Goodness-of-fit Tests For Elliptical And Independent Copulas Through Projection Pursuit

Abstract

Two goodness-of-fit tests for copulas are being investigated. The first one deals with the case of elliptical copulas and the second one deals with independent copulas. These tests result from the expansion of the projection pursuit methodology we will introduce in the present article. This method enables us to determine on which axis system these copulas lie as well as the exact value of these very copulas in the basis formed by the axes previously determined irrespective of their value in their canonical basis. Simulations are also presented as well as an application to real datasets.

keywords:

Copulas; Goodness-Of-Fit; Projection Pursuit; Elliptical Distributions.MSC:

62H05 62H15 62H40 62G15.Outline of the article

The need to describe the dependency between two or more random variables triggered the concept of copulas. Let us consider a joint cumulative distribution function (cdf) on and let us consider its cdf margins , , …,, then a copula is a function such that

Sklar, (1959) is the first to have established the bases of this new theory. Several parametric families of copulas have since been defined, namely elliptical, archimedean, periodic copulas etc - see Joe, (1997) and Nelsen, (2006) as well as appendix A for an overview of these families.

Finding criterias to determine the best copula for a given problem can only be achieved through a goodness-of-fit (GOF) approach.

Several GOF copula approaches have so far been proposed in the literature, e.g. Carriere, (1994), Genest and Rémillard, (2004), Fermanian, (2005), Genest Quessy and Rémillard, (2006), Michiels and De Schepper, (2008), Genest Favre Béliveau and Jacques, (2009), Mesfioui Quessy and Toupin, (2009), Genest Rémillard and Beaudoin, 2009- (2), Berg, (2009), Bücher and Dette, (2010), among others.

However, the field is still at an embryonic stage which explains the current shortage in recommendations.

In univariate distributions, the GOF assessment can be performed using for instance the well-known Kolmogorov test.

In the multivariate field, there are fewer alternatives. A simple way to build GOF approaches for multivariate random variables is to consider multi-dimensional chi-square approaches, as in for example Broniatowski, (2006).

However, these approaches present feasibility issues for high dimensional problems due to the curse of dimensionality.

In order to solve this, we will now introduce the theory of projection pursuit.

The objective of projection pursuit is to generate one or several projections providing as much information as possible about the structure of the dataset regardless of its size.

Once a structure has been isolated, the corresponding data are transformed through a Gaussianization. Through a recursive approach, this process is iterated to find another structure in the remaining data, until no futher structure can be evidenced in the data left at the end.

Friedman, (1984) and Huber, (1985) count among the first authors who introduced this type of approaches for evidencing structures. They each describe, with many examples, how to evidence such a structure and consequently how to estimate the density of such data through two different methodologies each. Their work is based on maximizing Kullback-Leibler divergence.

In the present article, we will introduce a new projection pursuit methodology based on the minimisation of any -divergence greater than the - distance (-PP). As we will develop later on, this way of implementing this methodology encompasses all other previous methods. This algorithm also presents the extra advantage of being more robust and more rapid from a numerical standpoint. Finally, this process allows not only to carry out GOF tests for elliptical and independent copulas but also to determine the axis system upon which these very copulas are based.

It will also enable us to derive the exact expression of these copulas in the basis constituted by these axes.

This paper is organised as follows : section 1 contains preliminary definitions and properties. In section 2, we present in details the -projection pursuit algorithm. In section 3, we present our first results. In section 4, we introduce our tests. In section 5, we provide two simulations pertaining to the two major situations described herein and we will study a real case.

1 Basic theory

1.1 An introduction to copulas

In this section, we will introduce the concept of copula. We will also define the family of elliptical copulas through a brief reminder of elliptical distributions - see appendix A for an overview of other families.

1.1.1 Sklar’s theorem

First, let us define a copula in

Definition 1.1.

A -dimensional copula is a joint cumulative distribution function defined on , with uniform margins.

Moreover, the following theorem explains in what extent a copula does describe the dependency between two or more random variables.

Theorem 1.1 (Sklar, (1959)).

Let be a joint multivariate distribution with margins ,…, , then, there exists a copula such that

| (1.1) |

Moreover, if marginal cumulative distributions are continuous, then the copula is unique. Otherwise, the copula is unique on the range of values of the marginal cumulative distributions.

1.1.

First, for any copula and any in , , we have

where and are called the Frechet-Hoeffding copula boundaries and are also copulas.

Moreover, we define the independent copula as , for any in , .

Finally, we define the density of a copula as the density associated with the cdf , that we will name :

Definition 1.2.

Should it exist, the density of is defined by , for any in , .

1.1.2 The Gaussian copula

The Gaussian copula can be used in several fields. For example, many credit models are built from this copula, which also presents the property to make extreme values (minimal or maximal) independent - in the limit ; see Joe, (1997) for more details. For example, in , it is derived from the bivariate normal distribution and from Sklar’s theorem. Defining as the standard bivariate normal cumulative distribution function with correlation, the Gaussian copula function is where and where is the standard normal cumulative distribution function. Then, the copula density function is :

where is the density function for the standard bivariate Gaussian with pearson product-moment correlation coefficient and where is the standard normal density. This definition can obviously be extended to .

1.1.3 The elliptical copula

Let us begin with defining the class of elliptical distributions and its properties - see also Cambanis, (1981), Landsman, (2003) :

Definition 1.3.

is said to abide by a multivariate elliptical distribution, denoted , if has the following density, for any in :

where is a positive-definite matrix and where is a -column vector,

where is referred as the "density generator",

where is a normalisation constant, such that ,

with .

Property 1.1.

1/ For any , for any matrix with rank , , and for any -dimensional vector , we have .

Therefore, any marginal density of multivariate elliptical distribution is elliptical, i.e.

, with .

2/ Corollary 5 of Cambanis, (1981) states that conditional densities with elliptical distributions are also elliptical. Indeed, if , with (resp. ) of size (resp. ), then with and

with and .

1.2.

Landsman, (2003) shows that multivariate Gaussian distributions derive from . They also show that if has an elliptical density such that its marginals verify and for then is the mean of and is a multiple of the covariance matrix of . Consequently, from now on, we will assume this is indeed the case.

Definition 1.4.

Let be an elliptical density on and let be an elliptical density on . The elliptical densities and are said to belong to the same family of elliptical densities, if their generating densities are and respectively, which belong to a common given family of densities.

1.1.

Consider two Gaussian densities and . They are said to belong to the same elliptical family as they both present as generating density.

Finally, let us introduce the definition of an elliptical copula which generalizes the above overview of the Gaussian copula :

Definition 1.5.

Elliptical copulas are the copulas of elliptical distributions.

1.2 Brief introduction to the -projection pursuit methodology (-PP)

Let us first introduce the concept of divergence.

1.2.1 The concept of divergence

Let be a strictly convex function defined by and such that . We define a divergence of from - where and are two probability distributions over a space such that is absolutely continuous with respect to - by

or , if and present and as density respectively.

Throughout this article, we will also assume that , that is continuous and that this divergence is greater than the distance - see also Appendix B page B.

1.2.2 Functioning of the algorithm

Let be a density on . We define an instrumental density with the same mean and variance as . We start with performing the test; should this test turn out to be positive, then and the algorithm stops, otherwise, the first step of our algorithm consists in defining a vector and a density by

| (1.2) |

where is the set of non null vectors of and (resp. ) stands for the density of (resp. ) when (resp. ) is the density of (resp. ).

In our second step, we will replace with and we will repeat the first step.

And so on, by iterating this process, we will end up obtaining a sequence of vectors in and a sequence of densities .

We will thus prove that the underlying structures of evidenced through this method are identical to the ones obtained through projection pursuit methodologies based on Kullback-Leibler divergence maximisation, such as Huber’s method - see appendix E.3. We will also evidence the above structures, which will enable us to infer more information on - see example below.

1.3.

First, to obtain an approximation of , we stop our algorithm when the divergence equals zero, i.e. we stop when since it implies with , or when our algorithm reaches the iteration, i.e. we approximate with .

Second, we get with .

Finally, the specific form of the relationship (1.2) establishes that we deal with M-estimation. We can therefore state that our method is more robust than projection pursuit methodologies based on Kullback-Leibler divergence maximisation - see Yohai, (2008), Toma, (2009) as well as Huber, (2004).

At present, let us study the following example:

1.2.

Let be a density defined on by , with being a bi-dimensional Gaussian density, and being a non Gaussian density. Let us also consider , a Gaussian density with the same mean and variance as .

Since , we have as , i.e. the function reaches zero for - where and are the third marginal densities of and respectively. We therefore obtain .

To recapitulate our method, if , we derive from the relationship ; should a sequence , , of vectors in defining and such that exist, then , i.e. coincides with on the complement of the vector subspace generated by the family - see also section 2 for a more detailed explanation.

In the remaining of the study of the algorithm, after having clarified the choice of , we will consider the statistical solution to the representation problem, assuming that is unknown and that , ,… are i.i.d. with density . We will provide asymptotic results pertaining to the family of optimizing vectors - that we will define more precisely below - as goes to infinity. Our results also prove that the empirical representation scheme converges towards the theoretical one.

2 The algorithm

2.1 The model

Let be a density on . We assume there exists non null linearly independent vectors , with of , such that

| (2.1) |

with , being an elliptical density on and with being a density on , which does not belong to the same family as . Let be a vector with as density.

We define as an elliptical distribution with the same mean and variance as .

For simplicity, let us assume that the family is the canonical basis of :

The very definition of implies that is independent from . Hence, the density of given is .

Let us assume that for some . We then get , since, by induction, we have .

Consequently, through lemma F.9 and through the fact that the conditional densities with elliptical distributions are also elliptical, as well as through the above relationship, we can infer that

In other words, coincides with on the complement of the vector subspace generated by the family .

Now, if the family is no longer the canonical basis of , then this family is again a basis of . Hence, lemma F.2 implies that

| (2.2) |

which is equivalent to , since by induction .

The end of our algorithm implies that coincides with on the complement of the vector subspace generated by the family .

Therefore, the nullity of the divergence provides us with information on the density structure.

In summary, the following proposition clarifies our choice of which depends on the family of distribution one wants to find in :

Proposition 2.1.

With the above notations, is equivalent to

More generally, the above proposition leads us to defining the co-support of as the vector space generated by the vectors .

Definition 2.1.

Let be a density on . We define the co-vectors of as the sequence of vectors which solves the problem where is an elliptical distribution with the same mean and variance as . We define the co-support of as the vector space generated by the vectors .

2.2 Stochastic outline of our algorithm

Let , ,.., (resp. , ,..,) be a sequence of independent random vectors with the same density (resp. ).

As customary in nonparametric divergence optimizations, all estimates of and , as well as all uses of Monte Carlo methods are being performed using subsamples , ,.., and , ,.., - extracted respectively from , ,.., and , ,.., - since the estimates are bounded below by some positive deterministic sequence - see Appendix C.

Let be the empirical measure based on the subsample , ,.,. Let (resp. for any in ) be the kernel estimate of (resp. ), which is built from , ,.., (resp. , ,..,).

As defined in section 1.2, we introduce the following sequences and :

| is a non null vector of such that | (2.3) | ||

| is the density such that with |

The stochastic setting up of the algorithm uses and instead of and , since is known. Thus, at the first step, we build the vector which minimizes the divergence between and and which estimates .

Proposition C.1 and lemma F.8 enable us to minimize the divergence between and . Defining as the argument of this minimization, proposition 3.3 shows us that this vector tends to .

Finally, we define the density as which estimates through theorem 3.1.

Now, from the second step and as defined in section 1.2, the density is unknown. Consequently, once again, we have to truncate the samples.

All estimates of and (resp. and ) are being performed using a subsample , ,.., (resp. , ,..,) extracted from , ,.., (resp. , ,.., - which is a sequence of independent random vectors with the same density ) such that the estimates are bounded below by some positive deterministic sequence (see Appendix C).

Let be the empirical measure based on the subsample , ,..,. Let (resp. , , for any in ) be the kernel estimate of (resp. and as well as ) which is built from , ,.., (resp. , ,.., and , ,.., as well as , ,..,).

The stochastic setting up of the algorithm uses and instead of and .

Thus, we build the vector which minimizes the divergence between and - since and are unknown - and which estimates .

Proposition C.1 and lemma F.8 enable us to minimize the divergence between and . Defining as the argument of this minimization, proposition 3.3 shows that this vector tends to in . Finally, we define the density as which estimates through theorem 3.1.

And so on, we will end up obtaining a sequence of vectors in estimating the co-vectors of and a sequence of densities such that estimates through theorem 3.1.

3 Results

3.1 Hypotheses on

Let , ,.., (resp. , ,..,) be a sequence of independent random vectors with the same density (resp. ).

As customary in nonparametric divergence optimizations, all estimates of and as well as all uses of Monte Carlo methods are being performed using subsamples , ,.., and , ,.., - extracted respectively from , ,.., and , ,.., - since the estimates are bounded below by some positive deterministic sequence - see appendix C.

Let be the empirical measure of the subsample , ,.,. Let (resp. for any in ) be the kernel estimate of (resp. ), which is built from , ,.., (resp. , ,..,).

At present, let us define the set of hypotheses on .

Discussion on several of these hypotheses can be found in appendix D.

In the remaining of this section, to be more legible we replace with . Let

where is the probability measure presenting as density.

Similarly as in chapter of Van der Vaart, (1998), let us define :

: For all , there is , such that for all verifying

:

: There exists , a neighbourhood of , and , a positive function, such that, for all ,

: There exists , a neighbourhood of , such that for all , there exists a such that for all

Putting , let us consider now four new hypotheses:

: and are finite and the expressions and

exist and are invertible.

: There exists such that .

: exists and is invertible.

: and are assumed to be positive and bounded and such that

where is the Kullback-Leibler divergence.

3.1.1 Estimation of the first co-vector of

Let be the class of all positive functions defined on and such that is a density on for all belonging to . The following proposition shows that there exists a vector such that minimizes in :

Proposition 3.1.

There exists a vector belonging to such that

3.1.

This proposition proves that simultaneously optimises (E.1), (E.2) and (1.2). In other words, it proves that the underlying structures of evidenced through our method are identical to the ones obtained through projection pursuit methodologies based on Kullback-Leibler divergence maximisation, such as Huber’s methods - see appendix E.

Following Broniatowski, (2009), let us introduce the estimate of , through

Proposition 3.2.

Let be such that

Then, is a strongly convergent estimate of , as defined in proposition 3.1.

3.1.2 Convergence study at the step of the algorithm:

In this paragraph, we show that the sequence converges towards and that the sequence converges towards .

Let with ,

and .

We state

Proposition 3.3.

Both and converge toward a.s.

Finally, the following theorem shows that converges almost everywhere towards :

Theorem 3.1.

It holds

3.1.3 Testing of the criteria

In this paragraph, through a test of our criteria, namely , we will build a stopping rule for this procedure. First, the next theorem enables us to derive the law of our criteria:

Theorem 3.2.

For a fixed , we have

,

where represents the step of our algorithm and where is the identity matrix in .

Note that is fixed in theorem 3.2 since where is a known function of - see section 3.1. Thus, in the case when , we obtain

Corollary 3.1.

We have .

Hence, we propose the test of the null hypothesis

: versus the alternative : .

Based on this result, we stop the algorithm, then, defining as the last vector generated, we derive from corollary 3.1 a -level confidence ellipsoid around , namely

where is the quantile of a -level reduced centered normal distribution and where is the empirical measure araising from a realization of the sequences and .

Consequently, the following corollary provides us with a confidence region for the above test:

Corollary 3.2.

is a confidence region for the test of the null hypothesis versus .

4 Goodness-of-fit tests

4.1 The basic idea

Let be a density defined on . Let us also consider , a known elliptical density with the same mean and variance as .

Let us also assume that the family is the canonical basis of and that .

Hence, since lemma F.9 page F.9 implies that if , we then have .

Moreover, we get with , as derived from property B.1 page B.1.

Consequently, i.e. , and then

where (resp. ) is the copula of (resp. ).

More generally, if is defined on , then the family is once again free - see lemma F.10 page F.10 -, i.e. the family is once again a basis of . The relationship therefore implies that , i.e. for any ,

since lemma F.9 page F.9 implies that if . In other words, for any , it holds

| (4.1) |

Finally, putting and defining vector (resp. density , copula of , density , copula of ) as the expression of vector (resp. density , copula of , density , copula of ) in basis , then, the following proposition provides us with the density associated with the copula of as being equal to the density associated with the copula of in basis :

Proposition 4.1.

With the above notations, should a sequence of not null vectors in defining and such that exist, then

4.2 With the elliptical copula

Let be an unknown density defined on . The objective of the present section is to determine whether the copula of is elliptical. We thus define an instrumental elliptical density with the same mean and variance as , and we follow the procedure of section 2.2. As explained in section 4.1, we infer from proposition 4.1 that the copula of equals the copula of when , i.e. when is the last vector generated from the algorithm and when is the canonical basis of . Thus, in order to verify this assertion, corollary 3.1 page 3.1 provides us with a -level confidence ellipsoid around this vector, namely

where is the quantile of a -level reduced centered normal distribution, where is the empirical measure araising from a realization of the sequences and - see appendix C - and where is a known function of , and - see section 3.1.

Consequently, keeping the notations introduced in section 4.1, we can perform a statistical test of the null hypothesis

| : versus : |

Since, under , we have , then the following theorem provides us with a confidence region for this test.

Theorem 4.1.

The set is a confidence region for the test of the null hypothesis versus the alternative .

4.1.

1/ If , for , then we reiterate the algorithm until is created in order to obtain a relationship for the copula of .

2/ If the do not constitute the canonical basis, then keeping the notations introduced in section 4.1, our algorithm meets the test :

| : versus : |

Thus, our method enables us to tell wether the copula of equals the copula of in the basis.

4.3 With the independent copulas

Let be a density on and let be a random vector with as density. The objective of this section is to determine whether is the product of its margins, i.e. whether the copula of is the independent copula. Let thus be an instrumental product of univariate Gaussian density - with as covariance matrix and with the same mean as - as explained at section 4.2, let us follow the procedure described at section 2.2, i.e. proposition 4.1 infers that the copula of is the independent copula when . Thus, we perform a statistical test of the null hypothesis :

| : versus the alternative : |

Since, under , we have , then the following theorem provides us with a confidence region for our test.

Theorem 4.2.

Keeping the notations of section 4.2, the set is a confidence region for the test of the null hypothesis versus the alternative .

4.2.

1/ As explained in section 4.2, if , for , we reiterate the algorithm until is created in order to derive a relationship for the copula of .

2/ If the do not constitute the canonical basis, then keeping the notations introduced in section 4.1, our algorithm meets the test :

| : versus the alternative : |

Thus, our method enables us to determine if the the copula of is the independent copula in the basis.

4.4 Study of the subsequence defined by for any

Let be the set of non-negative integers defined by , where - such that - is its cardinal. In the present section, our goal is to study the subsequence of the sequence defined by for any belonging to .

First, we have :

, through property B.1

, as explained in section 4.2,

, which amounts to the previous relationship written in the

basis with the notations introduced in section 4.2.

Moreover, defining as the previous integer , in the space , with , and as explained in section 2.1, the relationship implies that

where is the density of vector in the basis.

Consequently,

.

Hence, we can infer that

| (4.2) |

The following theorem explicitely describes the form of the copula in the basis :

Theorem 4.3.

4.3.

If there exists such that and , then the notation means . Thus, if, for any , we have , then, for any , we have , i.e. we have - where is the marginal density of .

At present, using relationship 4.2 and remark 4.3, the following corollary gives us the copula of as equals to 1 in the basis when, for any , :

Corollary 4.1.

In the case where, for any , , it holds:

5 Simulations

Let us examine two simulations and an application to real datasets. The first simulation studies the elliptical copula and the second studies the independent copula.

In each simulation, our program will aim at creating a sequence of densities , such that and where is a divergence - see appendix B for its definition - and

for all . We will therefore perform the tests introduced in theorems 4.1 and 4.2.

5.1.

We are in dimension (=d), and we use the divergence to perform our optimisations. Let us consider a sample of (=n) values of a random variable with a density law defined by :

where :

is the Gaussian copula with correlation coefficient ,

the Gumbel distribution parameters are and and the exponential density parameter is .

Let us generate then a Gaussian random variable with a density - that we will name - presenting the same mean and variance as .

We theoretically obtain and .

To get this result, we perform the following test:

Then, theorem 4.1 enables us to verify by the following 0.9(=) level confidence ellipsoid

And, we obtain

| Our Algorithm | ||

|---|---|---|

| Projection Study 0 : | minimum : 0.445199 | |

| at point : (1.0171,0.0055) | ||

| P-Value : 0.94579 | ||

| Test : | : : True | |

| Projection Study 1 : | minimum : 0.009628 | |

| at point : (0.0048,0.9197) | ||

| P-Value : 0.99801 | ||

| Test : | : : True | |

| (Kernel Estimation of , ) | 3.57809 |

Therefore, we can conclude that is verified.

5.2.

We are in dimension (=d), and we use the divergence to perform our optimisations.

Let us consider a sample of (=n) values of a random variable with a density law defined by

,

where the Gumbel distribution parameters are and and the exponential density parameter is .

Let be an instrumental product of univariate Gaussian densities - with as covariance matrix and with the same mean as .

We theoretically obtain and . To get this result, we perform the following test:

.

Then, theorem 4.2 enables us to verify by the following 0.9(=) level confidence ellipsoid

.

And, we obtain

| Our Algorithm | ||

|---|---|---|

| Projection Study 0 : | minimum : 0.057833 | |

| at point : (0.9890,0.1009) | ||

| P-Value : 0.955651 | ||

| Test : | : : True | |

| Projection Study 1 : | minimum : 0.02611 | |

| at point : (-0.1105,0.9290) | ||

| P-Value : 0.921101 | ||

| Test : | : : True | |

| (Kernel Estimation of , ) | 1.25945 |

Therefore, we can conclude that

5.0.1 Application to real datasets

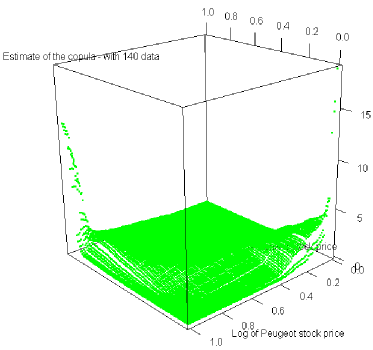

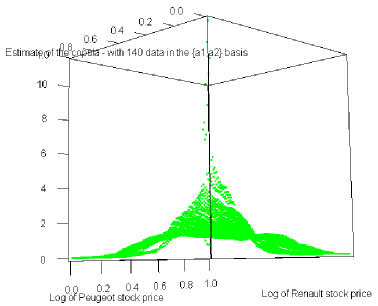

Let us for instance study the moves in the stock prices of Renault and Peugeot from January 4, 2010 to July 25, 2010. We thus gather 140(=n) data from these stock prices - see data below.

Let us also consider (resp. ) the random variable defining the stock price of Renault (resp. Peugeot). We will assume - as it is commonly done in mathematical finance - that the stock market abides by the classical hypotheses of the Black-Scholes model - see Black and Scholes, (1973).

Consequently, and each present a log-normal distribution as probability distribution.

Let be the density of vector , let us now apply our algorithm to with the Kullback-Leibler divergence as -divergence. Let us generate then a Gaussian random variable with a density - that we will name - presenting the same mean and variance as .

We first assume that there exists a vector such that .

In order to verify this hypothesis, our reasoning will be the same as in Simulation 5.1. Indeed, we assume that this vector is a co-factor of . Consequently, corollary 3.2 enables us to estimate by the following 0.9(=) level confidence ellipsoid

.

And, we obtain

| Our Algorithm | ||

|---|---|---|

| Projection Study 0 : | minimum : 0.02087685 | |

| at point : =(19.1,-12.3) | ||

| P-Value : 0.748765 | ||

| Test : | : : True | |

| K(Kernel Estimation of , ) | 4.3428735 |

Therefore, our first hypothesis is confirmed.

However, our goal is to study the copula of . Then, as explained in section 4.4, we formulate another hypothesis assuming that there exists a vector such that .

In order to verify this hypothesis, we will use the same reasoning as above. Indeed, we assume that this vector is a co-factor of . Consequently, corollary 3.2 enables us to estimate by the following 0.9(=) level confidence ellipsoid

.

And, we obtain

| Our Algorithm | ||

|---|---|---|

| Projection Study 1 : | minimum : 0.0198753 | |

| at point : =(8.1,3.9) | ||

| P-Value : 0.8743401 | ||

| Test : | : : True | |

| K(Kernel Estimation of , ) | 4.38475324 |

Therefore, our second hypothesis is confirmed.

In conclusion, as explained in corollary 4.1, the copula of is equal to in the basis.

| Date | Renault | Peugeot | Date | Renault | Peugeot | Date | Renault | Peugeot |

|---|---|---|---|---|---|---|---|---|

| 23/07/10 | 34.9 | 24.2 | 22/07/10 | 34.26 | 24.01 | 21/07/10 | 33.15 | 23.3 |

| 20/07/10 | 32.69 | 22.78 | 19/07/10 | 33.24 | 23.36 | 16/07/10 | 33.92 | 23.77 |

| 15/07/10 | 34.44 | 23.71 | 14/07/10 | 35.08 | 24.36 | 13/07/10 | 35.28 | 24.37 |

| 12/07/10 | 33.84 | 23.16 | 09/07/10 | 33.46 | 23.13 | 08/07/10 | 33.08 | 22.65 |

| 07/07/10 | 32.15 | 22.19 | 06/07/10 | 31.12 | 21.56 | 05/07/10 | 30.02 | 20.81 |

| 02/07/10 | 30.17 | 20.85 | 01/07/10 | 29.56 | 20.05 | 30/06/10 | 30.78 | 21.07 |

| 29/06/10 | 30.55 | 20.97 | 28/06/10 | 32.34 | 22.3 | 25/06/10 | 31.35 | 21.68 |

| 24/06/10 | 32.29 | 22.25 | 23/06/10 | 33.58 | 22.47 | 22/06/10 | 33.84 | 22.77 |

| 21/06/10 | 34.06 | 23.25 | 18/06/10 | 32.89 | 22.7 | 17/06/10 | 32.08 | 22.31 |

| 16/06/10 | 31.87 | 21.92 | 15/06/10 | 32.03 | 22.12 | 14/06/10 | 31.45 | 22.2 |

| 11/06/10 | 30.62 | 21.42 | 10/06/10 | 30.42 | 20.93 | 09/06/10 | 29.27 | 20.34 |

| 08/06/10 | 28.48 | 19.73 | 07/06/10 | 28.92 | 20.15 | 04/06/10 | 29.19 | 20.27 |

| 03/06/10 | 30.35 | 20.46 | 02/06/10 | 29.33 | 19.53 | 01/06/10 | 28.87 | 19.45 |

| 31/05/10 | 29.39 | 19.54 | 28/05/10 | 29.16 | 19.55 | 27/05/10 | 29.18 | 19.81 |

| 26/05/10 | 27.5 | 18.5 | 25/05/10 | 26.76 | 18.08 | 24/05/10 | 28.75 | 18.81 |

| 21/05/10 | 28.78 | 18.82 | 20/05/10 | 28.53 | 18.84 | 19/05/10 | 29.49 | 19.25 |

| 18/05/10 | 30.95 | 19.76 | 17/05/10 | 30.92 | 19.35 | 14/05/10 | 31.35 | 19.34 |

| 13/05/10 | 33.65 | 20.76 | 12/05/10 | 33.63 | 20.52 | 11/05/10 | 33.38 | 20.34 |

| 10/05/10 | 33.28 | 20.3 | 07/05/10 | 31 | 19.24 | 06/05/10 | 32.4 | 20.22 |

| 05/05/10 | 32.95 | 20.45 | 04/05/10 | 33.3 | 21.03 | 03/05/10 | 35.58 | 22.63 |

| 30/04/10 | 35.41 | 22.45 | 29/04/10 | 35.53 | 22.36 | 28/04/10 | 34.75 | 22.33 |

| Date | Renault | Peugeot | Date | Renault | Peugeot | Date | Renault | Peugeot |

|---|---|---|---|---|---|---|---|---|

| 27/04/10 | 36.2 | 22.9 | 26/04/10 | 37.65 | 23.73 | 23/04/10 | 36.72 | 23.5 |

| 22/04/10 | 34.36 | 22.72 | 21/04/10 | 35.01 | 22.86 | 20/04/10 | 35.62 | 22.88 |

| 19/04/10 | 34.08 | 21.77 | 16/04/10 | 34.46 | 21.71 | 15/04/10 | 35.16 | 22.22 |

| 14/04/10 | 35.1 | 22.22 | 13/04/10 | 35.28 | 22.45 | 12/04/10 | 35.17 | 21.85 |

| 09/04/10 | 35.76 | 21.9 | 08/04/10 | 35.67 | 21.67 | 07/04/10 | 36.5 | 21.89 |

| 06/04/10 | 36.87 | 22 | 01/04/10 | 35.5 | 21.97 | 31/03/10 | 34.7 | 21.8 |

| 30/03/10 | 34.8 | 22.24 | 29/03/10 | 35.7 | 22.73 | 26/03/10 | 35.54 | 22.58 |

| 25/03/10 | 35.53 | 22.73 | 24/03/10 | 33.8 | 21.82 | 23/03/10 | 34.1 | 21.58 |

| 22/03/10 | 33.73 | 21.64 | 19/03/10 | 34.12 | 21.68 | 18/03/10 | 34.44 | 21.75 |

| 17/03/10 | 34.68 | 21.98 | 16/03/10 | 34.33 | 21.88 | 15/03/10 | 33.57 | 21.53 |

| 12/03/10 | 33.9 | 21.86 | 11/03/10 | 33.27 | 21.58 | 10/03/10 | 33.12 | 21.47 |

| 09/03/10 | 32.69 | 21.54 | 08/03/10 | 32.99 | 21.66 | 05/03/10 | 32.89 | 21.85 |

| 04/03/10 | 31.64 | 21.26 | 03/03/10 | 31.65 | 20.7 | 02/03/10 | 31.05 | 20.2 |

| 01/03/10 | 30.26 | 19.54 | 26/02/10 | 30.2 | 19.39 | 25/02/10 | 29.42 | 18.98 |

| 24/02/10 | 30.9 | 19.49 | 23/02/10 | 30.54 | 19.74 | 22/02/10 | 31.89 | 20.06 |

| 19/02/10 | 32.29 | 20.67 | 18/02/10 | 32.26 | 20.41 | 17/02/10 | 31.69 | 20.31 |

| 16/02/10 | 31.08 | 19.8 | 15/02/10 | 30.25 | 19.66 | 12/02/10 | 29.56 | 19.57 |

| 11/02/10 | 31 | 20.4 | 10/02/10 | 32.78 | 21.21 | 09/02/10 | 33.31 | 22.31 |

| 08/02/10 | 32.63 | 21.95 | 05/02/10 | 32.15 | 22.33 | 04/02/10 | 33.72 | 22.86 |

| 03/02/10 | 35.32 | 23.93 | 02/02/10 | 35.29 | 23.8 | 01/02/10 | 35.31 | 24.05 |

| 29/01/10 | 34.26 | 23.64 | 28/01/10 | 33.94 | 23.31 | 27/01/10 | 33.85 | 23.88 |

| 26/01/10 | 34.97 | 24.86 | 25/01/10 | 35.06 | 24.35 | 22/01/10 | 35.7 | 24.95 |

| 21/01/10 | 36.1 | 25 | 20/01/10 | 36.92 | 25.35 | 19/01/10 | 38.4 | 25.81 |

| 18/01/10 | 39.28 | 25.95 | 15/01/10 | 38.6 | 25.7 | 14/01/10 | 39.56 | 26.67 |

| 13/01/10 | 39.49 | 26.13 | 12/01/10 | 38.36 | 25.98 | 11/01/10 | 39.21 | 26.65 |

| 08/01/10 | 39.38 | 26.5 | 07/01/10 | 39.69 | 26.7 | 06/01/10 | 39.25 | 26.32 |

| 05/01/10 | 38.31 | 24.74 | 04/01/10 | 38.2 | 24.52 |

Critics of the simulations

In the case where is unknown, we will never be sure to have reached the minimum of the -divergence: we have indeed used the simulated annealing method to solve our optimisation problem, and therefore it is only when the number of random jumps tends in theory towards infinity that the probability to get the minimum tends to 1.

We also note that no theory on the optimal number of jumps to implement does exist, as this number depends on the specificities of each particular problem.

Moreover, we choose the for the AMISE of the two simulations. This choice leads us to simulate 50 random variables - see Scott, (1992) page 151 -, none of which have been discarded to obtain the truncated sample.

This has also been the case in our application to real datasets.

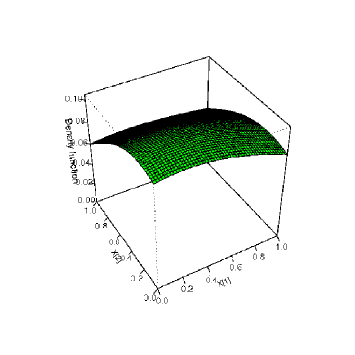

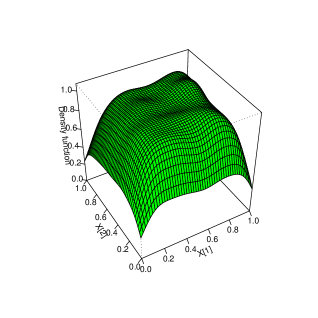

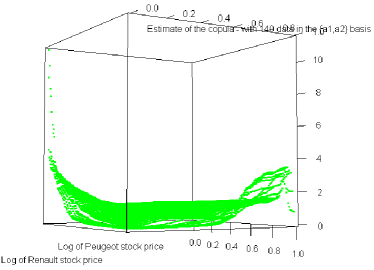

Finally, the shape of the copula in the case of real datasets in the basis is also noteworthy.

Figure 4 shows that the curve reaches a quite wide plateau around , whereas Figure 5 shows that this plateau prevails on almost the entire set. We can therefore conclude that the theoritical analysis is indeed confirmed by the above simulation.

Conclusion

Projection Pursuit is useful in evidencing characteristic structures as well as one-dimensional projections and their associated distribution in multivariate data. This article clearly evidences the efficiency of the -projection pursuit methodology for goodness-of-fit tests for copulas. Indeed, the robustness as well as the convergence results we achieved, convincingly fulfilled our expectations regarding the methodology used.

Appendix A On the different families of copula

There exists many copula families. Let us here present the most important amongst them.

A.1 Archimedean copulas

These copulas present a simple form with properties such as associativity and have a variety of dependent structures. They can generally be defined under the following form

where and where is known as a "generator function". This function must be at least times continuously differentiable, must have a decreasing and convex derivative, and must be such that .

Let us now present several examples :

1/ Clayton copula:

The Clayton copula is an asymmetric archimedean copula, exhibiting greater dependency in the negative tail than in the positive tail.

Let us define (resp. ) as the random vector having (resp ) as cumulative distribution function (CDF). Assuming that the vector has a Clayton copula, then this copula is given by:

And its generator is:

For in the Clayton copula, the random variables are statistically independent. The generator function approach can be extended to create multivariate copulas, simply by including more additive terms.

2/ Gumbel copula:

The Gumbel copula (a.k.a. Gumbel-Hougard copula) is an asymmetric archimedean copula, exhibiting greater dependency in the positive tail than in the negative tail. This copula is given by:

3/ Frank copula:

The Frank copula is a symmetric archimedean copula given by:

A.2 Periodic copula

In 2005, Aurélien Alfonsi and Damiano Brigo, (2005) introduced a way of constructing copulas based on periodic functions. Defining (resp. ) as a 1-periodic non-negative function that integrates to over (resp. as a double primitive of ), then both

are copula functions, the second one not being necessarily exchangeable.

Appendix B -Divergence

Let us call the density of if is the density of . Let be a strictly convex function defined by and such that .

Definition B.1.

We define a divergence of from , where and are two probability distributions over a space such that is absolutely continuous with respect to , by

| (B.1) |

The above expression (B.1) is also valid if and are both dominated by the same probability.

The most used distances (Kullback, Hellinger or ) belong to the Cressie-Read family (see Cressie-Read, (1984), Csiszár I., (1967) and the books of Friedrich and Igor, (1987), Pardo Leandro, (2006) and Zografos K., (1990)). They are defined by a specific . Indeed,

- with the Kullback-Leibler divergence, we associate

- with the Hellinger distance, we associate

- with the distance, we associate

- more generally, with power divergences, we associate , where

- and, finally, with the norm, which is also a divergence, we associate

Let us now present some well-known properties of divergences.

Property B.1.

We have

Property B.2.

The divergence function is

convex,

lower semi-continuous, for the topology that makes all the applications of the form continuous where is bounded and continuous, and

lower semi-continuous for the topology of the uniform convergence.

Finally, we will also use the following property derived from the first part of corollary (1.29) page 19 of Friedrich and Igor, (1987),

Property B.3.

If is measurable and if then with equality being reached when is surjective for .

Appendix C Study of the sample

Let , ,.., be a sequence of independent random vectors with same density . Let , ,.., be a sequence of independent random vectors with same density . Then, the kernel estimators , , and of , , and , for all , almost surely and uniformly converge since we assume that the bandwidth of these estimators meets the following conditions (see Bosq, (1999)):

: , , and ,

with .

Let us consider

and

Our goal is to estimate the minimum of .

To do this, it is necessary for us to truncate our samples:

Let us consider now a positive sequence such that where is the almost sure convergence rate of the kernel density estimator - , see lemma F.3 - where is defined by

for all in and all in , and finally where is defined by

for all in and all in .

We will generate , and from the starting sample and we will select the and vectors such that and , for all and for all .

The vectors meeting these conditions will be called and .

Consequently, the next proposition provides us with the condition required for us to derive our estimates:

Proposition C.1.

C.1.

With the Kullback-Leibler divergence, we can take for the expression , with .

Appendix D Hypotheses’ discussion

D.1 Discussion of .

Let us work with the Kullback-Leibler divergence and with and .

For all , we have

since, for any in , the function is a density.

The complement of in is and then the supremum looked for in is .

We can therefore conclude.

It is interesting to note that we obtain the same verification with , and .

D.2 Discussion of .

This hypothesis consists in the following assumptions:

We work with the Kullback-Leibler divergence, (0)

We have , i.e. - we could also derive the same proof with , and - (1)

Preliminary :

Shows that

through a reductio ad absurdum, i.e. if we assume .

Thus, our hypothesis enables us to derive

since implies , i.e. . We can therefore conclude.

Preliminary :

Shows that

through a reductio ad absurdum, i.e. if we assume .

Thus, our hypothesis enables us to derive

We can therefore conclude as above.

Let us now verify :

We have

Moreover, the logarithm is negative on

and is positive on .

Thus, the preliminary studies and show that and always present a negative product. We can therefore conclude, since is not null for all and for all - with .

Appendix E On Huber’s algorithms

In the present appendix, let us now first present the projection pursuit methodologies introduced by Huber, (1985). Secondly, we will show that our method encompasses Hubers’.

E.1 Huber’s analytic approach

Let be a density on . We define an instrumental density with the same mean and variance as . Huber’s methodology requires us to start with performing the test - with being the Kullback-Leibler divergence. Should this test turn out to be positive, then and the algorithm stops. If the test were not to be verified, the first step of Huber’s algorithm would amount to defining a vector and a density by

| (E.1) |

where is the set of non null vectors of and (resp. ) stands for the density of (resp. ) when (resp. ) is the density of (resp. ). More exactly, this results from the maximisation of since and it is assumed that is finite.

In a second step, Huber replaces with and goes through the first step again.

By iterating this process, Huber thus obtains a sequence of vectors of and a sequence of densities .

E.1.

This algorithm stops when the Kullback-Leibler divergence equals zero or when it reaches the iteration. We then obtain an approximation of from :

When there exists an integer such that with , he obtains , i.e. since by induction . Similarly, when, for all , Huber gets with , he assumes in order to derive .

Finally, he obtains with .

E.2 Huber’s synthetic approach

Keeping the notations of the above section, we start with performing the test; should this test turn out to be positive, then and the algorithm stops, otherwise, the first step of his algorithm would consist in defining a vector and a density by

| (E.2) |

More exactly, this optimisation results from the maximisation of since and it is assumed that is finite. In a second step, Huber replaces with and goes through the first step again. By iterating this process, Huber thus obtains a sequence of vectors of and a sequence of densities .

E.2.

First, in a similar manner to the analytic approach, this methodology enables us to approximate from :

To obtain an approximation of , Huber either stops his algorithm when the Kullback-Leibler divergence equals zero, i.e. implies with , or when his algorithm reaches the iteration, i.e. he approximates with .

Second, he gets with .

E.3 The first co-vector of simultaneously optimizes four problems

Let us first study Huber’s analytic approach.

Let be the class of all positive functions defined on and such that is a density on for all belonging to . The following proposition shows that there exists a vector such that minimizes in :

Proposition E.1 (Analytic Approach).

There exists a vector belonging to such that

and

Let us also study Huber’s synthetic approach:

Let be the class of all positive functions defined on and such that is a density on for all belonging to . The following proposition shows that there exists a vector such that minimizes in :

Proposition E.2 (Synthetic Approach).

There exists a vector belonging to such that

and

To recapitulate, the choice of enables us to simultaneously solve the following three optimisation problems, for :

- analytic approach -

- synthetic approach -

- our method.

We can therefore state that the methodology we introduced in the present article encompasses Hubers’.

Appendix F Proofs

Proof of propositions E.1 and E.2.

Let us first study proposition E.2.

Without loss of generality, we will prove this proposition with in lieu of .

Let us define . We remark that and present the same density conditionally to .

Indeed,

.

Thus, we can demonstrate this proposition.

We have and is the marginal density of

Hence,

and since is positive, then is a density.

Moreover,

| (F.2) |

as . Since the minimum of this last equation (F.2) is reached through the minimization of ,

then property B.1 necessarily implies that , hence .

Finally, we have

which completes the demonstration of proposition E.2.

Similarly, if we replace with and with , we obtain the proof of proposition E.1.

Proof of proposition 3.1.

The demonstration is also very similar to the one for proposition E.2, save for the fact we now base our reasoning at row F on

instead of .

Proof of lemma F.1.

lemme F.1.

We have .

We get the result since

.

Proof of proposition F.1.

Proposition F.1.

In the case where is known and keeping the notations introduced in section 3.1, as well as assuming to hold, then both and tend to a.s.

In the same manner as in Proposition 3.4 of Broniatowski, (2009), we prove this proposition through lemma F.1.

Proof of proposition 3.3.

Proposition 3.3 comes immediately from proposition C.1 page C.1 and lemma F.1 page F.1.

Proof of theorem 3.1.

We prove this theorem by induction.

First, by the very definition of the kernel estimator converges towards . Moreover, the continuity of and and proposition 3.3 imply that converges towards .

Finally, since, for any , , we conclude similarly as for .

Proof of lemma F.2.

lemme F.2.

We have .

Putting , let us determine in basis .

Let us first study the function defined by ,

We can immediately say that is continuous and since is a basis, its bijectivity is obvious.

Moreover, let us study its Jacobian.

By definition, it is since is a basis. We can therefore infer :

i.e. (resp. ) is the expression of (resp of ) in basis , namely

, with and being the expressions of and in basis .

Consequently, our results in the case where the family is the canonical basis of , still hold for in basis - see section 2.1. And then, if is the expression of in basis , we have

, i.e. .

Proof of lemma F.3.

lemme F.3.

For any continuous density , we have .

Defining as , we have . Moreover,

from page 150 of Scott, (1992), we derive that where . Then, we obtain . Finally, since the central limit theorem rate is , we infer that .

Proof of lemma F.4.

lemme F.4.

Let be an absolutely continuous density, then, for all sequences tending to in , sequence uniformly converges towards .

Proof.

For all in , let be the cumulative distribution function of and be a complex function defined by , for all and in .

First, the function is an analytic function, because is continuous and as a result of the corollary of Dini’s second theorem - according to which

"A sequence of cumulative distribution functions, which pointwise converges on towards a continuous cumulative distribution function on , uniformly converges towards on "-

we deduct that, for all sequences converging towards , uniformly converges towards .

Finally, the Weierstrass theorem, (see proposal page 220 of the "Calcul infinitésimal" book of Jean Dieudonné), implies that all sequences uniformly converge towards , for all tending to . We can therefore conclude.

∎

Proof of lemma F.5. By definition of the closure of a set, we have

lemme F.5.

The set is closed in for the topology of the uniform convergence.

Proof of lemma F.6. Since is greater than the distance, we have

lemme F.6.

For all , we have where .

lemme F.7.

is closed in for the topology of the uniform convergence.

Proof of lemma F.8.

lemme F.8.

is reached when the -divergence is greater than the distance as well as the distance.

Proof.

Indeed, let be and be for all >0. From lemmas F.5, F.6 and F.7 (see page F.6), we get is a compact for the topology of the uniform convergence, if is not empty. Hence, and since property B.2 (see page B.2) implies that is lower semi-continuous in for the topology of the uniform convergence, then the infimum is reached in . (Taking for example is necessarily not empty because we always have ). Moreover, when the divergence is greater than the distance, the very definition of the space enables us to provide the same proof as for the distance. ∎

Proof of lemma F.9.

lemme F.9.

For any , we have .

Assuming, without any loss of generality, that the , , are the vectors of the canonical basis, since

we derive immediately that . We note that it is sufficient to operate a change in basis on the to obtain the general case since is a basis - see lemma F.10.

Proof of lemma F.10.

lemme F.10.

If there exists , , such that , then the family of is free and is orthogonal.

Without any loss of generality, let us assume that and that the are the vectors of the canonical basis. Using a reductio ad absurdum based on the hypotheses and , where , we get and . Hence

It consequently implies that since

.

Therefore, , i.e. which leads to a contradiction. Hence, the family is free.

Moreover, using a reductio ad absurdum, we get the orthogonality. Indeed, we have

. The use of the same argument as in the proof of lemma F.11, enables us to infer the orthogonality of .

Proof of lemma F.11.

lemme F.11.

Should there exist a family such that with , with , and being densities, then this family is an orthogonal basis of .

Using a reductio ad absurdum, we have . We can therefore conclude.

Proof of proposition 4.1.

Through lemma F.10, we can consequently infer that is a basis of

Let us now write in the system.

Let us first study the function defined by

We can say is continuous and since is a basis, its bijectivity is obvious.

Let us also study its Jacobian. By definition, it is

since is a basis. Thus, we can infer that, in basis , the writing of (resp. ) exists and is unique. Defining (resp. ) as this new form of (resp. ), we have (resp. ). Similarly, let us define (resp. ) as being the form of (resp. ) in basis , we also have

(resp. ).

Now, through a finite induction in , , let us demonstrate the following property

Initialisation :

For . The above notations lead us to , since through the change in variables, i.e. by the very definition of conditional density. Hence, holds true.

For . Since is true, we can write

by the very definition of conditional density. Thus, holds true.

Going from to :

Let us assume is true, we can then show that .

, since is true,

Thus, is true.

Conclusion :

The induction principle enables us to infer that holds true for .

At present, since , the above entails that , i.e.

We finally obtain ,

where and are the respective copulas of and

Let us remark that, if the are the canonical basis of , we have

,

where and are the respective copulas of and

Proof of proposition C.1.

Let us first note that we will prove this proposition for , i.e. in the case where is not known. The initial case using the known density , will be an immediate consequence of the above.

Moreover, going forward, to be more legible, we will use (resp. ) in lieu of (resp. ).

We can therefore remark that we have , and , for all and for all , thanks to the uniform convergence of the kernel estimators.

Indeed, we have , by definition of , and then , by hypothesis on . This is also true for and .

This entails

Indeed, let us remark that

Moreover, since , as implied by lemma B.3, and since we assumed such that and and since , the law of large numbers enables us to state that

Furthermore,

and

as a result of the hypotheses initially introduced on

Consequently, , as it is a Cesàro mean. This enables us to conclude. Similarly, we obtain

Proof of theorem F.1.

Theorem F.1.

Assuming that to , and hold. Then,

,

where represents the step of the algorithm and with being the identity matrix in .

Proof.

Through a Taylor development of of rank 2, we get at point :

The lemma below enables us to conclude.

lemme F.12.

Let be an integrable function and let and ,

then,

Thus we get

i.e.

Hence abides by the same limit distribution as

, which is .∎

References

- Sklar, (1959) Sklar, M. Fonctions de répartition à dimensions et leurs marges. (French) Publ. Inst. Statist. Univ. Paris 8 1959 229–231.

- Joe, (1997) Joe, Harry Multivariate models and dependence concepts. Monographs on Statistics and Applied Probability, 73. Chapman & Hall, London, 1997. xviii+399 pp. ISBN: 0-412-07331-5 MR1462613 (98k:62011)

- Nelsen, (2006) Nelsen, Roger B. An introduction to Copulas. Second edition. Springer Series in Statistics. Springer, New York, 2006. xiv+269 pp. ISBN: 978-0387-28659-4; 0-387-28659-4 MR2197664.

- Carriere, (1994) Carriere, Jacques F. A large sample test for one-parameter families of Copulas. Comm. Statist. Theory Methods 23 (1994), no. 5, 1311–1317. (Reviewer: Paul Cabilio)

- Genest and Rémillard, (2004) Genest, Christian; Rémillard, Bruno. Tests of independence and randomness based on the empirical Copula process. Test 13 (2004), no. 2, 335–370.

- Fermanian, (2005) Fermanian, J-D. Goodness of fit tests for copulas. Journal of Multivariate Analysis (2005), 95, 119-152

- Genest Quessy and Rémillard, (2006) Genest, Quessy and Rémillard. Goodness-of-fit procedures for copula models based on the probability integral transformation. Scandinavian Journal of Statistics (2006), 33, 337-366

- Michiels and De Schepper, (2008) Michiels, Frederik; De Schepper, Ann. A Copula test space model—how to avoid the wrong Copula choice. Kybernetika (Prague) 44 (2008), no. 6, 864–878.

- Genest Favre Béliveau and Jacques, (2009) Genest, Favre, Béliveau and Jacques. Metaelliptical copulas and their use in frequency analysis of multivariate hydrological data. Water Resources Research (2009), 43, 12 pp.

- Mesfioui Quessy and Toupin, (2009) Mesfioui, Quessy and Toupin. On a new goodness-of-fit process for families of copulas. La Revue Canadienne de Statistique (2009), 37, 80-101

- Genest Rémillard and Beaudoin, 2009- (2) Genest, Rémillard and Beaudoin. Goodness-of-fit tests for copulas: A review and a power study. Insurance: Mathematics and Economics (2009), 44, 199-213

- Berg, (2009) Berg. Copula goodness-of-fit testing: an overview and power comparison. The European Journal of Finance (2009), 15, 675–701

- Bücher and Dette, (2010) Bücher, Axel and Dette, Holger. Some comments on goodness-of-fit tests for the parametric form of the copula based on -distances. J. Multivariate Anal. (2010) 101, no. 3, 749–763.

- Broniatowski, (2006) Broniatowski, M. and Leorato, S. An estimation method for the Neyman chi-square divergence with application to test of hypotheses. J. Multivariate Anal. (2006) 97, no. 6, 1409–1436.

- Friedman, (1984) Friedman , Jerome H.; Stuetzle, Werner; Schroeder, Anne. Projection pursuit density estimation. J. Amer. Statist. Assoc. 79 (1984), no. 387, 599–608.

- Huber, (1985) Huber Peter J. Projection pursuit, Ann. Statist. 13(2):435–525; 1985; With discussion.

- Cambanis, (1981) Cambanis, Stamatis; Huang, Steel; Simons, Gordon. On the theory of elliptically contoured distributions. J. Multivariate Anal. 11 (1981), no. 3, 368–385.

- Landsman, (2003) Landsman, Zinoviy M.; Valdez, Emiliano A. Tail conditional expectations for elliptical distributions. N. Am. Actuar. J. 7, (2003), no. 4, 55–71.

- Yohai, (2008) Yohai Victor J. Optimal robust estimates using the Kullback-Leibler divergence. Statistics and Probability Letters Volume 78; Issue 13; 15 September 2008, Pages 1811-1816.

- Toma, (2009) Toma Aida. Optimal robust M-estimators using divergences. Statistics and Probability Letters; Volume 79, Issue 1, 1 January 2009, Pages 1-5.

- Huber, (2004) Huber Peter J. Robust Statistics.Wiley 1981 (republished in paperback, 2004)

- Van der Vaart, (1998) Van der Vaart A. W. Asymptotic statistics; volume 3 of Cambridge Series in Statistical and Probabilistic Mathematics, Cambridge University Press, Cambridge, 1998.

- Scott, (1992) Scott, David W. Multivariate density estimation. Theory, practice, and visualization; Wiley Series in Probability and Mathematical Statistics: Applied Probability and Statistics. A Wiley-Interscience Publication. John Wiley and Sons, Inc., New York, 1992. xiv+317 pp. ISBN: 0-471-54770-0.

- Aurélien Alfonsi and Damiano Brigo, (2005) Aurélien Alfonsi and Damiano Brigo. New families of Copulas based on periodic functions. Communications in Statistics - Theory and Methods. Vol. 34, No. 7, (2005), pp. 1437-1447.

- Cressie-Read, (1984) Cressie, Noel; Read, Timothy R. C. Multinomial goodness-of-fit tests. J. Roy. Statist. Soc. Ser. B 46; (1984), no. 3, 440–464.

- Csiszár I., (1967) Csiszár, I. On topology properties of -divergences. Studia Sci. Math. Hungar. 2 1967 329–339.

- Friedrich and Igor, (1987) Liese Friedrich; Vajda Igor. Convex statistical distances; volume 95 of Teubner-Texte zur Mathematik [Teubner Texts in Mathematics]. BSB B. G. Teubner Verlagsgesellschaft, 1987, with German, French and Russian summaries.

- Pardo Leandro, (2006) Pardo Leandro. Statistical inference based on divergence measures; volume 185 of Statistics: Textbooks and Monographs. Chapman & Hall/CRC, Boca Raton, FL, 2006.

- Zografos K., (1990) Zografos, K.; Ferentinos, K.; Papaioannou, T. -divergence statistics: sampling properties and multinomial goodness of fit and divergence tests. Comm. Statist. Theory Methods 19(5):1785–1802(1990).

- Azé, (1997) Azé D.. Eléments d’analyse convexe et variationnelle; Ellipse; 1997.

- Bosq, (1999) Bosq D.; Lecoutre J.-P. Livre - Theorie De L’Estimation Fonctionnelle; Economica; 1999.

- Broniatowski, (2009) Broniatowski M.; Keziou A. Parametric estimation and tests through divergences and the duality technique. J. Multivariate Anal. 100 (2009), no. 1, 16–36.

- Black and Scholes, (1973) Black and Scholes. The pricing of options and corporate liabilities. Journal of Political Economy, 81:635-654, 1973.