Limit order books

Abstract

Limit order books (LOBs) match buyers and sellers in more than half of the world’s financial markets. This survey highlights the insights that have emerged from the wealth of empirical and theoretical studies of LOBs. We examine the findings reported by statistical analyses of historical LOB data and discuss how several LOB models provide insight into certain aspects of the mechanism. We also illustrate that many such models poorly resemble real LOBs and that several well-established empirical facts have yet to be reproduced satisfactorily. Finally, we identify several key unresolved questions about LOBs.

I Introduction

More than half of the markets in today’s highly competitive and relentlessly fast-paced financial world now use a limit order book (LOB) mechanism to facilitate trade (Roşu, 2009). The Helsinki, Hong Kong, Shenzhen, Swiss, Tokyo, Toronto, and Vancouver Stock Exchanges, together with Euronext and the Australian Securities Exchange, all now operate as pure LOBs (Luckock, 2001; Gu et al., 2008b); the New York Stock Exchange (NYSE), NASDAQ, and the London Stock Exchange (LSE) (Cont et al., 2010) all operate a bespoke hybrid LOB system. Thanks to technological advances, traders worldwide have real-time access to the current LOB, providing buyers and sellers alike “the ultimate microscopic level of description” (Bouchaud et al., 2002).

In an LOB, complicated global phenomena emerge as a result of the local interactions between many heterogeneous agents when the system throughput becomes sufficiently large. This makes an LOB an example of a complex system (Mitchell, 2009). The unusually rich, detailed, and high-quality historic data from LOBs provides a suitable testing ground for theories about well-established statistical regularities common to a wide range of markets (Bouchaud et al., 2009; Cont, 2001; Farmer and Lillo, 2004), as well as for popular ideas in the complex systems literature such as universality, scaling, and emergence.

The many practical advantages to understanding LOB dynamics include: gaining clearer insight into how best to act in given market situations (Harris and Hasbrouck, 1996); optimal order execution strategies (Obizhaeva and Wang, 2013); market impact minimization (Eisler et al., 2012); designing better electronic trading algorithms (Engle et al., 2006); and assessing market stability (Kirilenko et al., 2011). In this survey, we discuss some of the key ideas that have emerged from the analysis and modelling of LOBs in recent years, and we highlight the strengths and limitations of existing LOB models.

Investigations of LOBs have taken a variety of starting points, drawing on ideas from economics, physics, mathematics, statistics, and psychology. Unsurprisingly, there is no clear consensus on the best approach. This point is exemplified by the contrast between the approach normally taken in the economics literature, in which models focus on the behaviour of individual traders and present LOBs as sequential games (Foucault, 1999; Parlour, 1998; Roşu, 2009), with the approach normally taken in the physics literature, in which order flows are treated as random and techniques from statistical mechanics are used to explore the resulting dynamics (Challet and Stinchcombe, 2001; Cont et al., 2010; Smith et al., 2003). In the present paper, we discuss developments in both the economics and physics literatures, and we emphasize aspects of LOBs that are most relevant to practitioners.

Several other survey articles focus on particular aspects of LOBs. Friedman (2005) reviewed early studies of double auction style trading, of which LOBs are an example. Parlour and Seppi (2008) addressed the economic and theoretical aspects of LOB trading. Bouchaud et al. (2009) assessed the current understanding of price formation in LOBs. Chakraborti et al. (2011b, a) examined the role of econophysics in understanding LOB behaviour. In the present survey we note the similarities and differences between several empirical studies of historical LOB data, discuss LOB models from both the physics and economics literatures, highlight several modelling assumptions that are not well-supported by the empirical findings, and identify several key unresolved questions.

The remainder of the survey is organized as follows. In Section II, we give formal definitions related to LOBs and formulate a mathematically precise description of LOB trading. In Section III, we discuss some practical aspects of trading via LOBs and examine the difficulties that arise in quantifying them. In Section IV, we examine the important role of empirical studies of LOBs, highlighting both consensus and disagreement within the literature. We examine a selection of models in Section V. In Section VI, we discuss key unresolved problems, and we conclude in Section VII.

II A Mathematical Description of an LOB

In this section, we formulate a precise description of trading that is common to most LOB markets. Of course, some individual exchanges and trading platforms operate slight variations of these core principles. Harris (2003) provides a comprehensive review of specific details governing particular exchanges, so we do not reproduce them here.

II.1 Preliminaries

Before LOBs grew in popularity, most financial trades took place in quote-driven marketplaces, in which a handful of large market makers centralize buy and sell orders by publishing the prices at which they are willing to buy and sell the traded asset. The market makers set their sell price higher than their buy price in order to earn a profit in exchange for providing liquidity111Liquidity is difficult to define formally. Kyle (1985) identified the three key properties of a liquid market to be tightness (“the cost of turning around a position over a short period of time”), depth (“the size of an order-flow innovation required to change prices a given amount”), and resiliency (“the speed with which prices recover from a random, uninformative shock”). to the market, for taking on the risk of acquiring an undesirable inventory position, and for being exposed to possible adverse selection (i.e., encountering other traders who have better information about the value of the asset and who can therefore make a profit by buying or selling, often repeatedly, with the market maker (Parlour and Seppi, 2008)). The only prices available to other traders who want to buy or sell the asset are those made public by the market makers, and the only action available to such traders is to immediately buy or sell at one of the market makers’ prices. Ticket touts exemplify a quote-driven market in action.

An LOB is much more flexible because every trader has the option of posting buy (respectively, sell) orders.

Definition.

An order submitted at time with price and size (respectively, ) is a commitment to sell (respectively, buy) up to units of the traded asset at a price no less than (respectively, no greater than) .

We introduce the vector notation because it allows explicit calculation of the priority (see Section III.4) of any order at any time.

For a given LOB, the units of order size and price are set as follows.

Definition.

The lot size of an LOB is the smallest amount of the asset that can be traded within it. All orders222In some markets, there are two lot-size parameters: a minimum size and an increment . In such markets, all orders must arrive with a size . For simplicity, we assume . must arrive with a size .

Definition.

The tick size of an LOB is the smallest permissible price interval between different orders within it. All orders must arrive with a price that is specified to the accuracy of .

For example, if , then the largest permissible order price that is strictly less than is , and all orders must be submitted at a price with exactly 5 decimal places.

Definition.

The lot size and tick size of an LOB are collectively called its resolution parameters.

When a buy (respectively, sell) order is submitted, an LOB’s trade-matching algorithm checks whether it is possible to match to some other previously submitted sell (respectively, buy) order. If so, the matching occurs immediately. If not, becomes active, and it remains active until either it becomes matched to another incoming sell (respectively, buy) order or it is cancelled. Cancellation usually occurs because the owner of an order no longer wishes to offer a trade at the stated price, but rules governing a market can also lead to the cancellation of active orders. For example, on the electronic trading platform Hotspot FX, all active orders are cancelled at 5pm EST each day to prevent an overly large accumulation of active orders over time (Gould et al., 2013b; Knight-Hotspot, 2013).

It is precisely the active orders in a market that make up an LOB:

Definition.

An LOB is the set of all active orders in a market at time .

The evolution of an LOB is a càdlàg process, i.e., for a limit order that becomes active upon arrival it holds that . The active orders in an LOB can be partitioned into the set of active buy orders , for which , and the set of active sell orders , for which . An LOB can then be considered as a set of queues, each of which consists of active buy or sell orders at a specified price.

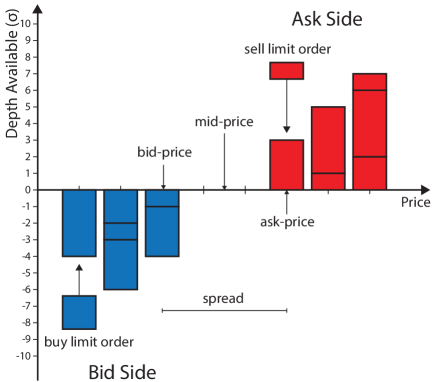

The terms bid price, ask price, mid price, and bid-ask spread are common to much of the finance literature and can be made specific in the context of an LOB:

Definition.

The bid price at time is the highest stated price among active buy orders at time ,

| (1) |

The ask price at time is the lowest stated price among active sell orders at time ,

| (2) |

Definition.

The bid-ask spread at time is .

Definition.

The mid price at time is .

In an LOB, is the highest price at which it is immediately possible to sell at least the lot size of the traded asset at time , and is the lowest price at which it is immediately possible to buy at least the lot size of the traded asset at time . It is sometimes helpful to consider prices relative to and .333Many different naming and sign conventions are used by different authors to describe slightly different definitions of relative price. We introduce an explicit distinction between bid-relative price and ask-relative price to avoid potential confusion.

Definition.

For a given price , the bid-relative price is and the ask-relative price is .

Observe the difference in signs between the two definitions: measures how much smaller is than , and measures how much larger is than .

It is often desirable to compare orders on the bid side and the ask side of an LOB. In these cases, the concept of a single relative price of an order is useful.

Definition.

For a given order , the relative price of the order is

| (3) |

Most traders assess the state of via the depth profile or relative depth profile.

Definition.

The bid-side depth available at price and at time is

| (4) |

The ask-side depth available at price and at time , denoted , is defined similarly using .

The depth available is often stated in multiples of the lot size. Because for buy orders and for sell orders, it follows that and for all prices .

Definition.

The bid-side depth profile at time is the set of all ordered pairs . The ask-side depth profile at time is the set of all ordered pairs .

Definition.

The mean bid-side depth available at price between times and is

| (5) |

The mean ask-side depth available at price between times and , denoted , is defined similarly using the ask-side depth available.

Because and vary, it is rarely illuminating to consider the depth available at a specific price over time. However, relative pricing provides a useful alternative.

Definition.

The bid-side depth available at relative price and at time is

| (6) |

The ask-side depth available at relative price and at time , denoted , is defined similarly using .

Definition.

The bid-side relative depth profile at time is the set of all ordered pairs . The ask-side relative depth profile at time is the set of all ordered pairs .

Definition.

The mean bid-side depth available at relative price between times and is

| (7) |

The mean ask-side depth available at relative price between times and , denoted , is defined similarly using the ask-side relative depth available.

Definition.

The mean bid-side relative depth profile between times and is the set of all ordered pairs . The mean ask-side relative depth profile between times and is the set of all ordered pairs .

Relative depth profiles provide no information about the absolute prices at which trades occur, nor do they contain information about the bid-ask spread or mid price. However, several studies have concluded that order arrival rates depend on relative prices rather than actual prices (see, e.g., Biais et al. (1995); Bouchaud et al. (2002); Potters and Bouchaud (2003); Zovko and Farmer (2002)), so it is common to consider the relative depth profiles and and simultaneously.

Figure 1 shows a schematic of an LOB at some instant in time, illustrating the definitions in this section. The horizontal lines within the blocks at each price level denote how the depth available at that price is composed of different active orders.

Time series of prices arise often during the study of LOBs. As discussed in Section IV.7, it is a recurring theme that the behaviour of such a time series depends significantly on how it is sampled. For example, consider the time series , for some times .

-

•

When the are spaced regularly in time, with seconds between successive samplings, such a time series is said to be sampled on a -second timescale.

-

•

When the are chosen to correspond to arrivals of orders, the may be spaced irregularly in time. Such a time series is said to be sampled on an event-by-event timescale.

-

•

When the are chosen to correspond to trades (i.e., matchings in an LOB), the may also be spaced irregularly in time. Such a time series is said to be sampled on a trade-by-trade timescale.

II.2 Orders: the building blocks of an LOB

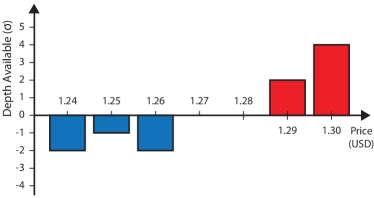

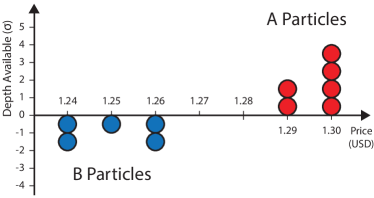

The actions of traders in an LOB can be expressed solely in terms of the submission or cancellation of orders of the lot size. For example, a trader who immediately sells units of the traded asset in the LOB displayed in Figure 2 can be considered as submitting 2 sell orders of size at the price , 1 sell order of size at the price , and 1 sell order of size at the price . Similarly, a trader who posts a sell order of size at the price can be considered as submitting 4 sell orders of size at a price of each.

Almost all of the published literature on LOBs adopts the following terminology. Orders that result in an immediate matching upon submission are known as market orders. Orders that do not, instead becoming active orders, are known as limit orders.444Some practitioners use the terms aggressive orders and resting orders, respectively, but this terminology is far less common in the published literature. However, it is important to recognize that this terminology is used only to emphasize whether an incoming order triggers an immediate matching or not. There is no fundamental difference between a limit order and a market order.

Some trading platforms allow traders to specify that they wish to submit a buy (respectively, sell) market order without explicitly specifying a price. Instead, such a trader specifies only a size, and the matching algorithm sets the price of the order appropriately to initiate the required matching.

II.3 Price changes in LOBs

In LOBs, the rules that govern matchings dictate how prices evolve through time. Consider a buy (respectively, sell) order that arrives immediately after time .

-

•

If (respectively, ), then is a limit order that becomes active upon arrival. It does not cause or to change.

-

•

If , then is a limit order that becomes active upon arrival. It causes to increase (respectively, to decrease) to at time .

-

•

If (respectively, ), then is a market order that immediately matches to one or more active sell (respectively, buy) orders upon arrival. Whenever such a matching occurs, it does so at the price of the active order, which is not necessarily equal to the price of the incoming order. Whether or not such a matching causes (respectively, ) to change at time depends on (respectively, ) and . In particular, the new bid price immediately after the arrival of a sell market order is

(8) Similarly, the new ask price immediately after the arrival of a buy market order is

(9)

Put another way, the incoming order matches to the highest priority active order of opposite type. If , then any residue size of is considered for matching to the next highest priority active order of opposite type, and so on until either there are no further active orders with prices that make them eligible for matching, in which case the residue of becomes active at the price , or is fully matched. The new bid (respectively, ask) price is then equal to the price of the highest priority active buy (respectively, sell) order after the matching occurs.

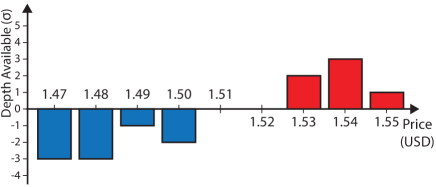

Table 1 lists several possible market events that could occur to the LOB displayed in Figure 2 and the resulting values of and that they would cause.

| Values after arrival (USD) | ||||

|---|---|---|---|---|

| Arriving order | ||||

| Initial Values | ||||

In the financial literature, price changes are commonly studied via returns.

Definition.

The bid-price return between times and is . The ask-price return between times and , denoted , and the mid-price return between times and , denoted , are defined similarly.

Definition.

The bid-price logarithmic return between times and is . The ask-price logarithmic return between times and , denoted , and the mid-price logarithmic return between times and , denoted , are defined similarly.

II.4 The economic benefits of LOBs

In an LOB, traders are able to choose between submitting limit orders and submitting market orders. Limit orders stand a chance of matching at better prices than do market orders, but they also run the risk of never being matched. Conversely, market orders never match at prices better than and , but they do not face the inherent uncertainty associated with limit orders. An LOB’s bid-ask spread can be considered as a measure of how highly the market values the immediacy and certainty associated with market orders versus the waiting and uncertainty associated with limit orders. Foucault et al. (2005) argued that the popularity of LOBs was due in part to their ability to allow some traders to demand immediacy, while simultaneously allowing others to supply it to those who later require it. He conjectured that arbitrageurs, technical traders, and indexers were most likely to place market orders (due to the fast-paced nature of their work) and that portfolio managers were most likely to place limit orders (because their strategies are generally more focused on the long term). In reality, most traders use a combination of both limit orders and market orders; they select their actions for each situation based on their individual needs at that time (Anand et al., 2005).

Glosten (1994) argued that LOBs are an effective way for patient traders to provide liquidity to less patient traders, even when liquidity is scarce. Luckock (2003) concluded that the volume traded in an LOB would always exceed that of a Walrasian market,555A Walrasian market is a market in which all traders send their desired buy or sell orders to a specialist, who then determines the market value of the asset by selecting the price that maximises the volume of trade. given the same underlying supply and demand.

Copeland and Galai (1983) noted that a limit order can be considered as a derivative contract written to the whole market, via which the order’s owner offers to buy or sell the specified quantity of the asset at the specified price to any trader wishing to accept. For example, a trader submits a sell limit order is offering the entire market a call option to buy units of the asset at price for as long as the order remains active. Traders offer such derivative contracts — i.e., submit limit orders — in the hope that they will be able to trade at better prices than if they simply submitted market orders. However, whether or not such a contract will be accepted by another trader (i.e., whether or not the limit order will eventually become matched) is uncertain.

III Challenges of Studying LOBs

In this section, we discuss some of the challenges that LOBs present researchers. In particular, we discuss technical issues associated with the study of empirical LOB data and present several challenges inherent in modelling LOBs.

III.1 Perfect rationality versus zero intelligence

Constructing a useful model of an LOB entails making several assumptions. One such assumption concerns the reason that order flows exist at all. Much of the economics literature assumes that orders are submitted because perfectly rational traders attempt to maximize their “utility” by making trades in markets driven by “information” (Parlour and Seppi, 2008). However, this assumption has come under scrutiny because utility maximisation is often inconsistent with direct observations of individual behaviour (Gode and Sunder, 1993; Kahneman and Tversky, 2000; Lux and Westerhoff, 2009).

At the other extreme lies the zero-intelligence approach, in which aggregated order flows are assumed to be governed by specified stochastic processes whose rate parameters are conditional on other variables such as (Daniels et al., 2003; Cont et al., 2010; Smith et al., 2003). In this way, order flow can be regarded as a consequence of traders blindly following a set of rules without strategic considerations. Much like perfect rationality, zero-intelligence assumptions are extreme simplifications that are inconsistent with empirical observations. However, zero intelligence has the appeal of leading to easily quantifiable models that can yield falsifiable predictions without the need for auxiliary assumptions. It is, therefore, a useful starting point for building models.666In Section V, we explore how some authors have attempted to quantify perfect rationality for modelling purposes and discuss the often highly unrealistic assumptions that such formulations require to be tested empirically. A detailed treatment can be found in Foucault et al. (2005).

Between the two extremes of perfect rationality and zero intelligence lies a broad range of other approaches that make weaker assumptions about traders’ behaviour and order flows, at the cost of resulting in models that are more difficult to study. Many such models rely exclusively on Monte Carlo simulation to produce output. Although such simulations still motivate interesting observations, it is often difficult to trace exactly how specific model outputs are affected by input parameters.

III.2 State-space complexity

It is a well-established empirical fact that current order flows depend on both and on recent order flows (Biais et al., 1995; Ellul et al., 2003; Hall and Hautsch, 2006; Hollifield et al., 2004; Lo and Sapp, 2010; Sandås, 2001). From a perfect-rationality perspective, this can be seen as traders reacting to the changing state of a market; from a zero-intelligence perspective, it can be considered as order flow rates depending on and on their recent history. Either way, a key task is to uncover the structure of such conditional behaviour, either to understand what information traders evaluate when making decisions or to quantify the conditional structure of order flows.

A problem with studying conditional behaviour is that the state space of an LOB is huge: if there are different choices for price in a given LOB, then the state space of the current depth profile alone, expressed in units of the lot size , is . This makes it very difficult to investigate conditional dependences, as the number of variables is so large. Therefore, a key modelling task is to find a way to simplify the evolving, high-dimensional state space, while retaining an LOB’s important features. Some authors have proposed ways to reduce dimensionality (see, e.g., Cont and de Larrard (2011); Eliezer and Kogan (1998); Smith et al. (2003)), but there is no consensus about a simplified state space upon which very general LOB models can be constructed.

III.3 Feedback and coupling

In addition to traders’ actions depending on , the state of also clearly depends on traders’ actions. These mutual dependences induce feedback between and trader behaviour. Also, as described in Section II.2, determines the boundary condition for sell limit order placement because any sell order placed at or below at least partially matches immediately. A similar role is played by for buy orders. Therefore, order flow creates a strong coupling between and . Smith et al. (2003) observed how such coupling makes LOB modelling a difficult problem.

III.4 Priority

As shown in Figure 1, several active orders can have the same price at a given time. Much like priority is given to active orders with the best (i.e., highest buy or lowest sell) price, LOBs also employ a priority system for active orders within each individual price level.

By far the most common priority mechanism currently used is price-time. That is, for active buy (respectively, sell) orders, priority is given to the active orders with the highest (respectively, lowest) price, and ties are broken by selecting the active order with the earliest submission time . Price-time priority is an effective way to encourage traders to place limit orders (Parlour, 1998). Without a priority mechanism based on time, there is no incentive for traders to show their hand by submitting limit orders earlier than is absolutely necessary.

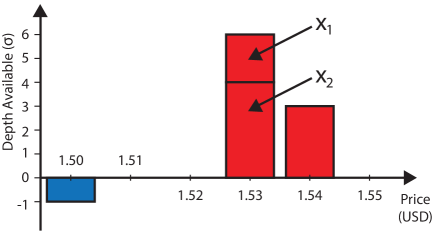

Another priority mechanism, commonly used in futures markets, is pro-rata (Field and Large, 2008). Under this mechanism, when a tie occurs at a given price, each relevant active order receives a share of the matching proportional to the fraction of the depth available that it represents at that price. For example, if a buy market order of size arrived at the LOB displayed in Figure 3, then of it would match to active order and of it would match to active order , because they correspond, respectively, to and of the depth available at . Traders in pro-rata priority LOBs are faced with the substantial difficulty of optimally selecting limit order sizes, because posting limit orders with larger sizes than the quantity that is really desired for trade becomes a viable strategy to gain priority.

Another alternative priority mechanism is price-size, in which ties are broken by selecting the active order of largest size among those at the best price. Until recently, no major exchanges used this priority mechanism. However, in October 2010, the first price-size trading platform, NASDAQ OMX PSX, was launched (NADSAQ, 2010). Some exchanges also allow traders to specify a minimum match size when submitting orders. Orders with a size smaller than this are not considered for matching to such orders. This is similar to a price-size priority mechanism: small active orders are often bypassed, effectively giving higher priority to larger orders.

Different priority mechanisms encourage traders to behave in different ways. Price-time priority encourages traders to submit limit orders early; price-size and pro-rata priority reward traders for placing large limit orders and thus for providing greater liquidity to the market. Traders’ behaviour is closely related to the priority mechanism used, so LOB models need to take priority mechanisms into account when considering order flow. Furthermore, priority plays a pivotal role in models that attempt to track specific orders.

III.5 Incomplete sampling and hidden liquidity

An LOB reflects only the subset of trading intentions that traders have announced up to time . However, the fact that no traders have submitted a limit order at a given price does not imply that none of them want to trade at this price, because they could be keeping their intentions private by submitting orders only when absolutely necessary (Tóth et al., 2011). Bouchaud et al. (2009) noted that a typical snapshot of at a given time is often very sparse, containing few active orders. However, this is not an indication that few people wish to trade; it is merely an indication that they have not yet announced any intention to do so. Indeed, some traders choose to submit only market orders and do not submit limit orders at all.777Arbitrageurs provide a key example, because their strategies depend on simultaneously buying and selling in an attempt to make instant profit. Limit orders are of little use to them because it is uncertain when (if ever) they will be matched.

III.5.1 Hidden orders

Many exchanges allow traders to conceal the extent of their intentions to trade, often at the cost of paying some penalty in terms of priority or price. For example, many exchanges allow traders to submit iceberg orders (also known as hidden-size orders), a type of limit order that specifies not only a total size and price but also a visible size. Other traders only see the visible size. Rules regarding the treatment of the hidden quantity vary greatly from one exchange to another. In some cases, once a quantity of at least the visible size matches to an incoming market order, another quantity equal to the visible size becomes visible. This quantity has priority equal to that of a standard limit order placed at this price at this time. This sort of iceberg order is similar to a trader first submitting a limit order, then watching the market carefully and submitting a new limit order at the same price and size at the exact moment that the previous limit order matches to an incoming market order. A trader acting in this way is sometimes deemed to be constructing a synthetic iceberg order. The only difference between a synthetic iceberg order and a genuine iceberg order occurs when a market order with a size larger than the (visible) depth available at the best price arrives. In this situation, the market order matches to any visible portions of active orders at the best price according to the usual priority rules, then matches to a portion of any hidden depth available at this price. By contrast, if a trader submits a small but entirely visible duplicate limit order immediately after the previous order matches, then a large incoming market order would match only to the active orders that existed when it arrived. The rest of the incoming market order would instead match to the active orders at the next best price.

Some exchanges have an alternative structure for iceberg orders. Whenever a quantity equal to at least the visible size of an iceberg order matches to an incoming market order, the rest of the order (i.e., the portion of the hidden component that does not match to the same incoming market order) is cancelled. Iceberg orders can thereby match incoming market orders of a larger size than is initially apparent, but otherwise they behave like any other order. This is the system currently used by the Reuters trading platform (Thomson-Reuters, 2011).

Some other trading platforms allow entirely hidden limit orders. These orders are given priority behind both entirely visible active orders at their price and the visible portion of iceberg orders at their price, but they give traders the ability to submit limit orders without revealing any information whatsoever to the market.

III.5.2 Dark pools

Recently, there has been an increase in the popularity of so-called dark pools (see, e.g., Carrie (2006); Hendershott and Jones (2005)). The matching rules governing trade in dark pools vary greatly from one exchange to another (Mittal, 2008). Some dark pools are essentially LOBs in which all active orders are entirely hidden. Other dark pools do not allow traders to specify prices for their orders. Instead, traders submit orders describing their desired quantity and whether they wish to buy or sell, and the dark pool holds all such requests in an entirely hidden, time-priority queue until they are matched to orders of the opposite type. Upon matching, trades occur either at the mid-price of another specified standard (i.e., non-dark) LOB for the same asset or at a price that is later negotiated by the two traders involved.

III.5.3 Displayed liquidity

Even in LOBs with no hidden liquidity, traders are not always able to view the set of all active orders in real time. Many exchanges display only active orders that lie within a certain range of relative prices. Furthermore, some electronic trading platforms only transmit updates to at a specific frequency, so all activity that has taken place since the most recent refresh signal is invisible to traders.

III.6 Volatility

Loosely speaking, volatility is a measure of the variability of returns of a traded asset (Barndorff-Nielsen and Shephard, 2010). The volatility of an asset provides some indication of how risky it is. All else held equal, an asset with higher volatility is expected to undergo larger price changes over a given time interval than an asset with lower volatility. For traders who wish to manage their risk exposure, volatility is an important consideration when deciding the assets in which to invest, and therefore often forms the basis of optimal portfolio construction (Rebonato, 2004).

Many different measures of volatility exist, and the exact form of volatility studied in a given situation depends on the type of available data and the desired purpose of the calculation (Shephard, 2005). Even when estimated on the same data, different measures of volatility sometimes exhibit different properties. For example, different measures of volatility follow different intra-day patterns in a wide range of different markets (see Cont et al. (2011) and references therein). Therefore, many empirical studies report results using several different measures of volatility.

In an LOB, traders have access to far more information than just and . In particular, information such as and is useful to predict how prices are likely to change (Biais et al., 1995; Bortoli et al., 2006; Ellul et al., 2003; Hall and Hautsch, 2006; Lo and Sapp, 2010). As discussed in Section IV.5, several empirical studies from a wide range of LOBs have reported links between volatility and other LOB properties. However, to our knowledge, there does not yet exist an estimate of volatility that takes the full state of into account. Instead, most estimates of volatility consider only changes in price series such as , , and . For further discussion of practical issues regarding volatility estimation, see Liu et al. (1999).

III.6.1 Model-free estimates of volatility

There is an extensive literature on the use of price series data to perform direct, model-free estimates of volatility (see, e.g., Aït-Sahalia et al. (2011); Andersen and Todorov (2010); Bandi and Russell (2006); Zhou (1996)). In this section, we discuss three methods for performing such estimates.

Definition.

Given the bid-price series sampled at regularly spaced times, the bid-price realized volatility is . The ask-price realized volatility, denoted , and the mid-price realized volatility, denoted , are defined similarly.

Realized volatility depends on the frequency at which price series are sampled. It is a useful measure for comparing the variability of return series sampled with the same frequency, but it is not appropriate to compare the realized volatility of a once-daily price series for one stock to a once-hourly price series for another.

Definition.

Given the bid-price series sampled at the times at which consecutive sell market orders arrive, the bid-price realized volatility per trade is . The ask-price realized volatility per trade, denoted , is defined similarly using consecutive buy market order arrival times. The mid-price realized volatility per trade, denoted , is defined similarly using consecutive market order arrival times (irrespective of whether they are buy or sell market orders).

Realized volatility per trade is useful for comparing how prices vary on a trade-by-trade basis.

Definition.

For a given trading day , the bid-price intra-day volatility is . The ask-price intra-day volatility, denoted , and the mid-price intra-day volatility, denoted , are defined similarly.

Intra-day volatility is useful for estimating the probability of very large price changes in a given day. It is particularly important for day traders, who unwind their trading positions before the end of each trading day.

III.6.2 Model-based estimates of volatility

A difficulty that arises when estimating any measure of volatility in an LOB is that many traders submit then immediately cancel limit orders. This can occur for a variety of reasons, but it is often the result of electronic trading algorithms searching for hidden liquidity. Such behaviour can cause and to fluctuate rapidly without any trades occurring, and it can be considered as microstructure noise rather than a meaningful change in price. One way to address this problem is to assume that the observed data is governed by a model from which an estimate of volatility that is absent of microstructure noise can be derived. The parameters of the model are then estimated from the data, and the volatility estimate is derived explicitly from the model. However, a drawback of this method is that it depends heavily on the model, and models that poorly mimic important aspects of the trading process may therefore give misleading volatility estimates.

III.7 Resolution parameters

Values of and vary greatly from between different trading platforms. Expensive stocks are often traded with share; cheaper shares are often traded with share. In foreign exchange (FX) markets, some trading platforms use values as large as million units of the base currency, whereas others use values as small as units of the base currency.888In FX markets, an XXX/YYY LOB matches exchanges of the base currency XXX to the counter currency YYY. A price in an XXX/YYY LOB denotes how many units of currency YYY are exchanged for a single unit of currency XXX. For example, a trade at the price in a GBP/USD market corresponds to 1 pound sterling being exchanged for US dollars. In equity markets, is often of the stock’s mid price , rounded to the nearest power of 10. For example, for Apple Inc. fluctuated between approximately $400 and approximately $700 in 2012, during which time it traded with . A given currency pair is often traded with different values of on different trading platforms. For example, on the electronic trading platform Hotspot FX, for the GBP/USD LOB and for the USD/JPY LOB, whereas on the electronic trading platform EBS, for the GBP/USD LOB and for the USD/JPY LOB (EBS, 2012; Hotspot, 2013).

It is a recurring theme in the literature (see, e.g., Biais et al. (1995); Foucault et al. (2005); Seppi (1997); Smith et al. (2003)) that an LOB’s resolution parameters and greatly affect trade within it. An LOB’s lot size dictates the smallest permissible order size, so any trader who wishes to trade in quantities smaller than is unable to do so. Furthermore, as we discuss in Section IV.6, traders who wish to submit large market orders often break them into smaller chunks to minimize their market impact. The size of controls the smallest permissible size of such chunks and therefore directly affects traders who implement such a strategy. An LOB’s tick size dictates how much more expensive it is for a trader to gain the priority (see Section III.4) associated with choosing a higher (respectively, lower) price for a buy (respectively, sell) order (Parlour and Seppi, 2008). In markets where is extremely small, there is little reason for a trader to submit a buy (respectively, sell) limit order at a price where there are already other active orders. Instead, he or she can gain priority over such active orders very cheaply, by choosing the price (respectively, ) for the limit order. Such a setup leads to LOBs that undergo extremely frequent changes in and due to the small depths available. This makes it difficult for other traders to monitor the state of the market in real time. In September 2012, the electronic FX trading platform EBS increased the size of for most of its currency pairs’ LOBs. Their reason for doing so was “to help thicken top of book price points, increase the cost of top of book price discovery and improve matching execution in terms of percent fill amounts” (EBS, 2012).

III.8 Bilateral trade agreements

On some exchanges, each trader maintains a block-list of other traders with whom he or she is unwilling to trade. A trade can only occur between traders and if does not appears on ’s block-list and vice-versa. The exchange shows each trader a personalized LOB that contains only the active orders owned by traders with whom it is possible for to trade. When a trader submits a market order, it can only match to active orders in their personalized LOB, bypassing any higher priority active orders from traders on their block-list.

On exchanges that use such bilateral trade agreements, it is possible for a buy (respectively, sell) market order to bypass all active orders at the globally lowest (respectively, highest) price available in and to match to an active order with a strictly higher (respectively, lower) price. Furthermore, given two traders and who do not have a bilateral trade agreement, it is possible for to simultaneously contain both an active buy order owned by and an active sell order owned by , with , without a matching occurring. Therefore, it is possible for such markets to have a negative bid-ask spread.

III.9 Opening and closing auctions

Many exchanges suspend standard limit order trading at the beginning and end of the trading day and instead use an auction system to match orders. For example, the LSE’s flagship order book SETS (SETS, 2011) has three distinct trading phases in each trading day. Between 08:00 and 16:30, the standard LOB mechanism is used in a period known as continuous trading. Between 07:50 and 08:00, a -minute opening auction takes place. Between 16:30 and 16:35, a -minute closing auction takes place. During both auctions, all traders can view and place orders as usual, but no orders are matched. Due to the absence of matchings, the highest price among buy orders can exceed the lowest price among sell orders. All orders are stored until the opening auction ends. At this time, for each price at which there is non-zero depth available, the trade matching algorithm calculates the total volume of trades that could occur by matching buy orders with a price greater than or equal to to sell orders with a price less than or equal to . It then calculates the uncrossing price

| (10) |

In contrast to standard LOB trading, all trades take place at the same uncrossing price . Given , if there is a smaller depth available for sale than there is for purchase (or vice versa), ties are broken using time priority.

Throughout the opening auction, all traders can see what the value of would be if the auction were to end at that moment. This allows all traders to observe the discovery of the price without any matchings taking place until the process is complete. Such a price-discovery process is common to many markets.999Biais et al. (1999) performed a formal hypothesis test on price-discovery data from the Paris Bourse. Working at the 2.5% level, they did not reject the null hypothesis that traders’ conditional expectations of asset price approached the market value of the asset during the final 9 minutes of the price-discovery process. However, they found that traders’ actions were not significantly different from noise during the early part of the price-discovery process.

III.10 Statistical issues

As we discuss in Section IV, many authors have reported statistical regularities in LOB data from a wide variety of different markets. However, such statistical analysis is fraught with difficulties because assumptions such as independence and stationarity, which are often required to ensure consistency of estimation, are rarely satisfied by LOB data (Cont, 2005; Mantegna and Stanley, 1999). Furthermore, suboptimal estimators have been employed commonly in the literature, and have often produced estimates with large variance or bias. For example, there are questions about the validity of many reported power laws throughout the scientific literature (Clauset et al., 2009; Stumpf and Porter, 2012). Many authors use ordinary least-squares regression on a log-log plot to estimate power-law exponents from LOB data, yet Clauset et al. (2009) showed that this method produces significant systematic estimation errors. They also showed that it is inappropriate to use power-law estimators designed for continuous data on discrete data (or vice versa), yet many LOB studies do precisely this.

In this section, we list some of the pitfalls of statistical estimation using LOB data and suggest some useful estimators for data analysis. However, these techniques are not “one-size-fits-all” approaches, and it is important to verify the necessary assumptions before implementing them on a given data set.

III.10.1 Power laws

Several LOB properties are reported to have power-law tails:

Definition.

A random variable is said to have a power-law tail with exponent if there exists some such that as

If there exists a such that is proportional to for all , then clearly has a power-law tail.101010This is not the only probability density function that has a power-law tail, but it is the most common in the literature. When attempting to fit power-law tails to empirical observations, it is often assumed that such a exists (and resides within the range of the data), because the existence of such a allows simple, closed-form expressions to be derived. Under this assumption, Clauset et al. (2009) provided a comprehensive algorithm for consistent estimation of and via maximum likelihood techniques, as well as for testing the hypothesis that the data really does follow a power law for . Several other consistent estimation procedures also exist (see, e.g., Hill (1975); Mu et al. (2009)), but no single estimator has emerged as the best to adopt in all situations. Therefore, some empirical studies report results using several different estimators and then draw inference based on the whole set of results. However, as Mu et al. (2009) highlighted, different estimators often produce vastly different estimates of , making such inference difficult.

III.10.2 Long-memory processes

As we discuss in Section IV.7, several time series related to LOBs have been reported to exhibit long memory. Intuitively, a time series has long memory if values from the present are correlated with values in the distant future. The study of long-memory processes involves considerable challenges, and caution is needed when applying standard statistical techniques to data with long memory (Beran, 1994). For example, the effective sample size of a long memory process is significantly smaller than the number of data points, so statistical estimators often converge at an extremely slow rate (Farmer and Lillo, 2004). Furthermore, the correlation structure can cause such estimators to converge to arbitrary values (Beran, 1994).

In this section, we discuss several practical challenges of estimating long memory. We denote by a real-valued, second-order stationary111111A time series is second-order stationary if its first and second moments are finite and do not vary with time. For a discussion of issues regarding stationarity in financial time series, see Taylor (2008). time series of length , .

One way to define long memory is via the asymptotic behaviour of the autocorrelation function.

Definition.

The autocorrelation function of a time series is given by

| (11) |

where is the mean of the series.

Definition.

A time series is said to exhibit long memory if there exists some such that decays like a power law,

| (12) |

The exponent describes the strength of the long memory: the smaller the value of , the stronger the long-range autocorrelations (Lillo and Farmer, 2004). Because of the slow decay of the autocorrelation function in a long-memory process, present values of the series can have a significant effect on its values in the distant future. It is a recurring mistake in the literature that if has long memory, its unconditional distribution must exhibit heavy tails. However, Preis et al. (2006, 2007) showed that such an implication does not hold in general.

A key difficulty when using Equation (12) to assess whether a given series has long memory is that it deals only with asymptotic behaviour. To study the large- behaviour, it is necessary to observe more than values of , but clearly any empirically observed time series is finite. Also, the values of the function can be small, making estimation of the functional form of very difficult. Therefore, direct estimation of from the autocorrelation function often produces very poor results (Lillo and Farmer, 2004).

An alternative way to characterize long memory is via the diffusion properties (Beran, 1994; Lillo and Farmer, 2004) of the integrated series ,

| (13) |

If is a long-memory process, then the standard deviation of scales as , with (Lillo and Farmer, 2004); if does not have long memory, then the standard deviation of scales as , (Beran, 1994). The exponent is called the Hurst exponent, and is related to by

| (14) |

Under some assumptions,121212Most commonly, that is a fractional Brownian motion, i.e., a self-similar process with Gaussian increments (Beran, 1994; Robinson, 2003). there are several asymptotically unbiased estimators of that are more robust to noise in than is direct estimation of from the autocorrelation function (Taqqu et al., 1995). However, the performance of such estimators on empirical data, which might not conform to these assumptions, varies considerably (Rea et al., 2009; Xu et al., 2005). Different disciplines tend to favour different estimators, although the choices are often based on historical reasons, not performance. Some of the most commonly used are:

- •

-

•

log-periodogram regression (Geweke and Porter-Hudak, 1983);

- •

IV Empirical Observations in LOBs

The empirical literature on LOBs is very large, yet different studies often present conflicting conclusions. Reasons for this include different trade matching algorithms operating differently, different asset classes being traded on different exchanges, differing levels of liquidity in different markets, and different researchers having access to data of differing quality. Furthermore, as traders’ strategies have evolved over time, so too have the statistical properties of the order flow they generate. This has become a particularly important consideration because competition and trading volumes have increased with the widespread uptake of electronic trading algorithms.

To aid comparisons, we present in Appendix A a description of the aims, date range, data source, and data type of each of the empirical studies of LOBs that we discuss in this survey. We now discuss the main findings of these empirical studies in more detail, including a selection of stylized facts that have consistently emerged from several different markets. However, we note in Section VI that there have been few recent data analyses, despite the many recent changes in markets.

IV.1 Order size

Given the heterogeneous motivations for trading within a single market, it is unsurprising that incoming order sizes vary substantially. Nevertheless, several regularities occur in empirical data.

For equities traded on the Paris Bourse, Bouchaud et al. (2002) reported that the distribution of was approximately uniform for incoming limit orders with . For two stocks traded on NASDAQ, Maslov and Mills (2001) reported power-law and log-normal distributions to fit the distribution of incoming limit order sizes . The mean reported power-law exponent was (i.e., with standard deviation ). However, the quality of the power-law fits was deemed to be weak, and the log-normal fits were deemed to be applicable over a wider range of limit order sizes than the power-law fits (although the authors stated no precise range of applicability for either). For four stocks on the Island ECN, Challet and Stinchcombe (2001) reported that incoming limit order sizes clustered strongly at round-number amounts such as 10, 100, and 1000. Mu et al. (2009) reported a similar round-number preference for market orders on the Shenzhen Stock Exchange. Mu et al. (2009) also studied the distribution of total trade sizes when aggregated over a variety of time windows and found it to exhibit a power-law tail. Different power-law exponent estimators produced different estimates of the tail exponent, but the authors judged the tail exponent to be larger than 2. Maslov and Mills (2001) reported similar power-law fits on NASDAQ. Studying 5 days of data covering 3 equities, they reported a mean power-law exponent of . Although they did not state a range of sizes over which their reported power-law distributions applied, Figure 1 in Maslov and Mills (2001) suggests an approximate range of 200 to 5000. In a study of the 1000 largest equities in the USA, Gopikrishnan et al. (2000) also reported power-law fits for the distribution of trade sizes. The mean reported power-law exponent was . However, Bouchaud et al. (2009) noted that the data studied by Gopikrishnan et al. contained information about trades that were privately arranged to occur off-book. They conjectured that this caused Gopikrishnan et al. to overestimate the frequency with which very large orders occurred.

On the Stockholm Stock Exchange, Hollifield et al. (2004) reported that buy (respectively, sell) market orders that walk up the book — i.e., those with a size (respectively, ) — accounted for only of submitted market orders. Therefore, the vast majority of submitted buy (respectively, sell) market orders matched only to active orders at (respectively, ), rather than at other prices.

IV.2 Relative price

As discussed in Section II.1, regularities in price series are best investigated via the use of relative pricing, as and themselves evolve through time. Unlike the distribution of order sizes, which seems to vary from market to market, the distribution of relative prices appears to exhibit power-law behaviour in all markets studied (Bouchaud et al., 2002; Potters and Bouchaud, 2003; Zovko and Farmer, 2002; Maskawa, 2007; Gu et al., 2008b; Mike and Farmer, 2008). This may be because some traders place limit orders deep into LOBs, under the optimistic belief that large price swings could occur (Bouchaud et al., 2002).

The distribution of relative prices of orders that arrived with non-negative relative price on the Paris Bourse (Bouchaud et al., 2002), NASDAQ (Potters and Bouchaud, 2003), the LSE (Zovko and Farmer, 2002; Maskawa, 2007), and the Shenzhen Stock Exchange (Gu et al., 2008b) were reported to follow such a power law, with different values of the exponent for the different markets. On the Paris Bourse, for buy and sell orders alike, the power-law exponent for relative prices from to over (even up to for some stocks) was approximately . On NASDAQ, the ranges of relative prices over which the distributions followed a power law and the power-law exponents themselves both varied from stock to stock. On the LSE, the value of the power-law exponent was approximately for relative prices between and for both buy and sell orders. In aggregated data describing all 23 studied stocks on the Shenzhen Stock Exchange, the power-law exponent for the distribution of non-negative relative prices131313Observe that the notation used by Gu et al. (2008b) assigns the opposite signs when measuring relative price than those that we employ. was for buy orders and for sell orders, and the power-law exponent for the distribution of negative relative prices was for buy orders and for sell orders. This asymmetry between buy orders and sell orders contrasts to the other studied markets, but the exact matching rules on the Shenzhen Stock Exchange prevent large price changes from occurring within a single day (which could account for this effect).

The maximum arrival rate of incoming orders was found to occur at a relative price of 0 on the LSE Mike and Farmer (2008), the Shenzhen Stock Exchange (Gu et al., 2008b), the Paris Bourse (Biais et al., 1995; Bouchaud et al., 2002), and NASDAQ (Challet and Stinchcombe, 2001), although the maximum arrival rate on the Tokyo Stock Exchange was found to occur inside the spread (Cont et al., 2010).

IV.3 Order cancellations

Several empirical studies covering a wide range of different markets have concluded that the vast majority of active orders end in cancellation rather than matching. The percentage of orders that were cancelled ranged from approximately to more than on the Island ECN (Hasbrouck and Saar, 2002; Challet and Stinchcombe, 2001), an exchange-traded fund that tracked the NASDAQ 100 (Potters and Bouchaud, 2003), S&P 500 futures contracts (Baron et al., 2012), and in FX markets (Gereben and Kiss, 2010; Lo and Sapp, 2010). Therefore, cancellations play a major role in the evolution of in all of these markets.

In recent years, electronic trading algorithms have surged in popularity across all markets, and such algorithms often submit and cancel vast numbers of limit orders over short periods as part of their trading strategies (Harris, 2002; Hendershott et al., 2011). The widespread use of such trading algorithms seems to have further increased the percentage of orders that are cancelled in recent data. In particular, a recent study of FX data found that more than of active orders ended in cancellation rather than matching (Gould et al., 2013b).

IV.4 Mean relative depth profile

Despite their different resolution parameters (see Section II.1) and the different prices at which trades occur in them, several qualitative regularities are common to the mean relative depth profiles in a wide range of markets.

No significant difference was detected between the mean bid-side and the mean ask-side relative depth profiles on the Paris Bourse (Biais et al., 1995; Bouchaud et al., 2002), NASDAQ (Potters and Bouchaud, 2003), and Standard and Poor’s Depositary Receipts (SPY)141414SPY is an exchange-traded fund that allows traders to effectively buy and sell shares in all of the 500 largest stocks traded in the USA. (Potters and Bouchaud, 2003). By contrast, Gu et al. (2008c) reported asymmetry between the mean bid-side and the mean ask-side relative depth profiles on the Shenzhen Stock Exchange, but this is unsurprising considering that this market has additional rules restricting price movements each day that essentially impose asymmetric restrictions on the range of relative prices over which traders can submit orders.

Mean relative depth profiles exhibit a hump shape151515More precisely, the absolute value of the mean depth available increases over the first few relative prices, and it subsequently decreases. in a wide range of markets, including the Paris Bourse (Bouchaud et al., 2002), NASDAQ (Potters and Bouchaud, 2003), the Stockholm Stock Exchange (Hollifield et al., 2004), and the Shenzhen Stock Exchange (Gu et al., 2008c). The maximal mean depth available for SPY was reported to occur at and , which could also be considered as a hump with its maximum at a relative price of 0 (Potters and Bouchaud, 2003).

The location of the hump varies across markets. However, it is difficult to perform direct comparisons between different markets because differences in their tick sizes affect both the granularity of the price axis and the ways in which traders behave (see Section III.7). There may also be strategic reasons that the hump occurs in different locations in different markets. For example, in markets in which large price changes are relatively common, more traders can choose to submit limit orders with larger relative prices than in those where such changes are rare. This increases the relative price at which the hump resides. Roşu (2009) conjectured that a hump would exist in all markets in which large market orders were sufficiently likely; this represents a trade-off between the optimism that a limit order placed away from or might eventually be matched (at a significant profit) and the pessimism that placing limit orders too far away from and might never match.

IV.5 Conditional frequencies of events

The properties that we have discussed thus far in this section have all been calculated unconditionally (i.e., without reference to other events or variables). However, several factors influence how traders interact with LOBs, so it is reasonable to study not only unconditional frequencies, but also the frequencies of those events given that some other condition was satisfied. However, the study of such conditional event frequencies in LOBs is difficult for two main reasons:

-

1.

The state space is very large. Deciding which of the enormous number of possible events or LOB states on which to condition is very difficult (Parlour and Seppi, 2008);

-

2.

There is a small latency between the time that a trader sends an instruction to submit or cancel an order and the time that the exchange server receives the instruction. Furthermore, some exchanges only send refresh signals at fixed time intervals, so traders cannot be certain that LOBs that they observe via their trading platform are perfect representations of the actual LOBs at that instant in time. Therefore, conditioning on the “most recent” event is problematic, as the most recent event recorded by the exchange (and thus appearing in the market data) may not be the most recent event that a given trader observed via the trading platform.

Nevertheless, several empirical studies of conditional event frequencies in LOBs have identified interesting behaviour. In this section, we review the key findings from several such publications, highlighting both the similarities and differences that have emerged across different markets. Most studies have used LOB data that dates back 10 years or more. Although this alleviates the aforementioned difficulties with latency (as the volume of order flows in LOBs was much smaller in the past than it is today, so the mean inter-arrival times between successive events were substantially longer than the latency times), it also inevitably raises the question of how representative such findings are of today’s LOBs. We return to this issue in Section VI.

IV.5.1 Order size

A simple example of conditional structure is the relationship between the size and the relative price of orders on the Paris Bourse, as studied by Bouchaud et al. (2002). For the stocks studied, the distribution of varied substantially according to the relative price of the corresponding orders. In particular, orders with larger relative price had smaller absolute size on average. Maslov and Mills (2001) made a similar observation for limit orders on NASDAQ.

IV.5.2 Relative price

On the Paris Bourse (Biais et al., 1995) and the Australian Stock Exchange (Hall and Hautsch, 2006; Cao et al., 2008), traders placed more orders with a relative price satisfying (i.e., limit orders falling inside of the bid-ask spread) at times when was larger than its median value. Similarly, on the NYSE (Ellul et al., 2003), the percentage of incoming orders that arrived with a relative price (i.e., were limit orders) increased as increased and decreased when decreased. Biais et al. (1995) argued that when is small, it is less expensive for traders to demand immediate liquidity, so market orders become more attractive. However, it is also possible to explain such an observation via a zero-intelligence approach: if limit order prices are chosen uniformly at random, then it is more likely that an incoming limit order price resides in the interval when the interval is wider.

On the Paris Bourse, Biais et al. (1995) found that the percentage of buy (respectively, sell) limit orders that arrived with relative price satisfying was higher at times when (respectively, ) was larger. They conjectured that this was evidence of traders competing for priority, as the only way to gain higher priority than the active orders in the (already long) queue in this situation is to submit an order with a better price. Furthermore, on the NYSE, Ellul et al. (2003) reported the arrival rate of buy (respectively, sell) limit orders with a relative price satisfying tended to increase as the total size of active buy (respectively, sell) orders increased. They also reported a similar result for the arrival of buy (respectively, sell) market orders. On the Australian Stock exchange, Hall and Hautsch (2006) calculated that the percentage of buy (respectively, sell) orders that were limit orders decreased as the total size of active buy (respectively, sell) orders increased, and Cao et al. (2008) reported that the proportion of arriving orders that were market orders increased when and were larger. On the LSE, Maskawa (2007) concluded that traders favoured placing their limit orders at relative prices similar to those where there was already a large number of active orders.

However, such conditional structure is not common to all markets. On the LSE, Mike and Farmer (2008) reported that the distribution of relative prices was independent of . On the Shenzhen Stock Exchange, Gu et al. (2008b) reported that the distribution of relative prices was independent of both and volatility. On the Paris Bourse, Biais et al. (1995) concluded that (respectively, ) had little impact on the rate of incoming sell (respectively, buy) market orders.

On the Swiss Stock Exchange, Ranaldo (2004) reported that order flow to depend on several factors, including volatility, recent order flow, and the state of . Traders submitted more limit orders and fewer market orders during periods when or volatility were high. The proportion of orders that arrived with negative relative price decreased as the inter-arrival time between recent orders increased. Traders submitted higher priced buy orders (respectively, lower priced sell orders) when the total size of active buy (respectively, sell) orders was greater. Ranaldo (2004) noted that buy order submission seemed to depend on both the sell side and the ask side of , whereas sell order submission seemed to depend only on the sell side of . He noted, however, that market performance during the sample period might have caused such asymmetry, because the percentage change in was positive for all but one of the stocks studied and exceeded for 4 of them.

On the LSE, Zovko and Farmer (2002) reported that the relative prices of incoming limit orders were conditional on the bid-price realized volatility per trade. They constructed two time series by calculating the mean relative price of arriving buy limit orders and the bid-price realized volatility per trade over 10 minute windows, and then calculated their cross correlation. They rejected (at the 2.5% level) the hypothesis that the two series were uncorrelated and observed that changes in bid-price realized volatility immediately preceded changes in mean relative price for buy limit orders.161616Zovko and Farmer (2002) noted that it was not clear from the cross-correlation function alone whether traders explicitly considered bid-price realized volatility when choosing the prices for their buy limit orders, or whether some other external factor first affected bid-price realized volatility and then affected traders’ actions. If the former could be demonstrated, it would support the widely-held belief that many traders consider realized volatility to be an important factor in deciding when to place a limit order (Zovko and Farmer, 2002). They also observed similar behaviour when comparing the time series of ask-price realized volatility and the time series of mean relative price for sell limit orders.

In FX markets, Lo and Sapp (2010) reported that traders submitted orders with higher relative prices during periods of high mid-price realized volatility.

IV.5.3 Order flows

On the Stockholm Stock Exchange, Sandås (2001) reported that order flows at time were conditional on both and on previous order flows. In FX markets, Lo and Sapp (2010) reported that order flows at time were conditional on several variables including , , , depth available behind the best prices, time of day, and recent order flows. However, the precise structure of the conditional dependences varied between currency pairs.

On the Australian Stock Exchange (Hall and Hautsch, 2006), the arrival rates of all market events were reported to increase and decrease together. The authors suggested that other exogenous factors (which they had not measured) might have influenced aggregate LOB activity. In a more recent study of the Australian Stock Exchange, Cao et al. (2008) reported that the arrival rates of market events at time were conditional on , but not on the state of at earlier times. This suggests that traders evaluated only an LOB’s most recent state — and not a longer history — when making order placement and cancellation decisions. Cao et al. (2008) did not find evidence that mid-price returns had a significant impact on order arrival or cancellation rates.

Using several different financial instruments traded in electronic LOBs, Toke (2011) reported that both buy limit order and sell limit order arrival rates increased following the arrival of a market order, but they found no evidence that market order arrival rates increased following the arrival of a limit order.

IV.5.4 Event clustering

Using data from 40 stocks on the Paris Bourse, Biais et al. (1995) observed strong clustering through time when studying the “action classes” (such as “arrival of buy market order”, “arrival of buy limit order within the spread”, and “cancellation of active sell order”) of market events. For all action classes, the conditional frequency with which a market event belonged to the specified action class, given that the previous market event also belonged to the same action class, was higher than the corresponding unconditional frequency. The authors offered numerous possible explanations for this phenomenon: traders might have strategically split large orders into smaller chunks to avoid revealing their full trading intentions or to minimize market impact (see Section IV.6); different traders might have mimicked each other; different traders might have independently reacted to new information; or different traders might have tried to undercut each other (i.e., cancelled active buy (respectively, sell) orders and resubmitted them at a slightly higher (respectively, lower) price solely to gain price priority). Bursts of small, frequent changes in and occurred more often when was large, which they argued provided evidence of undercutting. However, Bouchaud et al. (2009) concluded that the phenomenon was driven primarily by strategic order splitting and found no evidence that different traders mimicked each other.

On the NYSE, Ellul et al. (2003) reported that periods with above-average order arrival rates clustered together in time, as did periods with below-average order arrival rates. The rate of buy (respectively, sell) limit order arrivals increased after periods of positive (respectively, negative) mid-price returns, and the rate of limit order arrivals also increased late in the trading day. There was also a similar clustering of market events by action classes as was observed by Biais et al. (1995) on the Paris Bourse. However, Ellul et al. (2003) reported that the number of occurrences of market events from a specific action class in a given -minute window and the corresponding number of occurrences of market events in the previous -minute window were negatively correlated. Furthermore, they concluded that the arrival rate of market events from a given action class was more heavily conditional on the action class of the single most recent market event than it was on , whereas the distribution of the number of occurrences of market events from a given action class in a given -minute window was more heavily conditional on during the previous -minute window than it was on the number of occurrences of market events from any specific action class in the same window.

IV.5.5 Cancellations

On the Paris Bourse, Biais et al. (1995) reported that cancellations of buy (respectively, sell) active orders occurred more frequently after the arrival of a buy (respectively, sell) market order. They conjectured that this was evidence that traders submitted large orders in the hope of finding hidden liquidity and then cancelled any unmatched portions.

On the Australian Stock Exchange, Cao et al. (2008) concluded that priority considerations played a key role for traders when deciding whether or not to cancel their active orders. The cancellation rate for active buy (respectively, sell) orders increased when new, higher-priority buy (respectively, sell) limit orders arrived. In addition, the cancellation rate of active buy (respectively, sell) orders at prices (respectively, ) increased when (respectively, ) became zero. The authors proposed that this occurred because traders with active orders at price could, without substantial loss of priority, cancel and then resubmit them at price (respectively, ), to possibly gain a better price if the order eventually matched. No similar increase occurred when (respectively, ) became zero.

IV.5.6 Price movements

On the Paris Bourse, Biais et al. (1995) reported that decreased more frequently (respectively, increased more frequently) immediately after the arrival of a market order that caused to decrease (respectively, to increase). They suggested that such behaviour could be due to traders reacting to information, either because external sources of news caused a revaluation of the underlying asset or because traders interpreted the downward movement of (respectively, upward movement of ) itself as news. Indeed, Potters and Bouchaud (2003) found evidence on NASDAQ that each new trade was interpreted by traders as new information that directly affected the flow of incoming orders.

IV.5.7 Volatility

For Canadian stocks, Hollifield et al. (2006) reported that several different volatility measures were correlated with order flow rates. In FX markets, Lo and Sapp (2010) reported that mid-price realized volatility affected order flows. For US equities traded on Island ECN, Hasbrouck and Saar (2002) found a lower proportion of limit orders in the arriving order flow during periods with higher volatility (using a variety of different volatility measures). Submitted limit orders had an increased probability of execution and a shorter expected time until execution during such periods. Furthermore, on Euronext (Chakraborti et al., 2011b) and for German Index Futures (Kempf and Korn, 1999), mid-price realized volatility increased with the number of arriving market orders. Jones et al. (1994) reported a similar finding in a study of the NYSE; however, Ellul et al. (2003) later reported a positive correlation between higher mid-price realized volatility and the percentage of arriving orders that were limit orders.

On the Australian Stock Exchange, Hall and Hautsch (2006) reported that the number of arrivals and cancellations of large limit orders (i.e., those whose size was in the upper quartile of the unconditional empirical distribution of order sizes) in any given -minute window was positively correlated with mid-price realized volatility during both that window and the previous -minute window. However, in a more recent study (Cao et al., 2008) concluded that mid-price realized volatility per trade had only a minimal effect on order flows.

A weak but positive correlation between and realized mid-price volatility has been observed in a wide range of markets (see Wyart et al. (2008) and references therein). However, a much stronger positive correlation between and mid-price volatility was observed at the trade-by-trade timescale on the Paris Bourse (Bouchaud et al., 2004), the FTSE 100 (Zumbach, 2004), and the NYSE (Wyart et al., 2008). In a recent study of stocks traded on the NYSE, Hendershott et al. (2011) reported that the once-daily time series of bid-price realized volatility was positively correlated with the daily mean spread. Stocks with a lower mid price had higher bid-price realized volatilty on average. In FX markets, Lo and Sapp (2010) reported that the variance of the depth available at any given price increased during periods of high mid-price realized volatility. Hasbrouck and Saar (2002) investigated links between volatility and various aspects of the depth profile on the Island ECN, but they found only weak relationships.

IV.6 Market impact and price impact

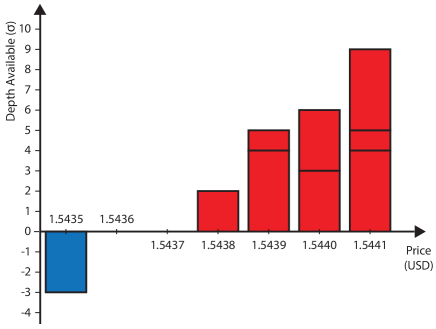

A key consideration for a trader who wishes to buy or sell a large quantity of an asset is how his or her actions might affect the asset’s LOB (Almgren and Chriss, 2001; Bouchaud et al., 2009; Cont et al., 2011; Eisler et al., 2012; Obizhaeva and Wang, 2013). For example, if trader wishes to buy shares using the LOB displayed in Figure 4, then submitting a single market order of size would result in purchasing shares at , shares at , shares at , and shares at . However, if were initially to submit only a market order of size , then it is possible that other traders might submit new limit orders, because by purchasing the shares with highest priority in the LOB, has made it more attractive for other participants to submit new sell limit orders than it was immediately before such a purchase. If this occurs, then could submit a market order that matches to these newly submitted limit orders and then repeat this process until all shares are purchased. Empirical observations suggest that such order splitting is very common in a wide range of different markets (Bouchaud et al., 2009). Of course, there is no guarantee that the initial market order of size would stimulate such submissions of limit orders from other traders. Indeed, it could even cause other traders to cancel their existing limit orders or to submit buy market orders, further increasing and thereby ultimately causing to pay a higher price for the total purchase of shares.