Autoregressive order identification for VAR models with non-constant variance

Abstract: The identification of the lag length for vector autoregressive models by mean of Akaike Information Criterion (), Partial Autoregressive and Correlation Matrices (PAM and PCM hereafter) is studied in the framework of processes with time varying variance. It is highlighted that the use of the standard tools are not justified in such a case. As a consequence we propose an adaptive which is robust to the presence of unconditional heteroscedasticity. Corrected confidence bounds are proposed for the usual PAM and PCM obtained from the Ordinary Least Squares (OLS) estimation. We also use the unconditional variance structure of the innovations to develop adaptive PAM and PCM. It is underlined that the adaptive PAM and PCM are more accurate than the OLS PAM and PCM for identifying the lag length of the autoregressive models. Monte Carlo experiments show that the adaptive have a greater ability to select the correct autoregressive order than the standard . An illustrative application using US international finance data is presented.

Keywords: Time varying unconditional variance;

VAR model; Model selection; AIC; Partial autoregressive matrices;

Partial autoregressive matrices.

1 Introduction

The analysis of time series using linear models is usually carried out following three steps. First the model is identified, then estimated and finally we proceed to the checking of the goodness-of-fit of the model (see Brockwell and Davis (1991, chapters 8 and 9)). Tools for the three phases in the specification-estimation-verification modeling cycle of time series with constant unconditional innovations variance are available in any of the specialized softwares as for instance R, SAS or JMulTi. The identification stage is important for the choice of a suitable model for the data. In this step the partial autoregressive and correlation matrices (PAM and PCM hereafter) are often used to identify VAR models with stationary innovations (see Tiao and Box (1981)). Information criteria are also extensively used. In the framework of stationary processes numerous information criteria have been studied (see e.g. Hannan and Quinn (1979), Cavanaugh (1997) or Boubacar Mainassara (2012)). One of the most commonly used information criterion is the Akaike Information Criterion () proposed by Akaike (1973). Nevertheless it is widely documented in the literature that the constant variance assumption is unrealistic for many economic data. Reference can be made to Mc-Connell, Mosser and Perez-Quiros (1999), Kim and Nelson (1999), Stock and Watson (2002), Ahmed, Levin and Wilson (2002), Herrera and Pesavento (2005) or Davis and Kahn (2008). In this paper we investigate the lag length identification problem of autoregressive processes in the important case where the unconditional innovations variance is time varying.

The statistical inference of processes with non constant variance has recently attracted much attention. Horváth and Steinebach (2000), Sanso, Arago and Carrion (2004) or Galeano and Pena (2007) among other contributions proposed tests to detect variance and/or covariance breaks in the residuals. Francq and Gautier (2004) studied the estimation of ARMA models with time varying parameters, allowing a finite number of regimes for the variance. Mikosch and Stărică (2004) give some theoretical evidence that financial data may exihibit non constant variance. In the context of GARCH models reference can be made to the works of Kokoszka and Leipus (2000), Engle and Rangel (2008), Dahlhaus and Rao (2006) or Horvath, Kokoszka and Zhang (2006) who investigated the inference for processes with possibly unconditional time varying variance. In the multivariate framework Bai (2000), Qu and Perron (2007) or Kim and Park (2010) among others studied autoregressive models with unconditionally non constant variance. Aue, Hörmann, Horvàth and Reimherr (2009) studied the break detection in the covariance structure of multivariate processes. Xu and Phillips (2008) studied the estimation of univariate autoregressive models whose innovations have a non constant variance. Patilea and Ra ssi (2012) generalized their findings in the case of Vector AutoRegressive (VAR) models with time-varying variance and found that the asymptotic covariance matrix obtained if one take into account of the non constant variance can be quite different from the standard covariance matrix expression. As a consequence they also provided Adaptive Least Squares (ALS) estimators which achieve a more efficient estimation of the autoregressive parameters. Patilea and Ra ssi (2011) proposed tools for checking the adequacy of the autoregressive order of VAR models when the unconditional variance is non constant.

In this paper modified tools for lag length identification in the case of multivariate autoregressive processes with time-varying variance are introduced. The unreliability of the use of the standard for the identification step in VAR modeling in presence of non constant variance is first highlighted. Consequently a modified based on the adaptive estimation of the non constant variance structure is proposed. We establish the suitability of the adaptive to identify the autoregressive order of non stationary but stable VAR processes through theoretical results and numerical illustrations. On the other hand it is also shown that the standard results on the OLS estimators of the PAM and PCM can be quite misleading. Consequently corrected confidence bounds are proposed. Using the adaptive approach more efficient estimators of the PAM and PCM are proposed. Therefore the identification tools proposed in this paper may be viewed as a complement of the above mentioned results on the estimation and diagnostic testing in the important framework of autoregressive models with non constant variance.

The structure of the paper is as follow. In Section 2 we define the model and introduce assumptions which give the general framework of our study. The asymptotic behavior of different estimators of the autoregressive parameters is given. We also describe the adaptive estimation of the variance. In Section 3 it is shown that the standard is irrelevant for model selection when the innovations variance is not constant. The adaptive is derived taking into account the time-varying variance in the Kullback-Leibler discrepancy. In Section 5 some Monte Carlo experiments results are given to examine the performances of the studied information criteria for VAR model identification in our non standard framework. We also investigate the lag length selection of a bivariate system of US international finance variables.

2 Estimation of the model

In this paper we restrict our attention to VAR models since they are extensively used for the analysis of multivariate time series (see e.g. Lütkepohl (2005)). Let us consider the -dimensional autoregressive process satisfying

| (2.1) | |||

where the ’s, , are such that

for all , with

and denotes the

determinant of a square matrix. We suppose that

are observed with .

Now let us denote by the integer part. For ease of exposition

we shall assume that the process is iid multivariate standard

Gaussian. Throughout the paper we assume that

the following conditions on the unconditional variance structure of the innovations process hold.

Assumption A1: The matrices

are positive definite and satisfy , where the

components of the matrix are measurable

deterministic functions on the interval , such that

, and each satisfies a

Lipschitz condition piecewise on a finite number of some

sub-intervals that partition .

The matrix is assumed positive definite for all .

The rescaling method of Dahlhaus (1997) is considered to specify the

unconditional variance structure in Assumption A1. Note that one should

formally use the notation with and

. Nevertheless we do not use the subscript to

lighten the notations. This specification allows to consider kinds of

time-varying variance which are commonly considered in the

literature as for instance abrupt shifts, smooth transitions or

periodic heteroscedasticity. Note that Sensier and Van Dijk (2004)

found that approximately 80% among 214 US macro-economic data they

investigated exhibit a variance break. Stărică (2003)

hypothesized that the returns of the Standard and Poors 500 stock

market index have a non constant unconditional variance. Then

considering the framework given by A1 is important given the

strong empirical evidence of non-constant unconditional variance

in many macro-economic and financial data. Our assumption is similar

to that of recent papers in the literature. For instance similar

structure for the variance was considered by Xu and Phillips

(2008) or Kim and Park (2010) among others. Our framework encompass

the important case of piecewise constant variance as considered in

Pesaran and Timmerman (2004) or Bai (2000).

Finally it is important to underline that the framework induced by A1 is different from the case of autoregressive processes with conditionally heteroscedastic but (strictly) stationary errors. For instance models like the GARCH or the All-Pass models cannot take into account for non constant unconditional variance in the innovations. The model identification problem for stationary processes which may display nonlinearities has been recently investigated by Boubacar Mainassara (2012) in a quite general framework.

In this part we introduce estimators of the autoregressive parameters. Let us rewrite (2.1) as follow

| (2.2) | |||

where is the vector of the true autoregressive parameters and . For a fitted autoregressive order , the OLS estimator is given by

where

and . If we suppose that the true unconditional covariance matrices are known, we can define the following Generalized Least Squares (GLS) estimator

| (2.3) |

with

Let us define with . Note that maximizes the conditional log-likelihood function (up to a constant and divided by )

| (2.4) |

(see Lütkepohl (2005, p 589)). If we assume that the innovations process variance is constant ( for all ) and unknown, the standard conditional log-likelihood function

| (2.5) |

where is a invertible matrix, is usually used

for the estimation of the parameters.

The estimator obtained by maximizing with

respect to corresponds to .

In this case the estimator of the constant variance is given by where are the residuals of the OLS estimation of (2.2).

In practice the assumption of known variance is unrealistic. Therefore we consider an adaptive estimator of the autoregressive parameters. We may first define adaptive estimators of the true unconditional variances as in Patilea and Ra ssi (2012)

where the weights are given by

with the bandwidth and

where is the kernel function which is such that . The bandwidth is taken in a range with some constants and at a suitable rate. Alternatively one can use different bandwidths cells for the ’s (see Patilea and Ra ssi (2012) for more details). The results in this paper are given uniformly with respect to . This justifies the approach which consists in selecting the bandwidth on a grid defined in a range using for example the cross validation criterion. Note also that the ’s are positive definite. Of course our results do not rely on a particular bandwidth choice procedure and are valid provided estimators of the ’s with similar asymptotic properties of the ’s are available. The non parametric estimator of the covariance matrices employed in this paper is similar to the variance estimators used in Xu and Phillips (2008) among others. Considering the ’s, we are in position to introduce the ALS estimators

with

Now we have to state the asymptotic behavior of the estimators and introduce some notations. Define

and the vector of dimension such that the first component is equal to one and zero elsewhere. Under A1 it is shown in Patilea and Ra ssi (2012) that

| (2.6) |

with

and

| (2.7) |

where

In addition we may use the following consistent estimators for the covariance matrices:

| (2.8) |

We make the following assumptions to state the asymptotic equivalence between the ALS and GLS estimators.

Assumption A1’: Suppose that all the conditions in Assumption A1 hold true. In addition where for any symmetric matrix the real value denotes its smallest eigenvalue.

Assumption A2: (i) The kernel is a bounded density function defined on the real line such that is nondecreasing on and decreasing on and . The function is differentiable except a finite number of points and the derivative is an integrable function. Moreover, the Fourier Transform of satisfies .

(ii) The bandwidth is taken in the range with and as , for some .

(iii) The sequence is such that

Under these additional assumptions Patilea and Ra ssi (2012) also showed that

| (2.9) |

and

| (2.10) |

where and . As a consequence and have the same asymptotic behavior and we can also write , unless at the break dates where we have . Using these asymptotic results we underline the unreliability of the standard and develop a criterion which is adapted to the case of non stationary but stable processes. Corrected confidence bounds for the PAM and PCM in our non standard framework are also proposed.

3 Derivation of the adaptive AIC

In the standard case (the variance of the innovations is constant with true variance ) the Kullback-Leibler discrepancy between the true model and the approximating model with parameter vector is given by

| (3.1) |

see Brockwell and Davis (1991, p 302). Akaike (1973) proposed the following approximately unbiased estimator of (3.1) to compare the discrepancies between competing VAR() models

where the term penalizes the more complicated models fitted to the data (see L tkepohl (2005), p 147). The terms corresponding to the nuisance parameters are neglected in the previous expressions since they do not interfere in the model selection when the is used. The identified model corresponds to the model which minimizes the . However in our non standard framework it is clear that the cannot take into account the non constant variance in the observations. In addition if we assume that the variance of the innovations is constant , we obtain

| (3.2) |

with so that the following result is used for the derivation of the standard

for large , where is a consistent estimator of . In view of (2.6) this property is obviously not verified in our case. Indeed Patilea and Ra ssi (2012) pointed out that and can be quite different. Therefore the standard have no theoretical basis in our non standard framework and we can expect that the use of the standard can be misleading in such a situation.

To remedy to this problem we shall use the more appropriate expression (2.4) in our framework for the Kullback-Leibler discrepancy between the fitted model and the true model

| (3.3) |

Using a second order Taylor expansion of about and since , we obtain

| (3.4) | |||||

Using again the second order Taylor expansion and taking the expectation we also write

| (3.5) | |||||

From (2.7) we have for large

and

Noting that

and using (3.4) and (3.5), we see that the following criterion based on the GLS estimator

is an approximately unbiased estimator of .

Nevertheless the is infeasible since it depends on the unknown variance of the errors. Thereby we will use the adaptive estimation of the variance structure to propose a feasible selection criterion. Recall that

and define

since we allowed for a finite number of variance breaks for the innovations. Therefore we can introduce the adaptive criterion

which gives an approximately unbiased estimation of (3.3) for large .

Finally note that if we suppose that is cointegrated, Kim and Park (2010) showed that the long run relationships estimated by reduced rank are -consistent. Therefore our approach for building information criteria can be straightforwardly extended to the cointegrated case since it is clear that the estimated long run relationships can be replaced by the true relationships in the preceding computations.

4 Identifying the lag length using partial autoregressive and partial correlation matrices

In this part we assume , so that the cut-off property of the presented tools can be observed. Following the approach described in Reinsel (1993) chapter 3, one can use the estimators of the autoregressive parameters to identify the lag length of (2.1). Consider the regression of on its past values

| (4.1) |

We can remark that the partial autoregressive matrices are equal to zero. The PAM are estimated using OLS or ALS estimation. Confidence bounds for the PAM can be proposed as follow. Let us introduce the dimensional matrix , so that from (2.6), (2.7) and (2.9) we write

| (4.2) |

where and correspond to

the OLS and ALS estimators of the null matrices

. Denote by (resp.

) the asymptotic standard deviation of the th

component of (resp. ) for

with obvious notations. From

(4.2) the -th component of

(resp. ) are usually compared with the 95%

approximate asymptotic confidence bounds

(resp.

) as suggested in Tiao and Box

(1981),

and where the ’s and ’s

can be obtained using the consistent estimators in (2.8).

Therefore the identified lag length for model (2.1) correspond

to the higher order of the matrix

which have an estimator of a component which is clearly beyond its confidence bounds about zero.

The identification of the lag length of standard VAR processes is usually performed using also the partial cross-correlation matrices which are the extension of the partial correlations of the univariate case. Consider the regressions

with . In our framework it is clear that the error process is unconditionally heteroscedastic, and then we define which converge under A1, and the consistent estimator of :

with obvious notations. The consistency of this estimator can be proved from standard computations and using lemmas 7.1-7.4 of Patilea and Ra ssi (2012). We also define the ’long-run’ innovations variance where the ’s are non constant and the consistent estimator of where we recall that the ’s are the OLS residuals.

Several definitions for the partial cross-correlations are available in the literature. In the sequel we concentrate on the definition given in Ansley and Newbold (1979) which is used in the VARMAX procedure of the software SAS. We propose to extend the partial cross-correlation matrices in our framework as follow

| (4.3) |

and it is clear that for we have . The expression (4.3) may be viewed as the ’long-run’ relation between the ’s and the ’s corrected for the intermediate values for each date . Consider the OLS and ALS consistent estimators

where is of dimension , so that and correspond to the ALS and OLS estimators of in (4.1). Using again (2.6), (2.7), (2.9) and from the consistency of and we obtain

| (4.4) |

| (4.5) |

Hence approximate confidence bounds can be built using (4.4)

and (4.5). Similarly to the partial autoregressive matrices

the highest order for which a cut-off is observed for an element

of ( resp. ) correspond to the

identified lag length for the VAR model. Note that for

(, so that the observed process is uncorrelated and

, ), we have

.

In this case similar results to (4.4) and (4.5) can be used.

Let us end this section with some remarks on the OLS and ALS estimation approaches of the PAM and PCM. If we assume that the variance of the error process is constant, the result (3.2) is used to identify the autoregressive order using the partial autoregressive and correlation matrices obtained from the OLS estimation. However as pointed out in the previous section this standard result can be misleading in our framework. The simulations carried out in the next section show that the standard bounds are not reliable in our framework. From the real example below it appears that the OLS PAM and PCM with the standard confidence bounds seem to select a too large lag length. Note that since the tools presented in this section are based on the results (2.6), (2.7) and on the adaptive estimation of the autoregressive parameters, they are able to take into account changes in the variance.

In the univariate case the partial autocorrelation function is used for identifying the autoregressive order. In such a case the asymptotic behavior of does not depend on the variance structure (see equation (4.6) below). Hence the ALS estimators of the partial autocorrelations do not depend on the variance function on the contrary to its OLS counterparts. In the general VAR case Patilea and Ra ssi (2012) also showed that that is positive semi-definite (the same result is available in the univariate case). Therefore the tools based on the ALS estimator are more accurate than the tools based on the OLS estimator for identifying the autoregressive order.

We illustrate the above remarks by considering the following simple case where we assume that with a real-valued function. The univariate stable autoregressive processes are a particular case of this specification of the variance. In this case we obtain

| (4.6) |

and

so that we have

| (4.7) |

with . Hence from (4.7) it is clear that the adaptive PAM and PCM are more reliable than the PAM and PCM obtained using the OLS approach. In addition from (4.6) the asymptotic behavior of the adaptive partial autoregressive and partial correlation matrices does not depend on the variance function. On the other hand we also see from (4.7) that the matrices and can be quite different.

5 Empirical results

For our empirical study the is computed using an adaptive estimation of the variance as described in Section 2. The ALS estimators of the PAM and PCM are obtained similarly. In particular the bandwidth is selected using the cross-validation method. The OLS partial autoregressive and partial correlation matrices used with the standard confidence bounds are denoted by and . Similarly we also introduce the , and the , with obvious notations. In the simulation study part the infeasible and tools are used only for comparison with the feasible tools.

It is important to note that when the and are used, the practitioners base their decision on the visual inspection of these tools. Results concerning automatically selected lag lengths over the iterations using several and do not really reflect their ability to identify the lag length in practice. For instance it is well known that there are cases where some or are beyond the confidence bounds but not taken into account for the lag length identification. Therefore we provide instead some simulation results which assess the ability of the studied methods to provide reliable confidence bounds for the choice of the lag length. The use of the modified and is also illustrated in the real data study below.

For a given tool we assume in our experiments that when the selected autoregressive order is such that , the model identification is suspected to be not reliable. For instance the more complicated models may appear not enough penalized by the information criterion, or the number of estimated parameters becomes too large when compared to the number of observations. In such situations the practitioner is likely to stop the procedure.

5.1 Monte Carlo experiments

In this part independent trajectories of bivariate VAR(2) () processes of length , and are simulated with autoregressive parameters given by

| (5.1) |

Recall that the process is assumed iid standard Gaussian. Two kinds of non constant volatilities are used. When the variance smoothly change in time we consider the following specification

| (5.2) |

In case of abrupt change the following variance specification is used

| (5.3) |

with . In this case we have a common variance break at the date . In all the experiments we take , and . Note that the autoregressive parameters as well as the variance structure are inspired by the real data study below. More precisely the autoregressive parameters in (5.1) are taken close to the two first adaptive PAM obtained for the government securities and foreign direct investment system. In addition the ratio between the first and last adaptive estimation of the residual variance of the studied real data are of the same order of the ratio for the residual variance of the simulated series. The results are given in Tables 1-3 and 7-9 for the variance specification (5.2) and in Tables 4-6 and 10-12 when specification (5.3) is used. To facilitate the comparison of the studied identification tools, the most frequently selected lag length for the studied information criteria and the correct order () are in bold type.

The small sample properties of the different information criteria for selecting the autoregressive order is first analyzed. According to Tables 1-6 we can remark that the and are selecting most frequently the true autoregressive order. However we note that the modified have a slight tendency to select . On the other hand we can see that the classical selects too large lags lengths in our framework. This is in accordance with the fact that is not consistent (see e.g. Paulsen (1984) or Hurvich and Tsai (1989)). We also note that the frequency of selected true lag length increase with for the and . The infeasible provide slightly better results than the . As expected it can be seen that the difference between the and seems more marked when the processes display an abrupt variance change. Indeed note that from (2.10) the variance is not consistently estimated at the break dates. Nevertheless such bias is divided by , and we note that the behavior of the and become similar as the samples increase in all the studied cases. According to our simulation results it appears that the adaptive is more able to select the appropriate autoregressive order than the standard when the underlying process is indeed a VAR process.

Now we turn to the analysis of the results for the PAM and PCM in Tables 7-12. Note that we used the 5% (asymptotic) confidence bounds in our study. From our results it emerges that the standard bounds do not provide reliable tools for the identification of the lag length when the variance is non constant. It can be seen that the frequencies of PAM and PCM with lag greater than beyond the standard bounds do not converge to 5%. On the other hand it is found that the PAM and PCM based on the OLS and adaptive approaches give satisfactory results. Indeed the frequencies of PAM and PCM with lag greater than beyond the standard and adaptive bounds converge to 5%. As above we can remark that the results when the variance is smooth are better than the case where the variance exihibits an abrupt break. When the PAM and PCM are equal to zero it seems that the adaptive and OLS method give similar results. In accordance with the theoretical the more accurate adaptive method is more able than the OLS method to detect the significant PAM and PCM with lag smaller or equal to . We can draw the conclusion that the standard bounds have to be avoided in our non standard framework. The modified adaptive and OLS methods give reliable approaches for identifying the lag length of a VAR model with non constant variance. It emerges that the more elaborated adaptive approach is preferable.

5.2 Real data study

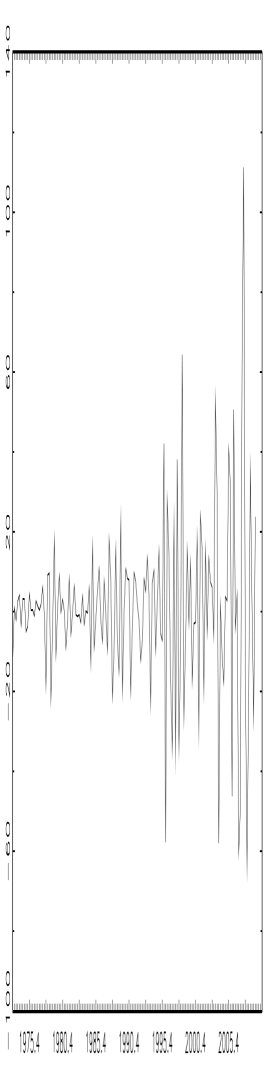

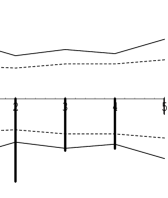

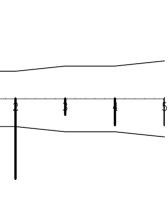

In this part we try to identify the VAR order of a bivariate system of variables taken from US international finance data. The first differences of the quarterly US Government Securities (GS hereafter) hold by foreigners and the Foreign Direct Investment (FDI hereafter) in the US in billions dollars are studied from January 1, 1973 to October 1, 2009. The length of the series is . The studied series are plotted in Figure 1 and can be downloaded from website of the research division of the federal reserve bank of Saint Louis: www.research.stlouisfed.org.

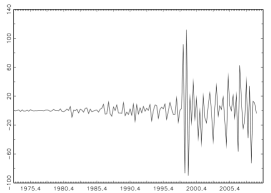

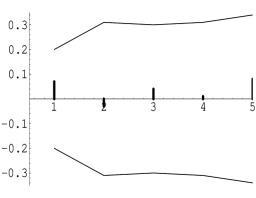

We first highlight some features of the studied series. The OLS residuals and the variances of the errors estimated by kernel smoothing are plotted in Figure 2. From Figure 1 it appears that the data do not have a random walk behavior, while from Figure 2 the estimated volatilities seem not constant. The residuals plotted in Figure 2 show that the variance of the first component of the residuals seems constant from January 1973 to October 1995 and then we may suspect an abrupt variance change. Similarly the variance of the second component of the residuals seems constant from January 1973 to July 1998 and then we remark an abrupt variance change. Therefore it clearly appears that the standard homoscedasticity assumption turns out to be not realistic for the studied series.

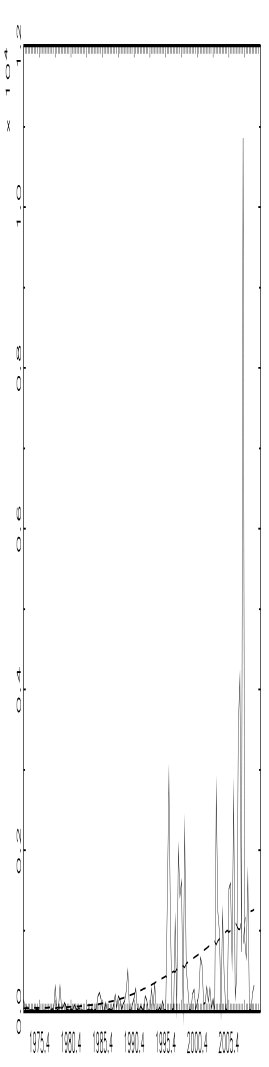

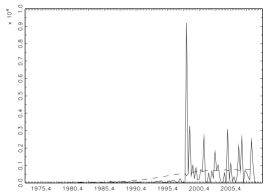

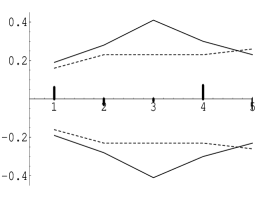

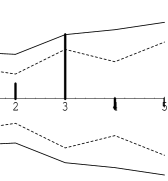

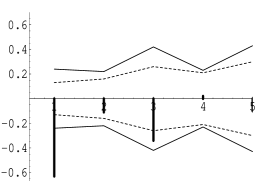

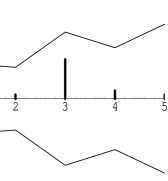

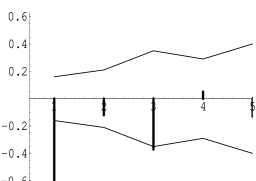

We fitted VAR() models with to the data and computed the and for each . In our VAR system the first component corresponds to the GS and the second corresponds to the FDI. From Table 13 the is decreasing as is increased so that the higher autoregressive order is selected, while the minimum value for the is attained for . If it is assumed that the studied processes follow a VAR model and since we noted that the variance of the studied processes seems non constant, it is likely that the is not reliable and selects a too large autoregressive order. In view of our above results the model identification with the more parsimonious seems more reliable. We also considered the obtained from the standard, OLS and ALS estimation methods. The are plotted in Figures 3 and 4 and it appear that we can identify using the modified tools while could be identified using the standard . We also see that the standard and OLS confidence bounds can be quite different. The PAM are given below with the 95% confidence bounds into brackets. We base our lag length choice on the which are clearly greater than its 95% confidence bounds (in bold type). The give for the studied data:

We obtain the following

and the following

It can be seen that the and in the and for and seem not significant, so that one can identify using our modified tools. The cut-off at is clearly marked for the and . If the are used we note that one could select again or even , and we note that the cut-off is not so clearly marked in this case. We also see that the 95% standard and OLS confidence bounds can be quite different. If the length was automatically selected using the and , larger lag lengths would have been chosen. Indeed we note that some of the and are only slightly beyond the 95% confidence bounds (see for instance the , or in Figures 3 and 4).

In general it emerges from our empirical study part that the standard identification tools lead to select large lag lengths for the VAR models with non constant variance. This may be viewed as a consequence to the fact that the standard tools are not adapted to our non standard framework. Note that the identification of the model is the first step of the VAR modeling of time series. In such situation the practitioner is likely to adjust a VAR model with a too large number of parameters which can affect the analysis of the series. The identification tools developed in this paper take into account for unconditional heteroscedasticity. From our real data study we found that the modified tools are more parsimonious.

References

-

Ahmed, S., Levin, A., and Wilson, B.A. (2002) "Recent US macroeconomic stability: Good luck, good policies, or good practices?" International Finance Discussion Papers, The board of governors of the federal reserve system, 2002-730.

-

Akaike , H. (1973) Information theory and an extension of the maximum likelihood principle, in: B.N. Petrov and F. Csaki, eds., 2nd International Symposium on Information Theory, pp. 267-281. Akademia Kiado, Budapest.

-

Ansley, C.F., and Newbold, P. (1979) Multivariate partial autocorrelations. ASA Proceedings of the Business and Economic Statistics Section, 349-353.

-

Aue, A., Hörmann, S., Horvàth, L., and Reimherr, M. (2009) Break detection in the covariance structure of multivariate time series models. Annals of Statistics 37, 4046-4087.

-

Bai, J. (2000) Vector autoregressive models with structural changes in regression coefficients and in variance-covariance matrices. Annals of Economics and Finance 1, 303-339.

-

Boubacar Mainassara, Y. (2012) Selection of weak VARMA models by Akaike’s information criteria. Journal of Time Series Analysis 33, 121-130.

-

Brockwell, P.J., and Davis, R.A. (1991) Time Series: Theory and methods. Springer, New York.

-

Cavanaugh, J.E. (1997) Unifying the derivations for the Akaike and corrected Akaike information criteria. Statistics and Probability Letters 33, 201-208.

-

Dahlhaus, R. (1997) Fitting time series models to nonstationary processes. Annals of Statistics 25, 1-37.

-

Dahlhaus, R., and Subba Rao, S. (2006) Statistical inference for time-varying ARCH processes. Annals of Statistics 34, 1075-1114.

-

Davis, S.J. and Kahn, J.A. (2008) Interpreting the great moderation: Changes in the volatility of economic activity at the macro and micro levels. Journal of Economic Perspectives 22, 155-180.

-

Engle, R.F., and Rangel, J.G. (2008) The spline GARCH model for low-frequency volatility and its global macroeconomic causes. Working paper, Czech National Bank.

-

Francq, C., and Gautier, A. (2004) Large sample properties of parameter least squares estimates for time-varying ARMA models. Journal of Time Series Analysis 25, 765-783.

-

Galeano, P., and Pena, D. (2007) Covariance changes detection in multivariate time series. Journal of Statistical Planning and Inference 137, 194-211.

-

Hannan, E.J., and Quinn, B.G. (1979) The determination of the order of an autoregression. Journal of the Royal Statistical Society B 41, 190-195.

-

Herrera, A.M., and Pesavento, E. (2005) The decline in the US output volatility: Structural changes and inventory investment. Journal of Business and Economic Statistics 23, 462-472.

-

Horvàth, L., Kokoszka, P. and Zhang, A. (2006) Monitoring constancy of variance in conditionally heteroskedastic time series. Econometric Theory 22, 373-402.

-

Horvàth, L., and Steinebach, J. (2000) Testing for changes in the mean or variance of a stochastic process under weak invariance. Journal of Statistical Planning and Inference 91, 365-376.

-

Hurvich, C.M., and Tsai, C.-L. (1989) Regression and time series model selection in small samples. Biometrika 76, 297-307.

-

Kim, C.S., and Park, J.Y. (2010) Cointegrating regressions with time heterogeneity. Econometric Reviews 29, 397-438.

-

Kim, C.J., and Nelson, C.R. (1999) Has the U.S. economy become more stable? A bayesian approach based on a Markov-switching model of the business cycle. The Review of Economics and Statistics 81, 608-616.

-

Kokoszka, P., and Leipus, R. (2000) Change-point estimation in ARCH models. Bernoulli 6, 513-539.

-

L tkepohl, H. (2005) New Introduction to Multiple Time Series Analysis. Springer, Berlin.

-

McConnell, M.M., Mosser P.C. and Perez-Quiros, G. (1999) A decomposition of the increased stability of GDP growth. Current Issues in Economics and Finance, Federal Reserve Bank of New York.

-

Mikosch, T., and Stărică, C. (2004) Nonstationarities in financial time series, the long- range dependence, and the IGARCH effects. Review of Economics and Statistics 86, 378-390.

-

Patilea, V., and Ra ssi, H. (2012) Adaptive estimation of vector autoregressive models with time-varying variance: application to testing linear causality in mean. Journal of Statistical Planning and Inference 142, 2891-2912.

-

Patilea, V., and Ra ssi, H. (2011) Corrected portmanteau tests for VAR models with time-varying variance. Working paper, Universit europ enne de Bretagne IRMAR-INSA.

-

Paulsen, J. (1984) Order determination of multivariate autoregressive time series with unit roots, Journal of Time Series Analysis 5, 115-127.

-

Pesaran, H., and Timmerman, A. (2004) How costly is it to ignore breaks when forecasting the direction of a time series. International Journal of Forecasting 20, 411-425.

-

Qu, Z., and Perron, P. (2007) Estimating and testing structural changes in multivariate regressions. Econometrica 75, 459-502.

-

Reinsel, G.C. (1993) Elements of Multivariate Time Series Analysis. Springer, New-York.

-

Sanso, A., Aragó, V., and Carrion, J.L. (2004). Testing for changes in the unconditional variance of financial time series. Revista de Economia Financiera 4, 32-53.

-

Sensier, M., and van Dijk, D. (2004) Testing for volatility changes in U.S. macroeconomic time series. Review of Economics and Statistics 86, 833-839.

-

Stărică, C. (2003) Is GARCH(1,1) as good a model as the Nobel prize accolades would imply?. Working paper, http://129.3.20.41/eps/em/papers/0411/0411015.pdf.

-

Stock, J.H., and Watson, M.W. (2002) "Has the business cycle changed and why?", NBER Macroannual 2002, M. Gertler and K. Rogoff eds., MIT Press.

-

Tiao, G.C., and Box, G.E.P. (1981) Modeling multiple times series with applications. Journal of the American Statistical Association 76, 802-816.

-

Xu, K.L., and Phillips, P.C.B. (2008) Adaptive estimation of autoregressive models with time-varying variances. Journal of Econometrics 142, 265-280.

Appendix: Tables and Figures

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 1.5 | 0.2 | 0.1 | 0.1 | 98.1 | |

| 8.0 | 58.4 | 15.6 | 9.0 | 9.0 | |

| 7.2 | 84.0 | 6.4 | 1.8 | 0.6 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | |

| 2.4 | 78.1 | 11.9 | 5.5 | 2.1 | |

| 0.2 | 86.6 | 9.8 | 2.4 | 1.0 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | |

| 1.6 | 84.1 | 9.3 | 3.8 | 1.2 | |

| 0.0 | 89.1 | 6.6 | 3.8 | 0.5 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 3.3 | 0.2 | 0.4 | 0.7 | 95.4 | |

| 19.2 | 44.7 | 16.6 | 11.3 | 8.2 | |

| 7.5 | 79.8 | 8.3 | 3.0 | 1.4 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 0.4 | 0.1 | 0.0 | 0.0 | 99.5 | |

| 19.3 | 63.7 | 11.2 | 4.3 | 1.5 | |

| 0.3 | 84.6 | 9.9 | 3.5 | 1.7 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | |

| 3.9 | 77.3 | 11.1 | 5.6 | 2.1 | |

| 0.0 | 86.5 | 8.2 | 4.3 | 1.0 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 72.4 | 93.6 | 11.4 | 11.3 | 12.8 | |

| 69.0 | 91.9 | 9.6 | 10.7 | 11.6 | |

| 69.8 | 92.8 | 10.1 | 9.9 | 10.7 | |

| 64.3 | 89.9 | 5.1 | 5.1 | 4.6 | |

| 39.1 | 94.0 | 10.6 | 10.0 | 12.6 | |

| 35.9 | 92.6 | 9.2 | 10.2 | 11.8 | |

| 34.4 | 94.1 | 8.2 | 8.9 | 11.2 | |

| 55.5 | 94.3 | 4.4 | 4.7 | 5.3 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 94.5 | 100.0 | 9.3 | 9.2 | 7.6 | |

| 93.3 | 100.0 | 7.5 | 7.5 | 6.0 | |

| 94.6 | 100.0 | 7.6 | 7.7 | 5.0 | |

| 93.4 | 99.9 | 4.8 | 5.6 | 3.6 | |

| 81.7 | 99.9 | 8.7 | 9.1 | 8.1 | |

| 74.4 | 100.0 | 6.7 | 7.4 | 6.6 | |

| 79.5 | 100.0 | 6.7 | 6.5 | 5.6 | |

| 93.6 | 100.0 | 4.8 | 5.2 | 4.2 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 99.9 | 100.0 | 10.1 | 10.1 | 8.7 | |

| 99.8 | 100.0 | 6.2 | 7.7 | 5.6 | |

| 100.0 | 100.0 | 6.3 | 6.3 | 5.8 | |

| 99.9 | 100.0 | 6.1 | 5.0 | 5.4 | |

| 99.4 | 100.0 | 8.1 | 8.5 | 8.5 | |

| 98.4 | 100.0 | 5.4 | 6.0 | 6.1 | |

| 99.6 | 100.0 | 5.2 | 6.6 | 6.2 | |

| 100.0 | 100.0 | 4.8 | 5.6 | 5.9 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 66.4 | 89.2 | 16.9 | 18.4 | 19.0 | |

| 58.4 | 84.1 | 10.8 | 15.4 | 14.3 | |

| 63.0 | 88.6 | 11.4 | 11.1 | 12.3 | |

| 56.9 | 85.9 | 15.1 | 8.5 | 7.4 | |

| 38.2 | 90.3 | 17.1 | 17.3 | 19.9 | |

| 22.9 | 85.5 | 10.7 | 13.5 | 13.6 | |

| 27.4 | 89.3 | 10.0 | 10.4 | 13.0 | |

| 51.6 | 92.9 | 13.4 | 10.4 | 6.9 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 91.4 | 99.6 | 16.3 | 16.1 | 15.5 | |

| 83.9 | 98.5 | 8.7 | 9.5 | 8.2 | |

| 89.7 | 99.6 | 7.9 | 8.7 | 6.9 | |

| 90.6 | 99.8 | 11.8 | 8.8 | 6.0 | |

| 76.7 | 99.7 | 14.5 | 15.5 | 14.2 | |

| 52.3 | 99.1 | 8.0 | 8.6 | 8.6 | |

| 66.1 | 99.8 | 7.9 | 7.9 | 7.2 | |

| 92.4 | 100.0 | 10.4 | 9.4 | 6.2 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 99.4 | 100.0 | 16.5 | 16.3 | 16.1 | |

| 97.9 | 100.0 | 6.1 | 7.1 | 5.9 | |

| 99.9 | 100.0 | 8.8 | 7.7 | 5.9 | |

| 99.8 | 100.0 | 10.9 | 9.5 | 7.3 | |

| 98.2 | 100.0 | 14.9 | 14.8 | 15.4 | |

| 90.2 | 100.0 | 5.8 | 7.2 | 5.9 | |

| 98.6 | 100.0 | 6.9 | 6.6 | 6.3 | |

| 100.0 | 100.0 | 8.4 | 7.8 | 7.4 |

| 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|

| 13.91 | 13.73 | 13.59 | 13.53 | 13.52 | |

| 11.80 | 11.61 | 11.74 | 11.77 | 11.80 |