Covariate assisted screening and estimation

Abstract

Consider a linear model , where and . The vector is unknown but is sparse in the sense that most of its coordinates are . The main interest is to separate its nonzero coordinates from the zero ones (i.e., variable selection). Motivated by examples in long-memory time series (Fan and Yao [Nonlinear Time Series: Nonparametric and Parametric Methods (2003) Springer]) and the change-point problem (Bhattacharya [In Change-Point Problems (South Hadley, MA, 1992) (1994) 28–56 IMS]), we are primarily interested in the case where the Gram matrix is nonsparse but sparsifiable by a finite order linear filter. We focus on the regime where signals are both rare and weak so that successful variable selection is very challenging but is still possible.

We approach this problem by a new procedure called the covariate assisted screening and estimation (CASE). CASE first uses a linear filtering to reduce the original setting to a new regression model where the corresponding Gram (covariance) matrix is sparse. The new covariance matrix induces a sparse graph, which guides us to conduct multivariate screening without visiting all the submodels. By interacting with the signal sparsity, the graph enables us to decompose the original problem into many separated small-size subproblems (if only we know where they are!). Linear filtering also induces a so-called problem of information leakage, which can be overcome by the newly introduced patching technique. Together, these give rise to CASE, which is a two-stage screen and clean [Fan and Song Ann. Statist. 38 (2010) 3567–3604; Wasserman and Roeder Ann. Statist. 37 (2009) 2178–2201] procedure, where we first identify candidates of these submodels by patching and screening, and then re-examine each candidate to remove false positives.

For any procedure for variable selection, we measure the performance by the minimax Hamming distance between the sign vectors of and . We show that in a broad class of situations where the Gram matrix is nonsparse but sparsifiable, CASE achieves the optimal rate of convergence. The results are successfully applied to long-memory time series and the change-point model.

doi:

10.1214/14-AOS1243keywords:

[class=AMS]keywords:

FLA

, and T1Supported in part by NSF Grant DMS-07-04337, the National Institute of General Medical Sciences of the National Institutes of Health Grants R01GM100474 and R01-GM072611. T2Supported in part by NSF CAREER award DMS-09-08613. T3The major work of this article was completed when Z. Ke was a graduate student at Department of Operations Research and Financial Engineering, Princeton University.

1 Introduction

Consider a linear regression model

| (1) |

The vector is unknown but is sparse, in the sense that only a small fraction of its coordinates is nonzero. The goal is to separate the nonzero coordinates of from the zero ones (i.e., variable selection). We assume , which is the standard deviation of the noise, is known and set without loss of generality.

In this paper, we assume the Gram matrix

| (2) |

is normalized so that all of the diagonals are , instead of as is often used in the literature. The difference between two normalizations is nonessential, but the signal vector are different by a factor of .

We are primarily interested in the cases where:

-

•

the signals (nonzero coordinates of ) are rare (or sparse) and weak;

-

•

the Gram matrix is nonsparse or even ill-posed (but it may be sparsified by some simple operations; see details below).

In such cases, the problem of variable selection is new and challenging.

While signal rarity is a well-accepted concept, signal weakness is an important but a largely neglected notion, and many contemporary researches on variable section have been focused on the regime where the signals are rare but strong. However, in many scientific experiments, due to the limitation in technology and constraints in resources, the signals are unavoidably weak. As a result, the signals are hard to find, and it is easy to be fooled. Partially, this explains why many published works (at least in some scientific areas) are not reproducible; see, for example, Ioannidis (2005).

We call sparse if each of its rows has relatively few “large” elements, and we call sparsifiable if can be reduced to a sparse matrix by some simple operations (e.g., linear filtering or low-rank matrix removal). The Gram matrix plays a critical role in sparse inference, as the sufficient statistics . Examples where is nonsparse but sparsifiable can be found in the following application areas:

-

•

Change-point problem. Recently, driven by researches on DNA copy number variation, this problem has received a resurgence of interest [Niu and Zhang (2012), Olshen et al. (2004), Tibshirani and Wang (2008)]. While existing literature focuses on detecting change-points, locating change-points is also of major interest in many applications [Andreou and Ghysels (2002), Siegmund (2011), Zhang et al. (2010)]. Consider a change-point model

(3) where is a piece-wise constant vector with jumps at relatively few locations. Let be the matrix such that , . We re-parametrize the parameters by

so that is nonzero if and only if has a jump at location . The Gram matrix has elements , which is evidently nonsparse. However, adjacent rows of display a high level of similarity, and the matrix can be sparsified by a second order adjacent differencing between the rows.

-

•

Long-memory time series. We consider using time-dependent data to build a prediction model for variables of interest, , where is an observed stationary time series and are white noise. In many applications, is a long-memory process. Examples include volatility process [Fan and Yao (2003), Ray and Tsay (2000)], exchange rates, electricity demands, and river’s outflow (e.g., the Nile’s). Note that the problem can be reformulated as (1), where the Gram matrix is asymptotically close to the auto-covariance matrix of (say, ). It is well known that is Toeplitz, the off-diagonal decay of which is very slow and the matrix -norm which diverges as . However, the Gram matrix can be sparsified by a first order adjacent differencing between the rows.

Further examples include jump detections in (logarithm) asset prices and time series following a FARIMA model [Fan and Yao (2003)]. Still other examples include the factor models, where can be decomposed as the sum of a sparse matrix and a low rank (positive semi-definite) matrix. In these examples, is nonsparse, but it can be sparsified either by adjacent row differencing or low-rank matrix removal.

1.1 Nonoptimality of -penalization method for rare and weak signals

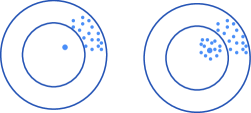

When the signals are rare and strong, the problem of variable selection is more or less well understood. In particular, Donoho and Stark (1989) [see also Donoho and Huo (2001)] have investigated the noiseless case where they reveal a fundamental phenomenon. In detail, when there is no noise, model (1) reduces to . Now, suppose are given, and consider the equation . In the general case where , it was shown in Donoho and Stark (1989) that under mild conditions on , while the equation has infinitely many solutions, there is a unique solution that is very sparse. In fact, if is full rank and this sparsest solution has nonzero elements, then all other solutions have at least nonzero elements; see Figure 1 (left).

In the spirit of Occam’s razor, we have reason to believe that this unique sparse solution is the ground truth we are looking for. This motivates the well-known method of -penalization, which looks for the sparsest solution where the sparsity is measured by the -norm. In other words, in the noiseless case, the -penalization method is a “fundamentally correct” (but computationally intractable) method.

In the past two decades, the above observation has motivated a long list of computable global penalization methods, including but not limited to the lasso, SCAD, MC, each of which hopes to produce solutions that approximate that of the -penalization method.

These methods usually use a theoretic framework that contains four intertwined components: “signals are rare but strong,” “the true is the sparsest solution of ,” “probability of exact recovery is an appropriate loss function” and “-penalization method is a fundamentally correct method.”

Unfortunately, the above framework is no longer appropriate when the signals are rare and weak. First, the fundamental phenomenon found in Donoho and Stark (1989) is no longer true. Consider the equation , and let be the ground truth. We can produce many vectors by perturbing such that two models and are indistinguishable (i.e., all tests—computable or not—are asymptotically powerless). In other words, the equation may have many very sparse solutions, where the ground truth is not necessarily the sparsest one; see Figure 1 (right).

In summary, when signals are rare and weak:

-

•

The situation is more complicated than that considered by Donoho and Stark (1989), and the principle of Occam’s razor is less relevant.

-

•

“Exact recovery” is usually impossible, and the Hamming distance between the sign vectors of and is a more appropriate loss function.

-

•

The -penalization method is not “fundamentally correct” if the signals are rare/weak and the Hamming distance is the loss function.

For example, it was shown in Ji and Jin (2012) that in the rare/weak regime, even when is very simple and when the tuning parameter is ideally set, the -penalization method is not rate optimal in terms of the Hamming distance. See Ji and Jin (2012) for details.

1.2 Limitation of UPS

That the -penalization method is rate nonoptimal implies that many other penalization methods (such as the lasso, SCAD, MC) are also rate nonoptimal in the rare/weak regime.

What could be rate optimal procedures in the rare/weak regime? To address this, Ji and Jin (2012) proposed a method called univariate penalization screening (UPS), and showed that UPS achieves the optimal rate of convergence in Hamming distance under certain conditions.

UPS is a two-stage screen and clean method [Wasserman and Roeder (2009)], at the heart of which is marginal screening. The main challenge that marginal screening faces is the so-called phenomenon of signal cancellation, a term coined by Wasserman and Roeder (2009). The success of UPS hinges on relatively strong conditions [e.g., see Genovese et al. (2012)], under which signal cancellation has negligible effects.

1.3 Advantages and disadvantages of sparsifying

Motivated by the application examples aforementioned, we are interested in the rare/weak cases where is nonsparse but can be sparsified by a finite-order linear filtering. That is, if we denote the linear filtering by a matrix , then the matrix is sparse in the sense that each row has relatively few large entries, and all other entries are relatively small.

In such challenging cases, we should not expect the -penalization method or the UPS to be rate optimal; this motivates us to develop a new approach.

Our strategy is to use sparsifying and so to exploit the sparsity of . Multiplying both sides of (1) by and then by gives

| (4) |

On one hand, sparsifying is helpful for both matrices and are sparse, which can be largely exploited to develop better methods for variable selection. On the other hand, “there is no free lunch,” and sparsifying also causes serious issues:

-

•

The post-filtering model (4) is not a regular linear regression model.

-

•

If we apply a local method (e.g., UPS, forward/backward regression) to model (4), we face so-called challenge of information leakage.

In Section 2.4, we carefully explain the issue of information leakage, and discuss how to deal with it.

We remark that while sparsifying can be very helpful, it does not mean that it is trivial to derive optimal procedures from model (4). For example, if we apply the -penalization method naively to model (4), we then ignore the correlations among the noise, which cannot be optimal. If we apply the -penalization method with the correlation structures incorporated, we are essentially applying it to the original regression model (1).

1.4 Covariate assisted screening and estimation (CASE)

To exploit the sparsity in and , and to deal with the two aforementioned issues that sparsifying causes, we propose a new variable selection method which we call covariate assisted screening and estimation (CASE). The main methodological innovation of CASE is to use linear filtering to create graph sparsity and then to exploit the rich information hidden in the “local” graphical structures among the design variables, which the lasso and many other procedures do not utilize.

At the heart of CASE is covariate assisted multivariate screening. Screening is a well-known method of dimension reduction in big data. However, most literature to date has been focused on univariate screening or marginal screening [Fan and Song (2010), Genovese et al. (2012)]. Extending marginal screening to (brute-force) -variate screening, , means that we screen all size- sub-models, and has two major concerns:

-

•

Computational infeasibility. A brute-force -variate screening has a computation complexity of , which is usually not affordable.

-

•

Screening inefficiency. The goal of screening is to remove as many noise entries as we can while retaining most of the signals. When we screen too many submodels than necessary, we have to set the bar higher than necessary to exclude most of the noise entries. As a result, we need signals stronger than necessary in order for them to survive the screening.

To overcome these challenges, CASE uses a new screening strategy called covariance-assisted screening, which excludes most size- submodels from screening but still manages to retain almost all signals. In detail, we first use the Gram matrix to construct a sparse graph called graph of strong dependence (GOSD). We then include a size- submodel in our screening list if and only if the nodes form a connected subgraph of GOSD. This way, we exclude many submodels from the screening by only using information in , not that in the response vector !

The blessing is, when GOSD is sufficiently sparse, it has no more than connected size- sub-graphs, where is a generic multi- term. Therefore, covariance-assisted screening only visits submodels, in contrast to submodels the brute-forth screening visits. As a result, covariance-assisted screening is not only computationally feasible, but is also efficient. Now, it would not be a surprise that CASE is a “fundamentally correct” procedure in the rare/weak regime, at least when the GOSD is sufficiently sparse, as in settings considered in this paper; see more discussion below.

1.5 Objective of the theoretic study

We now discuss the theoretic component of the paper. The objective of our theoretic study is three-fold:

-

•

to develop a theoretic framework that is appropriate for the regime where signals are rare/weak, and is nonsparse but is sparsifiable;

-

•

to appreciate the “pros” and “cons” of sparsifying, and to investigate how to fix the “cons”;

-

•

to show that CASE is asymptotic minimax and yields an optimal partition of the so-called phase diagram.

The phase diagram is a relatively new criterion for assessing the optimality of procedures. Call the two-dimensional space calibrated by the signal rarity and signal strength the phase space. The phase diagram is the partition of the phase space into different regions where in each of them inference is distinctly different. The notion of phase diagram is especially appropriate when signals are rare and weak.

The theoretic study is challenging for many reasons:

-

•

We focus on a very challenging regime, where signals are rare and weak, and the design matrix is nonsparse or even ill-posed. Such a regime is important from a practical perspective, but has not been carefully explored in the literature.

-

•

The goal of the paper is to develop procedures in the rare/weak regime that are asymptotic minimax in terms of Hamming distance, to achieve which we need to find a lower bound and an upper bound that are both tight. Compared to most works on variable selection where the goal is to find procedures that yield exact recovery for sufficiently strong signals, our goal is comparably more ambitious, and the study it entails is more delicate.

- •

1.6 Content and notation

The paper is organized as follows. Section 2 contains the main results of this paper: we formally introduce CASE and establishe its asymptotic optimality. Section 3 contains simulation studies, and Section 4 contains conclusions and discussions.

Throughout this paper, , , , and denotes the GOSD (in contrast, denotes the degree of GOLF, and denotes the Hamming distance). Also, and denote the sets of real numbers and complex numbers, respectively, and denotes the -dimensional real Euclidean space. Given , for any vector , denotes the -norm of ; for any matrix , denotes the matrix -norm of . When , coincides with the matrix spectral norm; we shall omit the subscript in this case. When is symmetric, and denote the maximum and minimum eigenvalues of , respectively. For two matrices and , means that is positive semi-definite.

2 Main results

This section is arranged as follows. Sections 2.1–2.6 focus on the model, ideas and the method. In Section 2.1, we introduce the rare and weak signal model. In Section 2.2, we formally introduce the notion of sparsifiability. The starting point of CASE is the use of a linear filter. In Section 2.3, we explain how linear filtering helps in variable selection by inducing a sparse graph and an interesting interaction between the graphical sparsity and the signal sparsity. In Section 2.4, we explain that linear filtering also causes a so-called problem of information leakage, and discuss how to overcome such a problem by the technique of patching. After all these ideas are discussed, we formally introduce the CASE in Section 2.5. In Section 2.6, we discuss the computational complexity and show that CASE is computationally feasible in a broad context.

Sections 2.7–2.9 focus on the asymptotic optimality of CASE. In Section 2.7, we introduce the asymptotic minimax framework where we use Hamming distance as the loss function. In Section 2.8, we study the lower bound for the minimax Hamming risk, and in Section 2.9, we show that CASE achieves the minimax Hamming risk in a broad context.

In Sections 2.10–2.11, we apply our results to long-memory time series and the change-point model. For both of them, we first derive explicit formulas for the convergent rates, and then use the formulas to derive the phase diagrams.

Proofs of results in this section can be found in the supplemental article [Ke, Jin and Fan (2014)], which contains Sections A–C.

2.1 Rare and weak signal model

Our primary interest is in the situations where the signals are rare and weak, and where we have no information on the underlying structure of the signals. In such situations, it makes sense to use the following rare and weak signal model; see Candès and Plan (2009), Donoho and Jin (2008), Jin, Zhang and Zhang (2014). Fix and . Let be the vector satisfying

| (5) |

and let be the set of vectors

| (6) |

We model by

| (7) |

where and is the Hadamard product (also called the coordinate-wise product). In Section 2.7, we further restrict to a subset of .

In this model, is either or a signal with a strength . Since we have no information on where the signals are, we assume that they appear at locations that are randomly generated. We are primarily interested in the challenging case where is small and is relatively small, so the signals are both rare and weak.

We remark that the theory developed in this paper is not tied to the rare and weak signal model, and applies to more general cases. For example, the main results can be extended to the case where we have some additional information about the underlying structure of the signals (e.g., Ising’s model [Ising (1925)]).

2.2 Sparsifiability, linear filtering and GOSD

As mentioned before, we are primarily interested in the case where the Gram matrix can be sparsified by a finite-order linear filtering.

Fix an integer and an -dimensional vector . Let be the matrix satisfying

| (8) | |||

| (9) |

The matrix can be viewed as a linear operator that maps any vector to . For this reason, is also called an order linear filter [Fan and Yao (2003)].

For and , we introduce the following class of matrices:

| (10) | |||

Matrices in are not necessarily symmetric.

Definition 2.2.

Fix an order linear filter . We say that is sparsifiable by if for sufficiently large , for some constants and .

In the long-memory time series model, can be sparsified by an order linear filter. In the change-point model, can be sparsified by an order linear filter.

The main benefit of linear filtering is that it induces sparsity in the graph of strong dependence (GOSD) to be introduced below. Recall that the sufficient statistics . Applying a linear filter to gives

| (11) |

where , and . Note that no information is lost when we reduce from the model to model (11), as is a nonsingular matrix.

At the same time, if is sparsifiable by , then both the matrices and are sparse, in the sense that each row of either matrix has relatively few large coordinates. In other words, for a properly small threshold to be determined, let and be the regularized matrices of and , respectively,

It is seen that

| (12) |

where each row of or has relatively few nonzeros. Compared to (11), (12) is much easier to track analytically, but it contains almost all the information about .

The above observation naturally motivates the following graph, which we call the graph of strong dependence (GOSD).

Definition 2.3.

For a given parameter , the GOSD is the graph with nodes , and there is an edge between and when any of the three numbers , and is nonzero.

Definition 2.4.

A graph is called -sparse if the degree of each node .

The definition of GOSD depends on a tuning parameter , the choice of which is not critical, and it is generally sufficient if we choose ; see Section B.1 in Ke, Jin and Fan (2014)for details. With such a choice of , it can be shown that in a general context, GOSD is -sparse, where does not exceed a multi- term as ; see Lemma B.1 in Ke, Jin and Fan (2014).

2.3 Interplay between the graph sparsity and signal sparsity

With these being said, it remains unclear how the sparsity of helps in variable selection. In fact, even when is -sparse, it is possible that a node is connected—through possible long paths—to many other nodes; it is unclear how to remove the effect of these nodes when we try to estimate .

Somewhat surprisingly, the answer lies in an interesting interplay between the signal sparsity and graph sparsity. To see this point, let be the support of , and let be the subgraph of formed by the nodes in only. Given the sparsity of , if the signal vector is also sparse, then it is likely that the sizes of all components of (a component of a graph is a maximal connected subgraph) are uniformly small. This is justified in the following lemma which is proved in Jin, Zhang and Zhang (2014).

Lemma 2.1

Suppose is -sparse, and the support is a realization from , where is the point mass at and is any distribution with support . With a probability (from randomness of ) at least , decomposes into many components with size no larger than .

In this paper, we are primarily interested in cases where for large , for some parameter and is bounded by a multi- term. In such cases, the decomposability of holds for a finite , with overwhelming probability.

Lemma 2.1 delineates an interesting picture: The set of signals decomposes into many small-size isolated “signal islands” (if only we know where), each of them is a component of and different ones are disconnected in the GOSD. As a result, the original -dimensional problem can be viewed as the aggregation of many separated small-size subproblems that can be solved parallelly. This is the key insight of this paper.

Note that the decomposability of attributes to the interplay between the signal sparsity and the graph sparsity, where the latter attributes to the use of linear filtering. The decomposability is not tied to the specific model of in Lemma 2.1, and holds for much broader situations (e.g., when is generated by a sparse Ising model [Ising (1925)]).

2.4 Information leakage and patching

While it largely facilitates the decomposability of the model, we must note that the linear filtering also induces a so-called problem of information leakage. In this section, we discuss how linear filtering causes such a problem and how to overcome it by the so-called technique of patching.

The following notation is frequently used in this paper.

Definition 2.5.

For , and a matrix , denotes the sub-matrix formed by restricting the rows of to , and denotes the sub-matrix formed by restricting the rows of to and columns to .

Note that when , is a vector, and is an vector.

To explain information leakage, we first consider an idealized case where each row of has nonzeros. In this case, there is no need for linear filtering, so and . Recall that consists of many signal islands, and let be one of them. It is seen that

| (13) |

and how well we can estimate is captured by the Fisher information matrix [Lehmann and Casella (1998)].

Come back to the case where is nonsparse. Interestingly, despite the strong correlations, continues to be the Fisher information for estimating . However, when is nonsparse, we must use a linear filtering as suggested, and we have

| (14) |

Moreover, letting , it follows that

By the definition of , and the dimension of the following null space ,

| (15) |

Compare (14) with (13), and imagine the oracle situation where we are told the mean vector of in both. The difference is that we can fully recover using (13), but are not able to do so with only (14). In other words, the information containing is partially lost in (14): if we estimate with (14) alone, we will never achieve the desired accuracy.

The argument is validated in Lemma 2.2 below, where the Fisher information associated with (14) is strictly “smaller” than ; the difference between two matrices can be derived by taking and in (17). We call this phenomenon “information leakage.”

To mitigate this, we expand the information content by including data in the neighborhood of . This process is called “patching.” Let be an extension of by adding a few neighboring nodes, and define similarly and . Assuming that there is no edge between any node in and any node in ,

| (16) |

The Fisher information matrix for under model (16) is larger than that of (14), which is captured in the following lemma.

Lemma 2.2

The Fisher information matrix associated with model (16) is

| (17) |

where is any matrix whose columns form an orthonormal basis of .

When the size of becomes appropriately large, the second matrix in (17) is small element-wise (and so is negligible) under mild conditions [see details in Lemma A.3 in Ke, Jin and Fan (2014)]. This matrix is usually nonnegligible if we set and (i.e., without patching).

Example 1.

Although one of the major effects of information leakage is a reduction in the signal-to-noise ratio, this phenomenon is very different from the well-known “signal cancellation” or “partial faithfulness” in variable selection. “Signal cancellation” is caused by correlations between signal covariates, and CASE overcomes this problem by using multivariate screening. However, “information leakage” is caused by the use of a linear filtering. From Lemma 2.2, we can see that the information leakage appears no matter for what signal vector . CASE overcomes this problem by the patching technique.

2.5 Covariate assisted screening and estimation (CASE)

In summary, we start from the post-filtering regression model

We have observed the following:

-

•

Signal decomposability. Linear filtering induces sparsity in GOSD, a graph constructed from the Gram matrix . In this graph, the set of all true signals decomposes into many small-size signal islands, each signal island is a component of GOSD.

-

•

Information patching. Linear filtering also causes information leakage, which can be overcome by delicate patching technique.

Naturally, these motivate a two-stage screen and clean approach for variable selection, which we call covariate assisted screening and estimation (CASE). CASE contains a patching and screening (PS) step and a patching and estimation (PE) step.

-

•

-step. We use sequential -tests to identify candidates for each signal island. Each -test is guided by , and aided by a carefully designed patching step. This achieves multivariate screening without visiting all submodels.

-

•

-step. We re-investigate each candidate with penalized MLE and certain patching technique, in hopes of removing false positives.

For the purpose of patching, the -step and the -step use tuning integers and , respectively. The following notation is frequently used in this paper.

Definition 2.6.

For any index , . For any subset of , . Similar notation applies to and .

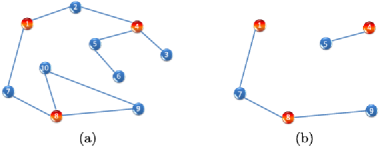

We now discuss two steps in detail. Consider the -step first. Fix . Suppose that has a total of connected subgraphs with size , which we denote by , arranged in the ascending order of the sizes, with ties breaking lexicographically.

Example 2(a).

We illustrate this with a toy example, where and the GOSD is displayed in Figure 2(a). For , GOSD has connected subgraphs, which we arrange as follows. Note that are singletons, are connected pairs and are connected triplets

Here we examine sequentially only the 30 submodels above to decide whether any variables have additional utilities given the variables recruited before, via -tests. The first 10 screening problems are just the univariate screening. After that, starting from bivariate screening, we examine the variables given those selected so far. Suppose that we are examining the submodel . The testing problem depends on how the variables are selected in the previous steps. For example, if the variables have already been selected in the univariate screening, there is no new recruitment, and we move on to examine the submodel . If the variables have been recruited so far, we need to test if variable has additional contributions given variable . If the variables have been recruited in the previous steps, we will examine whether variables together have any significant contributions. Therefore, we have never run regression for more than two variables. Similarly, for trivariate screening, we will never run regression for more than 3 variables. Clearly, multivariate screening improves the marginal screening in that it gives signal variables chances to be recruited if they are wrongly excluded by the marginal method.

We now formally describe the procedure. The -step contains sub-stages, where we screen sequentially, . Let be the set of retained indices at the end of stage , with as the convention. For , the th sub-stage contains two sub-steps:

-

•

(Initial step). Let represent the set of nodes in that have already been accepted by the end of the th sub-stage, and let be the set of other nodes in .

-

•

(Updating step). Write for short . Fixing a tuning parameter for patching, introduce

Figure 2: Illustration of graph of strong dependence (GOSD). Red: signal nodes. Blue: noise nodes. (a) GOSD with 10 nodes. (b) Nodes of GOSD that survived the -step. where is a random vector and can be thought of as the covariance matrix of . Define , a subvector of , and , a submatrix of , as follows:

Introduce the test statistic

(20) For a threshold to be determined, we update the set of retained nodes by if , and let otherwise. In other words, we accept nodes in only when they have additional utilities.

The -step terminates at . We then write so that

In the -step, as we screen, we accept nodes sequentially. Once a node is accepted in the -step, it stays there until the end of the -step; of course, this node could be killed in the -step. In spirit, this is similar to the well-known forward regression method, but the implementation of two methods are significantly different.

The -step uses a collection of tuning thresholds

A convenient choice for these thresholds is to let for a properly small fixed constant . See Section 2.9 (and also Sections 2.10–2.11) for more discussion on the choices of .

In the -step, we use -test for screening. This is the best choice when the coordinates of are Gaussian and have the same variance. When the Gaussian assumption on is questionable, we must note that the -test depends on the Gaussianity of for all -different , not on that of ; could be approximately Gaussian by central limit theorem. Therefore, the performance of -test is relatively robust to non-Gaussianity. If circumstances arise that the -test is not appropriate (e.g., misspecification of the model, low quantity of the data), we may need an alternative, say, some nonparametric tests. In this case, if the efficiency of the test is nearly optimal, then the screening in the -step would continue to be successful.

How does the -step help in variable selection? In Section A in Ke, Jin and Fan (2014), we show that in a broad context, provided that the tuning parameters are properly set, the -step has two noteworthy properties: the sure screening (SS) property and the separable after screening (SAS) property. The SS property says that contains all but a negligible fraction of the true signals. The SAS property says that if we view as a subgraph of (more precisely, as a subgraph of , an expanded graph of to be introduce below), then this subgraph decomposes into many disconnected components, each having a moderate size.

Together, the SS property and the SAS property enable us to reduce the original large-scale problem to many parallel small-size regression problems, and pave the way for the -step. See Section A in Ke, Jin and Fan (2014) for details.

Example 2(b).

We illustrate the above points with the toy example in Example 2(a). Suppose after the -step, the set of retained indices is ; see Figure 2(b). In this example, we have a total of three signal nodes, , and , which are all retained in and so the -step yields sure screening. On the other hand, contains a few nodes of false positives, which will be further cleaned in the -step. At the same time, viewing it as a subgraph of , decomposes into two disconnected components, and ; compare Figure 2(a). The SS property and the SAS property enable us to reduce the original problem of nodes to two parallel regression problems, one with nodes, and the other with nodes.

We now discuss the -step. Recall that is the tuning parameter for the patching of the -step, and let be as in Definition 2.6. The following graph can be viewed as an expanded graph of .

Definition 2.7.

Let be the graph where and there is an edge between nodes and when there exist nodes and such that there is an edge between and in .

Recall that is the set of retained indices at the end of the -step.

Definition 2.8.

Fix a graph and its subgraph . We say if is a connected subgraph of , and if is a component (maximal connected subgraph) of .

Fix . When , CASE estimates as . When , viewing as a subgraph of , there is a unique subgraph such that . Fix two tuning parameters and . We estimate by minimizing

| (21) | |||

subject to that is an vector each of which nonzero coordinate , where denotes the -norm of . Putting these together gives the final estimator of CASE .

2.6 Computational complexity of CASE, comparison with multivariate screening

The -step is closely related to the well-known method of marginal screening and has a moderate computational complexity.

Marginal screening selects variables by thresholding the vector coordinate-wise. The method is computationally fast, but it neglects “local” graphical structures, and is thus ineffective. For this reason, in many challenging problems, it is desirable to use multivariate screening methods which adapt to “local” graphical structures.

Fix . An -variate -screening procedure is one of such desired methods. The method screens all -tuples of coordinates of using -tests, for all , in an exhaustive (brute-force) fashion. Seemingly, the method adapts to “local” graphical structures and could be much more effective than marginal screening. However, such a procedure has a computational cost of [excluding the computational cost for obtaining from ; same below] which is usually not affordable when is large.

The main innovation of the -step is to use a graph-assisted -variate -screening, which is both effective in variable selection and efficient in computation. In fact, the -step only screens -tuples of coordinates of that form a connected subgraph of , for all . Therefore, if is -sparse, then there are connected subgraphs of with size ; so if is no greater than a multi- term (see Definition 2.10), then the computational complexity of the -step is only , up to a multi- term.

Example 2(c).

We illustrate the difference between the above three methods with the toy example in Example 2(a), where and the GOSD is displayed in Figure 2(a). Suppose we choose . Marginal screening screens all single nodes of the GOSD. The brute-force -variate screening screens all -tuples of indices, , with a total of such -tuples. The -variate screening in the -step only screens -tuples that are connected subgraphs of , for , and in this example, we only have such connected subgraphs.

The computational complexity of the -step consists two parts. The first part is the complexity of obtaining all components of , which is and where is the maximum degree of ; note that for settings considered in this paper, does not exceed a multi- term [see Lemma B.2 in Ke, Jin and Fan (2014)]. The second part of the complexity comes from solving (2.5), which hinges on the maximal size of . In Lemma A.2 in Ke, Jin and Fan (2014), we show that in a broad context, the maximal size of does not exceed a constant , provided the thresholds are properly set. Numerical studies in Section 3 also support this point. Therefore, the complexity in this part does not exceed . As a result, the computational complexity of the -step is moderate. Here, the bound is conservative; the actual computational complexity is much smaller than this.

How does CASE perform? In Sections 2.7–2.9, we set up an asymptotic framework and show that CASE is asymptotically minimax in terms of the Hamming distance over a wide class of situations. In Sections 2.10–2.11, we apply CASE to the long-memory time series and the change-point model, and elaborate the optimality of CASE in such models with the so-called phase diagram.

2.7 Asymptotic rare and weak model

In this section, we add an asymptotic framework to the rare and weak signal model introduced in Section 2.1. We use as the driving asymptotic parameter and tie to through some fixed parameters.

In particular, we fix and model the sparse parameter by

| (22) |

Note that as grows, the signal becomes increasingly sparse. It turns out that the most interesting range of signal strength is ; see, for example, Ji and Jin (2012). For much smaller , successful recovery is impossible. For much larger , the problem is relatively easy. The critical value of depends on in a complicate way. In light of this, we fix , and let

| (23) |

At the same time, recalling that in , we require so that for all . Fixing , we now further restrict to the following subset of :

| (24) |

Requiring the strength of each signal is mainly for technical reasons, and hopefully, such a constraint can be removed in the near future. From a practical point of view, since usually we do not have sufficient information on , we prefer to have a larger : we hope that when is properly large, is broad enough, so that neither the optimal procedure nor the minimax risk needs to adapt to .

Toward this end, we impose some mild regularity conditions on and the Gram matrix . Let be the smallest integer such that

| (25) |

For any Gram matrix and , let be the minimum of the smallest eigenvalues of all principle sub-matrices of . Introduce

| (26) |

For any two subsets and of , consider the optimization problem

up to the constraints that if and otherwise, where , and that in the special case of , the sign vectors of and are unequal. Introduce

The following lemma is elementary, so we omit the proof.

Lemma 2.3

For any , there is a constant such that .

In this paper, except for Section 2.11 where we discuss the change-point model, we assume

| (27) |

Under such conditions, is broad enough and the minimax risk (to be introduced below) does not depend on . See Section 2.8 for more discussion.

For any variable selection procedure , we measure the performance by the Hamming distance

where the expectation is taken with respect to . Here, for any vector , denotes the sign vector [for any number , when , , and correspondingly].

Under , , so the overall Hamming distance is

where is the expectation with respect to the law of . Finally, the minimax Hamming distance under is

In next section, we will see that the minimax Hamming distance does not depend on as long as (27) holds.

In many recent works, the probability of exact support recovery or oracle property is used to assess optimality; see, for example, Fan and Li (2001), Zhao and Yu (2006), Fan, Xue and Zou (2014), Zou (2006). However, when signals are rare and weak, exact support recovery is usually impossible, and the Hamming distance is a more appropriate criterion for assessing optimality. In comparison, study on the minimax Hamming distance is not only mathematically more demanding but also scientifically more relevant than that on the oracle property.

2.8 Lower bound for the minimax Hamming distance

We view the(global) Hamming distance as the aggregation of “local” Hamming errors. To construct a lower bound for the (global) minimax Hamming distance, the key is to construct lower bounds for “local” Hamming errors. Fix . The “local” Hamming error at index is the risk we make among the neighboring indices of in GOSD, say, , where is as in (25) and is the geodesic distance between and in the GOSD. The lower bound for such a “local” Hamming error is characterized by an exponent , which we now introduce.

For any subset , let be the vector such that the th coordinate is if and otherwise. Fixing two subsets and of , we introduce

| (28) |

subject to , and let

The exponent is defined by

| (30) |

The notation is frequently used in this paper.

Definition 2.10.

, as a positive sequence indexed by , is called a multi- term if for any fixed , and.

It can be shown that provides a lower bound for the “local” minimax Hamming distance at index , and that when (27) holds, does not depend on ; see Lemma 16 in Jin, Zhang and Zhang (2014) for details. In the remaining part of the paper, we will write it as for short.

At the same time, in order for the aggregation of all lower bounds for “local” Hamming errors to give a lower bound for the “global” Hamming distance, we need to introduce graph of least favorables (GOLF). Toward this end, recalling and as in (25) and (2.8), respectively, let

and when there is a tie, pick the one that appears first lexicographically. We can think as the “least favorable” configuration at index .

Definition 2.11.

GOLF is the graph where and there is an edge between and if and only if .

The following theorem is similar to Theorem 14 in Jin, Zhang and Zhang (2014), so we omit the proof.

Theorem 2.1

Suppose (27) holds so that does not depend on the parameter for sufficiently large . As , , where is the maximum degree of all nodes in .

In many examples, including those of primary interest of this paper,

| (31) |

In such cases, we have the following lower bound:

| (32) |

2.9 Upper bound and optimality of CASE

In this section, we show that in a broad context, provided the tuning parameters are properly set, CASE achieves the lower bound prescribed in Theorem 2.1, up to some terms. Therefore, the lower bound in Theorem 2.1 is tight, and CASE achieves the optimal rate of convergence.

For a given , we focus on linear models with the Gram matrix from

where we recall that the two terms on the right-hand side are defined in (2.2) and (26), respectively. The following lemma is proved in Section B in Ke, Jin and Fan (2014).

Lemma 2.4

For , the maximum degree of nodes in GOLF satisfies .

For any linear filter , let be the so-called characterization polynomial. We need some regularity conditions:

-

•

Regularization Condition A (RCA). For any root of , .

-

•

Regularization Condition B (RCB). There are constants and such that ( is as in Section 2.8).

For many well-known linear filters such as adjacent differences, seasonal differences, etc., RCA is satisfied. Also, RCB is only a mild condition since can be any positive number. For example, RCB holds in the change-point model and long-memory time series model with certain matrices. In general, is not because when is sparse, is very likely to be approximately singular, and the associated value of can be small when is large. This is true even for very simple [e.g., , and ].

At the same time, these conditions can be further relaxed. For example, for the change-point problem, the Gram matrix has barely any off-diagonal decay, and does not belong to . Nevertheless, with slight modification in the procedure, the main results continue to hold.

CASE uses tuning parameters . The choice of is flexible, and we usually set . For the main theorem below, we treat as given. In practice, taking to be a small integer (say, ) is usually sufficient, unless the signals are relatively dense (say, ). The choice of and are also relatively flexible, and letting be a sufficiently large constant and be for some constant is sufficient, where is as in Definition 2.2, and is as in RCB.

At the same time, in principle, the optimal choices of are

| (33) |

which depend on the underlying parameters that are unknown to us. Despite this, our numeric studies in Section 3 suggest that the choices of are relatively flexible; see Sections 3–4 for more discussions.

Last, we discuss how to choose . Let , where is a constant. It turns out that the main result (Theorem 2.2 below) holds as long as

| (34) |

where is an appropriately small constant, and for any subsets ,

here,

with

| (37) |

and

| (38) |

where with , and , and are defined similarly. Compared to (• ‣ 2.5), we see that , , and are all submatrices of . Hence, can be viewed as a counterpart of by replacing the submatrices of by the corresponding ones of .

From a practical point of view, there is a trade-off in choosing : a larger would increase the number of falsely selected variables in the -step, but would also reduce the computational cost in the -step. The following is a convenient choice which we recommend in this paper:

| (39) |

where is a constant, and is as in .

We are now ready for the main result of this paper.

Theorem 2.2

Suppose that for sufficiently large , , with and that RCA-RCB hold. Consider with the tuning parameters specified above. Then as ,

| (40) | |||

Combine Lemma 2.4 and Theorem 2.2. Given the parameter is appropriately large, both the upper bound and the lower bound are tight, and CASE achieves the optimal rate of convergence prescribed by

| (41) |

Theorem 2.2 is proved in Section A in Ke, Jin and Fan (2014), where we explain the key idea behind the procedure, as well as the selection of the tuning parameters.

2.10 Application to the long-memory time series model

The long-memory time series model in Section 1 can be written as a regression model,

where the Gram matrix is asymptotically Toeplitz and has slow off-diagonal decays. Without loss of generality, we consider the following idealized case where is an exact Toeplitz matrix generated by a spectral density :

| (42) |

In the literature [Chen, Hurvich and Lu (2006), Moulines and Soulier (1999)], the spectral density for a long-memory process is usually characterized as

| (43) |

where is the long-memory parameter, is a positive symmetric function that is continuous on and is twice differentiable except at .

In this model, the Gram matrix is nonsparse, but it is sparsifiable. To see the point, let and let be the first-order adjacent row-differencing. On one hand, since the spectral density is singular at the origin, it follows from the Fourier analysis that , and hence is nonsparse. On the other hand, it is seen that

where we recall that and note that denotes the Fourier transform of . Compared to , is nonsingular at the origin. Additionally, it is seen that , where , so is sparse (a similar claim applies to ). This shows that is sparsifiable by adjacent row-differencing.

In this example, there is a function that only depends on such that

where the subscript “lts” stands for long-memory time series. The following theorem can be derived from Theorem 2.2, and is proved in Section B in Ke, Jin and Fan (2014).

Theorem 2.3

For a long-memory time series model where , the minimax Hamming distance then satisfies . If we apply CASE by letting , , and the tuning parameters be set as in Section 2.9, then

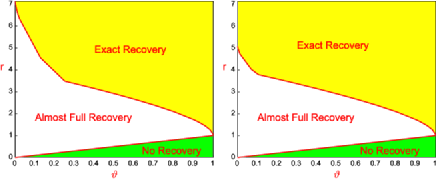

Theorem 2.3 can be interpreted by the so-called phase diagram. Phase diagram is a way to visualize settings where the signals are so rare and weak that successful variable selection is simply impossible [Ji and Jin (2012)]. In detail, for a spectral density and , let be the unique solution of . Note that characterizes the minimum signal strength required for exact support recovery with high probability. The following proposition is proved in Section B in Ke, Jin and Fan (2014).

Lemma 2.5

Under the conditions of Theorem 2.3, if exists, then is a decreasing function in , with limits and as and , respectively.

Call the two-dimensional space the phase space. Interestingly, there is a partition of the phase space as follows.

-

•

Region of no recovery . In this region, the minimax Hamming distance , where is approximately the number of signals. In this region, the signals are too rare and weak and successful variable selection is impossible.

-

•

Region of almost full recovery . In this region, the minimax Hamming distance is much larger than but much smaller than . Therefore, the optimal procedure can recover most of the signals but not all of them.

-

•

Region of exact recovery . In this region, the minimax Hamming distance is . Therefore, the optimal procedure recovers all signals with probability .

Because of the partition of the phase space, we call this the phase diagram.

From time to time, we wish to have a more explicit formula for the rate and the critical value . In general, this is a hard problem, but both quantities can be computed numerically when is given. In Figure 3, we display the phase diagrams for the autoregressive fractionally integrated moving average process (FARIMA) with parameters [Fan and Yao (2003)], where

| (44) |

Take , for example, for small .

2.11 Application to the change-point model

The change-point model in the Introduction can be viewed as a special case of model (1), where is as in (7), and the Gram matrix satisfies

| (45) |

For technical reasons, it is more convenient not to normalize the diagonals of to .

The change-point model can be viewed as an “extreme” case of what is studied in this paper. On one hand, the Gram matrix is “ill-posed,” and each row of does not satisfy the condition of off-diagonal decay in Theorem 2.2. On the other hand, has a very special structure which can be largely exploited. In fact, if we sparsify using the linear filter , where , it is seen that , and is a tri-diagonal matrix with , which are very simple matrices. For these reasons, we modify the CASE as follows:

-

•

Due to the simple structure of , we do not need patching in the -step (i.e., ).

-

•

For the same reason, the choices of thresholds are more flexible than before, and taking for a proper constant works.

-

•

Since is “extreme” (the smallest eigenvalue tends to as ), we have to modify the -step carefully.

In detail, the -step for the change-point model is as follows. Given , let be as in Definition 2.7. Recall that denotes the set of all retained indices at the end of the -step. We view as a subgraph of , and let be one of its components. The goal is to split into different subsets

and for each subset , , we construct a patched set . We then estimate separately using (2.5). Putting together gives our estimate of .

The subsets are recursively constructed as follows. Denote , , and write

First, letting be the largest index such that , define

Next, letting be the largest index such that , define

Continue this process until for some , , . In this construction, for each , if we arrange all the nodes of in the ascending order, then the number of nodes in front of is significantly smaller than the number of nodes behind .

In practice, we introduce a suboptimal but much simpler patching approach as follows. Fix a component of . In this approach, instead of splitting it into smaller sets and patching them separately as in the previous approach, we patch the whole set by

| (46) |

and estimate using (2.5). Our numeric studies show that two approaches have comparable performances.

Define

| (47) |

where “cp” stands for change-point. Choose the tuning parameters of CASE such that

| (48) |

that , and that [recall that we take for all in the change-point setting]. Note that the choice of is different from that in Section 2.5. The main result in this section is the following theorem which is proved in Section B in Ke, Jin and Fan (2014).

Theorem 2.4

For the change-point model, the minimax Hamming distance satisfies . Furthermore, with the tuning parameters specified above satisfies

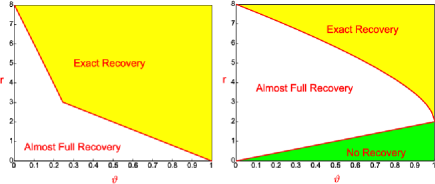

It is noteworthy that the exponent has a phase change depending on the ratios of . The insight is, when , the minimax Hamming distance is dominated by the Hamming errors we make in distinguishing between an isolated change-point and a pair of adjacent change-points, and when , the minimax Hamming distance is dominated by the Hamming errors of distinguishing the case of consecutive change-point triplets (say, change-points at ) from the case where we do not have a change-point in the middle of the triplets (i.e., the change-points are only at ).

Similarly, the main results on the change-point problem can be visualized with the phase diagram in Figure 4. An interesting point is that it is possible to have almost full recovery even when the signal strength parameter is as small as . See the proof of Theorem 2.4 for details.

Alternatively, one may apply the following approach to the change-point problem. Treat the liner change-point model as a regression model as in Section 1 (page 1), and let be the least-squares estimate. It is seen that , where we note that is tridiagonal and coincides with . In this simple setting, a natural approach is to apply a coordinate-wise thresholding to locate the signals. But this neglects the covariance of in detecting the locations of the signals and is not optimal even with the ideal choice of thresholding parameter , since the corresponding risk satisfies

The proof of this is elementary and omitted. The phase diagram of this method is displayed in Figure 4, right panel, which suggests the method is nonoptimal.

Other popular methods in locating multiple change-points include the global methods [Harchaoui and Lévy-Leduc (2010), Olshen et al. (2004), Tibshirani (1996), Yao and Au (1989)] and local methods [e.g., SaRa in Niu and Zhang (2012)]. The global methods are usually computationally expensive and can hardly be optimal due to the strong correlation nature of this problem. Our procedure is related to the local methods but is different in important ways. Our method exploits the graphical structures and uses the GOSD to guide both the screening and cleaning, but SaRa does not utilize the graphical structures and can be shown to be nonoptimal.

To conclude the section, we remark that the change-point model constitutes a special case of the settings we discuss in the paper, where setting some of the tuning parameters is more convenient than in the general case. First, for the change-point model, we can simply set and . Second, there is an easy-to-compute preliminary estimator available. On the other hand, the performance of CASE is substantially better than the other methods in many situations. We believe that CASE is potentially a very useful method in practice for the change-point problem.

3 Simulations

We conducted a small-scale numeric study where we compare CASE and several popular approaches. The study contains two parts, Section 3.1 and Section 3.2, where we investigate the change-point model and the long-memory time series model, respectively.

In this section, for convenience. The core tuning parameters for CASE are . We streamline these tuning parameters in a way so they only depend on two tuning parameters (calibrating the sparsity and the minimum signal strength, resp.). Therefore, essentially, CASE only uses two tuning parameters. Our experiments show that the performance of CASE is relatively insensitive to these two tuning parameters. Furthermore, these two tuning parameters can be set in a data driven fashion, especially in the change-point model. See details below.

We set so that in the screening stage of CASE, bivariate screening is the highest order screening we use. At least for examples considered here, using a higher-order screening does not have a significant improvement. For long-memory time series, we need a regularization parameter (but we do not need it for the change-point model). The guideline for choosing is to make sure the maximum degree of GOSD is (say) or smaller. In this section, we choose . The maximum degree of GOSD is much higher if we choose a much smaller ; in this case, CASE has similar performance, but is computationally much slower.

3.1 Change-point model

In this section, we use model (3) to investigate the performance of CASE in identifying multiple change-points. For a given set of parameters , we set and . First, we generate a vector by , where is the uniform distribution over [when , represents the point mass at ]. Next, we construct the mean vector in model (3) by , . Last, we generate the data vector by .

CASE, when applied to the change-point model, requires tuning parameters . Denote by the average number of signals. Given , we determine the tuning parameters as follows: As mentioned earlier, we take , and . Also, we take , and . contains thresholds for each pair of sets ; we take with

| (49) |

where , and is given in (38). With these choices, CASE only depends on two parameters .

Experiment 1a. We compare CASE with the lasso [Tibshirani (1996)], SCAD [Fan and Li (2001)] (penalty shape parameter ), MC [Zhang (2010)] (penalty shape parameter ) and SaRa [Niu and Zhang (2012)]. For tuning parameters and (integer), SaRa takes the following form:

The tuning parameters for the lasso, SCAD, MC and SaRa are ideally set (pretending we know ). For CASE, all tuning parameters depend on , so we implement the procedure using the true values of ; this yields slightly inferior results than that of setting ideally (pretending we know , as we do in the lasso, SCAD, MC and SaRa), so our comparison in this setting is fair. Note that even when are given, it is unclear how to set the tuning parameters of the lasso, SCAD, MC and SaRa.

Fix and . We let range in and range in . The parameters fall into the regime where exact-recovery is impossible. Table 1 reports the average Hamming errors of independent repetitions. We see that CASE consistently outperforms other methods, especially when is small, that is, signals are less sparse.

We also observe that three global penalization methods, the lasso, SCAD and MC, perform unsatisfactorily, with Hamming errors comparable to the expected number of signals . It suggests that the global penalization methods are not appropriate for the change-point model when the signals are rare and weak. Similar conclusions can be drawn in most experiments in this section. To save space, we only report results of the lasso, SCAD and MC in this experiment.

| 0.3 | CASE | |||||||

|---|---|---|---|---|---|---|---|---|

| lasso | ||||||||

| SCAD | ||||||||

| MC | ||||||||

| SaRa | ||||||||

| 0.45 | CASE | |||||||

| lasso | ||||||||

| SCAD | ||||||||

| MC | ||||||||

| SaRa | ||||||||

| 0.6 | CASE | |||||||

| lasso | ||||||||

| SCAD | ||||||||

| MC | ||||||||

| SaRa | ||||||||

| 0.75 | CASE | |||||||

| lasso | ||||||||

| SCAD | ||||||||

| MC | ||||||||

| SaRa | ||||||||

Experiment 1b. In this experiment, we investigate the performanceof CASE with estimated by SaRa; we call this the adaptiveCASE. In detail, we estimate by and , where the tuning parameters of SaRa are determined by minimizing ; this is a slight modification of Bayesian information criteria (BIC).

For experiment, we use the same setting as in Experiment 1a. Table 2 reports the average Hamming errors of CASE, SaRa and the adaptive CASE based on independent repetitions. First, the adaptive CASE [CASE but are estimated by SaRa] has a very similar performance to CASE. Second, although the adaptive CASE uses SaRa as the preliminary estimator, its performance is substantially better than that of SaRa (and other methods in the same setting; see Experiment 1a).

| 0.3 | CASE | |||||||

|---|---|---|---|---|---|---|---|---|

| adCASE | ||||||||

| SaRa | ||||||||

| 0.45 | CASE | |||||||

| adCASE | ||||||||

| SaRa | ||||||||

| 0.6 | CASE | |||||||

| adCASE | ||||||||

| SaRa | ||||||||

| 0.75 | CASE | |||||||

| adCASE | ||||||||

| SaRa | ||||||||

Experiment 2. In this experiment, we consider the post-filtering model, model (4), associated with the change-point model, and illustrate that the seeming simplicity of this model (where , and is tri-diagonal) does not mean it is a trivial setting for variable selection. In particular, if we naively apply the -penalization to the post-filtering model, we end up with naive soft/hard thresholding; we illustrate our point by showing that CASE significantly outperforms naive thresholding (since we use Hamming distance as the loss function, there is no difference between soft and hard thresholding). For both CASE and naive thresholding, we set tuning parameters assuming as known. The threshold of naive thresholding is set as , where and ; this threshold choice is known as theoretically optimal.

Fix and (so that the signals have equal strengths). Let range in , and range in . Table 3 reports the average Hamming errors of independent repetitions, which show that CASE outperforms naive thresholding in most cases, especially when is small or is small. It suggests that the post-filtering model remains largely nontrivial, and to deal with it, we need sophisticated methods.

| 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | |||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.35 | CASE | 7.3 | |||||||||

| nHT | 0.5 | ||||||||||

| 0.50 | CASE | 0.2 | |||||||||

| nHT | 0.2 | ||||||||||

| 0.75 | CASE | 0.0 | |||||||||

| nHT | 0.0 | ||||||||||

Experiment 3. In this experiment, we fix , and let range in (so signals may have different strengths). We investigate a case where the signals have the “half-positive-half-negative” sign pattern, that is, , and a case where the signals have the “all-positive” sign pattern, that is, . We compare CASE with SaRa for different values of and sign patterns (we do not include the lasso, SCAD, MC in this particular experiment, for at least for the experiments reported above, they are inferior to SaRa). The tuning parameters for both CASE and SaRa are set ideally as in Experiment 1a. The results of independent repetitions are reported in Table 4, which suggest that CASE uniformly outperforms SaRa for various values of and the two sign patterns.

| 1 | 1.5 | 2 | 2.5 | 3 | ||

|---|---|---|---|---|---|---|

| Half–half | CASE | |||||

| SaRa | ||||||

| All-positive | CASE | |||||

| SaRa | ||||||

3.2 Long-memory time series model

In this section, we investigate long-memory time series, focusing on the process [Fan and Yao (2003)], where is the long-memory parameter. We let where is constructed according to (42)–(44). For generated in ways to be specified, we let .

CASE uses tuning parameters , which are set in the same way as in the change-point model, except for two differences. First, different from that in the change-point model, we need a regularization parameter which we set as . Second, we take .

Experiment 4a. In this experiment, we compare CASE with the lasso, SCAD (shape parameter ) and MC (shape parameter ). Fixing and , we let range in , and let range in . For each pair of , we generate the vector by . Similar to that in Experiment 1a, the tuning parameters of CASE are set assuming as known, and the tuning parameters of the lasso, SCAD and MC are set ideally to minimize the Hamming error (assuming is known). By similar argument as in Experiment 1a, the comparison is fair. Table 5 reports the average Hamming errors based on independent repetitions. The results suggest that CASE outperforms the lasso and SCAD, and has a comparable performance to that of MC.

| 4 | 5 | 6 | 7 | 8 | |||

|---|---|---|---|---|---|---|---|

| 0.35 | CASE | ||||||

| lasso | |||||||

| SCAD | |||||||

| MC | |||||||

| 0.45 | CASE | ||||||

| lasso | |||||||

| SCAD | |||||||

| MC | |||||||

| 0.55 | CASE | ||||||

| lasso | |||||||

| SCAD | |||||||

| MC | |||||||

Experiment 4b. We investigate the setting where “signal cancellation” is more severe than that in Experiment 4b. Toward this end, we use the same setting as in Experiment 4a, except for that is generated in a way that signals appear in adjacent pairs with opposite signs, , , where is the point mass at . Hamming errors based on repetitions are reported in Table 6, suggesting that CASE significantly outperforms all the other methods.

It is noteworthy that MC behaves much more unsatisfactorily here than in Experiment 4a, and the main reason is that MC does not adequately address “signal cancellation.” In contrast, one of the major advantages of CASE is that it addresses adequately the “signal cancellation”; this is why it has satisfactory performance in both Experiments 4a and 4b.

| 4 | 5 | 6 | 7 | 8 | |||

|---|---|---|---|---|---|---|---|

| 0.35 | CASE | ||||||

| lasso | |||||||

| SCAD | |||||||

| MC | |||||||

| 0.45 | CASE | ||||||

| lasso | |||||||

| SCAD | |||||||

| MC | |||||||

| 0.55 | CASE | ||||||

| lasso | |||||||

| SCAD | |||||||

| MC | |||||||

Experiment 5. In some of the experiments above, we set the tuning parameters of CASE assuming as known. It is therefore interesting to investigate how the misspecification of affects the performance of CASE. Fix and . We consider two combinations of : . The vector is generated in the same way as in Experiment 4b, with the signals appearing in adjacent pairs. We fix one parameter of and mis-specify the other [since is not on the same scale as , the results are reported based on the misspecification of , instead of ; recall here ]. We then apply CASE with tuning parameters set based on the misspecified values of . Table 7 reports the average Hamming errors of independent repetitions, which is a rather flat function of misspecified values of (with fixed) or of misspecified values of (with fixed). In comparison, the Hamming errors of the lasso are 97.9 and 40.1 in the two settings, respectively, with the tuning parameter ideally set as in Experiment 1a. This suggests that CASE is relatively insensitive to the misspecification of , and outperforms the lasso as long as the misspecification of is not severe.

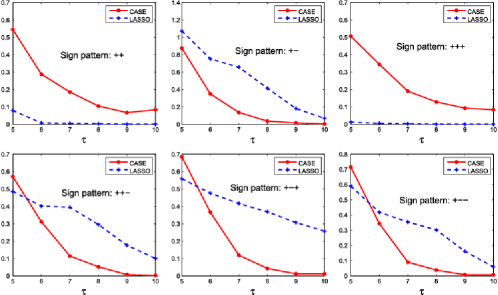

Experiment 6. In this experiment, we continue to investigate the effect of “signal cancellation,” where we compare CASE with the lasso using several choices of signal patterns (and so the levels of “signal cancellation” vary). Fix , , , and let range in . The experiment contains two parts. In the first part, we partition into blocks, where each block contains two adjacent indices. In fraction of the blocks, . In the fraction of the blocks, we have either that for both in the block (we denote the sign pattern by “”), or that if is the first index in the block and otherwise (sign pattern “”). In the second part, we partition into blocks (block size is ), and generate in a similar fashion, but with four different sign patterns in each block: “,” “,” “” and “.” Hamming errors based on independent repetitions are reported in Figure 5. The results suggest that (a) when the sign patterns are “” or “,” signal cancellation has negligible effects, and CASE is inferior to the lasso, (b) when the sign patterns are “,” “,” “” and “,” the effect of signal cancellation kicks in, and CASE outperforms the lasso in most cases. This is consistent with our theoretic insight that CASE adequately addresses signal cancellation, but the lasso does not.

4 Discussion

Variable selection when the Gram matrix is nonsparse is a challenging problem. We approach this problem by first sparsifying with a finite order linear filter, and then constructing a sparse graph GOSD. The key insight is that, in the post-filtering data, the true signals live in many small-size components that are disconnected in GOSD, but we do not know where. We propose CASE as a new approach to variable selection. This is a two-stage screen and clean method, where we first use a covariance-assisted multivariate screening to identify candidates for such small-size components, and then re-examine each candidate with penalized least squares. In both stages, to overcome the problem of information leakage, we employ a delicate patching technique.

We develop an asymptotic framework focusing on the regime where the signals are rare and weak so that successful variable selection is challenging but is still possible. We show that CASE achieves the optimal rate of convergence in Hamming distance across a wide class of situations where is nonsparse but sparsifiable. Such optimality cannot be achieved by many popular methods, including but not limited to the lasso, SCAD, MC and Dantzig selector. When is nonsparse, these methods are not expected to behave well even when the signals are strong. We have successfully applied CASE to two different applications: the change-point problem and the long-memory times series.

Compared to the well-known method of marginal screening [Fan and Song (2010), Wasserman and Roeder (2009)], CASE employs a covariance-assisted multivariate screening procedure, so that it is theoretically more effective than marginal screening, with only a moderate increase in the computational complexity. CASE is closely related to the graphical lasso [Friedman, Hastie and Tibshirani (2008), Meinshausen and Bühlmann (2006)], which also attempts to exploit the graph structure. However, the setting considered here is very different from that in Friedman, Hastie and Tibshirani (2008) and Meinshausen and Bühlmann (2006), and our emphasis on optimality is also very different.

The paper is closely related to the recent work Jin, Zhang and Zhang (2014) [see also Ji and Jin (2012)], but is different in important ways. The work in Jin, Zhang and Zhang (2014) is motivated by recent literature of compressive sensing and genetic regulatory network, and is largely focused on the case where the Gram matrix is sparse in an unstructured fashion. The current work is motivated by the recent interest on DNA-copy number variation and long-memory time series, and is focused on the case where there are strong dependence between different design variables, so is usually nonsparse and sometimes ill-posed. To deal with the strong dependence, we have to use a finite-order linear filter and delicate patching techniques. Additionally, the current paper also studies applications to the long-memory time series and the change-point problem which have not been considered in Jin, Zhang and Zhang (2014). Especially, the studies on the change-point problem encompasses very different and very delicate analysis on both the derivation of the lower bound and upper bound which we have not seen before in the literature. For these reasons, the two papers have very different scopes and techniques, and the results in one paper cannot be deduced from those in the other.

In this paper, we are primarily interested in the linear model, model (1), but CASE is applicable in much broader settings. For example, in model (1), we assume that the coordinates of have the same variance , and is known (and so without loss of generality, we assume ). When is unknown, the main results in this paper continue to hold, provided that we can estimate consistently [say, except for a probability of , there is an estimate such that ]. Such an estimator can be obtained by adapting the scaled-lasso approach by Sun and Zhang (2012) or the refitted cross validation by Fan, Guo and Hao (2012) to the post-filtering model (4). Correspondingly, we need to modify the tuning parameters of CASE slightly. For example, in the -step, is replaced by , and in the -step, and are replaced by and , respectively.

Also, in model (1), we have assumed that the coordinates of are Gaussian distributed. Such an assumption can also be relaxed. In fact, in the core of CASE is the analysis of low-dimensional sub-vectors of , where we note that each coordinate of has the form of for some constant and nonstochastic vector . Note that only depends on the design matrix and the index of the coordinate of (so there are different vectors at most). Essentially, the Gaussian assumption is only required for for all different choices of . Note that even when is non-Gaussian, could be approximately Gaussian by central limit theorem; this holds, for example, for the long-memory time series considered in the paper. As a result, the Gaussian assumption on can be largely relaxed.

The main results in this paper can be extended in many other directions. For example, we have used a rare and weak signal model where the signals are randomly generated from a two-component mixture. The main results continue to hold if we choose to use a much more general model, as long as the signals live in small-size isolated “islands” in the post-filtering data, where each island is a connected subgraph of GOSD.

Also, we have been focused on the change-point model and the long-memory time series model, where the post-filtering matrices have polynomial off-diagonal decay and are sparse in a structured fashion. CASE can be extended to more general settings, where the sparsity of the post-filtering matrices are unstructured, provided that we modify the patching technique accordingly: the patching set can be constructed by including nodes which are connected to the original set through a short-length path in the GOSD.

Still another extension is that the Gram matrix can be sparsified by an operator , but is not necessary linear filtering. To apply CASE to this setting, we need to design specific patching technique. For example, when is sparse, for a given , we can construct , where is a chosen threshold.

The paper is closely related to recent literature on DNA copy number variation and financial data analysis, and it is of interest to further investigate such connections. To save space, we leave explorations along this line to the future.

A key component of our approach is the notion of “sparsifiability,” meaning that we can make the Gram matrix sparse by some simple operations. Usually, to find such a simple operation, we need a good understanding about the structure of . In some applications, it is not hard to find such an operation:

-

•

In compressive sensing or genome-wide association study (GWAS), where the rows of the design matrix are i.i.d. samples from a -dimensional distribution of zero means and a sparse covariance matrix . In Compressive Sensing, is usually proportional to the identity matrix, and in GWAS, is a banded matrix. In such examples, is already sparse, and so sparsifiable.

-

•

The current paper is largely motivated by the change-point problem and long-memory time series models, where can be sparsifiable by a liner filter .

-

•

Another example of sparsifiability is that is the sum of a symmetric low-rank matrix and a sparse matrix ; when spectral norm of is much smaller than the smallest nonzero eigenvalue of , is sparsifiable by principle component analysis (PCA).

In more complicated case where we have little understanding about the structure , how to sparsify it with a simple operation is a nontrivial problem, though we can always try linear filtering, PCA or both. We leave the study along this line for future.