American and Bermudan options in currency markets with proportional transaction costs

Abstract

The pricing and hedging of a general class of options (including American, Bermudan and European options) on multiple assets are studied in the context of currency markets where trading is subject to proportional transaction costs, and where the existence of a risk-free numéraire is not assumed. Constructions leading to algorithms for computing the prices, optimal hedging strategies and stopping times are presented for both long and short option positions in this setting, together with probabilistic (martingale) representations for the option prices.

Keywords: American options, optimal stopping, proportional transaction costs, currencies.

MSC: 91G20, 91G60, 60G40.

1 Introduction

We consider the pricing and hedging of a wide class of options within the model of foreign exchange markets proposed by Kabanov [11], where proportional transaction costs are modelled as bid-ask spreads between currencies. This model has been well studied; see e.g. [12, 13, 27].

The results of this paper apply to any option that can be described in full by a payoff process together with an exercise policy specifying the circumstances in which it can be exercised at each date up to its expiration. This includes American, Bermudan and European options. For such options, we compute the ask price (seller’s price, upper hedging price) as well as the bid price (buyer’s price, lower hedging price), and derive probabilistic (martingale) representations for these prices. We also construct optimal superhedging trading strategies for the buyer and the seller, together with optimal stopping times consistent with the exercise policy.

American options are being traded and hedged in large volumes throughout financial markets where transaction costs in the form of bid ask spreads are commonplace. The theory of American options under transaction costs developed to-date does not fully address the practical significance of the pricing and hedging problem in that it offers non-constructive existence proofs and tackles the short (seller’s) position in American options only. This paper goes some way towards bridging the gap between the known theoretical results cited later in this introduction and practical considerations of being able to compute some prices, hedging strategies and stopping times for American options under transaction costs. In doing so this paper also provides alternative constructive proofs of the known results, and extends these results to both parties to the option contract, that is, not just the holder of a short position (the seller) but also to the party holding a long position (the buyer) in the option.

It is well known in complete models without transaction costs that the best stopping time for the holder of an American or Bermudan option is also the most expensive stopping time for the seller to hedge against, and that hedging against this particular stopping time protects the seller against all other stopping times. Chalasani and Jha [5] observed that this is no longer the case for American options in the presence of proportional transaction costs: to hedge against all (ordinary) stopping times, the seller must in effect be protected against a certain randomised stopping time (see Definition 2.5). Thus the optimal stopping times of the buyer and seller of an American option no longer coincide, and it may cost the seller more to hedge against all stopping times than to hedge against the best stopping time for the buyer. This is true in general for any option that allows more than one exercise time (i.e. any non-European option).

There is a geometrical explanation for this apparent lack of symmetry. For both parties to an option, the price, optimal stopping time and optimal superhedging strategy solve a linear optimization problem over the set of superhedging strategies. The superhedging strategies for the seller form a convex set. In contrast, each superhedging strategy for the buyer hedges against a specific stopping time, so that a convex combination of two superhedging strategies for different stopping times may no longer be a superhedging strategy for the buyer. Thus the pricing problem (4.2) for the seller is convex, whereas if the exercise policy allows more than one stopping time, then the pricing problem (4.9) for the buyer is a mixed integer programming problem that is generally not convex (not even in the friction-free case; for American options see [19]).

The linear optimization problems (4.2) and (4.9) both grow exponentially with the number of time steps, even for options with path-independent payoffs (see [6, 26] for results on European options). Various special cases of European and American options have been studied in binomial two-asset models with proportional transaction costs. The replication of European options has been well studied (see e.g. [1, 4, 18, 20]), and the first algorithm (with exponential running time) for computing the bid and ask prices for European options was established by Edirisinghe, Naik and Uppal [9]. In a similar technical setting, Kociński [14, 15] studied the exact replication of American options, Perrakis and Lefoll [21, 22] investigated the pricing of American call and put options, and Tokarz and Zastawniak [28] worked with general American options under small proportional transaction costs. Recently, Loehne and Rudloff [17] established an algorithm for finding the set of superhedging strategies for European (but not for American or Bermudan) options in a similar technical setting to the present paper.

The main contribution of this paper is to provide constructive and efficient algorithms for computing the option prices, optimal hedging strategies and stopping times for both the long and short positions in American-style options in multi-asset markets under proportional transaction costs. Another goal is to establish in a constructive manner probabilistic (martingale) representations for American-style options for both the seller’s (long) and buyer’s (short) positions in such options.

Previous work in this direction involves non-constructive representation theorems for the short position in American options. This includes the pioneering paper by Chalasani and Jha [5], who treated American options with cash settlement and no transaction costs at the time of settlement in a single-stock market model. Moreover, for American options in currency markets, Bouchard and Temam [3] established dual representations for the set of initial endowments that allow to superhedge the short position. Their work, based on a non-constructive existence argument, allows for a general setting based on an arbitrary probability space. Similar work has been carried out in a continuous time model [2, 7].

The convex duality methods deployed in these papers do not, however, lend themselves to studying hedging or pricing for the opposite party to an American option contract, namely the option’s buyer, as this involves an inherently non-convex optimisation problem. Ideas going beyond convex duality are necessary and are developed here.

The constructions and numerical algorithms put forward in the present paper call naturally for a discretisation. It is a reasonable compromise between admitting models based or arbitrary probability spaces and possibly continuous time (such work involves topological and functional analytic questions of theoretical interest, but non-constructive existence proofs) and being able to actually compute the prices, hedging strategies and stopping times (as demanded by the applied nature of the problem in hand), and the dual counterparts thereof.

The constructive results for American-style options in multi-asset markets under transaction costs are new. Similar questions were studied by Loehne and Rudloff [17] for European options, also in the discrete setting. Their results on European options are covered by the present work as a special case. In fact, even when specialised to European options, our results are still slightly more general as we are able to relax the robust no-arbitrage condition of Schachermayer [27] that was assumed in [17], and require just the weak no-arbitrage property (2.4) of Kabanov and Stricker [13].

The proofs of the main results (Theorems 4.4 and 4.10) include constructions of the sets of superhedging strategies and stopping times for both the buyer and seller, together with the approximate martingales and pricing measures involved in the martingale representations of both the bid and ask price of an option with general exercise policy (subject to mild regularity conditions) on multiple assets under proportional transaction costs in a general discrete time setting. Such constructions extend and improve upon each of the various special cases mentioned above, as well as the results we previously reported for European and American options in two-asset models [24, 25]. These constructions are efficient in that their running length grows only polynomially with the number of time steps when pricing options with path-dependent payoffs and exercise policies in recombinant tree models.

The paper is organised as follows. In Section 2 we fix the notation, specify the market model with transaction costs, and review various notions concerning convex sets and functions, randomised stopping times and approximate martingales. The notion of an exercise policy is introduced in Section 3. The main pricing and hedging results for the buyer and seller are presented in Section 4 as Theorems 4.4 and 4.10, and various special cases are discussed. Section 5 is devoted to the proof of Theorem 4.4 for the seller, while Theorem 4.10 is proved in Section 6. In Section 7 the constructions in Sections 5 and 6 are applied to two realistic examples. Appendix A gives the proof of a technical lemma used in the proof of Theorem 4.4.

2 Preliminaries and notation

2.1 Convex sets and functions

For any set , define

and define the cone generated by as

We say that a non-empty cone is compactly -generated if is compact, non-empty and .

Let denote the scalar product in . For any non-empty convex cone , denote by the polar of , i.e.

If is a non-empty closed convex cone, then is also a non-empty closed convex cone [23, Theorem 14.1].

The effective domain of any convex function is defined as

The epigraph of is defined as

The function is called proper if and for all .

Define the convex hull of any set as the smallest convex set containing . Define the convex hull of a finite collection of proper convex functions as the greatest convex function majorised by , equivalently

for each , where the infimum is taken over all and for such that

Also note that

The closure of a proper convex function is defined as the unique function whose epigraph is

| (2.1) |

If is not proper, then is defined as the constant function . A proper convex function is called closed if , equivalently if is closed.

Define the support function of a non-empty convex set as

The function is convex, proper and positively homogeneous. If is closed, then is closed [23, Theorem 13.2]. We shall make use of the identity

| (2.2) |

2.2 Proportional transaction costs in a currency market model

We consider a market model with assets (henceforth referred to as currencies following the terminology of Kabanov [11] and others) and discrete trading dates on a finite probability space with filtration . The exchange rates between the currencies are represented as an adapted matrix-valued process , where for any and the quantity is the amount in currency that needs to be exchanged in order to receive one unit of currency at time .

We assume without loss of generality that is trivial, that and that for all . Let be the collection of atoms (called nodes) of at any time . A node at time is called a successor of a node at time if . Denote the collection of successors of any node by .

We write for the family of -measurable -valued random variables, where for convenience . Throughout this paper we shall implicitly and uniquely identify random variables in with functions on , and we shall throughout adopt the notation

Writing for the family of non-negative random variables in , a portfolio is called solvent whenever it can be exchanged into a portfolio in without additional investment, i.e. if there exist -measurable random variables for such that

| (2.3) |

Here represents the number of units of currency obtained by exchanging currency . The solvency condition (2.3) can be written as

where is the convex cone in generated by the unit vectors , forming the canonical basis in and the vectors , . We refer to as the solvency cone. Observe that is a polyhedral cone and therefore closed.

A self-financing strategy is a predictable -valued process with initial value such that

Denote the set of all self-financing strategies by .

The model with transaction costs is said to satisfy the weak no-arbitrage property of Kabanov and Stricker [13] if

| (2.4) |

This formulation is formally different but equivalent to that of [13], and was introduced by Schachermayer [27], who called it simply the no-arbitrage property.

We have the following fundamental result.

Theorem 2.1 ([13, 27]).

The model satisfies the weak no-arbitrage property if and only if there exist a probability measure equivalent to and an -valued -martingale such that

| (2.5) |

Remark 2.2.

Condition (2.5) can equivalently be written as

If the model satisfies the weak no-arbitrage property, then is a non-empty polyhedral cone, and it is compactly -generated with

for all .

Definition 2.3 (Equivalent martingale pair).

A pair satisfying the conditions of Theorem 2.1 is called an equivalent martingale pair.

Denote the family of equivalent martingale pairs by . Let

for all .

We assume from here on that the model satisfies the weak no-arbitrage property, so that , equivalently for all .

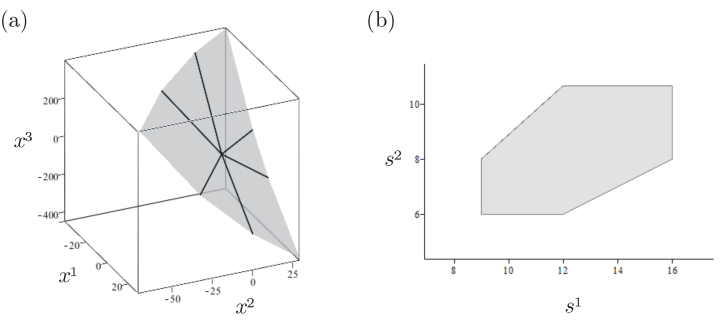

Example 2.4.

Consider three assets, where asset 3 is a cash account. Suppose that in a friction-free market assets 1 and 2 can be bought/sold, respectively, for and units of cash (asset 3). The friction-free exchange rate matrix would then be

Now assume that whenever an asset is exchanged into a different asset , transaction costs are charged at a fixed rate against asset , resulting in each off-diagonal exchange rate increased by a factor . If , the exchange rate matrix becomes

The cone consisting of solvent portfolios and the section , which generates the cone , are shown in Figures 1(a), (b), respectively.

2.3 Randomised stopping times

Definition 2.5 (Randomised stopping time).

A randomised (or mixed) stopping time is a non-negative adapted process such that

We write for the collection of all randomised stopping times.

Let be the set of (ordinary) stopping times. Any stopping time can be identified with the randomised stopping time defined by

for all . Here denotes the indicator function of .

For any adapted process and , define the value of at as

Moreover, define the processes and as

for all . Observe that is a predictable process since

whenever . For notational convenience define

| (2.6) |

Definition 2.6 (-approximate martingale pair).

For any the pair is called a -approximate martingale pair if is a probability measure and an adapted process satisfying

for all . If in addition is equivalent to , then is called a -approximate equivalent martingale pair.

Denote the family of -approximate martingale pairs by , and write for the family of -approximate equivalent martingale pairs. For an ordinary stopping time we write and and say that is a -approximate (equivalent) martingale pair whenever it is a -approximate (equivalent) martingale pair.

For any and define

Noting that , it follows that , and the weak no-arbitrage property implies that all these families are non-empty.

We have the following simple result.

Lemma 2.7.

Fix any , and let be any adapted -valued process. Then for any , any and any there exists a -approximate martingale pair such that

Proof.

The weak no-arbitrage property guarantees the existence of some . If , then the claim holds with and . If not, fix , let and

∎

3 Exercise policies

In the next section and onwards we will consider the pricing and hedging of an option that may only be exercised in certain situations, namely at any time the owner of the option is only allowed to exercise on a subset of . This setting contains a wide class of options, for example:

-

•

A European option corresponds to and for all .

-

•

A Bermudan option with exercise dates corresponds to

(3.1) -

•

An American option corresponds to for all .

-

•

An American-style option with random expiration date corresponds to for all .

The introduction of exercise policies allows the unification of results for specific types of options, most notably European and American ones. More immediately, we shall use exercise policies as a theoretical tool in Section 6 when deriving the pricing and hedging theorem for the buyer of an option with a general exercise policy from the corresponding results for the seller of a related European-style option.

An exercise policy is formally defined as follows.

Definition 3.1 (Exercise policy).

An exercise policy is a sequence of subsets of such that for all ,

| (3.2) |

and

| (3.3) |

The condition is consistent with the intuitive notion of allowing the buyer to make exercise decisions based on information available at time . Condition (3.2) is consistent with allowing the buyer to determine on the basis of information currently available whether or not there are future opportunities for exercise. Condition (3.3) ensures that there is at least one opportunity to exercise the option in each scenario.

Define the sequence of sets associated with an exercise policy as

for all . For each , the set contains those scenarios in which it is possible to exercise the option in at least one of the time steps . Write for convenience.

For an exercise policy , define the sets of randomised and ordinary stopping times consistent with as

The following result specifies the relationship between , and .

Proposition 3.2.

For all ,

Proof.

For the first equality, it is clear from the definition of that

We now show for any that there exists a stopping time such that . Define

so that is a sequence of mutually disjoint sets in with and for all . Moreover it is a partition of since

The random variable

is therefore a stopping time in with as required.

The second equality holds because

for all . ∎

4 Main results and discussion

An option consists of an adapted -valued payoff process and an exercise policy . The seller delivers the portfolio to the buyer at a stopping time chosen by the buyer among the stopping times consistent with .

4.1 Pricing and hedging for the seller

Consider the hedging and pricing problem for the seller of the option . A self-financing trading strategy is said to superhedge for the seller if

| (4.1) |

Definition 4.1 (Ask price).

The ask price or seller’s price or upper hedging price of at time in terms of any currency is defined as

| (4.2) |

The interpretation of the ask price is that an endowment of at least units of asset at time would enable an investor to settle the option without risk. A superhedging strategy for the seller is called optimal if .

Our main aims are to compute the option price algorithmically and to find a probabilistic dual representation for it, to construct the set of initial endowments that allow the seller to superhedge, and to construct an optimal superhedging strategy for the seller. To this end, consider the following construction.

Construction 4.2.

For all , let

| (4.3) |

Define

For , let

| (4.4) | ||||

| (4.5) |

For each the set is the collection of portfolios in that allows the seller to settle the option at time . We shall demonstrate in Proposition 5.2 that for each the sets , and have natural interpretations as collections of portfolios that are of importance to the seller of the option. The set is the collection of portfolios at time that allow the seller to settle the option in the future (at time or later). The set consists of those portfolios that may be rebalanced at time into a portfolio in , and consists of all portfolios that allow the seller to remain solvent after settling the option at time or any time in the future.

Remark 4.3.

On , where exercise is allowed, the set is a translation of , so it is non-empty and polyhedral. It is then straightforward to show by backward induction that the following holds for all :

-

•

, , are all non-empty.

-

•

on .

-

•

on and on .

-

•

and are polyhedral on and is polyhedral on .

Note in particular that the non-empty set is polyhedral since .

The main pricing and hedging result for the seller reads as follows.

Theorem 4.4.

The set is the collection of initial endowments allowing the seller to superhedge , and

where is the support function of . An optimal superhedging strategy for the seller can be constructed algorithmically, and so can a randomised stopping time and -approximate martingale pair such that

| (4.6) |

Any stopping time and -approximate martingale pair satisfying (4.6) are called optimal for the seller of . Note that the optimal superhedging strategy, stopping time and approximate martingale pair are not unique in general.

The proof of Theorem 4.4 appears in Section 5, together with details of the construction of the optimal stopping time and approximate martingale pair for the seller. An optimal superhedging strategy can be found using the following construction with initial value .

Construction 4.5.

Take as given. For all choose any

| (4.7) |

4.2 Pricing and hedging for the buyer

Consider now the pricing and hedging problem for the buyer of the option . A pair consisting of a self-financing trading strategy and a stopping time superhedges for the buyer if

| (4.8) |

Definition 4.6 (Bid price).

The bid price or buyer’s price or lower hedging price of at time in terms of currency is defined as

| (4.9) |

The interpretation of the bid price is that is the largest amount in currency that can be raised at time by the owner of the option by setting up a self-financing trading strategy with the property that it leaves him in a solvent position after exercising . A superhedging strategy for the buyer is called optimal if .

Just as in the seller’s case, the aims are to algorithmically compute , to establish a probabilistic representation for it, to find the set of initial endowments allowing superhedging for the buyer, and to construct an optimal superhedging strategy for the buyer. The key to this is the following construction.

Construction 4.7.

For all , let

Define

For , let

| (4.10) |

For each the set is the collection of portfolios in that allows the buyer to be in a solvent position after exercising the option at time . For the set is the collection of portfolios at time that allow the buyer to superhedge the option in the future (at time or later), and consists of those portfolios that may be rebalanced at time into a portfolio in . The set consists of all portfolios that allow the buyer to remain solvent after exercising the option at time or any time in the future.

Remark 4.8.

Construction 4.7 differs from Construction 4.2 in two respects. Firstly, the payoff is treated differently because it is delivered by the seller and received by the buyer. Secondly, there is a union of sets in (4.10) where there is an intersection in (4.5). This encapsulates the opposing positions of the seller and the buyer: any portfolio held by the seller at time must enable him to settle the option at time or later, whereas any portfolio held by the buyer needs to enable him to achieve solvency by exercising the option, either at time or at some point in the future. The union in (4.10) also illustrates the fact that the pricing problem for the buyer is not convex.

Remark 4.9.

On the set is polyhedral and non-empty. It is possible to show the following by backward induction on :

-

•

on .

-

•

on and on .

-

•

and on , and on can be written as a finite union of non-empty closed polyhedral sets (but , and are not convex in general).

Note in particular that since , the last item applies to , so it is non-empty and closed.

Here is the main pricing and hedging theorem for the buyer.

Theorem 4.10.

The set is the collection of initial endowments allowing superhedging of by the buyer, and

An optimal superhedging strategy with

can be constructed algorithmically, and so can a -approximate martingale pair such that

| (4.11) |

A -approximate martingale pair is called optimal for the buyer if it satisfies (4.11). The proof of this theorem appears in Section 6, together with full details of the construction of an optimal -approximate martingale pair. An optimal superhedging strategy can be obtained by means of the following construction with initial choice and with .

Construction 4.11.

Take as given, and define

For , choose any

| (4.12) |

and define

| (4.13) |

4.3 Special cases

4.3.1 European options

Consider a European-style option that offers the payoff at some given stopping time (in particular, we can have for an ordinary European option with expiry time ). Here is the set of -valued -measurable random variables. In our framework the payoff of such an option is the adapted process with

and its exercise policy is given by

It follows that and . For clarity we denote this European option by instead of .

Observe that a trading strategy superhedges the option for the seller if and only if superhedges for the buyer. It also follows directly from (4.2) and (4.9) that

Thus the pricing and hedging problems for the buyer and seller of a European-style option are symmetrical. In particular, this means that the pricing problem for the buyer is convex, and the hedging problem for the seller does not involve any randomised stopping times.

Constructions 4.2 and 4.7 can be simplified considerably due to the simple structure of the exercise policy. Noting that at each time step we have on and on , Construction 4.2 can now be rewritten as follows for each :

| (4.14) | |||||

| (4.15) |

where the auxiliary sets are omitted, for simplicity. Theorem 4.4 gives the ask price of as

| (4.16) |

since and . A similar simplification is possible for the buyer; note that , and are convex for all . The bid price of is

which is consistent with Theorem 4.10.

Consider the special case , which corresponds to a classical European option. The simplified construction (4.14)–(4.15) leads to the same set of superhedging portfolios as in [17, Theorem 2]. The representations for the bid and ask prices can be simplified further by noting that

For any , the adapted process defined by

is a -martingale such that , and

Thus the supremum in (4.16) need only be taken over , and it follows that

This result extends [1, 9, 24] in two-asset models. Its conclusions are technically closest to the non-constructive results for currency models in [8, 13].

4.3.2 Bermudan options

The exercise policy for a Bermudan option with payoff process that can be exercised at given times is defined in (3.1). The collections of ordinary and randomised stopping times consistent with this exercise policy are

Note that and are closed non-empty strict subsets of whenever . Theorems 4.4 and 4.10 can then be used to compute and . Moreover optimal superhedging strategies for the seller and for the buyer can be constructed algorithmically.

4.3.3 American options

Consider an American option with expiration date that offers the payoff at a stopping time chosen by the buyer. The exercise policy satisfies for all , and the sets of stopping times consistent with the exercise policy are

Denote this American-style option by instead of . Theorems 4.4 and 4.10 give the ask and bid prices as

This directly extends [5, 25, 28] for two-asset models. In the context of currency models, this is consistent with the results in [3] for the seller.

Remark 4.12.

In this work it is assumed that trading strategies are rebalanced at each time instant only after it becomes known that the option is not to be exercised at that time instant. In their work on pricing American options for the seller, Bouchard and Temam [3] follow a different convention by assuming that the portfolios in a hedging strategy must be rebalanced before exercise decisions become known. The method in this paper also applies to their case, provided that the order of the operations in (4.4) and (4.5) is interchanged, i.e. replace these equations by

Ask prices obtained in this way are in general higher than the ask prices presented above. This is because a superhedging strategy for the seller in this setting will also superhedge under our definition, but the converse is not always true. Because of this, superhedging as we have defined above is easier to achieve, and it is therefore more natural for traders to follow than the approach of Bouchard and Temam.

5 Pricing and hedging for the seller

This section is devoted to the proof of Theorem 4.4. Recall that a trading strategy superhedges the option for the seller if (4.1) holds. In view of Proposition 3.2, this is equivalent to

or

| (5.1) |

We now have the following result.

Proposition 5.1.

The ask price defined in (4.2) is finite and

| (5.2) | ||||

| (5.3) |

Proof.

We show by backward induction below that if , and with superhedges for the seller, then

| (5.4) |

for all . The property then gives

and the inequality (5.2) is immediate. The equality (5.3) follows directly from Lemma 2.7. The property holds true since and has a trivial superhedging strategy for the seller, given by where

| (5.5) |

for all and .

Observe that for any we have on , and on we have , so that since (see Definition 2.6). This means that

To prove (5.4) by backward induction, first note that at time ,

Suppose for some that

The self-financing condition together with (see Definition 2.6) gives

Combining this with the inductive assumption, we obtain

This concludes the inductive step. ∎

The next result shows that is the set of initial endowments of self-financing trading strategies that allow the seller to superhedge . It also links Construction 4.2 with the problem of computing the ask price in (4.2).

Proposition 5.2.

Proof.

We establish that superhedges for the seller if and only if for all . Equation (5.6) then follows directly from (4.2). The minimum in (5.6) is attained because is polyhedral, hence closed, and is finite by Proposition 5.1.

If superhedges for the seller, then it satisfies (5.1), and clearly . For any suppose inductively that . We have since is predictable, and since it is self-financing. Thus , which concludes the inductive step.

For the converse, fix any and apply Construction 4.5. We now show by induction that the resulting process satisfies for all . For any , suppose by induction that . This means that , and so . By (4.7) we have both and , which concludes the inductive step. The process that has been constructed is clearly predictable, self-financing and satisfies (5.1) since for all . Thus it superhedges for the seller, which establishes the correctness of Construction 4.5.

It is now straightforward to see that Construction 4.5 with the initial choice results in an optimal superhedging strategy for the seller of . ∎

Consider now the following result, which will be proved later in this section.

Proposition 5.3.

There exist , such that

| (5.7) |

where is the support function of .

Proof of Theorem 4.4.

Note from the proof above that the randomised stopping time and -approximate martingale pair of Proposition 5.3 are optimal for the seller.

The remainder of this section is devoted to establishing Proposition 5.3. For all , let , , , be the support functions of , , , , respectively.

Remark 5.4.

Proposition 5.3 depends on the following technical result.

Lemma 5.5.

-

(a)

For all and we have

(5.8) (5.9) -

(b)

Fix any and .

-

(i)

If , then

(5.10) and . Moreover, for each there exist , and such that

-

(ii)

If , then

and .

-

(iii)

If , then

and is a compactly -generated cone.

-

(iv)

If , then

-

(i)

-

(c)

For each and with , we have

(5.11) and is a compactly -generated cone. Moreover, for every there exist and for each such that

Proof of Proposition 5.3.

We construct the process by backward recursion, together with auxiliary adapted processes , , and predictable . Fix any .

As , Lemma 5.5(b) ensures that is non-empty and compact, and there exists such that

| (5.12) |

Note that is an appropriate starting value for the recursion below since .

For any , suppose that is an -measurable random variable such that on and on . For any we now construct , and such that

| (5.13) |

There are four possibilities:

- •

- •

- •

- •

Note that on and on . For any and we now construct and such that

| (5.17) | ||||

| (5.18) |

There are two possibilities:

- •

- •

This concludes the recursive step.

The randomised stopping time is defined by and

for . It is clear from the construction that on for all , which implies that . Observe also that

for all ; recall that by definition. It follows from (5.13) that

for all . Equations (5.8) and (5.15) give

| (5.21) |

Since on , equations (5.14) and (5.16) may be combined with (5.8) to yield

| (5.22) |

It is possible to show by backward induction that

| (5.23) |

for all . At time this follows from the notational conventions and . Suppose that (5.23) holds for some . Then

which concludes the inductive step.

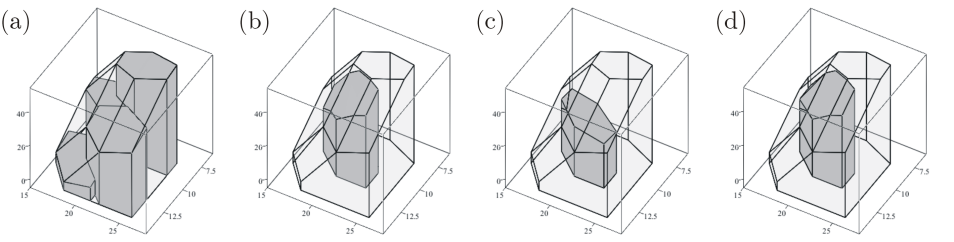

Example 5.6.

Consider a single-step model with four nodes at time , that is, , and three assets. We take asset 3 to be a cash account with zero interest rate, take the cash prices of assets 1 and 2 in a friction-free market in Table 1, and introduce transaction costs at the rate in a similar manner as in Example 2.4, with the matrix-valued exchange rate process

for . Consider the American option with payoff process in Table 1 in this model; its exercise policy is .

Construction 4.2 is formulated in terms of the convex sets , , , , but it is easier to visualise it by drawing the support functions , , , of , , , or indeed the sections , , , , which are shown in Figure 2 for the above single-step model with transaction costs. Observe that all the polyhedra in Figure 2 are unbounded below, but have been truncated when drawing the pictures.

The construction proceeds as follows:

- •

- •

- •

- •

- •

The ask price of the American option is the maximum of ; see Theorem 4.4. The polyhedron has vertices:

and its highest point turns out to be at . This is the ask price of the American option.

6 Pricing and hedging for the buyer

Recall that a pair consisting of a self-financing trading strategy and stopping time superhedges the option for the buyer if (4.8) holds, equivalently if .

The next result shows that the set given by Construction 4.7 is the collection of initial endowments allowing the buyer to superhedge , and that it can be used to compute the bid price directly.

Proposition 6.1.

Proof.

We show below that if and only if there exists a superhedging strategy for the buyer of with and

| (6.2) |

The two representations of are equivalent since if superhedges for the buyer and

then also superhedges for the buyer. Once the result for is established, equation (6.1) follows directly from (4.9). The minimum is attained because is closed and is finite.

Suppose that superhedges for the buyer and satisfies (6.2). We show by backward induction on that on for all . At time this is trivial because . For any , suppose that on . Since on , this means that on . On we then have as , and because of the self-financing property. However on because of (6.2), and so on , which concludes the inductive step. Finally, if and if , and therefore .

Conversely, we can use Construction 4.11 to produce sequences and from any initial point . We shall verify that is a predictable process and is a stopping time. For any suppose by induction that is -measurable and is a stopping time (and observe that for these conditions are satisfied). Then and is -measurable, which implies that is -measurable. We also have by (4.12). It follows that is -measurable. To show that is a stopping time, we need to verify that for each. For any this is satisfied because , and for any we have . It remains to check for that . We have and because , we only need to observe that belongs to . This is so because and since has already been shown to be -measurable and therefore -measurable. This completes the induction argument. Moreover, observe from (4.12) that for all , that is, is a self-financing strategy. Combined with predictability, it means that . Furthermore, observe that . This is so by (4.12) since given that . Since we already know that is a stopping time, we can conclude that .

Next we show by induction that on for all . This is clearly so for . Suppose that on for some . By (4.12), on we have , and so by the induction hypothesis. Moreover, on we have , which can be written as . This shows that on , completing the induction step. In particular, it follows that .

Finally, we shall see that . We already know that . We also know that on , so

for any . It means that .

We have verified that that is a superhedging strategy for the buyer of . To complete the proof observe that on we have and by (4.13), which implies that . ∎

Let us now establish Theorem 4.10.

Proof of Theorem 4.10.

Note first that is a superhedging strategy for the buyer of if and only if it is a superhedging strategy for the seller of the European-style option with payoff and expiration date of Section 4.3.1. Denoting the European-style option by , the bid price of defined in (4.9) can be written as

| (6.3) |

The equality (6.3) shows that is finite because is finite and the ask prices are all finite by Proposition 5.1. Equation (4.16) in conjunction with Lemma 2.7 gives

| (6.4) |

and so

An optimal superhedging strategy for the buyer of may be constructed using the second half of the proof of Proposition 6.1 with . Such a strategy superhedges for the seller, so

whence

| (6.5) |

Thus the construction in the proof of Proposition 5.3 of the optimal stopping time and approximate martingale pair for the seller of the European option can be used to construct and such that

It is moreover clear from the construction in the proof of Proposition 5.3 and the structure of the exercise policy of that . Thus and

as required. ∎

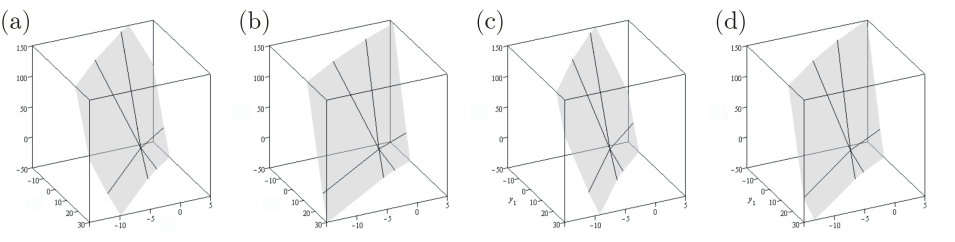

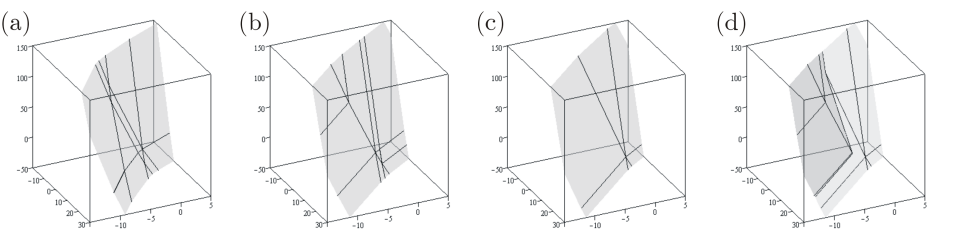

Example 6.2.

Consider the computation of the bid price of the American option in Example 5.6 using Construction 4.7. In contrast to the seller’s case, some of the sets involved in this construction may fail to be convex, and there is no convex dual representation like that for the seller in Figure 2. To visualise the sets we just draw their boundaries.

The construction for the buyer proceeds as follows:

-

•

The first step is to compute in each of the four scenarios; see Figure 3.

-

•

Then we take the intersection of , , , to obtain . This set appears in Figure 4(a).

-

•

Next, the set in Figure 4(b) is the sum of and the solvency cone .

-

•

Then we take , which appears in Figure 4(c).

-

•

Finally, the set is the union of and . It appears in Figure 4(d); the dark gray region belongs to (but not ), and the light gray region belongs to (but not ).

The unbounded and non-convex set has vertices. Of these, the point is a vertex of , the points and are vertices of , and

are common to both and . The lowest number such that is . By Theorem 4.10, the bid price of the option is .

7 Numerical examples

We now use the methods developed in this paper to study two examples with a realistic flavour in some detail.

Example 7.1.

Consider a binomial tree model with two risky assets. We assume a notional friction-free exchange rate between the two assets satisfying

for , where is given, and where is a sequence of independent identically distributed random variables taking the values

each with positive probability. Here , is the volatility of the exchange rate, is the depreciation rate of the first asset in terms of the second, the time horizon is year and is the number of steps in the model. We further assume that for the actual exchange rates between the assets are

where is the transaction cost rate. A portfolio is solvent at time if and only if

| (7.1) |

In friction-free models the owner of an option benefits from exercising it if and only if the option payoff can be converted into a non-negative number of units of one of the assets (and for this reason it is standard practice to represent options in friction-free models as non-negative cash payoffs). In the presence of transaction costs, where assets are not freely exchangeable, the situation is no longer so clear-cut, since the benefit from receiving a payoff consisting of a portfolio of assets depends greatly on the current position held in the underlying assets at the time that the payoff becomes available. Motivated by the work of [22], we make no assumption on the form of the payoff itself but award the owner of an option the right to not exercise the option at all. This is done by formally adding an extra time step in the model and setting the option payoff at that time to be zero.

Consider an American call option on the second asset with expiration date , strike and physical delivery. This corresponds to the payoff process with

for and . We say that the option is in the money at time if is a solvent portfolio at time , and out of the money if it isn’t. An implementation in C++ of Constructions 4.2 and 4.7 (see also Section 4.3.3) gives the ask and bid prices as

It is interesting to note that the optimal stopping times for the buyer and seller of the American call option are by no means unique, and also that the sets of optimal stopping times for the buyer and seller differ. To see this, consider the two scenarios and depicted in Figure 5. The asset price histories associated with and coincide up to time step . In scenario , the option is in the money at all times after step , whereas in scenario the option moves out of the money at time step and stays out of the money until maturity.

Consider first the superhedging problems for the seller of the American call option in these two scenarios. The optimal superhedging strategy for the seller can be constructed as in the proof of Proposition 5.2 from an initial endowment of ; see Figure 6. The optimal stopping time for the seller can be constructed as in the proof of Proposition 5.3; see Figure 7.

In scenario , where the option matures in the money, the optimal superhedging strategy for the seller converges to the option payoff; in particular, it becomes a static strategy for in this scenario. This coincides with the earliest time instant when the optimal stoping time becomes non-zero ( becomes less than ). Figure 7 depicts one possibility, but note that the optimal stopping time for the seller is highly non-unique on this path.

In scenario , where the option matures out of the money, the optimal superhedging strategy for the seller converges to zero; in particular for . This feature results from the need for the seller to remain solvent in the event that the buyer never exercises the option, which is likely if the option is both close to maturity and out of the money. The amount of trading required to transform the asset holdings in scenario from a superhedging to a solvent position over the latter part of the model attracts high transaction costs, with the result that the optimal stopping time for the seller, shown in Figure 7, corresponds to the buyer never exercising the option.

Consider now the superhedging and optimal exercise problems for the buyer of the American call. The optimal superhedging strategy and optimal stopping time can be constructed as in the last part of the proof of Proposition 6.1. The values of the optimal superhedging strategy in scenarios and are depicted in Figure 8.

The construction in the proof of Proposition 6.1 gives the optimal exercise time for the buyer in these scenarios as

At first glance this appears to be contrary to the received wisdom that it is never optimal to exercise an American call early. There is however no contradiction; it is rather the case that the optimal exercise time is not unique and this particular construction returns the earliest optimal stopping time. In particular, recall that the optimal stopping time constructed in Proposition 6.1 is the first stopping time at which the buyer can exercise the option and remain solvent, i.e.

where is given by (7.1). The values of in scenarios and appear in Figure 9, which confirms why the first optimal exercise time in these scenarios should be .

Example 7.2.

Consider a model with three currencies and steps with time horizon based on the two-asset recombinant Korn-Muller model [16] with Cholesky decomposition, that is, consider the process with

for , where is the step size and , and where is a sequence of independent identically distributed random variables taking the values

each with positive probability. Here , and . The exchange rates with transaction costs are modelled as

for and , where .

The pricing and hedging constructions of Section 4 was implemented by means of the Maple Convex package [10] for an American put option with physical delivery on a basket containing one unit each of the first two currencies and with strike in the third currency, i.e.

for . As in the previous example we allow for the possibility that the option holder may refrain from exercising by adding an additional time step and taking . Constructions 4.2 and 4.7 give the ask and bid prices of this option in the three currencies as

Let us now use Constructions 4.5 and 4.11 to compute the hedging strategies for the buyer and seller in the scenario corresponding to the path

Table 2 gives the resulting strategy for the seller starting from the initial endowment , with the bullet in each graph representing . For the set has only one element, which becomes . For we have and so it was natural to let to avoid trading (and the associated transaction costs). For the choice of is no longer unique; the choice in Table 2 avoids trading (and the associated transaction costs) but any other element of would have been acceptable in each case.

| 0 | ![[Uncaptioned image]](/html/1108.1910/assets/num2calZa0.png) |

|||

| 1 | ![[Uncaptioned image]](/html/1108.1910/assets/num2calZa1.png) |

|||

| 2 | ![[Uncaptioned image]](/html/1108.1910/assets/num2calZa2.png) |

![[Uncaptioned image]](/html/1108.1910/assets/num2inta2.png) |

||

| 3 | ![[Uncaptioned image]](/html/1108.1910/assets/num2calZa3.png) |

![[Uncaptioned image]](/html/1108.1910/assets/num2inta3.png) |

||

| 4 | ![[Uncaptioned image]](/html/1108.1910/assets/num2calZa4.png) |

N/A |

Table 3 gives the optimal strategy for the buyer starting from the initial endowment along the same path (omitted to save space). Again the bullet in each graph represents . Since we have , which reflects that it is in the buyer’s best interest to wait rather than exercise the option at time . Since we have , which means that in this path it is optimal to exercise the option at time . Construction 4.11 completes the strategy by formally setting and , but in practice a market agent exercising the option at time would create the portfolio

and liquidate it immediately (for example, into units of currency ).

| ? | |||||

|---|---|---|---|---|---|

![[Uncaptioned image]](/html/1108.1910/assets/num2calZb0.png) |

No | ||||

![[Uncaptioned image]](/html/1108.1910/assets/num2calZb1.png) |

Yes | 1 | N/A | ||

| 2–4 | N/A | N/A | 1 | N/A |

Appendix A Appendix: Proof of Lemma 5.5

Lemma A.1.

Fix some , and let be non-empty closed convex sets in such that is compactly -generated for all . Define ; then

and for each there exist and with for all such that

The cone is moreover compactly -generated and

| (A.1) |

Proof.

Let . Then see [23, Corollary 16.5.1]. Since is proper it follows that is proper and

| (A.2) |

by (2.1), so that .

For any , the compact -generation of means that is compact and non-empty. Thus the positive homogeneity of guarantees the existence of a closed proper convex function with compact such that is generated by , i.e.

Let ; then

is compact [23, Corrolary 9.8.2]. Moreover, is closed and proper, and for each there exist and such that for all and

| (A.3) |

see [23, Corollary 9.8.3] (the common recession function is since is compact for all ).

The paper concludes with the proof of Lemma 5.5.

Proof of Lemma 5.5.

For each , since is a cone, the support function of is

| (A.5) |

Thus , and so is compactly -generated.

For any we have on , together with

for on [23, p. 113]. Similarly,

Equalities (5.8) and (5.9) then follow from (2.2) and (A.5).

We now turn to claims (b) and (c). Note first that the sets , , and are non-empty for all . This is easy to check by taking the trivial superhedging strategy for the seller defined by (5.5) and following the backward induction argument in the proof of Proposition 5.2.

We show below by backward induction that is compactly -generated on While doing so we will establish claims (b) and (c) for all . At time , using and (4.3), the set is compactly -generated on , while on . This establishes claim (b) for since .

At any time , suppose that is compactly -generated on . For any there are now two possibilities:

- •

- •

In summary, we have shown that is compactly -generated whenever

This concludes the inductive step, and completes the proof of Lemma 5.5. ∎

References

- [1] Bensaid, B., Lesne, J.P., Pagès, H., Scheinkman, J.: Derivative asset pricing with transaction costs. Mathematical Finance 2, 63–86 (1992)

- [2] Bouchard, B., Chassagneux, J.F.: Representation of continuous linear forms on the set of ladlag processes and the pricing of American claims under proportional transaction costs. Electronic Journal of Probability 14, 612–632 (2009)

- [3] Bouchard, B., Temam, E.: On the hedging of American options in discrete time markets with proportional transaction costs. Electronic Journal of Probability 10, 746–760 (2005)

- [4] Boyle, P.P., Vorst, T.: Option replication in discrete time with transaction costs. The Journal of Finance XLVII(1), 347–382 (1992)

- [5] Chalasani, P., Jha, S.: Randomized stopping times and American option pricing with transaction costs. Mathematical Finance 11(1), 33–77 (2001)

- [6] Chen, G.Y., Palmer, K., Sheu, Y.C.: The least cost super replicating portfolio in the Boyle-Vorst model with transaction costs. International Journal of Theoretical and Applied Finance 11(1), 55–85 (2008)

- [7] De Vallière, F., Denis, E., Kabanov, Y.: Hedging of American options under transaction costs. Finance and Stochastics 13, 105–119 (2009)

- [8] Delbaen, F., Kabanov, Y.M., Valkeila, E.: Hedging under transaction costs in currency markets: A discrete-time model. Mathematical Finance 12, 45–61 (2002)

- [9] Edirisinghe, C., Naik, V., Uppal, R.: Optimal replication of options with transactions costs and trading restrictions. The Journal of Financial and Quantitative Analysis 28(1), 117–138 (1993)

- [10] Franz, M.: Convex—a Maple package for convex geometry (2009). URL http://www.math.uwo.ca/$∼$mfranz/convex/

- [11] Kabanov, Y.M.: Hedging and liquidation under transaction costs in currency markets. Finance and Stochastics 3, 237–248 (1999)

- [12] Kabanov, Y.M., Rásonyi, M., Stricker, C.: No-arbitrage criteria for financial markets with efficient friction. Finance and Stochastics 6, 371–382 (2002)

- [13] Kabanov, Y.M., Stricker, C.: The Harrison-Pliska arbitrage pricing theorem under transaction costs. Journal of Mathematical Economics 35, 185–196 (2001)

- [14] Kociński, M.: Optimality of the replicating strategy for American options. Applicationes Mathematicae 26(1), 93–105 (1999)

- [15] Kociński, M.: Pricing of the American option in discrete time under proportional transaction costs. Mathematical Methods of Operations Research 53, 67–88 (2001)

- [16] Korn, R., Müller, S.: The decoupling approach to binomial pricing of multi-asset options. Journal of Computational Finance 12(3), 1–30 (2009)

- [17] Löhne, A., Rudloff, B.: An algorithm for calculating the set of superhedging portfolios and strategies in markets with transaction costs (2011). URL http://arxiv.org/abs/1107.5720

- [18] Palmer, K.: A note on the Boyle-Vorst discrete-time option pricing model with transactions costs. Mathematical Finance 11(3), 357–363 (2001)

- [19] Pennanen, T., King, A.J.: Arbitrage pricing of American contingent claims in incomplete markets - a convex optimization approach. Stochastic Programming E-Print Series 14 (2004). URL http://edoc.hu-berlin.de/docviews/abstract.php?id=26772

- [20] Perrakis, S., Lefoll, J.: Derivative asset pricing with transaction costs: An extension. Computational Economics 10, 359–376 (1997)

- [21] Perrakis, S., Lefoll, J.: Option pricing and replication with transaction costs and dividends. Journal of Economic Dynamics and Control 24, 1527–1561 (2000)

- [22] Perrakis, S., Lefoll, J.: The American put under transactions costs. Journal of Economic Dynamics and Control 28, 915–935 (2004)

- [23] Rockafellar, R.T.: Convex Analysis. Princeton Landmarks in Mathematics and Physics. Princeton University Press (1996)

- [24] Roux, A., Tokarz, K., Zastawniak, T.: Options under proportional transaction costs: An algorithmic approach to pricing and hedging. Acta Applicandae Mathematicae 103(2), 201–219 (2008). DOI 10.1007/s10440-008-9231-5

- [25] Roux, A., Zastawniak, T.: American options under proportional transaction costs: Pricing, hedging and stopping algorithms for long and short positions. Acta Applicandae Mathematicae 106, 199–228 (2009). DOI 10.1007/s10440-008-9290-7

- [26] Rutkowski, M.: Optimality of replication in the CRR model with transaction costs. Applicationes Mathematicae 25(1), 29–53 (1998)

- [27] Schachermayer, W.: The fundamental theorem of asset pricing under proportional transaction costs in finite discrete time. Mathematical Finance 14(1), 19–48 (2004)

- [28] Tokarz, K., Zastawniak, T.: American contingent claims under small proportional transaction costs. Journal of Mathematical Economics 43(1), 65–85 (2006)