Sensitivities via Rough Paths

Abstract.

Motivated by a problematic coming from mathematical finance, this paper is devoted to existing and additional results of continuity and differentiability of the Itô map associated to rough differential equations. These regularity results together with Malliavin calculus are applied to sensitivities analysis for stochastic differential equations driven by multidimensional Gaussian processes with continuous paths, especially fractional Brownian motions. Precisely, in that framework, results on computation of greeks for Itô’s stochastic differential equations are extended. An application in mathematical finance, and simulations, are provided.

Key words and phrases:

Rough paths, Rough differential equations, Malliavin calculus, Sensitivities, Mathematical finance, Gaussian processesAcknowledgements. Many thanks to Laure Coutin and Laurent Decreusefond for their advices. That work was supported by ANR Masterie.

1. Introduction

Motivated by a problematic coming from mathematical finance, this paper is devoted to existing and additional results of continuity and differentiability of the Itô map associated to rough differential equations (RDEs). These regularity results together with Malliavin calculus are applied to sensitivities analysis for stochastic differential equations (SDEs) driven by multidimensional Gaussian processes with continuous paths, especially fractional Brownian motions.

In order to state the problematic mentioned above, let’s remind some notions of mathematical finance.

Consider a probability space , a -dimensional Brownian motion and the natural filtration associated to ( and ).

Consider the financial market consisting of assets (one risk-free asset and risky assets) over the filtered probability space . At time , the deterministic price of the risk-free asset is denoted by , and prices of the risky assets are given by the random vector .

In a first place, assume that the process is the solution of a stochastic differential equation, taken in the sense of Itô :

where, and are (globally) Lipschitz continuous functions.

Let be the risk-neutral probability measure of the market (i.e. such that is a -martingale).

Theorem 1.1.

Consider an option of payoff . Then, there exists an admissible strategy such that :

where is the associated wealth process.

Refer to D. Lamberton and B. Lapeyre [12], Theorem 4.3.2 for a proof in the case of the Black-Scholes model.

With notations of Theorem 1.1, . It is the option’s price and, when with a function from into , it is useful to get the existence and an expression of the sensitivities of to perturbations of the initial condition and of the volatility function in particular :

In finance, these sensitivities are called greeks. For instance, involves in a procedure called -hedging that allows to compute the admissible strategy of Theorem 1.1 (cf. [12], Subsection 4.3.3). However, there are no reasons to use these quantities in finance only. Indeed, they could also be used in pharmacokinetic as mentioned at [18], Section 5.

Greeks have been studied by many authors. In [7], E. Fournié et al. have established the existence of greeks and have provided expressions of them via Malliavin calculus by assuming that satisfied the uniform elliptic condition (cf. Theorem 1.2). In [10], E. Gobet and R. Münos have extended these results by assuming that only satisfied the hypoelliptic condition. On computation of greeks in the Black-Scholes model, refer to P. Malliavin and A. Thalmaier [16], Chapter 2. On sensitivities in models with jumps, refer to N. Privault et al. [21] and [6]. Finally, via the cubature formula for the Brownian motion, J. Teichmann has provided estimators of Malliavin’s weights for computation of greeks (cf. J. Teichmann [24]). On the regularity of the solution map associated to SDEs taken in the sense of Itô, refer to H. Kunita [11].

At the following theorem, is the divergence operator associated to the Brownian motion (cf. D. Nualart [20], Section 1.3).

Theorem 1.2.

When and are differentiable, of bounded and Lipschitz continuous derivatives, and :

-

(1)

If satisfies the uniform elliptic condition (i.e. there exists such that for every , ), then exists and there exists an adapted -dimensional process such that :

-

(2)

Let be a function such that, for every belonging to a closed neighborhood of , satisfies the uniform elliptic condition. Then exists and there exists an (anticipative) -dimensional process such that :

Refer to [7], propositions 3.2 and 3.3 for a proof.

Under technical assumptions stated at Subsection 2.3, the main purpose of this paper is to extend Theorem 1.2 for the following SDE, taken in the sense of rough paths introduced by T. Lyons in [14] :

where, is a centered -dimensional Gaussian process with continuous paths of finite -variation (), and and satisfy the following assumption.

Assumption 1.3.

and are times differentiable, bounded and of bounded derivatives.

In order to solve that problematic, subsections 2.1 and 2.2 are devoted to existing and additional results of continuity and differentiability of the Itô map associated to rough differential equations. In particular, the continuous differentiability of the Itô map with respect to the collection of vector fields is proved in addition to existing regularity results for the initial condition and for the driving signal, coming from P. Friz and N. Victoir [9], chapters 4 and 11. In order to apply the (probabilistic) integrability results coming from T. Cass, C. Litterer and T. Lyons [2], tailor-made upper-bounds are provided for each derivative. Subsection 2.3 reminds definitions and results related to the natural geometric rough paths associated to a Gaussian process having a covariance function satisfying the technical Assumption 2.11, called enhanced Gaussian process by P. Friz and N. Victoir. Results of subsections 2.1 and 2.2 are applied together with results coming from [2], in order to get the (probabilistic) integrability of the solution of a Gaussian RDE and their derivatives. The main problematic is solved at Section 3 by using results of Section 2 together with Malliavin calculus arguments. Simulations of and are provided at Subsection 4.2.

The fractional Brownian motion (fBm) introduced in [17] by B.B. Mandelbrot and W. Van Ness has been studied by many authors in order to generalize the Brownian motion classically used to modelize risky assets prices process. For instance, the regularity of the process paths and its memory are both continuously controlled via the Hurst parameter of the fBm. However, the fBm is not a semi-martingale if (cf. [20], Proposition 5.1.1). In [22], L.C.G. Rogers has shown the existence of arbitrages for assets having a prices process modelized by a fBm. In order to bypass that difficulty, several approaches have been studied. For instance, in [3], P. Cheridito assumed that the prices process was modelized by a mixed fractional Brownian motion that is a semi-martingale that involves a fBm. At Subsection 4.1, prices of the risky assets are modelized by a fractional SDE, in which the volatility is modelized by another one. Results of Section 3 are applied in order to show the existence and provide an expression of the sensitivity of the option’s price with respect to collection of vector fields of the volatility’s equation.

This paper uses many results on rough paths and rough differential equations coming from [9] and, T. Lyons and Z. Qian [15]. It also involves Malliavin calculus results coming from [20].

Notations and, short definitions and results, used throughout the paper are stated below. However, in a sake of rigor, original well stated results of the literature are cited throughout the paper.

Notations (general) :

-

•

and () are equipped with their euclidean norms, both denoted by .

-

•

The canonical basis of is denoted by . With respect to that basis, for ; the -th component of any vector is denoted by .

-

•

The closed ball of for , of center and of radius , is denoted by .

-

•

The usual matrix (resp. operator) norm on (resp. ) is denoted by (resp. ).

-

•

Consider . The set of dissections of is denoted by . In particular, .

-

•

.

-

•

The space of continuous (resp. continuously differentiable) functions from into is denoted by (resp. ), and is equipped with the uniform norm .

-

•

Differentiability means differentiability in the sense of Fréchet in general (cf. H. Cartan [1], Chapter I.2).

-

•

Consider two Banach spaces and . Let be a derivable map at point , in the direction ; the associated directional derivative is denoted by :

Notations (rough paths) :

-

•

Consider and . The space of continuous functions of finite -variation (resp. -Hölder continuous functions) from into is denoted by

(resp. , that is a subset of ), and is equipped with the -variation distance (resp. the -Hölder distance ). Refer to [9], chapters 5 and 8 about these spaces.

-

•

Consider and a continuous function of finite -variation. The step- tensor algebra over is denoted by

the step- signature of is denoted by

and the step- free nilpotent group over is denoted by

Refer to [9], Chapter 7.

-

•

For , the -th component of any is denoted by .

-

•

The space of geometric -rough paths is denoted by

and is equipped with the -variation distance , or with the uniform distance , associated to the Carnot-Carathéodory’s distance. Refer to [9], Chapter 9.

-

•

The closed ball of for , of center and of radius , is denoted by .

-

•

For every , is a control. Refer to [9], Chapter 1 about properties of controls.

- •

-

•

Consider . The space of collections of -Lipschitz (resp. locally -Lipschitz) vector fields on is denoted by (resp. ) (cf. [9], Definition 10.2). is equipped with the -Lipschitz norm such that, for every ,

-

•

The closed ball of for , of center and of radius , is denoted by .

-

•

Consider , a compact interval of , a control and . Let’s put :

and

where, and for every ,

In the sequel, .

-

•

Consider and satisfying the -non explosion condition (i.e. and are respectively globally Lipschitz continuous and -Hölder continuous on ). The unique solution of with initial condition or , is denoted by .

-

•

By [9], Exercice 10.55, if is a collection of affine vector fields and is a control satisfying for every , there exists a constant , not depending on and , such that :

By [9], Theorem 10.36, if , there exists a constant , not depending on , and , such that for every ,

By [9], Theorem 10.47, if , there exists a constant , not depending on and , such that for every ,

Notations (Gaussian stochastic analysis) :

-

•

For every , is equipped with the Borel -algebra associated to the usual topology on .

-

•

is equipped with the Borel -algebra associated to the usual euclidean topology on , and is equipped with the Borel -algebra associated to the Carnot-Carathéodory’s topology on . These -algebras are both denoted by .

-

•

Let be a -dimensional centered Gaussian process with continuous paths. Its Cameron-Martin’s space is denoted by

with

(cf. [9], Subsection 15.2.2 and Section 15.3), its reproducing kernel Hilbert space is denoted by , and the Wiener integral with respect to defined on is denoted by (cf. [20], Section 1.1).

-

•

The Malliavin derivative associated to is denoted by for the -valued (resp. -valued) random variables, and its domain in (resp. ) is denoted by (resp. ) (cf. [20], Section 1.2).

-

•

For -valued random variables, the divergence associated to is denoted by , and its domain in is denoted by (cf. [20], Section 1.3).

-

•

The vector space of -valued (resp. -valued) random variables locally derivable in the sense of Malliavin is denoted by (resp. ) (cf. [20], Subsection 1.3.5).

2. Regularity of the Itô map : existing and additional results

This section is devoted to the regularity of the Itô map associated to a RDE. On one hand, results of continuity and differentiability of the Itô map with respect to the initial condition and the driving signal coming from [9], Chapter 11 are stated. In addition, the continuous differentiability of the Itô map with respect to the collection of vector fields is proved. On the other hand, in order to apply the integrability results coming from [2], tailor-made upper-bounds are provided for each derivative.

Let’s first synthesize existing continuity results for the Itô map and the rough integral.

Theorem 2.1.

Consider :

-

(1)

The Itô map is uniformly continuous from

-

(2)

The map

is uniformly continuous from

In both cases, the uniform continuity holds when and are equipped with the uniform distance .

Refer to [9], corollaries 10.39,40,48 for a proof.

Remark. Consider , and a collection of affine vector fields on . By [9], Theorem 10.53, belongs to the ball of for every , where

and is a constant not depending on and . Moreover, for every and every ,

So, if is the collection of vector fields satisfying on , then

Therefore, by Theorem 2.1, the map is uniformly continuous from

The uniform continuity holds when and are equipped with the uniform distance .

The following technical corollary of [9], Theorem 9.26 allows to apply integrability results of [2] to differential equations having a drift term.

Corollary 2.2.

Consider such that , , and . There exists a constant , depending only on and , such that :

Proof.

On one hand, for every ,

On the other hand, since and, and are two controls :

is also a control.

Then, by [9], Proposition 7.52, there exists a constant , depending only on and , such that for every ,

In conclusion,

by super-additivity of the control . ∎

2.1. Differentiability of the Itô map with respect to and

In order to prove the continuous differentiability of the Itô map for RDEs with respect to the collection of vector fields, let’s first prove it for ODEs.

Proposition 2.3.

Consider , and a continuous function of finite -variation. Then, the map is continuously differentiable from

Proof.

In a first step, the derivability of the Itô map with respect the collection of vector fields is established at every points and in every directions of . In a second step, via [9], Proposition B.5, the continuous differentiability of that partial Itô map is proved.

Step 1. Consider , , and the solution of the following ODE :

| (2) |

For every ,

where,

Firstly, since is continuously differentiable on , by [9], Lemma 4.2 :

where, when .

By [9], Theorem 3.18 :

| (3) |

with

and .

Secondly, since is continuously differentiable and of bounded derivative on , it is a collection of Lipschitz continuous vector fields. Then, by [9], Theorem 3.18 again :

| (4) |

Thirdly,

| (5) |

Therefore, inequalities (3), (4) and (5) imply that :

In conclusion, by Gronwall’s lemma :

Step 2. The solution of equation (2) satisfies :

where, and are two collections of vector fields, respectively defined by :

for every , and .

Firstly, by the second point of Theorem 2.1, the map is uniformly continuous on every bounded sets of

Secondly, the map is uniformly continuous on every bounded sets of

by construction.

Thirdly, maps and are respectively uniformly continuous on every bounded sets of

by Theorem 2.1 and its remark.

Therefore, by composition, the map is uniformly continuous on every bounded sets of

In conclusion, by [9], Proposition B.5, the map is continuously differentiable from

∎

Theorem 2.4.

Consider :

-

(1)

Let be a collection of -Lipschtiz vector fields on . The map is continuously differentiable from

For every , the Jacobian matrix of at point is denoted by .

Moreover, for every , there exists a constant only depending on , , and , such that for every , -

(2)

For every , is an invertible matrix. Moreover, for every , there exists a constant only depending on , , and , such that for every ,

-

(3)

Consider . The map is continuously differentiable from

Moreover, for every and , there exists two constants and , depending on (continuously) and not on , such that :

Proof.

Refer to [9], theorems 11.3-6 for a proof of the Itô map’s continuous differentiability with respect to the initial condition, and refer to [2], Corollary 3.4 for the upper-bound provided at the first point for ; .

Let be the identity matrix of . Proofs of points 1 and 2 are similar because if is a continuous function of finite -variation, then

as mentioned at the proof of [9], Proposition 4.11.

The proof of the third point is detailed. In a first step, the continuous differentiability of the Itô map with respect to the collection of vector fields is established. In a second step, in order to apply integrability results coming from [2], a tailor-maid upper-bound for the derivative of the Itô map with respect to is provided.

Step 1. Since , there exists a sequence of functions belonging to and satisfying :

| (6) |

Consider , , , ,

and .

By Proposition 2.3, the map is continuously differentiable from

In particular, with

where,

are three collections of vector fields, respectively defined by :

for every , and .

Consider . By Taylor’s formula applied to between and , and [9], Definition 10.17 (RDE’s solution(s)) :

| (7) |

uniformly.

Via Lebesgue’s theorem and [9], Proposition B.1, let show that the derivative of at point , in the direction , exists in equipped with the norm and coincides with .

On one hand, the continuity results of Theorem 2.1 imply that :

in equipped with .

On the other hand, by applying successively [9], theorems 10.47 and 10.36, for every and every ,

with

and

where is depending on and , but not on and .

By [9], Exercice 10.55, there exists a constant , not depending on and , such that :

because

By super-additivity of the control :

In the right-hand side of that inequality, since and are not depending on and , and since

by (6) ;

in equipped with .

Therefore, by Lebesgue’s theorem and inequality (7) :

Since is continuous from

by Theorem 2.1 ; by [9], Proposition B.1, the derivative of at point , in the direction , exists in equipped with and coincides with .

Finally, as at the second step of the proof of Proposition 2.3, via [9], Proposition B.5 and Lemma 4.2 ; the map is continuously differentiable from

Step 2. Consider and .

By applying successively [9], theorems 10.47 and 10.36, for every ,

with

and

where is depending on (continuously), but not on .

By [9], Exercice 10.55, there exists a constant , not depending on and , such that :

because

However,

Therefore,

with and . ∎

Notations. In the sequel, matrices and will be respectively denoted by and in a sake of simplicity. Moreover, for every , let’s put :

Then,

At the following corollary, upper-bounds provided at the previous theorem are extended to RDEs having a drift term.

Corollary 2.5.

Consider , such that , a continuous function of finite -variation, and :

-

(1)

Let be a collection of -Lipschitz vector fields on . For every , there exists a constant depending only on , , , and , such that for every ,

-

(2)

Consider . For every and , there exists two constants and , depending on but not on and , such that :

Proof.

By Corollary 2.2, there exists a constant , depending only on and , such that for every ,

Therefore, by Theorem 2.4 :

-

(1)

For a given collection of vector fields ; for every , there exists a constant depending only on , , and , such that for every ,

with .

-

(2)

For a given initial condition ; for every and , there exists two constants and , depending on but not on , such that :

with .

∎

2.2. Differentiability of the Itô map with respect to the driving signal

Let’s first remind the notion of differentiability introduced by P. Friz and N. Victoir on .

Definition 2.6.

Consider a Banach space , such that , and an open set of . The map is continuously differentiable in the sense of Friz-Victoir on if and only if, for every ,

is continuously differentiable.

With notations of Definition 2.6, if is continuously differentiable from into in the sense of Friz-Victoir, in particular :

is derivable at every points and in every directions of .

Notation. For every continuous functions of finite -variation,

In the sequel, is called the Friz-Victoir (directional) derivative operator.

Theorem 2.7.

Consider a collection of -Lipschitz vector fields on and . The map is continuously differentiable from

in the sense of Friz-Victoir.

Moreover, for every and every continous function of finite -variation,

(Duhamel’s principle).

Finally, consider and a control satisfying :

Then,

-

(1)

There exists a constant , not depending on and , such that for every continous function of finite -variation,

-

(2)

There exists a constant , not depending on and , such that for every continous function of finite -variation,

Proof.

Refer to [9], theorems 11.3-6 and Exercice 11.9 for a proof of the first part.

Consider a continuous function of finite -variation, , and

By [9], Theorem 11.3 :

where,

are three collections of vector fields, respectively defined by :

for every , and .

By applying successively [9], theorems 10.47 and 10.36, for every ,

with

and, by [9], Proposition 7.52 :

where, are two constants not depending on , and .

On one hand, by [9], Exercice 10.55, there exists a constant , not depending on , and , such that :

with , because

| (14) |

and

On the other hand, by [9], Theorem 10.53, there exists a constant , not depending on , and , such that for every satisfying ,

by (14).

Therefore, by super-additivity of the control , there exists a constant , not depending on , and , such that :

∎

At the following corollary, the upper-bound provided at the previous theorem are extended to RDEs having a drift term.

Corollary 2.8.

Consider , such that , such that , a continuous function of finite -variation, , , a collection of -Lipschitz vector fields on and . Then, there exists a constant , not depending on and , such that for every continuous function of finite -variation,

Proof.

Finally, let study the second order continuous differentiability of the Itô map with respect to the driving signal. In order to apply Fernique’s theorem at Section 3, tailor-maid upper-bounds are provided for .

Lemma 2.9.

Consider , and the collection of affine vector fields on defined by :

The map is continuously differentiable from

Moreover, consider a continuous map of finite -variation, and a control satisfying :

Then,

-

(1)

There exists a constant , not depending on and , such that for every continuous map of finite -variation,

-

(2)

There exists a constant , not depending on and , such that for every continuous map of finite -variation,

Proof.

Since is a collection of affine vector fields on , they are locally -Lipschitz on . Then, by [9], Theorem 10.3, is derivable at every points and in every directions of .

Consider a continuous map of finite -variation.

Firstly,

where, is the collection of affine vector fields defined by :

for every and .

By putting :

where, is the collection of affine vector fields defined by :

for every and .

Then, .

Secondly, there exists a constant , depending only on , such that for every ,

By construction, is a control.

By [9], Exercice 10.55, there exists a constant , not depending on , and , such that :

with , because

Thirdly, by [9], Theorem 10.53, there exists a constant , not depending on , and , such that for every ,

Therefore, by super-additivity of the control , there exists a constant , not depending on , and , such that :

Finally, by the remark following Theorem 2.1, since and is a collection of affine vector fields on , and (then) are uniformly continuous on bounded set of

In conclusion, by [9], Proposition B.5, is continuously differentiable as stated. ∎

Proposition 2.10.

Consider , and . The maps

are continuously differentiable.

Moreover, let be a continuous map of finite -variation. there exists three strictly positive constants , and , not depending on , such that for every continuous function of finite -variation,

Proof.

Proofs are similar for , and . It is detailed for .

At the proof of Theorem 2.4, with the same notations, it has been established that :

where,

When , since and are respectively two collections of -Lipschitz vector fields on and by construction, by Theorem 2.7 :

are continuously differentiable.

Moreover, by Proposition 2.9, is a continuously differentiable map from

Then, by composition, is a continuously differentiable map from

Let be a continuous function of finite -variation :

Then,

where, is the usual operator norm on

or on

Let’s find upper-bounds for each term of the product of the right-hand side of inequality (2.2) :

-

(1)

Since , by the second point of Theorem 2.7 for the control , there exists a constant , not depending on and , such that :

(21) -

(2)

Let be a continuous function of finite -variation such that .

On one hand, by construction of the rough integral :where,

is the collection of -Lipschitz vector fields (as ) defined by :

On the other hand, by [9], Theorem 10.36, for every ,

with

where, is a constant not depending on . However, for every ,

(22) where, for every ,

and

Then, as at the proof of point 2 of Theorem 2.7, by using (22) ; there exists a constant , not depending on and , such that :

Therefore,

(23) -

(3)

Let be the continuous map of finite -variation such that .

On one hand, it has been established at Lemma 2.9 that there exists a collection of affine vector fields on () such that :On the other hand, by applying successively [9], theorems 10.36 and 10.47, for every ,

with

where, is a constant not depending on .

Then, as at the proof of point 2 of Lemma 2.9 ; there exists a constant , not depending on and , such that :Therefore,

(24)

In conclusion, inequalities (21), (23), (24) and (2.2) imply together that there exists a constant , not depending on and , such that :

∎

2.3. Application to Gaussian stochastic analysis

Consider a -dimensional stochastic process and the probability space , where is the vector space of continuous functions from into , is the -algebra generated by cylinder sets of , and is the probability measure induced by the process on .

In order to prove Corollary 2.17 that is crucial at Section 3, let’s first state existing results on Gaussian rough paths established by P. Friz and N. Victoir in [8], and by T. Cass, C. Litterer and T. Lyons in [2].

Consider the two following technical assumptions on the stochastic process .

Assumption 2.11.

is a -dimensionnel centered Gaussian process with continuous paths. Moreover, its covariance function is of finite 2D -variation with (cf. [9], Definition 5.50).

Assumption 2.12.

There exists such that :

Example. By [9], Proposition 15.5, Proposition 15.7 and Exercice 20.2, a fractional Brownian motion of Hurst parameter satisfies assumptions 2.11 and 2.12.

Theorem 2.13.

Consider a stochastic process satisfying Assumption 2.11, and . For almost every , there exists a geometric -rough path over satisfying :

-

(1)

There exists a deterministic constant , only depending on , and , such that :

(generalized Fernique’s theorem).

-

(2)

Let be a sequence of linear approximations, or of mollifier approximations, of the process . Then, is the limit in -variation, in for every , of the sequence (universality).

is the enhanced Gaussian process associated to .

Refer to [9], Theorem 15.33 for a proof.

Proposition 2.14.

Refer to [9], Lemma 15.58 for a proof.

Proposition 2.15.

For every geometric -rough path and every ,

Refer to [2], Proposition 4.6 for a proof.

Theorem 2.16.

Refer to [2], Theorem 6.4 and Remark 6.5 for a proof.

Corollary 2.17.

3. Sensitivity analysis for Gaussian rough differential equations

This section solves the problematic stated in introduction of the paper by using the deterministic results on RDEs of subsections 2.1 and 2.2, the probabilistic results on Gaussian RDEs of Subsection 2.3 and Malliavin calculus arguments.

Assume that , and defined in introduction satisfy the following condition.

Assumption 3.1.

Example. A fractional Brownian motion of Hurst parameter satisfies Assumption 3.1. Indeed, it as been stated at Subsection 2.3 that satisfies assumptions 2.11 and 2.12. Moreover, by the first point of L. Decreusefond and S. Ustunel [4], Theorem 3.3 :

Consider . By the second point of [4], Theorem 3.3 :

Assume also that the function satisfies one of the two following assumptions.

Assumption 3.2.

The function is continuously differentiable from into . Moreover, there exists two constants and such that, for every ,

Assumption 3.3.

There exists two constants and such that, for every ,

The following results are solving, at least partially, the problematic stated in introduction of the paper.

Notations :

-

•

Under Assumption 3.1, the enhanced Gaussian process associated to is denoted by , with , and is the collection of vector fields defined by :

for every and .

-

•

Let be the space of functions from into , times differentiable, bounded and of bounded derivatives.

-

•

For every , is denoted by .

Lemma 3.4.

Let be the map from into such that :

for every and . Then, is an isometry from into .

Proof.

On one hand, the linearity of as a map from into is a straightforward consequence of the linearity of as a map from into .

On the other hand, by construction of and of the scalar products on and :

for every functions . ∎

The following corollary extends [9], Proposition 20.5 to Gaussian RDEs having a drift term.

Lemma 3.5.

For every and almost every , the map is continuously differentiable from

In particular, for every , and for every ,

Proof.

By Proposition 2.14, for almost every and every ,

Then, almost surely :

| (25) |

Moreover, Assumpution 2.12 and Corollary 2.8 imply that is continuously differentiable from

Then, by equality (25), the map is also continuously differentiable from

and for almost every and every ,

with .

Moreover, by Duhamel’s principle (cf. Theorem 2.7), for every and every ,

In conclusion, by [20], Proposition 4.1.3 and Lemma 4.1.2, is continuously -differentiable and then locally derivable in the sense of Malliavin, with :

∎

Theorem 3.6.

Proof.

Proofs of points 1 and 2 are similar :

-

(1)

On one hand, for every , and , by Taylor’s formula, and the first point of Corollary 2.5 ; there exists a constant depending only on , , and such that :

Moreover, since satisfies Assumption 3.2, there exists two constants and , depending only on , such that for every ,

Then, by the triangle inequality together with [9], Theorem 10.36, there exists a constant , not depending on , , , , and , such that :

Since satisfies assumptions 2.11 and 2.12, by Corollary 2.17, the generalized Fernique’s theorem (cf. Theorem 2.13) and Cauchy-Schwarz’s inequality :

is bounded by an integrable random variable not depending on . Therefore, by Lebesgue’s theorem, is differentiable on and

(26) On the other hand, consider . By construction, paths of the process are continuously differentiable from into and . Then, since satisfies Assumption 3.1, is a -valued random variable. By Duhamel’s principle (cf. Theorem 2.7) :

Therefore, by equality (26), Lemma 3.5 and [20], Proposition 1.2.3 (Malliavin derivative’s chain rule) :

-

(2)

Let be fixed. On one hand, for every and , by Taylor’s formula :

At [9], Theorem 10.36, the constant involving in the upper-bound doesn’t depend on the signal and on the collection of vector fields. At the second point of Corollary 2.5, the two constants involving in the upper-bound continuously depend on the -Lipschitz norm of the collection of vector fields. Then, there exists a constant , depending on and but not on and , such that for every ,

and

Since satisfies assumptions 2.11 and 2.12, by Proposition 2.15, Theorem 2.16, the generalized Fernique’s theorem (cf. Theorem 2.13) and Cauchy-Schwarz’s inequality :

is bounded by an integrable random variable not depending on . Therefore, by Lebesgue’s theorem, is differentiable on and

(27) On the other hand, consider satisfying Assumption 3.1. By construction, paths of the process are continuously differentiable from into and . Then, is a -valued random variable. By Duhamel’s principle (cf. Theorem 2.7) :

Therefore, by equality (27), Lemma 3.5 and [20], Proposition 1.2.3 (Malliavin derivative’s chain rule) :

∎

Remarks :

- (1)

- (2)

Assumption 3.7.

The process is -dimensional, Gaussian, centered and with continuous paths of finite -variation (). Moreover

and there exists a constant such that :

Functions and are times differentiable, bounded and of bounded derivatives and, for every , is an invertible matrix. Moreover, the function is bounded.

Example. A fractional Brownian motion of Hurst parameter satisfies Assumption 3.7. Indeed, by Kolmogorov’s continuity criterion, there exists and such that for every ,

| (28) |

where .

Corollary 3.8.

Proof.

Consider and satisfying Assumption 3.7. If necessary, processes and introduced at Theorem 3.6 will be respectively denoted by and .

With notations of Proposition 2.10 :

where,

and

First order derivatives of and with respect to the function , in the direction , can be written as sums of products that only involve , and , and their first order derivatives with respect to , in the direction .

Then, by Proposition 2.10, there exists two constants and , not depending on and , such that :

| (29) |

and

| (30) |

because

On one hand, let show that and belong to :

-

(1)

Firstly, for every and , by Taylor’s formula and inequality (29) :

where is a deterministic constant, not depending on , , and . Then, by Lebesgue’s theorem :

(31) and is locally derivable in the sense of Malliavin.

Secondly, since is an isometry from into , and and satisfy Assumption 3.7, there exists two deterministic constants and such that :Then, by Corollary 2.17, .

Thirdly, since is an isometry, in particular is a linear and continuously differentiable map :Then, by equality (31), and since and satisfy Assumption 3.7 :

by Fernique’s theorem.

-

(2)

Firstly, for every and , by Taylor’s formula and inequality (30) :

where is a deterministic constant, not depending on , , and . Then, by Lebesgue’s theorem :

(38) and is locally derivable in the sense of Malliavin.

Secondly, since is an isometry from into , and and satisfy Assumption 3.7, there exists a deterministic constant such that :Then, by Corollary 2.17, .

Thirdly, as at the first point, by equality (38), and since and satisfy Assumption 3.7 :by Fernique’s theorem.

Therefore, and belong to and, if satisfies Assumption 3.2, by Theorem 3.6 :

and

On the other hand, consider a function satisfying Assumption 3.3, a regularizing sequence of functions from into with compact supports, the support of , and for every .

Since satisfies Assumption 3.3, there exists two constants and , such that for every ,

| (40) |

So, and the sequence of functions converges almost everywhere to . In particular,

By construction, for every , satisfies Assumption 3.2. Then,

and

By inequality (40), for every ,

Therefore, by Lebesgue’s theorem :

Moreover, since the random variables and belong to , by Lebesgue’s theorem :

and

∎

4. Application to mathematical finance and simulations

In a first subsection, Theorem 3.6 and Corollary 3.8 are applied to the calculation of sensitivities in a financial market model with stochastic volatility, such that each equation is driven by a fractional Brownian motion of Hurst parameter belonging to . In a second subsection, still with a fractional Brownian signal, simulations of the sensitivities with respect to the initial condition and to the collection of vector fields are provided, when the Hurst parameter of the fBm belongs to .

4.1. Computation of sensitivities in a fractional stochastic volatility model

In this subsection, the prices process of risky assets is the solution of a fractional stochastic volatility model (taken in the sense of rough paths), and the sensitivity of an option’s price to perturbations of the volatility is calculated by using Theorem 3.6 and Corollary 3.8.

Consider a stochastic process , and , , and five functions satisfying one of the two following assumptions.

Assumption 4.1.

Assumption 4.2.

Consider the financial market model consisting of risky assets, of prices at time such that :

and an option of payoff on these assets.

Consider , the enhanced Gaussian process associated to , and the collection of -Lipschitz vector fields on () defined by :

where,

and is the canonical projection from into for .

Rigorously, with and .

4.2. Simulations

In order to simulate the sensitivities studied in this paper, let’s first remind a result coming from [13] on the convergence of the explicit Euler scheme associated to a differential equation driven by a -Hölder continuous function from into (), taken in the sense of Young.

Proposition 4.4.

Consider , a -Hölder continuous function with , and a collection of differentiable vector fields on such that its derivative is -Hölder continuous from into itself ( and ). Then, there exists a constant such that for every ,

where, is the step- explicit Euler scheme associated to for the dissection :

with

for .

Refer to [13], Proposition 5 for a proof.

Corollary 4.5.

Consider , a -dimensional fractional Brownian motion of Hurst parameter , and two functions from into satisfying Assumption 1.3 for and as close to as possible, the vector field on such that for every , , and for arbitrarily chosen. Then, for every ,

where, for every , , and are respectively the explicit Euler schemes associated to , and for the dissection . Moreover, the rate of convergence of each sequence is .

Proof.

Processes and satisfy respectively :

where,

and, and are two collections of affine vector fields on defined by :

Since paths of are almost surely -Hölder continuous by Kolmogorov’s continuity criterion, [9], Theorem 6.8 implies that paths of and are also almost surely -Hölder continuous. Then, , and satisfy conditions of Proposition 4.4, and there exists a random variable such that for every ,

admit as upper-bound.

Finally, by reading carefully the proof of [13], Proposition 5, belongs to for every by Fernique’s theorem. Therefore, for every ,

because . ∎

Remark. About the approximation of the solution of SDEs driven by a fBm, refer also to A. Neuenkirch and I. Nourdin [19].

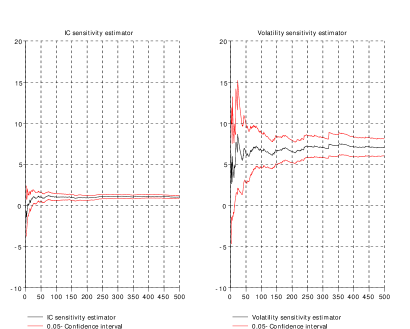

Let be fixed. With assumptions and notations of Corollary 4.5, at each iteration of step- explicit Euler schemes, the value of is computed via the Wood-Chang’s algorithm (cf. T. Dieker [5] about simulation methods of the fBm).

Let be a function satisfying Assumption 3.2. With notations of Section 3, in order to approximate (resp. ),

is estimated by the empirical mean (resp. ) of the -sample from the distribution of (resp. ). By Corollary 4.5, and belong to . Then,

-

(1)

By the strong law of large numbers :

-

(2)

By the central limit theorem and Slutsky’s lemma :

where, (resp. ) is the empirical standard deviation of the -sample from the distribution of (resp. ).

At level , the second point provides the following confidence intervals :

and

where, and is the distribution function of .

Example. Assume that , , , , , , , and :

| Statistics | Values |

|---|---|

| -confidence intervals | |

| Length of the confidence interval | |

| -confidence intervals | |

| Length of the confidence interval |

Appendix A Fractional Brownian motion

Essentially inspired by [20] and [4], this appendix provides basics on the fractional Brownian motion, and the explicit expression of the isometry defined at Lemma 3.4 for that Gaussian process.

Definition A.1.

A fractional Brownian motion of Hurst parameter is a centered Gaussian process of covariance function defined by :

Let be a fractional Brownian motion of Hurst parameter . The associated reproducing kernel Hilbert space is denoted by , the Wiener integral with respect to is denoted by , and the isometry provided at Lemma 3.4 is denoted by .

Definition A.2.

Consider and :

-

(1)

If

exists for every , is the -fractional integral of .

-

(2)

If

exists for every , is the -fractional derivative of .

-

(3)

If they are both defined :

On fractional operators, refer to S. Samko et al. [23].

Notation. is the set of functions defined on by

Theorem A.3.

Let be the operator defined on by :

where,

and is the Gauss hyper-geometric function. Then,

-

(1)

Let be the map defined by :

For every ,

where, is the map defined by for every .

-

(2)

The operator extends as an isometry from into the closed subspace of .

-

(3)

The process is a standard Brownian motion, and

-

(4)

The divergence associated to satisfies .

Refer to [4], Theorem 2.1 and Corollary 3.1, and [20], Proposition 5.2.2 for a proof.

Remark. At [4], Theorem 3.3, L. Decreusefond and S. Ustunel proved that :

Corollary A.4.

The isometry satisfies . In particular,

Proof.

On one hand, the isometry property of the Itô’s stochastic integral together with the third point of Theorem A.3 imply that for every ,

So, by definitions of and :

Then, the construction of at Lemma 3.4 implies that :

That equality extends on by a classical continuity argument.

On the other hand, since and are two invertible maps, the restriction is also invertible. Then, by the first point of Theorem A.3 :

∎

References

- [1] H. Cartan. Cours de calcul différentiel. Méthodes, Hermann, 2007.

- [2] T. Cass, C. Litterer and T. Lyons. Integrability Estimates for Gaussian Rough Differential Equations. arXiv:1104.1813v3, 2011.

- [3] P. Cheridito. Regularizing Fractional Brownian Motion with a View towards Stock Prince Modeling. Thèse de doctorat de l’université de Zürich, 2001.

- [4] L. Decreusefond and A. Ustunel. Stochastic Analysis of the Fractional Brownian Motion. Potential Anal., 10(2) : 177-214, 1999.

- [5] T. Dieker. Simulation of Fractional Brownian Motion. Master thesis, University of Twente, 2004.

- [6] Y. El Khatib and N. Privault. Computations of Greeks in Markets with Jumps via the Malliavin Calculus. Finance and Stochastics 8, 161-179, 2004.

- [7] E. Fournié, J-M. Lasry, J. Lebuchoux, P-L. Lions and N. Touzi. Applications of Malliavin Calculus to Monte-Carlo Methods in Finance. Finance Stochast. 3, 391-412, 1999.

- [8] P. Friz and N. Victoir. Differential Equations Driven by Gaussian Signals. Ann. Inst. Henri Poincaré Probab. Stat. 46, no. 2, 369Ð41, 2010.

- [9] P. Friz and N. Victoir. Multidimensional Stochastic Processes as Rough Paths : Theory and Applications. Cambridge Studies in Applied Mathematics, 120. Cambridge University Press, Cambridge, 2010.

- [10] E. Gobet and R. Münos. Sensitivity Analysis using Itô-Malliavin Calculus and Martingales, and Application to Stochastic Optimal Control. Siam J. Control Optim. Vol. 43, No. 5, pp. 1676-1713, 2005.

- [11] H. Kunita. Stochastic Flows and Stochastic Differential Equations. Cambridge Studies in Applied Mathematics, 24. Cambridge University Press, Cambridge, 1997.

- [12] D. Lamberton and B. Lapeyre. Introduction au calcul stochastique appliqué à la finance. Seconde Edition. Mathématiques et Applications, Ellipses, 1997.

- [13] A. Lejay. Controlled Differential Equations as Young Integrals : A Simple Approach. Journal of Differential Equations 248, 1777-1798, 2010.

- [14] T. Lyons. Differential Equations Driven by Rough Signals. Rev. Mat. Iberoamericana, 14(2):215-310, 1998.

- [15] T. Lyons and Z. Qian. System Control and Rough Paths. Oxford University Press, 2002.

- [16] P. Malliavin and A. Thalmaier. Stochastic Calculus of Variations in Mathematical Finance. Springer Finance, Springer-Verlag, Berlin, 2006.

- [17] B.B. Mandelbrot et J.W. Van Ness. Fractional Brownian Motion, Fractional Noises and Applications. SIAM Rev., 10, 422-437, 1968.

- [18] N. Marie. A Generalized Mean-Reverting Equation and Applications. In revision, preprint on arXiv:1208.1165v4, 2012.

- [19] A. Neuenkirch and I. Nourdin. Exact Rate of Convergence of some Approximation Schemes Associated to SDEs Driven by a Fractional Brownian Motion. Journal of Theoretical Probability, 20(4), pp. 871-899, 2007.

- [20] D. Nualart. The Malliavin Calculus and Related Topics. Second Edition. Probability and its Applications (New York), Springer-Verlag, Berlin, 2006.

- [21] N. Privault and X. Wei. A Malliavin Calculus Approach to Sensitivity in Insurance. Insurance : Mathematics and Economics 35, 679-690, 2004.

- [22] L.C.G. Rogers. Arbitrage with Fractional Brownian Motion. Mathematical Finance, Vol. 7, No. 1, 95-105, 1997.

- [23] S. Samko, A. Kilbas and O. Marichev. Fractional Integrals and Derivatives. Gordon and Breach Science, 1993.

- [24] J. Teichmann. Calculating the Greeks by Cubature Formulas. Proceedings of the Royal Society London A 462, 647-670, 2006.