How much multifractality is included in monofractal signals?

Abstract

We investigate the presence of residual multifractal background for monofractal signals which appears due to the finite length of the signals and (or) due to the long memory the signals reveal. This phenomenon is investigated numerically within the multifractal detrended fluctuation analysis (MF-DFA) for artificially generated data. Next, the analytical formulas enabling to describe the multifractal content in such signals are provided. Final results are shown in the frequently used generalized Hurst exponent multifractal scenario and are presented as a function of time series length and the autocorrelation exponent value . The multifractal spectrum approach is also discussed. The obtained results may be significant in any practical application of multifractality, including financial data analysis, because the ’true’ multifractal effect should be clearly separated from the so called ’multifractal noise’. Examples from finance in this context are given. The provided formulas may help to decide whether we do deal in particular case with the signal of real multifractal origin. They also push further findings already existing in literature.

Keywords: multifractality, multifractal noise, time series analysis, autocorrelations, multifractal detrended analysis, generalized Hurst exponent, long-range memory

PACS: 05.45.Tp, 89.75.Da, 05.40.-a, 89.75.-k, 89.65.Gh

1 Introduction

Multifractality [1, 2, 3, 4, 5, 6, 7] is the property of complex and composite systems that has been attracting more and more attention in recent years. The practical fruits of multifractality are not precisely known yet but at least in the case of financial markets some interesting features of this phenomenon were shown (see e.g. [8, 9, 10, 11, 12, 13, 14, 15, 16, 17]) that rise hopes for future applications. Since the paper by Kantelhardt et.al. [18] we know that multifractality may result not only from long-range correlations but also from fat tails in probability distributions (PDF) of investigated data. Normally, one expects multifractality in time series as a result of different form of autocorrelations appearing at various time scales. However, we always deal in practise with finite samples of data collected in time series of given length. In such a case, multifractality may appear even if no difference in autocorrelation properties exists for various time scales. It is because large fluctuations cannot be detected as frequent as small fluctuations in finite samples of data with long memory – mainly due to the insufficient data statistics. In other words, large fluctuations are not able to be formed in small samples of data, contrary to small fluctuations. Therefore, one gets in the case of shorter time series the multifractal property which itself is not programmed to be multifractal in a sense of different autocorrelation properties at various scales. The latter multifractality, related to variety of autocorrelations, is more substantial and has to be somehow separated from the former one which we shall call the multifractal background or residual noise further on. The preliminary analysis of this problem had already been made in [19, 20]. Our goal is to describe the presence of multifractal background quantitatively for time series with long memory induced by explicit form of autocorrelations in data. Our approach is directly based on Fourier filtering method (FFM) [21] and differs therefore from other approaches, where the long-memory effect was inserted into a signal by the particular choice of power spectrum (amplitude adjusted Fourier transform method [22]) [19] or log-normal cascade implementation [20], instead of direct shaping the artificial data with autocorrelation exponent discussed further on.

We use the multifractal detrended fluctuation analysis (MF-DFA) [4] as the commonly accepted technique to find multifractal properties of time series. This method is described elsewhere (see e.g. [4, 16, 17, 18]) so we will not recall it in details here. To keep the standard notation we will note the -deformed fluctuation of the time series signal around its local trend (assumed linear in our approach) in a time window of size as . Usually, the multifractal properties are presented as the multifractal spectrum [7], called sometimes also Hölder description. Equivalently, in the Hurst language, one can consider the spread of generalized Hurst exponents [18], calculated within MF-DFA for fluctuations from the power law:

| (1) |

Both descriptions are linked together via relations [23, 24]

| (2) |

We start in this article with the generalized Hurst exponent description of multifractality. Our results are then easy translated into Hölder language with the use of Eq.(2). Finally, we compare our findings with the properties of real data from financial market, commonly believed to exhibit multifractal features.

2 Generalized Hurst exponents for finite monofractal signals

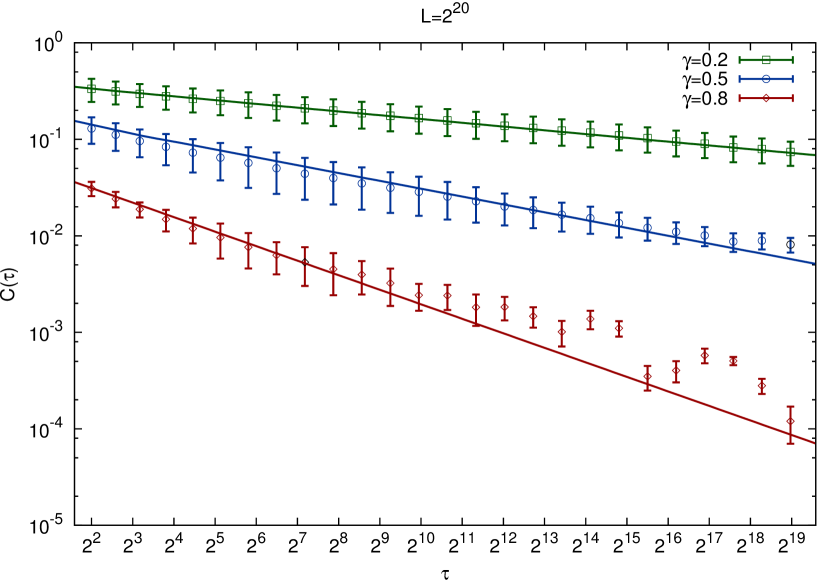

Our aim is to evaluate the multifractal effect in finite artificial signals of various lengths for given constant level of persistency, i.e. that autocorrelations are not changing with the time scale. Such signals are built by us within FFM [21]. The level of autocorrelations is modulated by the proper choice of scaling exponent responsible for the magnitude of autocorrelation function . The latter one satisfies for stationary series with long memory the known power law:

| (3) |

where are increments of time series, is the time-lag between observations and the average is taken over all data in the series.

In the quantitative analysis of residual multifractality left in monofractal finite signals, we concerned the ensembles of numerically generated time series of length , with the pre-assumed autocorrelation exponent value , each containing independent realizations. Thus, the spread of exponents covers the range . The obtained quantities have been averaged over such statistical ensemble with given and as input parameters.

First, we examined the FFM procedure for time series generation, in order to check its accuracy towards replication of the pre-assumed autocorrelation properties coming out from the particular choice of exponent as input. Fig.1 demonstrates its efficiency. It is seen that the power law in Eq.(3) is reproduced very well even for large time-lags. Moreover, a coincidence between input and output ’s is also satisfactory. The length of generated data-samples was chosen as powers of to improve performance of fast Fourier transform algorithm.

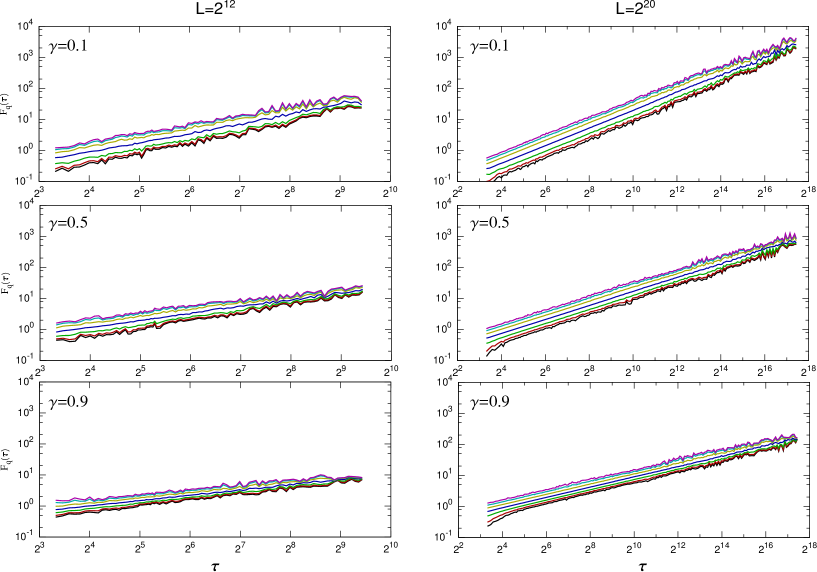

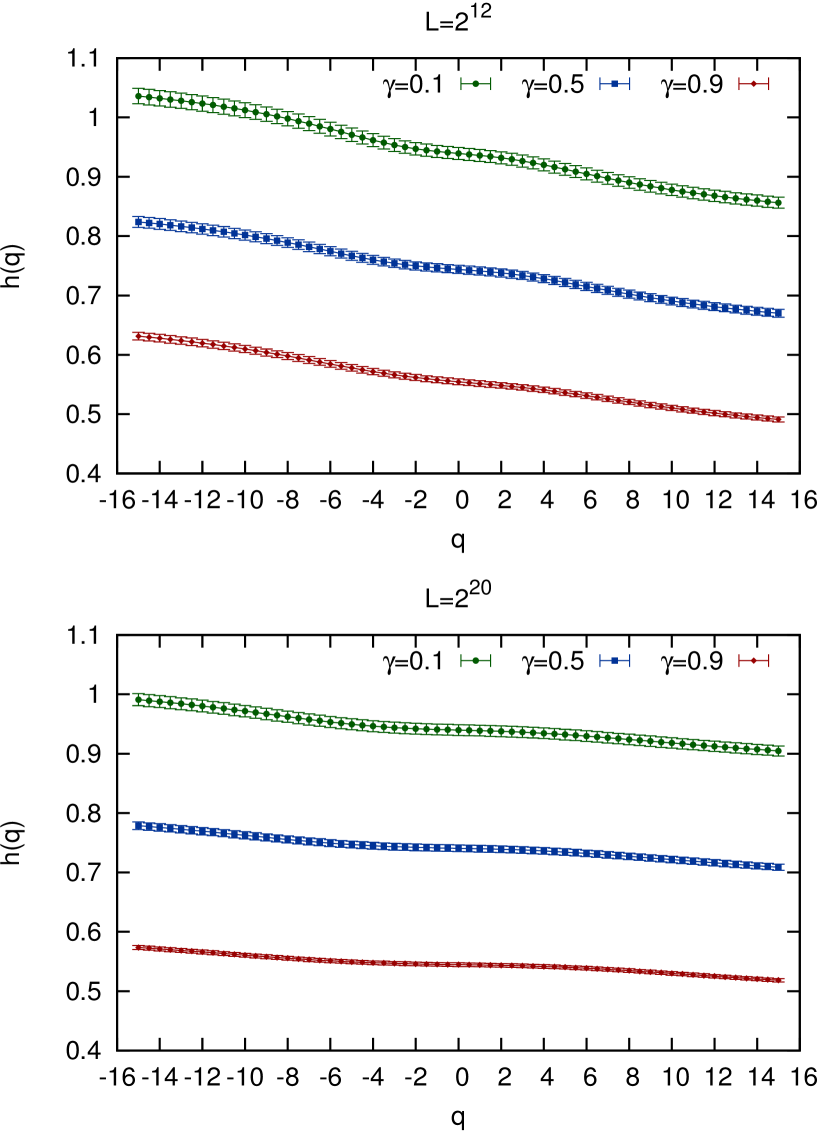

The next problem we had to examine, is the performance of MF-DFA technique which strictly depends on the power law scaling between fluctuations and the box size (see Eq.(1)). An exact extraction of the generalized Hurst exponent is then possible only for well determined scaling range in the fitting procedure vs . Fig.2 clearly shows the expected power law dependence for various lengths of the signal and for different values of deformation parameter . The latter one was uniformly distributed in the range from to . These plots justify the scaling range from till which was chosen by us to be used further on.

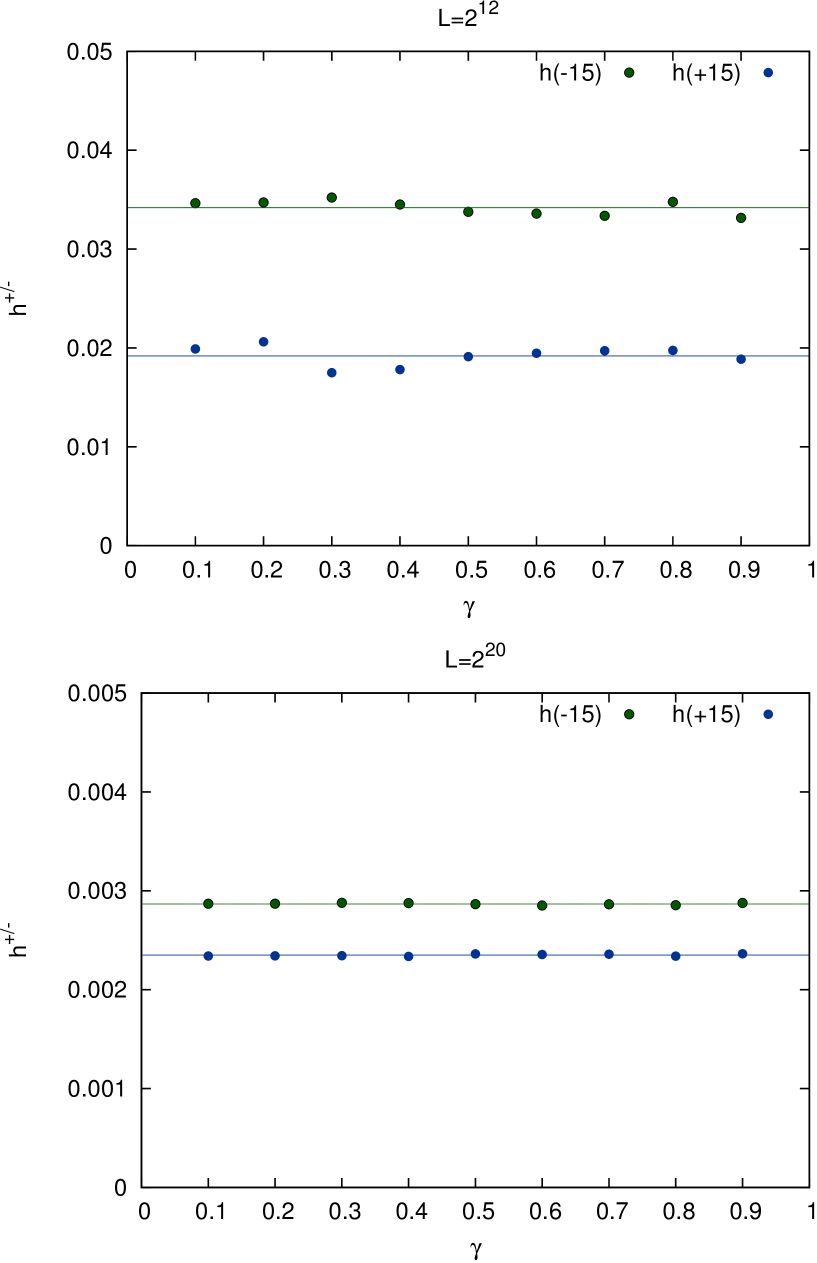

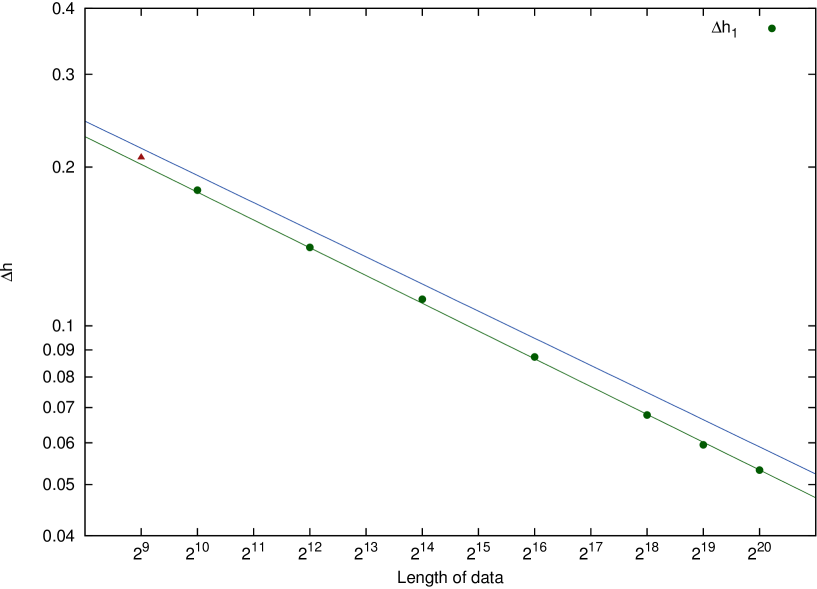

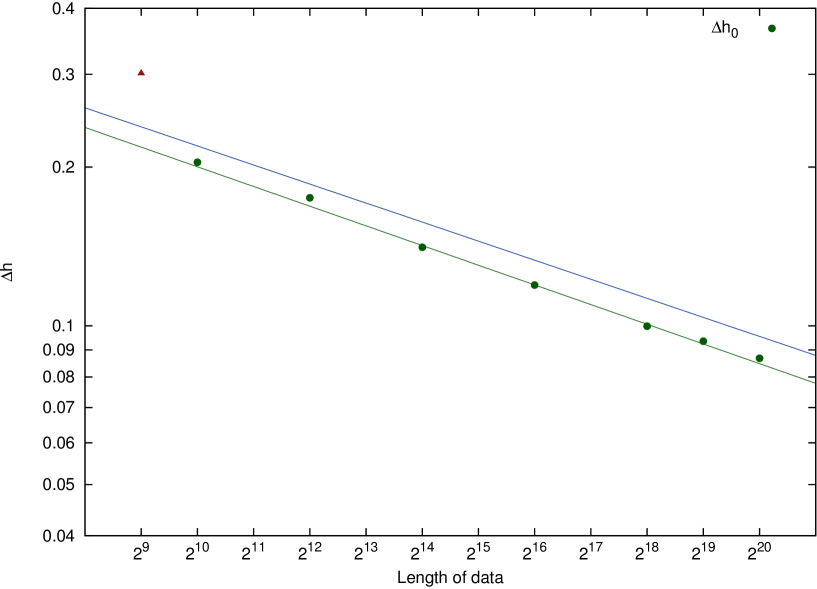

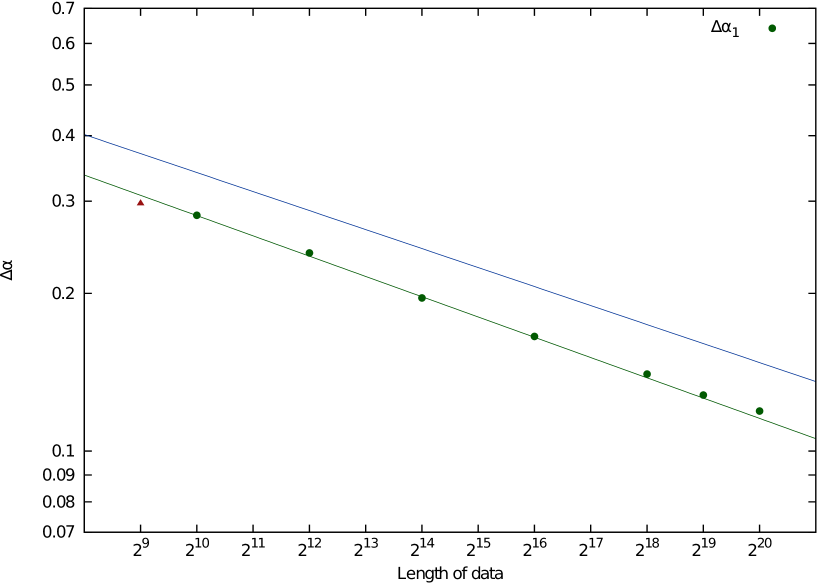

To determine quantitatively the amount of multifractal residual noise present in given time series, the edge values of function were investigated for them. Let us introduce the new parameter defined as the difference between the two asymptotic limits

| (5) |

and assume for numerical reasons that such asymptotic limits are reached already at . Such assumption is justified in Fig.3, where plots for are shown for and for respectively.

Generally, we may expect that is the unknown function of and . The form of dependence is thus a crucial problem. To simplify it, one may consider the case for a moment, e.g. (), corresponding to uncorrelated data. Fig.4 shows the edge characteristics of presented for two distinct series of length , generated with the autocorrelation exponent , and then shuffled. The dependence on is evidently absent proving that shuffling procedure was effective enough, while the residual dependence on is still kept and obvious.

The detailed analysis of the latter dependence is revealed in Fig.5 collecting results for various data lengths. Astonishingly, this figure suggests a power law dependence between and .

| (6) |

where and are constant.

The knowledge of confidence level for this relation is crucial in practise. Its meaning is that any result measured above the particular value has probability less than . To obtain this confidence level one has to correct and parameters by the corresponding quantiles calculated from the uncertainties , of the fit and from the standard deviation resulting from the series statistics333exponential dependence in this formula comes from the uncertainty of regression fit in logarithmic scale:

| (7) |

where is the respective factor for the particular confidence level.

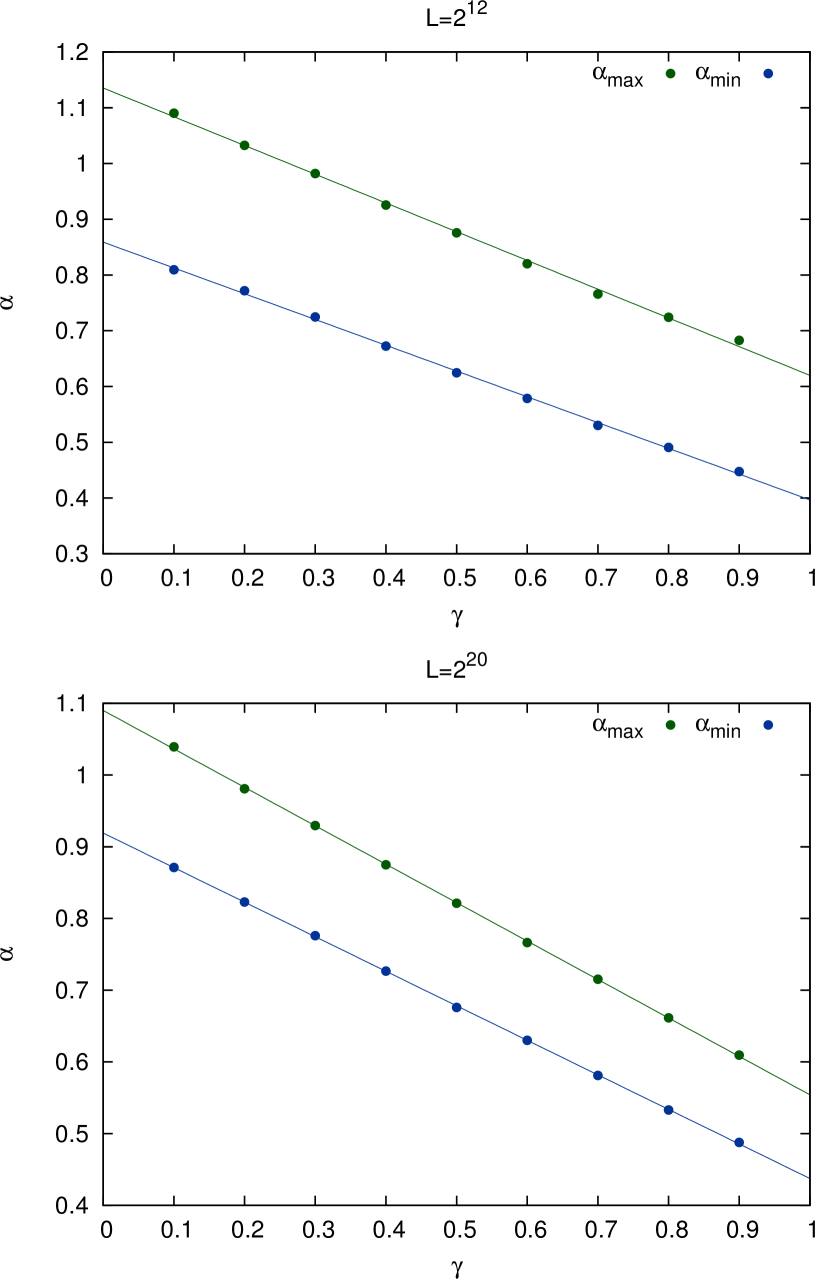

Let us take now a closer look at the case of autocorrelated () finite signals. The edge values for versus the autocorrelation exponent value were investigated, keeping fixed. Examples of this dependence for and are shown in Fig.6. We found that cases for other lengths (not shown) look similarly and indicate the excellent linear decreasing function of versus in the whole range of autocorrelation exponent. Thus one gets:

| (8) |

where the coefficients and depend on only. They can be further specified if the form of and functions are used as boundary conditions.

The first boundary condition, i.e. , was already specified in Eq.(6). The profile of the second one () can be deduced from Figs. 6,7. The extrapolation of the fitting lines versus to the point (see Fig.6) gives the collection of values, plotted against the length of time series in Fig.7. This can be done for the central values as well as for the data satisfying confidence level. It is seen from the Fig.7 that for fully autocorrelated time series () is represented again by the power law:

| (9) |

with some constants and to be determined from the fit.

Linking the shape of boundary conditions given by Eqs.(6) and (9) with the general linear dependence in Eq.(8), one arrives with the final formula for :

| (10) |

The shape of the confidence level for multifractal background noise will be given by the same formula but with different coefficients calculated according to formulas like in Eq.(7). The final values of these coefficients are collected in Table 1.

| 0.603 | 0.175 | 0.453 | 0.124 | 0.631 | 0.171 | 0.484 | 0.120 |

|---|

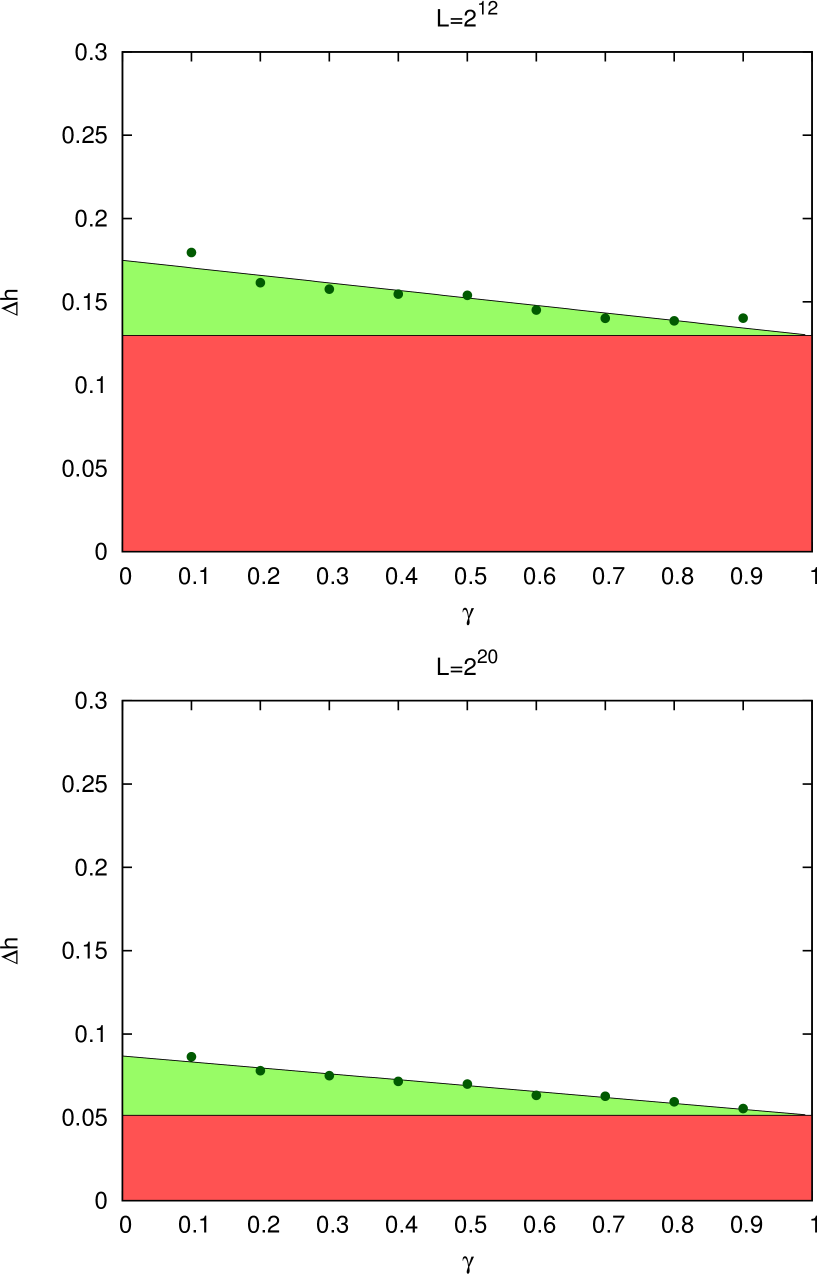

Our results may also be presented graphically in a form of ’phase-like’ diagrams (see Fig.8).Three separable areas in plane can be distinguished for every . The first area corresponds to multifractality connected entirely with finite size effects. It is marked in red in Fig.8. The second domain, marked in light green, is related to range where multifractality may occur due to the long memory present in data but independent on the chosen time scale. The ’true’ multifractality, i.e. the one related with long memory entirely dependent on the time scale, may occur only in the white region (at confidence level).

3 Multifractal spectrum analysis of finite size effects.

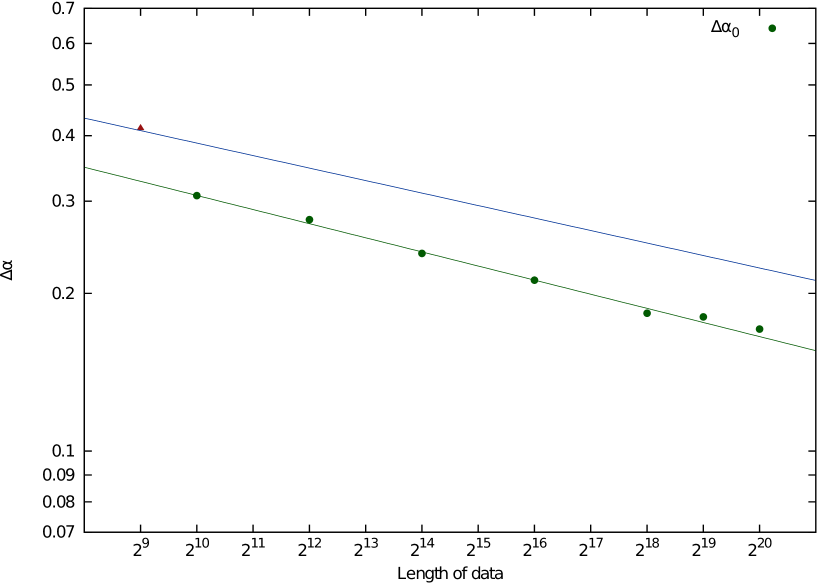

The multifractal spectrum width is considered as another useful measure of multifractality included in analyzed signal. Analogically to the analysis, one may ask for the dependence of multifractal spectrum width on the signal length and on its persistency level . These results are obtained with use of Eq.(2) applied to previously discussed generalized Hurst exponent calculations. Thus, the results should lead to similar qualitative conclusions, nevertheless quantitatively they might be also valuable from practical point of view.

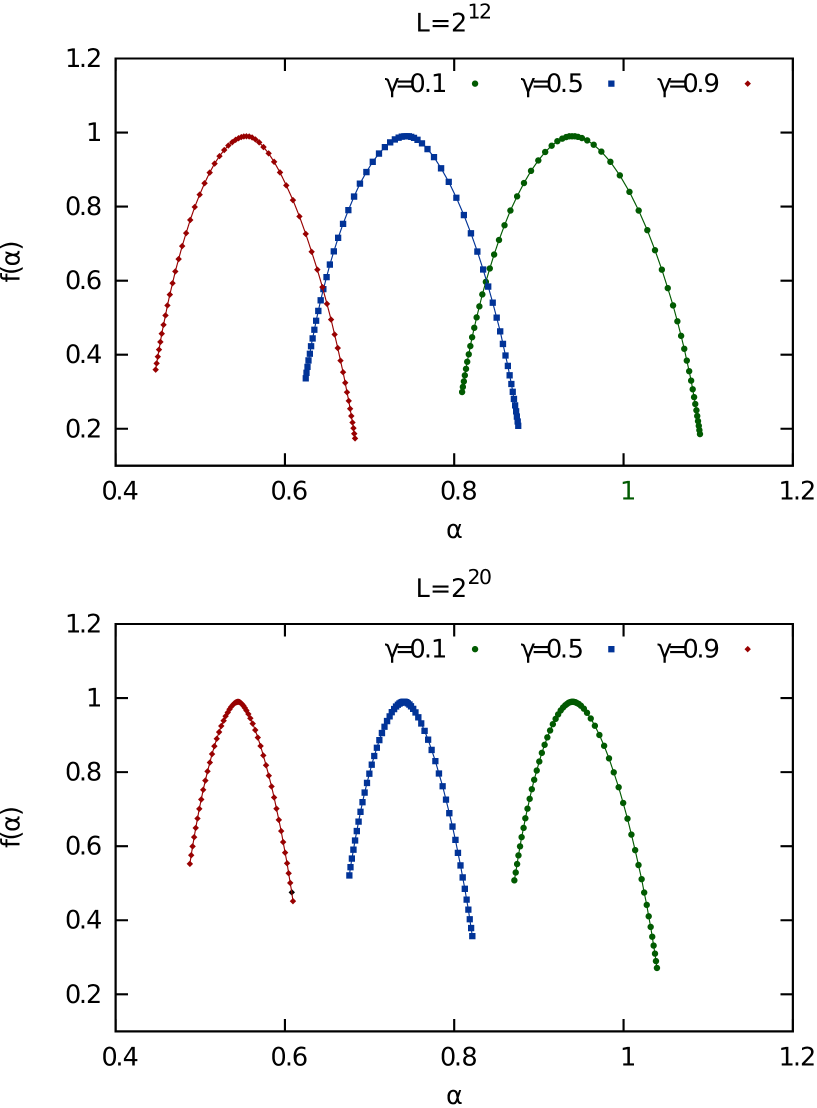

The examples of multifractal spectrum () for finite monofractal signals are shown in Fig.9. Three cases: for strongly autocorrelated, medium autocorrelated, and weakly autocorrelated signals are considered there for two distinct lengths of data: and .

As previously, the first step is to examine the characteristics obtained for randomly shuffled signal (). Fig.10 shows the minimal and maximal value of parameter revealing lack of dependence on . This proves again that shuffling was sufficient. The dependence of on obeys a power-law relation:

| (11) |

shown in Fig.11, with unknown constants and . The 95% confidence level is given by equation analogical to Eq.(7).

The edge values for as a function of are presented in Fig.12 for particular lengths and , to confront them with previous findings for . The linear dependence for all other lengths (not presented) is also observed. Once we repeat the same approach as in the previous section to dependence taking into account the second boundary condition , we arrive with the final formula describing the character of multifractal spectrum width (see Fig.13), similar to the one found in Eq.(10):

| (12) |

The values of fitted parameters are gathered in Table 2.

| 0.686 | 0.129 | 0.572 | 0.089 | 0.784 | 0.120 | 0.670 | 0.079 |

|---|

4 Concluding remarks

We have shown qualitatively and quantitatively how multifractality arises from the finite size effects and (or) from autocorrelations not changing with the time scale being formed by the specific autocorrelation exponent . This kind of multifractality, called by us ’multifractal noise’, should be clearly distinguished from the ’real multifractality’ caused by memory effects dependent on the time scale and thus leading to different scaling properties at various scales. We provided analytical formulas describing the multifractal noise threshold which turns out to be the power law function of time series length and the linear function of autocorrelation exponent . Our approach differs from the one presented in Ref.[19] where long memory in signals was produced from the induced power spectrum profile instead of the direct autocorrelation input between data resulting immediately from Eq.(3).

Two description methods for multifractality were considered, i.e. the generalized Hurst exponents and the multifractal spectrum analysis. In both cases multifractal residual effect in monofractal finite signals has been found. We have shown that this effect measured by the spread of generalized Hurst exponent or the width of multifractal spectrum grows linearly with autocorrelations level in time series and decays according to power-law with their length. We have estimated numerically the level of such multifractal noise and we captured it in simple analytical equations.

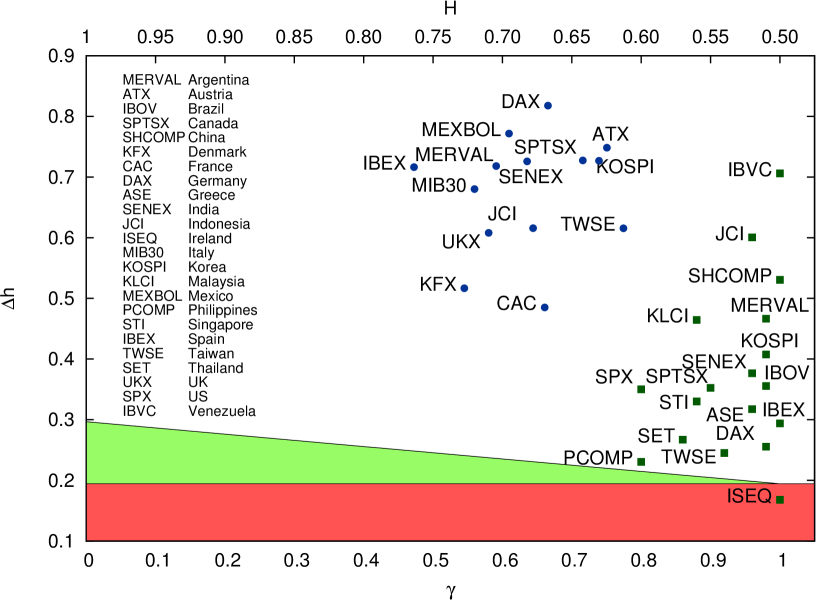

Finally, one should compare the obtained multifractal noise threshold with examples of the real multifractal data. We took them from finance because of common agreement that multifractality is a characteristic feature of financial markets. This problem is considered in Fig.14, where the simulated ’phase-like’ diagram for data length is shown, together with multifractal properties of various markets – both for price indices and for volatilities. The particular length has been chosen as the average length of available data for analyzed markets. The multifractal properties for price indices were taken from [27], once the respective features for volatilities were originally calculated by us for the purpose of this paper and are based on historical data available in web [28].

The multifractality for the volatility series is noticed. However, the presence of multifractality for the price index data is already not so obvious for all markets. One may find indices where multifractality comes indeed as a result of scaling properties changing with the time scale (e.g. Venezuela, Indonesia, China). Simultaneously, there are markets where the observed multifractality is generated mainly (e.g. Philippines, Taiwan, Germany) or even entirely (Ireland) by the finite size effects. In the case of Philippines, Taiwan, Thailand, Germany, Spain and Greece almost of multifractality in price indices is related to such an effect.

Thus, the multifractal properties of real financial data, may substantially (even in ) originate from the multifractal noise, what makes difficult in some cases to separate what main phenomenon is really responsible for the effects one observes. This confirms that multifractality is very tiny and delicate effect and one should be especially careful drawing far-reaching conclusions from the multifractal analysis in finance and in other areas. Our formulas are general enough to be applied also to other kind of real data in order to distinguish if and how their multifractal properties result from the pure multifractal origin.

References

- [1] S. Ghashghaie, W. Breymann, J. Peinke, P. Talkner, and Y. Dodge, Nature 381, 767 (1996).

- [2] R. N. Mantegna and H. E. Stanley, Nature 383, 587 (1996).

- [3] B. B. Mandelbrot, Sci. Am. 298, 70 (1999).

- [4] J.W. Kantelhardt, arXiv: 0804.0747v1 [phys.data-an].

- [5] Z. Eisler, J. Kertész, Physica A 343 (2004) 603.

- [6] H.G.E. Hentschel, I. Procaccia, Physica D 8 (1983) 435 .

- [7] T.C Halsey, M.H. Jensen, L.P. Kadanoff, I. Procaccia, B.I. Shraiman, Phys. Rev. A 33 (1983) 1141 .

- [8] K. Matia, Y. Ashkenazy, and H. E. Stanley, Europhys. Lett. 61, 422 (2003).

- [9] J. Kwapień, P. Oświȩcimka, and S. Drożdż, Physica A 350 (2005) 466 .

- [10] P. Oświȩcimka, J. Kwapień, and S. Drożdż, Physica A 347 (2005) 626 .

- [11] L. G. Moyana, J. de Souza, and S. M. D. Queiros, Physica A 371 (2006) 118 .

- [12] J. Jiang, K. Ma, and X. Cai, Physica A 378 (2007) 399 .

- [13] K. E. Lee and J. W. Lee, Physica A 383 (2007) 65 .

- [14] G. Lim, S. Kim, H. Lee, K. Kim, and D.-I. Lee, Physica A 386 (2007) 259 .

- [15] Z.-Y. Su, Y.-T.Wang, and H.-Y. Huang, J. Korean Phys. Soc. 54 (2009) 1395 .

- [16] P. Oświȩcimka, J. Kwapień, S. Drożdż, A.Z. Górski, R. Rak, Act. Phys. Pol. A 114 (2008) 3 .

- [17] Ł. Czarnecki, D. Grech, Act. Phys. Pol. A 117 (2010) 4 .

- [18] J.W. Kantelhardt, S.A. Zschiegner, E. Koscielny-Bunde, S. Havlin, A. Bunde, H.E. Stanley, Physica A 316 (2002) 87 .

- [19] Wei-Xing Zhou, arXiv:0912.4782v1 [q-fin.ST].

- [20] S. Drożdż, J. Kwapień, P. Oświȩcimka and R. Rak, Eur.Phys.Lett. 88 (2009) 60003, arXiv:0907.2866 [physics.data-an].

- [21] H.A. Makse, S. Havlin, M. Schwartz, H.E. Stanley, Phys.Rev. E 53 (1996) 2 .

- [22] T. Schreiber and A. Schmitz, Phys. Rev. Lett. 77 (1996) 635. .

- [23] J. Feder, Fractals, New York, Plenum Press (1988).

- [24] H.-O. Peitgen, H. Jürgens, D. Saupe, Chaos and Fractals, nd ed. Springer (2004).

- [25] H.E. Hurst, Trans. Am. Soc. Civ. Eng. 116 (1951) 770 .

- [26] J.W. Kantelhardt, E. Koscielny-Bunde, H.H.A. Rego, S. Havlin , A. Bunde Physica A 295 (2001) 441 .

- [27] L. Zunino, B.M. Tabak, A.Figliola, D.G. Pérez, M. Garavaglia, O.A. Rosso, Physica A 387 (2008) 6558

- [28] http://finance.yahoo.com