A unified approach to determining the early exercise boundary position at expiry for American style of general class of derivatives

Abstract

In this paper, we present a unified method for calculating the limit of early exercise boundary at expiry. We price American style of general derivative using a formula expressed as a sum of the value of European style of derivative and so called American premium. We use the latter expression to calculate an analytic formula for limit of early exercise boundary at expiry. Method applied on American style plain vanilla, Asian and lookback options yields identical results with already known values. Results for selected American style of derivative strategies are compared with limits calculated by the PSOR method.

Keywords: American style of derivative; early exercise boundary; limit at the expiry.

AMS-MOS classification: 91B28 JEL classification: C65, G13

1 Introduction

The growth of variety in financial derivatives traded on markets has increased the need for more general and more accurate valuation of their prices. The breakpoint in valuation methods for the financial derivatives is dated to early 70. of the century. The cornerstone laid by Black, Scholes and Merton in Black and Scholes (1973) and Merton (1973) or its modifications occur in majority of all pricing techniques. The well known Black-Scholes partial differential equation and the theory behind it are considered as an important basis in the financial engineering. However, the theory of valuation has undergone many changes since that time.

The most basic classification of the financial derivatives is according to their expiration time (one of the main properties). The European style of derivatives can be exercised only at the expiration time . On the other hand, by buying the American style of derivatives the holder obtains a right to exercise it at any moment by the expiration time. The early exercise boundary of financial derivative splits the (time–underlying) space into continuation region and stopping region . The derivative is exercised if spot value of the underlying is in the stopping region, i.e. , the derivative is held otherwise.

We created a unified approach for calculation of the analytic value of limit of the early exercise boundary at expiry. Note that position of the early exercise boundary at the expiry was already calculated for many particular cases of derivatives Albanese and Campolieti (2006), Alobaidi and Mallier (2006), Bokes and Ševčovič (2011), Chiarella and Ziogas (2005), Dai and Kwok (2006), Detemple (2006), Kwok (2008), Ševčovič (2008), Wilmott et al. (1995), Wu et al. (1999), etc. In this paper, we present theorem that generalizes these methods into one formula. It can be used to determine the limit of exercise boundary for American style of a general derivative that can be written in desired form (1).

In the second section of this paper, we summarize a method of valuation of the American style of derivatives driven by a Brownian motion (it can be used to calculate the value of a derivative in form required by following method). In the third section, we present the main result of the paper. The method of calculation of the limit of early exercise boundary is presented in Theorem 3.1. Next section consists of several examples where the method is applied on plain vanilla options, American style of their strategies, on the Asian and lookback options, shout options and British style of vanilla option. In the last section, we compare the position of early exercise boundary (of condor spread) calculated by our theorem and values calculated by the classical PSOR method.

2 Value of the American style of derivatives

In this paper, we analyze the American style of derivative with price given by the formula

| (1) |

where is the price of European style of derivative, is conditioned expected value according to the information at time , is the indicator function for stopping region and is American style bonus function. The value of an American style vanilla option in this form was first introduced by Kim (1990).

Remark 2.1

Price process of the American style derivative discounted by the numeraire is a supermartingale according to the risk neutral measure. It is the Snell envelope of the pay-off process discounted by the numeraire and (1) discounted by the numeraire is the Doob-Meyer decomposition of this supermartingale. For further details see (Karatzas and Shreve, 1988; Chapter 1).

As an example, we can assume an underlying driven by a stochastic differential equation

for on their domain . The values , and are drift, volatility and differential of standard -dimensional Brownian motion under the joined risk-neutral measure , respectively. The covariance matrix of is defined for by

where is the correlation coefficient and .

Let and be the pay-off function and the numeraire, respectively. The value of an American style of derivative on the underlying asset is then given by

where

and

The bonus function in (1) at expiry is then given by the expression

| (2) |

Values of on the set of zero measure where and are not differentiable are defined as the arithmetic average of limes superior and limes inferior at each point of this set.

3 Limit of the early exercise boundary at expiry

In this section, we determine the main result of the paper - the position of the early exercise boundary at expiry for a general class of financial derivatives. The result is stated for a wide class of integral equations for pricing American style of derivatives of the form (3). This problem has been already considered by many authors for American style of certain derivatives (e.g. Albanese and Campolieti, 2006; Alobaidi and Mallier, 2006; Bokes and Ševčovič, 2011; Chiarella and Ziogas, 2005; Dai and Kwok, 2006; Detemple, 2006; Kwok, 2008; Ševčovič, 2008; Wilmott et al., 1995; Wu et al., 1999). Presented method is a unified approach solving the generalized problem of finding the position of the early exercise boundary at expiry.

Let be a subset of Euclidean space . In what follows, we shall denote by a boundary of the set with respect to the topology , i.e. .

Theorem 3.1

Consider an American style of derivative on the underlying with the stopping and continuation regions defined by the open sets and , respectively. Let for be a (set of) manifold(s) of the early exercise boundary at time . Suppose that the value of is given by the equation

| (3) |

where denotes a price of the corresponding European style of derivative and is a function representing the early exercise bonus. Furthermore, we suppose that

| (4) |

where is the pay-off function at time for both American style and European style of derivative, i.e.

| (5) |

Then the limit of early exercise boundary at expiry is given by

| (6) |

where .

Lemma 3.1

Consider a mutually disjoint decomposition of a topological space , where . Moreover, consider a set so that , where is the closure of the set , then .

P r o o f: [of Lemma 3.1]

Let . For each , there exists a neighborhood so that and . This implies, that , i.e. , because , but .

Since and , we have and the proof of Lemma follows.

P r o o f: [of Theorem 3.1]

Part 1). First, we show that

We have

for any by (4). In the limit , we can omit the conditioned expected value operator and we obtain

If , then we obtain

Now suppose that there exists such that . Notice that in the stopping region we have the identity for any and, consequently, . Then we have

In the stopping region, exercising the derivative (American style) gives holder higher pay-off than keeping it (European style), i.e.

for sufficiently close to expiry . According to (5), the value of difference between European style of derivative and pay-off is increasing (from negative values to zero at maturity). The derivative of this difference is positive in the stopping region. This is a contradiction and the proof of first part follows.

Part 2). Now, we show that

The function can be determined on the stopping region by the following property

To span the function on the whole domain , we omit the function and we have

Notice, that the function nullifies movements from the pay-off function .

On the continuous region , the holder of a financial derivative does not want to exercise it, because keeping this derivative yields better pay-off, i.e.

for sufficiently close to expiry . According to (5), the value of difference between European style of derivative and pay-off is decreasing (from positive values to zero at maturity). The derivative of this difference is negative and so is the value of function in the continuation region. The function have positive values only on .

Remark 3.1

Notice, that according to the second part of the proof of Theorem 3.1, we can determine function of the American style bonus function at expiry by the formula

Remark 3.2

The limit of early exercise boundary analyzed in this paper is the expansion of the zeroth order. For several financial derivatives of American style, higher order expansion was already calculated. Further details on this expansion can be found in Dewynne et al. (1993), Ševčovič (2001), Wilmott et al. (1995) for plain vanilla the call option, in Stamicar et al. (1999), Zhu (2006), Zhu and He (2007) for the plain vanilla put option and in Bokes and Ševčovič (2011) for average strike Asian options.

4 Calculation of the early exercise boundary position at expiry

In this section, we calculate the limit of early exercise boundary at expiry for several types of American style of financial derivatives and their strategies. The underlying of all derivatives presented in this section is driven by a geometric Brownian motion. Theorem 3.1 does not have limitation on the distribution of underlying and can be used also in other models for underlying assets. The method can be used also e.g. on Lévy processes - the most simple approach is to apply Remark 3.1 (either analytically or numerically).

We use parameters , and to denote risk-free continuous interest rate, continuous dividend rate and volatility of underlying, respectively. The underlying asset is driven by stochastic differential equation

| (7) |

where is the Wiener process.

We present examples of application of presented method. Results for the most basic of them are well known (e.g. vanilla options or Asian options with arithmetic and geometric averaging). The position of early exercise boundary for many other derivatives is calculated by complicated methods or specified only by the argumentation without any mathematical formulation. However, we include the derivation for comparison purposes.

Some of the examples presented are American types of strategies of vanilla options. Trading these derivatives is not very common, we use them only to demonstrate Theorem 3.1 on more complex types of derivatives.

4.1 Plain vanilla options

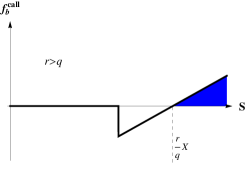

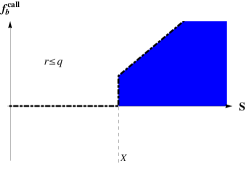

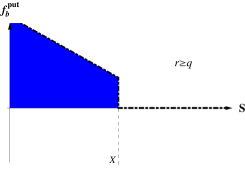

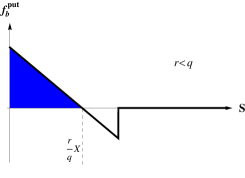

The European style of vanilla call/put option gives its holder right to buy/sell the underlying at maturity time for the expiration price . The position of the early exercise boundary at expiry for call and put vanilla option is equal to boundary of set of positive values of (see Figure 1) and (see Figure 2), i.e.

respectively. This result is well known and can be found also in Albanese and Campolieti (2006), Detemple (2006), Kwok (2008), Wilmott et al. (1995) and many other sources.

We derive the position of the early exercise boundary according to the method presented in this paper. The pay-off functions for call and put options are

respectively. The value of European style of vanilla option (the well known solution of Black-Scholes partial differential equation extended by Merton) for both call and put option is given by

| (8) | |||||

| (9) |

where .

We know the value of both pay-off function and European style of option, so we can calculate at the expiry according to Remark 3.1, i.e. for call option and put option we have

respectively.

4.2 Option strategies

There are many option strategies that can be considered. European style of these financial derivatives is linear combination of plain vanilla options, therefore the derivation is similar for all of them. The position of early exercise boundary at expiry is calculated only for very few of them. The results for American style strangle spread was presented by Alobaidi and Mallier (2006), Chiarella and Ziogas (2005).

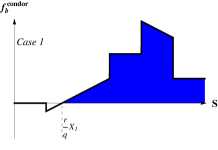

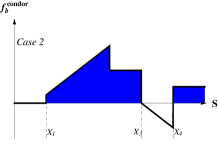

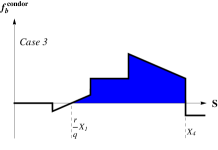

The most complex frequently used strategy consisting of vanilla options is European style of condor spread and its restriction butterfly spread. The European style of condor spread is a linear combination of four vanilla call options. There are three different cases, when determining the position of the early exercise boundary at expiry by the boundary of set of positive values of .

In the first case, if we have and , then the set of boundary points has only one element (see Figure 3 (left)).

In the second case, we have and . The set of boundary points has three elements (see Figure 3 (center)).

In the last case, we have and the set of boundary points has two elements (see Figure 3 (right)).

We present derivation for the position of the early exercise boundary at expiry for a condor spread according to the method presented in this paper. The pay-off function of a condor spread is

for , where the case is called a butterfly spread. The price of a European style of condor is calculated by the formula

where the function is defined by (8).

Once more, we use Remark 3.1 to calculate the bonus function for American style of condor spread.

4.3 Asian and lookback options

Options with some extra properties are usually called exotic options. Subgroup of exotic options called path-dependent options contains also Asian and lookback options. Asian and lookback options depends on some type of average () and the extreme value (maximum or minimum ) of the underlying through the lifespan of the option, respectively.

We calculate the value of limit at the expiry for American style of floating strike of both Asian and lookback options. The pay-off functions of floating strike Asian call, Asian put, lookback call and lookback put options are

respectively. Now, we use (2) to determine the bonus function . According to Hansen and Jorgensen (2000) we can use the numeraire . We define the general exponentially weighted average at time by the formula

where for regular and for weighted average. By setting the parameter to values , , and , we can construct expressions for continuous geometric average, continuous arithmetic average, minimum value and maximum value, respectively.

The function for call option and for put option has form

and

respectively. The value according to (7) and is drift of the stochastic differential equation

According to Hansen and Jorgensen (2000) and Bokes and Ševčovič (2011) we have the form of stochastic differential equation for geometric average

for the arithmetic average

and for both maximum and minimum the equation has form

Finally, the stochastic differential equation for the exponentially weighted general average has form

The bonus function at the expiry for call and put Asian options with continuous geometric average has form

and

respectively. The boundary of set of positive values is given by

and

where is the positive solution of transcendental equation

The solution is unique on for and .

The bonus function at the expiry for call and put Asian options with continuous arithmetic average has form

and

respectively. The boundary of set of positive values is given by

and

Finally, the bonus function at the expiry for call and put lookback options has form

and

respectively. The boundary of set of positive values is given by

and

The same results for the limit of early exercise boundary at expiry can be found in Detemple (2006), Wu et al. (1999) for geometric average Asian options, in Ševčovič (2008) for arithmetic average Asian options, in Dai and Kwok (2006) for arithmetic average Asian and lookback options and in Bokes and Ševčovič (2011) for both geometric and arithmetic Asian options.

This is the first time that the position of early exercise boundary at expiry for general average is mentioned in the literature. It can be derived similarly as the previous examples. The bonus function at the expiry for call and put Asian options with general exponentially weighted average has form

and

respectively. The boundary of set of positive values is given by

and

where is the positive solution of transcendental equation

The solution is unique on for and .

4.4 Shout options

Shout options are financial derivatives similar to European plain vanilla options. The difference is that the holder of a shout option can once during the life of derivative ”shout” to the writer, i.e. the option expires and the strike price is reset to actual spot price of the underlying asset. The shouting action is conditioned by in-the-money position of the option. According to this property, we need to know optimal shouting boundary along with the limit of the boundary at the expiry. The position of optimal shouting boundary at expiry, i.e. the boundary of set of positive values for call shout option is the same as for put shout option:

This result can be also found in Alobaidi et al. (2011). However, the value of this limit was derived only by argumentation and without any mathematical formulation.

Now, we present the derivation according to the Theorem 3.1. The pay-off function of call and put shout option is

and

respectively. The functions and are defined by (8) and (9), respectively.

Notice, that the underlying is under the same measure as for the vanilla option, thus we have the numeraire . In this case, we use the idea from (2) to determine the bonus function :

4.5 British vanilla options

The British vanilla option is financial derivative hedging the real trend of the underlying asset. This feature allows its holder to exercise the option prior to the expiry and receive the best prediction of the pay-off according to the real trend of underlying restricted to the contract drift .

The position of the early exercise boundary for British plain vanilla call and put option is equal to the boundary of set of positive values of and , i.e.

and

respectively. This result is consistent with the calculation presented in Peskir and Samee (2008a,b). However, the derivation presented in this paper is much shorter and straightforward.

Now, we present the derivation according to the method presented in this paper. The pay-off functions of call and put British vanilla option are

and

respectively. The function is standard normal cumulative distribution function and the expression .

Notice again, that the underlying is under the same measure as for the vanilla option, thus we have the numeraire . We can use the idea from (2) to determine the bonus function :

and

5 Verification by numerical method

In this section, we compare and verify analytic values of the limit of early exercise boundary with values calculated by the PSOR (projected successive over relaxation) method introduced in Elliot and Ockendom (1982). For further details on the PSOR method see Kwok (2008) or Wilmott et al. (1995). Values for plain vanilla options, Asian options and lookback options were derived in other sources. We present only the results of comparison for condor spread as a case with several different values of the limit at the expiry (results for all of the other examples are very similar).

In Table 1, we present values of the limit of early exercise boundary at expiry calculated by the PSOR method with 250 time and 40000 space steps. The space domain was bounded to the interval . The SOR was calculated with parameter and tolerance . The expiration time has to be chosen close to zero, we set the value in the calculation.

Each numerical value tends to analytic value calculated by the formulae presented in section 4. The numerical results are improving with increasing density of the time–space mesh and decreasing tolerance (as expected). The relative error of results with the highest precision is of the order .

| error | ||||||||||||||||||

| 1 | 3 | 4 | 5 |

|

|

|

||||||||||||

| 1 | 3 | 4 | 5 |

|

|

|

||||||||||||

| 1 | 2 | 3 | 4.5 |

|

|

|

6 Conclusions

In this paper, we presented a unified method for calculation of a limit of the early exercise boundary at expiry. The method is applicable for American style of a wide range of financial derivatives. We calculated and compared the analytic value of early exercise boundary limit for plain vanilla options as well as for Asian and lookback options. The results coincides with the well known values that can be found in Albanese and Campolieti (2006), Alobaidi and Mallier (2006), Bokes and Ševčovič (2011), Chiarella and Ziogas (2005), Dai and Kwok (2006), Detemple (2006), Kwok (2008), Ševčovič (2008), Wilmott et al. (1995), Wu et al. (1999) and in many other sources. Moreover, we also calculated the analytic value of the limit for shout option and American style of exponentially weighted floating strike Asian option with general average, British vanilla option and option strategies (represented by condor spread). We verified values by their comparison with values calculated by the PSOR method. Presented straightforward method is simple and unifies the approach to methods so far used for the calculation of limit of exercise boundary.

Acknowledgments

This research was supported by VEGA 1/0381/09 and APVV SK-BG-0034-08 grants.

References

- [1] Albanese, C. & Campolieti, G. (2006). Advanced derivatives pricing and risk management. Theory, tools and hands-on programming application, Elsevier, London.

- [2] Alobaidi, G. & Mallier, R. (2006). The American straddle close to expiry, Boundary Value Problems 2006, 1–14.

- [3] Alobaidi, G., Mallier, R. & Mansi, S. (2011). Laplace transforms and shout options, Acta Mathematica Universitatis Comenianae 80(1), 79–102.

- [4] Black, F. & Scholes, M. (1973). The pricing of options and corporate liabilities, Journal of Political Economy 81, 637–654.

- [5] Bokes, T. & Ševčovič, D. (2011). Early exercise boundary for American type of floating strike Asian option and its numerical approximation, Applied Mathematical Finance.

- [6] Chiarella, C. & Ziogas, A. (2005). Evaluation of American strangles, Journal of Economic Dynamics and Control 29(1-2), 31–62.

- [7] Dai, M. & Kwok, Y. K. (2006). Characterization of optimal stopping regions of American Asian and lookback options, Math. Finance 16(1), 63–82.

- [8] Detemple, J. (2006). American-Style Derivatives: Valuation and Computation, Chapman and Hall/CRC, Boca Raton.

- [9] Dewynne, J. N., Howison, S. D., Rupf, I. & Wilmott, P. (1993). Some mathematical results in the pricing of American options, European J. Appl. Math. 4(4), 381–398.

- [10] Elliot, C. M. & Ockendom, J. R. (1982). Weak and Variational Methods for Free and Moving Boundary Problems, Pitman.

- [11] Hansen, A. T. & Jorgensen, P. L. (2000). Analytical valuation of American-style Asian options, Management Science 46(8), 1116–1136.

- [12] Karatzas, I. & Shreve, S. E. (1988). Brownian Motion and Stochastic Calculus, Springer-Verlag, New York.

- [13] Kim, I. J. (1990). The Analytic Valuation of American Options, The Review of Financial Studies 3(4), 547–572.

- [14] Kwok, Y. K. (2008). Mathematical models of financial derivatives, Springer Finance, second edn, Springer-Verlag, Berlin.

- [15] Merton, R. C. (1973). The theory of rational option pricing, Bell Journal of Economics and Management Science 4, 141–183.

- [16] Peskir, G. & Samee, F. (2008a). The British call option, Probab. Statist. Group Manchester (Research Report) 2, 24 pp.

- [17] Peskir, G. & Samee, F. (2008b). The British put option, Probab. Statist. Group Manchester (Research Report) 1, 23 pp.

- [18] Ševčovič, D. (2001). Analysis of the free boundary for the pricing of an American call option, European J. Appl. Math. 12(1), 25–37.

- [19] Ševčovič, D. (2008). Transformation methods for evaluating approximations to the optimal exercise boundary for a linear and nonlinear Black-Scholes equation, in M. Ehrhardt (ed.), Nonlinear Models in Mathematical Finance: New Research Trends in Option Pricing, Nova Science Publishers, Inc., Hauppauge, pp. 153–198.

- [20] Stamicar, R., Ševčovič, D. & Chadam, J. (1999). The early exercise boundary for the American put near expiry: numerical approximation, Canad. Appl. Math. Quart. 7(4), 427–444.

- [21] Wilmott, P., Howison, S. & Dewynne, J. (1995). The mathematics of financial derivatives, Cambridge University Press, Cambridge. A student introduction.

- [22] Wu, L., Kwok, Y. K. & Yu, H. (1999). Asian options with the American early exercise feature, International Journal of Theoretical and Applied Finance 2(1), 101–111.

- [23] Zhu, S. P. (2006). A new analytical approximation formula for the optimal exercise boundary of American put options, International Journal of Theoretical and Applied Finance 9(7), 1141–1177.

- [24] Zhu, S. P. & He, Z. W. (2007). Calculating the early exercise boundary of American put options with an approximation formula, International Journal of Theoretical and Applied Finance 10(7), 1203–1227.