Asymptotic Inference of Autocovariances of Stationary Processes

Abstract

The paper presents a systematic theory for asymptotic inference of autocovariances of stationary processes. We consider nonparametric tests for serial correlations based on the maximum (or ) and the quadratic (or ) deviations. For these two cases, with proper centering and rescaling, the asymptotic distributions of the deviations are Gumbel and Gaussian, respectively. To establish such an asymptotic theory, as byproducts, we develop a normal comparison principle and propose a sufficient condition for summability of joint cumulants of stationary processes. We adopt a simulation-based block of blocks bootstrapping procedure that improves the finite-sample performance.

keywords:

[class=AMS]keywords:

thebibliographysize \startlocaldefs \endlocaldefs

and

1 Introduction

If is a real-valued stationary process, then from a second-order inference point of view it is characterized by its mean and the autocovariance function , . Assume . Given observations , the natural estimates of and the autocorrelation are

| (1) |

respectively. The estimator plays a crucial role in almost every aspect of time series analysis. It is well-known that for linear processes with independent and identically distributed (iid) innovations, under suitable conditions, , where stands for convergence in distribution, denotes the normal distribution with mean zero and variance . Here can be calculated by Bartlett’s formula (see Section 7.2 of Brockwell and Davis (1991)). Other contributions on linear processes include Hannan and Heyde (1972), Hosoya and Taniguchi (1982), Anderson (1991) and Phillips and Solo (1992) etc. Romano and Thombs (1996) and Wu (2009) considered the asymptotic normality of for nonlinear processes. As a primary goal of the paper, we shall study asymptotic properties of the quadratic (or ) and the maximum (or ) deviations of .

1.1 The Theory

Testing for serial correlation has been extensively studied in both statistics and econometrics, and it is a standard diagnostic procedure after a model is fitted to a time series. Classical procedures include Durbin and Watson (1950, 1951), Box and Pierce (1970), Robinson (1991) and their variants. The Box-Pierce portmanteau test uses as the test statistic, and rejects if it lies in the upper tail of distribution. An arguable deficiency of this test and many of its modified versions (for a review see for example Escanciano and Lobato (2009)) is that the number of lags included in the test is held as a constant in the asymptotic theory. As commented by Robinson (1991):

”…unless the statistics take account of sample autocorrelations at long lags there is always the possibility that relevant information is being neglected…”

The problem is particularly relevant if practitioners have no prior information about the alternatives. The attempt of incorporating more lags emerged naturally in the spectral domain analysis; see among others Durlauf (1991), Hong (1996) and Deo (2000). The normalized spectral density should equal to when the serial correlation is not present. Let be the lag-window estimate of the normalized spectral density, where is a kernel function and is the bandwidth satisfying the natural condition and . The former aims to include correlations at large lags. A test for the serial correlation can be obtained by comparing and the constant function using a suitable metric. In particular, using the quadratic metric and rectangle kernel, the resulting test statistic is the Box-Pierce statistic with unbounded lags. Hong (1996) established the following result:

| (2) |

under the condition that are iid, which implies that all in the preceding equation are zero. Lee and Hong (2001) and Duchesne, Li and Vandermeerschen (2010) studied similar tests in spectral domain, but using a wavelet basis instead of trigonometric polynomials in estimating the spectral density and henceforth working on wavelet coefficients. Fan (1996) considered a similar problem in a different context and proposed adapative Neyman test and thresholding tests, using and as test statistics respectively, where is a threshold value. Escanciano and Lobato (2009) proposed to use with being selected by AIC or BIC.

It has been an important and difficult question on whether the iid assumption in Hong (1996) can be relaxed. Similar problems have been studied by Durlauf (1991), Deo (2000) and Hong and Lee (2003) for the case that are martingale differences. Recently Shao (2011) showed that (2) is true when is a general white noise sequence, under the geometric moment contraction (GMC) condition. Since the GMC condition, which implies that the autocovariances decay geometrically, is quite strong, the question arises as to whether it can be replaced by a weaker one. Furthermore, one may naturally ask: what if the serial correlation is present in (2)? To the best of our knowledge, there has been no results in the literature for this problem. This paper shall address these questions and substantially generalizes earlier results. We shall prove that (2) remains true even if all or some of are not zero, but the variance of the limiting distribution, being different, will depend on the values of . Furthermore, we derive the limiting distribution of when the serial correlation is present. The latter result enables us to calculate the asymptotic power of the Box-Pierce test with unbounded lags.

1.2 The Theory

Another natural omnibus choice is to use the maximum autocorrelation as the test statistic. Wu (2009) obtained a stochastic upper bound for

| (3) |

and argued that in certain situations the test based on (3) has a higher power over the Box-Pierce tests with unbounded lags in detecting weak serial correlation. It turns out that the uniform convergence of autocovariances is also closely related to the estimation of orders of ARMA processes or linear systems in general. The pioneer works in this direction were given by E. J. Hannan and his collaborators, see for example Hannan (1974) and An, Chen and Hannan (1982). For a summary of these works we recommend (Hannan and Deistler, 1988, Section §5.3) and references therein. In particular, An, Chen and Hannan (1982) showed that if for some , then with probability one

| (4) |

The question of deriving the asymptotic distribution of (3) is more challenging. Although Wu (2009) was not able to obtain the limiting distribution of (3), his work provided important insights into this problem. Assuming , and , he showed that, for ,

| (5) |

and we use the superscript to denote the transpose of a vector or a matrix. The asymptotic distribution in (5) does not depend on the speed of . It suggests that, at large lags, the covariance structure of is asymptotically equivalent to that of the Gaussian sequence

| (6) |

where ’s are iid standard normal random variables. Define the sequences and as

| (7) |

According to Berman (1964) (also see Remarks 3 and 4), under the condition ,

Therefore, Wu (2009) conjectured that under suitable conditions, one has the Gumbel convergence

| (8) |

In a recent work, Jirak (2011) proved this conjecture for linear processes and for growing with at most logarithmic speed. We shall prove (8) in Section 4 for general stationary processes; and our result allows to grow as for some , and can be arbitrarily close to under appropriate moment and dependence conditions. The latter result substantially relaxes the severe restriction on the growth speed in (4) and Jirak (2011) and, moreover, the obtained distributional convergence are more useful for statistical inference. For example, other than testing for serial correlation and estimating the order of a linear system, (8) can also be used to construct simultaneous confidence intervals of autocovariances.

1.3 Relations with the Random Matrix Theory

In a companion paper, using the asymptotic theory of sample autocovariances developed in this paper, Xiao and Wu (2010) studied convergence properties of estimated covariance matrices which are obtained by banding or thresholding. Their bounds are analogs under the time series context to those of Bickel and Levina (2008b, a). There is an important difference between these two settings: we assume that only one realization is available, while Bickel and Levina (2008b, a) require multiple iid copies of the underlying random vector.

There has been some related works in the random matrix theory literature that are similar to (8). Suppose one has iid copies of a -dimensional random vector, forming a data matrix . Let , , be the sample correlations. Jiang (2004) showed that the limiting distribution of , after suitable normalization, is Gumbel provided that each column of consists of iid entries and each entry has finite moment of some order higher than 30, and converges to some constant. His work was followed and improved by Zhou (2007) and Liu, Lin and Shao (2008). In a recent article, Cai and Jiang (2010) extended those results in two ways: (i) the dimension could grow exponentially as the sample size provided exponential moment conditions; and (ii) they showed that the test statistic also converges to the Gumbel distribution if each column of is Gaussian and is -dependent. The latter generalization is important since it is one of the very few results that allow dependent entries. Their method is Poisson approximation (see for example Arratia, Goldstein and Gordon, 1989), which heavily depends on the fact that for each sample correlation to be considered, the corresponding entries are independent. Schott (2005) proved that converges to normal distribution after suitable normalization, under the conditions that each column of contains iid Gaussian entries and converges to some positive constant. His proof heavily depends on the normality assumption. Techniques developed in those papers are not applicable here since we have only one realization and the dependence structure among the entries can be quite complicated.

1.4 A Summary of Results of the Paper

We present the main results in Section 2, which include a central limit theory of (2) and the Gumbel convergence (8). The proofs are given in Section 4. In Section 5 we prove a normal comparison principle, which is of independent interest. Since summability conditions of joint cumulants are commonly used in time series analysis (see for example Brillinger (2001) and Rosenblatt (1985)) and is needed in the proof of Theorem 4, we present a sufficient condition in Section 6. Some auxiliary lemmas are collected in Section 7. We also conduct a simulation study in Section 3, where we design a simulation-based block of blocks bootstrapping procedure that improves the finite-sample performance.

2 Main Results

To develop an asymptotic theory for time series, it is necessary to impose suitable measures of dependence and structural assumptions for the underlying process . Here we shall adopt the framework of Wu (2005). Assume that is a stationary causal process of the form

| (9) |

where , are iid random variables, and is a measurable function for which is a properly defined random variable. For notational simplicity we define the operator : suppose is a random variable which is a function of the innovations , then , where is an iid copy of . Namely in is replaced by .

For a random variable and , we write if , and in particular, use for the -norm . Assume , . Define the physical dependence measure of order as

| (10) |

which quantifies the dependence of on the innovation . Our main results depend on the decay rate of as . Let and define

| (11) | |||||

| (12) |

where is defined in (31). It is easily seen that . We use , and as shorthands for , and respectively. We make the convention that for .

There are several reasons that we use the framework (9) and the dependence measure (10). First, the class of processes that (9) represents is huge and it includes linear processes, bilinear processes, Volterra processes, and many other time series models. See, for instance, Tong (1990) and Wiener (1958). Second, the physical dependence measure is easy to work with and it is directly related to the underlying data-generating mechanism. Third, it enables us to develop an asymptotic theory for complicated statistics of time series.

2.1 Maximum deviations of sample autocovariances

Note that is a biased estimate of with . It is then more convenient to consider the centered version instead of . Recall (7) for and .

Theorem 1.

Assume , for some , and , for some . If satisfies and with

| (13) |

then for all ,

| (14) |

In (13), if or , then the second and third conditions are automatically satisfied, and hence Theorem 1 allows a very wide range of lags with . In this sense Theorem 1 is nearly optimal.

For the maximum deviation over the whole range , it seems not possible to derive a limiting distribution by using our method. However, we can obtain a sharp bound . The upper bound is given in (16), while the lower bounded can be obtained by applying Theorem 1 and choosing a sufficiently small such that (13) holds. Using Theorem 2, Xiao and Wu (2010) derived convergence rates for the thresholded autocovariance matrix estimates.

Theorem 2.

Assume , for some , and , for some . If

| (15) |

then for ,

| (16) |

Since , we can assume . For a detailed discussion on their relationship, see Remark 6 of Xiao and Wu (2010). It turns out that for the special case of linear processes the condition (13) can be weakened to the following one:

| (17) |

See Remark 2. Furthermore, for linear processes the condition (15) can be relaxed to as well.

In practice, the mean is often unknown and we can estimate it by the sample mean . The usual estimates of autocovariances and autocorrelations are

| (18) |

2.2 Box-Pierce tests

Box-Pierce tests (Box and Pierce, 1970; Ljung and Box, 1978) are commonly used in detecting lack of fit of a particular time series model. After a correct model has been fitted to a set of observations, one would expect the residuals to be close to a sequence of iid random variables, and therefore one should perform some tests for serial correlations as model diagnostics. Suppose is an iid sequence, let be its sample autocorrelations. Then the distribution of is approximately . Logically, it is not sufficient to consider a fixed number of correlations as the number of observations increases, because there may be some dependencies at large lags. We present a normal theory about the Box-Pierce test statistic, which allows the number of correlations included in to go to infinity.

Theorem 4.

Assume , and . If and for some , then

To see the connection to the Box-Pierce test, we have the following corollary on autocorrelations. Using the same argument, we can show that the same asymptotic law holds for the similar Ljung-Box test statistic .

Corollary 5.

Under the conditions of Theorem 4, the same result holds if is replaced by . Furthermore,

| (20) |

Remark 1.

Theorem 4 clarifies an important historical issue in testing of correlations. If for all , which means are uncorrelated; then and for all , and (20) becomes

| (21) |

In an influential paper, Romano and Thombs (1996) argued that, for fixed , the chi-squared approximation for does not hold if are only uncorrelated but not independent. One of the main reasons is that for fixed , are not asymptotically independent if are not independent. However, interestingly, the situation is different if the number of correlations included in can increase to infinity. According to (5), and are asymptotically independent if and , because the asymptotic covariance is . Therefore, the original Box-Pierce approximation of by , with unbounded , is still asymptotically valid in the sense of (21) since as . This observation again suggests that the asymptotic behaviors for bounded and unbounded lags are different. A similar observation has been made in Shao (2011), whose result also suggests that (21) is true under the assumption that for some . Our condition is much weaker.

The next theorem consists of two separate but closely related parts, one is on the estimation of , and the other is related to the power of the Box-Pierce test. Define the projection operator

Theorem 6.

Assume , and . If and , then

| (22) |

where with . Furthermore, if , then

| (23) |

where with .

Corollary 7.

Under conditions of Theorem 6, the same results hold if is replaced by . Furthermore, there exist positive numbers and such that

As an immediate application, we consider testing whether is an uncorrelated sequence. According to (21), we can use the test statistic

whose asymptotic distribution under the null hypothesis is . The null is rejected when , where is the -th quantile of a standard normal random variable . However, under the alternative hypothesis , the distribution of should be approximated according to Corollary 7, and the asymptotic power is

which increases to 1 as goes to infinity.

3 A Simulation Study

Suppose is a sequence of autocorrelations, one might be interested in the hypothesis test that for all . This hypothesis is, however, impossible to test in practice, except in some special parametric cases. A more tractable hypothesis is

| (24) |

In traditional asymptotic theory, one often assumes that is a fixed constant, for example, the popular Box-Pierce test for serial correlation. Our results in the previous section provide both and based tests, which allow to grow as increases. Nonetheless, the asymptotic tests can perform poorly when the sample size is not large enough, namely, there may exist noticeable differences between the true and nominal probabilities of rejecting (hereafter referred as error in rejection probability or ERP). In a recent paper, Horowitz et al. (2006) showed that the Box-Pierce test with bootstrap-based -values can significantly reduce the ERP. They used the blocks of blocks bootstrapping with overlapping blocks (hereafter referred as BOB) invented by Künsch (1989). For finite sample, our based test is similar as the traditional Box-Pierce test considered in their paper, so in this section our focus will be on the based tests. We shall provide simulation evidence showing that the BOB works reasonably well.

Throughout this section, we let the innovations be iid standard normal random variables, and consider the following four models.

| I.I.D.: | (25) | |||

| AR(1): | (26) | |||

| Bilinear: | (27) | |||

| ARCH: | (28) |

We generate each process with length , and compute

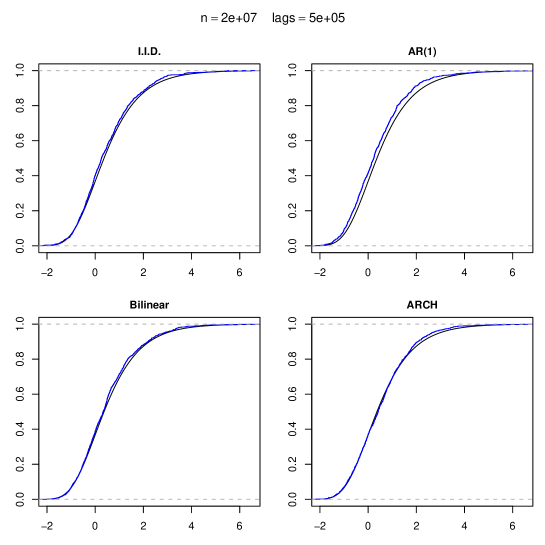

| (29) |

with and , where is chosen as . Based on 1000 repetitions, we plot the empirical distribution functions in Figure 1. We see that these four empirical curves are close to the one for the Gumbel distribution, which confirms our theoretical results.

One the other hand, these empirical distributions are not very close to the limiting one if the sample size is not large, because the Gumbel type of convergence in (14) is slow. This is a well-known phenomenon; see for example Hall (1979). It is therefore not reasonable to use the limiting distribution to approximate the finite sample distributions. To perform the test (24), we repeat the BOB procedure as described in Horowitz et al. (2006) (called SBOB in their paper). Since in the bootstrapped tests, the test statistics are not to be compared with the limiting distribution, we can ignore the norming constants in (29) and simply use the following test statistics

where is the self-normalized version with estimated as , with . For simplicity, we refer these two tests as -test and -test, respectively.

From the series , for some specified number of lags that will be included in the test and block size , form , and blocks , . For simplicity assume is an integer. Suppose is obtained by sampling a block from the set of blocks , and then sampling a column from , let represent the covariance of the bootstrap distribution of , conditional on . Denote by the -th entry of , set

The explicit formula of was also given in Horowitz et al. (2006). The BOB algorithm is as follows.

-

1.

Sample times with replacement from to obtain blocks , which are laid end-to-end to form a series of vectors .

-

2.

Pretend that is a random sample of size from some -dimensional population distribution, let be the sample correlation of the first entry and the -th entry. Then calculate the test statistic and , where .

-

3.

Repeat steps 1 and 2 for times. The bootstrap -value of the -test is given by . For a nominal level , we reject if . The -test is performed in the same manner.

We compare the BOB tests and the asymptotic tests for the four models listed at the beginning of this section, with for (26), for (27) and for (28). We set the series length as , and consider four choices of : , , and 25. The BOB tests are performed with , and the asymptotic tests are carried out by comparing with the corresponding quantiles of the Gumbel distribution. The empirical rejection probabilities based on 10,000 repetitions are reported in Table LABEL:tab:sbob. All probabilities are given in percentages. For all cases, we see that the asymptotic tests are too conservative, and the ERP are quite large. At the nominal level , the rejection probabilities are often less than or around , and at most ; while at nominal level , they are often less than and at most . Except for the bilinear models with and , the bootstrapped tests significantly reduce the ERP, which are often less than at nominal level , less than at level , and less than at level . The performance of -test and -test are similar, with the former being slightly more conservative. The BOB tests are roughly insensitive to the block size, which provides additional evidence of the findings on BOB tests in Davison and Hinkley (1997).

[

caption = Empirical rejection probabilities (in percentages),

label = tab:sbob,

pos = ht,

]lrrrcrrrcrrrcrrr \tnote[]The values 1, 5, 10 in the 2nd row

indicate nominal levels in percentages. The numbers in the third

row starting with the model name “I.I.D.” are for the asymptotic

tests. The fourth row staring with is for BOB

-tests with block size 5. The fifth row is for BOB -tests with the same block size 5. Other rows should be read

similarly. Test

1 5 10 1 5 10 1 5 10 1 5 10

I.I.D. .00 .34 1.6 .02 .69 2.3 .03 .93 3.2 .04 1.0 3.3

1.3 5.1 10.0 1.1 5.2 9.8 .95 4.7 9.3 1.0 4.7 9.6

1.4 5.3 10.4 1.2 5.6 10.5 1.1 5.1 10.1 1.1 5.1 10.2

.83 4.8 10.0 1.1 4.9 9.6 1.1 4.9 10.1 .65 4.3 8.9

.94 5.1 10.3 1.2 5.4 10.3 1.1 5.5 11.0 .78 4.7 9.6

AR(1) .01 .17 1.2 .01 .36 1.8 .02 .77 2.5 .02 .88 2.8

1.3 5.7 10.9 1.3 5.5 11.4 1.3 5.5 10.9 1.1 5.7 11.2

1.3 5.7 11.2 1.4 5.9 11.7 1.3 6.0 11.5 1.2 6.0 11.7

.98 5.5 10.9 1.0 5.8 11.3 1.1 5.3 10.6 .86 4.9 10.5

1.0 5.7 11.0 1.1 6.1 11.9 1.2 5.6 11.0 .83 5.0 10.9

Bilinear .34 2.8 6.4 .43 2.5 5.8 .51 2.5 5.9 .40 2.8 5.9

2.8 8.7 14.4 1.8 7.1 12.7 1.2 6.1 12.0 1.2 5.4 10.9

2.7 8.6 14.5 1.8 7.3 12.9 1.3 6.2 12.2 1.1 5.5 11.1

2.7 8.4 14.6 2.1 7.2 13.5 1.5 6.3 12.0 1.3 5.2 10.8

2.5 8.3 14.6 2.1 7.5 13.9 1.5 6.2 12.0 1.2 5.3 10.9

ARCH .05 .82 3.2 .06 1.5 3.9 .09 1.3 4.0 .12 1.4 4.4

.99 5.0 10.5 1.2 4.9 9.7 .80 4.6 9.9 .82 4.7 9.3

1.1 5.4 10.9 1.4 5.3 10.4 .92 5.1 10.7 .94 5.1 10.2

.86 5.1 10.5 1.0 5.0 10.3 .69 4.8 9.7 .63 4.3 8.9

.98 5.5 11.0 1.2 5.6 11.0 .89 5.1 10.4 .76 4.7 9.5

The bootstrapped tests still perform relatively poorly for bilinear models when is small (7 and 12). This is possibly due to the heavy-tailedness of the bilinear process. Tong (1981) gave necessary conditions for the existence of even order moments. On the other hand, Horowitz et al. (2006) showed that the iterated bootstrapping further reduce the ERP. It is of interest to see whether the iterated procedure has the same effect for the based tests, in particular, whether it makes the ERP reasonably small for the bilinear models when is small. The simulation for the iterated bootstrapping will be computationally expensive and we do not pursue it here.

4 Proofs

This section provides proofs for the results in Section 2. For readability we list the notation here. For a random variable , write that , , if . Write if . To express centering of random variables concisely, we define the operator as . For a vector , let be the usual Euclidean norm, , and . For a square matrix , denotes the operator norm defined by . Let us make some convention on the constants. We use , and for constants. The notation is reserved for the constant appearing in Burkholder’s inequality, see (31). The values of may vary from place to place, while the value of is fixed within the statement and the proof of a theorem (or lemma). A constant with a symbolic subscript is used to emphasize the dependence of the value on the subscript.

The framework (9) is particularly suited for two classical tools for dealing with dependent sequences, martingale approximation and -dependence approximation. For , define be the -field generated by the innovations , and the projection operator . Set , , and define and similarly. Define the projection operator , and , then and become martingale difference sequences with respect to the filtrations and , respectively. For , define , then is a -dependent sequence.

4.1 Some Useful Inequalities

We collect in Proposition 8 some useful facts about physical dependence measures and martingale and -dependence approximations. We expect that it will be useful in other asymptotic problems that involve sample covariances. Hence for convenience of other researchers, we provide explicit upper bounds.

We now introduce a moment inequality (30) which follows from the Burkholder inequality (see Burkholder, 1988). Let be a martingale difference sequence and for every , , , then

| (30) |

where and the constant

| (31) |

We note that when , the constant in (30) equaled to in Burkholder (1988), and it was improved to by Rio (2009).

Proposition 8.

-

1.

Assume and . Recall that .

(32) (33) (34) (35) (36) (37) where

-

2.

For , define . For , let be the physical dependence measures for the sequence . Then

(38) (39) (40) (41)

Proof.

The inequalities (32) and (38) are obtained by the first principle. Since and , we have

which proves (35). For (37), it can be similarly proved as Proposition 1 of Liu and Wu (2010), and (40) was given by Lemma 1 of the same paper. (34) is a special case of (40). Define , then is also a stationary process of the form (9). By Hölder’s inequality, . Applying (34) to , we obtain (36). To see (39), we first write . Since , and is a martingale difference sequence, by (30), we have

The above argument also leads to (33). Using a similar argument as in the proof of Theorem 2 of Wu (2009), we can show (41). Details are omitted. ∎

4.2 Proof of Theorem 1

The proof is quite complicated and will be divided into several steps. We first give the outline.

4.1.0. Outline

Step 1: -dependence approximation.

Define . Set , . Define , , and . We next show that it suffices to consider .

Lemma 9.

Assume , , and for some and . If with , then there exists a such that and

Step 2: Throw out small blocks.

Let , where . For each , we apply the blocking technique and split the integer interval into alternating large and small blocks

| (42) | ||||

where is the largest integer such that . Denote by the size of a block . By definition we know when is large enough. For define

Note that . We show that the sums over small blocks are negligible.

Lemma 10.

Assume the conditions of Theorem 1. Then

Step 3: Truncate sums over large blocks.

We show that it suffices to consider

Lemma 11.

Assume the conditions of Theorem 1. Then

Step 4: Compare covariance structures.

In order to prove Lemma 14, we need the autocovariance structure of to be close to that of . However, this only happens when is large. We show that there exists an such that for , (i) does not contribute to the asymptotic distribution; and (ii) the autocovariance structure of converges to that of uniformly on .

Lemma 12.

Under conditions of Theorem 1, there exists a constant such that for ,

| (43) |

Step 5: Moderate deviations.

Let be as in Lemma 12. For , define and , where is defined in (6). Let and . For fixed , set , where the constants and are defined in (7). In the following lemma we provide a moderate deviation result for .

Lemma 14.

Assume conditions of Theorem 1. Then there exists a constant such that for all ,

4.2.1 Step 1: -dependence approximation

4.2.2 Step 2: Throw out small blocks

In this section, as well as many other places in this article, we often need to split an integer interval into consecutive blocks with the size . Since may not be a multiple of , we make the convention that unless the size of the last block is specified clearly, it has the size , and all the other ones have the same size .

Proof of Lemma 10.

It suffices to show that for any ,

Observe that , are independent. By (36), . By Corollary 1.6 of Nagaev (1979), for any , there exists a constant such that

| (45) | ||||

where we resolve the constant into the constant in the last inequality. It remains to show that

| (46) |

holds for any , where is the smallest integer such that . This choice of will be explained later. We adopt the technique of successive -dependence approximations from Liu and Wu (2010) to prove (46).

For , set . Define , , and

In particular, is same as defined in Step 2, and . Without loss of generality assume . Let be such that . We first consider the difference between and for . Split the block into consecutive small blocks with size . Define

| (47) |

Observe that and are independent if . Similar as (45), for any , there exists a constant such that, for sufficiently large ,

| (48) | ||||

Similarly as (44), we have . It follows that

Under the condition (17), there exists a , such that

Recall that is the smallest integer such that . We now consider the difference between and for . The problem is more complicated than the preceding case , since now it is possible that for some . We consider three cases.

Case 1: . Partition the block into consecutive smaller blocks with same size . Define and as in (47). Observe that is a martingale difference sequence with respective to the filtration , and so is the sequence and filtration labelled by even . Set and . For each , define

for . By Lemma 1 of Haeusler (1984), for any , there exists a constant such that

| (49) | ||||

By (35), , and hence by (37), . Observe that and are independent if , so similarly as (45), we have

The same inequality holds for the sum over even . For the first term in (49), we claim that

| (50) |

which together with the preceding two inequalities implies that

It follows that under condition (17), there exists a such that

| (51) | ||||

Case 2: . Partition the block into consecutive smaller blocks with size . Define and as in (47). Similarly as (44), we have

Similar as (48), for any , there exist a constant such that

It follows that that under condition (17), there exists a such that

| (52) | ||||

Case 3: . We use the same argument as in Case 2. But this time we claim that

| (53) |

where is defined in (35). Since , under condition (13), there exist constants and such that for large enough

| (54) | ||||

Alternatively, if we use the bound from (41), , it is still true that under condition (13), there exist constants and such that for large enough

| (55) | ||||

Combine (51), (52), (54) and (55), we have shown that

| (56) |

for . Therefore, to prove (46), it suffices to show

| (57) |

By considering two cases (i) and (ii) under the condition , and using similar arguments as those in proving (56), we can obtain (57). The proof of Lemma 10 is complete.

We now turn to the proof of the two claims (50) and (53). For (53), we have

Similarly as in the proof of (44), we have

For the second term , write

For a pair such that , by the inequality (30), we have

For the pairs such that , by the triangle inequality

Putting these pieces together, the proof of (53) is complete. The key observation in proving (50) is that since , and are independent, hence the product has finite -th moment. The rest of the proof is similar to that of (53). Details are omitted. ∎

Remark 2.

Condition (13) is only used to deal with Case 3, while (17) suffices for the rest of the proof. In fact, for linear processes, one can show that the term in (53) can be removed, so we have (54) under condition (17) and do not need (55). So (17) suffices for Theorem 1. Furthermore, for nonlinear processes with , the term can also be removed from (53). Details are omitted.

4.2.3 Step 3: Truncate sums over large blocks

4.2.4 Step 4: Compare covariance structures

Proof of Lemma 12.

4.2.5 Step 5: Moderate deviations.

Proof of Lemma 14.

Note that for , . Let and . Since , by Fact 2.2 of Einmahl and Mason (1997),

By Lemma 23, the smallest eigenvalue of is bounded from below by some uniformly on . By Lemma 13 we have , where the first inequality is taken from Problem 7.2.17 of Horn and Johnson (1990). It follows that by (76) and elementary calculations that

By Lemma 22, we have

Putting these pieces together and observing that and have the same distribution, we have

which together with a similar lower bound completes the proof of Lemma 14. ∎

4.2.6 Proof of Theorem 1

After these preparation steps, we are now ready to prove Theorem 1.

Proof of Theorem 1.

Set . It suffices to show

| (59) |

Without loss of generality assume . Define the events and . Let

By the inclusion-exclusion formula, we know for any

| (60) |

By Lemma 14, By Lemma 20 with elementary calculations, we know , and hence . By letting go to infinity first and then go to infinity in (60), we obtain (59), and the proof is complete. ∎

4.3 Proof of Theorem 2

Proof of Theorem 2.

We start with an -dependence approximation that is similar to the proof of Theorem 1. Set for some . Define , , and . Similarly as the proof of Lemma 10, we have under the condition (15)

For , we consider two cases according to whether or not.

Case 1: . We first split the interval into the following big blocks of size

where is the smallest integer such that . For each block , we further split it into small blocks of size

where is the smallest integer such that . Now define and

| (61) |

for . Observe that each () is a sum of independent random variables. By (36), . By Corollary 1.7 of Nagaev (1979) where we take in their result, we have for any

| (62) | ||||

where the range of in the sum is as in (61). Clearly, . Similarly as the proof of Lemma 12, we can show that . Therefore, if , then .

Case 2: . This case is easier. By splitting the interval into blocks with size and using a similar argument as (62), we have

The proof is complete.

∎

4.4 Box-Pierce tests

Similarly as the proof of Theorem 1, we use -dependence approximations and blocking arguments to prove Theorem 4. We first outline the intermediate steps and give the main proof in Section 4.4.1, and then provide proofs of the intermediate lemmas in Section 4.4.2 and Section 4.4.3. We prove Theorem 6 in Section 4.4.4, and prove Corollary 5 and 7 in Section 4.4.5.

4.4.1 Proof of Theorem 4

Step 1: -dependence approximation.

Step 2: Throw out small blocks.

Let , where . Split the interval into alternating small and large blocks similarly as (42):

where is the largest integer such that . Define , , and , for . Set . Observe that by construction, are iid random variables. In the following lemma we show that it suffices to consider .

Lemma 15.

Assume , , and , then

Step 3: Central limit theorem concerning ’s.

Lemma 16.

Assume , , and , then

We are now ready to prove Theorem 4.

4.4.2 Step 2: Throw out small blocks.

Let be the collection of all double arrays such that

For , define . It is easily seen that and . Furthermore, this fact implies the following proposition, which will be useful in computing sums of products of cumulants. For , let be the collection of all -dimensional array such that

Note that , and if .

Proposition 17.

For , and , if and , define an array by

then , and .

In Lemma 18 we present an upper bound for . We formulate the lemma in a more general way for later uses in the proofs of Lemma 15 and Lemma 16. For a -dimensional random vector such that for , denote by its -th order joint cumulant. For the stationary process , we write

We need the assumption of summability of joint cumulants in Lemma 18, Lemma 15 and Lemma 16. For this reason, we provide a sufficient condition in Section 6.

Lemma 18.

Assume , , and . For , and , set and , then we have

where is a symmetric double array of non-negative numbers such that , and

Proof.

Write

For the sum of the second term, we have

Similarly, for the sum of the last term

Observe that and similarly . For the sum of the first term, it holds that

Utilizing the summability of cumulants, the proof is complete. ∎

In the proof of Lemma 15, we need the concept of indecomposable partitions. Consider the table

| … | ||

| ⋮ | ⋮ | |

| … |

Denote the -th row of the table by . A partition of the table is said to be indecomposable if there are no sets () and rows () such that .

Proof of Lemma 15.

Write

Using Lemma 16, we know . We can express as

| (64) |

where for (assume without loss of generality that is even),

Consider the first term in (64), write

By Lemma 18, it holds that

where is the (defined in Lemma 18) for the sequence . Similarly,

To deal with , we express it in terms of cumulants

Apparently and . Using the multilinearity of cumulants, we have

for . By Theorem II.2 of Rosenblatt (1985), we know

| (65) |

where the sum is over all indecomposable partitions of the table

By Theorem 21, the condition implies that all the joint cumulants up to order eight are absolutely summable. Therefore, using Proposition 17, we know

and it follows that We have shown that which, in conjunction with similar results for the other three terms in (64), implies that and hence . The proof is now complete. ∎

4.4.3 Step 3: Central limit theorem concerning ’s.

Proof of Lemma 16.

Let and . By Lemma 18 we know . Write

Using similar a argument as the one for dealing with the term in Lemma 15, we know

and it follows that

Therefore, it suffices to consider

Let . Observe that is a martingale difference sequence with respect to . We shall apply the martingale central limit theorem. Write

For the first term, by Lemma 18, we have

Using Lemma 18 and Proposition 17, we obtain

Therefore, we have

Using Lemma 18 and Lemma 24, we know

and it follows that

| (66) |

To verify the Lindeberg condition, we compute

We express in terms of cumulants

From Lemma 18, it is easily seen that

and similarly and . By multilinearity of cumulants,

Each cumulant in the preceding equation is to be further simplified similarly as (65). Using summability of joint cumulants up to order eight and Proposition 17, we have

Using orders obtained for , , and , we obtain . Then, by (66), we can apply Corollary 3.1. of Hall and Heyde (1980) to obtain

and the lemma follows. ∎

4.4.4 Proof of Theorem 6

Proof of Theorem 6.

We shall only prove (23), since (22) can be obtained by very similar arguments. Write , and hence

Using the conditions and , it is easily seen that and . Furthermore

Define . For the term , write

Clearly . Define , then

It follows that

Set , then is a stationary process of the form (9). Furthermore

Since , utilizing Theorem 1 in Hannan (1973) we have , and then (23) follows. ∎

4.4.5 Proof of Corollary 5 and 7

Proof of Corollary 5 and 7.

By (34), we know , and it follows that

Theorem 4 holds for because

In Theorem 6, (23) holds with replaced by because

and (22) can be proved similarly. Now we turn to the sample autocorrelations. Write

Since

and similarly , (20) follows by applying the Slutsky theorem. To show the limit theorems in Corollary 7, note that using the Cramer-Wold device, we have

converges to a bivariate normal distribution. Then Corollary 7 follows by applying the delta method. ∎

5 A Normal Comparison Principle

In this section we shall control tail probabilities of Gaussian vectors by using their covariance matrices. Denote by the density of a -dimensional multivariate normal random vector with mean zero and covariance matrix , where we always assume for and is nonsingular. For , we use to denote the marginal density of the sub-vector . Let

The partial derivative with respect to is obtained similarly as equation (3.6) of Berman (1964) by using equation (3) of Plackett (1954)

| (67) | ||||

| (68) |

where stands for . If all the have the same value , we use the simplified notation and . The following simple facts about conditional distribution will be useful. For four different indicies , we have

| (69) | ||||

| (70) | ||||

| (71) |

Lemma 19.

For every , , and , there exists positive constants and such that for

-

1.

if for all , then

(72) (73) (74) where and for ;

-

2.

if for all such that , , then

(75)

Proof.

The following facts about normal tail probabilities are well-known:

| (76) |

By (76), the inequalities (72) – (74) with are true for the random vector with iid standard normal entries. The idea is to compare the desired probability with the corresponding one for such a vector. We first prove (72) by induction. When , the inequality is trivially true. When , by (67), there exists a number between and such that

which, together with , implies (72) for with and some . Now for , assume (72) holds for all dimensions less than . There exists a matrix for some such that

| (77) |

By (69), for . Therefore, by writing the density in (67) as the product of the density of and the conditional density of given , where denotes the sub-vector ; we have

| (78) |

where is the correlation matrix of the conditional distribution of given and . By (70) and (71), we know for and ,

Therefore, all the off-diagonal entries of are less than if we let . Applying the induction hypothesis, if , then

and equation (78) becomes

Therefore, (72) holds for and some .

Lemma 20.

Let be a stationary mean zero Gaussian process. Let . Assume , and . Let , , and for . Define the event , and

Then for all .

Proof.

Note that . If consists of iid random variables, by the equality in (76),

When the ’s are dependent, the result is still trivially true when . Now we deal with the case. Let , then by stationarity, and . Consider an ordered subset , where . We define an equivalence relation on by saying if there exists such that , and for . For any , denote by the number of which are less than or equal to . To similify the notation, we sometimes use instead of . is divided into equivalence classes . Suppose , assume w.l.o.g. that . Pick , and for , and set . Define and similarly, then . By (75) of Lemma 19, there exists a number depending on and the sequence , such that when ,

Note that . Pick for some . For any , since there are at most ordered subset such that , we know the sum of over these is dominated by

when is large enough, which converges to zero. Therefore, it suffices to consider all the ordered subsets such that for all .

Let be an ordered subset such that for , and be the collection of all such subsets. Let be the -dimensional covariance matrix of . There exists a matrix for some such that

Let , , be the correlation matrix of the conditional distribution of given and . By (73) of Lemma 19, for large enough

It follows that

| (79) | |||

| (80) | |||

| (81) |

For each fixed pair , the inner sum in (79) is bounded by

| (82) | ||||

| (83) |

Since , it also holds that . Note that , it follows that . Therefore, the term in (83) converges to zero, and the proof is complete. ∎

Remark 3.

This lemma provides another proof of Theorem 3.1 in Berman (1964), which gives the asymptotic distribution of the maximum term of a stationary Gaussian process. They also showed that the theorem is true if the condition is replaced by . Under the later condition, if we replace by in (79), by in (82), then the term in (82) converges to zero, and hence our result remains true.

Remark 4.

In the proof, the upper bounds on and are expressed through the absolute values of the correlations, so we can obtain the same bounds for probabilities of the form for any . Therefore, our result can be used to show the asymptotic distribution of the maximum absolute term of a stationary Gaussian process. Specifically, we have

Deo (1972) obtained this result under the condition for some , whereas we only need .

6 Summability of Cumulants

For a -dimensional random vector such that for , the -th order joint cumulant is defined as

| (84) |

where the summation extends over all partitions of the set into non-empty blocks. For a stationary process , we abbreviate

Summability conditions of cumulants are often assumed in the spectral analysis of time series, see for example Brillinger (2001) and Rosenblatt (1985). Recently, such conditions were used by Anderson and Zeitouni (2008) in studying the spectral properties of banded sample covariance matrices. While such conditions are true for some Gaussian processes, functions of Gaussian processes (Rosenblatt, 1985), and linear processes with iid innovations (Anderson, 1971), they are not easy to verify in general. Wu and Shao (2004) showed that the summability of joint cumulants of order holds under the condition that for some . We present in Theorem 21 a generalization of their result. To simplify the proof, we introduce the composition of an integer. A composition of a positive integer is an ordered sequence of strictly positive integers such that . Two sequences that differ in the order of their terms define different compositions. There are in total different compositions of the integer . For example, we are giving in the following all of the eight compositions of the integer 4.

Theorem 21.

Assume , and . If

| (85) |

then

| (86) |

Proof.

By symmetry of the cumulant in its arguments and stationarity of the process, it suffices to show

Set , we claim

| (87) | ||||

| (88) | ||||

| (89) | ||||

| (90) |

where the sum is taken over all the increasing sequences such that , and is a composition of the integer . We first consider the last summand which corresponds to the sequence ,

Observe that and are independent. By definition, only partitions for which and are in the same block contribute to the sum in (84). Suppose is a partition of the set , since

it follows that

and therefore

provided that .

The other terms in (87) are easier to deal with. For example, for the term corresponding to the sequence , we have

Since implies , it follows that

We have shown that every cumulant in (87) is absolutely summable over , and it remains to show the claim (87). We shall derive the case , (87) for other values of are obtained using the same idea. By multilinearity of cumulants, we have

Since and are independent, the last cumulant is 0. Apply the same trick for the first two cumulants, we have

and

Then the proof is complete. ∎

Remark 5.

When , (85) reduces to the short-range dependence or short-memory condition . If , then the process may be long-memory in that the covariances are not summable. When , we conjecture that (85) can be weakened to . It holds for linear processes. Let . Assume and , then . Let be the -th cumulant of . Set , by multilinearity of cumulants, we have

Therefore, the condition suffices for (86). For a class of functionals of Gaussian processes, Rosenblatt (1985) showed that (86) holds if , which in turn is implied by under our setting. It is unclear whether in general the weaker condition implies (86).

7 Some Auxiliary Lemmas

Suppose that is a -dimensional random vector, and . If , then by (76), it is easily seen that the ratio of over tends to zero provided that , and . It is a similar situation when is not an identity matrix, as shown in the following lemma, which will be used in the proof of Lemma 14.

Lemma 22.

Let be a -dimensional normal random vector. Assume is nonsingular. Let and be the smallest and largest eigenvalue of respectively. Then for such that , then for any ,

| (91) |

Proof.

The preceding lemma requires the eigenvalues of to be bounded both from above and away from zero. In our application, is taken as the covariance matrix of , where is defined in (6). Furthermore, we need such bounds be uniform over all choices of . Let be the spectral density of . A sufficient condition would be that there exists such that

| (94) |

because the eigenvalues of the autocovariance matrix are bounded from above and below by the maximum and minimum values that takes respectively. For the proof see Section 5.2 of Grenander and Szegö (1958). Clearly the upper bound in (94) is satisfied in our situation, because . However, the existence of lower bound in (94) rules out some classical times series models. For example, if is the moving average of the form , then , and . Nevertheless, although the minimum eigenvalue of the autocovariance matrix converges to as the dimension of the matrix goes to infinity, there does exist a positive lower bound for the smallest eigenvalues of all the principal sub-matrices with a fixed dimension.

Lemma 23.

If , then for each , there exists a constant such that

Proof.

We use induction. It is clear that we can choose to be a non-increasing sequence. Without loss of generality, let us assume . The statement is trivially true when . Suppose it is true for all dimensions up to , we now consider the dimension case. There exist an integer such that . If all the differences for , there are possible choices of . Since the process is non-deterministic, for all these choices, the corresponding covariance matrices are non-singular. Pick to be the smallest eigenvalue of all these matrices. If there is one difference , set and , then and . It follows that for any real numbers such that ,

Setting , the proof is complete. ∎

The following lemma is used in the proof of Lemma 13.

Lemma 24.

Assume , , and . Assume , , and . Define . Then

| (95) |

Proof.

Let , then and are independent, because . Define . By (41), we have for any ,

| (96) |

By (36), for any , and it follows that

| (97) | ||||

For any , define , where . Observe that and are independent, we have

| (98) | ||||

| (99) | ||||

| (100) |

According to the proof of Theorem 2 of Wu (2009), when , where . By (35) and (38), ; and hence

| (101) | ||||

| (102) |

By (36) and (38), for any . Combining (100) and (101), we have

| (103) |

Observe that when , and are independent for . Therefore,

| (104) | ||||

| (105) | ||||

| (106) | ||||

| (107) | ||||

| (108) |

By (39), . Since and , we have

| (109) | |||||

| (110) |

Combining (97), (103) and (109), the lemma follows by noting that , are dominated by ; and , and are all dominated by . ∎

References

- An, Chen and Hannan (1982) {barticle}[author] \bauthor\bsnmAn, \bfnmHong Zhi\binitsH. Z., \bauthor\bsnmChen, \bfnmZhao Guo\binitsZ. G. and \bauthor\bsnmHannan, \bfnmE. J.\binitsE. J. (\byear1982). \btitleAutocorrelation, autoregression and autoregressive approximation. \bjournalAnn. Statist. \bvolume10 \bpages926–936. \endbibitem

- Anderson (1971) {bbook}[author] \bauthor\bsnmAnderson, \bfnmT. W.\binitsT. W. (\byear1971). \btitleThe statistical analysis of time series. \bpublisherJohn Wiley & Sons Inc., \baddressNew York. \endbibitem

- Anderson (1991) {btechreport}[author] \bauthor\bsnmAnderson, \bfnmT. W.\binitsT. W. (\byear1991). \btitleThe asymptotic distributions of autoregressive coefficients \btypeTechnical Report No. \bnumber26, \binstitutionStanford University, Department of Statistics. \endbibitem

- Anderson and Zeitouni (2008) {barticle}[author] \bauthor\bsnmAnderson, \bfnmGreg W.\binitsG. W. and \bauthor\bsnmZeitouni, \bfnmOfer\binitsO. (\byear2008). \btitleA CLT for regularized sample covariance matrices. \bjournalAnn. Statist. \bvolume36 \bpages2553–2576. \endbibitem

- Arratia, Goldstein and Gordon (1989) {barticle}[author] \bauthor\bsnmArratia, \bfnmR.\binitsR., \bauthor\bsnmGoldstein, \bfnmL.\binitsL. and \bauthor\bsnmGordon, \bfnmL.\binitsL. (\byear1989). \btitleTwo moments suffice for Poisson approximations: the Chen-Stein method. \bjournalAnn. Probab. \bvolume17 \bpages9–25. \endbibitem

- Berman (1964) {barticle}[author] \bauthor\bsnmBerman, \bfnmSimeon M.\binitsS. M. (\byear1964). \btitleLimit theorems for the maximum term in stationary sequences. \bjournalAnn. Math. Statist. \bvolume35 \bpages502–516. \endbibitem

- Bickel and Levina (2008a) {barticle}[author] \bauthor\bsnmBickel, \bfnmPeter J.\binitsP. J. and \bauthor\bsnmLevina, \bfnmElizaveta\binitsE. (\byear2008a). \btitleCovariance regularization by thresholding. \bjournalAnn. Statist. \bvolume36 \bpages2577–2604. \endbibitem

- Bickel and Levina (2008b) {barticle}[author] \bauthor\bsnmBickel, \bfnmPeter J.\binitsP. J. and \bauthor\bsnmLevina, \bfnmElizaveta\binitsE. (\byear2008b). \btitleRegularized estimation of large covariance matrices. \bjournalAnn. Statist. \bvolume36 \bpages199–227. \endbibitem

- Box and Pierce (1970) {barticle}[author] \bauthor\bsnmBox, \bfnmG. E. P.\binitsG. E. P. and \bauthor\bsnmPierce, \bfnmDavid A.\binitsD. A. (\byear1970). \btitleDistribution of residual autocorrelations in autoregressive-integrated moving average time series models. \bjournalJ. Amer. Statist. Assoc. \bvolume65 \bpages1509–1526. \endbibitem

- Brillinger (2001) {bbook}[author] \bauthor\bsnmBrillinger, \bfnmDavid R.\binitsD. R. (\byear2001). \btitleTime series. \bseriesClassics in Applied Mathematics \bvolume36. \bpublisherSociety for Industrial and Applied Mathematics (SIAM), \baddressPhiladelphia, PA. \bnoteData analysis and theory, Reprint of the 1981 edition. \endbibitem

- Brockwell and Davis (1991) {bbook}[author] \bauthor\bsnmBrockwell, \bfnmPeter J.\binitsP. J. and \bauthor\bsnmDavis, \bfnmRichard A.\binitsR. A. (\byear1991). \btitleTime series: theory and methods, \beditionSecond ed. \bseriesSpringer Series in Statistics. \bpublisherSpringer-Verlag, \baddressNew York. \endbibitem

- Burkholder (1988) {barticle}[author] \bauthor\bsnmBurkholder, \bfnmDonald L.\binitsD. L. (\byear1988). \btitleSharp inequalities for martingales and stochastic integrals. \bjournalAstérisque \banumber157-158 \bpages75–94. \bnoteColloque Paul Lévy sur les Processus Stochastiques (Palaiseau, 1987). \endbibitem

- Cai and Jiang (2010) {btechreport}[author] \bauthor\bsnmCai, \bfnmTony\binitsT. and \bauthor\bsnmJiang, \bfnmTiefeng\binitsT. (\byear2010). \btitleLimiting laws of coherence of random matrices with applications to testing covariance structure and construction of compressed sensing matrices \btypeTechnical Report, \binstitutionUniversity of Pennsylvania and University of Minnesota. \endbibitem

- Davison and Hinkley (1997) {bbook}[author] \bauthor\bsnmDavison, \bfnmA. C.\binitsA. C. and \bauthor\bsnmHinkley, \bfnmD. V.\binitsD. V. (\byear1997). \btitleBootstrap methods and their application. \bseriesCambridge Series in Statistical and Probabilistic Mathematics \bvolume1. \bpublisherCambridge University Press, \baddressCambridge. \endbibitem

- Deo (1972) {barticle}[author] \bauthor\bsnmDeo, \bfnmChandrakant M.\binitsC. M. (\byear1972). \btitleSome limit theorems for maxima of absolute values of Gaussian sequences. \bjournalSankhyā Ser. A \bvolume34 \bpages289–292. \endbibitem

- Deo (2000) {barticle}[author] \bauthor\bsnmDeo, \bfnmRohit S.\binitsR. S. (\byear2000). \btitleSpectral tests of the martingale hypothesis under conditional heteroscedasticity. \bjournalJ. Econometrics \bvolume99 \bpages291–315. \endbibitem

- Duchesne, Li and Vandermeerschen (2010) {barticle}[author] \bauthor\bsnmDuchesne, \bfnmPierre\binitsP., \bauthor\bsnmLi, \bfnmLinyuan\binitsL. and \bauthor\bsnmVandermeerschen, \bfnmJill\binitsJ. (\byear2010). \btitleOn testing for serial correlation of unknown form using wavelet thresholding. \bjournalComputational Statistics and Data Analysis \bvolume54 \bpages2512 - 2531. \endbibitem

- Durbin and Watson (1950) {barticle}[author] \bauthor\bsnmDurbin, \bfnmJ.\binitsJ. and \bauthor\bsnmWatson, \bfnmG. S.\binitsG. S. (\byear1950). \btitleTesting for serial correlation in least squares regression. I. \bjournalBiometrika \bvolume37 \bpages409–428. \endbibitem

- Durbin and Watson (1951) {barticle}[author] \bauthor\bsnmDurbin, \bfnmJ.\binitsJ. and \bauthor\bsnmWatson, \bfnmG. S.\binitsG. S. (\byear1951). \btitleTesting for serial correlation in least squares regression. II. \bjournalBiometrika \bvolume38 \bpages159–178. \endbibitem

- Durlauf (1991) {barticle}[author] \bauthor\bsnmDurlauf, \bfnmSteven N.\binitsS. N. (\byear1991). \btitleSpectral based testing of the martingale hypothesis. \bjournalJ. Econometrics \bvolume50 \bpages355–376. \endbibitem

- Einmahl and Mason (1997) {barticle}[author] \bauthor\bsnmEinmahl, \bfnmUwe\binitsU. and \bauthor\bsnmMason, \bfnmDavid M.\binitsD. M. (\byear1997). \btitleGaussian approximation of local empirical processes indexed by functions. \bjournalProbab. Theory Related Fields \bvolume107 \bpages283–311. \endbibitem

- Escanciano and Lobato (2009) {barticle}[author] \bauthor\bsnmEscanciano, \bfnmJ. Carlos\binitsJ. C. and \bauthor\bsnmLobato, \bfnmIgnacio N.\binitsI. N. (\byear2009). \btitleAn automatic Portmanteau test for serial correlation. \bjournalJ. Econometrics \bvolume151 \bpages140–149. \endbibitem

- Fan (1996) {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. (\byear1996). \btitleTest of significance based on wavelet thresholding and Neyman’s truncation. \bjournalJ. Amer. Statist. Assoc. \bvolume91 \bpages674–688. \endbibitem

- Grenander and Szegö (1958) {bbook}[author] \bauthor\bsnmGrenander, \bfnmUlf\binitsU. and \bauthor\bsnmSzegö, \bfnmGabor\binitsG. (\byear1958). \btitleToeplitz forms and their applications. \bseriesCalifornia Monographs in Mathematical Sciences. \bpublisherUniversity of California Press, \baddressBerkeley. \endbibitem

- Haeusler (1984) {barticle}[author] \bauthor\bsnmHaeusler, \bfnmErich\binitsE. (\byear1984). \btitleAn exact rate of convergence in the functional central limit theorem for special martingale difference arrays. \bjournalZ. Wahrsch. Verw. Gebiete \bvolume65 \bpages523–534. \endbibitem

- Hall (1979) {barticle}[author] \bauthor\bsnmHall, \bfnmPeter\binitsP. (\byear1979). \btitleOn the rate of convergence of normal extremes. \bjournalJ. Appl. Probab. \bvolume16 \bpages433–439. \endbibitem

- Hall and Heyde (1980) {bbook}[author] \bauthor\bsnmHall, \bfnmP.\binitsP. and \bauthor\bsnmHeyde, \bfnmC. C.\binitsC. C. (\byear1980). \btitleMartingale limit theory and its application. \bpublisherAcademic Press Inc. [Harcourt Brace Jovanovich Publishers], \baddressNew York. \bnoteProbability and Mathematical Statistics. \endbibitem

- Hannan (1973) {barticle}[author] \bauthor\bsnmHannan, \bfnmE. J.\binitsE. J. (\byear1973). \btitleCentral limit theorems for time series regression. \bjournalZ. Wahrscheinlichkeitstheorie und Verw. Gebiete \bvolume26 \bpages157–170. \endbibitem

- Hannan (1974) {barticle}[author] \bauthor\bsnmHannan, \bfnmE. J.\binitsE. J. (\byear1974). \btitleThe uniform convergence of autocovariances. \bjournalAnn. Statist. \bvolume2 \bpages803–806. \endbibitem

- Hannan and Deistler (1988) {bbook}[author] \bauthor\bsnmHannan, \bfnmE. J.\binitsE. J. and \bauthor\bsnmDeistler, \bfnmManfred\binitsM. (\byear1988). \btitleThe statistical theory of linear systems. \bseriesWiley Series in Probability and Mathematical Statistics. \bpublisherJohn Wiley & Sons Inc., \baddressNew York. \endbibitem

- Hannan and Heyde (1972) {barticle}[author] \bauthor\bsnmHannan, \bfnmE. J.\binitsE. J. and \bauthor\bsnmHeyde, \bfnmC. C.\binitsC. C. (\byear1972). \btitleOn limit theorems for quadratic functions of discrete time series. \bjournalAnn. Math. Statist. \bvolume43 \bpages2058–2066. \endbibitem

- Hong (1996) {barticle}[author] \bauthor\bsnmHong, \bfnmYongmiao\binitsY. (\byear1996). \btitleConsistent testing for serial correlation of unknown form. \bjournalEconometrica \bvolume64 \bpages837–864. \endbibitem

- Hong and Lee (2003) {bunpublished}[author] \bauthor\bsnmHong, \bfnmY.\binitsY. and \bauthor\bsnmLee, \bfnmY. J.\binitsY. J. (\byear2003). \btitleConsistent testing for serial uncorrelation of unknown form under general conditional heteroscedasticity. \bnotePreprint, Cornell University, Department of Economics. \endbibitem

- Horn and Johnson (1990) {bbook}[author] \bauthor\bsnmHorn, \bfnmRoger A.\binitsR. A. and \bauthor\bsnmJohnson, \bfnmCharles R.\binitsC. R. (\byear1990). \btitleMatrix analysis. \bpublisherCambridge University Press, \baddressCambridge. \bnoteCorrected reprint of the 1985 original. \endbibitem

- Horowitz et al. (2006) {barticle}[author] \bauthor\bsnmHorowitz, \bfnmJoel L.\binitsJ. L., \bauthor\bsnmLobato, \bfnmI. N.\binitsI. N., \bauthor\bsnmNankervis, \bfnmJohn C.\binitsJ. C. and \bauthor\bsnmSavin, \bfnmN. E.\binitsN. E. (\byear2006). \btitleBootstrapping the Box-Pierce Q test: A robust test of uncorrelatedness. \bjournalJ. Econometrics \bvolume133 \bpages841-862. \endbibitem

- Hosoya and Taniguchi (1982) {barticle}[author] \bauthor\bsnmHosoya, \bfnmYuzo\binitsY. and \bauthor\bsnmTaniguchi, \bfnmMasanobu\binitsM. (\byear1982). \btitleA central limit theorem for stationary processes and the parameter estimation of linear processes. \bjournalAnn. Statist. \bvolume10 \bpages132–153. \endbibitem

- Jiang (2004) {barticle}[author] \bauthor\bsnmJiang, \bfnmTiefeng\binitsT. (\byear2004). \btitleThe asymptotic distributions of the largest entries of sample correlation matrices. \bjournalAnn. Appl. Probab. \bvolume14 \bpages865–880. \endbibitem

- Jirak (2011) {barticle}[author] \bauthor\bsnmJirak, \bfnmMoritz\binitsM. (\byear2011). \btitleOn the maximum of covariance estimators. \bjournalJournal of Multivariate Analysis \bvolume102 \bpages1032 - 1046. \endbibitem

- Künsch (1989) {barticle}[author] \bauthor\bsnmKünsch, \bfnmHans R.\binitsH. R. (\byear1989). \btitleThe jackknife and the bootstrap for general stationary observations. \bjournalAnn. Statist. \bvolume17 \bpages1217–1241. \endbibitem

- Lee and Hong (2001) {barticle}[author] \bauthor\bsnmLee, \bfnmJin\binitsJ. and \bauthor\bsnmHong, \bfnmYongmiao\binitsY. (\byear2001). \btitleTesting for serial correlation of unknown form using wavelet methods. \bjournalEconometric Theory \bvolume17 \bpages386–423. \endbibitem

- Liu, Lin and Shao (2008) {barticle}[author] \bauthor\bsnmLiu, \bfnmWei-Dong\binitsW.-D., \bauthor\bsnmLin, \bfnmZhengyan\binitsZ. and \bauthor\bsnmShao, \bfnmQi-Man\binitsQ.-M. (\byear2008). \btitleThe asymptotic distribution and Berry-Esseen bound of a new test for independence in high dimension with an application to stochastic optimization. \bjournalAnn. Appl. Probab. \bvolume18 \bpages2337–2366. \endbibitem

- Liu and Wu (2010) {barticle}[author] \bauthor\bsnmLiu, \bfnmWeidong\binitsW. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2010). \btitleAsymptotics of spectral density estimates. \bjournalEconometric Theory \bvolume26 \bpages1218-1245. \endbibitem

- Ljung and Box (1978) {barticle}[author] \bauthor\bsnmLjung, \bfnmGM\binitsG. and \bauthor\bsnmBox, \bfnmGeorge E. P.\binitsG. E. P. (\byear1978). \btitleMeasure of lack of fit in time-series models. \bjournalBiometrika \bvolume65 \bpages297-303. \endbibitem

- Nagaev (1979) {barticle}[author] \bauthor\bsnmNagaev, \bfnmS. V.\binitsS. V. (\byear1979). \btitleLarge deviations of sums of independent random variables. \bjournalAnn. Probab. \bvolume7 \bpages745–789. \endbibitem

- Phillips and Solo (1992) {barticle}[author] \bauthor\bsnmPhillips, \bfnmPeter C. B.\binitsP. C. B. and \bauthor\bsnmSolo, \bfnmVictor\binitsV. (\byear1992). \btitleAsymptotics for linear processes. \bjournalAnn. Statist. \bvolume20 \bpages971–1001. \endbibitem

- Plackett (1954) {barticle}[author] \bauthor\bsnmPlackett, \bfnmR. L.\binitsR. L. (\byear1954). \btitleA reduction formula for normal multivariate integrals. \bjournalBiometrika \bvolume41 \bpages351–360. \endbibitem

- Rio (2009) {barticle}[author] \bauthor\bsnmRio, \bfnmEmmanuel\binitsE. (\byear2009). \btitleMoment inequalities for sums of dependent random variables under projective conditions. \bjournalJ. Theoret. Probab. \bvolume22 \bpages146–163. \endbibitem

- Robinson (1991) {barticle}[author] \bauthor\bsnmRobinson, \bfnmP. M.\binitsP. M. (\byear1991). \btitleTesting for strong serial correlation and dynamic conditional heteroskedasticity in multiple regression. \bjournalJ. Econometrics \bvolume47 \bpages67–84. \endbibitem

- Romano and Thombs (1996) {barticle}[author] \bauthor\bsnmRomano, \bfnmJoseph P.\binitsJ. P. and \bauthor\bsnmThombs, \bfnmLori A.\binitsL. A. (\byear1996). \btitleInference for autocorrelations under weak assumptions. \bjournalJ. Amer. Statist. Assoc. \bvolume91 \bpages590–600. \endbibitem

- Rosenblatt (1985) {bbook}[author] \bauthor\bsnmRosenblatt, \bfnmMurray\binitsM. (\byear1985). \btitleStationary sequences and random fields. \bpublisherBirkhäuser Boston Inc., \baddressBoston, MA. \endbibitem

- Schott (2005) {barticle}[author] \bauthor\bsnmSchott, \bfnmJames R.\binitsJ. R. (\byear2005). \btitleTesting for complete independence in high dimensions. \bjournalBiometrika \bvolume92 \bpages951–956. \endbibitem

- Shao (2011) {barticle}[author] \bauthor\bsnmShao, \bfnmXiaofeng\binitsX. (\byear2011). \btitleTesting for white noise under unknown dependence and its applications to diagnostic checking for time series models. \bjournalEconometric Theory \bvolumeFirstView \bpages1-32. \bnotehttp://dx.doi.org/10.1017/S0266466610000253. \endbibitem

- Tong (1981) {barticle}[author] \bauthor\bsnmTong, \bfnmH.\binitsH. (\byear1981). \btitleA note on a Markov bilinear stochastic process in discrete time. \bjournalJ. Time Ser. Anal. \bvolume2 \bpages279–284. \endbibitem

- Tong (1990) {bbook}[author] \bauthor\bsnmTong, \bfnmHowell\binitsH. (\byear1990). \btitleNonlinear time series. \bseriesOxford Statistical Science Series \bvolume6. \bpublisherThe Clarendon Press Oxford University Press, \baddressNew York. \bnoteA dynamical system approach,. \endbibitem

- Wiener (1958) {bbook}[author] \bauthor\bsnmWiener, \bfnmNorbert\binitsN. (\byear1958). \btitleNonlinear problems in random theory. \bseriesTechnology Press Research Monographs. \bpublisherThe Technology Press of The Massachusetts Institute of Technology and John Wiley & Sons, Inc., New York. \endbibitem

- Wu (2005) {barticle}[author] \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2005). \btitleNonlinear system theory: another look at dependence. \bjournalProc. Natl. Acad. Sci. USA \bvolume102 \bpages14150–14154 (electronic). \endbibitem

- Wu (2007) {barticle}[author] \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2007). \btitleStrong invariance principles for dependent random variables. \bjournalAnn. Probab. \bvolume35 \bpages2294–2320. \endbibitem

- Wu (2009) {barticle}[author] \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2009). \btitleAn asymptotic theory for sample covariances of Bernoulli shifts. \bjournalStochastic Process. Appl. \bvolume119 \bpages453–467. \endbibitem

- Wu and Shao (2004) {barticle}[author] \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. and \bauthor\bsnmShao, \bfnmXiaofeng\binitsX. (\byear2004). \btitleLimit theorems for iterated random functions. \bjournalJ. Appl. Probab. \bvolume41 \bpages425–436. \endbibitem

- Xiao and Wu (2010) {bunpublished}[author] \bauthor\bsnmXiao, \bfnmHan\binitsH. and \bauthor\bsnmWu, \bfnmWei Biao\binitsW. B. (\byear2010). \btitleCovariance matrix estimation for stationary time series. \bnotepreprint. \endbibitem

- Zhou (2007) {barticle}[author] \bauthor\bsnmZhou, \bfnmWang\binitsW. (\byear2007). \btitleAsymptotic distribution of the largest off-diagonal entry of correlation matrices. \bjournalTrans. Amer. Math. Soc. \bvolume359 \bpages5345–5363. \endbibitem