On Nash Dynamics of Matching Market Equilibria

Email: ningc@ntu.edu.sg

†Department of Computer Science, University of Liverpool, UK.

Email: xiaotie@liv.ac.uk )

Abstract

In this paper, we study the Nash dynamics of strategic interplays of buyers in a matching market setup by a seller, the market maker. Taking the standard market equilibrium approach, upon receiving submitted bid vectors from the buyers, the market maker will decide on a price vector to clear the market in such a way that each buyer is allocated an item for which he desires the most (a.k.a., a market equilibrium solution). While such equilibrium outcomes are not unique, the market maker chooses one (max-eq) that optimizes its own objective — revenue maximization. The buyers in turn change bids to their best interests in order to obtain higher utilities in the next round’s market equilibrium solution.

This is an -person game where buyers place strategic bids to gain the most from the market maker’s equilibrium mechanism. The incentives of buyers in deciding their bids and the market maker’s choice of using the max-eq mechanism create a wave of Nash dynamics involved in the market. We characterize Nash equilibria in the dynamics in terms of the relationship between max-eq and min-eq (i.e., minimum revenue equilibrium), and develop convergence results for Nash dynamics from the max-eq policy to a min-eq solution, resulting an outcome equivalent to the truthful VCG mechanism.

Our results imply revenue equivalence between max-eq and min-eq, and address the question that why short-term revenue maximization is a poor long run strategy, in a deterministic and dynamic setting.

1 Introduction

The Nash equilibrium paradigm in Economics has been based on a rationality assumption that each individual will maximize its own utility function. Making it further to a dynamic process where multiple agents play interactively in a repeated game, the Nash dynamics refers to a process where participants take turns to choose a strategy to maximize their own utility function. We pose the question of what impact of such strategic behavior of the seller, as the market maker, can have on Nash dynamics of the buyers in a matching market setting [28], where the seller has products and there are unit-demand potential buyers with different private values for different items.

We base our consideration on the market equilibrium framework: The market maker chooses a non-negative price vector and an allocation vector; the outcome is called a market competitive equilibrium if all items with positive prices are sold out and everyone gets his maximum utility at the corresponding allocation, measured by the difference between the buyer’s value of the item and the charged price, i.e., . To achieve its own objective, i.e., revenue maximization, the market maker is naturally to set all items the highest possible prices so that there is still a supported allocation vector that clears the market and maximizes everyone’s utility. This yields a seller-optimal outcome and is called a maximum competitive equilibrium. Alternatively, at another extreme, the outcome of the market can be buyers-optimal, i.e., a minimum competitive equilibrium where all items have the lowest possible prices to ensure market clearance and utility maximization. Maximum and minimum equilibria represent the contradictory interests of the two parties in a two-sided matching market at the two extremes; and, as shown by Shapley and Shubik [28], both equilibria always exist and their prices are unique.

Using market equilibrium as a mechanism for computing prices and allocations yields desirable properties of efficiency and fairness. The winners in the mechanism, however, will bid against the protocol to reduce their payments; further, the losers may increase their bids to be more competitive (to their best interests). The problem becomes an -person game played in turn between the seller and the buyers where buyers make strategic moves to (mis)report their bids for the items, in response to other buyers’ bids and the solution selected by the market maker.

It is well-known that the minimum equilibrium mechanism admits a truthful dominant strategy for every buyer [22, 8], resulting in a solution equivalent to the VCG protocol [30, 5, 15]. However, it is hardly convincing a rational economic agent who dominates the market to make a move that maximizes the collective returns of its buyers by sacrificing its own revenue. Clearly, the Nash equilibrium paradigm has always assumed that an economic agent is a utility maximizer; for the market marker, it implies revenue maximization. Further, success in bringing great revenue (in a short term) will bring a large number of eyeballs and lead to positive externalities, which could breed more success (in a long term). Indeed, quite a few successful designs, like the generalized second price auction for sponsored search markets [1] and the FCC spectrum auction for licenses of electromagnetic spectra [6, 23], do not admit a truthful dominant strategy.

Our interest is to find out the properties of the game between the seller and the buyers (among which they compete with each other for the items), especially with these two extremes of the solution concepts — their relationship proves to be significant in the incentive analysis of the buyers in the market. In particular, we are interested in the dynamics of the outcomes when the market maker adopts the maximum equilibrium mechanism and the buyers adopt a particular type of strategy, that of the best response strategy. With the best response strategy, a buyer would announce his bids for all items that would result in the maximum utility for himself, under the fixed bids of other buyers and the maximum equilibrium mechanism prefixed by the market maker. The best response strategy varies depending on the circumstances of the market and has its nature place in the analysis of dynamics of strategic interplays of agents.

For the special case of single item markets where the market maker has only one item to sell, maximum equilibrium corresponds to the first price auction protocol and minimum equilibrium corresponds to the second price auction protocol. The first price auction sells the item to the buyer with the highest bid at a price equal to his bid (i.e., the highest possible price so that everyone is happy with his corresponding allocation). Under a dynamic setting, buyers take turns in making their moves in response to what they are encountered in the previous round(s). In a simple setting when all buyers bid their true values initially, the winner with the highest bid will immediately shade his bid down to the smallest value so that he is still a winner. Such best response bidding of the winner results in an outcome equivalent to the Vickrey second price auction, which charges the winner at the smallest possible price (i.e., the second highest bid) so that everyone’s utility is maximized. The observation of convergence from the first price to the second price goes hand-in-hand with the seminal revenue equivalence theory in Bayesian analysis [30, 26]. Therefore, both the Bayesian model and the dynamic best response model point to the same unification result of the first price and the second price solution concepts in the single item markets.

The story is hardly ending for the process of Nash dynamics with multiple items being sold in the market, which illustrates a rich structure that a single item market does not possess. First of all, in a single item market, the best response decision of a buyer is binary, that is, he decides either to or not to compete with the highest bid of others for the item at a smallest cost. With multiple items, however, a buyer needs to make his decision in the best response over all items rather than a single item. In particular, he may desire any item in a subset — each of which brings him the same maximum utility — and lose interest for other items. The buyer’s best response, therefore, is in accordance with his strategic bids for the items in both subsets. For example, it is possible that one increases hid bid for one item but decreases for another in a best response. This opens many possibilities that would complicate the analysis; in particular, best responses of a buyer are not unique. Indeed, as Example 3.1 shows, not all best responses guarantee convergence, again because of the multiplicity in possibilities of bidding strategies.

Second, in a single item market, the submitted bids of buyers illustrate a monotone property to the price of the item. That is, when a buyer increases his bid, the price is always monotonically non-decreasing. With multiple items, while it is true that the prices of the items are still monotone with respect to the bids of the losers, counter-intuitively, the prices are no longer monotone with respect to the bids of the winners, as the following Example 1.1 shows. This non-monotonicity further requires extra efforts to analyze the multiplicity of best response strategies and their properties.

Example 1.1 (Non-monotonicity).

There are three buyers and two items with submitted bids , , and (the bids of all unspecified pairs are zero). For the given bid vector, is the maximum equilibrium price vector, and assigning to and to are supported allocations. If a winner increases his bid of to , then is the maximum equilibrium price vector (with the same allocations) where the price of is decreased from 3 to 2. Hence, the maximum equilibrium prices are not monotone with respect to the submitted bids (of the winners).

Finally, the maximum market equilibrium solution has no closed form as in the single item case, and the convergence of the best responses depends on a careful choice of the bidding strategy. Recall that a major difficulty in analyzing the best responses is that, in addition to bidding strategically for the items that bring the maximum utility, buyers may have (almost arbitrarily) different bidding strategies for those items that they are not interested in; these decisions indeed play a critical role to the convergence of the best responses. As not all best responses necessarily lead to convergence (Example 3.1), we restrict to a specific bidding strategy, called aligned best response, where a bid vector of a buyer is called aligned if any allocation of an item with positive bid brings him the maximum utility. The aligned bidding strategy illustrates the preference of a buyer over all items and is shown to be a best response (Lemma 3.1 and 3.2). While the aligned best response still does not have a monotone property in general (see Figure 3), the prices do exhibit a pattern of monotonicity when the bids of the buyers have already been aligned. Based on these properties, we show that the aligned best response always converges and maximizes social welfare, summarized by the following claim.

Theorem. In the maximum competitive equilibrium mechanism game, for any initial bid vector and any ordering of the buyers, the aligned best response always converges. Further, the allocation at convergence maximizes social welfare.

In addition to proving convergence, another important question is that which Nash equilibrium to which the best response will converge. In contrast with single item markets where Nash equilibrium is essentially unique, in multi-item markets there can be several Nash equilibria with completely irrelevant price vectors (see Appendix D); this is another remarkable difference between single item and multi-item markets. Despite of the multiplicity of Nash equilibria, if we start with an aligned bid vector (e.g., bid truthfully), the best response always converges to one at a minimum competitive equilibrium, i.e., a VCG outcome.

Theorem. Starting from an aligned bid vector, the aligned best response of the maximum equilibrium mechanism converges to a minimum competitive equilibrium at truthful bidding.

1.1 Related Work and Motivation

The study of competitive equilibrium in a matching market was initiated by Shapley and Shubik in an assignment model [28]. They showed that maximum and minimum competitive equilibria always exist and gave a simple linear program to compute one. Their results were later improved to the models with general utility functions [7, 13]. Leonard [22] and Demange and Gale [8] studied strategic behaviors in the market and proved that the minimum equilibrium mechanism admits a truthful dominant strategy for every buyer. Later, Demange, Gale and Sotomayor [9] gave an ascending auction based algorithm that converges to a minimum equilibrium. Our study focuses on Nash dynamics in the matching market model; the convergence from maximum equilibrium to minimum equilibrium implies revenue equivalence, and addresses the question that why short-term revenue maximization is a poor long run strategy in a dynamic framework.

The Nash dynamics of best responses has its nature place in the analysis of interplays of strategic agents. In general, characterizing equilibria of the dynamics is difficult or intractable. There have been extensive studies in the literature for some special settings, e.g., potential games [25], congestion games [4], evolutionary games [18], concave games [11], correlated equilibrium [17], sink equilibria [14], and market equilibrium [31], to name a few. Complexity issues have also been addressed in the analysis of best responses [2, 12, 25]. Recently, Nisan et al. [27] independently considered best response dynamics in matching market and show a similar convergence result for running first price auctions for all items individually. To the best of our knowledge, our work is the first to study best response dynamics in the maximum competitive equilibrium mechanism.

Despite the motivation is mainly from theoretical curiosity, our setting does capture some realistic applications, such as eBay electronic market and sponsored search market, which have attracted a lot research efforts in recent years. The mechanism used in the sponsored search market is that of the generalized second price (GSP) auction. Because GSP is not truthful in general, a number of studies have focused on strategic considerations of advertisers. Edelman et al. [10] and Varian [29] independently showed that certain Nash equilibrium in the GSP auction derives the same revenue as the well-known truthful VCG scheme. Cary et al. [3] showed that a certain best response bidding strategy converges to the best Nash equilibrium. Recently, Leme and Tardos [21] considered other possible Nash equilibrium outputs and showed that the ratio between the worst and best Nash equilibria is upper bounded by 1.618. These results putting together illustrate a pretty complete overview of the structure of strategic behaviors in GSP. Our results are not directly about GSP but in a different way to reconfirm the revenue equivalence: While the search engine may adopt a different protocol with the goal of revenue maximization (i.e., the maximum equilibrium mechanism), with rational advertisers its overall revenue will eventually be the same as in the VCG protocol.

Another widely studied problem related to our model is that of spectrum markets. In designing the FCC spectrum auction protocol, a multiple stage bidding process, proposed by Milgrom [23], to digest coordination, optimization and withdrawal, is adopted. It is conducted in several stages to allow buyers to change their bids when the seller announces the tentative prices of the licenses for the winners. Therefore, it is created as an alternative game played between the seller and the buyers as a whole. Our best response analysis considers the dynamic aspect of the model and illustrates the convergence of the dynamic process.

Organization. We will first describe our model and maximum/minimum competitive equilibrium (mechanism) in Section 2. In Section 3, we define the aligned bidding strategy and show that it is a best response and always converges. In Section 4, we characterize Nash equilibria in the maximum equilibrium mechanism game; and based on the characterization, we show that the maximum equilibrium mechanism converges to a minimum equilibrium output. We conclude our discussions in Section 5.

2 Preliminaries

We have a market with unit-demand buyers, where each buyer wants at most one item, and indivisible items, where each item can be sold to at most one buyer. We will denote buyers by and items by throughout the paper. For every buyer and item , there is a value , representing the maximum amount that is willing to pay for item . We will assume that there are dummy buyers all with value zero for each item , i.e., . This assumption is without loss of generality, and implies that the number of items is always less than or equal to the number of buyers, i.e., .

The outcome of the market is a tuple , where

-

•

is a price vector, where is the price charged for item ;

-

•

is an allocation vector, where is the item that wins. If does not win any items, denote . Note that different buyers must win different items, i.e., for any if .

Given an output , let denote the utility that obtains. We will assume that all buyers have quasi-linear utilities. That is, if wins item (i.e., ), his utility is ; if does not win any item (i.e., ), his utility is .

Buyers’ preferences over items are according to their utilities — higher utility items are more preferable. We say that buyer (strictly) prefers to if , is indifferent between and if , and weakly prefers to if . In particular, a utility of zero, , means that is indifferent between buying item at price and not buying anything at all; a negative utility means that the buyer strictly prefers to not buy the item at price .

We consider the following solution concept in this paper.

Definition 2.1.

(Competitive equilibrium) We say a tuple is a competitive equilibrium if (i) for any item , if no one wins in allocation , and (ii) for any buyer , his utility is maximized by his allocation at the given price vector. That is,

-

•

if wins item (i.e., ), then ; and for every other item , ;

-

•

if does not win any item (i.e., ), then for every item , . (For notational simplicity, we write .)

The first condition above is an efficiency condition (i.e., market clearance), which says that all unallocated items are priced at zero (or at some given reserve price). The assumption that there is a dummy buyer for each item allows us to assume, without loss of generality, that all items are allocated in an equilibrium. The second is a fairness condition (i.e., envy-freeness), implying that each buyer is allocated with an item that maximizes his utility at these prices. That is, if wins item , then cannot obtain higher utility from any other item; and if does not win any item, then cannot obtain a positive utility from any item. Namely, all buyers are happy with their corresponding allocations at the given price vector.

For any given matching market, Shapley and Shubik [28] proved that there always is a competitive equilibrium. Actually, what they showed was much stronger — there is the unique minimum (respectively, maximum) equilibrium price vector, defined formally as follows.

Definition 2.2.

(Minimum equilibrium min-eq and maximum equilibrium max-eq) A price vector is called a minimum equilibrium price vector if for any other equilibrium price vector , for every item . An equilibrium is called a minimum equilibrium (denoted by min-eq) if is the minimum equilibrium price vector. The maximum equilibrium price vector and a maximum equilibrium (denoted by max-eq) are defined similarly.

For example, there are there buyers and one item; the values of buyers are and . Then and are the minimum and maximum equilibrium prices, respectively. Allocating the item to the first buyer , together with any price , yields a competitive equilibrium. When there is a single item, it can be seen that the outcome of the minimum equilibrium and the maximum equilibrium corresponds precisely to the “second price auction” and the “first price auction”, respectively.

Consider another example: There are there buyers and two items ; the values of buyers are , , and . Then is the minimum equilibrium price vector and is the maximum equilibrium price vector. Note that the allocation vectors supported by the minimum or maximum equilibrium price vector may not be unique. In this example, we can allocate and arbitrarily to and to form an equilibrium. Indeed, as Gul and Stacchetti [16] showed, if both and are equilibrium price vectors and is a competitive equilibrium, then is an equilibrium as well.

2.1 Maximum Equilibrium Mechanism Game

In this paper, we will consider a maximum equilibrium as a mechanism, that is, every buyer reports a bid for each item (note that can be different from his true value ), and given reported bids from all buyers , the maximum equilibrium mechanism (again denoted by max-eq) outputs a maximum equilibrium with respect to . Let denote the (maximum) equilibrium returned by the mechanism.

Let denote the utility that obtains in . That is, if , then if and if . Note that the (true) utility of every buyer is defined according to his true valuations , rather than the bids ; and the “equilibrium” output is computed in terms of the bid vector , rather than the true valuations (i.e., it is only guaranteed that for any item ). Therefore, the true utility of a buyer might not be maximized at the corresponding allocation and the given price vector . Further, the output might not even be a real equilibrium with respect to the true valuations of the buyers.

Considering competitive equilibria as mechanisms defines a multi-parameter setting and it is natural to consider strategic behaviors of the buyers. While it is a dominant strategy for every buyer to report his true valuations in the minimum equilibrium mechanism (i.e., the mechanism outputs a min-eq for the given bid vector) [8], the max-eq mechanism does not in general admit a dominant strategy. This is true even for the degenerated single item case — it is well-known that the first price auction is not incentive compatible. Therefore, in the max-eq mechanism, buyers will behave strategically to maximize their utilities. In particular, fixing bids of other buyers, buyer will naturally place his bid vector to maximize his own utility; such a vector is called a best response. The focus of the present paper is to consider convergence of best response dynamics, i.e., buyers iteratively change their bids according to best responses while all the others remain their previous bids unchanged. We say a best response dynamics converges if it eventually reaches a state where no buyer is willing to change his bid anymore; hence, it arrives at a Nash equilibrium.

As our focus is on the convergence of best response dynamics, we discretize the bidding space of every buyer to be a multiple of a given arbitrarily small constant , and assume that all ’s and ’s are multiples of . In practice, can be, e.g., one cent or one dollar (or any other unit number). This assumption is natural in the context of two-sided markets with money transfers, and implies that if a buyer increases his bid for an item, it must be by at least . In addition, we assume that the bid that every buyer submits for every item is less than or equal to his true valuation, i.e., . This assumption is rather mild because (i) bidding higher than the true valuations carries the risk of a negative utility, and (ii) as Lemma 3.1 and 3.2 below show, for any given fixed bids of other buyers, there always is a best response strategy for every buyer to bid less than or equal to his true valuations.

2.2 Computation of Maximum Equilibrium

Shapley and Shubik [28] gave a linear program to compute a min-eq; their approach can be easily transformed to compute a max-eq by changing the objective to maximize the total payment. Next we give a combinatorial algorithm to iteratively increase prices to converge to a max-eq. The idea of the algorithm is important to our analysis in the subsequent sections.

Definition 2.3 (Demand graph).

Given any given bid vector and price vector , its demand graph is defined as follows: is the set of buyers and is the set of items, and if and for any .

In a demand graph , every edge represents that item gives maximal utility to buyer , presumed that his true valuations are given by . Note that demand graph is uniquely determined by the given bid vector and price vector, and is independent to any allocation vector. However, an equilibrium allocation must be selected from the set of edges in the demand graph. The following definition of alternating paths in the demand graph is crucial to our analysis. (Recall that all items are allocated out in an equilibrium.)

Definition 2.4.

(-alternating path) Given any equilibrium of a given bid , let be its demand graph. For any item , a path in graph is called a -alternating path if edges are in and not in the allocation alternatively, i.e., for all . Denote by (or simply when the parameters are clear from the context) the subgraph of (containing both buyers and items including itself) reachable from through -alternating paths with respect to . A -alternating path in is called critical if .

For any given bid vector , let be an arbitrary equilibrium. Note that for any buyer with , is an edge in the demand graph . We consider the following recursive rule to increase prices: For any item , increase prices of all items in continuously with the same amount until one of the following events occurs:

-

1.

There is buyer such that (note that );

-

2.

There is buyer and item such that obtains maximal utility from as well; then we add edge to the demand graph and update for each .

The process continues iteratively until we cannot increase the price for any item. Denote the algorithm by Alg-max-eq. We have the following result.

Theorem 2.1.

Starting from an arbitrary equilibrium for the given bid vector , let be the final price vector in the above price-increment process Alg-max-eq. Together with the original allocation vector , is a max-eq with respect to .

The above algorithm Alg-max-eq and theorem illustrate the idea of defining (and the corresponding -alternating paths), summarized in the following corollary. (Note that if is a critical -alternating path in , then the last pair where is the exact reason that why we are not able to increase the price further in the Alg-max-eq to derive a higher equilibrium price vector.)

Corollary 2.1.

Given any bid vector and , for any item , there is a critical -alternating path in the subgraph .

3 Best Response Dynamics

For any given bid vector , assume that the max-eq outputs , i.e., . If is not a Nash equilibrium, there is a buyer who is able to obtain more utility by unilaterally changing his bid. Such a buyer will therefore naturally choose a vector (called a best response) to bid so that his utility is maximized in the max-eq mechanism, given fixed bids of all other buyers.

Consider the following example: There are three buyers and two items , with , , and . Then is the maximum equilibrium price and obtains utility 8. Consider a scenario where changes his bid to ; then the maximum equilibrium price vector becomes . Given the equilibrium price vector , however, there are two different equilibrium allocations which give him different true utilities (where either wins with utility or wins with utility ). Hence, different selections of equilibrium allocations may lead to different true utilities, which in turn will certainly affect best response strategies of the buyers.

To analyze the best responses of the buyers, it is therefore necessary to specify a framework about their belief on the resulting equilibrium allocations. We will consider worst case analysis in this paper, i.e., all buyers are risk-averse and always assume the worst possible allocations when making their best responses111When buyers report the same bids on some items, a certain tie-breaking rule should be specified to decide an equilibrium allocation. In the literature, ties are broken either by an oracle access to the true valuations or by a given fixed order of buyers [19, 20]. In our worst-case analysis framework, we actually do not need to specify a tie-breaking rule explicitly. It essentially implies that (i) a buyer who changes his bid has the lowest priority in tie-breaking, and (ii) any buyer who bids zero cannot win the corresponding item at price zero due to the existence of dummy buyers (i.e., there is no free lunch).. The above bid vector , therefore, is not a best response for since his utility in the worst allocation is only 8. In the worse-case analysis framework, the best responses of in the above example are given by and where wins at price with utility (it can be seen that there is no bid vector such that can obtain a utility higher than or equal to 10 given fixed bids of the other two buyers)222For any fixed bids of other buyers, the utility that a risk-averse buyer obtains in a best response is always within a distance of to that in a best possible allocation that a risk-seeking buyer may obtain. Thus, the worst case analysis (i.e., with risk-averse buyers) does provide a “safe” equilibrium allocation in which the corresponding utility is almost the same as the maximal..

The above example further shows that best response strategies may not be unique: While always wants to bid for , he can bid any value between 0 and 10 for to constitute a best response. While the bids for those items in which a buyer is not interested (i.e., in the above example) will not affect the utility that the buyer obtains after his best response bidding, they do affect the overall convergence of the best response dynamics, as the following example shows.

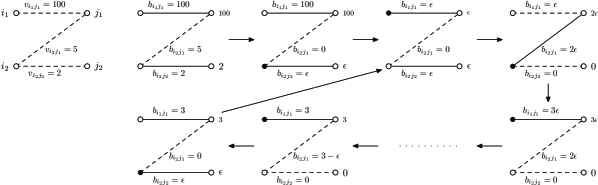

Example 3.1.

(Non-convergence of a best response) There are two buyers and two items , where , , and . (There still are dummy buyers; we do not describe them explicitly.) Consider the following specific best response strategy: Every buyer in the best response always bids zero to those items that he is not interested in. Since , we assume that always bids zero to . The process in Figure 1 shows that the best response dynamics does not converge. (For all examples in the paper, the black vertices on the left denote the buyers who change their bids in the best response, the solid lines denote allocations, and the numbers along with item vertices denote the maximum equilibrium prices.)

3.1 Best Response Strategy

Given the non-convergence of a specific best response shown in Example 3.1, one would ask if there are any best response strategies that always converge for any given instance. We consider the following bidding strategy.

Lemma 3.1.

(Best response of losers) For any given bid vector , let . Given fixed bids of other buyers, consider any buyer with ; let .

-

•

If , a best response of is to bid the same vector .

-

•

Otherwise, a best response of is given by vector , where . Further, the utility that obtains after the best response bidding is either or .333Note that if , then certainly improves his utility through the best response bidding. If , however, it is possible that obtains the same utility after the best response bidding. For such a case, is still a best response and we assume that will continue to change his bid according to it. This assumption is without loss of generality as our focus is on the convergence of the best response strategy. Further, in practice, buyers usually do not have complete information about the market (e.g., bid vectors of others) and are unaware of the exact utility they will obtain if change their bids. Hence, continuing to bid the best response provides a safe strategy for the buyers to maximize their utilities.

Lemma 3.2.

(Best response of winners) For any given bid vector , let . Given fixed bids of other buyers, consider any buyer with . Denote by the bid vector derived from where changes his bid to 0 for all items. Let and .

-

•

If or , a best response of is to bid the same vector .

-

•

Otherwise, a best response of is given by vector , where . Further, the utility that obtains after the best response bidding is either or .444Similar to the discussions for Lemma 3.1, if , then strictly improves his utility after the best response bidding; if , it is possible that obtains the same utility after the best response bidding. Again for such a case, is still a best response and we assume that will continue change his bid according to it.

The best response defined in the above two lemmas has two remarkable properties: First, if then ; second, if then . Hence, the best response captures the preference of over all items. In addition, given fixed bids of other buyers, the difference gives the maximal possible utility (up to a gap of ) that is able to obtain from item .

We say a bid vector aligned if for any , . That is, is derived from by moving the curve down in parallel capped at 0. It can be seen that the bid vectors defined in the above Lemma 3.1 and Lemma 3.2 are aligned. Hence, we will refer such bidding strategy by aligned best response. In the following, unless stated otherwise, all best responses are aligned according to these two lemmas. The following Figure 2 shows the convergence of Example 3.1 according to the aligned best response when both buyers bid their true values initially (as in Figure 1).

3.2 Properties of the Best Response

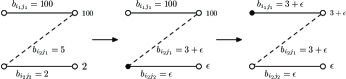

Example 1.1 shows that maximum equilibrium prices may not be monotone with respect to the submitted bid vectors. Such non-monotonicity still occurs even for the aligned best response of the winners defined in Lemma 3.2. In the example of the Figure 3, when a winner changes his bid, the price of is increased from 2 to in the maximum equilibrium. Hence, the maximum equilibrium prices may not be monotonically decreasing with respect to the aligned best responses of the winners.

However, as the following claim shows, we do have monotonicity for the maximum equilibrium prices given a certain condition. This property is crucial in the analysis of convergence.

Lemma 3.3.

When a loser makes a best response bidding (by Lemma 3.1), the maximum equilibrium prices will not decrease. On the other hand, when a winner, who has already made at least one aligned best response bidding, makes a best response bidding (by Lemma 3.2), the maximum equilibrium prices will not increase.

We have the following corollary.

Corollary 3.1.

Given a bid vector and , any loser is willing to make a best response bidding only if there is an item such that . For any winner who has already made a best response bidding, the following claims hold:

-

•

is willing to make a best response bidding only if the price of item will decrease in (defined in Lemma 3.2).

-

•

Let and , then is a max-eq for as well. Hence, we can assume without loss of generality that when places a best response bidding, the allocation remains the same.

3.3 Convergence of the Best Response Dynamics

In this subsection we will show that the aligned best response defined in Lemma 3.1 and 3.2 always converges. In the rest of this subsection we will assume that all buyers have already made a best response bidding; this assumption is without loss of generality since our goal is to prove convergence. Hence, the results established in the last subsection can be applied directly.

Proposition 3.1.

Given a bid vector and , assume that a winner first makes a best response bidding.

-

•

If next another winner makes a best response bidding, then will not change his bid in the best response.

-

•

If next a loser makes a best response bidding, then as long as is still a winner after ’s bid, he will not change his bid in the best response.

Similar to Proposition 3.1, we have the following claim for the best response of losers.

Proposition 3.2.

Given a bid vector and , assume that a loser first makes a best response bidding and becomes a winner.

-

•

If next another winner makes a best response bidding, then will not change his bid in the best response.

-

•

If next another loser makes a best response bidding, then as long as is still a winner after ’s bid, he will not change his bid in the best response.

The above two propositions imply the following corollary.

Corollary 3.2.

Given a bid vector and ,

-

•

if a winner makes a best response bidding, then unless becomes a loser (due to the best responses of others), he will not change his bid in the best response;

-

•

if a loser makes a best response bidding and becomes a winner, then unless becomes a loser again (due to the best responses of others), he will not change his bid in the best response.

We are now ready to prove our main theorem.

Theorem 3.1.

Proof.

By Corollary 3.2, after all buyers have already made a best response bidding, only losers are willing to make best responses to become a winner and winners are willing to make best responses only if they become a loser. By Lemma 3.3, the prices will be monotonically non-decreasing when losers make best responses. Hence, the process eventually terminates. ∎

The above theorem only says that the aligned best response is guaranteed to converge in finite steps; indeed it may take a polynomial of steps to converge. This is true even for the simplest setting with one item and two buyers of the same value : The two buyers with initial bids zero keep increasing their bids by one by one to beat each other until the price reaches to . However, in most applications like advertising markets, the value of is rather small. Further, to guarantee efficient convergence, we may set to be sufficiently large so that the rally between the winners and losers is fast (e.g., in most ascending auctions, the minimum increment of a bid is scaled according to the expected value of ).

4 Characterization of Nash Dynamics: From max-eq to min-eq

Theorem 3.1 in the previous section shows that the aligned best response always converges for any given initial bid vector. However, it does not answer the questions of at which condition(s) the dynamics of the best response stops (i.e., reaches to a stable state), and how the stable state looks like. We will answer these questions in this section.

Theorem 4.1.

For any Nash equilibrium bid vector of the max-eq mechanism, let and . Then for any item , we have either or . That is, the max-eq and min-eq price vectors differ by at most , i.e., .

The above characterizations apply to all Nash equilibria in the max-eq mechanism, and gives a necessary condition that when a bid vector forms a Nash equilibrium. Note that the other direction of the claim does not hold. For example, there are one item and two buyers with the same true value . In the bid vector with , we have . However, is not a Nash equilibrium as the loser in the can increase his bid to win the item.

In general, there can be multiple Nash equilibria for a given market. To compare different Nash equilibria, we use a universal benchmark — the solution given by the truthful min-eq mechanism, i.e., , where is the true valuation vector. This is equivalent to the outcome of the second price auction in single item markets and the VCG mechanism for the general multi-item markets. In Appendix D, we give two examples to show that, for a given Nash equilibrium with , there could be no fixed relation between the price vectors and , i.e., it can be either or . This is a remarkable difference between single item and multi-item markets — in the former we always have (i.e., ).

However, if we initially start with an aligned bid vector for all buyers (e.g., bid truthfully), then there is a strong connection between the max-eq price vector at a converged Nash equilibrium and : The two price vectors are “almost” identical, up to a gap of . We summarize our results in the following theorem.

Theorem 4.2.

For any Nash equilibrium bid vector converged from the aligned best response, starting from an aligned bid vector for all buyers, let and , where is the true valuation vector. Then we have

-

•

either or for all items;

-

•

.

We comment that if we start with an arbitrary bid vector, as long as all buyers bid at least one aligned best response in the dynamics, the convergence result from max-eq to min-eq still holds. In particular, this includes the case when all buyers bid very low at the beginning. In addition, for any given bid vector , if the max-eq mechanism outputs , it is not necessary that is a Nash equilibrium. For example, it is possible that the bids of losers are quite small and therefore winners still want to decrease their bids to pay less.

Finally, we characterize allocations at all Nash equilibria. We say an allocation efficient if is maximized, i.e., social welfare is maximized. It is well-known that all allocations in competitive equilibria are efficient at truthful bidding. This can be easily generalized to say that for any given bid vector , any equilibrium allocation maximizes . We have the following result, which says that any Nash equilibrium converged from the aligned best response actually maximizes the real social welfare with respect to .

Theorem 4.3.

For any Nash equilibrium bid vector of the max-eq mechanism converged from the aligned best response (starting from an arbitrary bid vector), let . Then is an efficient allocation that maximizes social welfare.

We note that the above claim does not hold for general Nash equilibria. For example, buyers and are interested in item at values and . Then allocating the item to at price is a Nash equilibrium for the bid vector (since the second buyer still obtains a non-positive utility even if he can win the item at a higher bid). This allocation does not maximize social welfare, and the example can be easily generalized to arbitrary number of items with large deficiency. In the aligned best response bidding, however, will continue to bid to win the item by Lemma 3.1, which leads to an efficient allocation.

5 Concluding Remarks

In this paper, we analyze the dynamics of best responses of the maximum competitive equilibrium mechanism in a matching market. While a best response strategy may not necessarily converge, we show that a specific bidding strategy, aligned best response, always converges to a Nash equilibrium. The outcome at such a Nash equilibrium is actually a minimum equilibrium given truthful bidding if we start with an aligned bid vector. In other words, our results show that maximum equilibrium converges to minimum equilibrium, which is a reminiscence of the convergence of dynamic bidding from first price auction to second price auction in a single item market.

In our discussions, we assume that all buyers have complete information for the market, including, say, submitted bid vectors of others, market prices and their corresponding allocation. We note that the first one, submitted bids of other buyers, in not necessary in the dynamics: The best response of losers defined in Lemma 3.1 applies automatically, and the best response of winners defined in Lemma 3.2 can be implemented by a two-step strategy without requiring extra information in the market.

References

- [1] G. Aggarwal, A. Goel, R. Motwani, Truthful Auctions for Pricing Search Keywords, EC 2006, 1-7.

- [2] E. Ben-Porath, The Complexity of Computing a Best, Response Automaton in Repeated Games with Mixed Strategies, Games and Economic Behavior, V.2, 1-12, 1990.

- [3] M. Cary, A. Das, B. Edelman, I. Giotis, K. Heimerl, A. Karlin, C. Mathieu, M. Schwarz, On Best-Response Bidding in GSP Auctions, EC 2007, 262-271.

- [4] S. Chien, A. Sinclair, Convergence to Approximate Nash Equilibrium in Congestion Games, Games and Economic Behavior, 2009.

- [5] E. H. Clarke, Multipart Pricing of Public Goods, Public Choice, V.11, 17-33, 1971.

- [6] P. Cramton, The FCC Spectrum Auctions: An Early Assessment, Journal of Economics and Management Strategy, V.6(3), 431-495, 1997.

- [7] V. Crawford, E. Knoer, Job Matching with Heterogeneous Firms and Workers, Econometrica, V.49(2), 437-450, 1981.

- [8] G. Demange, D. Gale, The Strategy of Two-Sided Matching Markets, Econometrica, V.53, 873-888, 1985.

- [9] G. Demange, D. Gale, M. Sotomayor, Multi-Item Auctions, Journal of Political Economy, V.94(4), 863-872, 1986.

- [10] B. Edelman, M. Ostrovsky, M. Schwarz, Internet Advertising and the Generalized Second-Price Auction, American Economic Review, 97(1), 242-259, 2007.

- [11] E. Even-Dar, Y. Mansour, U. Nadav, On the Convergence of Regret Minimization Dynamics in Concave Games, STOC 2009, 523-532.

- [12] A. Fabrikant, C. H. Papadimitriou, The Complexity of Game Dynamics: BGP Oscillations, Sink Equilibria, and Beyond, SODA 2008, 844-853.

- [13] D. Gale, Equilibrium in a Discrete Exchange Economy with Money, International Journal of Game Theory, V.13, 61-64, 1984.

- [14] M. Goemans, V. Mirrokni, A. Vetta, Sink Equilibria and Convergence, FOCS 2005, 142-154.

- [15] T. Groves, Incentives in Teams, Econometrica, V.41, 617-631, 1973.

- [16] F. Gul, E. Stacchetti, Walrasian Equilibrium with Gross Substitutes, Journal of Economic Theory, V.87, 95-124, 1999.

- [17] S. Hart, A. Mas-Colell, A Simple Adaptive Procedure Leading to Correlated Equilibrium, Econometrica, V.68, 1127-1150, 2000.

- [18] J. Hofbauer, K. Sigmund, Evolutionary Game Dynamics, Bulletin of the American Mathematical Society, V.40, 479-519, 2003.

- [19] N. Immorlica, D. Karger, E. Nikolova, R. Sami, First-Price Path Auctions, EC 2005, 203-212.

- [20] A. R. Karlin, D. Kempe, T. Tamir, Beyond VCG: Frugality of Truthful Mechanisms, FOCS 2005, 615-626.

- [21] R. P. Leme, E. Tardos, Pure and Bayes-Nash Price of Anarchy for Generalized Second Price Auction, FOCS 2010.

- [22] H. B. Leonard, Elicitation of Honest Preferences for the Assignment of Individuals to Positions, Journal of Political Economy, V.91, 461 479, 1983.

- [23] P. Milgrom, Putting Auction Theory to Work, Cambridge University Press, 2004.

- [24] V. Mirrokni, A. Skopalik, On the Complexity of Nash Dynamics and Sink Equilibria, EC 2009, 1-10.

- [25] D. Monderer, L. Shapley, Potential Games, Games and Economic Behavior, V.14(1), 124-143, 1996.

- [26] R. Myerson, Optimal Auction Design, Mathematics of Operations Research, V.6, 58-73, 1981.

- [27] N. Nisan, M. Schapira, G. Valiant, and A. Zoha, Best Response Auctions, EC 2011.

- [28] L. Shapley, M. Shubik, The Assignment Game I: The Core, International Journal of Game Theory, V.1(1), 111-130, 1971.

- [29] H. Varian, Position Auctions, International Journal of Industrial Organization, V.6, 1163-1178, 2007.

- [30] W. Vickrey, Counterspeculation, Auctions, and Competitive Sealed Tenders, Journal of Finance, V.16, 8-37, 1961.

- [31] F. Wu, L. Zhang, Proportional Response Dynamics Leads to Market Equilibrium, STOC 2007, 354-363.

Appendix A Proof of Theorem 2.1

Lemma A.1.

Let and be any two equilibria for the given bid vector . Let and be the subset of buyers who win items in in the equilibrium . Then all buyers in win all items in in the equilibrium as well. In particular, this implies that if is allocated to a dummy buyer in (i.e., essentially no one wins ), then its price is zero in all equilibria.

Proof.

Note that since for any , all items in must be sold out in equilibrium ; hence, and all buyers in win all items in in . Consider any buyer , let . For any item , since , we have

where the second inequality follows from the fact that is an equilibrium. Hence, buyer always strictly prefers item to all other items not in at price vector , which implies that his allocation . ∎

Proof of Theorem 2.1. By the rule of increasing prices, since the initial is an equilibrium, all buyers are always satisfied with their respective allocations in the course of the algorithm. Further, it can be seen that any item that is allocated to a dummy buyer (i.e., it has initial price ) will never have its price increased. Hence, the final output is an equilibrium as well.

Assume that is a max-eq for the given bid vector ; we know that for all items. Let and be the subset of buyers who win items in in the max-eq equilibrium. By Lemma A.1, we know that all buyers in win all items in in equilibrium as well. Assume that ; and consider any and the subgraph reachable from in the demand graph of the final output .

We claim that all items in are in . Otherwise, consider an item and the -alternating path defining to be in . Assume without loss of generality that is the first item on the path which is not in , i.e., and . since , by Lemma A.1, we have . Hence,

which contradicts to the fact that obtains his utility-maximized item in the max-eq.

Since all items in have their prices increased, again by Lemma A.1, all items in are sold out. Therefore, at the end of the algorithm when reaching to , we should still be able to increase prices for items in , which is a contradiction. That is, and is a max-eq.

Appendix B Proofs in Section 3

B.1 Proof of Lemma 3.1

Proof.

Given fixed bids of other buyers, consider any bid vector of buyer . Denote the resulting bid vector by , and let . A basic observation is that no matter what bid that submits, everyone other than is still happy with the original equilibrium . Hence, if for any , then is still a max-eq for . Otherwise, let . Consider subgraph and its critical -alternating path with respect to , where for and the pair and is the reason that cannot be increased in by the algorithm (i.e., ). Consider reallocating each to for . By the definition of -alternating path, we know that all these buyers are still happy with their new allocations. Further, we reallocate to ; then obtains his utility-maximized item at price under bid vector . This new allocation, together with the price vector , constitutes an equilibrium. In both cases, is an equilibrium price vector under bid vector . Hence, the price of every item in is larger than or equal to , i.e., .

We next analyze the best response of defined in the statement of the claim. If for any , then cannot get a positive utility from any item at price vector , as well as . Hence, bidding the original (losing) price vector is a best response strategy. It suffices to consider there is an item such that and the best response strategy described in the second part of the statement (denoted by ).

Let ; by the assumption, . It can be seen that for any , ; and any , , i.e., . That is, given bid vector and price vector , always desires those items in . Consider any item , by the same reassignment argument described above, we can reallocate to , as well as a few other reallocations through a critical -alternating path, to derive an equilibrium , where is the corresponding new allocation. Note that may not be a max-eq. Consider subgraph ; we ask whether can be increased further by the algorithm Alg-max-eq to get a max-eq.

If the answer is ‘no’, then is indeed a max-eq under bid vector (it can be shown that the price of any other item cannot be increased as well), and the utility that obtains satisfies

If the answer is ‘yes’, then we can increase prices of all items in by , which gives an equilibrium , where if and otherwise. Further, is a max-eq under bid vector since the price of is tight with the bid of , i.e., (again, prices of other items cannot be increased). Hence, the utility that obtains is

Next we consider the utility that obtains in the equilibrium with bid vector . Note that all other buyers bid the same values in and . Let ; then

If one of the above inequalities is strict, then . That is, , which implies that is a best response strategy. It remains to consider the case when all inequalities are tight, i.e., and ; in this case, we have . Consider the following two cases regarding the relation between and .

-

•

If , consider the subgraph . Since the price of cannot be increased, there is a critical -alternating path inside where and . Since

we know that and (otherwise, , then in the worst allocation the utility of is less than ). We claim that all items in have . Otherwise, consider the first item where . Note that ; then we have

Hence, and . This implies that there must be a buyer such that and , which is impossible since does not get his utility-maximized item in . Therefore, essentially defines a critical -alternating path in .

-

•

If , starting from , we expand the path through the following rule: if the current last edge is , expand if ; if the current last edge is , expand if . The process stops when there is no more item or buyer to expand; denote the final path by . Note that edges in are in and alternatively. Further, since wins in and in , plus the fact that , we have ; then since wins in and in , we have ; the argument inductively implies that for every item , . At the end of path , does not win any item in , which implies that . If we consider path in , the above arguments show that it is actually a critical -alternating path.

Hence, in both cases we cannot increase price in the equilibrium , which contradicts to our assumption that the answer is ‘yes’. ∎

B.2 Proof of Lemma 3.2

Proof.

Given fixed bids of other buyers, consider any bid vector of buyer . Denote the resulting bid vector by , and let . Consider the two equilibria and in the following virtual scenario: first bids 0 and loses in the max-eq and then bids according to yielding a new max-eq . By a similar argument as the proof of the above lemma, we know that for all items. In particular, the argument applies to the case when , hence .

Since the bid of any buyer is always less than or equal to his true value, we have

If , then certainly cannot obtain more utility when bidding since

If , then

and

Hence, , which implies that bidding the original vector is a best response strategy.

It remains to consider and analyze the best response , denote by , defined in the statement of the claim. Consider a virtual scenario where first bids 0 and loses in the equilibrium . By the above Lemma 3.1 for loser’s best response, we know that is a best response strategy for in the virtual scenario and . Since bidding according to is a specific strategy for , we have . These two inequalities together imply that bidding according to is a best response strategy for . ∎

B.3 Proof of Lemma 3.3

Proof.

The first part of the claim follows directly from the proof of Lemma 3.1, thus we will only prove the second part. Consider bid vector and equilibrium , bid vector (derived from where a winner bids 0 for all items) and equilibrium , and best response , all defined in the statement of Lemma 3.2. If does not change his bid, then the maximum equilibrium prices remain the same. Hence, in the following we assume that changes his bid according to and analyze the relation between and , where . What we need to show is that .

By the proof of Lemma 3.2, we know that for all items. If , i.e., for all items, let . Note that . Since is an equilibrium with respect to , we have and . Since has already made a best response bidding (either as a loser or a winner), his bids for different items are aligned, i.e., . Thus,

Hence, already obtains his maximally possible utility and will not change his bid. In the following, we assume and there is an item such that .

Let and be the set of buyers who win items in in . We claim that . Otherwise, all buyers in win all items in in as well with positive utilities and they strictly prefer their corresponding allocations to those items that are not in . Hence, we can increase the prices of all items in by to derive another equilibrium; this contradicts to the fact that is a max-eq. Therefore, there is exactly one buyer who wins an item in in given bid vector , i.e., . Next when changes his bid vector according to , by the proof of Lemma 3.1, the new allocation vector , together with the given price vector , constitutes an equilibrium. Let ; since

we must have . That is, when “joins the market again” from to , he grabs an item in “again”. Since every buyer in obtains a positive utility for his corresponding allocation in in and strictly prefers it to those items that are not in , he has to win an item in in . Hence, the only buyer who is kicked out of winning an item in is . That is, buyers in “again” win all items in . Finally, without loss of generality, we can assume that in all items that are not in have the same allocations as ; this still keeps an equilibrium and will not affect the computation of the maximum equilibrium price vector. Our argument above can be summarized as below:

| bid vector | equilibrium | winners for items in |

|---|---|---|

| max-eq | ||

| max-eq | ||

| max-eq |

Finally we consider running the algorithm Alg-max-eq on equilibrium to derive the maximum equilibrium . By the proof of Lemma 3.1, we have either or . To the end of proving , it remains to show that it is impossible that for all items; assume otherwise that there is such an item (this implies that ). Then again by the proof of Lemma 3.1, the price of is increased (from to ) through a -alternating path in the subgraph . That is, for , and . Consider subgraph , since , we cannot increase and there is a critical -alternating path in . Further, it can be seen that all items in are not in (since every buyer in strictly prefers the corresponding allocation in to those items in at price vector ). Since all items that are not in have the same allocations in and , we can expand path through , which gives a critical -alternating path in . Therefore, we cannot increase the price of any item in , including . This contradicts to our assumption that ; hence the lemma follows. ∎

B.4 Proof of Corollary 3.1

Proof.

The claims for best responses follow directly from Lemma 3.1 and 3.2, and the proof of Lemma 3.3. For the last claim, note that if is an equilibrium for , then by the algorithm Alg-max-eq to increase prices to derive the maximum equilibrium price vector , is a max-eq for . Recall in the proof of Lemma 3.3, is an equilibrium of and all items that are not in have the same allocations as , where . Thus, it remains to show that all items in have the same allocations in and . Since all items in are allocated to the same subset of buyers in both and , for any buyer , we have

and

(The last inequality is because of the following argument: Assume that . Since has already made a best response bidding, his bid vector over different items has already been aligned. By the best responses defined in Lemma 3.1 and 3.2, we have . Hence and . Therefore, .) If items in are allocated in different ways in and , then there are and such that items in are allocated to buyers in in and which forms an augmenting path. Adding the above two inequalities (regarding and ) for all buyers in gives . Hence, all inequalities are tight, which implies that every buyer gets the same utility from and . Therefore, we can change the allocation of items in according to , which still gives an equilibrium. ∎

B.5 Proof of Proposition 3.1

Proof.

Assume that and , where is the resulting bid vector after makes his best response bidding (by Corollary 3.1, we can assume that the equilibrium allocation is the same for and ). Further, by the proof of Corollary 3.1, we know that is an equilibrium for . In the two allocations and , consider the following alternating path:

where wins in and wins in , and (this implies, in particular, ). Further, we have

We will analyze the relation between and the price vector after makes his best response bidding to show the desired result.

-

•

First consider the next best response is made by another winner . After makes his best response bidding denote the resulting bid vector by ), by Corollary 3.1, we know that all winners have the same allocations . Further, the above set of equations still holds for all buyers in for . This is because, if is one of them, say , then both and are reduced by the same amount to derive and ; so we still have . Hence, the price of any item in path , as well as those that give the maximal utility to , cannot be smaller than in (otherwise, has to be a winner).

Therefore, when bids zero for all items after makes his best response bidding, the price of item cannot be smaller than in a as reallocating items according to where becomes a winner gives an equilibrium allocation. By Corollary 3.1, which says that every winner obtains the same item after his best response bidding, we know that the best response of is to bid the same vector, i.e., do not change his bid.

-

•

Next consider the next best response is made by a loser ; let be the resulting bid vector. By the proof of Lemma 3.1, let be an equilibrium of , where is the maximum equilibrium price of defined above and is derived from (the allocation before ’s bid) through an alternating path:

where wins in and wins in , and does not win in . (Note that to derive a max-eq for , we still need to verify if the price of can be increased in the subgraph .)

Assume that is still a winner after ’s bid; note that the item that wins in can be either the one defined above according to or the same item . Next we consider the setting when bids zero for all items, i.e., , for the two possibilities respectively.

If it is the former, i.e., and , then the price of and cannot be smaller than (which is at least ) and (which is at least ) respectively in a as we are able to reallocate items back to , respectively, where becomes a winner. Since defined in Lemma 3.2 will not increase, the best response of is to bid the same vector, i.e., do not change his bid.

If it is the latter, i.e., wins the same item in and , we claim that the price of cannot be smaller than in a . This is because: (i) We can reallocate items according to such that becomes a winner. (ii) If any item in appears in or (i.e., is the last buyer on path ), similar to the above arguments, we can reallocate items according and such that becomes a winner. (Note that for the last case , since and the bids of have already been aligned, will give the maximal utility for when its price is .)

∎

B.6 Proof of Proposition 3.2

B.7 Proof of Corollary 3.2

Appendix C Proofs in Section 4

To prove our results, we need the following definition, which is similar to -alternating path.

Definition C.1 (-alternating path).

Given any equilibrium of a given bid , let be its demand graph. For any item , a path in is called a -alternating path if edges are not in and in the allocation alternatively, i.e., for all possible . Denote by (or simply when the parameters are clear from the context) the subgraph of (containing both buyers and items including itself) reachable from through -alternating paths with respect to . A -alternating path in is called critical if and .

Note that the major difference between and -alternating paths is that in the former, edges in the path are in and not in the allocation alternatively; whereas in the latter, edges in the path are not in and in alternatively. Similar to Corollary 2.1, we have the following claim. (The last pair and in a critical -alternating path is the exact reason that why the price cannot be decreased further, since otherwise will have to be a winner and items are over-demanded.)

Corollary C.1.

Given any bid vector and , for any item , there is a critical -alternating path in .

C.1 Proof of Theorem 4.1

Proof.

By the definition of and , we have . Let and , i.e., is the subset of buyers that win items in in the max-eq . Then for any , either or . Assume that ; similar to the proof of Lemma A.1, we know that all buyers in still win items in in the min-eq .

Consider any and let . Consider a bid vector where and for any ; denote the resulting bid vector by (where the bids of all other buyers remain the same). Consider a tuple , where if and if , and if and if . It can be seen that is an equilibrium for . Note that ; thus, cannot obtain if its price is increased any further.

Let ; note that . We claim that still wins at price in . (This fact implies that obtains more utility from by paying less when bidding ; thus max-eq is not a Nash equilibrium.) Assume otherwise, then does not win any item in since for any . Because , there must be a (non-dummy) buyer winning : assume that wins , wins , wins , , wins in , and is the first buyer in the chain that is not in (such buyer must exist since is not a winner). Let (note that ); then we have and at least one of the two inequalities is strict (since wins another item at a higher price compared to ). This implies that there must be another buyer winning in . In the process all dummy buyers will not be introduced to win any item; hence, the same argument continues and will not stop, which contradicts to the fact that buyers and items are finite. ∎

C.2 Proof of Theorem 4.2

The claim follows from the following two claims.

Proposition C.1.

For any item , .

Proof.

Assume otherwise that there is an item such that . Assume that wins in and in , i.e., and . Since is an equilibrium for the true valuation vector , we have . Hence, if , then

That is, (defined in Lemma 3.2). If has yet made any best response bidding, then he should bid his best response according to Lemma 3.2. If he has already made best response bidding, then his bid vector has already been aligned and the above inequality implies that , which contradicts to the fact that is an equilibrium for the bid vector . Hence, we must have .

Consider the subgraph given by the exclusive-OR operation of the two allocations and . For any alternating path where wins in and wins in , if for any , then by the above argument and considering buyer , we have . Applying the same argument recursively yields . Since and does not win any item in , by Corollary 3.1 buyer should continue to make a best response bidding, which contradicts to the fact that is a Nash equilibrium. Hence, for any alternating path in , all items have . For any alternating cycle in , if there is an item with , by applying the above argument for recursively, all items in the cycle have .

Continue to consider the above item with . Since , by Corollary C.1 and abusing notations, there is a critical -alternating path in , where for , does not win any item and . Consider buyer ; by the definition of , we have

By the same above argument, we have . Then considering the alternating cycle containing , we have . The same argument applies to all items in recursively; hence, we have for all items in the path . This implies, in particular, that is a winner in since and by the best response characterized in Corollary 3.1.

Consider the item that wins in ; let . Since any buyer in an alternating cycle of win in both and , and must be at an endpoint of an alternating path of . Further, by the above argument regarding the prices of items in alternating paths, we have . Therefore,

That is, (defined in Lemma 3.2). We can apply the same argument above for to get a similar contradiction.

Hence, the claim follows. ∎

Proposition C.2.

For every item , if then the corresponding winner can obtain more utility by bidding his best response.

Proof.

From the above claim, we have . Let and . and and , i.e., and are the subset of buyers that win items in and in the max-eq , respectively. Then for any , we have .

Consider any buyer and item . If does not win any item in the min-eq , i.e., , then , which implies that cannot win in . If wins an item not in in , then

This implies that if wins in , then he should continue to make a best response bidding by Lemma 3.2, which contradicts the fact that is a Nash equilibrium. Therefore, all buyers in win all items in in both and .

Assume that ; consider any and let . Consider a bid vector where and for any ; denote the resulting bid vector by (where the bids of all other buyers remain the same). Consider a tuple , where if and if . It can be seen that is an equilibrium for . Note that ; thus, cannot obtain if its price is increased any further.

Similar to the proof of Theorem 4.1, we can show that in still wins at price in . Since

we know that obtains more utility when changing bids from to , which is again a contradiction. ∎

C.3 Proof of Theorem 4.3

Proof.

Consider the equilibrium . For any loser , by the best response rule of Lemma 3.1, we know that for all items. For any winner , we have ; further, for any item , by the best response rule of Lemma 3.2, we have , where the first inequality follows from the fact that the dynamics converges, and the second inequality follows from the observation that when bids zero, all prices will not increase.

Let be an efficient allocation and maximizes social welfare. Given the existence of dummy buyers, we can assume without loss of generality that all items all sold out in both and . Consider the exclusive-OR relation given by the two allocations; it can be seen that it contains either alternating paths of even length where both endpoints are buyers or alternating cycles.

If there is an alternating path of even length, say,

By the above discussions, we have

Adding these inequalities together yields

which implies that has the same maximum total valuation on such a path as .

The analysis is similar on alternating cycles. Hence, the allocation is efficient as well, which completes the proof.

∎

Appendix D Nash Equilibria with Various Equilibrium Prices

The following examples show that in general the max-eq prices in a Nash equilibrium can be either (much) smaller or higher than the min-eq price vector at truthful bidding. These examples are in contrast with the statement of Theorem 4.2 which says that when buyers bid aligned vectors initially, we always have .

Example D.1.

(Nash equilibrium with small max-eq prices) There are buyers and items . Buyer only desires with value ; buyer only desires and with value for ; and buyer only desires with value . That is, all buyers have the same value for the items that they desire. It can be seen that in the minimum equilibrium , for all items. On the other hand, consider the bid vector , allocation vector (where and does not win any item), and price vector given by the following figure:

![[Uncaptioned image]](/html/1103.4196/assets/x4.png)

It can be seen that is a max-eq of . Further, is a Nash equilibrium for the max-eq mechanism. (Indeed, for any buyer , the maximum equilibrium price vector for bid vector where bids zero for all items is the same as . For any buyer , , by Lemma 3.2, the utility of is maximized when bidding ; in this case, however, the price of will be increased to ; hence, will obtain the same utility as . We can verify that buyers and cannot obtain more utilities similarly.) Hence, the equilibrium price vector in a Nash equilibrium of the max-eq mechanism can be (much) smaller than the minimum equilibrium price vector .

Example D.2.

(Nash equilibrium with large max-eq prices) There are buyers and items . Buyer only desires with value ; buyer only desires and with value for ; and buyer only desires with value . It can be seen that in the minimum equilibrium , for all items. On the other hand, consider the bid vector , allocation vector (where and does not win any item), and price vector given by the following figure:

![[Uncaptioned image]](/html/1103.4196/assets/x5.png)

It can be seen that is a max-eq of . Further, is a Nash equilibrium for the max-eq mechanism. (Indeed, for any buyer , the maximum equilibrium price vector for bid vector where bids zero for all items is the same as . Similar to the above example, we can verify that no buyer cannot obtain more utility by unilaterally changing his bid.) Hence, the equilibrium price vector in a Nash equilibrium of the max-eq mechanism can be (much) larger than the minimum equilibrium price vector .

The above examples are not contradictory to Theorem 4.2, which says that starting from any aligned bid vector, the aligned best response dynamics converges to the min-eq prices. In particular, the initials bid vectors in the above examples are not aligned; hence, the claim in Theorem 4.2 does not apply here.