Fractional Lévy-driven Ornstein–Uhlenbeck processes and stochastic differential equations

Abstract

Using Riemann–Stieltjes methods for integrators of bounded -variation we define a pathwise integral driven by a fractional Lévy process (FLP). To explicitly solve general fractional stochastic differential equations (SDEs) we introduce an Ornstein–Uhlenbeck model by a stochastic integral representation, where the driving stochastic process is an FLP. To achieve the convergence of improper integrals, the long-time behavior of FLPs is derived. This is sufficient to define the fractional Lévy–Ornstein–Uhlenbeck process (FLOUP) pathwise as an improper Riemann–Stieltjes integral. We show further that the FLOUP is the unique stationary solution of the corresponding Langevin equation. Furthermore, we calculate the autocovariance function and prove that its increments exhibit long-range dependence. Exploiting the Langevin equation, we consider SDEs driven by FLPs of bounded -variation for and construct solutions using the corresponding FLOUP. Finally, we consider examples of such SDEs, including various state space transforms of the FLOUP and also fractional Lévy-driven Cox–Ingersoll–Ross (CIR) models.

doi:

10.3150/10-BEJ281keywords:

and

1 Introduction

In this paper we consider (stationary) solutions to SDEs of the form

| (1) |

where is a fractional Lévy process (FLP) of bounded -variation for and and are appropriate coefficient functions. Applying pathwise Riemann–Stieltjes integration for functions of bounded -variation, we solve such equations by constructing explicit solutions. The basic model will be a fractional Lévy–Ornstein–Uhlenbeck process (FLOUP) introduced by the stochastic integral representation

We further show that this is the unique stationary pathwise solution of the corresponding Langevin equation

| (2) |

Using this relation we will consider SDEs of the form and impose assumptions on the coefficient functions and , under which solutions can be constructed by monotone transformation of .

Although our paper is purely theoretical, we are aiming at applications where positive solutions of (1) are of interest. An approach, developed in [1] for SDEs driven by FBM, can be modified to SDEs driven by FLPs. On the other hand, a squared FLOUP is positive and a solution to the SDE

We will discuss various examples with different state spaces and different and . We will also present some properties of the respective solutions, also concerning the stationary distribution.

Our paper is organized as follows. Section 2 considers FLPs and pathwise integration. Section 3 introduces the FLOUP as a pathwise improper Riemann–Stieltjes integral and shows that it is the unique stationary pathwise solution of the corresponding Langevin equation. Moreover, we calculate its autocovariance function and show that the increments of an FLOUP exhibit long-range dependence. Section 4 mainly extends Buchmann and Klüppelberg [1] from fractional Brownian motion to FLPs and states structural conditions for the coefficient functions and , which guarantee an existence (and uniqueness) theorem. Section 5 provides examples and simulations. The Appendix reviews the Riemann–Stieltjes analysis via -variation.

The following notation will be used throughout. We always assume a complete probability space . We denote the -measurable real functions by , the Hilbert space of square integrable random variables by , the vector space of continuous real functions on by and by the supremum norm. Furthermore, and are the spaces of real functions on , which are Lipschitz continuous on compacts and continuously differentiable, respectively. The spaces of integrable and square integrable real functions are denoted by and , respectively. When speaking of a two-sided Lévy process we mean the following: given two independent copies of the same Lévy process, and , we take

| (3) |

The Dirac measure in we denote by . Finally, for we set .

Integrals throughout this paper are considered in the Riemann–Stieltjes sense, if not stated otherwise.

2 Fractional Lévy processes and pathwise integration

Fractional Lévy processes (FLPs) were introduced as a natural generalization of the integral representation of fractional Brownian motion (FBM). We shortly review the main properties of FLPs, see [12], Section 3, for details and more background. For notational convenience we work with the fractional integration parameter instead of the Hurst index , where . Because we are only interested in long memory models, we restrict ourselves to . Furthermore, we only consider FLPs with existing second moments. Analogously to [11] for FBM we choose (like Marquardt [12]) the following definition.

Definition 2.1.

Let be a zero-mean two-sided Lévy process with and without a Brownian component. For we define

| (4) |

We call a fractional Lévy process (FLP) and the driving Lévy process of .

The integrals above exist in the -sense; see [12], Theorem 3.5, for details.

Recall that, by the Lévy–Itô decomposition, every Lévy process can be represented as the sum of a Brownian motion and an independent jump process. The Brownian motion gives rise to an FBM, which has been studied extensively; see, for instance, [13] for general background or [1] in the context of the present paper.

The next result ensures that there is, in fact, a modification of that equals a pathwise improper Riemann integral and gives first properties.

Proposition 2.2 (([12], Theorems 3.7, 4.1 and 4.4)).

Let be an FLP with . Then the following assertions hold:

-

[(iii)]

-

(i)

has a modification that equals the improper Riemann integral

(5) Furthermore, is continuous in .

-

(ii)

For we have

(6) -

(iii)

has stationary increments and is symmetric, i.e., .

From now on, we always work with the modification of Proposition 2.2(i).

Next we define integration with respect to FLPs. As has been shown in [12], Theorem 4.10, FLPs may not be semimartingales, and integration in the -sense has been developed in [12], Section 5. Theorem 4.4 in [12] also shows that FLPs are only Hölder continuous up to the fractional integration parameter and not to the Hurst index as in the case for FBM. Therefore, pathwise Riemann–Stieltjes integration by Hölder continuity does not make sense for SDEs. On the other hand, using an approach like Young [17] based on -variation of the sample paths, integration in a pathwise Riemann–Stieltjes sense can be defined; for details see the Appendix. This means we have a chain rule and a density formula provided the integrator is of bounded -variation for .

We recall the definition of -variation over a compact interval . Let . We define for the -variation of as

| (7) |

where the supremum is taken over all subdivisions of . If , then we say that is of bounded -variation on . We will further call an FLP of bounded -variation if it is a.s. of bounded -variation on compacts.

Let be an FLP of bounded -variation, and . For we define

| (8) |

Then we define for every stochastic process with sample paths a.s. and for with the integral

| (9) |

pathwise in the Riemann–Stieltjes sense.

As stated in the Appendix the integral in (9) always exists on finite intervals . We consider also improper integrals, where or . The existence of the tail integral has then to be justified.

For example, FLPs, where the driving Lévy process is of finite activity, are of bounded -variation for all cf. Theorem 2.25 of [12].

3 Fractional Lévy–Ornstein–Uhlenbeck processes

We introduce fractional Lévy–Ornstein–Uhlenbeck processes (FLOUPs) as improper Riemann–Stieltjes integrals and prove that they are stationary solutions of the Langevin equation (2). To show the existence of the improper Riemann–Stieltjes integral, we first need some knowledge about the long-time behaviour of FLPs. A similar result considering has been proven by Muneya Matsui (personal communication).

Theorem 3.1

Let be an FLP, . Then for all we have

| (10) |

Proof.

Without loss of generality we can assume that . By the law of the iterated logarithm (LIL) for Lévy processes (cf. [14], Proposition 48.9) we find a random variable and a constant such that a.s. for all

| (11) |

We can always make smaller and so we choose . For any such path we can assume that and estimate

Therefore, it suffices to show that a.s.

| (13) |

and

| (14) |

We start with (13). Using the LIL we get an upper bound of (3) as follows:

| (15) | |||

where we have used in the last line the change of variable . Now note that for large and

Combining with for we get an upper bound for by

| (16) | |||

By a binomial expansion we get and, therefore (writing for ),

| (17) | |||

which ensures the existence of the two integrals in .

Theorem 3.1 ensures the existence of the improper Riemann–Stieltjes integral.

Lemma 3.2

Let be an FLP, and . Then for

| (18) |

exists a.s. as a Riemann–Stieltjes integral and is equal to

| (19) |

Furthermore, the function defined by is continuous.

Proof.

From Theorem 3.1 we know that for all there is a null set such that for we have

| (20) |

and, hence, for all and , the integral exists as a Riemann–Stieltjes integral. For a compact interval this is clear. Now consider . It suffices to show that exists for . This follows from the inequality

for some constant , and the integral on the right-hand side exists for . Similarly,

| (21) |

Now it follows by Wheeden and Zygmund [16], Theorem 2.21, that also exists as a Riemann–Stieltjes integral and is equal to (19). Since is continuous in for all , the result is proven. ∎

Now we are ready to define the central object of this paper. Recall that all integrals are Riemann–Stieltjes integrals based on Lemma 3.2.

Definition 3.3.

Let be an FLP, and . Then

| (22) |

is called an FLOUP.

Before returning to the Langevin equation in connection with the FLOUP, we present some distributional properties of . With a little effort one can prove that is stationary, i.e., for all , , ,

| (23) |

For details see [5], Lemma 6.1.3.

Although we mainly concentrate on Riemann–Stieltjes integrals, there exist several results based on integrals in the -sense that we can use. Fractional integration can be considered as a transformation of classical Riemann–Liouville fractional integrals, which are defined for by

if the integrals exist for almost all . This is, for instance, the case if with . The following result is a Riemann–Stieltjes version of Theorem 3.5 of [12].

Proposition 3.4.

Let be an FLOUP driven by an FLP of bounded -variation, , and . Then its finite-dimensional distributions have a characteristic function

for and , where is the Lévy measure of . Furthermore, for every , the random variable is infinitely divisible with a characteristic triple given by , where

| (25) | |||||

| (26) |

Proof.

For simple functions, the Riemann–Stieltjes integral and the -integral agree a.s. (see [12], Proposition 5.2). Now approximate the function by simple functions. While a.s. and -convergence of the Riemann–Stieltjes sums imply both convergence in probability, the integrals are equal in probability and thus in distribution. Therefore the result follows as in Theorem 3.5 of [12]. ∎

We now turn to the second-order properties of an FLOUP. Cheridito, Kawaguchi and Maejima [2] present details concerning the long memory property of an OU process driven by FBM. Similarly, we shall show that the increments of the FLOUP exhibit long-range dependence. First, however, we need the following result (see also Proposition 4.4 of [9] and Proposition 5.7 of [12]).

Theorem 3.5

Let be an FLP of bounded -variation, , , and with for , such that and exist as Riemann–Stieltjes integrals. Then we have

| (27) | |||

Proof.

The proof follows again by using approximating simple functions and the fact that

| (28) |

for , which can be found in Gripenberg and Norros [6], page 404. ∎

Now we have everything together to derive the covariance structure of an FLOUP. The lengthy calculation works in a manner similar to that of Theorem 2.3 of [2]. The asymptotic is up to a multiplicative factor the same as in the FBM case.

Theorem 3.6

Let be an FLP, , and the corresponding FLOUP. Then for and for fixed we have as

Now it is clear that the increments of an FLOUP exhibit long-range dependence in the sense of a non-summability property of the autocovariance function.

We now return to the Langevin equation presented in (2).

Theorem 3.7

Let be an FLP, and . Then the unique stationary pathwise solution of (2) is given a.s. by the corresponding FLOUP

Proof.

From Lemma 3.2 we know that exists for all a.s. as a Riemann–Stieltjes integral. We fix and consider the pathwise SDE

| (29) |

where . Obviously, . By arguments similar to those in the proof of [2], Proposition A.1, we obtain

is the unique pathwise solution of (29) and, therefore, by (23) a stationary solution of (2).

On the other hand, let be a stationary solution of (2). We show that holds for almost all . Set and assume that . For fix with . Then we have for by (29)

where we supressed the chosen for simplicity. Since and we conclude that for . Therefore, on we have for . For a given we define -wise the random variable with for on . Hence,

Furthermore, we know that for . Choosing a sequence of real numbers with we get by continuity of

Putting everything together we arrive at

| (30) |

Hence, . However, we have now

where is independent of . Thus, and, by stationarity, for all . However, we also have for fixed

| (31) |

Hence, by stationary , but , which is a contradiction and, thus, we conclude that . ∎

The following Ornstein–Uhlenbeck operator will be used in the next section to obtain solutions to SDEs with different starting values. The operator here modifies the starting value of the FLOUP and the lemma shows that this modified process still solves the Langevin equation.

Definition 3.8.

Let be an FLP, , and the corresponding FLOUP. We define the Ornstein–Uhlenbeck operator by

| (32) | |||

It is immediate from this definition that a.s. for .

The next lemma shows that transformed by the Ornstein–Uhlenbeck operator still satisfies the Langevin equation; its proof follows directly by the definition.

Lemma 3.9

Let be an FLP, , and be the corresponding FLOUP. For a continuous process the identity holds for all if and only if

| (33) |

4 Solutions of fractional SDEs by state space transforms and proper triples

In this section we start with SDEs driven by FLPs. Using pathwise integration we must solve for almost all a deterministic integral equation. Consequently, we build on an extensive theory starting with the seminal work by Young [17]. We also recall that for Brownian motion the pathwise approach goes back to [4] and [15] leading to the Fisk–Stratonovich integral. Required is that is Lipschitz-continuous and with bounded first and second derivatives. Readable accounts on the history can be found in [8] and in Ikeda and [7].

Regularity assumptions of sample paths of the driving process like Hölder continuity or bounded -variation for have been considered by Lyons [10]. We shall work in the framework of -variation, however, to go beyond the work of Lyons, who proves only existence and uniqueness theorems under certain Lipschitz assumptions on the coefficient functions and gives no analytical form of the solution.

The approach by Zähle [19] is indeed comparable to ours, where explicit solutions can be given under differentiability and Lipschitz conditions on the coefficient functions. Most of her results can be applied to SDEs driven by an FLP of bounded -variation for . We believe that the contribution of our work is two-fold. First, our assumptions are easy to verify and, second, we are able to present analytic solutions to SDEs of the form

| (34) |

In this situation we cannot apply the results of [19], since the volatility coefficient does not match the required differentiability assumption. Lyons [10] provides us at least with an existence theorem, but gives no closed form solution.

Aiming at solutions to similar SDEs, driven however by FBM, Buchmann and Klüppelberg [1] presented a theory that can be modified to cover SDEs driven by FLPs. The idea is to present solutions to SDEs like, for instance, (34) as monotone transformations of the FLOUP. The question we shall answer is, given an SDE

| (35) |

for specific and , which monotone transformation of the FLOUP is a solution to (35)?

First we have to establish certain regularity conditions on the coefficients and .

Definition 4.1.

(i) A triple is called strongly proper if and only if it satisfies the following properties:

-

[(P1)]

-

(P1)

is an open interval, where and .

-

(P2)

There exists a strictly decreasing , absolutely continuous with respect to the Lebesgue measure such that on where are the zeros of , and

-

(P3)

There exists such that holds on Lebesgue-a.e.

-

(P4)

The inverse function is differentiable and .

(ii) We call the triple proper if only (P1)–(P3) are satisfied.

(iii) The interval is called the state space, the unique constant in (P3) is called the friction coefficient (FC) and the unique function , , is called the state space transform (SST) for .

Condition (P4) differs from the -proper assumption required in [1], because we work with -variation instead of Hölder continuity.

As pointed out in [1], is by (P2) strictly decreasing and a.e. differentiable on with . Condition (P3) implies that and have Lebesgue measure zero. Also we have that is non-negative and , where denotes the locally integrable functions on ; is dense and open in by (P1). Therefore, the equality extends to . It follows that and are uniquely determined by and .

As can be seen from Definition 4.1 our coefficient functions are only defined on the interval , which can be any interval in . To account for this situation we need to specify what will be understood to be a solution to an SDE.

Definition 4.2.

Let be an FLP of bounded -variation, and . Suppose that is a non-empty interval and . We refer to a stochastic process as a pathwise solution of the SDE

| (36) |

if for almost all sample paths the following conditions are satisfied: and the image of is a subset of such that for :

-

[(S1)]

-

(S1)

is a.s. Riemann–Stieltjes integrable with respect to on ;

-

(S2)

The following integral equation holds:

The space of all solutions of (36) is denoted by .

We consider now an SDE as given in . If we assume that the triple is strongly proper with SST and FC , we define the following operator

| (37) |

with Ornstein–Uhlenbeck operator as in Definition 3.3. We also remark that

| (38) |

Before we state our main results we state the following technical lemma, which will be needed in the proofs.

Lemma 4.3 ((Version of Lemma 3.2 [1]))

Let be a strongly proper triple with the corresponding SST . Then with derivative . Also with for all .

Next we state the existence theorem. Let denote all mappings from into .

Theorem 4.4

Let be an FLP of bounded -variation, and . If is strongly proper with SST and FC , then

Proof.

Because we consider pathwise solutions we can w.l.o.g. assume that a.s. for some . Now fix and and define

We show that . Obviously takes only values in . Since and is of bounded -variation, we know that . With the chain rule from Theorem A.2 we get for

| (39) |

since solves ,

| (40) |

The Riemann–Stieltjes integral is additive with respect to a sum of integrators, if the Riemann–Stieltjes integrals exist separately for each integrator. This is true in our case, because is of finite variation and is of bounded -variation. Since is continuous and also of bounded -variation, and imply for

Furthermore, is differentiable and is continuous as a function of and, thus, we get by the density formula for Riemann–Stieltjes integrals on compacts for

From Lemma 4.3 we obtain , hence . By Definition 4.1(P3) and the interpretation following this definition we find that . This yields

where we used in the last line the equality . Finally, we have . ∎

The following result ensures uniqueness under natural conditions.

Theorem 4.5

Let be an FLP of bounded -variation, and . Let also be strongly proper with SST and FC . Furthermore, assume that . Then

Proof.

From , we know by Lemma 4.3 that and for all . Let . From Definition 4.1 we know that a.s. and from we get by the chain rule from Theorem A.2 for

| (41) |

Since , we know that for

| (42) |

Now is of finite variation and by the density formula of Theorem A.3 the integral is of bounded -variation as a function of . By putting and together and using again Theorem A.3, we get for

since is proper, and hold for all . Thus,

Hence, is a solution of (33). Fixing we see by Lemma 3.9 that and, finally, . ∎

The next corollary covers the important case of a stationary solution.

Corollary 4.6.

Let be an FLP of bounded -variation, and and be the corresponding FLOUP. Furthermore, let be strongly proper with SST and FC . Set for . Then the following assertions hold:

-

[(ii)]

-

(i)

is a stationary pathwise solution of the SDE

(43) -

(ii)

If , then is the unique stationary pathwise solution of .

5 Examples of SDEs driven by FLPs

5.1 Examples by means of strongly proper triples

This section is dedicated to examples, which we illustrate by simulations. For those we consider as driving Lévy process a compensated Poisson process with intensity ; that is,

where is a Lévy process with drift and Lévy measure without Brownian component. Of course, we consider this process to be defined on the whole of using .

In a first step we simulate sample paths of and compute the corresponding FLP by a Riemann–Stieltjes approximation; that is, we approximate

From Theorem 2.55 of [12] we know that the quality of this approximation is

Furthermore, the Poisson-FLP is of finite variation by Theorem 2.25 of [12].

Now we use a version of the explicit Euler method for the SDE (2)

to compute sample paths of the FLOUP. We want to remark that all these computations are pathwise. Probability comes in only through the underlying paths of the driving Lévy processes.

Next we study some examples of solutions to the SDE (36) given by strongly proper triples. We will mainly draw from structural results of [1] taking into account that their -proper condition has to be replaced by our assumption (P4) in Definition 4.1.

For the rest of this section, let be an FLP of bounded -variation, and .

Example 5.1.

As a first example, we consider for parameters and an SDE of the form

We analyse this SDE by taking the volatility coefficient defined by for and as given. The question is now, what drift functions and intervals lead to strongly proper triples as defined in Definition 4.1? More precisely, we want to find elements in the set

Using Proposition 5.5 of [1] we see that only leads to a non-empty . We consider the cases , and separately.

Take first . For a triple to be proper we must have that with . This results in with state space and SST is affine, more precisely, for .

If , by Proposition 5.6 of [1], the state space can only be either or . For we get

and the state space transform is for . Simple calculation ensures that condition (P4) of Definition 4.1 is satisfied, and every element of leads to a strongly proper triple. An example of an SDE of this kind for can be found in (49). The case can be treated analogously.

Finally, we consider . Proposition 5.8 of [1] shows that the only possible state space is the whole real line and

Furthermore, the SST is given by

The derivative of can easily be calculated yielding that only leads to strongly proper triples. An example for such an SDE (with ) is a fractional Cox–Ingersoll–Ross-type model, which is investigated in detail in Section 5.2 (cf. the SDE in (46)).

Example 5.2.

We consider the following SDEs with affine drift.

that is, is defined by for . To find suitable volatility coefficients and state spaces, we consider the set

and, if there is a , we investigate

Proposition 5.1 of [1] implies that there exist with being proper if and only if . In this case it also follows that and . A FC leads again to an affine model, namely for some .

If we choose an FC for some , then by Proposition 5.3 of [1], every is of the form

for some . Setting for the SST takes the form

Calculating the derivative of we see that a possible proper triple is strongly proper if and only if . An example of such an SDE is for parameters and given by

| (44) |

Example 5.3.

Consider the SDE

| (45) |

This example provides a bounded state space model. Define the triple by , and where . It can be shown that this triple is in fact strongly proper with FC . More precisely, we have and, therefore,

is the unique stationary solution of the SDE (45).

5.2 Fractional Cox–Ingersoll–Ross models

Whenever positive phenomena are modeled – for instance, interest rates, volatilities or default rates in finance – the Cox–Ingersoll–Ross (CIR) [3] model is the most prominent model. It is the solution to

where denotes standard Brownian motion, and . General existence and uniqueness theorems of Brownian SDEs cannot be applied here, because the square root is clearly not Lipschitz continuous. However, Ikeda and Watanabe [7], page 221, showed that for any there exists a unique non-negative solution. We shall consider analogous SDEs driven by FLPs.

Within the framework of strongly proper triples, Examples 5.1 and 5.2 show that our theory only covers CIR models with mean reversion to . Consider for a solution to the pathwise SDE

| (46) |

Define , choose and take . Example 5.1 implies that is strongly proper with SST

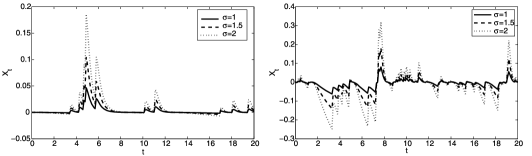

and, by Theorem 4.4, a stationary solution of is given by with , cf. Figure 1. Obviously, this CIR model takes also negative values.

A natural non-negative transformation of the FLOUP is given by for (cf. Figure 2), and, using the chain rule from Theorem A.2 and the existence of all appearing Riemann–Stieltjes integrals, we get

Defining now and we have as a solution to

However, the triple is not strongly proper, because assumption (P2) of Definition 4.1 is violated.

We can now formulate the following general result.

Proposition 5.4.

This result is not surprising, because Theorem 4.5 does not hold for the SDE (47). However, the reverse is not true: a solution of (47) does not necessarily solve (48), because it can be negative. Also the constant process, , , solves both (48) and (47).

Considering a squared Ornstein–Uhlenbeck process leads in the case of a driving Brownian motion to a CIR model with mean reversion to positive values. This approach does not work for pathwise integrals, neither in the FLP case nor for FBM, since the Itô term in the chain rule vanishes by finite -variation for some .

A positive process based on Theorem 4.4 is given as a solution to

| (49) |

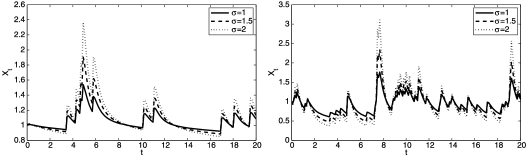

for , cf. Figure 3. Example 5.1 states that the triple for state space is strongly proper and the SST can be calculated as .

Appendix: Riemann–Stieltjes integration

As mentioned in the Introduction, all integrals in this paper are considered Riemann–Stieltjes integrals, if not stated otherwise. That is, for functions , we take the limit of

| (A.1) |

where is a partition and an intermediate partition of , that is,

while letting go to zero. Using the Banach–Steinhaus theorem, one can prove that if for a right-continuous and all continuous the Riemann–Stieltjes sums of (A.1) converge, is already of bounded variation. However, we can weaken this assumption on the integrator by restricting the space of possible integrands. Recall the definitions in (7) and (8). Exploiting the concept of -variation we now state an existence theorem for Riemann–Stieltjes integrals proven by Young [17].

Theorem A.1

Let be a compact interval, and for some with . Then exists in the Riemann–Stieltjes sense.

As in the classical Riemann–Stieltjes calculus, a chain rule can be proven; see [18], Theorem 3.1.

Theorem A.2 ((Chain rule))

Let be a compact interval and for some . Furthermore, let with . Then the Riemann–Stieltjes integral exists and we have

| (A.2) |

At last we state a density formula, which we have not found in the literature; for a proof we refer to [5], Theorem 4.3.2.

Theorem A.3 ((Density formula))

Let be a compact interval, and for some and with . For all we define . Then we have and

| (A.3) |

Acknowledgement

We thank Martina Zähle for interesting discussions and useful comments, which led to an improvement of our paper.

References

- [1] Buchmann, B. and Klüppelberg, C. (2006). Fractional integral equations and state space transforms. Bernoulli 12 431–456. MR2232725

- [2] Cheridito, P., Kawaguchi, H. and Maejima, M. (2003). Fractional Ornstein–Uhlenbeck processes. Electron. J. Probab. 8 1–14. MR1961165

- [3] Cox, J.C., Ingersoll, J.E. and Ross, S.A. (1985). A theory of term structure of interest rates. Econometrica 53 385–407. MR0785475

- [4] Doss, H. (1977). Liens entre équations différentielles stochastiques et ordinaires. Ann. Inst. Henri Poincaré 13 99–125. MR0451404

- [5] Fink, H. (2008). Fractional Lévy Ornstein–Uhlenbeck processes. Bachelor’s thesis, Technische Universität München.

- [6] Gripenberg, N. and Norros, I. (1996). On the prediction of fractional Brownian motion. J. Appl. Probab. 33 400–410. MR1385349

- [7] Ikeda, N. and Watanabe, S. (1989). Stochastic Differential Equations and Diffusion Processes, 2nd ed. Amsterdam: North-Holland. MR1011252

- [8] Karatzas, I. and Shreve, S.E. (1988). Brownian Motion and Stochastic Calculus. New York: Springer. MR0917065

- [9] Klüppelberg, C. and Matsui, M. (2010). Generalized fractional Lévy processes with fractional Brownian motion limit and applications to stochastic volatility. Available at http://www-m4.ma.tum.de/Papers/index.html. To appear.

- [10] Lyons, T. (1994). Differential equations driven by rough signals (I): An extension of an equality of L.C. Young. Math. Res. Lett. 1 451–464. MR1302388

- [11] Mandelbrot, B.B. and Hudson, R.L. (1968). Fractional Brownian motions, fractional noises and applications. SIAM Rev. 10 422–437. MR0242239

- [12] Marquardt, T. (2006). Fractional Lévy processes with an application to long memory moving average processes. Bernoulli 12 1009–1126. MR2274856

- [13] Samorodnitsky, G. and Taqqu, M. (1994). Stable Non-Gaussian Random Processes: Stochastic Models with Infinite Variance. New York: Chapman & Hall. MR1280932

- [14] Sato, K.-I. (2006). Additive processes and stochastic integrals. Illinois J. Math. 50 825–851. MR2247848

- [15] Sussman, H. (1978). On the gap between deterministic and stochastic ordinary differential equations. Ann. Probab. 6 19–41. MR0461664

- [16] Wheeden, R.L. and Zygmund, A. (1977). Measure and Integral. New York: Marcel Dekker. MR0492146

- [17] Young, L.C. (1936). An inequality of Hölder type, connected with Stieltjes integration. Acta Math 67 251–282. MR1555421

- [18] Zähle, M. (1998). Integration with respect to fractal functions and stochastic calculus I. Probab. Theory Related Fields 111 333–374. MR1640795

- [19] Zähle, M. (2001). Integration with respect to fractal functions and stochastic calculus II. Math. Nachr. 225 145–183. MR1827093