Divergence of the multilevel Monte Carlo Euler method for nonlinear stochastic differential equations

Abstract

The Euler–Maruyama scheme is known to diverge strongly and numerically weakly when applied to nonlinear stochastic differential equations (SDEs) with superlinearly growing and globally one-sided Lipschitz continuous drift coefficients. Classical Monte Carlo simulations do, however, not suffer from this divergence behavior of Euler’s method because this divergence behavior happens on rare events. Indeed, for such nonlinear SDEs the classical Monte Carlo Euler method has been shown to converge by exploiting that the Euler approximations diverge only on events whose probabilities decay to zero very rapidly. Significantly more efficient than the classical Monte Carlo Euler method is the recently introduced multilevel Monte Carlo Euler method. The main observation of this article is that this multilevel Monte Carlo Euler method does—in contrast to classical Monte Carlo methods—not converge in general in the case of such nonlinear SDEs. More precisely, we establish divergence of the multilevel Monte Carlo Euler method for a family of SDEs with superlinearly growing and globally one-sided Lipschitz continuous drift coefficients. In particular, the multilevel Monte Carlo Euler method diverges for these nonlinear SDEs on an event that is not at all rare but has probability one. As a consequence for applications, we recommend not to use the multilevel Monte Carlo Euler method for SDEs with superlinearly growing nonlinearities. Instead we propose to combine the multilevel Monte Carlo method with a slightly modified Euler method. More precisely, we show that the multilevel Monte Carlo method combined with a tamed Euler method converges for nonlinear SDEs with globally one-sided Lipschitz continuous drift coefficients and preserves its strikingly higher order convergence rate from the Lipschitz case.

doi:

10.1214/12-AAP890keywords:

[class=AMS]keywords:

T1Supported in part by the research project “Numerical solutions of stochastic differential equations with nonglobally Lipschitz continuous coefficients” and by the Collaborative Research Centre “Spectral Structures and Topological Methods in Mathematics,” both funded by the German Research Foundation.

, and

1 Introduction

We consider the following setting in this introductory section. Let , , let be a probability space with a normal filtration and let be an -measurable mapping with for all . Moreover, let be a smooth globally one-sided Lipschitz continuous function with at most polynomially growing derivatives, and let be a smooth globally Lipschitz continuous function with at most polynomially growing derivatives. In particular, we assume that there exists a real number such that and for all . These assumptions ensure the existence of an up to indistinguishability unique adapted stochastic process with continuous sample paths solving the stochastic differential equation (SDE)

| (1) |

for ; see, for example, Alyushina Alyushina1987 , Theorem 1 in Krylov Krylov1990 or Theorem 2.4.1 in Mao m97 . The function is the drift coefficient, and the function is the diffusion coefficient of the SDE (1). Our goal in this introductory section is then to efficiently compute the deterministic real number

| (2) |

where is a smooth function with at most polynomially growing derivatives. Note that this question is not treated in the standard literature in computational stochastics (see, e.g., Kloeden and Platen kp92 and Milstein m95 ) which concentrates on SDEs with globally Lipschitz continuous coefficients rather than the SDE (1). The computation of statistical quantities of the form (2) for SDEs with nonglobally Lipschitz continuous coefficients is an important aspect in financial engineering, in particular, in option pricing. For details the reader is refereed to the monographs Lewis l00 , Glasserman g04 , Higham h04 and Szpruch s10 .

In order to simulate the quantity (2) on a computer, one has to discretize both the solution process of the SDE (1) as well as the underlying probability space . The simplest method for discretizing the SDE (1) is the Euler method (a.k.a. Euler–Maruyama method). More formally, the Euler approximations , , , for the SDE (1) are defined recursively through and

| (3) |

for all and all . Convergence of Euler’s method both in the strong as well as in the numerically weak sense is well known in the case of globally Lipschitz continuous coefficients and of the SDE; see, for example, Section 14.1 in Kloeden and Platen kp92 and Section 12 in Milstein m95 . The case of superlinearly growing and hence nonglobally Lipschitz continuous coefficients of the SDE is more subtle. Indeed, Theorem 2.1 in the recent article hjk11 shows in the presence of noise that Euler’s method diverges to infinity both in the strong and numerically weak sense if the coefficients of the SDE grow superlinearly; see Theorem 2.1 below for a generalization hereof. In this situation, Theorem 2.1 in hjk11 also proves the existence of events , , and of real numbers such that and for all , . Clearly, this implies the divergence of absolute moments of the Euler approximation, that is, for all .

The classical method for discretizing expectations is the Monte Carlo Euler method. Let , , , for be suitable independent copies of the Euler approximations (3); see Section 3 for the precise definition. The Monte Carlo Euler approximation of (2) with time steps and Monte Carlo runs (see Duffie and Glynn dg95b for more details on this choice) is then the random real number

| (4) |

Convergence of the Monte Carlo Euler approximations (4) is well known in the case of globally Lipschitz continuous coefficients and ; see, for example, Section 14.1 in Kloeden and Platen kp92 and Section 12 in Milstein m95 . Recently, convergence of the Monte Carlo Euler approximations (4) has also been established for the SDE (1). More formally, Corollary 3.23 in HutzenthalerJentzen2012PhiArxiv (which generalizes Theorem 2.1 in hj11 ) implies

| (5) |

-almost surely; see also Theorem 3.1 below. The Monte Carlo Euler method is thus strongly consistent (see, e.g., Nikulin n01 , Cramér c99 or Appendix A.1 in Glasserman g04 ) for the SDE (1). The reason why convergence (5) of the Monte Carlo Euler method does hold although the Euler approximations diverge is as follows. The events , , on which Euler’s method diverges (see Theorem 2.1 below) are rare events and their probabilities decay to zero faster than any polynomial in as ; see Lemma 2.6 in hjk10b for details. Therefore, for large the event is too unlikely to occur in any of Monte Carlo simulations in (4).

Considerably more efficient than the Monte Carlo Euler method are the so-called multilevel Monte Carlo Euler methods in Giles g08b ; see also Creutzig et al. cdmr09 , Dereich dereich2011 , Giles g08a , Giles, Higham and Mao ghm09 , Heinrich h98 , heinrich01 , Heinrich and Sindambiwe hs99 and Kebaier k05 for related results. In this method, time is discretized through the Euler method and expectations are approximated by the multilevel Monte Carlo method. More formally, let , , , for and be suitable independent copies of the Euler approximations (3); see Section 6 for the precise definition. Then the multilevel Monte Carlo Euler approximations for the SDE (1) which we investigate in this article are defined as

| (6) |

for . Clearly, there are also other multilevel Monte Carlo methods than (6); see, for example, Giles g08b for more details. For simplicity, we refer to (6) as the multilevel Monte Carlo Euler method throughout this article. In the case of globally Lipschitz continuous coefficients of the SDE (1), this method has been shown to converge significantly faster to the target quantity (2) than the Monte Carlo Euler method (4). More precisely, in the case of globally Lipschitz continuous coefficients and , the multilevel Monte Carlo Euler method (6) converges with order while the Monte Carlo Euler method converges with order with respect to the computational effort; see Section 1 in Giles g08b or Creutzig et al. cdmr09 for details. In the general setting of the SDE (1) where does not need to be globally Lipschitz continuous, convergence of the multilevel Monte Carlo Euler method (6) remained an open question.

The convergence (5) of the Monte Carlo Euler method, and the fact that Euler’s method diverges on very rare events only, shaped our first guess that the multilevel Monte Carlo Euler method should converge too. However, convergence of the multilevel Monte Carlo Euler method fails to hold in the general setting of the SDE (1). To prove this, it suffices to establish nonconvergence for one counterexample which we choose to be as follows. Let , let , , for all and let be standard normally distributed. Clearly, this choice satisfies the assumptions of the SDE (1) and the SDE (1) thus reduces to the random ordinary differential equation

| (7) |

for . The main observation of this article is that the approximation error of the multilevel Monte Carlo Euler method for the SDE (7) diverges to infinity. More formally, Theorem 4.1 below implies

| (8) | |||

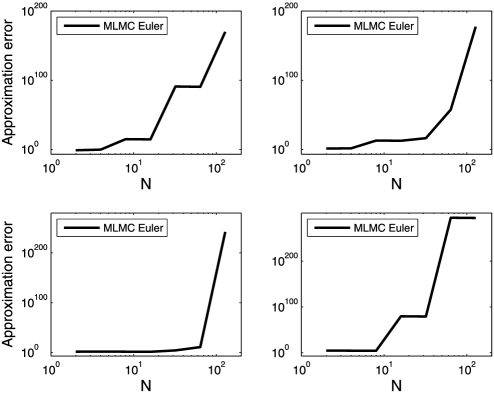

-almost surely. Note that the multilevel Monte Carlo Euler method diverges on an event that is not rare but has probability one. Thus—in contrast to classical Monte Carlo simulations—the multilevel Monte Carlo Euler method is very sensitive to the rare events on which Euler’s method diverges in the sense of Theorem 2.1 below. To visualize the divergence (1), Figure 1 depicts four random sample paths of the approximation error of the multilevel Monte Carlo Euler method (6) for the SDE (7) with and shows explosion even for small values of . We emphasize that we are only able to establish the divergence (1) for the simple SDE (7). Even in this simple case, the proof of the divergence (1) is rather involved and requires precise estimates on the speed of divergence of Euler’s method for the random ordinary differential equation (7) on an appropriate event of instability; see below for an outline.

Comparing the convergence result (5) for the Monte Carlo Euler method and the divergence result (1) for the multilevel Monte Carlo Euler method reveals a remarkable difference between the classical Monte Carlo Euler method and the new multilevel Monte Carlo Euler method. The classical Monte Carlo Euler method applies both to SDEs with globally Lipschitz continuous coefficients and to SDEs with possibly superlinearly growing coefficients such as our SDE (1). The multilevel Monte Carlo Euler method, however, produces often completely wrong values in the case of SDEs with superlinearly growing nonlinearities. This is particularly unfortunate as SDEs with superlinearly growing nonlinearities are very important in applications; see, for example, l00 , hmps11 , s10 for applications in financial engineering. We recommend not to use the multilevel Monte Carlo Euler method for applications with such nonlinear SDEs.

Nonetheless, the multilevel Monte Carlo method can be used for SDEs with nonglobally Lipschitz continuous coefficients when being combined with a strongly convergent numerical approximation method. For example, in hjk10b the following slight modification of the Euler method (3) is proposed. Let , , , be defined recursively through and

| (9) |

for all and all . Following hjk10b we refer to this numerical approximation as a tamed Euler method. Additionally, let , , , for and be independent copies of the tamed Euler approximations (9). In Theorem 6.2 below we then prove convergence of the multilevel Monte Carlo tamed Euler method for all locally Lipschitz continuous test functions on the path space whose local Lipschitz constants grow at most polynomially. In particular, Theorem 6.2 below implies the existence of finite random variables , , such that

| (10) | |||

for all and all -almost surely. To sum it up, the classical Monte Carlo Euler method converges [see (5)], the new multilevel Monte Carlo Euler method, in general, fails to converge [see (1)] and the new multilevel Monte Carlo tamed Euler method converges and preserves its striking higher convergence order from the Lipschitz case [see (1)]. Thus, concerning applications, the message of this article is that the multilevel Monte Carlo Euler method (6) needs to be modified appropriately when being applied to SDEs with superlinearly growing nonlinearities. This is a crucial difference to the classical Monte Euler method which has been shown to converge for such SDEs and which does not need to be modified. However, when modified appropriately [see, e.g., (9)], the multilevel Monte Carlo method preserves its strikingly higher convergence order from the global Lipschitz case and is significantly more efficient than the classical Monte Carlo Euler method, even for such nonlinear SDEs. Thereby, this article motivates future research in the construction and the analysis of “appropriately modified” numerical approximation methods.

For the interested reader, we now outline the central ideas in the proof of (1). For this we use the random variables , , , defined by for all , , . Then we note for every , and every that is strictly increasing in if and only if . It turns out that increases in double exponentially fast for all , and all ; see Lemma 4.4 and Corollary 4.7 below for details. A central observation in our proof of the divergence (1) is then that the behavior of the multilevel Monte Carlo Euler method is dominated by the highest level that produces such double exponentially fast increasing trajectories. More precisely, a key step in our proof of (1) is to introduce the random variables , , by

for all . Using the random variables , , we now rewrite the multilevel Monte Carlo Euler method in (1) as

| (12) | |||

| (13) | |||

| (14) | |||

| (15) | |||

| (16) |

for all . Due to the definition of , , it turns out that the asymptotic behavior of the multilevel Monte Carlo Euler method (12) is essentially determined by the three sums in (14)–(16); see inequality (4.2), estimate (4.2) and inequalities (4.2), (4.2) in the proof of Theorem 4.1 for details. In order to investigate these three summands, we—roughly speaking—quantify the value of the largest summand in each of the three sums in (14)–(16). For this we introduce the random variables and for by

| (17) |

and

| (18) |

for all . Using the random variables and for we then distinguish between three different cases [see inequality (4.2), inequality (4.2) and inequalities (4.2), (4.2) below]. First, on the events , , the middle sum in (15) will be positive with large absolute value and will essentially determine the behavior of the multilevel Monte Carlo Euler approximations (12); see estimate (4.2) for details. Second, on the events , , the sum in (14) will be positive with large absolute value and will essentially determine the behavior of the multilevel Monte Carlo Euler approximations (12); see inequality (4.2) for details. Finally, on the events , , the sum in (16) will be negative with large absolute value and will essentially determine the behavior of the multilevel Monte Carlo Euler approximations (12); see inequalities (4.2) and (4.2) for details. This very rough outline of the case-by-case analysis in our proof of (1) also illustrates that the multilevel Monte Carlo Euler approximations (12) assume both positive (first and second case) as well as negative values (third case) with large absolute values. We add that this case-by-case analysis argument in our proof of (1) requires that the probability that the random variables and are close to each other in some sense must decay rapidly to zero as goes to infinity; see inequality (117) below. We verify the above decaying of the probabilities in Lemma .5 below which is a crucial step in our proof of (1). Additionally, we add that the level is approximately of order as goes to infinity; see Lemma .1 for the precise assertion. In view of the above case-by-case analysis of the multilevel Monte Carlo Euler method, we find it quite remarkable to observe that the essential behaviour of the multilevel Monte Carlo Euler method in (1) is determined by the levels around the order as goes to infinity.

The remainder of this article is organized as follows. Theorem 2.1 in Section 2 slightly generalizes the result on strong and weak divergence of the Euler method of Hutzenthaler, Jentzen and Kloeden hjk11 . Convergence of the Monte Carlo Euler method is reviewed in Section 3. The main result of this article, that is, divergence of the multilevel Monte Carlo Euler method for the SDE (7), is presented and proved in Section 4. We believe that the multilevel Monte Carlo Euler method diverges more generally and formulate this as Conjecture 5.1 in Section 5. Section 6 contains our proof of almost sure and strong convergence of the multilevel Monte Carlo tamed Euler method for all locally Lipschitz continuous test functions on the path space whose local Lipschitz constants grow at most polynomially.

2 Divergence of the Euler method

Throughout this section assume that the following setting is fulfilled. Let , let be a probability space with a filtration and let be a one-dimensional standard -Brownian motion. Additionally, let be an -measurable mapping and let be two -measurable mappings. We then define the Euler approximations , , , recursively by and

| (19) |

for all and all . The following theorem generalizes Theorem 2.1 in Hutzenthaler, Jentzen and Kloeden hjk11 .

Theorem 2.1 ((Strong and weak divergence of the Euler method))

Assume that the above setting is fulfilled, and let be real numbers such that for all with . Moreover, assume that or that there exists a real number such that for all . Then there exists a real number and a sequence of nonempty events , , such that and for all and all . In particular, the Euler approximations (19) satisfy for all .

Theorem 2.1 immediately follows from Lemmas 2.2 and 2.3 below. More results on Euler’s method for SDEs with possibly superlinearly growing nonlinearities can, for example, be found in gk96b , g98b , mt04 , mt05 and in the references therein.

Lemma 2.2 ((Tails of , )).

Assume that the above setting is fulfilled and let . Then there exists a real number such that for all and all .

By assumption we have . Therefore, there exists a real number such that

| (20) |

Moreover, we have

for all and all . Definition (20) and Lemma 4.1 in hjk11 therefore show

for all and all . This completes the proof of Lemma 2.2.

Lemma 2.3.

Assume that the above setting is fulfilled and let be real numbers such that for all with . Moreover, assume that there exist real numbers , such that for all and all . Then there exists a real number and a sequence of nonempty events , , such that and for all and all . In particular, the Euler approximations (19) satisfy for all .

Define real numbers , , by

| (21) |

for all . We also use the function defined by for all and by for all . Furthermore, we define events , , by

for all . In particular, the definition of implies

for all , and all .

In the next step let and be arbitrary. We then claim

| (24) |

for all . We now show (24) by induction on . The base case follows from definition (2) of . For the induction step assume that (24) holds for one . In particular, this implies

| (25) |

Moreover, definition (19), the triangle inequality and equation (2) yield

and the estimate for all with , inequality (25) and definition (21) therefore show

The induction hypothesis hence yields

Inequality (24) thus holds for all , and all . In particular, we obtain

| (26) |

for all and all . Additionally, Lemma 4.1 in hjk11 yields

| (27) | |||

-almost surely for all and all . Therefore, we obtain

for all . This shows the existence of a real number such that

| (28) |

for all . Combining (26) and (28) finally gives

for all . This, (26) and (28) then complete the proof of Theorem 2.1.

3 Convergence of the Monte Carlo Euler method

The Monte Carlo Euler method has been shown to converge with probability one for one-dimensional SDEs with superlinearly growing and globally one-sided Lipschitz continuous drift coefficients and with globally Lipschitz continuous diffusion coefficients; see hj11 . The Monte Carlo Euler method is thus strongly consistent (see, e.g., Nikulin n01 , Cramér c99 or Appendix A.1 in Glasserman g04 ) for such SDEs. After having reviewed this convergence result of the Monte Carlo Euler method, we complement in this section this convergence result with the behavior of moments of the Monte Carlo Euler approximations for such SDEs. More precisely, an immediate consequence of Theorem 2.1 is Corollary 3.2 below which shows for such SDEs that the Monte Carlo Euler approximations diverge in the strong -sense for every . We emphasize that this strong divergence result does not reflect the behavior of the Monte Carlo Euler method in a simulation and it is presented for completeness only. Indeed, the events on which the Euler approximations diverge (see Theorem 2.1) are rare events, and their probabilities decay to zero very rapidly; see, for example, Lemma 4.5 in hj11 for details. This is the reason why the Monte Carlo Euler method is strongly consistent and thus does converge according to hj11 ; see also Theorem 3.1 below and Corollary 3.23 in HutzenthalerJentzen2012PhiArxiv .

Throughout this section assume that the following setting is fulfilled. Let , let be a probability space with a normal filtration , let , , be a family of independent one-dimensional standard -Brownian motions and let , , be a family of independent identically distributed -measurable mappings with for all . Moreover, let be two -measurable mappings such that there exists a predictable stochastic process which satisfies -almost surely and

| (29) |

-almost surely for all . The drift coefficient is the infinitesimal mean of the process and the diffusion coefficient is the infinitesimal standard deviation of the process . We then define a family , , , of Euler approximations by and

| (30) |

for all and all . For clarity of exposition we recall the following convergence theorem from hj11 . Its proof can be found in hj11 .

Theorem 3.1 ((Strong consistency and convergence with probability one of the Monte Carlo Euler method))

Assume that the above setting is fulfilled, let be four times continuously differentiable and let be a real number such that , and for all . Then there exist finite -measurable mappings , , such that

| (31) |

for all and all -almost surely.

In contrast to pathwise convergence of the Monte Carlo Euler method for SDEs with globally one-sided Lipschitz continuous drift and globally Lipschitz continuous diffusion coefficients (see Theorem 3.1 above for details), strong convergence of the Monte Carlo Euler method, in general, fails to hold for such SDEs which is established in the following corollary of Theorem 2.1, that is, in Corollary 3.2. As mentioned above we emphasize that Corollary 3.2 does not reflect the behavior of the Monte Carlo Euler method in a practical simulation because the events on which the Euler approximations diverge (see Theorem 2.1) are rare events, and their probabilities decay to zero very rapidly; see Lemma 4.5 in hj11 for details.

Corollary 3.2 ((Strong divergence of the Monte Carlo Euler method)).

Assume that the above setting is fulfilled and let be real numbers such that for all with . Moreover, assume that or that there exists a real number such that for all . Moreover, let be -measurable with for all . Then

| (32) |

for all .

4 Counterexamples to convergence of the multilevel Monte Carlo Euler method

Theorem 4.1 below establishes divergence with probability one of the multilevel Monte Carlo Euler method (6) for the SDE (7). This, in particular, proves that the multilevel Monte Carlo Euler method is in contrast to the classical Monte Carlo Euler method not consistent (see, e.g., Nikulin n01 , Cramér c99 or Appendix A.1 in Glasserman g04 ) for the SDE (7).

Throughout this section assume that the following setting is fulfilled. Let , let be a probability space and let , , , be a family of independent normally distributed -measurable mappings with mean zero and standard deviation . Moreover, let be the unique stochastic process with continuous sample paths which fulfills the SDE

| (34) |

for . We then define a family of Euler approximations , , , , , by and

| (35) |

for all , , and all .

Theorem 4.1 ([Main result of this article: Divergence with probability one of the multilevel Monte Carlo Euler method for the SDE (34)])

Assume that the above setting is fulfilled. Then

| (36) |

-almost surely for all .

4.1 Simulations

We illustrate Theorem 4.1 with numerical simulations. To this end we observe that the exact solution of the random ordinary differential equation (87) satisfies

| (37) |

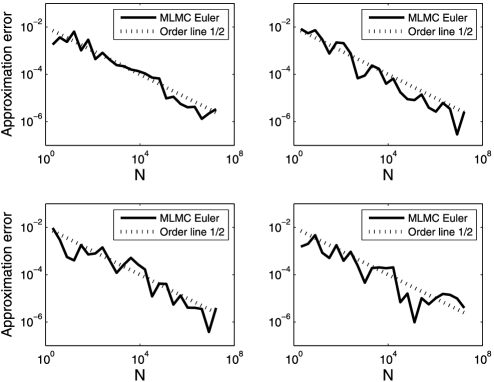

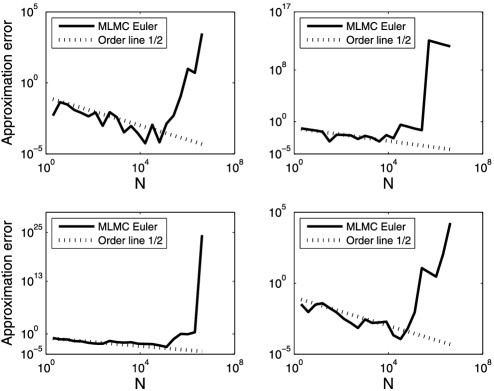

for all . The real number can then be computed approximatively by numerical integration or by the Monte Carlo method. Figure 1 depicts four random sample paths of the approximation error of the multilevel Monte Carlo Euler approximations in the case and in (87) where (calculated with the integrate-function of R). The sample paths clearly diverge even for small . For some other SDEs, however, pathwise divergence does not emerge for small . For example, let us choose a standard deviation as small as in (34) where . Here the exact value satisfies (calculated with the integrate-function of R). Then sample paths of the multilevel Monte Carlo Euler approximation seem to converge even for reasonably large ; see Figure 2 for four sample paths. So the sample paths of the multilevel Monte Carlo Euler method for some SDEs first seem to converge, but diverge as becomes sufficiently large. To see this in a plot, we tried different values of and found sample paths in case of and which first seem to convergence to the exact value (calculated with the integrate-function of R) but diverge for larger values of ; see Figure 3 for four sample paths.

4.2 Proof of Theorem 4.1

First of all, we introduce more notation in order to prove Theorem 4.1. Let , , , , be defined recursively through and

| (38) |

for all , and all and let be fixed for the rest of this section. This notation enables us to rewrite the multilevel Monte Carlo Euler approximation in (36) as

| (39) | |||

for all . Additionally, let be defined as

for every . Furthermore, define and by

| (41) |

and

| (42) |

for every . Moreover, we define the mappings by and by for all . Additionally, we fix a real number for the rest of this section. In the next step the following events are used in our analysis of the multilevel Monte Carlo Euler method. Let , , , , , be defined by

| (43) | |||||

| (46) |

for all . Additionally, define and by and by

for all . Next we prove a few lemmas that we use in our proof of Theorem 4.1.

Lemma 4.2 ((Dynamics for small initial values)).

Assume that the above setting is fulfilled. Then we have for all , and all .

Fix and . We prove by induction on . The base case is trivial. For the induction step , note that the induction hypothesis implies

| (48) |

for all . This completes the proof of Lemma 4.2.

Lemma 4.3 ((Dynamics for large initial values)).

Assume that the above setting is fulfilled. Then we have for all , and all . In particular, we have

| (49) |

for all , and all .

Fix and . We prove by induction on . The base case is trivial. For the induction step , note that the induction hypothesis implies

for all . This completes the induction. Assertion (49) then immediately follows by taking absolute values in (38).

Lemma 4.4 ((Growth bound for large initial values)).

Assume that the above setting is fulfilled. Then we have

| (51) |

for all , and all .

Fix and . We prove (51) by induction on . The base case is trivial. For the induction step , note that Lemma 4.3 and the induction hypothesis imply

for all . This completes the proof of Lemma 4.4.

Lemma 4.5 ((Monotonicity)).

Assume that the above setting is fulfilled. Then we have

| (53) |

for all , all satisfying , and all .

Fix and with , . We prove (53) by induction on . The base case is trivial. For the induction step , note that Lemma 4.3 and the induction hypothesis imply

for all . This completes the proof of Lemma 4.5.

Lemma 4.6 ((Dynamics of multiples of the initial value)).

Assume that the above setting is fulfilled. Then we have

| (55) |

for all , , and all .

Fix . We prove (55) by induction on . The base case is trivial. For the induction step , note that Lemma 4.3 and the induction hypothesis imply

for all , and all . This completes the proof of Lemma 4.6.

Corollary 4.7.

Assume that the above setting is fulfilled. Then we have for all , , and all .

Lemma 4.8.

Assume that the above setting is fulfilled. Then we have

| (58) |

for all , and all .

We apply the inequality for all . Noting that for all and all , we infer from Corollary 4.7

for all , and all . This completes the proof of Lemma 4.8.

Lemma 4.9 ((Almost sure finiteness of )).

Assume that the above setting is fulfilled. Then .

The proof of Lemma 4.9 is postponed to the Appendix. We now present the proof of Theorem 4.1. It makes of use of Lemma 4.9.

Proof of Theorem 4.1 Fix throughout this proof. Our proof of Theorem 4.1 is then divided into four parts. In the first part we analyze the behavior of the multilevel Monte Carlo Euler approximations on the events for ; see inequality (4.2). In the second part of this proof we concentrate on the events for ; see inequality (4.2). In the third part of this proof we investigate the events for [see inequality (4.2)] and in the fourth part we analyze the behavior of the multilevel Monte Carlo Euler approximations on the events for [see inequality (4.2)]. Combining all four parts [inequalities (4.2), (4.2), (4.2) and (4.2)] and Lemma 4.9 will then complete the proof of Theorem 4.1 as we will show below. In these four parts we will frequently use

| (60) |

for all .

We begin with the first part and consider the events for . Note that Lemma 4.5, the inequalities on [see (4.2)] and on for all , [see (4.2)] and the definition (4.2) of imply

| (61) | |||

on and Lemmas 4.8, 4.4 and 4.2 hence yield

on for all . Therefore, we obtain

| (62) | |||

on and the estimate on [see (43)] hence shows

| (63) | |||

on for all where is a function defined by

for all .

In the next step we analyze the behavior of the multilevel Monte Carlo Euler approximations on the events for . To this end note that Lemma 4.5, the inequalities on [see (46)] and on for all , [see (4.2)] and the definition (4.2) of imply

on for all . Lemmas 4.5, 4.4 and 4.2 therefore show

| (64) | |||

on for all . By definition of and of we have on [see (43)] for all . Consequently we get the inequality on [see (4.2)] for all . Lemmas 4.6 and 4.5 hence yield

| (65) | |||

on for all . Lemma 4.8 and therefore imply

on for all . The inequalities and for all hence give

| (66) | |||

on for all . This shows

on for all and, using the estimate on [see (43)],

| (67) | |||

on for all . It follows from

| (68) |

that there exists an such that

| (69) |

for all . Using this, we deduce from (4.2)

| (70) | |||

on for all .

Next, we analyze the behavior of the multilevel Monte Carlo Euler approximations on the events for . Note that Lemma 4.5 and the inequality on for all , [see (4.2)] imply

| (71) | |||

on for all . Therefore Lemma 4.5, the inequality on [see (46)] and Lemma 4.2 result in

| (72) | |||

on for all . Lemmas 4.6, 4.5 and the estimate on [see (43) and (4.2)] and Lemma 4.4 hence yield

on for all . Therefore Lemma 4.8 implies

| (73) | |||

on for all . The inequality for all hence shows

| (74) | |||

on for all . Consequently

on for all . The estimate on [see (43)] therefore implies

on for all . Finally, we obtain

| (75) | |||

on for all .

Finally, we analyze the behavior of the multilevel Monte Carlo Euler approximations on the events for . Note that Lemma 4.5 and the inequality on for all , [see (4.2)] imply

on for all and, applying Lemmas 4.8, 4.5, 4.4 and 4.2,

on for all . Therefore, we obtain

on and hence, using on ,

| (76) | |||

on for all .

5 Divergence of the multilevel Monte Carlo Euler method

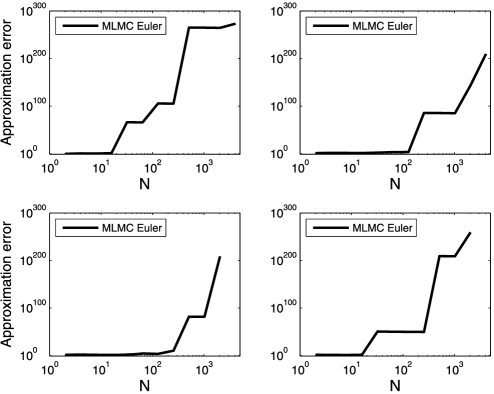

Motivated by Figure 4 below and by the divergence result of the multilevel Monte Carlo Euler method in Section 4, we conjecture in this section that the multilevel Monte Carlo Euler method diverges with probability one whenever one of the coefficients of the SDE grows superlinearly; see Conjecture 5.1. Whereas divergence with probability one seems to be quite difficult to establish, strong divergence is a rather immediate consequence of the divergence of the Euler method in Theorem 2.1 above. We derive this strong divergence in Corollary 5.2 below. For practical simulations the much more important question is, however, consistency and inconsistency, respectively; see, for example, Nikulin n01 , Cramér c99 , Appendix A.1 in Glasserman g04 and also Theorem 4.1 above and Conjecture 5.1 below.

Throughout this section assume that the following setting is fulfilled. Let , let be a probability space with a normal filtration , let , , , be a family of independent one-dimensional standard -Brownian motions and let , , , be a family of independent identically distributed -measurable mappings with for all . Moreover, let be two continuous mappings such that there exists a predictable stochastic process which satisfies -almost surely and

| (81) |

-almost surely for all . The drift coefficient is the infinitesimal mean of the process and the diffusion coefficient is the infinitesimal standard deviation of the process . We then define a family of Euler approximations , , , , , by and

for all , , and all .

Conjecture 5.1 ((Divergence with probability one of the multilevel Monte Carlo Euler method)).

Assume that the above setting is fulfilled and let be real numbers such that for all with . Moreover, assume that or that there exists a real number such that for all . Moreover, let be -measurable with for all . Then we conjecture

| (82) | |||

-almost surely.

To support this conjecture, we ran simulations for the stochastic Ginzburg–Landau equation given by the solution of

| (83) |

for all . Its solution is known explicitly (e.g., Section 4.4 in kp92 ) and is given by

| (84) |

for . We used this explicit solution to compute . Figure 4 shows four sample paths of the approximation error of the multilevel Monte Carlo Euler method for the Ginzburg–Landau equation (83). Only finite values of the sample paths are plotted. The next corollary is an immediate consequence of Theorem 2.1 above.

Corollary 5.2 ((Strong divergence of the multilevel Monte Carlo Euler method)).

Assume that the above setting is fulfilled and let be real numbers such that for all with . Moreover, assume that or that there exists a real number such that for all . Additionally, let be -measurable with for all . Then we obtain

| (85) | |||

for all .

First of all, note that the assumption for all , the continuity of , the inequality for all with and the estimate for all imply for all . Therefore, we obtain

for all . The estimate for all and Theorem 2.1 hence give

In the case , the triangle inequality and Jensen’s inequality then yield

| (86) | |||

for all . This shows (5.2) in the case . In the case , the estimate for all shows and this implies (5.2) in the case . The proof of Corollary 5.2 is thus completed.

6 Convergence of the multilevel Monte Carlo tamed Euler method

In this section we combine the multilevel Monte Carlo method with a tamed Euler method. We aim at path-dependent payoff functions. Therefore, we consider piecewise linear time interpolations of the numerical approximations, which have continuous sample paths and which are implementable. Theorem 6.1 shows that these piecewise linear interpolations of the tamed Euler approximations converge in the strong sense with the optimal convergence order according to Müller-Gronbach’s lower bound in the Lipschitz case in m02 . Theorem 6.2 then establishes almost sure and strong convergence of the multilevel Monte Carlo method combined with the tamed Euler method. The payoff function is allowed to depend on the whole path. We assume the payoff function only to be locally Lipschitz continuous and the local Lipschitz constant to grow at most polynomially.

Throughout this section assume that the following setting is fulfilled. Let , let be a probability space with a normal filtration , let , let , , , be a family of independent standard -Brownian motions and let , , , be a family of independent identically distributed -measurable mappings with for all . Here and below we use the Euclidean norm for all and all . Moreover, let be a continuously differentiable and globally one-sided Lipschitz continuous function whose derivative grows at most polynomially and let be a globally Lipschitz continuous function. More formally, suppose that there exists a real number such that , and for all . Here and below we use and for all . Then consider the SDE

| (87) |

for . Under the assumptions above, the SDE (87) is known to have a unique solution. More formally, there exists an up to indistinguishability unique adapted stochastic process with continuous sample paths fulfilling

| (88) |

-almost surely for all ; see, for example, Theorem 2.4.1 in Mao m97 . The drift coefficient is the infinitesimal mean of the process and the diffusion coefficient is the infinitesimal standard deviation of the process . In the next step we define a family of tamed Euler approximations , , , , , by and

for all , , and all . In order to formulate our convergence theorem for the multilevel Monte Carlo tamed Euler approximations, we now introduce piecewise continuous time interpolations of the time discrete numerical approximations (6). More formally, let , , , , be a family of stochastic processes with continuous sample paths defined by

for all , , , and all .

The following corollary is a direct consequence of Hutzenthaler, Jentzen and Kloeden hjk10b and Müller-Gronbach m02 ; see also Ritter r90b . It asserts that the piecewise linear approximations , , converge in the strong sense to the exact solution. The convergence order is except for a logarithmic term.

Corollary 6.1 ((Strong convergence of the tamed Euler method)).

Assume that the above setting is fulfilled. Then there exists a family , , of real numbers such that

| (91) |

for all and all .

The convergence rate for obtained in (91) is sharp according to Müller-Gronbach’s lower bound established in Theorem 3 in m02 in the case of globally Lipschitz continuous coefficients; see also Hofmann, Müller-Gronbach and Ritter hmr00a .

Proof of Corollary 6.1 Let , , be stochastic processes defined by

for all , , and all . Theorem 1.1 in hjk10b then shows the existence of a family , , of real numbers such that for all and all . The triangle inequality hence yields

| (92) | |||

for all and all . Moreover, we have

| (93) | |||

for all , and all . Combining (6), (6) and Hölder’s inequality then gives

| (94) | |||

for all and all where , , is a sequence of independent one-dimensional standard Brownian motions. Moreover, Theorem 1.1 in hjk10b , in particular, implies

| (95) |

for all . Additionally, Corollary 2 in Müller-Gronbach m02 (see also Ritter r90b ) shows

| (96) |

for all . Combining (6), (95) and (96) finally completes the proof of Corollary 6.1.

Proposition 6.2 ((Strong consistency, converence with probability one and strong convergence of the multilevel Monte Carlo tamed Euler method)).

Assume that the above setting is fulfilled, let and let be a function from the space of continuous functions into the real numbers satisfying

| (97) | |||

for all . Then there exists a family , , of real numbers such that

| (98) | |||

for all and all . In particular, there are finite -measurable mappings , , such that

for all and all -almost surely.

The convergence rate for obtained in (6.2) is the same as in Remark 8 in Creutzig et al. cdmr09 . For numerical approximation results for SDEs with globally Lipschitz continuous coefficients but under less restrictive smoothness assumption on the payoff function, the reader is referred to Giles, Higham and Mao ghm09 and Dörsek and Teichmann dt10 . Moreover, numerical approximation results for SDEs with nonglobally Lipschitz continuous and at most linearly growing coefficients can be found in Yan y02 , for instance. {pf*}Proof of Proposition 6.2 The triangle inequality gives

for all and all and the Burkholder–Davis–Gundy inequality in Theorem 6.3.10 in Stroock s93 shows the existence of real numbers , , such that

for all and all . In the next step estimate (6.2), Hölder’s inequality and the triangle inequality show

and Corollary 6.1 and again estimate (6.2) hence give

for all and all . The triangle inequality, again Corollary 6.1 and the estimate for all then yield

and finally

for all and all . This shows (6.2). Inequality (6.2) then immediately follows from Lemma 2.1 in Kloeden und Neuenkirch kn07 . This completes the proof of Proposition 6.2.

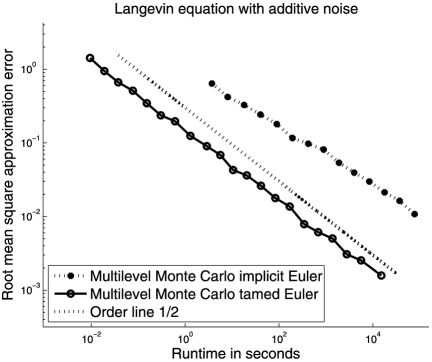

It is well known that the multilevel Monte Carlo method combined with the (fully) implicit Euler method converges too. The following simulation indicates that this multilevel Monte Carlo implicit Euler method is considerably slower than the multilevel Monte Carlo tamed Euler method. We choose a multi-dimensional Langevin equation as an example. More precisely, we consider the motion of a Brownian particle of unit mass in the -dimensional potential , , with . The corresponding force on the particle is then for . More formally, let , , , , for all , and let be the identity matrix for all . Thus the SDE (87) reduces to the Langevin equation

| (100) |

for . Then the implicit Euler scheme for the SDE (100) is given by mappings , , , satisfying and

| (101) |

for all and all . Note that we used the Matlab function in our implementation of the implicit Euler scheme (101).

Figure 5 displays the root mean square approximation error of the multilevel Monte Carlo implicit Euler method for the uniform second moment of the exact solution of (100) as function of the runtime when . In addition Figure 5 shows the root mean square approximation error of the multilevel Monte Carlo tamed Euler method for the uniform second moment of the exact solution of (100) as function of the runtime when . We see that both numerical approximations of the SDE (100) apparantly converge with rate close to . Moreover the multilevel Monte Carlo implicit Euler method was considerably slower than the multilevel Monte Carlo tamed Euler method. This is presumably due to the additional computational effort which is required to determine the zero of a nonlinear equation in each time step of the implicit Euler method (101). More results on implicit numerical methods for SDEs can be found in h96 , hms02 , t02 , hmps11 , s10 , MaoSzpruch2012pre , ms12 , for instance.

Appendix: Proof of Lemma 4.9

The definition (4.2) of , , and independence of , , , imply

for all . The inequality

for all therefore yields

for all . Next we estimate for all to get

This completes the proof of Lemma .1.

Subadditivity of the probability measure and the inequality for all (e.g., Lemma 22.2 in klenke2008 ) imply

for all . Summing over results in

and this completes the proof of Lemma .2.

Lemma .3.

Let be a probability space, and let be a standard normally distributed -measurable mapping. Then

| (108) |

for all and all .

Monotonicity of the exponential function yields

for all . Apply the standard estimate for all (e.g., Lemma 22.2 in klenke2008 ), inequality (Appendix: Proof of Lemma 4.9) and for all to get

for all and all . This completes the proof of Lemma .3.

Let be defined as

| (111) |

for all . Inserting definition (4.2) we get

for all . The method of rejection sampling hence results in

for all . In order to apply Lemma .3, we note that

for all and all . Lemma .3 applied to the standard normally distributed variable thus leads to

for all . Summing over results in

This completes the proof of Lemma .4.

First of all, define a filtration , , through

| (118) |

for all and every where denotes the smallest sigma-algebra generated by its argument. Moreover, define an -measurable mapping through for every . Next observe that the identity

for every shows that is a stopping time with respect to the filtration , , for every . Consequently, the sigma-algebras for are well-defined. By definition (118) the random variables , , are independent of for every . Indeed, observe that (118) shows that

for all , , and all . Next we note that is -measurable for every . Indeed, observe that

| (120) | |||

for all , and all . In the next step we observe that (Appendix: Proof of Lemma 4.9), (Appendix: Proof of Lemma 4.9), the fact that is measurable with respect to for all and the inequality for all and all show

| (121) | |||

-almost surely for all . Now we apply inequality (Appendix: Proof of Lemma 4.9) to obtain

| (122) | |||

for all . Next we observe that

on for all . Inserting (Appendix: Proof of Lemma 4.9) into (Appendix: Proof of Lemma 4.9) results in

for all . Combining (Appendix: Proof of Lemma 4.9), Lemmas .1 and .2 then shows

This completes the proof of Lemma .5.

We now present the proof of Lemma 4.9. It makes use of Lemmas .1–.5 above. {pf*}Proof of Lemma 4.9 Combining the subadditivity of the probability measure and Lemmas .1, .2, .4 and .5 shows

| (126) | |||

The lemma of Borel–Cantelli (e.g., Theorem 2.7 in klenke2008 ) therefore implies

| (127) |

Hence, we obtain

This completes the proof of Lemma 4.9.

Acknowledgments

We would like to express our sincere gratitude to Weinan E, Klaus Ritter, Andrew M. Stuart, Jan van Neerven and Konstantinos Zygalakis for their very helpful advice.

References

- (1) {barticle}[mr] \bauthor\bsnmAlyushina, \bfnmL. A.\binitsL. A. (\byear1987). \btitleEuler polygonal lines for Itô equations with monotone coefficients. \bjournalTheory Probab. Appl. \bvolume32 \bpages340–345. \bidmr=0902767 \bptokimsref \endbibitem

- (2) {bbook}[mr] \bauthor\bsnmCramér, \bfnmHarald\binitsH. (\byear1999). \btitleMathematical Methods of Statistics. \bpublisherPrinceton Univ. Press, \blocationPrinceton, NJ. \bidmr=1816288 \bptokimsref \endbibitem

- (3) {barticle}[mr] \bauthor\bsnmCreutzig, \bfnmJakob\binitsJ., \bauthor\bsnmDereich, \bfnmSteffen\binitsS., \bauthor\bsnmMüller-Gronbach, \bfnmThomas\binitsT. and \bauthor\bsnmRitter, \bfnmKlaus\binitsK. (\byear2009). \btitleInfinite-dimensional quadrature and approximation of distributions. \bjournalFound. Comput. Math. \bvolume9 \bpages391–429. \biddoi=10.1007/s10208-008-9029-x, issn=1615-3375, mr=2519865 \bptokimsref \endbibitem

- (4) {barticle}[mr] \bauthor\bsnmDereich, \bfnmSteffen\binitsS. (\byear2011). \btitleMultilevel Monte Carlo algorithms for Lévy-driven SDEs with Gaussian correction. \bjournalAnn. Appl. Probab. \bvolume21 \bpages283–311. \biddoi=10.1214/10-AAP695, issn=1050-5164, mr=2759203 \bptokimsref \endbibitem

- (5) {bmisc}[auto:STB—2012/12/05—11:57:16] \bauthor\bsnmDoersek, \bfnmP.\binitsP. and \bauthor\bsnmTeichmann, \bfnmJ.\binitsJ. (\byear2010). \bhowpublishedA semigroup point of view on splitting schemes for stochastic (partial) differential equations. Unpublished manuscript. Available at arXiv:\arxivurl1011.2651v1. \bptokimsref \endbibitem

- (6) {barticle}[mr] \bauthor\bsnmDuffie, \bfnmDarrell\binitsD. and \bauthor\bsnmGlynn, \bfnmPeter\binitsP. (\byear1995). \btitleEfficient Monte Carlo simulation of security prices. \bjournalAnn. Appl. Probab. \bvolume5 \bpages897–905. \bidissn=1050-5164, mr=1384358 \bptokimsref \endbibitem

- (7) {bincollection}[mr] \bauthor\bsnmGiles, \bfnmMike\binitsM. (\byear2008). \btitleImproved multilevel Monte Carlo convergence using the Milstein scheme. In \bbooktitleMonte Carlo and Quasi-Monte Carlo Methods 2006 \bpages343–358. \bpublisherSpringer, \blocationBerlin. \biddoi=10.1007/978-3-540-74496-2_20, mr=2479233 \bptokimsref \endbibitem

- (8) {barticle}[mr] \bauthor\bsnmGiles, \bfnmMichael B.\binitsM. B. (\byear2008). \btitleMultilevel Monte Carlo path simulation. \bjournalOper. Res. \bvolume56 \bpages607–617. \biddoi=10.1287/opre.1070.0496, issn=0030-364X, mr=2436856 \bptokimsref \endbibitem

- (9) {barticle}[mr] \bauthor\bsnmGiles, \bfnmMichael B.\binitsM. B., \bauthor\bsnmHigham, \bfnmDesmond J.\binitsD. J. and \bauthor\bsnmMao, \bfnmXuerong\binitsX. (\byear2009). \btitleAnalysing multi-level Monte Carlo for options with non-globally Lipschitz payoff. \bjournalFinance Stoch. \bvolume13 \bpages403–413. \biddoi=10.1007/s00780-009-0092-1, issn=0949-2984, mr=2519838 \bptokimsref \endbibitem

- (10) {bbook}[mr] \bauthor\bsnmGlasserman, \bfnmPaul\binitsP. (\byear2004). \btitleMonte Carlo Methods in Financial Engineering: Stochastic Modelling and Applied Probability. \bseriesApplications of Mathematics (New York) \bvolume53. \bpublisherSpringer, \blocationNew York. \bidmr=1999614 \bptokimsref \endbibitem

- (11) {barticle}[mr] \bauthor\bsnmGyöngy, \bfnmIstván\binitsI. (\byear1998). \btitleA note on Euler’s approximations. \bjournalPotential Anal. \bvolume8 \bpages205–216. \biddoi=10.1023/A:1008605221617, issn=0926-2601, mr=1625576 \bptokimsref \endbibitem

- (12) {barticle}[mr] \bauthor\bsnmGyöngy, \bfnmIstván\binitsI. and \bauthor\bsnmKrylov, \bfnmNicolai\binitsN. (\byear1996). \btitleExistence of strong solutions for Itô’s stochastic equations via approximations. \bjournalProbab. Theory Related Fields \bvolume105 \bpages143–158. \biddoi=10.1007/BF01203833, issn=0178-8051, mr=1392450 \bptokimsref \endbibitem

- (13) {barticle}[mr] \bauthor\bsnmHeinrich, \bfnmS.\binitsS. (\byear1998). \btitleMonte Carlo complexity of global solution of integral equations. \bjournalJ. Complexity \bvolume14 \bpages151–175. \biddoi=10.1006/jcom.1998.0471, issn=0885-064X, mr=1629093 \bptokimsref \endbibitem

- (14) {bincollection}[auto:STB—2012/12/05—11:57:16] \bauthor\bsnmHeinrich, \bfnmS.\binitsS. (\byear2001). \btitleMultilevel Monte Carlo methods. In \bbooktitleLarge-Scale Scientific Computing. \bseriesLecture Notes in Computer Science \bvolume2179 \bpages58–67. \bpublisherSpringer, \blocationBerlin. \bptokimsref \endbibitem

- (15) {barticle}[mr] \bauthor\bsnmHeinrich, \bfnmStefan\binitsS. and \bauthor\bsnmSindambiwe, \bfnmEugène\binitsE. (\byear1999). \btitleMonte Carlo complexity of parametric integration. \bjournalJ. Complexity \bvolume15 \bpages317–341. \biddoi=10.1006/jcom.1999.0508, issn=0885-064X, mr=1716737 \bptokimsref \endbibitem

- (16) {bbook}[mr] \bauthor\bsnmHigham, \bfnmDesmond J.\binitsD. J. (\byear2004). \btitleAn Introduction to Financial Option Valuation: Mathematics, Stochastics and Computation. \bpublisherCambridge Univ. Press, \blocationCambridge. \bidmr=2064042 \bptokimsref \endbibitem

- (17) {barticle}[mr] \bauthor\bsnmHigham, \bfnmDesmond J.\binitsD. J., \bauthor\bsnmMao, \bfnmXuerong\binitsX. and \bauthor\bsnmStuart, \bfnmAndrew M.\binitsA. M. (\byear2002). \btitleStrong convergence of Euler-type methods for nonlinear stochastic differential equations. \bjournalSIAM J. Numer. Anal. \bvolume40 \bpages1041–1063 (electronic). \biddoi=10.1137/S0036142901389530, issn=0036-1429, mr=1949404 \bptokimsref \endbibitem

- (18) {barticle}[mr] \bauthor\bsnmHofmann, \bfnmNorbert\binitsN., \bauthor\bsnmMüller-Gronbach, \bfnmThomas\binitsT. and \bauthor\bsnmRitter, \bfnmKlaus\binitsK. (\byear2000). \btitleStep size control for the uniform approximation of systems of stochastic differential equations with additive noise. \bjournalAnn. Appl. Probab. \bvolume10 \bpages616–633. \biddoi=10.1214/aoap/1019487358, issn=1050-5164, mr=1768220 \bptokimsref \endbibitem

- (19) {bincollection}[mr] \bauthor\bsnmHu, \bfnmYaozhong\binitsY. (\byear1996). \btitleSemi-implicit Euler–Maruyama scheme for stiff stochastic equations. In \bbooktitleStochastic Analysis and Related Topics, V (Silivri, 1994). \bseriesProgress in Probability \bvolume38 \bpages183–202. \bpublisherBirkhäuser, \blocationBoston, MA. \bidmr=1396331 \bptokimsref \endbibitem

- (20) {barticle}[mr] \bauthor\bsnmHutzenthaler, \bfnmMartin\binitsM. and \bauthor\bsnmJentzen, \bfnmArnulf\binitsA. (\byear2011). \btitleConvergence of the stochastic Euler scheme for locally Lipschitz coefficients. \bjournalFound. Comput. Math. \bvolume11 \bpages657–706. \biddoi=10.1007/s10208-011-9101-9, issn=1615-3375, mr=2859952 \bptokimsref \endbibitem

- (21) {bmisc}[auto:STB—2012/12/05—11:57:16] \bauthor\bsnmHutzenthaler, \bfnmM.\binitsM. and \bauthor\bsnmJentzen, \bfnmA.\binitsA. (\byear2012). \bhowpublishedNumerical approximations of stochastic differential equations with non-globally Lipschitz continuous coefficients. Unpublished manuscript. Available at arXiv:\arxivurl1203.5809. \bptokimsref \endbibitem

- (22) {barticle}[mr] \bauthor\bsnmHutzenthaler, \bfnmMartin\binitsM., \bauthor\bsnmJentzen, \bfnmArnulf\binitsA. and \bauthor\bsnmKloeden, \bfnmPeter E.\binitsP. E. (\byear2011). \btitleStrong and weak divergence in finite time of Euler’s method for stochastic differential equations with non-globally Lipschitz continuous coefficients. \bjournalProc. R. Soc. Lond. Ser. A Math. Phys. Eng. Sci. \bvolume467 \bpages1563–1576. \biddoi=10.1098/rspa.2010.0348, issn=1364-5021, mr=2795791 \bptokimsref \endbibitem

- (23) {barticle}[auto:STB—2012/12/05—11:57:16] \bauthor\bsnmHutzenthaler, \bfnmM.\binitsM., \bauthor\bsnmJentzen, \bfnmA.\binitsA. and \bauthor\bsnmKloeden, \bfnmP. E.\binitsP. E. (\byear2012). \btitleStrong convergence of an explicit numerical method for SDEs with non-globally Lipschitz continuous coefficients. \bjournalAnn. Appl. Probab. \bvolume22 \bpages1611–1641. \bptokimsref \endbibitem

- (24) {barticle}[mr] \bauthor\bsnmKebaier, \bfnmAhmed\binitsA. (\byear2005). \btitleStatistical Romberg extrapolation: A new variance reduction method and applications to option pricing. \bjournalAnn. Appl. Probab. \bvolume15 \bpages2681–2705. \biddoi=10.1214/105051605000000511, issn=1050-5164, mr=2187308 \bptokimsref \endbibitem

- (25) {bbook}[mr] \bauthor\bsnmKlenke, \bfnmAchim\binitsA. (\byear2008). \btitleProbability Theory: A Comprehensive Course (Universitext). \bpublisherSpringer London Ltd., \blocationLondon. \biddoi=10.1007/978-1-84800-048-3, mr=2372119 \bptokimsref \endbibitem

- (26) {barticle}[mr] \bauthor\bsnmKloeden, \bfnmP. E.\binitsP. E. and \bauthor\bsnmNeuenkirch, \bfnmA.\binitsA. (\byear2007). \btitleThe pathwise convergence of approximation schemes for stochastic differential equations. \bjournalLMS J. Comput. Math. \bvolume10 \bpages235–253. \bidissn=1461-1570, mr=2320830 \bptokimsref \endbibitem

- (27) {bbook}[mr] \bauthor\bsnmKloeden, \bfnmPeter E.\binitsP. E. and \bauthor\bsnmPlaten, \bfnmEckhard\binitsE. (\byear1992). \btitleNumerical Solution of Stochastic Differential Equations. \bseriesApplications of Mathematics (New York) \bvolume23. \bpublisherSpringer, \blocationBerlin. \bidmr=1214374 \bptokimsref \endbibitem

- (28) {barticle}[mr] \bauthor\bsnmKrylov, \bfnmN. V.\binitsN. V. (\byear1990). \btitleA simple proof of the existence of a solution to the Itô equation with monotone coefficients. \bjournalTheory Probab. Appl. \bvolume35 \bpages583–587. \bidmr=1091217 \bptokimsref \endbibitem

- (29) {bbook}[mr] \bauthor\bsnmLewis, \bfnmAlan L.\binitsA. L. (\byear2000). \btitleOption Valuation Under Stochastic Volatility: With Mathematica Code. \bpublisherFinance Press, \blocationNewport Beach, CA. \bidmr=1742310 \bptokimsref \endbibitem

- (30) {bbook}[mr] \bauthor\bsnmMao, \bfnmXuerong\binitsX. (\byear1997). \btitleStochastic Differential Equations and Their Applications. \bpublisherHorwood Publishing Limited, \blocationChichester. \bidmr=1475218 \bptokimsref \endbibitem

- (31) {bmisc}[auto:STB—2012/12/05—11:57:16] \bauthor\bsnmMao, \bfnmX.\binitsX. and \bauthor\bsnmSzpruch, \bfnmL.\binitsL. (\byear2012). \bhowpublishedStrong convergence rates for backward Euler–Maruyama method for nonlinear dissipative-type stochastic differential equations with super-linear diffusion coefficients. Stochastics. To appear. \bptokimsref \endbibitem

- (32) {barticle}[mr] \bauthor\bsnmMao, \bfnmXuerong\binitsX. and \bauthor\bsnmSzpruch, \bfnmLukasz\binitsL. (\byear2013). \btitleStrong convergence and stability of implicit numerical methods for stochastic differential equations with non-globally Lipschitz continuous coefficients. \bjournalJ. Comput. Appl. Math. \bvolume238 \bpages14–28. \biddoi=10.1016/j.cam.2012.08.015, issn=0377-0427, mr=2972586 \bptnotecheck year\bptokimsref \endbibitem

- (33) {bbook}[mr] \bauthor\bsnmMilstein, \bfnmG. N.\binitsG. N. (\byear1995). \btitleNumerical Integration of Stochastic Differential Equations. \bseriesMathematics and Its Applications \bvolume313. \bpublisherKluwer Academic, \blocationDordrecht. \bidmr=1335454 \bptokimsref \endbibitem

- (34) {bbook}[mr] \bauthor\bsnmMilstein, \bfnmG. N.\binitsG. N. and \bauthor\bsnmTretyakov, \bfnmM. V.\binitsM. V. (\byear2004). \btitleStochastic Numerics for Mathematical Physics. \bpublisherSpringer, \blocationBerlin. \bidmr=2069903 \bptokimsref \endbibitem

- (35) {barticle}[mr] \bauthor\bsnmMilstein, \bfnmG. N.\binitsG. N. and \bauthor\bsnmTretyakov, \bfnmM. V.\binitsM. V. (\byear2005). \btitleNumerical integration of stochastic differential equations with nonglobally Lipschitz coefficients. \bjournalSIAM J. Numer. Anal. \bvolume43 \bpages1139–1154 (electronic). \biddoi=10.1137/040612026, issn=0036-1429, mr=2177799 \bptokimsref \endbibitem

- (36) {barticle}[mr] \bauthor\bsnmMüller-Gronbach, \bfnmThomas\binitsT. (\byear2002). \btitleThe optimal uniform approximation of systems of stochastic differential equations. \bjournalAnn. Appl. Probab. \bvolume12 \bpages664–690. \biddoi=10.1214/aoap/1026915620, issn=1050-5164, mr=1910644 \bptokimsref \endbibitem

- (37) {bincollection}[auto:STB—2012/12/05—11:57:16] \bauthor\bsnmNikulin, \bfnmM. S.\binitsM. S. (\byear2001). \btitleConsistent estimator. In \bbooktitleEncyclopaedia of Mathematics (\beditor\binitsM. \bfnmMichiel \bsnmHazewinkel, ed.). \bpublisherSpringer, \blocationBerlin. \bptokimsref \endbibitem

- (38) {barticle}[mr] \bauthor\bsnmRitter, \bfnmKlaus\binitsK. (\byear1990). \btitleApproximation and optimization on the Wiener space. \bjournalJ. Complexity \bvolume6 \bpages337–364. \biddoi=10.1016/0885-064X(90)90027-B, issn=0885-064X, mr=1085383 \bptokimsref \endbibitem

- (39) {bbook}[mr] \bauthor\bsnmStroock, \bfnmDaniel W.\binitsD. W. (\byear1993). \btitleProbability Theory, an Analytic View. \bpublisherCambridge Univ. Press, \blocationCambridge. \bidmr=1267569 \bptokimsref \endbibitem

- (40) {bmisc}[auto:STB—2012/12/05—11:57:16] \bauthor\bsnmSzpruch, \bfnmL.\binitsL. (\byear2010). \bhowpublishedNumerical approximations of nonlinear stochastic systems. Ph.D. thesis, Univ. Strathclyde, Glasgow, UK. \bptokimsref \endbibitem

- (41) {barticle}[mr] \bauthor\bsnmSzpruch, \bfnmLukasz\binitsL., \bauthor\bsnmMao, \bfnmXuerong\binitsX., \bauthor\bsnmHigham, \bfnmDesmond J.\binitsD. J. and \bauthor\bsnmPan, \bfnmJiazhu\binitsJ. (\byear2011). \btitleNumerical simulation of a strongly nonlinear Ait-Sahalia-type interest rate model. \bjournalBIT \bvolume51 \bpages405–425. \biddoi=10.1007/s10543-010-0288-y, issn=0006-3835, mr=2806537 \bptokimsref \endbibitem

- (42) {barticle}[mr] \bauthor\bsnmTalay, \bfnmD.\binitsD. (\byear2002). \btitleStochastic Hamiltonian systems: Exponential convergence to the invariant measure, and discretization by the implicit Euler scheme. \bjournalMarkov Process. Related Fields \bvolume8 \bpages163–198. \bidissn=1024-2953, mr=1924934 \bptokimsref \endbibitem

- (43) {barticle}[mr] \bauthor\bsnmYan, \bfnmLiqing\binitsL. (\byear2002). \btitleThe Euler scheme with irregular coefficients. \bjournalAnn. Probab. \bvolume30 \bpages1172–1194. \biddoi=10.1214/aop/1029867124, issn=0091-1798, mr=1920104 \bptokimsref \endbibitem