Multifractal modeling of short-term interest rates

Abstract

We propose a multifractal model for short-term interest rates. The model is a version of the Markov-Switching Multifractal (MSM), which incorporates the well-known level effect observed in interest rates. Unlike previously suggested models, the level-MSM model captures the power-law scaling of the structure functions and the slowly decaying dependency in the absolute value of returns. We apply the model to the Norwegian Interbank Offered Rate with three months maturity (NIBORM3) and the U.S. Treasury Bill with three months maturity (TBM3). The performance of the model is compared to level-GARCH models, level-EGARCH models and jump-diffusions. For the TBM3 data the multifractal out-performs all the alternatives considered.

1 Introduction

Interest rates play an important role for financial institutions, for instance in risk management. Interest-rate risk is often assessed via simple stress tests, where one considers parallel shifts in the yield curve (typically 100 or 200 basis points) and reports the changes in the value of the portfolio. This approach can be improved by stochastic modeling of future movements in the interest-rate yield curve. Vasicek [1977] and Cox et al. [1985] argue that the yield curve is given by the spot rate alone. Short-term interest rates, such as NIBORM3 and TBM3, are frequently used as proxies for the spot rate, and hence accurate modeling of these time series is potentially very important. To our knowledge the present paper is the first published study considering the Norwegian rate, while the TBM3 has been studied by e.g. Andersen and Lund [1997], Chapman and Pearson [2001], Durham [2003], Johannes [2004] and Bali and Wu [2006].

Traditionally, short-term rates have been modeled by Itô stochastic differential equations on the form

| (1) |

where is the time variable, denotes the risk-free rate and is a Brownian motion. If we discretize this equation, by letting and , then we obtain a stochastic difference equation on the form , where are independent and Gaussian distributed random variables with unit variance. It is convenient to write this equation on the form

| (2) |

with and . Here with . Throughout the paper we will consider linear drift terms on the form . If , then (1) has a stationary solution, and the discretized equation has a stationary solution for sufficiently small . For a fixed we write . In this case we have stationarity for .

The number is called the Constant Elasticity Variance (CEV) parameter. For the models feature the so-called level effect. It is generally accepted that this effect is present in interest-rate data, see for instance Longstaff et al. [1992]. The level effect introduces volatility persistence, i.e. strong dependence between the absolute values of the increments . However, if is a Brownian motion, then the variables

| (3) |

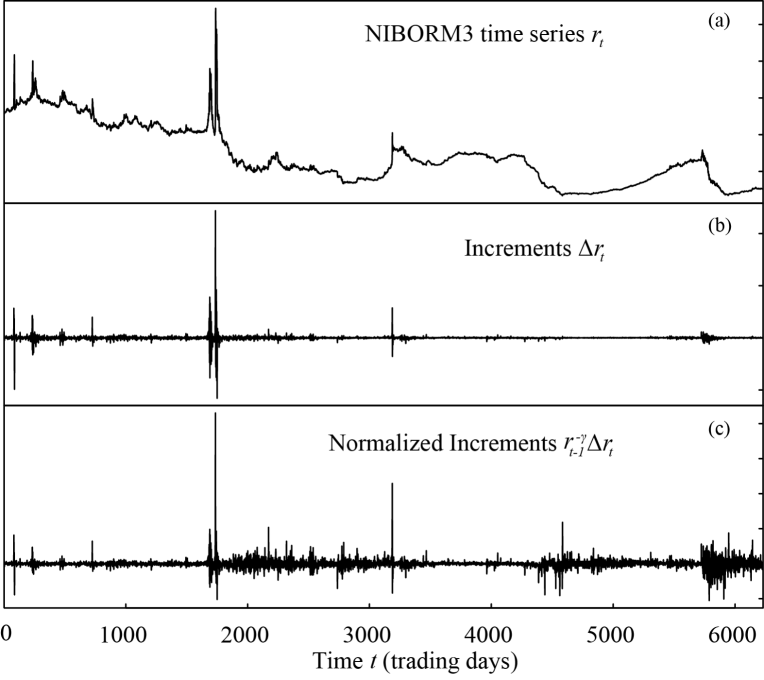

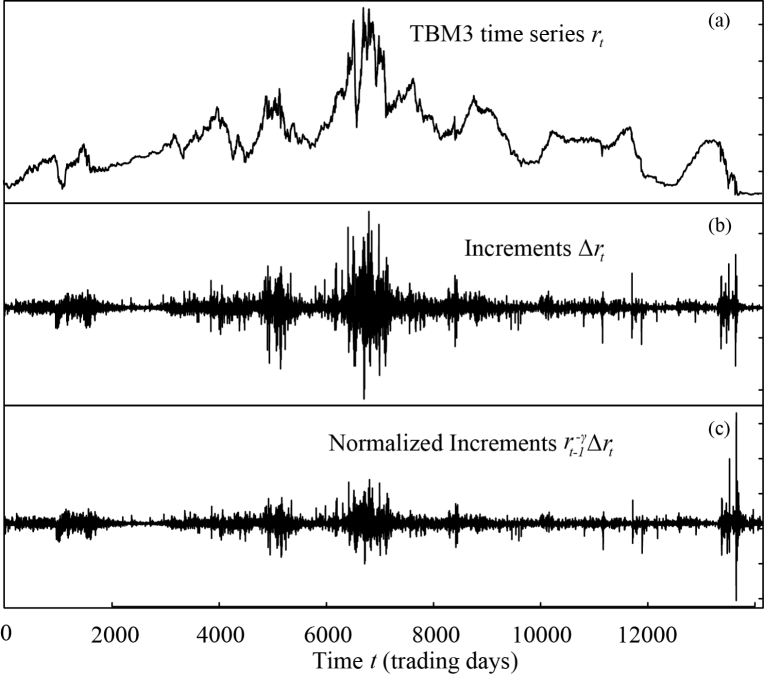

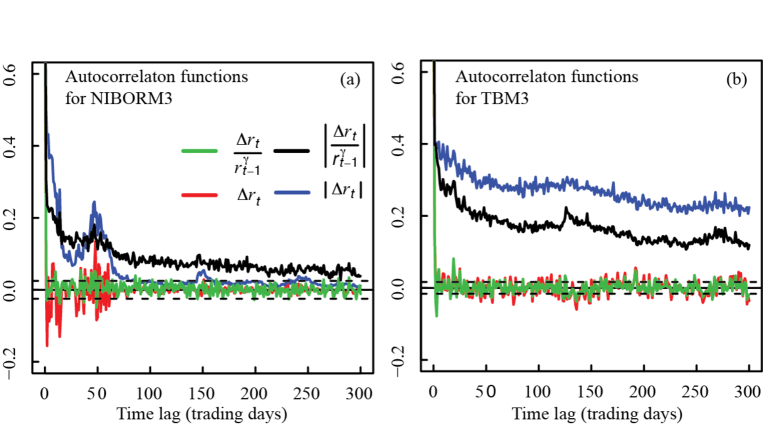

are i.i.d. and Gaussian, and hence the volatility persistence will vanish under a simple transformation of the increments. Such processes are called pure-level models and have been studied by Cox et al. [1985] and Longstaff et al. [1992]. Using time-series data for short-term interest rates we can optimize the likelihood to determine the parameters , and . These results are shown in table A. We can then transform the data according to (3). The resulting time series (which are plotted in figures 1(c) and 2(c)) are realizations of the so-called normalized increment process. Just from inspection of figures 1(c) and 2(c)) we can observe that the resulting time series exhibit strong volatility persistence. This is confirmed in figures 1(a) and 1(b), where we have plotted the autocorrelation functions for the absolute values of the normalized increments. As a consequence of these observations we conclude that pure-level models are insufficient, and we will therefore replace the process with dependent variables .

In our empirical investigations we find that the dependency structure in the variables resembles the stylized facts of logarithmic returns of asset prices, namely that the variables themselves are uncorrelated (or weakly correlated) whereas their absolute values have slowly decaying autocorrelation functions. To describe this dependency several authors (e.g. Brenner et al. [1996] and Koedijk et al. [1997]) have suggested using a generalized autoregressive conditional heteroskedasticity (GARCH) model for the process . The corresponding process is then called a level-GARCH model. These models can be further improved by letting be an Exponential GARCH (EGARCH) model or a Markov Switching GARCH (MSGARCH) model. The level-EGARCH model was introduced by Andersen and Lund [1997] and has been reported to perform better than the standard GARCH model on the TBM3 data.

In this work we propose a multifractal model, specifically a level-MSM model, as an alternative to level-EGARCH models and level-MSGARCH models for short-term interest rates. This model is a slight modification of the standard MSM model constructed by Calvet and Fisher (2004). The motivation for introducing multifractal models for short-term interest rates is similar to the motivation for multifractal modeling of asset prices, namely that these models capture the dependency structure and scaling properties of the process . Secondly, encouraging results (in- and out-of-sample) have been obtained in a preliminary study of the NIBORM3 data Løvsletten [Autumn 2010].

We follow Calvet and Fisher (2004) and use an adjusted version of the Vuong test Vuong [1989] for model selection, and the main result of this work is that the level-MSM model performs well compared against level-EGARCH models, level-MSGARCH models and jump-diffusions.

The paper is organized as follows: In section 2 we define the level-MSM model and consider some basic properties. Technical details about multifractal processes are presented in appendix 5. A brief description of the alternative models are presented in section 3, and in section 4 the results of the Vuong test are presented. In section 5 we make some concluding remarks.

Remark 1.1.

The data analyzed in this paper is freely available online. Both data sets are given with daily resolution. The TBM3 data is taken from the period 1951-01-04 to 2010-09-22, and consists of 14172 data points. The NIBORM3 data is taken from the period 1986-01-02 to 2010-09-24, and consists of 6231 data points. The TBM3 data contains several days with zero value, which causes certain technical problems in the stochastic modeling. The problem is resolved by a simple variable shift . In order to be consistent with our set of models, we estimate the constant by estimating the conditional standard deviations (for various ) and fitting a function to this data set. With this approach we find .

2 Multifractal models

The application of multifractal processes to finance was introduced by Mandelbrot et al. [1997]. A process is multifractal if the structure functions are power laws in , and one define a scaling function through the relation as , i.e.

Using Hölder’s inequality it is easy to show that the scaling function is concave, and we also note that if the process is -self similar, i.e. , then . We are therefore interested in the situations where is strictly concave. In this case we see that

If we assume that also has stationary increments, then this implies that the -lagged increments are more leptokurtic for small than for larger . In particular, can not be a Gaussian process.

In financial time series one will most often want the process to have uncorrelated and stationary increments. In order for this to be satisfied we must impose the condition , because otherwise the variables have slowly decaying autocorrelation. In fact, for

where . The advantage of a multifractal process (with strictly concave scaling function) is that it has strongly dependent increments, even for . For instance, in the MSM model111It is pointed out by Lux [2006] that the MSM model is only a finite-level approximation, and so equation (4) is only valid on time scales up to . Here and are parameters in the MSM model. See section 2.2. we have and

| (4) |

See proposition 1 in Calvet and Fisher [2004]. This inherent long-range volatility persistence serves as our motivation for modeling short-term interest rates using multifractals.

2.1 Mandelbrot’s MMAR processes

The multifractal models introduced by Mandelbrot et al. [1997] are stochastic processes on the form

| (5) |

defined for , where is a random probability measure on and is a Brownian motion with . The process is itself a multifractal process with scaling function , and if and are independent, then . By construction, the measures we will mention in this paper satisfy , i.e. . It follows that . We note that processes with correlated increments are useful in other applications (see e.g. Rypdal and Rypdal [2010]), and the Borownian motion can in these situations be replaces by a fractional Brownian motion with .

There are several choices for the measure , and for completeness we give three examples in the appendix. We also show how a particular construction, the Poisson multifractal, leads to a discrete-time MSM model defined in the next section.

2.2 The MSM model

The Markov Switching Multifractal model of order is given by

| (6) |

where , and the function is the product of the vector components. The innovatons are Gaussian distributed with unit variance, and in this setting also assumed to be independent. The process is a Markov chain defined by the following updating scheme:

| (7) |

Components are updated independently of all previous updates, and the frequencies are related to each other through (17).

For simplicity we choose a two-point distribution :

| (8) |

This version of the MSM model is known as the binomial multifractal Calvet and Fisher [2004]. To higlight the number of multipliers we will use the notation MSM(). Note that, unlike GARCH, the number of parameters remains unchanged with increasing order.

Let denote the sample space of . We also define vectors and with components and respectivly. Here , and is the density of the normal distribution with zero mean and variance . With this notation the density of is given by

| (9) |

where is the transitition matrix of the Markov chain, that is . This is seen by conditioning on the underlying Markov-chain at time and , and using Bayes’ rule. It is easily seen, once again using Bayes’ rule, that the vectors follow the recursion

| (10) |

where denotes the Hadamard product. We start the recursion with the limiting probabilities of .

2.3 The level-MSM model for interest rates

We propose the following level-MSM model for short-term interest rates:

| (11) |

where is the binomial MSM model defined above. The likelihood

for data , with taken as a pre-sample value, now follows from equations (9) and (10) together with the relation

where is the density of .

We have fitted the level-MSM models to the two time series under consideration for . For the case , the maximum likelihood (ML) estimates for the parameters and are reported in table A. In this table the estimates of and for the alternative models are also included. As expected the estimates for the parameter are negative, but we observe that none of these ML estimates are significantly different from zero for the TBM3 data. The estimates for are also very small for the NIBORM3 data, and we will therefore consider the model defined by (11) with . The corresponding ML estimates for the other parameters are presented in table A. From these results we also see that the likelihoods increase monotonically with . Using a Vuong test we compare the level-MSM of order against level-MSM models of lower order. When comparing two models with this method, the null-hypothesis is that both models are equally far from the data-generating process measured by the Kullback-Leibler distance. Hence small -values indicate that the level-MSM model of order is significantly closer to the true generating process than the level-MSM models of order or lower.

The same model-selection-test is used to compare the level-MSM model with various alternative models, and more details on the test are presented in section 4.

3 Alternative models

In this section we briefly discuss some processes which we use for benchmarking the level-MSM model. As for the level-MSM model we have first considered these models with drift terms on the form . The ML estimates for the parameters and are reported in table A. Again we see that the contribution from the parameter is negligible. Consequently we will consider models with drift terms on the form .

3.1 The level-GARCH model

In this paper we prefer the standard level-GARCH model proposed by Koedijk et al. [1997]. As is common for this model, we include student- distributed innovations. The model then reads

| (12) |

where the innovations are i.i.d. 222 is a centralized, unit-variance student- distribution with degrees of freedom.. For we have the pure-GARCH(1,1) model, and for we have the standard level model.

The estimated parameters for the NIBORM3 and TBM3 data are presented in table A. We observe that simulated paths with these exponents have far too wild fluctuations compared to the real data, indicating that this model fails to accurately describe the interest-rate fluctuations. In addition, we know that the GARCH models exhibit exponentially decaying autocorrelation functions for the absolute values of the increments. This means that the long-range volatility persistence observed in the short-term interest rates is not inherent in these models.

3.2 The level-EGARCH model

Instead of using (12), Andersen and Lund [1997] propose using the EGARCH model. They find that this model gives an adequate fit to the TBM3 data, and a better fit compared to the standard GARCH model. In the EGARCH model the logarithm of the conditional variance replaces the conditional variance. The variance-recursion is then

| (13) |

The extra parameter controls potentially different responses to positive and negative returns. The use of the logarithm guarantees positive values of the volatility for all parameter values. In addition, this model provides the extra flexibility by letting the conditional distribution be non-symmetric. As we will become apparent from the results presented in the next section, the EGARCH model gives better results than the GARCH model for both of the time series considered in this paper. This confirms the results of Andersen and Lund [1997].

The ML estimates for the parameters in the EGARCH model are presented in table A.

3.3 Jump-diffusions

The final class of alternative models considered are the jump-diffusions. Both Johannes [2004] and Das [2002] propose these processes in order to describe the large spikes observed in interest-rate data. As a discretized jump-diffusion model we use the following specification:

where is the jump-indicator assumed to follow a Bernoulli-distribution. The probability of a jump taking place at time is then given by . By letting follow a GARCH-process, conditional heteroschedacity in levels is also accomodated Das [2002]; Hong et al. [2004]. The innovations are distributed as and .The variance recursion in the GARCH process is given by

where .

The ML estimates for the parameters in the jump-diffusion model are presented in table A.

4 In-sample comparision

To test the binomial MSM model against the alternative models we emply a version of the Vuong test which is adjusted for heteroschedacity and autocorrelation (HAC) Calvet and Fisher [2004]. For each of the alternative models the null-hypothesis is that this model and the level-MSM model of order are equidistant from the true data-generating process, measured in the Kullback-Leibler distance Kullback and Leibler [1951]. In the classical Vuong test it is assumed that the data-generating process is i.i.d., and then the log-ratio of the likelihoods for the two models will converge to a normal distribution with zero mean, and with a variance which is consistently estimated by the sample variance for the log-ratio of the likelihoods. Using the corresponding normal distribution one can then easily calculate a -value under the null-hypothesis. In the HAC-adjusted version of this test, the data-generating process may exhibit dependence, but the variables should be identically distributed. This is satisfied if we assume that the data-generating process is stationary.

The results of this test are presented in table A. We observe that for the TBM3 data, the level-MSM model of order is significantly closer to the data-generating process than any of the alternative models. For the NIBORM3 data the EGARCH model performs best, whereas the level-MSM model performs better than the standard level-GARCH model and jump-diffusions.

5 Concluding remarks

In this paper we have introduced a multifractal model for short-term interest rates. The model combines the well-established level effect described in Longstaff et al. [1992] with the discretized multifractal model of Calvet and Fisher [2001]. In a comparison with level-GARCH, level-EGARCH and jump-diffusions, we find that this model well describes the fluctuations of the TBM3 and NIBORM3 time series. The main result of this work is that the level-MSM outperforms all alternatives for the TBM3 data. This motivates further research on multifractal modeling of short-term interest rates, in particular an out-of-sample analysis of the level-MSM model.

It is also interesting to note in the level-GARCH model the

parameter estimates (for both the TBM3 data and the NIBORM3 data) fall

outside the covariance-stationarity region.

As a result the level-GARCH model has a wild volatility pattern, which does not seem to be an accurate description of the interest-rate data. This confirms the results of e.g. Andersen and Lund [1997].

Examples of multifractal measures

In this appendix we give examples of random measures that can be used to define multifractal processes via (5). For the Poisson multifractal we show how a discretization leads to the model in (6).

Example 1: In the simplest case is a randomized dyadic Bernoulli measure with probabilities and . This measure is constructed through an iterative procedure, where we in the first step divide the interval in two pieces and of equal length. One of the intervals is chosen at random and given a mass , while the other interval is given the mass . This procedure is then repeated recursively, i.e. the interval is divided into the equally sized intervals and . One of these intervals is given the mass and the other is given the mass . Formally the measure can be defined by letting be a random bijection333With probability for each of the two outcomes and and be independent copies of . The measure is constructed by assigning the mass to the dyadic intervals

A simple combinatory argument shows that for , the random variable has density

When the processes and are independent, we obtain the density of :

From this density we can easily calculate the structure functions and see that as , where and .

Remark .1.

The function is sometimes called the scaling function of the random measure. The dyadic measure defined by has a multifractal spectrum given by the Legendre transform of : , and the Hentchel-Procaccia dimension spectrum is . See e.g. Pesin [1997] for an account of the relation between scaling functions and spectra of fractal dimensions. The function is often called the singularity spectrum of the process .

Example 2: A different class of multifractal measures are the -adic random multiplicative cascades (see e.g. Mandelbrot et al. [1997] for a more detailed account). For an integer and we define the -adic subintervals of as

For a positive random variable , with , let

where are independent copies of and

Again a stochastic process is constructed according to equation (5) with . This process has a scaling function , where

. Popular choices for the multiplier are log-normal distributions, which give quadratic scaling functions, or other log-infinitely divisible distributions.

Almost every realization of the measure has the multifracal spectrum .

Example 3: The Poisson multifractal measure on generalizes the -adic multiplicative cascade by introducing randomness in the construction of the intervals . In the original multifractal models, each interval on level are divided into pieces of equal length at level . As a result the interval length decreases as with the level . In the Poisson multifractal measure, the splitting of an interval at level is preformed by drawing the lengths of the new pieces randomly from an exponential distribution with rate . This means that the mean and median length of an interval at level are and respectively, so to maintain exponential decay of interval lengths (as a function of level), one chooses . Note that no longer is restricted to the integers.

Formally, the Poisson multifractal measure on the interval is defined via a sequence of measures specified on randomly generated intervals

where the numbers are defined by the following recursive construction: Let denote independent and exponentially distributed random variables with rates . Define

| (14) |

and

| (15) |

This means that the interval is divided into subintervals by the cuts made by a Poisson process with rate . We start with an interval . A sequence of measures can now be defined via the formula

where are independent copies of a positive random variable satisfying . If , then converges weakly to a Borel measure on . With this choice of random measure the model given by equation (5) has scaling function

| (16) |

Calvet and Fisher constructed their MSM model by discretizing the time interval and assigning discrete geometric (rather than an exponential) distributions on the waiting times . More precisely one will fix an integer determining the number of levels that are to be included in the discrete model, and consider the integer values , where for some positive integer . As for the construction of the Poisson multifractal one makes random partitions of the interval . These are constructed using the recursive procedure described by equations (14) and (15), where the variables are replaced by discrete random variables with geometric distributions , with . This choice of parameters implies that the median of is proportional to . Note that the parameters are given by through the formula

| (17) |

A measure is defined by specifying that if is an integer and , then

where are independent copies of a positive random variable with . Again we define , and by taking the composition with a fractional Brownian motion we get a discrete-time stochastic process . We denote , and observe that

where and is a discrete version of a white Gaussian noise. We can simplify notations by denoting for .

We finally remark that there exists a large class of multifractal random measures, knowns as log-infinitely divisible cascades Bacry et al. [2001]; Bacry and Muzy [2003]; Bacry et al. [2008], which have multifractal scaling and stationary increments. However, there only exists approximate maximum likelihood methods for these processes Løvsletten and Rypdal [2011], and hence the Voung-testing preformed in this paper is not available.

Acknowledgment. This project was partly funded by Sparebank 1 Nord-Norge and the Norwegian Research Council (project number 208125).

Appendix A Figures and tables

CEV-models. Innovations \colrule U.S. Treasury Bill Normal NIBORM3 Normal \botrule \tabnoteThe constant elasticity volatility (CEV) model of Longstaff et al. [1992] with normal and student- innovations.

Multifractal models BIC Vuong HAC-adj. \colrule U.S. Treasury Bill M3 -3.1446 13.573 9.091 () () -3.1964 11.618 10.138 () () -3.2165 8.4076 7.562 () () -3.2281 5.036 4.805 () () -3.2308 4.346 4.335 () () -3.2326 3.4883 3.112 () (0.001) -3.2352 1.131 0.938 (0.129) (0.174) -3.2358 \colrule NIBORM3 -2.7250 5.219 5.298 () () -2.7755 3.054 3.093 (0.001) () -2.8039 3.424 3.588 () () -2.8102 3.292 3.265 () (0.001) -2.8133 2.702 2.866 (0.003) (0.002) -2.8162 1.809 1.727 (0.0352) (0.042) -2.8175 1.058 0.940 (0.145) (0.173) -2.8181 \botrule \tabnoteML-estimates for the binomial multifractal with estimated standard errors in parantesis. The Vuong-column reports the likelihood ratio statistic with corresponding -value in brackets Vuong [1989]. The null hypothesis is that MSM(9) and MSM(K) have equal Bayesian Information Criteria, with the alternative hypothesis being that the MSM(9) is closer to the true data generating process. The HAC-adjusted version of the Vuong test Calvet and Fisher [2004] corrects for heteroschedacity and autocorrelation in the addends.

Level-GARCH BIC \colrule U.S. Treausury Bill M3 NIBORM3 -2.8113 \botrule \tabnoteML estimates for the parameters in the level-GARCH model. Standard deviations are in brackets.

Level-EGARCH BIC \colrule U.S. Treausury Bill M3 -3.2324 \colrule NIBORM3 -2.8245 \botrule \tabnoteML estimates for the parameters in the level-EGARCH model. Standard deviations are in brackets.

Jump-diffusion BIC \colrule U.S. Treasury Bill M3 -3.1839 \colrule NIBORM3 -2.7431 \botrule \tabnoteML estimates for the parameters in the jump-diffusion model. Standard deviations are in brackets.

In-sample model comparison. Model BIC Vuong Hac-adj. \colrule U.S. Treasury Bill M3 MSM(9) -3.2358 GARCH 22873.03 -3.2241 -4.064() -3.477() EGARCH 22936.53 -3.2324 -1.420 (0.078) -1.361 (0.087) Jump-diffusion 7 22597.89 -3.1839 -9.878 () -9.240 () \colrule NIBORM3 MSM(9) -2.8181 GARCH -2.8113 -1.099(0.136) -1.086(0.139) EGARCH 8828.90 -2.8245 1.231(0.891 ) 1.470 (0.929) Jump-diffusion 7 8579.61 -2.7430 -6.964() -5.765() \botrule \tabnoteThe Vuong-column reports the test-statistic for differences in BIC. The null hypothesis is that the multifractal and the alternative model are equally good, with the alternative hypothesis being that the multifractal model performs best. The HAC-adjusted column adjusts for heteroschedacity and autocorrelation in the addends. Corresponding -values are in brackets.

Linear drift Model \colrule U.S. Treasury Bill M3 MSM(9) GARCH EGARCH Jump-diffusion \colrule NIBORM3 MSM(9) GARCH EGARCH Jump-diffusion \botrule \tabnoteA linear term in the drift term was added and the parameters estimated using ML. In the TBM3 none of the parameters are significantly different from zero. Standard deviations are reported in brackets.

References

- Andersen and Lund [1997] T. G. Andersen and J. Lund. Estimating continuous-time stochastic volatility models of the short-term interest rate. Journal of Econometrics, 77(2):343 – 377, 1997.

- Bacry and Muzy [2003] E. Bacry and J. F. Muzy. Log-Infinitely Divisible Multifractal Processes. Communications in Mathematical Physics, 236(3):449–475, 2003.

- Bacry et al. [2001] E. Bacry, J. Delour, and J. F. Muzy. Multifractal random walk. Physical Review E, 2001.

- Bacry et al. [2008] E. Bacry, A Kozhemyak, and J. F. Muzy. Continuous cascade models for asset returns. Journal of Economic Dynamics and Control, 32(1):156–199, 2008.

- Bali and Wu [2006] T. G. Bali and L. Wu. A comprehensive analysis of the short-term interest-rate dynamics. Journal of Banking and Finance, 30(4):1269 – 1290, 2006.

- Brenner et al. [1996] R. J. Brenner, R. H. Harjes, and K. F. Kroner. Another look at models of the short-term interest rate. Journal of Financial and Quantitative Analysis, 31:85–107, 1996.

- Calvet and Fisher [2001] L. Calvet and A. Fisher. Forecasting multifractal volatility. Journal of Econometrics, 105(1):27 – 58, 2001.

- Calvet and Fisher [2004] L. Calvet and A. Fisher. How to Forecast Long-Run Volatility: Regime Switching and the Estimation of Multifractal Processes. Journal of Financial Econometrics, 2(1):49–83, 2004.

- Chapman and Pearson [2001] D. A. Chapman and N. D. Pearson. Recent advances in estimating term-structure models. Financial Analysts Journal, 57:77–95, 2001.

- Cox et al. [1985] J. C. Cox, J. E. Ingersoll Jr., and S. A. Ross. A theory of the term structure of interest rates. Econometrica, 53:385–407, 1985.

- Das [2002] S. R. Das. The surprise element: jumps in interest rates. Journal of Econometrics, 106(1):27 – 65, 2002.

- Durham [2003] G. B. Durham. Likelihood-based specification analysis of continuous-time models of the short-term interest rate. Journal of Financial Economics, 70(3):463 – 487, 2003.

- Hong et al. [2004] Y. Hong, H. Li, and F. Zhao. Out-of-sample performance of discrete-time spot interest rate models. Journal of Business and Economic Statistics, 22(4):457–473, 2004.

- Johannes [2004] M. Johannes. The statistical and economic role of jumps in continuous-time interest rate models. The Journal of Finance, 59(1):227–260, 2004.

- Koedijk et al. [1997] K. G. Koedijk, J. A. Nissen, P. C. Schotman, and C. P. Wolff. The Dynamics of Short-Term Interest Rate Volatility Reconsidered. European Finance Review, 1(1):105–130, 1997.

- Kullback and Leibler [1951] S. Kullback and R. A. Leibler. On information and sufficiency. Ann. Math. Stat., 22:79–86, 1951.

- Longstaff et al. [1992] F. A. Longstaff, K. C. Chan, G. Andrew Karolyi, and A. B. Sanders. An empirical comparison of alternative models of the short-term interest rate. The Journal of Finance, 47:1209–1227, 1992.

- Løvsletten and Rypdal [2011] O. Løvsletten and M. Rypdal. Approximate Maximum Likelihood Estimation in Multifractal Random Walks. preprint, 2011.

- Løvsletten [Autumn 2010] O. Løvsletten. Empirical analysis and stochastic modeling of temporal fluctuations in the norwegian interbank offered rate. Master thesis, written in Norwegian, Autumn 2010. URL http://complexityandplasmas.net/nordforsk/Papers.html.

- Lux [2006] T. Lux. The markov-switching multifractal model of asset returns : Gmm estimation and linear forecasting of volatility. Economics Working Papers, 17, 2006.

- Mandelbrot et al. [1997] B. Mandelbrot, A. Fisher, and L. Calvet. A Multifractal Model of Asset Returns. Cowles Foundation for Research in Economics, 1997.

- Pesin [1997] Y. Pesin. Dimension Theory in Dynamical Systems. Chicago Lectures in Mathematics, 1997.

- Rypdal and Rypdal [2010] M. Rypdal and K. Rypdal. Stochastic modeling of the ae index and its relation to fluctuations in bz of the imf on time scales shorter than substorm duration. Journal of Geophysical Research, 115, 2010.

- Vasicek [1977] O. Vasicek. An equilibrium characterization of the term structure. Journal of Financial Economics, 5(2):177 – 188, 1977.

- Vuong [1989] Q. H. Vuong. Likelihood ratio tests for model selection and non-nested hypotheses. Econometrica, 57:307–333, 1989.