Sparsity considerations for dependent variables

Abstract

The aim of this paper is to provide a comprehensive introduction for the study of -penalized estimators in the context of dependent observations. We define a general -penalized estimator for solving problems of stochastic optimization. This estimator turns out to be the LASSO [30] in the regression estimation setting. Powerful theoretical guarantees on the statistical performances of the LASSO were provided in recent papers, however, they usually only deal with the iid case. Here, we study this estimator under various dependence assumptions.

doi:

10.1214/11-EJS626keywords:

[class=AMS]keywords:

and

t1Research partially supported by the French “Agence Nationale pour la Recherche” under grant ANR-09-BLAN-0128 “PARCIMONIE”.

t2The authors would like to thank the anonymous reviewers for their valuable comments and suggestions to improve the quality of the paper.

1 Introduction

1.1 Sparsity in high dimensional estimation problems

In the last few years, statistical problems in large dimension received a lot of attention. That is, estimation problems where the dimension of the parameter to be estimated, say , is larger than the size of the sample, usually denoted by . This setting is motivated by modern applications such as genomics, where we often have the number of patients with a very rare desease, and of the order of or even (CGH arrays), see for example [25] and the references therein. Other examples appear in econometrics, we refer the reader to Belloni and Chernozhukov [3, 4].

Probably the most famous example is high dimensional regression estimation: one observes pairs for with , and one wants to find a such that for a new pair , would be a good prediction for . If , it is well known that a good estimation cannot be performed unless we make an additional assumption. Very often, it is quite natural to assume that there exists such a that is sparse: most of its coordinates are equal to . If we let denote the number of non-zero coordinates in , this means that . In the genomics example, it means that only a few genes are relevant to explain the desease. Early examples of estimators introduced to deal with this kind of problems include the now famous AIC [1] and BIC [29]. Both can be written

| (1.1) |

where differs in AIC and BIC. Despite AIC and BIC may give poor results when (see [7]), taking leads to estimators with very satisfying statistical properties ( being the variance of the noise). See for example [7, 9] for such results, and [5] in the case of unknown variance.

The main problem with this so-called penalization approach is that the effective computation of the estimators defined in (1.1) is very time consuming. In practice, these estimators cannot be used for more than a few tens. This motivated the study of the LASSO introduced by Tibshirani [30]. This estimator is defined by

The convexity of this minimization problem ensures that the estimator can be computed for very large , see Efron et al. [19] for example. This motivated a lot of theoretical studies on the statistical performances of this estimator. The results with the weakest hypothesis can be found in the work of Bickel et al. [8] or Koltchinksii [23]. See also very nice reviews in the paper by Van de Geer and Bühlmann [31] or in the PhD Thesis of Hebiri [21]. Also note that a quantity of variants of the idea of -penalization were studied simultaneously to the LASSO: among others the basis pursuit [13, 12], the Dantzig Selector [14], the Elastic Net [33]…

Another problem of estimation in high dimension is the so-called problem of sparse density estimation. In this setting, we observe random variables with (unknown) density and the purpose is to estimate as a linear combination of some functions , …, . If and

we can use the SPADES (for SPArse Density Estimator) by Bunea et al. [11, 10] or the iterative feature selection procedure in [2].

One of the common features of all the theoretical studies of sparse estimators is that they focus only on the case where the observations are independent. For example, for the density estimation case, in [10] and [2] the observations are assumed to be iid. The purpose of this paper is to propose a unified framework. Namely, we define a general stochastic optimization problem that contains as a special case regression and density estimation. We then define a general -penalized estimator for this problem, in the special case of regression estimation this estimator is actually the LASSO and in the case of density estimation it is SPADES. Finally, we provide guarantees on the statistical performances of this estimator in the spirit of [8], but we do not only consider independent observations: we want to study the case of dependent observations, and prove that we can still recover the target in this case, under various hypothesis.

1.2 General setting and -penalized estimator

We now give the general setting and notations of our paper. Note that the cases of regression and density estimation will appear as particular cases.

We observe random variables in . Let be the distribution of . We have a function such that for any , is a quadratic function. The objective is the estimation of a value that minimizes the following expression which only depends on and :

All the results that will follow are intended to be interesting in the case on the condition that is small.

We use the following estimator:

and denotes any solution of this minimization problem.

We now detail the notations in the two examples of interest:

-

1.

in the regression example, with the deterministic, and

(1.2) where (the are not necessarily iid, they may be dependent and have different distribution). Here we take . In this example, is known as the LASSO estimator [30].

-

2.

in the density estimation case, have the same density wrt Lebesgue measure (but they are not necessarily independent). We have a family of functions and we want to estimate the density of by functions of the form

In this case we take

and note that this leads to

Then is the estimator known as SPADES [10].

1.3 Overview of the paper

In Section 2 we provide a sparsity inequality that extend the one of Bickel et al. [8] to the case of non iid variables. This result involves two assumptions: the first one is about the function and is already needed in the iid case. It is usually refered as Restricted Eigenvalue Property. The other hypothesis is more involved, it is specific to the non iid case. It roughly says that we are able to control the deviations of empirical means of dependent variables around their expectations.

In Section 3, we provide several examples of classical assumptions on the observations that can ensure that we have such a control. These assumptions are expressed in terms of weak dependence coefficients, so in the beginning of this section we briefly introduce weak dependence. We also provide some references.

We apply the results of Sections 2 and 3 to regression estimation in Section 4 and to density estimation in Section 5.

Finally the proofs are given in Section 7.

2 Main result

2.1 Assumptions and result

First, we need an assumption on the quadratic form .

Assumption with . As is a quadratic form, we have the matrix

that does not depend on , and we assume that the matrix has only on its diagonal (actually, this just means that we renormalize the observations in the regression case, or the function in the density estimation case), that it is non-random (here again, this is easily checked in the two examples) and that it satisfies

Note that this condition, usually referred as restricted eigenvalue property (REP), is already required in the iid setting, see [8, 31] for example. In these paper it is also discussed why we cannot hope to get rid of this hypothesis.

We set for simplicity

Recall that as is a quadratic function it may be written as for a -matrix valued function on and a vector function so that

Theorem 2.1.

Let us assume that Assumption is satisfied. Let us assume that the distribution of is such that there is a constant and a decreasing continuous function with

| (2.1) |

Let us put

Then

The arguments of the proof of Theorem 2.1 are taken from [8]. The proof is given in Section 7, page 7.

Note that the hypothesis in this theorem heavily depend on the distribution of the variables , …, , and particulary on their type of dependence. Section 3 will provide some examples of situations where this hypothesis is satisfied.

Also note that the upper bound in the inequality is minimized if we make the choice . Then

It is important to remark that the choice may be impossible in practice, as the practitionner may not know and . Moreover, this choice is not necessarily the best one in practice: in the regression case with iid noise , we will see that this choice leads to . This choice requires the knowledge of . Moreover it is not usually the best choice in practice, see for example the simulations in [21]. Even in the iid case, the choice of a good in practice is still an open problem. However, note that

-

1.

the question is in some sense meaningless. For example the value of that minimizes the quadratic risk is not the same than the value of that may ensure, under some supplementary hypothesis, that identifies correctly the non-zero coordinates in , see for example Leeb and Pötscher [24] on that topic. One has to be careful to what one means when one say a good choice for .

-

2.

some popular methods like cross-validation seem to give good results for the quadratic risk, at least in the iid case. An interesting open question is to know if one can prove theoretical results for cross validation in this setting. See also the bootstrap method proposed in [4].

- 3.

2.2 Remarks on the density and regression estimation setting

First, note that in the regression setting (Equation 1.2), for any and we have

Then, in the density estimation context,

So, in both cases, the assumption given by Equation 2.1 is satisfied if we have a control of the deviation of empirical means to their expectation. In the next sections, we discuss some conditions to obtain such controls with dependent variables.

3 Models fitting conditions of Theorem 2.1

In this section, we give some results that allow to control the deviation of empirical means to their expectations for general (non iid) obsrevations. The idea will be, in the next sections, to apply these results to the processes for . For the sake of simplicity, in this section, we deal with a generic process and the applications are given in the next sections. Various examples of pairs are given. We will use the classical notation

3.1 Weak dependence ()

We are going to introduce some coefficients in order to control the dependence of the . The first example of such coefficients are the -mixing coefficients first introduced by Rosenblatt [27],

The idea is that the faster decreases to , the less dependent are and for large . Assumptions on the rate of decay allows to prove laws of large numbers and central limit theorems. Different mixing coefficients were then studied, we refer the reader to [18, 26] for more details.

The main problem with mixing coefficients is that they exclude too many processes. It is easy to build a process satisfying a central limit theorem with constant , see [15] Chapter 1 for an example. This motivated the introduction of weak dependence coefficients. The monograph [15] provides a comprehensive introduction to the various weak dependence coefficients. Our purpose here is not to define all these coefficients, but rather to introduce some examples that allow to satisfy condition (2.1) in Theorem 2.1.

Definition 3.1.

We put, for any process ,

| (3.3) |

We precise in §-3.1.1 and in §-3.1.2 that suitable decays of those coefficients yield (2.1). Those two sections will provide quite different forms of the function .

Definition 3.2.

Let us assume that for any , for any and respectively and -Lipschitz, where eg.,

We also assume that for any with ,

with . Then is said to be -dependent with -dependence coefficients .

Remark 3.1.

Other functions allow to define the , and -dependence, see [15].

We finally provide some basic properties, proved in [15]. The following result allows a comparison between different type of coefficients.

Proposition 3.1.

If then

Finally the following property will be useful in this paper.

Proposition 3.2.

If is -dependent and is -Lipschitz and bounded, then is also -dependent with

3.1.1 Moment inequalities

In Doukhan and Louhichi [16] it is proved that if for an even integer we have

| (3.5) |

then Marcinkiewicz-Zygmund inequality follows:

and thus and is of the order of in (2.1). However, explicit constants are needed in Theorem 2.1. We actually have the following result.

Proposition 3.3.

Remark 3.2.

3.1.2 Exponential inequalities

Using the previous inequality, Doukhan and Louhichi [16] proved exponential inequalities that would lead to in . Doukhan and Neumann [17] use alternative cumulant techniques to get in for suitable bounds of the previous covariances (3.3).

Theorem 3.1.

[17] Let us assume that . Let be one of the following functions:

-

(a)

,

-

(b)

,

-

(c)

,

-

(d)

, for some .

We assume that there exist constants , , and a nonincreasing sequence of real coefficients such that, for all -tuples and all -tuples with the following inequality is fulfilled:

| (3.6) |

where

Then

where can be chosen as any number greater than or equal to and

Remark 3.3.

This result yields convienient bounds for the function . A recent paper by Olivier Wintenberger [32] is also of interest: it directly yields alternative results from our main result. In this paper, we do not intend to provide the reader with encyclopedic references but mainly to precise some ideas and techniques so that this will be developed in further papers.

3.2 Long range dependence )

3.2.1 Power decays

Assume now that is a centered series satisfies then may occur, eg. if

for then ; then holds.

3.2.2 Gaussian case

In the special case of Gaussian processes , tails of are classically described because and here . We thus may obtain simultaneously subGaussian tails and .

3.2.3 Non subGaussian tails

Assume that that for each , and is a stationary Gaussian processes with, for some , ,

| (3.7) |

Let for a function with Hermite rank , and since

their covariance series is non -th summable in case .

The case and is investigated by using the following expansion in the seminal work by Rosenblatt [28].

Set for the covariance matrix of the Gaussian random vector :

Quoting that

with

( is given by Equation (3.7)), this is thus clear that for small enough ,

Here the conditions in the main theorem hold with and for any .

4 Application to regression estimation

In this section we apply Theorem 2.1 and the various examples of Section 3 to obtain results for regression estimation. Note that the results in the iid setting are already known, they are only given here for the sake of completeness, in order to provide comparison with the other cases.

Let us remind that in the regression case, we want to apply the results of Section 3 to

For the sake of simplicity, in this whole session dedicated to regression, let us put

4.1 Regression in the iid case

Under the usual assumption that the are iid and subGaussian,

for some known , then we have

So we can apply Theorem 2.1 in order to obtain the following well known result:

4.2 Regression estimation in the dependent case

4.2.1 Marcinkiewicz-Zygmund type inequalities

Let us remark that, for any ,

Thus, we apply Theorem 2.1 and Proposition 3.3 to obtain the following result.

Corollary 4.2.

In the context of Equation 1.2, under Assumption , if the satisfy, for some even integer ,

the choice

leads to

Remark 4.1.

This result aims at filling a gap for non subGaussian and non iid random variables.

The result still allows to deal with the sparse case in case . In this case we deal with the case and we get a rate of convergence in probability .

If and the least squares methods apply which make such sparsity algorithms less relevant.

Moreover if the present method is definitely not efficient. Hence in the case of heavy tails, such as considered in the paper by Bartkiewicz et al. [6], our results are useless. Anyway, using least squares for heavy tailed models (without second order moments) does not look to be a good idea!

4.2.2 Exponential inequalities

Corollary 4.3.

Let us assume that the satisfy the hypothesis of Theorem 3.1: let be one of the functions of Theorem 3.1, we assume that there are constants , , and a nonincreasing sequence of real coefficients such that, for all -tuples and all -tuples with the following inequality is fulfilled:

where

Let be a positive constant and let us put

Let us assume that , and are such that

then for

we have

So the rate is the same than in the iid case. The only difference is in the constant, and a restriction for very large values of .

Proof.

For the sake of shorteness, let us put

and note that . First, note that for any ,

if we put and . Using Theorem 3.1, we obtain for any ,

where and

in other words:

Now, let us put , we obtain

Remark that we cannot in general compute explicitely the inverse of this function but we can upper-bound the range for :

In this case,

and so

So we can take, following Theorem 2.1,

as soon as . For example, for a fixed number of observations and a fixed confidence level , we have the restriction:

Under this condition we have, by Theorem 2.1,

this ends the proof. ∎

4.3 Simulations

In order to illustrate the results, we propose a very short simulation study. The purpose of this study is not to show the good performances of the estimator in practice or to give recipes for the choice of . The aim is more to show that the performances of the iid setting are likely to be obtained in the dependent setting if the dependence coefficients are small.

We use the following model:

where the ’s will be treated as fixed design, but in practice will be iid vectors in with , with distribution where is given by .

The parameter is given by . This is the toy example used by Tibshirani [30]. Let .

The noise satisfies , for , where the are iid and . Note that this ensure that for any , so the noise level does not depent on . In the experiments,

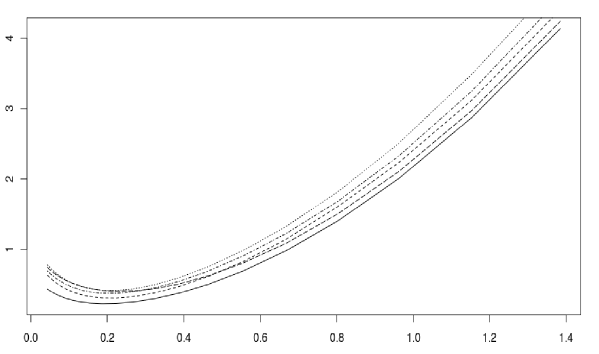

We fixed a grid of values and we computed, for every experiment, the LASSO estimator with for all . We have repeated the experiment times for every value of and report the results in Figure 1.

We can remark that all the curves are very similar. The minimum reconstruction error is obtained for , that corresponds to . Note that in the iid case, it is smaller than the theoretical value given by Theorem 2.1, for , that would correspond to , a value that would not event stand in the figure!

5 Application to density estimation

Here we apply Theorem 2.1 and Section 3 to the context of density estimation. Let us remind that in this setting,

5.1 Density estimation in the iid case

If the are iid with density and if for any then we can apply Hoeffding inequality [22] to upper bound

We obtain

So we can apply Theorem 2.1.

Corollary 5.1.

In the context of density estimation, under Assumption , if the are iid with density and if for any , the choice leads to

This result is essentially known, see [11].

5.2 Density estimation in the dependent case

Note that if as previously we work with bounded , we automatically have moments of any order. So we will only state a result based on exponential inequality.

Corollary 5.2.

Let us assume that there are and such that is -Lipschitz and for any . Let us assume that , …, satisfy

for some . Let us put a , define

and assume that , and the confidence level are such that

Then

| (5.1) |

Remark 5.1.

The assumption that the are all -Lipschitz for a constant excludes a lot of interesting dictionaries. If we assume that the are -Lipschitz (this would be the case if we used the first functions in the Fourier basis for example), then we will suffer a loss in (5.1) when compared to the iid case. However, note that Equation (5.2) below is the starting point of our proof, so we cannot hope to find a simple way to remove this hypothesis when using -weak dependence. This will be the object of a future work.

Proof.

6 Conclusion

In this paper, we showed how the LASSO and other -penalized methods can be extended to the case of dependent random variables.

An open and ambitious question to be adressed later is to find a good data-driven way to calibrate the regularization parameter when we don’t know in advance the dependence coefficients of our observations.

Anyway this first step with sparsity in the dependent setting is done for accurate applications and our brief simulations let us think that such techniques are reasonable for time series.

Here again extensions to random fields or to dependent point processes seem plausible.

7 Proofs

Proof of Theorem 2.1.

By definition,

and so

| (7.1) |

Now, as is quadratic wrt we have, for any ,

| (7.2) |

Moreover, as is the minimizer of , we have the relation

| (7.3) |

Pluging (7.2) and (7.3) into (7.1) leads to

and then

| (7.4) |

Now, we remind that we have the hypothesis

that becomes, with a simple union bound argument,

and so, if we put ,

Also remark that . So until the end of the proof, we will work on the event

true with probability at least . Going back to (7.4), we have

and then

that leads to the following inequality that will play a central role in the end of the proof:

| (7.5) |

First, if we remind that , (7.5) leads to

and so

So we can take in Assumption . So, (7.5) leads to

| (7.6) | ||||

| (7.7) |

We conclude that

Now remark that (7.6) to (7.7) states that a convex quadratic function of is negative, so both roots of that quadratic are real. This leads to

This ends the proof. ∎

Proof of Proposition 3.3.

First

The same combinatorial arguments as in [16] yield for

| (7.8) | |||||

| (7.9) |

Let us now assume the condition (3.5) then

A rough bound is thus and we thus derive

| (7.10) |

Now using precisely condition (3.5) with the relation (7.8) we see that if , and then the sequence recursively defined as

| (7.11) |

satisfies Remember that

hence as in [16] we quote that

is less that the -th Catalan number, and this ends the proof. ∎

References

- Aka [73] H. Akaike. Information theory and an extension of the maximum likelihood principle. In B. N. Petrov and F. Csaki, editors, 2nd International Symposium on Information Theory, pages 267–281. Budapest: Akademia Kiado, 1973.

- Alq [08] P. Alquier. Density estimation with quadratic loss, a confidence intervals method. ESAIM: P&S, 12:438–463, 2008. \MR2437718

- [3] A. Belloni and V. Chernozhukov. -penalized quantile regression in high-dimensional sparse models. Annals of Statistics, 32(11):2011–2055, 2011.

- [4] A. Belloni and V. Chernozhukov. High dimensional sparse econometric models: An introduction. In P. Alquier, E. Gautier, and G. Stoltz, editors, Inverse Problems and High-Dimensional Estimation. Springer Lecture Notes in Statistics, 2011.

- BGH [09] Y. Baraud, C. Giraud, and S. Huet. Gaussian model selection with an unknown variance. Annals of Statistics, 37(2):630–672, 2009. \MR2502646

- BJMW [10] K. Bartkiewicz, A. Jakubowskin, T. Mikosch, and O. Wintenberger. Infinite variances stable limits for sums of dependent random variables. Probability Theory and Related Fields, 2010.

- BM [01] L. Birgé and P. Massart. Gaussian model selection. Journal of the European Mathematical Society, 3(3):203–268, 2001. \MR1848946

- BRT [09] P. J. Bickel, Y. Ritov, and A. Tsybakov. Simultaneous analysis of lasso and Dantzig selector. Annals of Statistics, 37(4):1705–1732, 2009. \MR2533469

- BTW [07] F. Bunea, A.B. Tsybakov, and M.H. Wegkamp. Aggregation for Gaussian regression. Annals of Statistics, 35:1674–1697, 2007. \MR2351101

- BTWB [10] F. Bunea, A. Tsybakov, M. Wegkamp, and A. Barbu. SPADES and mixture models. Annals of Statistics, 38(4):2525–2558, 2010. \MR2676897

- BWT [07] F. Bunea, M. Wegkamp, and A. Tsybakov. Sparse density estimation with penalties. Proceedings of 20th Annual Conference on Learning Theory (COLT 2007) - Springer, pages 530–543, 2007. \MR2397610

- CDS [01] S. S. Chen, D. L. Donoho, and M. A. Saunders. Atomic decomposition by basis pursuit. SIAM Review, 43(1):129–159, 2001. \MR1639094

- Che [95] S. S. Chen. Basis pursuit, 1995. PhD Thesis, Stanford University.

- CT [07] E. Candes and T. Tao. The Dantzig selector: statistical estimation when is much larger than . Annals of Statistics, 35, 2007. \MR2382644

- DDL+ [07] J. Dedecker, P. Doukhan, G. Lang, J. R. León R., S. Louhichi, and C. Prieur. Weak dependence: with examples and applications, volume 190 of Lecture Notes in Statistics. Springer, New York, 2007. \MR2338725

- DL [99] P. Doukhan and S. Louhichi. A new weak dependence condition and applications to moment inequalities. Stochastic Processes and their Applications, 84(2):313–342, 1999. \MR1719345

- DN [07] P. Doukhan and M. H. Neumann. Probability and moment inequalities for sums of weakly dependent random variables, with applications. Stochastic Processes and their Applications, 117(7):878–903, 2007. \MR2330724

- Dou [94] P. Doukhan. Mixing, volume 85 of Lecture Notes in Statistics. Springer-Verlag, New York, 1994. Properties and examples. \MR1312160

- EHJT [04] B. Efron, T. Hastie, I. Johnstone, and R. Tibshirani. Least angle regression. Annals of Statistics, 32(2):407–499, 2004. \MR2060166

- FHHT [07] J. Friedman, T. Hastie, H. Höfling, and R. Tibshirani. Pathwise coordinate optimization. Annals of Applied Statist., 1(2):302–332, 2007. \MR2415737

- Heb [09] M. Hebiri. Quelques questions de selection de variables autour de l’estimateur lasso, 2009. PhD Thesis, Université Paris 7 (in english).

- Hoe [63] W. Hoeffding. Probability inequalities for sums of bounded random variables. Journal of the American Statistical Association, 58:13–30, 1963. \MR0144363

- [23] V. Koltchinskii. Sparsity in empirical risk minimization. Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, 45(1):7–57, 2009. \MR2500227

- LP [05] H. Leeb and B. M. Pötscher. Sparse estimators and the oracle property, or the return of hodges’ estimator. Cowles Foundation Discussion Papers 1500, Cowles Foundation, Yale University, 2005.

- RBV [08] F. Rapaport, E. Barillot, and J.-P. Vert. Classification of array-CGH data using fused SVM. Bioinformatics, 24(13):1375,1382, 2008.

- Rio [00] E. Rio. Théorie asymptotique pour des processus aléatoire faiblement dépendants. SMAI, Mathématiques et Applications 31, Springer, 2000. \MR2117923

- Ros [56] M. Rosenblatt. A central limit theorem and a strong mixing condition. Proc. Nat. Ac. Sc. U.S.A., 42:43–47, 1956. \MR0074711

- Ros [61] M. Rosenblatt. Independence and dependence. Proceeding 4th. Berkeley Symp. Math. Stat. Prob. Berkeley University Press, pages 411–443, 1961. \MR0133863

- Sch [78] G. Schwarz. Estimating the dimension of a model. Annals of Statistics, 6:461–464, 1978. \MR0468014

- Tib [96] R. Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society B, 58(1):267–288, 1996. \MR1379242

- vdGB [09] S. A. van de Geer and P. Bühlmann. On the conditions used to prove oracle results for the lasso. Electronic Journal of Statistics, 3:1360–1392, 2009. \MR2576316

- Win [10] O. Wintenberger. Deviation inequalities for sums of weakly dependent time series. Electronic Communications in Probability, 15:489–503, 2010. \MR2733373

- ZH [05] H. Zou and T. Hastie. Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society B, 67(2):301–320, 2005. \MR2137327