Efficient simulation and calibration of general HJM models by splitting schemes

Abstract.

We introduce efficient numerical methods for generic HJM equations of interest rate theory by means of high-order weak approximation schemes. These schemes allow for QMC implementations due to the relatively low dimensional integration space. The complexity of the resulting algorithm is considerably lower than the complexity of multi-level MC algorithms as long as the optimal order of QMC-convergence is guaranteed. In order to make the methods applicable to real world problems, we introduce and use the setting of weighted function spaces, such that unbounded payoffs and unbounded characteristics of the equations in question are still allowed. We also provide an implementation, where we efficiently calibrate an HJM equation to caplet data.

1. Introduction

The Heath-Jarrow-Morton equation (HJM-equation) of interest rate theory ([26]; see [14, 5, 15] for expositions) is a stochastic partial differential equation (SPDE) on the state space of forward rate curves, which is flexible enough to describe complicated dynamical features such as non-constant (local or stochastic) volatility, non-constant correlation, or jumps, or dependence structures. An analysis of geometric properties was performed in [16]. As forward rate curves already encode all the market’s information on default-free bond prices, it only remains to estimate volatilities either from the time series or from option prices or from both of them. For this purpose it is required that the numerical treatment of the HJM-equation can be performed efficiently: it is the purpose of this article to actually show that efficient numerical methods for the HJM-equation are at hand, how to construct and how to implement them.

In the case of generic SPDEs we usually neither have sufficient analytical information on the marginal’s distribution, nor on its Fourier-Laplace transform, nor its short-time asymptotics. We are therefore forced to apply simulation techniques to approximate the random variables in question and we face two main sources of problems in such a procedure:

1.1. Discretization error

Numerical weak or strong approximation schemes with probabilistic flavor are built upon stochastic Taylor expansion and its iteration along steps due to the Markov property. Depending on the local error of the method this leads (at least for some class of test functions) to a global error , which is called error of order . The method is called high order method if , and standard or low order method otherwise. There are schemes, e.g. cubature methods [31, 32, 35] or splitting methods [38, 37], that substantially increase and therefore reduce the global discretization error for a fixed number of discretization steps . When applying the theory of weighted spaces we can also enlarge the sets of test functions and generic equations, which can be treated by the discretization method.

1.2. Integration error

Having discretized the SPDE problem we still have to evaluate the random variables involved in each local step, which usually leads to a numerical integration problem on some , where is the fixed number of dimensions which are needed for each local discretization step. Here we can apply three approaches: (deterministic) numerical integration, Monte-Carlo algorithms (MC) or Quasi-Monte-Carlo algorithms (QMC). Due to the -dependence of integration space we do not try a direct numerical integration method, even though we have some hope that such an approach could possibly work. MC algorithms lead to integration errors , where denotes the number of integration points, whereas QMC algorithms lead to integration errors approximately . In both cases the integration error dominates the total error asymptotically, which can be seen by complexity analysis. Let us be more precise on this: we assume that operations are performed to calculate the value of the functional which we intend to integrate. Here we tacitly assume that dealing with elements in state space is , which is strictly speaking only guaranteed to be true in a finite dimensional setting. However dealing, e.g., with curves on the real line numerically can still be of if only the relevant parts of the curve are actually calculated. Hence the total complexity of the method is , where is a constant. Given an accuracy the following inequality has to hold true additionally,

whence we end up with the simple constraint minimization problem to minimize the complexity

given the previous inequality on accuracy. Its asymptotic solution is given by with and . This can be improved by multi-level methods [27, 18, 7] to a complexity estimate of order almost , which is in turn the complexity of one dimensional MC integration. In other words, the complexity is equal to the integration of a functional where evaluating at a single point is of order . Multi-level methods improve by telescoping errors on different levels of discretization . However, in this case the asymptotic complexity is not improved by higher-order methods anymore, since it depends on weak and strong convergence orders so that one is restricted to low order Euler-like methods.

If we perform the same complexity analysis in case of higher order discretization schemes with a QMC algorithm instead of an MC algorithm we obtain an asymptotic complexity with and , which is indeed considerably better than multi-level MC in case of higher order methods (). On the other hand it is not better than multi-level QMC [19] theoretically could be. We emphasize that a multi-level QMC is theoretically far from being understood, and additionally we would need strong order methods which are not always at hand. An additional problematic aspect is the need of high-dimensional integration spaces, where QMC is not known to perform well anymore.

We claim that standard QMC with high-order weak approximation schemes is superior to multilevel MC due to the low dimensionality of the integration space as long as the QMC order of convergence is understood to hold true. For accuracy the dimension of integration space is of order , which in real world implementations is often sufficiently small such that the QMC order of convergence is ensured.

The goal of this work is therefore twofold: first we want to show how actually the theory of weighted spaces applies to the HJM equation. We even show that we have a simple weak approximation method of order within this setting. Second, we claim that a QMC algorithm integrating the resulting functional is numerically efficient. We underline this statement by a calibration of a time-homogeneous, non-linear, diffusive HJM-equation to caplet data, i.e., we calibrate this equation to ten volatility smiles simultaneously. Our method is not only fast enough for the calibration of the model, but also the computer programming itself is almost as easy as a standard Euler-Maruyama scheme due to the use of a splitting approach.

Let us compare our results to well-known and recent results on splitting schemes and weak approximation methods for SPDEs. In contrast to classical results on the Lie-Trotter splitting such as [2, 3, 17, 1, 4, 39, 33, 42, 28, 20, 22, 21], we focus on a higher order method for nonlinear problems in the spirit of [38], hence allowing us to conclude the practical efficiency of the method as explained above. The topic of weak approximation for SPDEs was recently analysed in [9]. While there, the focus was on space-time white noise driving the system, we consider only finite-dimensional noise, and can obtain the same rate of convergence as in the finite-dimensional setting with bounded and smooth vector fields. Contrary to [36], our model is inherently infinite-dimensional and does not allow a reduction to a low-dimensional stochastic differential equation.

2. Weighted spaces and analysis of stochastic partial differential equations

We provide an overview of the theory of weighted spaces that is at the core of the presented numerical method. For more details, see also [40, 12, 11, 10].

2.1. The generalised Feller condition

Given a fixed , we consider the following setup.

-

(1)

For , is a separable Hilbert space, and its norm is denoted by .

-

(2)

is compactly and densely embedded into for .

-

(3)

is the generator of a strongly continuous semigroup of contractions on .

-

(4)

For , is bounded.

-

(5)

For , is a strongly continuous semigroup of contractions on .

In many cases, it will be adequate to choose , e.g., if is a differential operator on a bounded domain. If, however, is a differential operator on an unbounded domain, will usually not be compactly embedded into . As we are interested in the HJM equation, where the underlying space variable varies in , we consider the above, more general setup.

Definition 1.

Let . Given a left-continuous, increasing function with , set , we define the enveloping space , where denotes the space of times continuously Fréchet differentiable functions and

| (1) |

Here, is the linear space of bounded multilinear forms endowed with the norm

| (2) |

which makes a Banach space.

Given an orthonormal basis , define the space of bounded smooth cylindrical functions by

| (3) |

The closure of in is denoted by , .

Remark 2.

The above assumptions on the weight function are very restrictive. A weaker assumption on the weight function on which our analysis can be performed would be that the sets are weakly compact, and hence bounded, in , and that is bounded on bounded sets. This is applied in Section 5.1.

Applying [40, Corollary 5.3, Remark 5.4], we see that our space coincides with the space defined by M. Röckner and Z. Sobol. Hence, the following result is proved in [40, Theorem 5.1].

Proposition 3.

There exists an isometric isomorphy from , the dual space to , to the space

| (4) |

where the latter space is endowed with the norm , denoting the total variation measure to . The inverse of this isometry is given by for all and .

This result allows us to obtain a generalisation of the well-known Feller condition for the strong continuity of operator semigroups on , a locally compact topological space, to the infinite-dimensional setting.

Corollary 4 (generalised Feller condition).

Fix . Let be a family of continuous operators on satisfying the generalised Feller condition, i.e.,

-

(1)

, the identity on ,

-

(2)

for , ,

-

(3)

for all with some and , where is the space of bounded and linear operators on and endowed with the operator norm, and finally

-

(4)

for all and .

Then, is a strongly continuous semigroup on , i.e., for every , .

Proof.

Hence, in contrast to the weak continuity of Markov semigroups for infinite dimensional stochastic equations [6], the above result allows us to work with standard strongly continuous semigroups.

Usually, the difficult part in verifying the generalised Feller condition for a given Markov semigroup is proving that . The following result can often be applied to this problem.

Theorem 5.

For and , is dense.

Proof.

Apply Proposition 16 to obtain an orthonormal basis of that is simultaneously orthogonal in . Defining using , we see that every can be extended to a smooth cylindrical function on , as

| (5) | |||

Whence .

Next, we show . Given and , we shall construct such that . Let denote the -orthogonal projection onto . For arbitrary, we estimate

| (6) |

As is of operator norm one for all , it is easy to see by the properties of that the final term goes to zero as goes to infinity, and hence can be made smaller than by choosing , depending on but not on , large enough. For the first term, note that is precompact in . Hence, there exists such that for , with . Choose according to Corollary 17 to obtain that whenever and .

Finally, choose in such a way that and . Here, . Such a choice is always possible, as is finite dimensional and we can thus apply a standard mollifying argument. It follows similarly as above that , and plugging the results together, we obtain

| (7) |

Thus, , and the claim follows. ∎

Theorem 6.

Fix . Let be a time homogeneous Markov property on the stochastic basis with values in . Assume that

-

(1)

the mapping , is almost surely continuous with respect to the norm topology on for every ,

-

(2)

if and , then almost surely,

-

(3)

for some and , for all and , and

-

(4)

has almost surely càdlàg paths in the weak topology of .

Then, for all , where , satisfies the generalised Feller condition, and hence, is a strongly continuous semigroup on .

Proof.

First, we prove that for fixed and . Let . Set , then

| (8) |

with , , otherwise the indicator function of the set . The Markov inequality yields

| (9) |

and this term goes to zero as goes to infinity. Furthermore,

| (10) |

and dominated convergence proves that this also goes to zero as goes to infinity. Finally, note that is weakly continuous, as . Weak compactness of yields that for , and monotone convergence proves . Hence, we have shown .

2.2. Application to stochastic partial differential equations

Let be the solution of the stochastic partial differential equation

| (12a) | ||||

| (12b) | ||||

Here, is a -dimensional standard Brownian motion. The vector fields are assumed to be of the form , where is a smooth function on with values in , and is a bounded linear mapping. These are typical assumptions for HJM models to be applied in practice, see [16]. Then, it follows that (12) admits unique solutions in every space , , given that the initial value is smooth enough.

Lemma 7.

Fix and . For some , there exists such that

| (13) |

Proof.

We apply Itô’s formula. For ,

| (14) |

Taking expectations, the boundedness of the and the dissipativity of yield, as all moments are uniformly bounded by [8, Theorem 7.3.5], a constant independent of such that

| (15) |

For , we similarly obtain

| (16) |

and trivially, . Note that . Summing up, the monotone convergence theorem proves

| (17) |

Here, we have used that , and that for . As , we obtain that with a constant depending on ,

| (18) |

The method of the moving frame (see [43]) allows us to conclude that

for .

Hence, an application of Gronwall’s inequality proves the claim.

∎

Hence, the choice of weight function , , is appropriate. This is particularly important in the application of our results to the HJM equation, see Section 5.

Corollary 8.

Given and , the Markov semigroup of is strongly continuous on .

Proof.

Choose some and . We perform an analysis of the infinitesimal generator with domain of , considered as strongly continuous semigroup on . In the following, denotes the directional derivative for sufficiently smooth functions and vector fields .

Lemma 9.

Fix . For and , . Furthermore, the directional derivative defines a bounded linear operator from to , .

Proof.

The special form of proves for . The estimate can be shown by a direct calculation using the boundedness of and its derivatives, and the result follows from the density of in . ∎

Lemma 10.

Fix and . The operator maps to , and defines a bounded linear operator from to , .

Proof.

Given , there exists a -orthogonal projection with finite-dimensional range such that . Hence, , and it is easy to see that this function is in . The boundedness is again shown by a direct calculation, where we apply that for all with some constant . ∎

An application of Itô’s formula, see [8, Theorem 7.2.1], yields that for and ,

| (19) |

Theorem 11.

Fix . For and , the operator , given by the right hand side of (19), is well-defined as a bounded linear operator. Furthermore, for , , and on this space, .

Proof.

Corollary 12.

Fix . Given , we have the Taylor expansion

| (20) |

where the operator is bounded uniformly in for given .

Proof.

Theorem 11 proves that is a bounded linear operator for . Hence, a standard Taylor expansion argument can be applied to prove the stated theorem. ∎

Lemma 13.

For , and , is a bounded linear operator. Its operator norm is bounded uniformly for , where can be chosen arbitrarily.

Proof.

This is consequence of smooth dependence on the initial value in . By considering the sensitivity equations, see [8, Theorem 7.3.6], all derivatives are shown to satisfy bounds of the type

| (21) |

where is independent of .

The boundedness of in the norms given above then follows from the Cauchy-Schwarz inequality together with the property

for some constants , .

Due to Theorem 5, it follows that .

A density argument proves the claim.

∎

Corollary 14.

For , and , is a core for .

3. The rate of convergence of splitting schemes for stochastic partial differential equations

As numerical discretisation scheme, we suggest the use of a splitting scheme. Decomposing the drift coefficient further, , we define the split problems

| (22a) | |||||

| (22b) | |||||

| (22c) | |||||

We stress that all of these problems can be solved by finding the corresponding deterministic flows; in the case of ; we need to evaluate the flow induced by the vector field at the stochastic time . In particular, the processes , , are deterministic. The split semigroups are defined by and , . We consider the following splitting schemes.

- Lie-Trotter splitting, forward ordering:

-

The Lie-Trotter splitting with forward ordering is of first order and reads

(23) - Lie-Trotter splitting, backward ordering:

-

The Lie-Trotter splitting with backward ordering is obtained by reversing the order of the operators in the Lie-Trotter splitting with forward ordering,

(24) and is also of first order.

- Ninomiya-Victoir splitting:

-

The Ninomiya-Victoir splitting is a generalisation of the well-known Strang splitting to more than two generators and reads

(25) It is of second order.

The theory of Section 2 now applies not only to the continuous semigroup , but also to every split semigroup and , yielding spaces invariant to the dynamics of on which we can apply the generators , and , and , and

| (26) |

Hence, we obtain the following result.

Theorem 15.

Let , and assume that is any splitting approximation of based on the split semigroups and , , , which is of formal order . For ,

| (27) |

Proof.

The theory of [25] yields this result in the following manner. Clearly, all split semigroups are stable on the space in the sense that the operator norms of the operators are bounded by with some constant independent of and of the semigroup. Furthermore, for every , is a bounded linear operator on by Lemma 13, and on this space, we have that all generators of the split semigroups and the original semigroup are well-defined together with their products, and satisfy

| (28) |

Hence, we obtain the claimed result from [25, Theorem 2.3, Sections 4.1, 4.4]. ∎

4. Symmetrically weighted sequential splitting

Applying the theory of [23, 24] allows us to obtain asymptotic expansions for the forward and backward ordering of the Lie-Trotter splitting and the Ninomiya-Victoir splitting if the function is sufficiently smooth. Using symmetry, we can even prove that the Ninomiya-Victoir splitting and the symmetrically weighted sequential splitting, going back at least to [41, equation (25)] and given by

| (29) |

have asymptotic expansions not only in , but even . Hence, every extrapolation step would improve convergence by two orders. In particular, the symmetrically weighted sequential splitting is of second order. Comparing the dimension of integration space of different second order schemes and in view of possible extrapolations we use SWSS in our numerical computations detailed below. Indeed dimension of integration space for the Ninomiya-Victoir scheme is , whereas sequential splitting leads to dimension .

5. Application: the Heath-Jarrow-Morton equation

As application of our theoretical results, we provide a numerical method for the efficient simulation of the Heath-Jarrow-Morton equation of interest rate theory. It is of the form specified in (12), where the infinitesimal generator is given by the differential operator . In order to include a stochastic volatility process, the Hilbert spaces , are specified as follows. We set

| is times weakly differentiable and | ||||

| (30) |

Here, , and

| (31) |

It is easy to see that for , and that every function in is continuous and bounded (see also [14]). The scalar product on reads

| (32) |

With the induced norm,

| (33) |

where is a constant, becomes a bounded linear operator. It agrees with the generator of the shift semigroup on the first component of , .

Consider the Heath-Jarrow-Morton equation with stochastic volatility in Itô form,

| (34a) | ||||

| (34b) | ||||

| (34c) | ||||

| (34d) | ||||

The stochastic volatility is chosen as a mean-reverting Ornstein-Uhlenbeck process. The HJM drift satisfies the condition

| (35) |

We assume that are of the form required in Section 2.2, i.e., , where and is bounded linear. Rewriting the equation in Stratonovich form, we see that

| (36) |

and it follows easily that with some . Hence, Theorem 15 applies to prove the optimal rate of convergence of of a splitting scheme for sufficiently smooth functions , given that the initial value satisfies .

5.1. The money market account

In order to calculate standard payoffs, we not only need the instantaneous forward curve, but also the money market account . It is given by , where

| (37) |

and can therefore be easily included into our splitting scheme. Here, we denote by the short rate induced by our HJM model.

To recover the optimal rate of convergence, we argue as follows. On the product space , we consider the weight function (see Remark 2). As proved before,

| (38) |

Furthermore, as ,

| (39) |

Altogether, an application of Gronwall’s inequality proves

| (40) |

and we can apply the above theorems to all functions contained in by evident modifications of the above proofs.

Now, the money market account is not included in the above setting. More precisely, , and this growth is larger that the quadratic growth admitted by . We deal with this problem in the following way: Actually, should be nonnegative from an economic point of view. Hence, we replace the money market account by , where is with bounded derivatives, satisfies for all , and is bounded from below by with some . In our numerical experiments, performed using the model calibrated to the data from [30], we never encountered paths with . Furthermore, even if becomes slightly negative on some paths, this is numerically innocent, as we can adjust accordingly. We want to stress that our modification only acts on economically dubious paths where the money market account falls significantly in the long run, and neither limits temporary decrease, or any increase whatsoever.

Clearly, . Hence, the modified payoff of a zero coupon bond with time to maturity ,

| (41) |

is included in our setup, and lies in for all if is chosen large enough: first, note that depends on only via the bounded linear functional , . It follows that

| (42) |

Choosing , the claim is proved, as it is clear that we can approximate by functions of the form with in the norm of .

While standard payoffs, such as caplets and swaptions, do not satisfy the smoothness assumptions required in our results, we can at least prove that they are contained in a space on which convergence – albeit without rates – is ensured. A similar argument as for the bond price can be used to prove that the modified payoffs of caplets,

| (43) |

where is the LIBOR rate, and payer swaptions,

are contained in . Here, however, taking the positive part makes these functions nonsmooth. As the space of functions on which a rate of convergence is proved is dense in , we still obtain convergence.

6. Numerics for the Heath-Jarrow-Morton equation

We present the results of numerical computations for a Heath-Jarrow-Morton model. We do neither claim that the chosen HJM model is particularly well suited nor that the chosen calibration strategy is the best. We only want to demonstrate that a non-linear infinite-dimensional HJM model with stochastic volatility can be efficiently calibrated to market data with a satisfactory result.

First, a numerical calibration to caplet prices is performed, afterwards, a payer swaption is priced using the calibrated model. In our numerics, space discretisation is performed using piecewise affine and continuous functions, where the mesh is aligned with the time mesh. Hence, the partial differential equation

| (44) |

is solved exactly by shifting .

6.1. Calibration

We demonstrate the efficiency of the presented method by performing the calibration of a parametrised, time-homogeneous Heath-Jarrow-Morton model to the caplet volatility surface provided in [30]. Note that the bond prices given there are automatically reproduced in our model by choosing them as the initial value.

We set , and specify . Here, is assumed to be of the exponential-polynomial type [14], . It is easy to see that under such assumptions, the regularity required in [14, Section 5.2] is satisfied. In our experiments, we choose .

There are several economically sound possibilities for choosing . Guided by the Cox-Ingersoll-Ross model, one could choose with some , where the absolute values are necessary as we cannot guarantee positive interest rates by this approach. This ansatz, however, is not contained in our general setup, as is not a smooth function of .

Instead, we assume . This ensures that the volatilities are bounded and vanish if the benchmark yields driving the equation go to zero. We discretize the HJM-equation by the symmetrically weigthed sequential splitting scheme, as described in Section 4. The calibration is performed by combining a custom-written genetic algorithm, searching for global minima, with the Levenberg-Marquardt implementation from [34] to optimise locally. The model caplet values are calculated numerically, using time steps per year and quasi-Monte Carlo paths, based on the direction vectors for Sobol′ sequences of Joe and Kuo [29].

All in all, parameters are used to match prices, and total calibration time is minutes running on 16 cores of a Primergy RX200 S6 spotting 4 Intel Xeon CPU X5650 processor, each of which provides 6 cores. The calculation of option prices takes about seconds and therefore merits to be called efficient.

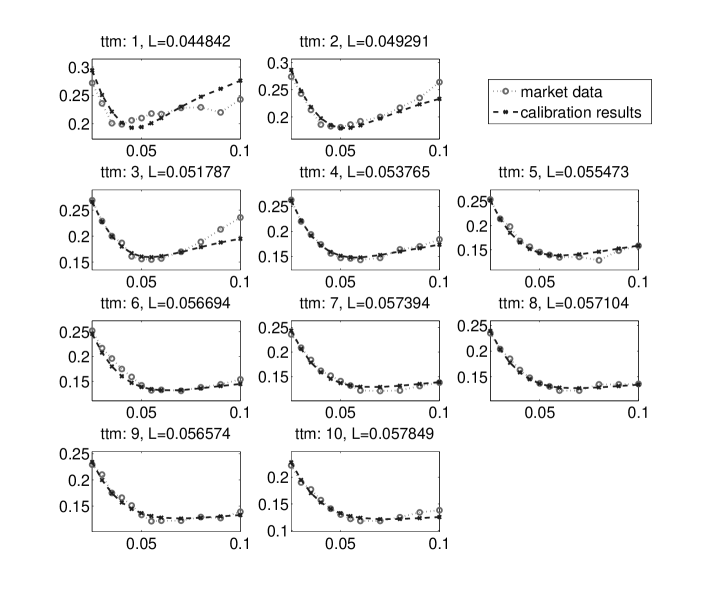

We are able to match the market volatilites taken from [30] very well using the -type volatilies. Only the error in the earlier time slices is significant, see Figure 1. This is typical for models without jumps. These are well known to misprice options close to maturity. This behaviour can also be connected to the short end of interest rates depending more on announcements by central banks than random fluctuations.

With respect to the martingale property of traded assets, numerical calculations show that bond prices and LIBOR rates satisfy the expected value property to a very high precision already using quasi-Monte Carlo paths.

6.2. Pricing

As an application, we price an at the money payer swaption with a time to maturity of years, where the underlying swap pays out quarter annually over three years, i.e., at the times for and . A reference computation with paths and time steps per year yields the value . Using paths and time steps per year, as in the calibration, we obtain . The relative error is thus approximately . As the calculation of the coarser approximation takes seconds, we have established the efficiency of the suggested method.

7. Conclusions

We introduce an analytic setup for the analysis of weak approximation methods for stochastic partial differential equations. The Heath-Jarrow-Morton equation of interest theory is shown to be included in the class where this approach is applicable. Moreover, the set of admissible test functions contains important payoffs such as caplets and swaptions. We argue that higher-order weak approximation schemes can be used together with QMC algorithms to obtain an efficient pricing method, which is even superior to multi-level MC. The efficiency of our numerical method is proved by the calibration of the model to given caplet data.

Appendix A Functional analytic results

Proposition 16.

Let , be separable Hilbert spaces with norms and such that is compactly and densely embedded into . Then, there exists an orthonormal basis of that is simultaneously orthogonal in . Furthermore, .

Proof.

By the Riesz representation theorem, there exists a bounded operator such that

| (45) |

With the compact embedding, we set . is clearly compact and also symmetric, as

| (46) |

Thus, there exists an orthonormal basis of and a sequence decreasing monotonically to zero such that , and we see that . We obtain

| (47) |

whence is orthogonal in and , and the claim is proved. ∎

Corollary 17.

Under the assumptions of Proposition 16, let denote the -orthogonal projection onto . Then,

| (48) |

Proof.

By Parseval’s identity,

| (49) |

where we apply that and that is orthogonal in . As decreases to zero, the claim follows. ∎

Acknowledgements

The numerical calculations were performed on the computing facilities of the Departement Mathematik of ETH Zürich. Parts of the computer implementation were written by Dejan Velušček, whom the authors thank for his support. Financial support from the ETH Foundation is gratefully acknowledged.

References

- [1] A. Bensoussan, Splitting up method in the context of stochastic PDE, Stochastic partial differential equations and their applications (Charlotte, NC, 1991), Lecture Notes in Control and Inform. Sci., vol. 176, Springer, Berlin, 1992, pp. 22–31. MR 1176767

- [2] A. Bensoussan and R. Glowinski, Approximation of Zakai equation by the splitting up method, Stochastic systems and optimization (Warsaw, 1988), Lecture Notes in Control and Inform. Sci., vol. 136, Springer, Berlin, 1989, pp. 257–265. MR 1180784

- [3] A. Bensoussan, R. Glowinski, and A. Răşcanu, Approximation of the Zakai equation by the splitting up method, SIAM J. Control Optim. 28 (1990), no. 6, 1420–1431. MR 1075210 (91m:65243)

- [4] by same author, Approximation of some stochastic differential equations by the splitting up method, Appl. Math. Optim. 25 (1992), no. 1, 81–106. MR 1133253 (92k:60139)

- [5] René A. Carmona and Michael R. Tehranchi, Interest rate models: an infinite dimensional stochastic analysis perspective, Springer Finance, Springer-Verlag, Berlin, 2006. MR 2235463 (2008a:91001)

- [6] Sandra Cerrai, A Hille-Yosida theorem for weakly continuous semigroups, Semigroup Forum 49 (1994), no. 3, 349–367. MR 1293091 (95f:47058)

- [7] Jakob Creutzig, Steffen Dereich, Thomas Müller-Gronbach, and Klaus Ritter, Infinite-dimensional quadrature and approximation of distributions, Found. Comput. Math. 9 (2009), no. 4, 391–429. MR 2519865 (2010h:65027)

- [8] Giuseppe Da Prato and Jerzy Zabczyk, Second order partial differential equations in Hilbert spaces, London Mathematical Society Lecture Note Series, vol. 293, Cambridge University Press, Cambridge, 2002. MR 1985790 (2004e:47058)

- [9] Arnaud Debussche, Weak approximation of stochastic partial differential equations: the nonlinear case, Math. Comp. 80 (2011), no. 273, 89–117. MR 2728973 (2011j:65014)

- [10] Philipp Dörsek, Numerical Methods for Stochastic Partial Differential Equations, Ph.D. thesis, Vienna University of Technology, October 2011.

- [11] by same author, Semigroup Splitting And Cubature Approximations For The Stochastic Navier-Stokes Equations, ArXiv e-prints (2011).

- [12] Philipp Dörsek and Josef Teichmann, A Semigroup Point Of View On Splitting Schemes For Stochastic (Partial) Differential Equations, ArXiv e-prints (2010).

- [13] Klaus-Jochen Engel and Rainer Nagel, One-parameter semigroups for linear evolution equations, Graduate Texts in Mathematics, vol. 194, Springer-Verlag, New York, 2000, With contributions by S. Brendle, M. Campiti, T. Hahn, G. Metafune, G. Nickel, D. Pallara, C. Perazzoli, A. Rhandi, S. Romanelli and R. Schnaubelt. MR MR1721989 (2000i:47075)

- [14] Damir Filipović, Consistency problems for Heath-Jarrow-Morton interest rate models, Lecture Notes in Mathematics, vol. 1760, Springer-Verlag, Berlin, 2001. MR 1828523 (2002e:91001)

- [15] by same author, Term-structure models, Springer Finance, Springer-Verlag, Berlin, 2009, A graduate course. MR MR2553163

- [16] Damir Filipović and Josef Teichmann, On the geometry of the term structure of interest rates, Proc. R. Soc. Lond. Ser. A Math. Phys. Eng. Sci. 460 (2004), no. 2041, 129–167, Stochastic analysis with applications to mathematical finance. MR 2052259 (2005b:60145)

- [17] Patrick Florchinger and François Le Gland, Time-discretization of the Zakai equation for diffusion processes observed in correlated noise, Stochastics Stochastics Rep. 35 (1991), no. 4, 233–256. MR 1113256 (92i:60139)

- [18] Michael B. Giles, Multilevel Monte Carlo path simulation, Oper. Res. 56 (2008), no. 3, 607–617. MR 2436856 (2009g:65008)

- [19] Michael B. Giles and Benjamin J. Waterhouse, Multilevel quasi-Monte Carlo path simulation, Advanced financial modelling, Radon Ser. Comput. Appl. Math., vol. 8, Walter de Gruyter, Berlin, 2009, pp. 165–181. MR 2648461 (2011c:91261)

- [20] István Gyöngy, Approximations of stochastic partial differential equations, Stochastic partial differential equations and applications (Trento, 2002), Lecture Notes in Pure and Appl. Math., vol. 227, Dekker, New York, 2002, pp. 287–307. MR 1919514 (2003b:60096)

- [21] István Gyöngy and Nicolai Krylov, On the rate of convergence of splitting-up approximations for SPDEs, Stochastic inequalities and applications, Progr. Probab., vol. 56, Birkhäuser, Basel, 2003, pp. 301–321. MR 2073438 (2005f:65012)

- [22] by same author, On the splitting-up method and stochastic partial differential equations, Ann. Probab. 31 (2003), no. 2, 564–591. MR 1964941 (2004c:60182)

- [23] by same author, Expansion of solutions of parameterized equations and acceleration of numerical methods, Illinois J. Math. 50 (2006), no. 1-4, 473–514 (electronic). MR 2247837 (2008c:65003)

- [24] by same author, Accelerated numerical schemes for pdes and spdes, Stochastic Analysis 2010 (Dan Crisan, ed.), Springer Berlin Heidelberg, 2011, pp. 131–168.

- [25] Eskil Hansen and Alexander Ostermann, Exponential splitting for unbounded operators, Math. Comp. 78 (2009), no. 267, 1485–1496. MR MR2501059

- [26] David Heath, Robert Jarrow, and Andrew Morton, Bond pricing and the term structure of interest rates: A new methodology for contingent claims valuation., Econometrica 60 (1992), no. 1, 77–105 (English).

- [27] Stefan Heinrich, Multilevel Monte Carlo methods., Berlin: Springer, 2001 (English).

- [28] Kazufumi Ito and Boris Rozovskii, Approximation of the Kushner equation for nonlinear filtering, SIAM J. Control Optim. 38 (2000), no. 3, 893–915 (electronic). MR 1756900 (2001b:93074)

- [29] Stephen Joe and Frances Y. Kuo, Constructing Sobol′ sequences with better two-dimensional projections, SIAM J. Sci. Comput. 30 (2008), no. 5, 2635–2654. MR 2429482 (2009j:65066)

- [30] Wolfgang Kluge, Time-inhomogeneous lévy processes in interest rate and credit risk models, Ph.D. thesis, University of Freiburg, 2005.

- [31] Shigeo Kusuoka, Approximation of expectation of diffusion process and mathematical finance, Taniguchi Conference on Mathematics Nara ’98, Adv. Stud. Pure Math., vol. 31, Math. Soc. Japan, Tokyo, 2001, pp. 147–165. MR 1865091 (2003k:60198)

- [32] by same author, Approximation of expectation of diffusion processes based on Lie algebra and Malliavin calculus, Advances in mathematical economics. Vol. 6, Adv. Math. Econ., vol. 6, Springer, Tokyo, 2004, pp. 69–83. MR MR2079333 (2005h:60124)

- [33] François Le Gland, Splitting-up approximation for SPDEs and SDEs with application to nonlinear filtering, Stochastic partial differential equations and their applications (Charlotte, NC, 1991), Lecture Notes in Control and Inform. Sci., vol. 176, Springer, Berlin, 1992, pp. 177–187. MR 1176783

-

[34]

M.I.A. Lourakis, levmar: Levenberg-marquardt nonlinear least squares

algorithms in C/C++, [web page]

http://www.ics.forth.gr/~lourakis/levmar/, Jul. 2004, [Accessed on 14 Jun. 2011.]. - [35] Terry Lyons and Nicolas Victoir, Cubature on Wiener space, Proc. R. Soc. Lond. Ser. A Math. Phys. Eng. Sci. 460 (2004), no. 2041, 169–198, Stochastic analysis with applications to mathematical finance. MR MR2052260 (2005b:35306)

- [36] Mariko Ninomiya, Application of the Kusuoka approximation with a tree-based branching algorithm to the pricing of interest-rate derivatives under the HJM model, LMS J. Comput. Math. 13 (2010), 208–221. MR 2669158 (2011d:65020)

- [37] Mariko Ninomiya and Syoiti Ninomiya, A new higher-order weak approximation scheme for stochastic differential equations and the Runge-Kutta method, Finance Stoch. 13 (2009), no. 3, 415–443. MR 2519839 (2010f:65013)

- [38] Syoiti Ninomiya and Nicolas Victoir, Weak approximation of stochastic differential equations and application to derivative pricing, Appl. Math. Finance 15 (2008), no. 1-2, 107–121. MR MR2409419 (2009d:60227)

- [39] A. Răşcanu and C. Tudor, Approximation of stochastic equations by the splitting up method, Qualitative problems for differential equations and control theory, World Sci. Publ., River Edge, NJ, 1995, pp. 277–287. MR 1372759 (96m:60131)

- [40] Michael Röckner and Zeev Sobol, Kolmogorov equations in infinite dimensions: well-posedness and regularity of solutions, with applications to stochastic generalized Burgers equations, Ann. Probab. 34 (2006), no. 2, 663–727. MR 2223955 (2007b:35323)

- [41] Gilbert Strang, Accurate partial difference methods. I. Linear Cauchy problems, Arch. Rational Mech. Anal. 12 (1963), 392–402. MR 0146970 (26 #4489)

- [42] M. Sun and R. Glowinski, Pathwise approximation and simulation for the Zakai filtering equation through operator splitting, Calcolo 30 (1993), no. 3, 219–239 (1994). MR 1353268 (96g:93067)

- [43] Josef Teichmann, Another approach to some rough and stochastic partial differential equations, Stoch. Dynam. 11 (2011), no. 2–3, 535–550.