shortciteNdissmann2011, inference as in \shortciteNaas2009 or Bayesian techniques as in Min and Czado (2010)) extend to the non-simplified case only if the dependence on the variables that are conditioned on is of a simple form (we discuss this in Section 5, see in particular Example 5.1).

3 Archimedean copulas

In this section, we characterize the Archimedean copulas that are simplified PCCs. A -dimensional Archimedean copula is given by

| (3) |

for an Archimedean generator function . Here, is the class of functions , which are strictly decreasing on (with , ) and differentiable on up to order , such that , and where further is non-increasing and convex (McNeil and Nešlehová (2009), Joe (1997), Müller and Scarsini (2005)). These copulas have the appealing property that the conditional distribution function is given in a simple analytical form which facilitates the study of their properties. Given a Gamma random variable with shape parameter , rate parameter , density

mean and variance , the Laplace transform (LT) is

The Archimedean copula corresponding to this LT as generator function is called MTCJ111This copula is also called Clayton copula due to its appearance in Clayton (1978). It is the copula of the multivariate Pareto distribution Mardia (1962) and of the multivariate Burr distribution Takahasi (1965). It was first mentioned as a multivariate copula in Cook and Johnson (1981) and as a bivariate copula in Kimeldorf and Sampson (1975). The extension to negative dependence was given in Genest and MacKay (1986) for the bivariate case and in (Joe, 1997, pp. 157-158) for the multivariate case. Since many properties were discovered studying the corresponding distribution function and Cook and Johnson (1981) mentioned its general form we call it MTCJ copula. copula. From the form of the conditional distributions derived in Takahasi (1965) it is obvious that the copulas corresponding to bivariate conditional margins of the MTCJ copula are again MTCJ copulas. The above gamma LT family extends to Archimedean generators (for the generalized MTCJ family)

| (4) |

The conditional generator (c.f. Mesfioui and Quessy (2008)) when conditioning on variables becomes

| (5) |

For , , so the parameter range is consistent, and the (generalized) MTCJ copula is a simplified PCC where all bivariate building blocks are MTCJ with corresponding choice of parameters. In fact, under a weak regularity assumption, it is the only multivariate Archimedean copula that constitutes a simplified PCC.

Theorem 3.1

A -dimensional Archimedean copula with a generator that is twice continuously differentiable on the set where it is positive is a simplified PCC if and only if its generator is in the family (4).

Proof

Appendix A.

Note that the differentiability condition for the generator is satisfied for all Archimedean copulas if . This adds a further aspect making the MTCJ copula unique222The MTCJ copula also is the only Archimedean copula invariant under truncation, in the sense that for a rv , C also is the copula of , Ahmadi Javid (2009). among Archimedean copulas. Using different parameters than obtained through Equation (5), PCCs with MTCJ copulas with freely chosen parameters as building blocks naturally generalize the MTCJ copula to what we call an extended MTCJ copula.

4 Elliptical copulas

In this section, we characterize the elliptical copulas that have all conditional distributions in location-scale families. We show that not all elliptical copulas are simplified PCCs and characterize the scale mixtures of Normals which are of the simplified type. By referring to a -dimensional elliptical copula we mean a copula arising from an elliptical distribution such as the multivariate Normal or Student- distribution. A multivariate distribution is elliptical if its characteristic function has the form

for , , and positive definite . If the distribution has a density, this implies that it is given by

for a generator function , which can be uniquely determined from , see \shortciteNcambanis1981. For the two examples we mentioned, the generator functions have the form

and lead to simplified PCCs.

Theorem 4.1

The multivariate Gaussian distribution and the multivariate Student- distribution are PCCs of the simplified form.

For the Gaussian distribution this is quite obvious since all conditional distributions are again Gaussian and do depend on the values of the variables that they are conditioned on only through their mean, i.e., they all are in the same location family. For the Student- distribution the covariances also depend on these values, but only through a scaling factor such that all conditional distributions remain in the same location-scale family. Since changes of location and scale do not affect the copula of a multivariate distribution, this implies that the Student- distribution is a simplified PCC. For clarification, we derive the explicit form of the copulas corresponding to bivariate conditional distributions in Appendix B.1. Just as for the MTCJ copula, changing the degrees of freedom in the bivariate building blocks of the PCC leads to a natural extension of the multivariate Student-t distribution in which different bivariate conditional margins can have different degrees of freedom.

While the copulas corresponding to these distributions are the most popular examples they also have a unique position within the class of elliptical distributions as the following theorems show.

Theorem 4.2

Let us assume that the generator function of the density of a -dimensional elliptical distribution is differentiable. Then, the conditional distributions remain within the same location-scale family for all values of the variables that are conditioned on, if and only if

-

(a)

the support of is and the distribution is the multivariate Student-t (or Pearson type VII) distribution or in its limiting case the multivariate Normal distribution or

-

(b)

has compact support and , for up to rescaling (the Pearson type II distribution).

Proof

Appendix B.2.

Here, case can be seen as an analogue to the extension of the MTCJ to negative dependence.

The proof that the Student-t distribution is a simplified PCC relied on the fact that in this case, conditioning only affects the location and scale of the distribution. Theorem 4.2 now shows that the t-distribution is the only elliptical distribution where this proof strategy is successful. Just as the MTCJ can be constructed using a Gamma mixture, also the Student-t distribution arises from the multivariate Normal distribution using a Gamma mixture for the square of the inverse scale parameter. For the distribution function of the MTCJ copula, we have

where is a cdf on , c.f. (Joe, 1997, p. 86), while

holds for the density of a multivariate Student-t distribution. When only considering scale mixtures of Normals, we obtain the following theorem.

Theorem 4.3

Consider a -dimensional scale mixture of Normals which is a simplified PCC

-

a)

in or

-

b)

for all correlation matrices ,

then it is a simplified PCC if and only if the mixing distribution is the Gamma distribution.

Proof

Appendix B.3.

This contradicts the claim made in Example 4.1 of Hobæk Haff (2012) that all elliptical distributions are simplified PCCs.

Although this shows that the intersection between simplified PCCs and elliptical distributions is limited, it turns out that the deviation from the simplifying assumption can be ignored in many applications. In fact, the values of Kendall’s corresponding to bivariate conditional distributions are independent of the variables that are conditioned. \shortciteNcambanis1981 showed that the conditional correlation coefficient is equal to the partial correlation for elliptical distributions, and \shortciteNlindskog2003 demonstrated that the relationship between the correlation coefficient and Kendall’s for the Normal distribution

holds for all atom-free elliptical distributions.

5 Non continuous and non-simplified PCCs

In order to complete the list of examples for the classification in Figure 1, we need to find distributions which are not absolutely continuous but simplified PCCs and distributions which are neither absolutely continuous nor simplified PCCs. For the first case, let us consider a PCC with bivariate Cuadras-Augé (which are a special case of the bivariate Marshall-Olkin (MO) copula, where the distribution is exchangeable) copulas as building blocks. Exempli gratia,

c.f. (Mai and Scherer, 2012, Chapter 1). For the joint distribution of , , this implies that

where the conditional cdf is given by (Mai and Scherer, 2012, Example 1.8)

Note that here is a copula. A scatterplot of the bivariate margin of this distribution is shown in the left panel of Figure 2 for illustration.

While this copula is of simplified form by construction, the multivariate MO copula (c.f. (Mai and Scherer, 2012, Chapter 3)),

in contrast is neither a simplified nor an absolutely continuous PCC. We derive the copula of bivariate conditional distributions for the trivariate case in Appendix C, the cdf of the conditional copula of is plotted in the right hand panel of Figure 2 for different values of the conditioned . Note that, due to the non continuity of and this copula is uniquely defined only outside the shaded areas.

![[Uncaptioned image]](/html/1205.4844/assets/x2.png)

![[Uncaptioned image]](/html/1205.4844/assets/x3.png)

right panel: Cdf of the bivariate conditional copulas of a trivariate MO copula with parameter (see Appendix C). The cdf for is plotted solid (it is uniquely determined outside the light grey area), the dashed lines correspond to the cdf for (which is uniquely determined outside the dark grey area).

Weakening the simplifying assumption

Whereas the case of PCCs which are not absolutely continuous will rarely be relevant in practice, there is a wide range of applications for distributions involving non-simplified PCCs.

Although the simplifying assumption sounds restrictive on the first glance, fairly general distributions can be obtained while keeping the simplified assumption for parts of the distribution. Staying in the parametric and absolutely continuous framework, the parameters of otherwise simplified PCCs can be made depending on the values of variables that are conditioned on. In cases where there is an underlying economic assumption for how covariates should influence the dependence, this can be done in the form of parametric models. Examples for this were studied by for example Patton (2006) and \shortciteNbartram2007, who considered models where the dependence parameter of the conditional copula depends on previous realizations of the time series, or Stöber and Czado (2011) and Almeida and Czado (2011), who considered dependence of the parameter on an underlying Markov or AR(1) process, respectively. In particular, the Markov switching R-vine copula model of Stöber and Czado (2011) implies that the copula of a multivariate time series at each point in time is given by a discrete mixture of simplified PCC’s, which will usually be of non-simplified form as for the mixture of Normals.

When there is no a priori knowledge for how the dependence parameter should be influenced, non-parametric models as in \shortciteNacar2011 can be applied. While this is fairly straightforward when conditioning on just one variable, it raises the question how interactions should be included when conditioning on multiple variables. For the elliptical and Archimedean distributions which we studied in Sections 3 and 4, we observe the following:

-

•

For elliptical distributions, the Kendall’s of conditional distributions does not depend on the values which are conditioned on. The distribution however can depend on these variables. Assuming zero means and correlations, and conditioning on realizations, the conditional distribution will only depend on . If the generator function is monotonely decreasing (as for the multivariate Normal or Student-t distribution, and generally if , see (Joe, 1997, Section 4.9)), this implies in particular that the conditional distribution only depends on . For this reason, one might consider to make the dependence parameter of conditional copulas depend on the likelihood of observations that are conditioned on, for data where the distribution appears to be close to the elliptical family. However, since the values of Kendall’s must not be affected — which are closely related to parameter values for most well known bivariate parametric families — keeping the simplifying assumption will always be a close approximation in these cases.

-

•

For an Archimedean copula with generator function , we have observed that when conditioning on realizations the conditional distribution will only depend on . In particular, this implies that it only depends on , which is the cdf of , evaluated at . Thus, for data showing dependence behavior close to that of the Archimedean class, we recommend to consider analyzing dependence of the parameters of conditional copulas on this joint probability.

As a simple example for how the conditional copula can depend on the values of conditioning variables in the Archimedean case, let us consider the three-dimensional Frank copula.

Example 5.1 (Three-dimensional Frank copula)

Let have cdf with LT of the logarithmic series distribution:

i.e., the three-dimensional Frank copula. Then, the copula corresponding to the conditional distribution of is of the Ali-Mikhail-Haq family (LT of geometric distribution)

with parameter , thus depending on the conditioning value . How the strength of dependence between depends on the parameter and the conditioning value is illustrated in Figure 4.

Remark 5.2 (Extensions of Archimedean copulas)

As for the multivariate Student-t copula, this decomposition allows for a natural extension of the Frank copula by assuming different parameters for the different bivariate copulas in the models, and similar extension arise for other Archimedean copulas. The possible range of dependence induced by this extension is illustrated in Figure 3.

![[Uncaptioned image]](/html/1205.4844/assets/x4.png)

![[Uncaptioned image]](/html/1205.4844/assets/x5.png)

![[Uncaptioned image]](/html/1205.4844/assets/x6.png)

6 Conclusion and summary

While many popular statistical models are built by (sequential) conditioning, the implications on the properties of a distribution arising from this construction remained largely unknown. In addition, whether and under which assumptions popular classes of dependence models can be decomposed in this way was not investigated.

In this paper, we filled in this gap by characterizing the most common classes of copulas in terms of their decomposability as a PCC.

We showed that only the -dimensional Archimedean copula based on the gamma LT or its generalization into can be decomposed using a PCC in which the building blocks are independent of the values that are conditioned on. For elliptical copulas, the situation is more challenging. While the multivariate Normal and Student-t distribution are simplified PCCs, the conjecture that this is true for all elliptical distributions does not hold. The Student-t distribution even is the only non-bounded elliptical distribution in which conditioning affects only the location and scale of the resulting conditional distribution but not the correlation matrix. Just as for the MTCJ in the Archimedean family, this distribution arises from a Gamma mixture for the square of the inverse scale parameter of a multivariate normal distribution. We have shown, that this makes it the only scale mixture of Normals which is a simplified PCC in dimension .

Whereas the simplifying assumption for PCCs is convenient, it is often too restrictive, and also the assumption of dealing with absolutely continuous PCC is sometimes too strong. We illustrated this with several examples and demonstrated that in most applications, however, simplified PCC can be extended to adapt to the situation.

While our classification results provide important insights into the properties of distributions arising from conditioning, we believe that further research in this direction remains necessary, in particular considering how well general distributions can be approximated by simplified PCCs.

Figure 1 does not include the extreme value copulas which is another general class. Extreme value copulas are used for data that are multivariate maxima or minima, and in this context, PCCs would not be considered. It can be shown that extreme value copulas which do not have independent subcomponents are not simplified PCCs; for example, given a trivariate extreme value copula which satisfies for all powers with , it can be shown that the copula obtained by conditioning on has lower tail form as , where does not depend on but the multiplying factor is slowly varying in and depends on .

Appendix A Proofs involving Archimedean copulas - Theorem 3.1

Because the proof is more intuitive, we first outline the case where is the LT of a positive random variable. In this case, there is a representation of the copula as a mixture of powers. The mixture distribution from which the Archimedean copula arises can be written as (c.f. (Joe, 1997, p. 86)):

where is the cdf of a positive rv, with corresponding density , and

is the common univariate cdf with being the LT of A. Without loss of generality we can assume that on , then , , is a copula. Also on is differentiable. With , the marginal cdf of the last variables and its density are:

and the conditional cdf of the first variables given the last is:

where

In this case, has the same parameter form of density as if

| (6) |

where is a positive-valued function (it is not absorbed in the term only if it is a non-power function) and is a (finite) normalizing constant. From above, has the same density form with parameters . The conditional copula does not depend on only if is a rate (or reciprocal scale) parameter, since Archimedean copulas are invariant to scale changes of the mixing distribution (Mai and Scherer, 2012, p. 60). For to be a rate or inverse scale parameter of (6) only, must be a power of . Hence is a gamma density, and is a MTCJ copula.

For the general case, where is not necessarily a LT, we prove the result by construction a functional equation. Let

be an Archimedean copula. Let be a random vector with this distribution. Suppose has support where is infinite for a Laplace transform, but could be finite for which is not a Laplace transform. The case of finite support implies that for . Let be the conditional distribution given . We will show now that the copula for this is another Archimedean copula, say based on , where . By differentiation, with and with ,

with th () margin . Note that is monotone increasing by definition of . Hence for and the copula of the conditional distribution of given is:

Defining and , this is a Archimedean copula

with generator function . As , , and can be positive or infinite but not 0, by the definition of .

Consider first the case where is finite and positive, and is finite. The copula of the conditional distribution does not depend on or if and only if there is a continuous differentiable scale function such that and

Writing the above functional equation in as and differentiating with respect to yields

With if follows that

or

This has solution where . Since must be decreasing, there are 2 possibilities

-

(i)

, , , or

-

(ii)

, , .

By integrating over we obtain , since . In case (i), we must have and in case (ii), in order for (see also (Joe, 1997, pp. pages 157–158)). In case (i) the obtained generating function support on and corresponds to the "standard" MTCJ copula, whereas case (ii), with bounded yields the extended MTCJ copula.

If or is infinite, the above is modified as follows. Let . There is a continuous differentiable scale function such that and

Cross-multiplying and differentiating the above with respect to , and then setting to yields

This has solution where so that . The conclusion is the same as above, because after integrating to get , one would conclude that this leads to and being finite.

As an illustration for how the copulas of conditional distributions are derived when the conditioning is on more than one variable, let us consider the case where and

is an Archimedean copula. Let be a random vector with this distribution and let for and . Then, the conditional distribution of given is

The copula corresponding to this distribution is again Archimedean, based on a generator . By differentiation, with , , has th margin . Note that is monotone decreasing because is the generator of a -dimensional Archimedean copula. Hence, for and the copula of the conditional distribution can be expressed as

This is an Archimedean copula with and . The same pattern extends to conditional distributions of Archimedean copulas with three or more conditioning variables.

Appendix B Proofs involving elliptical copulas

B.1 Theorem 4.1

In the remainder, we will use the following notation. A -dimensional Student-t distribution with mean vector 0, correlation matrix and degrees of freedom is denoted as . Its pdf is and we write for the cdf.

Let us consider a -dimensional random vector , with , distributed according to a multivariate Student-t distribution with degrees of freedom, mean and scale matrix

Let us define

then we have for the conditional distribution of given :

c.f. \shortciteN[Lemma 2.2]nikoloulopoulos2009. Taking () yields

so that we can now determine the corresponding copula:

where the additive constants and scaling factors cancel. This is a bivariate Student-t copula with degrees of freedom and correlation matrix and does not depend on anymore.

B.2 Theorem 4.3

The proof is similar to that for Archimedean copulas in that the same functional equation can be obtained. Without loss of generality, let us consider the case of a -dimensional elliptical distribution with zero means and zero correlations. In this case, the density of the distribution is given by

For we obtain

For this distribution to be in the same location-scale family irrespective of the values of , we must have that for given there exists such that

With , , and this implies that

| (7) |

where equals times a constant depending on and , are differentiable scale functions. Since if and only if for all values of , we must have . Using in Equation 7, we conclude that is finite. Thus, we can define and obtain from Equation 7 that

Using that by the definition of ,

In other words, the function must fulfill the differential equation

where , . From this, we obtain for that which corresponds to the elliptical generator of a Pearson type VII (scaled Student-t) distribution. For to yield a well defined density in dimensions, must be given in the form , , to ensure integrability with respect to .

For , , which leads to a well-defined density for and is differentiable and thus a valid solution for .

By integration, we obtain that the generator function for lower-dimensional margins is proportional to . Ergo, also the conditional distributions of the lower-dimensional margins remain within the same location-scale family for all values of the conditioning variables.

B.3 Theorem 4.4

A general scale mixture of Normals in dimension can be written as where is a random variable on with density , and is multivariate Gaussian with zero mean vector and covariance matrix . Without loss of generality, we can assume that all diagonal entries of are , i.e., is a correlation matrix. This implies for the -variate generator that

Similarly, if is the leading matrix of , and , then by marginalizing out the last components we get

Hence, the univariate margin is

In the above, the density could be replaced with in a Stieltjes integral. However, this would not affect the remainder of this proof; we omit it for notational convenience. Note that

Let be the cdf corresponding to the marginal generator . Then, the copula density for is

| (8) |

with . From this general form of the density, we will obtain two equations for the moments of the mixing variable which will lead to necessary conditions on the conditional distributions of simplified PCCs in the elliptical class. Directly from (8) we get that

| (9) |

This means that if are two different mixing variables, then the copula densities with fixed are different unless the necessary condition of

holds. For the second equation, let us consider

| (10) |

where is the element of and . Note that is not a scaling factor of the marginal distribution but a function of the correlation matrix. In particular, we can obtain all from correlation matrices

where is the identity matrix. Using , we determine the first derivative of (10) as

After taking the second derivative with respect to and then setting , all terms are 0 except

| (11) |

Let us now consider the analogon for conditional densities. Let be the density of and let be the density of or any . Let

For this, we decompose as where and is the conditional covariance matrix of given . Writing the conditional densities in mixture form,

and

so that

| (12) |

is a scale mixture with mixing density , where is a normalizing constant. We denote the random variable with this density by .

For , Equations (9) and (12) imply that a necessary condition for the copula corresponding to the distribution of given to be independent of is that

| (13) |

is a constant over . Similarly, we obtain from (11) that

| (14) |

must be equal to a constant . To rewrite these equations, let and let be a random variable with density proportional to . let be random variable with density proportional to ; this is an Laplace transform tilt of the density of with normalizing constant , the LT of at . Note that has finite positive integer moments for and .

Then, (13) can be rewritten as

| (15) |

which must be constant over while (14) leads to

| (16) |

which, for all , must be equal to a constant . This implies the following recursive relation for the moments of : if we know that (15) is constant for and , then it is also constant for . Thus, it is sufficient to show that (15) is constant for and , or and .

Let us now consider case a), where the copula is a simplified PCC in . From the three-dimensional marginal distributions, we obtain that (15) is constant for . By conditioning on , we conclude with a similar calculation as for (12) that

This, together with (15) being constant for implies that (15) is constant for and thus for all .

In case b), where the copula is a simplified PCC for all , we know that for a three-dimensional marginal distribution, (16) holds for all :

Thus, and must be constants over . Together with (15) being constant in for , this means that (15) is constant for and thus for all . Note that, more precisely, we only require two different values of in (16) for the argument above.

Summing up, we obtain that with the moments of are connected to the moments of via

for all , , where .

With all of the positive integer moments of and existing, the Laplace transforms of and , for , where the constant may depend on , can be written as

Hence in a neighborhood of 0 for the Taylor series expansion of the LTs about 0. By (Feller, 1971, Section VII.6), the Taylor series in a positive neighborhood of 0 uniquely determines the distribution. Hence for . The combination that Laplace transform tilting of the density leads to a scale-changed random variable, implies that has a gamma density (Marshall and Olkin, 2007, p. 576, Theorem 18.B.6). Hence, also is Gamma distributed, and the corresponding scale mixture is the multivariate t-distribution.

Appendix C Trivariate Marshall-Olkin (MO) copula

To determine the bivariate conditional distributions of a three-dimensional MO copula, we work with the parameterization of (Mai and Scherer, 2012, Chapter 3). The three-dimensional MO copula is the survival copula of the rvs defined as

where are independent and exponentially distributed. For simplicity let us assume that all rate parameters are equal, i.e., , . This implies that for all , and thus we can determine the conditional survival distribution of as

If and , we know that . Using this,

since implies and implies , which further yields .

Let be the random variable with cdf , then we obtain

Putting together the conditional probabilities, the conditional survival function is

For the generalized inverse of the conditional survival function of e.g. , this implies that

Given this, we can evaluate the copula of the bivariate conditional distribution of to see that it depends on the value of in the areas where it is uniquely determined. To arrive at the conditional copula of the trivariate MO copula, and not of the corresponding distribution, we further have to transform . For the marginal survival function we obtain that , with inverse .

Acknowledgements

Jakob Stöber gratefully acknowledges financial support by TUM’s Topmath program and a research stipend from Allianz Deutschland AG, while Harry Joe is supported by an NSERC Discovery grant.

References

- Aas et al. (2009) Aas, K., C. Czado, A. Frigessi, and H. Bakken (2009). Pair-copula construction of multiple dependence. Insurance: Mathematics and Economics 44, 182–198.

- Acar et al. (2011) Acar, E. F., R. V. Craiu, and F. Yao (2011). Dependence calibration in conditional copulas: A nonparametric approach. Biometrics 67(2), 445–453.

- Ahmadi Javid (2009) Ahmadi Javid, A. (2009). Copulas with truncation-invariance property. Comm. Statist. A. - Theor. 38, 3756–3771.

- Almeida and Czado (2011) Almeida, C. and C. Czado (2011). Efficient Bayesian inference for stochastic time-varying copula models. Computational Statistics and Data Analysis. To appear.

- Ang and Chen (2002) Ang, A. and J. Chen (2002). Asymmetric correlations of equity portfolios. Journal of Financial Economics 63, 443–494.

- Bartram et al. (2007) Bartram, S., S. Taylor, and Y. Wang (2007). The euro and European financial market dependence. Journal of Banking and Finance 31, 1461–1481.

- Bauer et al. (2011) Bauer, A., C. Czado, and T. Klein (2011). Pair-copula constructions for non Gaussian DAG models. To appear in the Canadian Journal of Statistics..

- Bedford and Cooke (2001) Bedford, T. and R. Cooke (2001). Probability density decomposition for conditionally dependent random variables modeled by vines. Ann. Math. Artif. Intell. 32, 245–268.

- Bedford and Cooke (2002) Bedford, T. and R. Cooke (2002). Vines — a new graphical model for dependent random variables. Annals of Statistics 30, 1031–1068.

- Cambanis et al. (1981) Cambanis, S., S. Huang, and G. Simons (1981). On the theory of elliptically contoured distributions. Journal of Multivariate Analysis 11, 386–385.

- Clayton (1978) Clayton, D. G. (1978). A model for association in bivariate life tables and its application in epidemiological studies of familial tendency in chronic disease incidence. Biometrica 65(1), 141–151.

- Cook and Johnson (1981) Cook, R. D. and M. E. Johnson (1981). A family of distributions for modeling non-elliptically symmetric multivariate data. J. Roy. Statist. Soc. B 43, 210–218.

- Dißmann et al. (2011) Dißmann, J., E. C. Brechmann, C. Czado, and D. Kurowicka (2011). Selecting and estimating regular vine copulae and application to financial returns. submitted.

- Feller (1971) Feller, W. (1971). An introduction to Probability Theory and Its Applications (second ed.), Volume 2. New York: Wiley.

- Genest and MacKay (1986) Genest, C. and R. MacKay (1986). Copules archimédiennes et familles de lois bidimensionelles dont les marges sont données. Canadian Journal of Statistics 14, 145–159.

- Hobæk Haff et al. (2010) Hobæk Haff, I., K. Aas, and A. Frigessi (2010). On the simplified pair-copula construction — simply useful or too simplistic? Journal of Multivariate Analysis 101, 1296–1310.

- Hobæk Haff (2012) Hobæk Haff, I. H. (2012). Parameter estimation for pair-copula constructions. To appear in Bernoulli..

- Joe (1996) Joe, H. (1996). Families of -variate distributions with given margins and bivariate dependence parameters. In L. Rüschendorf and B. Schweizer and M. D. Taylor (Ed.), Distributions with Fixed Marginals and Related Topics, Volume 28, Hayward, CA, pp. 120–141. Inst. Math. Statist.

- Joe (1997) Joe, H. (1997). Multivariate Models and Dependence Concepts. Chapman & Hall, London.

- Kimeldorf and Sampson (1975) Kimeldorf, G. and A. R. Sampson (1975). Uniform representations of bivariate distributions. Comm. Statist. 4, 617–627.

- Lindskog et al. (2003) Lindskog, F., A. McNeil, and U. Schmock (2003). Kendall’s tau for elliptical distributions. Credit Risk: Measurement, Evaluation and Management; Physica-Verlag, Heidelberg, 149–156.

- Longin and Solnik (2001) Longin, F. and B. Solnik (2001). Extreme correlations in international equity markets. Journal of Finance 56, 649–676.

- Mai and Scherer (2012) Mai, J.-F. and M. Scherer (2012). Simulating Copulas: Stochastic Models, Sampling Algorithms, and Applications. to appear at World Scientific.

- Mardia (1962) Mardia, K. V. (1962). Multivariate Pareto distributions. Ann. Math. Statist. 33, 1008–1015.

- Marshall and Olkin (2007) Marshall, A. W. and I. Olkin (2007). Life Distributions: Structure of Nonparametric, Semiparametric and Parametric Families. New York: Springer.

- McNeil and Nešlehová (2009) McNeil, A. and J. Nešlehová (2009). Multivariate Archimedean copulas, -monotone functions and -norm symmetric distributions. The Annals of Statistics 37.

- Mesfioui and Quessy (2008) Mesfioui, M. and J.-F. Quessy (2008). Dependence structure of conditional archimedean copulas. Journal of Multivariate Analysis 99, 372–385.

- Min and Czado (2010) Min, A. and C. Czado (2010, Fall). Bayesian inference for multivariate copulas using pair-copula constructions. Journal of Financial Econometrics 8(4), 511–546.

- Müller and Scarsini (2005) Müller, A. and M. Scarsini (2005). Archimedean copulae and positive dependence. Journal of Multivariate Analysis 93, 434–445.

- Nelsen (2006) Nelsen, R. B. (2006). An Introduction to Copulas. Springer, New York.

- Nikoloulopoulos et al. (2009) Nikoloulopoulos, A., H. Joe, and H. Li (2009). Extreme value properties of multivariate t copulas. Extremes 12, 129–148. 10.1007/s10687-008-0072-4.

- Patton (2006) Patton, A. (2006). Modelling asymmetric exchange rate dependence. International Economic Review 47(2), 527–556.

- Sklar (1959) Sklar, M. (1959). Fonctions de répartition à dimensions et leurs marges. Publ. Inst. Statist. Univ. Paris 8, 229–231.

- Stöber and Czado (2011) Stöber, J. and C. Czado (2011). Detecting regime switches in the dependence structure of high dimensional financial data. preprint.

- Takahasi (1965) Takahasi, K. (1965). Note on the multivariate Burr’s distribution. Ann. Inst. Statist. Math. 17, 257–260.