Returns in futures markets and t-distribution

Laurent Schoeffel

CEA Saclay, Irfu/SPP, 91191 Gif/Yvette Cedex,

France

The probability distribution of log-returns of financial time series, sampled at high frequency, is the basis for any further developments in quantitative finance. In this letter, we present experimental results based on a large set of time series on futures. Then, we show that the t-distribution with gives a nice description of almost all data series. This appears to be a quite general result that stays robust on a large set of any financial data as well as on a wide range of sampling frequency of these data, below one hour.

1 Introduction

Returns in financial time series are the most fundamental inputs to quantitative finance. To a certain extend, they provide some insights in the the dynamical content of the market. In this letter, we consider several financial series on futures, using always a five minutes sampling. Each future contract is characterized by a price series , from which we extract the log-returns . The analysis is then driven on these log-returns .

From standard quantitative analysis [1, 2, 3, 4], we know that the distribution of log-returns , namely , can be written quite generally as

| (1) |

where is an objective function and a normalization factor. In particular, it can be shown easily that can be derived by minimizing a generating functional , subject to some constraints on the mean value of the objective function. It reads

| (2) |

where is an arbitrary constant.

In addition, the expression given in Eq. (1) for the probability distribution can also be seen as the outcome of an equation of motion for . From Eq. (1) and (2), we can express the stochastic process as a Markovian process of the form [1, 2, 3, 4]

| (3) |

where is a Gaussian process satisfying and . In Eq. (3), functions and depends only on . Adopting the Itô convention [1, 2, 3, 4], the distribution function , associated with this equation of motion (Eq. (3)), is given by the following Fokker-Planck equation

| (4) |

From Eq. (4), we can finally extract the stationary solution for in the form of Eq. (1)

| (5) |

2 Parameterizations of

In Eq. (3), (4) and (5), functions and are not specified and any choice can be considered. Obviously, only specific choices will have a chance to get a reasonable agreement with real data. For example, let us consider three cases:

-

(i)

If and , we obtain , and thus we predict a Gaussian shape for the log-returns distribution.

-

(ii)

In the more general case where and is not constant, we obtain

and thus we predict non-Gaussian shape for the log-returns distribution.

-

(iii)

Let us specify the case (ii). Introducing a constant and defining the two functions and as and , we get

(6) In this scenario follows the so-called t-distribution. It depends on one parameter to be fitted on real data, for normalized log-returns. Let us notice that Eq. (6) is equivalent to the q-exponential form of Ref. [5, 6]

(7) where we have conserved the notations of Ref. [5, 6]. Obviously, Eq. (6) and (7) are directly related by . In particular, is equivalent to .

3 Experimental Analysis of

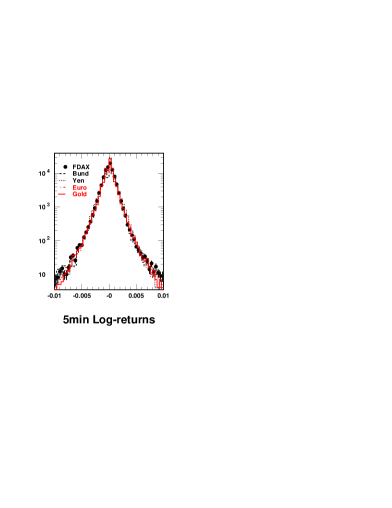

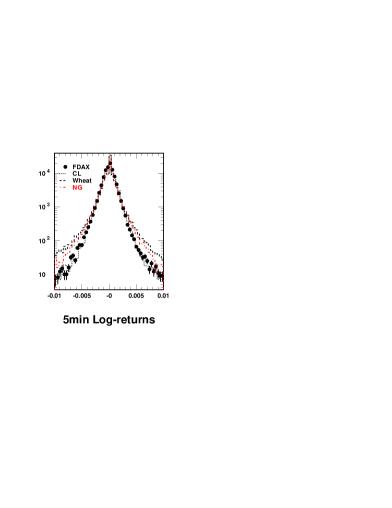

In Fig. 1, we present the log-returns (five minutes sampling) for a large set of futures. To make the comparison, we have scaled for all futures to the volatility of the DAX future (FDAX). On the left hand side (LHS) of Fig. 1, we observe that futures on DAX, Bund, Yen, Euro, Gold present the same probability distribution for , hence is universal for all these data series once the volatility is normalized to the same value. On the right hand side of Fig. 1, we provide comparisons with futures on commodities. We observe that data series on CL (Crude Oil) follows the same as FDAX, but other data series on Wheat and NG (Natual Gaz) exhibit some larger tails.

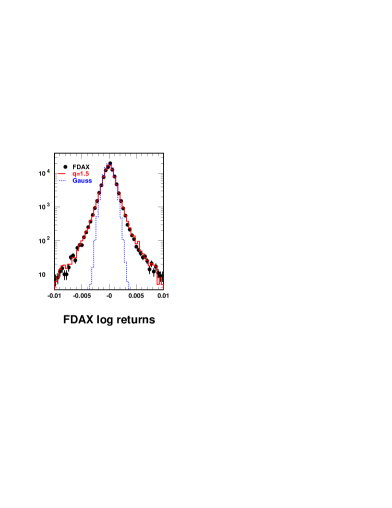

We can use results developed in section 2 in order to compare with experimental distributions of Fig. 1. We use predictions exposed in cases (i) and (iii), respectively the Gaussian and the q-exponential forms (or t-distribution). Results are shown in Fig. 2. For data, we only display for FDAX.

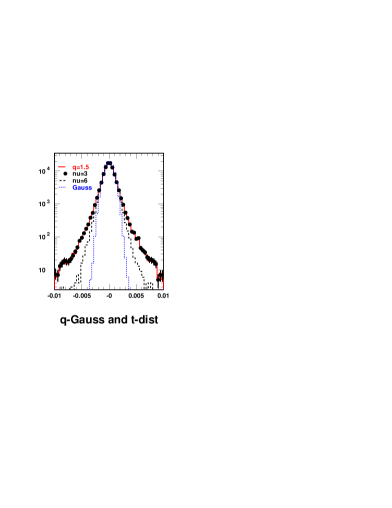

In Fig. 2, we show that the q-exponential probability distribution of Eq. (7), with , gives a good description of the data. Similarly, it corresponds to in the form of the t-distribution of Eq. (6). Let us notice that futures with larger tails discussed above correspond to smaller values of . Also, we observe in Fig. 2 that the Gaussian approximation fails to describe properly the data. On the right hand side of Fig. 2, we observe that when is increased above in Eq. (6), then stands in the middle of the correct probability density and the Gaussian approximation. When tends to infinity, the t-distribution recovers the Gaussian limit.

4 Conclusion

From the theory point of view, the probability distribution of log-returns of financial time series, sampled at high frequency, can be expressed quite generally as . In this expression, the function can be derived using the formalism of stochastic differential equations applied to quantitative finance. Several cases have been considered in this letter. Then, we have shown that real data (with normalized log-returns) are compatible with a distribution of the form

We have exemplified this property on a sample of data sets. However, this is a quite general result that stays robust on a larger set of financial data as well as on a wide range of sampling frequency of these data, below one hour. Interestingly also, this probability distribution corresponds to the equation of motion Eq. 3, with the expressions of and given in case (iii). This can serve as a basis for a Monte-Carlo simulation of market data and subsequent risk analysis.

References

- [1] R. Mantegna and H. E. Stanley, An Introduction to Econophysics, Cambridge Univ. Press, Cambridge, 2000.

- [2] D. Duffie, Dynamic Asset Pricing, 3rd ed., Princeton University Press, Princeton, NJ, 2001.

- [3] J. Voit, The Statistical Mechanics of Financial Markets, Springer, Berlin, 2003.

- [4] see e.g. J.P. Bouchaud, M. Potters, Theory of Financial Risks and Derivative Pricing, Cambridge University Press (2004).

- [5] C. Tsallis, Braz. J. Phys. 29 (1999) 1.

- [6] D. Prato and C. Tsallis, Phys. Rev. E 60 (1999) 2398.