The CUSUM test for detecting structural changes in strong mixing processes

Fatemeh Azizzadeh, S.

Rezakhah

School of Mathematics and Computer Science,

Amirkabir University of Technology, Tehran, IranFaculty of Mathematics and Computer Science,

Amirkabir University of Technology, Tehran, Iran.

Email: rezakhah@aut.ac.ir, fatemeh_aziz@aut.ac.irF. Azizzadeh, S. Rezakhah

Faculty

of Mathematics and Computer Science, Amirkabir University of

Technology, Tehran, Iran. Email: rezakhah@aut.ac.ir, fatemeh_aziz@aut.ac.ir

The CUSUM test for detecting structural changes in strong mixing processes

Fatemeh Azizzadeh, S.

Rezakhah

School of Mathematics and Computer Science,

Amirkabir University of Technology, Tehran, IranFaculty of Mathematics and Computer Science,

Amirkabir University of Technology, Tehran, Iran.

Email: rezakhah@aut.ac.ir, fatemeh_aziz@aut.ac.irF. Azizzadeh, S. Rezakhah

Faculty

of Mathematics and Computer Science, Amirkabir University of

Technology, Tehran, Iran. Email: rezakhah@aut.ac.ir, fatemeh_aziz@aut.ac.ir

Abstract

Strong mixing property holds for a broad class of linear and nonlinear

time series models such as ARMA and GARCH models.

In this article we study correlation structure of

strong mixing sequences, and some asymptotic properties are presented.

We also present a new method for detecting change point in correlation structure of strong mixing sequences, and

present a nonparametric CUSUM test statistic for this. Asymptotic

consistency of this test statistics is shown. This method is applied to simulated data

of some linear and nonlinear models and power of the test

is evaluated. For linear models, it is shown that

this method have a better performance in compare to Berkes et al.(2009).

MSC: Primary 62M10, 60F17, Secondary 62G20, 62G10.

Key words and Phrases: structural changes, Strong mixing,

Functional central limit theorem, CUSUM test, Brownian bridge.

1 Introduction

Change point detection in a sequence of random

variables was first proposed by Page(1954).

This study started by detecting changes in

the mean of a sequence of independent random variables and then

extended to dependent sequences. Change point detection is widely

used in various fields such as quality control, economics,

finance and medicine. Review

of earlier works can be found in Csörgö and

Horváth(1988), Brodsky and Darkhovsky (1993) and

Csörgö and Horváth(1997).

Among different methods for change point detection,

the CUSUM test proposed by Page(1954), for mean change detection,

is widely used for its simplicity.

Inclán and Tiao(1994) proposed a CUSUM of squares test for testing a variance change in i.i.d. normal random variables.

Lee and Park(2001) extended the CUSUM test of squares test of Inclán and

Tiao(1994) for linear processes. Lee et al.(2003) studied

change of parameters in a random coefficient AR(1)

model, thus detecting changes in the auto-covariances of a linear

process

Galeano and Pena(2007) studied changes in variance and correlation

structure of the multivariate time series. Zhou and Liu(2009) used

a weighted CUSUM statistic for mean change detection in infinite variance AR(p)

process. Berkes et al.(2009) considered a CUSUM test to detect changes

in the mean and in the covariance structure of a linear process.

Recently Qin et al.(2010) studied mean change detection in -mixing

processes.

In this article we study change in the correlation structure of strong

mixing sequences. Let be a stationary process.

As a measure of dependence we use Rosenblatt’s -mixing

coefficient as

where A and B are in the -fields

and

respectively.

The sequence is said to be -mixing or strong

mixing (SM) if

Strong mixing processes are asymptotically independent.

Strong mixing property holds for a large class of linear

and nonlinear stationary time series such as ARMA and GARCH models,

m-dependent processes, broad class of

Gaussian processes and ergodic Markov processes( Bosq 1996, and Bradley 2005).

Ibragimov(1962) showed some results for stationary strong

mixing sequences and proved central limit theorem for strict stationary

SM processes. Davydov(1968) obtained some

moment inequalities and Rio(1993) presented some covariance

inequalities and bounds on the variance of partial sums of

SM processes. Herrndorf(1985), Doukhan et al.(1994), and

Merlevede and Peligard(2000) studied functional central

limit theorem on SM processes. Romano

and Thombs(1996) used central limit theorem, established by

Ibragimov(1962), to show that sample auto-covariances of strictly

stationary SM sequences converge in distribution to normal

distribution.

By using functional central limit theorem for SM

sequences, we propose a new test statistic for detecting

changes in correlation structure of stationary strong

mixing processes.

This test is a nonparametric one and does not depend on any

assumptions about the underlying distribution or model.

The rest of this paper is organized as follows:

In section 2 a nonparametric test statistic for detection of change points, in broad class of linear and non linear process, is constructed

and its asymptotic properties, under no change null hypothesis, are studied.

Also the consistency of this test statistic is shown

in section 2. Section 3 is devoted to the simulation results on

different linear and nonlinear models. In this section

the method of Berkes et al.(2009) has been compared

with the method of this paper for some some linear models.

By simulation we show that this test statistic have

a better performance and is more powerful in many cases.

2 Main results

In this section we present some preliminary results which will be used later in this paper.

We present functional central limit

theorem for sample auto-covariances of SM processes. We also introduce

a new test statistic for detecting changes in the correlation

structure of stationary SM processes,

which we call CUSUM strong mixing(CSSM).

Finally we show consistency and

asymptotic convergence of this empirical CSSM test statistic.

Let be a sequence of random variables on some

probability space , satisfying

Let for .

Consider the Skorokhod space of all functions on

which are right continuous with left limit. Let

to be a random function as

If is weakly convergent to a standard Brownian motion ,

then is said to satisfy the functional central limit

theorem or strong invariance principle (Billingsley, 1999).

Herrndorf(1985) proved functional central limit theorem for strong

mixing sequences without stationarity assumption but

assumed convergence of the variance of partial sums.

For as a sequence of zero-mean stationary process

the sample auto-covariances

, , are defined as:

Asymptotic covariance of sample autocovariances is known as

Bartlett’s estimator and is defined as:

Let

where

is the covariance matrix whose entries are defined by (2.3). Now we have the following result.

Theorem 1: Let be a stationary

strong mixing process which satisfies:

•

i)

•

ii)

, for some

in which is the mixing coefficient, defined by (1.2). Then

where denotes convergence in distribution,

are independent Brownian bridge, for .

Before proceeding to the proof of this theorem we present some lemmas,

which are necessary for our proof.

Lemma 1: (Davydov, 1968) Let the process

be strong mixing, and random variables

and be measurable with respect to

and ,

introduced by (1.1), respectively.

Moreover if the moments and

exist for where , then

Lemma 2: Let be a

zero-mean strong mixing process, where

Then is convergent.

Proof of Lemma 2: By lemma 1,

Let , then

An alternative proof for lemma 2 can be found in Rio (1993).

Proof of Theorem 1:

Let

where is auto-covariance function of

.

By (2.4) and (2.6), it is immediate that

Any Brownian bridge has the same distribution as ,

where is a standard Brownian motion (Billingsley, 1999).

Therefore if ,

where are independent Brownian motions for ,

then . So it is enough to show that converges

to a vector of Brownian motions.

As

so by assuming

we have that

By (2.7),

and

So relation (1.1) implies that, .

Hence form a zero mean, strong

mixing process, where by assumption (ii),

Also by (2.7) and assumption (i),

for some . Let .

Using (2.9) and (2.10), lemma 2

implies that ,

for some .

If , then (2.9), (2.10), and functional

central limit theorem, introduced by Herrndorf(1985), assert that

For ,

By Bartlett’s formula (2.3),

.

So

Hence by (2.11) and (2.12),

where , are independent Brownian motions.

The second part on right hand of (2.8) tends to zero as

, so (2.13) implies that

where , are independent Brownian motions.

2.1 CUSUM test statistic

Using theorem 1 and (2.4), a CUSUM test statistic is

constructed as:

By continuous mapping theorem

For detecting changes in time series , under the assumptions

of theorem 1, the following test is proposed for testing hypothesis

: no change occur in the auto-covariance function of

: there is a such that auto-covariance function of

is different from auto-covariance function of

The strategy of this test is to reject when is large.

By (2.14) and (2.15), the critical region of the test

at significant level is , where is the -quantile

point of the distribution of .

The critical values can be found in Kiefer(1959) and Lee et al.(2003).

Example:

Let be an MA(1) process as:

where is an iid normal sequence with mean zero

and variance . In linear processes where ,

Bartlett’s formula has explicit form as:

where is the corresponding autocovariance function at lag

of , see Brockwell and Davis(1991).

If the noise is Gaussian, , so

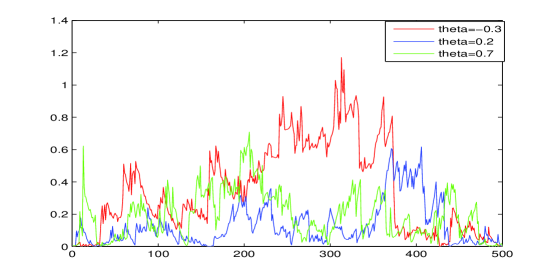

Figure 1: behavior of for different values of parameter in MA(1) model

Let , therefore corresponding covariance matrix

can be written as

By (2.4), for we have that

and by (2.15)

Figure 1 shows the behavior of test statistic

for different values of parameter in an MA(1) process without

change point. For , at significant level , the

critical value is .

2.2 Consistent estimation of covariance matrix

In this section we evaluate asymptotic behavior of the covariance

function of estimators , defined by (2.3).

Bartlett(1946) derived an explicit formula for the asymptotic

behavior of covariance function of sample autocovariances,

when there exist a linear model for the data(Priestley, 1981).

We present a consistent estimator for the case that

there is no model for data, or we have nonlinear process.

Using (2.3), Bartlett’s estimator can be written as:

For stationary process , let

and .

By theorem 3 it is shown that has

the same asymptotic behavior as .

For the evaluation of ,

one can easily verify that

By replacing with and with in last summation we have

where

and for

in which and

.

Let

where

and is a sequence of positive integers that

Now we have the following result.

Theorem 2: Under the assumptions of theorem 1, if for some then

Proof : The proof is organized in three

steps:

Step 1:

.

By lemma 1 and (2.19),

So for , by assumption (ii) of theorem 1,

and

Step 2:

is of order .

For , by (2.19) and (2.22)

where , and . As by the assumption of the theorem

, so by lemma 2

and . Similarly . Also

Also by lemma 2,

and

Thus by relations (2.25), (2.26) and (2.27) we have that .

By similar method, one can easily verify that

. Therefore,

Step 3: Steps 1 and 2 are applied to prove the main result.

By Minkowski inequality we have

So by (2.23) and (2.28)

As , (2.24) implies that

Finally by (2.30) and (2.31), we arrive at the assertion of the theorem.

Theorem 3: Under the assumptions of theorem 2,

we have that

.

Proof : As

so by theorem 2 the second part on the right tends to zero, and for the first part,

by (2.2) and (2.16)

Corollary 1: Under the assumptions of theorem 2,

by choosing , where

defined by (2.20),

is a consistent estimator of covariance matrix in relation

(2.4).

Corollary 2: Under the assumptions of theorem 2,

by (2.4), (2.14), (2.15), and corollary 1, we have

where

in which , and

is defined by (2.20).

3 Simulation results

In this section, we investigate the performance of the proposed

test statistic , by a simulation study.

As this test statistic is to be applied for linear and nonlinear models,

we consider simulations of such classes of time series.

Test statistics are evaluated by using

relations (2.32) and (2.33) with and relation (2.20) with .

For creating change in the covariance structure of time series,

the parameters are changed at the midpoint of the series.

Empirical powers are evaluated, and for the case that there is

no change in data, probability of type error is reported.

The critical value of the test statistic at level

is (Lee at el. 2003).

Simulations are repeated 1000 times, for the following linear and nonlinear models, to

evaluated empirical powers.

Linear models:

•

Model 1:

ARMA(1,1): ,

•

Model 2:

MA(2): ,

where is a sequence of iid normal

random variables with mean zero and variance 1.

Table 1: Empirical power of for ARMA(1,1), where the initial parameter .

0.2

0.4

0.5

0.6

0.1

0.408

0.761

0.935

0.3

0.295

0.874

0.968

0.989

0.5

0.734

0.977

0.994

0.998

0.7

0.935

0.995

0.999

1.000

Table 1 reports results of the test for simulated data

from ARMA(1,1), where 250 samples are generated with , and then 250 more samples

for different values of

as reported in the table. In table 1, empirical powers are evaluated

for cases where one or both parameters have changed.

In all cases high empirical powers shows ability of this test

statistic. The value pointed by ∗ is type error, empirical level,

which is slightly below .

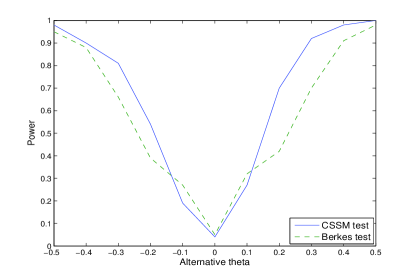

Figure 2: Empirical power of CSSM in comparison with Berkes et al.(2009)

in MA(2) model, .

parameter changes from 0 to alternative .

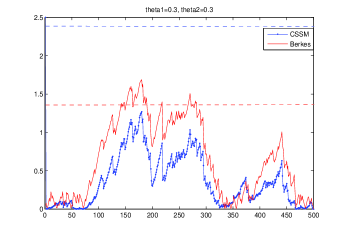

Figure 3: Behavior of CSSM and Berkes statistic in simulated samples from MA(2) model,

without change point.

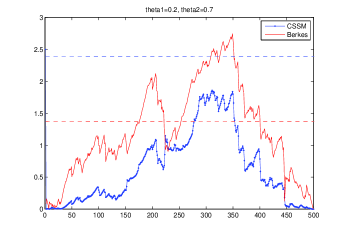

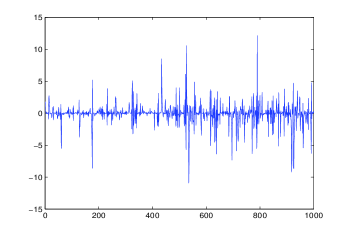

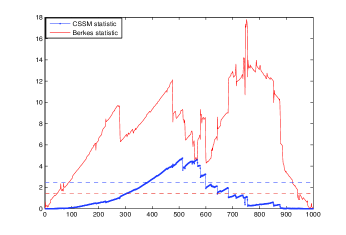

Figure 4: Simulated samples from 2-dependent model with a change point in , variance

of change from 1 to 1.26(left), Corresponding test statistics(right).

As a comparison of CSSM with the Berkes method for linear models, mode 2

with is considered and

250 samples are generated with at first stage

and then 250 more samples for some alternative ,

and empirical powers are plotted in figure 2.

As empirical powers show, CSSM test has a

better performance, with smaller type error.

To visualize this, we follow a simulation of model 2, where there is no change in

time series data. So we generate 500 samples from MA(2) with

once and again with . Then we evaluate CSSM and Berkes

test statistics, and plot them with corresponding critical values, 2.408 and 1.36

in figure 3. As figure 3 shows Berkes method indicate a change point by mistake

where CSSM statistic is far beyond such miss detection.

Nonlinear models:

As nonlinear models, we consider followings:

•

Model 3:

2-dependent:

•

Model 4:

GARCH(1,1): where

in which is a sequence of iid normal

random variables with mean zero and variance one, .

Figure 4(left) shows 1000 generated samples of a 2-dependent

process, model 3, with a change point at , where variance

of changes from 1 to 1.26. Figure 4(right) shows the

behavior of CSSM and Berkes test statistics.

Corresponding critical values are 2.408 and

1.36 respectively which are presented by horizontal lines.

Figure 4(right) shows that the supremums of both

statistics exceed corresponding critical values and a change in process is detected, but CSSM statistics is more precise, as

CSSM detects the change at t=512 and Berkes statistic

detects it at t=750.

Table 2 reports the empirical power of the CSSM,

for 2-dependent model, model 3.

In table 2(a) change of the variance of , from

to alternative values is proposed.

In table 2(b) change of the mean of , from

to alternative values, has been considered.

Table 2: Empirical power in 2-dependent model.

Table 2(a)

Table 2(b)

change in variance of

change in mean of

Power

Power

0.8

0.622

0.0

0.049

0.6

0.960

0.5

0.285

0.4

0.975

1.0

0.961

0.2

0.989

1.5

0.999

Table 3: Empirical power of test in GARCH(1,1) model.

n

500

800

1000

no change

0.034

0.035

0.032

(0.8, 0.1, 0.2)

0.528

0.748

0.894

(0.8, 0.1, 0.5)

0.735

0.931

0.967

(0.8, 0.4, 0.2)

0.974

0.999

1.000

Table 3 shows the empirical power of the CSSM statistics in a GARCH(1,1) model.

These simulations are done for different values of .

Parameters initial values are

, and empirical powers

for different alternatives are reported.

Simulations show that the powers has significant increase with sample size.

4 Conclusion

In this article a nonparametric CUSUM test statistic is proposed

for detecting structural changes in strong mixing time series. Under

a sufficient condition this test

statistic converges in distribution to the supremum of the sum of

independent standard Brownian bridges. This method covers a broad

class of linear and nonlinear time series such as ARMA and

GARCH models, m-dependent models and many others.

Beside the wide applications, simulation results

shows that our test statistic in comparison with Berkes et al.(2009)

has a better performance and is more powerful.

5 Acknowledgment

The authors would like to thank the referee for careful reading of the paper and a number of valuable comments and suggestions that have improved the quality of the paper.

References

[1] Bartlett, M. S. (1946) On the theoretical specification

and sampling properties of autocorrelated time series, J. Royal

Statistical Society 8: 27 41.

[2] Berkes, I., Gombay, E. Horvath, L. (2009).

Testing for changes in the covariance structure of linear

processes, J. Stat. Plan. and Infer. 139:2044-2063.

[3] Billingsley, P. (1999). Convergence of probability measures,

Willey, New York.

[4] Bosq, D. (1996). Nonparametric statistics for stochastic processes,

Springer, New York.

[5] Bradley, R.C. (2005). Basic properties of strong mixing conditions. A survey and

some open questions, Probability Surveys 2:107 144.

[6]

Brockwell, P. Davis, R. Time series: theory and methods, Springer, New York, 1991.

[7] Brodsky, B. E. Darkhovski, B.S. (1993). Nonparametric

methods in change point problems, Kluwer Academic Publishers, Dordrecht.

[8] Csörgö, M. Horváth, L. (1988). Nonparametric methods for change

point problems, In: Krishnaiah, P.R., Rao, C.R. (Eds.), Handbook

of Statistics, Vol. 7. Elsevier, New York, pp. 403-425.

[9] Csörgö, M. Horváth, L. (1997). Limit Theorems in Change-Point

Analysis, Willey, Chichester, UK.

[10] Davydov, Y.A. (1968). Convergence of distributions generated

by stationary stochastic processes, Theor. Probab. Appl. 13:691-696.

[11] Galeano, P. Pena, D. (2007). Covariance changes detection in

multivariate time series, J. Stat. Plan. and Infer. 137:194-211.

[12] Herrndorf, N. (1985). A Functional Central Limit Theorem for Strongly Mixing

Sequences of Random Variables, Z. Wahrscheinlichkeitstheor.

verw. Gebiete 63:97-108.

[13] Ibragimov, I. (1962). Some Limit Theorems for Stationary

Processes, Theory of Probability and Its Applications 7:349-382.

[14] Inclán, C. Tiao, G. C. (1994). Use of cumulative sums of

squares for retrospective detection of changes of variances, J.

Amer. Statist. Assoc. 89:913-923.

[15] Kiefer, J. (1959). K-sample analogues of the Kolmogorov-Smirnov and Cramer-von

Mises tests, Annal. Math. Stat. 30:420-447.

[16] Lee, S. Ha, J. Na, O. Na, S. ( 2003). The cusum test for

parameter change in time series models, Scand. J. Statist. 30:781-796.

[17] Lee, S. Park, S. (2001). The cusum of squares test for scale

changes in infinite order moving average processes, Scand. J.

Statist 28:625-644.

[18] Page, E. S. (1954). Continuous inspection schemes, Biometrika

41:100-115.

[19] Priestley, M. B. (1981). Spectral Analysis and Time Series,

Academic Press, New York.

[20] Qin, R. Tian, Z. Jin, H. Zhang, X. (2010). Strong

convergence rate of robust estimator of change point, Math. Comput. Simul. 80:2026-2032.

[21] Rio, E. (1993). Covariance inequalities for strongly mixing processes,

Ann. Inst. H. Poincare Probab. Statist. 29:587-597.

[22] Romano, J.P., Thombs, L.A. (1996). Inference for autocorrelation

under weak assumptions, J. Amer. Statist. Assoc. 91 (434):590-600.

[23] Zhou, J. Liu, S. Y. (2009). Inference for mean

change-point in infinite variance AR(p) process, Stat. Probab. Lett. 79:6-15.