Collateralized CDS and Default Dependence 111

This research is supported by CARF (Center for Advanced Research in Finance) and

the global COE program “The research and training center for new development in mathematics.”

All the contents expressed in this research are solely those of the authors and do not represent any views or

opinions of any institutions.

The authors are not responsible or liable in any manner for any losses and/or damages caused by the use of any contents in this research.

-Implications for the Central Clearing-

)

Abstract

In this paper, we have studied the pricing of a continuously collateralized CDS. We have made use of the ”survival measure” to derive the pricing formula in a straightforward way. As a result, we have found that there exists irremovable trace of the counter party as well as the investor in the price of CDS through their default dependence even under the perfect collateralization, although the hazard rates of the two parties are totally absent from the pricing formula. As an important implication, we have also studied the situation where the investor enters an offsetting back-to-back trade with another counter party. We have provided simple numerical examples to demonstrate the change of a fair CDS premium according to the strength of default dependence among the relevant names, and then discussed its possible implications for the risk management of the central counter parties.

Keywords : CVA, CSA, CCP, swap, collateral, derivatives, OIS, EONIA, Fed-Fund, basis, risk management

1 Introduction

The recent financial crisis, exemplified by the collapse of Lehman Brothers, is the major driver of the increased use of collateral agreements based on CSA (credit support annex published by ISDA), which is now almost a market standard among financial institutions [10]. Coupled with the explosion of various basis spreads, such as Libor-OIS and the cross currency swap (CCS) basis, the effects of collateralization on the derivative pricing, particularly from the view point of funding costs, have become important research topics. Johannes & Sundaresan (2007) [11] have first emphasized the cost of collateral using swap rates in U.S. market. In a series of works Fujii & Takahashi (2009, 2010) [5, 6, 7], we have developed a framework of interest-rate modeling in the presence of collateralization and multiple currencies. We have also pointed out the importance of choice of collateral currency and the embedded cheapest-to-deliver option in collateral agreements [8]. Piterbarg (2010) [12] discussed the general issue of option pricing under collateralization.

This financial crisis has also brought about serious research activity on the credit derivatives and counter party default risk, and large amount of research papers have been published since the crisis. The regulators have also been working hard to establish the new rules for the counter party risk management, and also for the migration toward the CCPs (central counter parties) particularly in the CDS (credit default swap) market. The excellent reviews and collections of recent works are available in the books edited by Lipton & Rennie [4] and Bielecki, Brigo & Patras [1], for example. However, the effects of collateralization on credit derivatives remain still largely unclear. It seems partly because that the idea of collateral cost appeared only recently, and also because the detailed collateral modeling is very complicated, due to the existence of settlement lag, threshold, and minimum transfer amount, e.t.c..

In this paper, based on the market development toward more stringent collateral management requiring a daily (or even intra-day) margin call, we have studied the pricing of CDS under the assumption of continuous collateralization. This is expected to be particularly relevant for the CCPs dealing with CDS and other credit linked products, for which the assumption of continuous collateralization seems to be a reasonable proxy of the reality. Although we have studied the similar issues for the standard fixed income derivatives in the previous work [9], the result cannot be directly applied to the credit derivatives since the behavior of hazard rates generally violates the so called ”no-jump” condition (e.g. Collin-Dufresne, Goldstein & Hugonnier (2004) [2]) if there exists non-trivial default dependence among the relevant parties. In this work, we apply the technique introduced by Schönbucher (2000) [13] and adopted later by [2] in order to eliminate the necessity of this condition.

As a result, we have obtained a simple pricing formula for the collateralized CDS. We will see, under the perfect collateralization, that the CDS price does not depend on the counter party hazard rates at all as expected. However, very interestingly, there remains irremovable trace of the two counter parties through the default dependence. This gives rise to a very difficult question about the appropriate pricing method for CCPs. A CCP acts as a buyer as well as a seller of a given CDS at the same time, by entering a back-to-back trade between the two financial firms. However, the result tells us that the mark-to-market values of the two offsetting CDSs are not equal in general even at the time of inception, if the CCP adopts the same price for the two firms. Although the detailed work will be left in a separate paper, we think that the result has important implications for the proper operations of CCPs for credit derivatives.

2 Fundamental Pricing Formula

2.1 Setup

We consider a filtered probability space , where is a spot martingale measure, and is a sub--algebra of satisfying the usual conditions. We denote the set of relevant firms and introduce a strictly positive random variable in the probability space as the default time of each party . We define the default indicator process of each party as and denote by the filtration generated by this process. We assume that we are given a background filtration containing other information except defaults and write . Thus, it is clear that is an as well as stopping time. We assume the existence of non-negative hazard rate process where

| (2.1) |

is an -martingale. We also assume that there is no simultaneous default for simplicity.

For collateralization, we assume the same setup adopted in [9] and repeat it here once again for convenience: Consider a trade between the party and . If the party has a negative mark-to-market value, it has to post the cash collateral 444According to the ISDA survey [10], more than of collateral being used is cash. If there is a liquid repo or security-lending market, we may also carry out similar formulation with proper adjustments of its funding cost. to the counter party , where the coverage ratio of the exposure is denoted by . We assume the margin call and settlement occur instantly. Party is then a collateral receiver and has to pay collateral rate on the posted amount of collateral, which is mark-to-market, to the party . This is done continuously until the end of the contract. Following the market conventions, we set the collateral rate as the time- value of overnight (O/N) rate of the collateral currency used by the party . It is not equal to the risk-free rate , in general, which is necessary to make the system consistent with the cross currency market 555See Ref. [8] for details.. We denote the recovery rate of the party by . We assume that all the processes except default times, such as are adapted to the background filtration . As for the details of exposure to the counter party and the recovery scheme, see [9].

2.2 CDS Pricing

We denote the CDS reference name by party-, the investor by party-, and the counter party by party-, respectively. Let us define and its corresponding indicator process, . We assume that the investor is a protection buyer and party- is a seller. Under this setup, the CDS price from the view point of the investor can be written as

| (2.2) | |||||

where denotes the cumulative dividend process representing the premium payment for the CDS, and denotes the money-market account with the risk-free interest rate. Other variables are defined as follows (See also [9] for details.):

Here, is the difference of the risk-free and collateral rates relevant for the collateral currency chosen by the party- at the time , which represents the instantaneous return of the posted collateral. Thus the term summarizes the return (or cost) of collateral from the view point of the investor. represents the default payoff when party- defaults first among the set .

Although we can follow the same procedures used in the previous work [9] based on the arguments of Duffie & Huang (1996) [3], we need a careful treatment to avoid the jump in the value process at the time of counter party default 666See the remark just after the proposition in [9].. In this work, we apply the measure change technique introduced by Schönbucher [13] and used by Collin-Dufresne et.al. (2004) [2], which leads to the following proposition in a clearcut way.

Proposition 1

Under the assumptions given in 2.1 and appropriate integrability conditions, the pre-default value corresponding to the CDS contract specified in Eq. (2.2) is given by

| (2.3) |

where

| (2.4) | |||||

and it satisfies for all . Here, the ”survival measure” is defined by

| (2.5) |

and the filtration denotes the augmentation of under .

Proof: Using the Doob-Meyer decomposition, one obtains

| (2.6) | |||||

Let us define

| (2.7) |

where we have used

| (2.8) |

and . Then, we can proceed as

Thus, on the set , we can write

Simple algebra gives us

Integrating the linear terms gives us the desired result.

Now, the method used in [9] gives us the CDS valuation formula under various situations

of collateralization. Let us summarize some of the useful results here:

Corollary 1

Assume the perfect and symmetric collateralization with domestic currency . Then, we have

| (2.9) |

as the pre-default value of the CDS given in Eq (2.2).

Corollary 2

Assume the perfect and symmetric collateralization but the collateral currency 777We use ”” to denote the currency type instead of counter party. is different from the evaluation currency . In this case, we have

| (2.10) |

where . and the associated denote the measure related to the money-market account of currency .

Notice that, as we have demonstrated in the work [8], the term structure of ,

which is the spread of collateral cost between the two currencies,

can easily be bootstrapped from the cross currency swap information in the market.

It is also straightforward to derive the leading order approximation under the imperfect collateralization, or , using the Gateaux derivative. See [9] for the details.

Corollary 3

Assume symmetric collateralization with domestic currency, but consider the imperfect collateralization . In this case, in the leading order approximation, we have

| (2.11) |

where

| (2.12) |

and

| (2.13) | |||||

In the previous work [9], we have interpreted as CCA (collateral cost adjustment) and as CVA. Although it still seems a reasonable interpretation, we need to be more careful about the interpretation of , the CDS value under the perfect collateralization. In fact, in the reminder of the paper, we will concentrate on this value and we will soon realize that the proper understanding of this simplest situation is quite non-trivial and critical for the risk management of CDS trades.

3 Financial Implications

Let us concentrate on the simplest case, where the symmetric and perfect collateralization is done continuously with domestic currency. As we have seen, the pre-default value of the CDS is given by

| (3.1) |

and one can easily confirm that the hazard rates of the investor as well as the counter party are absent from the pricing formula. Naively, it looks as if we succeed to recover the risk-free situation by the stringent collateral management. However, we will just see that it is quite misleading and dangerous to treat the result of Eq. (3.1) as the usual risk-free pricing formula.

The key point resides in the new measure and the filtration . As was emphasized in the works [13, 2], the transformation in Eq. (2.5) puts zero weight on the events where the parties default. It can be easily checked as follows: By construction, we know that

| (3.2) |

is a -martingale. Then, Maruyama-Girsanov’s theorem implies that

| (3.3) |

should be a -martingale, where denotes the (conditional or predictable) quadratic covariation. Now, one can easily check that

| (3.4) | |||||

and thus itself becomes a -martingale. In other words, under the new measure, the parties do not default almost surely.

Let us consider the financial implications of this fact. By our construction of filtration, hazard rate process of party can be written in the following form in general:

| (3.5) |

where denotes the set of all the subgroups of including also the empty set. Let us define , then is adapted to the filtration , and hence includes the information of default times of the parties included in the set although they are not explicitly shown in the formula. Importantly, it is not the hazard rate (or default intensity) under the new measure .

In the new measure, the parties included in are almost surely alive for all , and hence given in Eq. (3.5) is equivalent to given below:

| (3.6) |

where , and denotes the set of all the subgroups of and the empty set. Thus, the pre-default value of the CDS can also be written as

| (3.7) |

Now, let us consider the difference from the situation where the same CDS is being traded between the two completely default risk free parties. In this case, the pre-default value of the CDS is given by

| (3.8) |

Here, we have assumed that the collateralization is still being carried out. It is now clear that the most important quantity to understand is

| (3.9) |

Considering allows us to have a better image. In this case, can be simply obtained by the knowledge of marginal default distribution of the reference entity. On the other hand, does not contain the contribution from the scenarios where the parties included in the set default in the future, and hence the value of protection from the CDS becomes smaller than the former one.

In order to understand this fact, it is instructive to consider the predictable nature of collateralization. Even under the perfect collateralization, the party can only recover the contract value just before the default of the counter party. In the case of non-credit sensitive products, such as the standard interest rate swaps e.t.c., it does not cause any problem and we can consider the valuation just as if we are in risk-free world once we take the cost of collateral into account appropriately. However, in the case of credit derivatives, the contract value is expected to change discretely following the jump of the relevant hazard rate because of the direct feedback or contagious effect from the counter party default. Although the marginal default intensity contains the contribution from all the scenarios, the investor cannot receive this value in reality. In addition, the investor cannot receive any return caused by his default and all the following events after it. Thus, the quantity can be interpreted as the net discounted value that should be obtained by the investor if he and his counter party were default free.

It is easy to imagine that the quantity is determined

by the size of the price jump caused by contagious (or feedback) effects from the defaults of the two parties

and hence the default dependence among the relevant names.

Although it is difficult to obtain the difference in a generic situation,

we will demonstrate its significance in a simple but important setup in the following

sections.

Remark: In the market, the claim to the defaulted entity is to be made just after the default event. Thus, some additional value may be recovered on top of the collateral amount, because the claim is based on the market value after the default. This additional claim can be interpreted as the substitution cost, but the proper theoretical handling is difficult since it does depend on the choice of the next counter party and the exact timing of execution. Although ISDA document allows to include the cost of actual replacements, it is now clear that this is a huge burden of complicated litigious works on the administrator of the defaulted company. Since it is very difficult to prove the cost of replacement claimed by the creditors, such as the bid/offer spreads at the time of executions, is actually fair. It also crucially depends on whether the set of trades were unwound in a net basis or one-by-one, which should have a significant impact on the modeling of recovery scheme.

According to the recent article [16], the settlement of claims against Lehman Brothers has completed only 11% up to now. It seems that we need a clear rule to guarantee the fairness among the creditors and to speed up the settlement process. Once the detailed procedures and the rights of a creditor are finely defined, more accurate recovery handling will be possible.

4 Special Cases

We first list up the two special cases which provide us better understanding. Especially, the second example can be applied to the back-to-back trade, which is the most relevant situation for the CCPs.

4.1 3-party Case

The simplest situation to calculate the collateralized CDS is the case where there are only three relevant names, , which are the reference entity, the investor and the counter party, respectively. In this case, since , the set contains only the empty set . Thus, under the survival measure , we have

| (4.1) |

and particularly,

| (4.2) |

Since we know that is adapted to the background filtration , the evaluation of CDS value is quite straightforward in this case.

4.2 4-party Case

Now, let us add one more party and consider the 4-party case, . We first consider the trade of a CDS between the investor (party-) and the counter party (party-). The reference entity is party-. In this case, we have . Therefore, the relevant processes under the survival measure are

| (4.3) | |||||

| (4.4) |

Here, we have made the dependence on the default time in explicitly. Since the feedback effect only appears through the party in the survival measure, we can proceed in similar fashion done in Ref. [2].

In this case, the perfectly collateralized CDS pre-default value turns out to be

Here, the important point is not the possible contagious effect from the party-, but rather the lack of the contagious effects from the other names included in the set , which are included in the marginal default intensity of the reference entity.

Now, because of the symmetry, if the investor enters a back-to-back trade with the counter party , the pre-default value of this offsetting contract is given as follows:

Here, is defined according to the new survival set by

| (4.7) |

and the filtration denotes the augmentation of under .

Now let us consider . It is easy to check that it is not zero in general and does depend on the default intensities of party- and -, and also their contagious effects to the reference entity. Suppose that the investor is a CCP just entered into the back-to-back trade with the party- and - who have the same marginal default intensities. Even under the perfect collateralization, if the CCP applies the same CDS price (or premium) to the two parties, it has, in general, the mark-to-market loss or profit even at the inception of the contract. For example, consider the case where the protection seller (party-2) has very high default dependence with the reference entity, while the buyer (party-3) of the protection from the CCP has smaller one. In this case, the in should be smaller than that of . If the CCP uses the same CDS premium to the two parties, CCP should properly recognizes the loss, which stems from the difference of the contagion size from the default of the two parties. Since the party has high default dependence, the short protection position of the CCP with the party suffers bigger loss at the time of the default of the party .

5 Examples using a Copula

In order to separate the marginal intensity and default dependence, we will adopt here the copula framework. After explaining the general setup, we will apply Clayton copula to demonstrate quantitative impact.

5.1 Framework

Suppose that we are given a non-negative process adapted to the background filtration for each party . Suppose also that there exists a uniformly distributed random variable . We assume that, under , the -dimensional random vector

| (5.1) |

is distributed according to the -dimensional copula

| (5.2) |

We further assume that is independent from and also that copula function is -times continuously differentiable.

Now, let us define the default time as

| (5.3) |

Then, given the information , one obtains the joint default distribution as

| (5.4) |

where we have used the notation of

| (5.5) |

and

| (5.6) |

Following the well known procedures 888See, the works[14, 15], for example., one obtains

Here, we have defined as the set containing all the subgroups of with the empty set, and

| (5.8) |

is the set of for all , and similarly for . In the expression of Eq. (LABEL:zcb_copula), we have not properly ordered the arguments of the copula function just for simplicity, which should be understood in the appropriate way.

hazard rate of party- is calculated as

| (5.9) | |||||

Hence, as we have done in Eq (3.6) for the survival set , can be replaced as follows under the new measure :

| (5.10) |

where and is the set of all the subgroups of

with an additional empty set.

One can observe that both and are equal to the marginal intensity

if there is no default dependence (or in the case of the product copula).

Now, let us apply the copula framework to the two special cases given in Sec. 4.

(3-party Case): In the 3-party case with , we have

| (5.11) |

where .

(4-party Case): In the 4-party case with , we have

| (5.12) | |||||

| (5.13) |

under , and

| (5.14) | |||||

| (5.15) |

under .

5.2 Numerical Examples

In this paper, we adopt Clayton copula just for its analytical tractability and easy interpretation of its parameter [14]. Clayton copula belongs to Archimedean copula family, whose general form is given by

| (5.16) |

where the function is called the generator of the copula, and is its pseudo-inverse function. For Clayton copula, the generator function is given by

| (5.17) |

for , and hence we have

| (5.18) |

For this copula, one can easily check that

| (5.19) |

which means that the hazard rate jumps to times of its value just before the default of any other party.

In the following two figures, we have shown the numerical examples of the par premium of the perfectly collateralized CDS under Clayton copula. For simplicity, we have assumed continuous payment of the premium, and also assumed that the recovery rate , the collateral rate , and the marginal intensity of each name is constant.

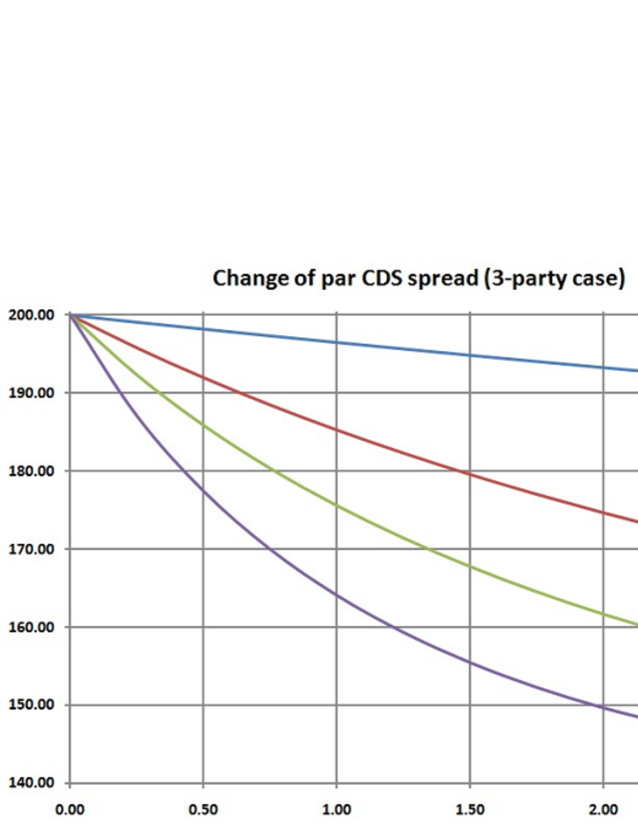

In Fig. 1, we have shown the results of 3-party case for the set of maturities; 1yr, 5yr, 10yr and 20yr. Here, the effective marginal intensity of each party is given as follows:

The horizontal axis denotes the value of the copula parameter . Considering the situation where major financial institutions are involved, and recalling the events just after the Lehman collapse, the significant jump of hazard rates seems possible. One can see that there is meaningful deviation of the par CDS premium from the marginal intensity even within the reasonable range of the jump size, or .

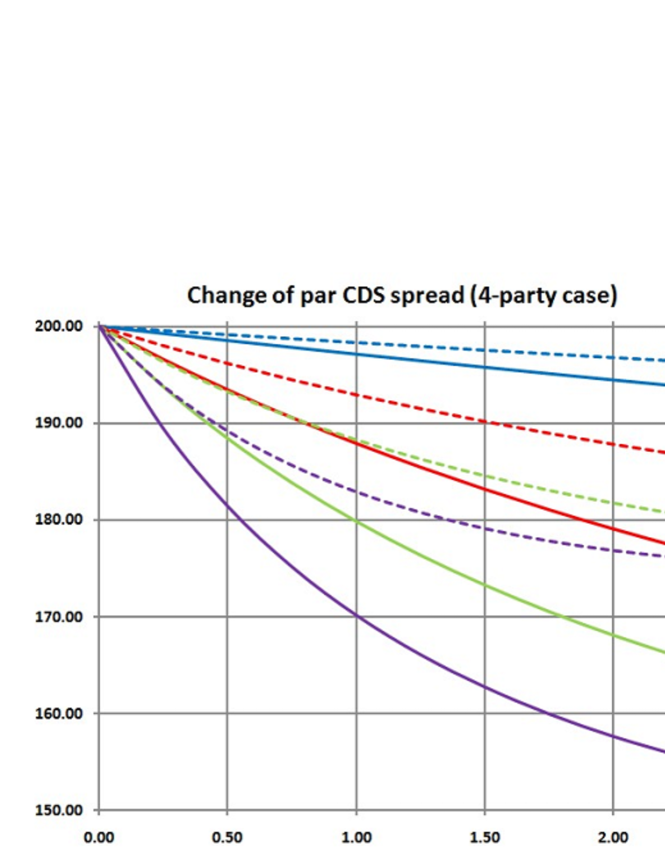

If Fig. 2, we have shown the corresponding results for the 4-party case. Here, we have set the effective marginal intensities as

In this case, we have modeled the situation where the investor has very high credit quality, which enters back-to-back trades with the two firms that have quite different credit worthiness. In the figure, we have used the solid lines for the trade with party-, and the dashed lines for the offsetting trade with party-. The result tells us that the back-to-back trades have non-zero mark-to-market value if the investor applies the same premium. This fact is very important for a CCP. It tells us that, even under the very stringent collateral management, the CCP has to recognize that it is not free from the ”risk”. It is, in fact, free from the credit risk of the counter party, but still suffers from the contagious effects from the defaults of its counter parties.

6 Conclusions

In this paper, we have studied the pricing of CDS under continuous collateralization. We have made use of the ”survival measure” to avoid the ”no-jump” condition required in the previous work [9]. It allows us straightforward derivation of pricing formula of CDS under various situations of collateralization.

In the later part, we have focused on the situation where the CDS is perfectly collateralized. We have shown that there exists irremovable trace of the two parties in the CDS price through their default dependence among the relevant names. For numerical examples, we have adopted Clayton copula to show the change of the par CDS premium according to the dependence parameter. The results have shown that there exists significant deviation of the par premium from the marginal intensity of the reference entity when the default dependence is high.

We should emphasize that these numerical calculations are solely for demonstrative purpose. Because of the simplicity of the chosen copula, there is no way to assign different dependence among the relevant names. The detailed analysis with dynamic underlying processes, and more realistic dependence structure is left for our future research. However, we still think that our results are enough to demonstrate the importance of default dependence or contagious effects among the relevant names even under the very stringent collateral management. This fact seems particularly important for the CCPs, where the members are usually major broker-dealers that are expected to have very significant impacts on all the other names just we have experienced in this crisis.

References

- [1] Bielecki, T., Brigo, D., Patras, F., 2011, ”Credit Risk Frontiers,” Bloomberg Press.

- [2] Collin-Dufresne, P., Goldstein, R., and Hugonnier, J., 2004, ”A General Formula for Valuing Defaultable Securities,” Econometrica, 72, 1377-1407.

- [3] Duffie, D., Huang, M., 1996, ”Swap Rates and Credit Quality,” Journal of Finance, Vol. 51, No. 3, 921.

- [4] Lipton, A., Rennie, A., 2011, ”The Oxford Handbook of Credit Derivatives,” Oxford University Press.

- [5] Fujii, M., Shimada, Y., Takahashi, A., 2009, ”A note on construction of multiple swap curves with and without collateral,” CARF Working Paper Series F-154, available at http://ssrn.com/abstract=1440633.

- [6] Fujii, M., Shimada, Y., Takahashi, A., 2009, ”A Market Model of Interest Rates with Dynamic Basis Spreads in the presence of Collateral and Multiple Currencies”, Forthcoming in Wilmott Magazine, available at http://ssrn.com/abstract=1520618.

- [7] Fujii, M., Takahashi, A., 2010, ”Modeling of Interest Rate Term Structures under Collateralization and its Implications.” Forthcoming in Proceedings of KIER-TMU International Workshop on Financial Engineering, 2010.

- [8] Fujii, M., Takahashi, A., 2011, ”Choice of Collateral Currency”, Risk Magazine, Jan., 2011: 120-125.

- [9] Fujii, M., Takahashi, A., 2010, ”Derivative pricing under Asymmetric and Imperfect Collateralization and CVA,” CARF Working paper series F-240, available at http://ssrn.com/abstract=1731763.

-

[10]

ISDA Margin Survey 2010,

http://www.isda.org/c_and_a/pdf/ISDA-Margin-Survey-2010.pdf Market Review of OTC Derivative Bilateral Collateralization Practices,

http://www.isda.org/c_and_a/pdf/Collateral-Market-Review.pdf

ISDA Margin Survey 2009,

http://www.isda.org/c_and_a/pdf/ISDA-Margin-Survey-2009.pdf - [11] Johannes, M. and Sundaresan, S., 2007, ”The Impact of Collateralization on Swap Rates”, Journal of Finance 62, 383-410.

- [12] Piterbarg, V. , 2010, ”Funding beyond discounting : collateral agreements and derivatives pricing” Risk Magazine.

- [13] Schönbucher, P., 2000, ”A Libor Market Model with Default Risk,” Working Paper, University of Bonn.

- [14] Schönbucher, P., Schubert, D., 2000, ”Copula-Dependent Default Risk in Intensity Models,” Working Paper, University of Bonn.

- [15] Rogge, E., Schönbucher,P., 2002, ”Modeling Dynamic Portfolio Credit Risk,” Working Paper.

- [16] ”Vexed by valuations,” March 2011, Risk Magazine.