Adlakha and Johari \RUNTITLEMean Field Equilibrium in Dynamic Games with Complementarities

Mean Field Equilibrium in Dynamic Games with Complementarities

Sachin Adlakha \AFFDepartment of Electrical Engineering, Stanford University, Stanford, CA, 94305, \EMAILadlakha@stanford.edu \AUTHORRamesh Johari \AFFDepartment of Management Science and Engineering, Stanford University, Stanford, CA, 94305, \EMAILramesh.johari@stanford.edu

We study a class of stochastic dynamic games that exhibit strategic complementarities between players; formally, in the games we consider, the payoff of a player has increasing differences between her own state and the empirical distribution of the states of other players. Such games can be used to model a diverse set of applications, including network security models, recommender systems, and dynamic search in markets. Stochastic games are generally difficult to analyze, and these difficulties are only exacerbated when the number of players is large (as might be the case in the preceding examples).

We consider an approximation methodology called mean field equilibrium to study these games. In such an equilibrium, each player reacts to only the long run average state of other players. We find necessary conditions for the existence of a mean field equilibrium in such games. Furthermore, as a simple consequence of this existence theorem, we obtain several natural monotonicity properties. We show that there exist a “largest” and a “smallest” equilibrium among all those where the equilibrium strategy used by a player is nondecreasing, and we also show that players converge to each of these equilibria via natural myopic learning dynamics; as we argue, these dynamics are more reasonable than the standard best response dynamics. We also provide sensitivity results, where we quantify how the equilibria of such games move in response to changes in parameters of the game (e.g., the introduction of incentives to players).

1 Introduction

This paper studies a class of games that exhibit strategic complementarities between players. A strategic complementarity exists if, informally, “higher” actions by other players increase the return to higher actions for a given player. Games with strategic complementarities are a powerful modeling tool, applicable in a wide range of situations, including: systems with positive network effects (such as network security models, recommender systems, and social networks); coordination problems; dynamic search in markets; social learning; and oligopoly models (e.g., quantity or price competition with complementarities).

Our focus in this paper is on dynamic games with strategic complementarities. Strategic complementarities have long provided a fertile analytical ground for static game theoretic models; see, e.g., Milgrom and Roberts (1990), Vives (1990), and Topkis (1998). However, the literature on dynamic games with complementarities has emerged relatively recently by comparison. Much of the attention in prior work on such games has focused on developing existence proofs for equilibrium; see, e.g., Curtat (1996), Amir (2002, 2005), Sleet (2001), Vives (2009) for these results.

In this paper we consider a class of dynamic games referred to as stochastic games; in these games agents’ actions directly affect underlying state variables that influence their payoff (Shapley 1953). The standard solution concept for stochastic games is Markov perfect equilibrium (Fudenberg and Tirole 1991). Despite the previously cited existence results for Markov perfect equilibria in games with complementarities, there remain two significant obstacles, particularly as the number of players grows large. First is computability: the state space of the preceding games expands in dimension with the number of players, and thus the “curse of dimensionality” kicks in, making computation of Markov perfect equilibria essentially infeasible (Pakes and McGuire 2001, Doraszelski and Pakes 2007). Second is plausibility: as the number of players grows large, it becomes increasingly difficult to believe that individual players track the exact behavior of the other agents. Rather than treat the growth of the population as an impediment to analysis, this paper addresses these obstacles by exploiting an asymptotic regime where the number of players grows large to simplify analysis of equilibria.

We consider an approximation methodology where agents optimize only with respect to long run average estimates of the distribution of other players’ states, that we refer to as mean field equilibrium; this notion has been utilized across a range of work in economics, operations research, and control (as we discuss below). In a mean field equilibrium, individuals take a simpler view of the world: they postulate that fluctuations in the empirical distribution of other players’ states have “averaged out” due to large scale, and thus optimize holding the state distribution of other players fixed. Mean field equilibrium requires a consistency check: the postulated state distribution must arise from the optimal strategies agents compute.

Our results provide valuable insight into the structure of mean field equilibria in such games, as well as computational tools to determine such equilibria. To motivate our results, we first provide several examples of stochastic games with complementarities where the approach taken in this paper applies. These examples—particularly the first four—often exhibit large numbers of players, and thus the benefits of mean field equilibrium are significant. We demonstrate in Section 8 that each of these examples can be analyzed using the results we develop in this paper.

Example 1.1 (Interdependent security)

In interdependent security games, as introduced in Kunreuther and Heal (2003), a large number of agents make individual decisions about their own security. However, the ultimate security of an agent depends on the security decisions made by other agents. For example, imagine a network of computers where each individual user makes an investment in keeping her own machine secure. This investment may be in the form of advanced anti-virus filters, firewalls, etc. While these investments improve the security of the individual computer, it can still be affected if the other computers in the network are not properly secured. In the interdependent security games we consider, agents take actions at some cost to improve their own security level, and earn a payoff each period that depends on whether or not a security breach occurs. The fact that the probability of a security breach is influenced by others’ security levels introduces strategic complementarities into the stochastic game. \halmos

Example 1.2 (Collaborative filtering)

Many large online recommendation systems, such as those used by Netflix and Amazon, rely on collaborative filtering. In such systems, if an individual puts forth greater effort in maintaining their profile, the recommendations they receive will improve. However, the recommendations other individuals receive improve as well, and typically other individuals will feel a stronger incentive to exert additional effort to maintain their profile in this case. In the absence of such effort, the profile of an agent becomes stale and useless both to her and others in the system. Thus collaborative filtering systems exhibit strong strategic complementarities. \halmos

Example 1.3 (Dynamic search with learning)

In dynamic search models, traders in a market exert effort to find trading partners (Diamond 1982). Such models are commonly used to study, e.g., decentralized matching in labor markets. We consider a model where at each time step, traders also gain experience by exerting effort; this experience makes future effort more productive. Of course traders’ experience increases as they put forth more effort; but their experience also increases as others put forth more effort since this increases the likelihood of useful interactions per unit effort. This creates strategic complementarities between the players; such a model was considered by Curtat (1996). \halmos

Example 1.4 (Coordination games)

There exist many examples in operations and economics where agents are trying to coordinate on a common goal; for example, this is the case when firms try to coordinate on a common standard. In a coordination game, a collection of agents take individual actions to converge on a common state. One such stylized model is the linear-quadratic decentralized coordination problem studied by Huang et al. (2005). Agents can change their state by exerting effort at some cost. Further, each agent incurs an additional state-dependent cost each time period; this cost is quadratic in the distance to the average of other agents’ states. This type of game can be shown to exhibit strategic complementarities between agents. \halmos

Example 1.5 (Oligopolies and complementary goods)

Consider competition among firms producing complementary goods. In particular, suppose firms have effective monopolies in their own markets, but that their goods are complements, so that the consumption of one good will increase the demand and consumption of others. Such models naturally exhibit strategic complementarities.

One potential issue in using mean field models to analyze oligopolies with complementary goods is that the number of firms may not be too large, thus raising questions about the validity of a mean field limit in the first place. However, even in such a setting mean field models have value, because they provide structural insight into optimal strategies under a model of rationality that is perhaps more plausible, as discussed above. Indeed, econometric analysis using mean field models of dynamic oligopolies has proven valuable for a range of industries with relatively small numbers of firms (see Weintraub et al. (2010) for examples). \halmos

Our main results provide conditions that ensure existence of mean field equilibria in stochastic games with complementarities. We also establish that simple learning procedures converge to equilibria, and provide insight into sensitivity of equilibria to parameter changes. We consider a general class of models with parsimonious assumptions over model primitives that ensure strategic complementarities. In particular, our model class allows players to be coupled both via their payoff function and state transitions, i.e., players’ payoffs and state transitions can depend on states or actions of other players. We also discuss extensions of our results to models with multidimensional state and action spaces, and with heterogeneity among players. Details of our results follow.

-

1.

Structural characterization of mean field equilibrium. We establish existence of a mean field equilibrium in a general stochastic game model using lattice theoretic techniques. Lattice theoretic methods are typically applied in games with complementarities; the key techniques we use are due to Tarski (1955), Kamae et al. (1977), Hopenhayn and Prescott (1992), Zhou (1994), and Topkis (1998). Despite the use of lattice theoretic techniques in our analysis, existence of equilibria in our game cannot be inferred from existence results for other games in the literature. Moreover, we show that there exists a “largest” and “smallest” equilibrium among the set of all mean field equilibria with nondecreasing strategies. Thus, in particular, there is a natural dominance relationship among the mean field equilibria of a given stochastic game with complementarities. This is particularly valuable in dynamic games, because our characterization applies to the distribution of states of agents in equilibrium.

We note that prior literature has established existence of equilibrium in stochastic games with complementarities; however, these results typically also require use of topological fixed-point theorems such as Kakutani’s theorem (Curtat 1996, Amir 2002, 2005). More closely related to our paper is the work of Sleet (2001), who considers mean field equilibria of a dynamic price-setting game with stochastic, exogenous firm-specific demand shocks per period. The general analytical techniques in this paper can be applied to recover the existence result for that game.

-

2.

Convergence to equilibrium. We provide two convergence results. First, we study a standard best response dynamic (BRD). In this algorithm, at each time step, each agent computes the stationary population state distribution that would be induced by the current strategies of others, and in turn computes the best response to that state distribution. Using monotonicity properties derived in establishing the existence of mean field equilibrium, we show that BRD converges.

However, BRD is unsatisfying both computationally and practically. From a computational standpoint, BRD requires computation of a stationary distribution given the current strategy choices of agents in the system; this is in principle a complex procedure to execute at each iteration. More importantly, BRD is an implausible approach to play in an actual game: it is unlikely that agents would explicitly compute the stationary distribution their competitors would obtain.

Instead, we consider a more a natural form of myopic learning dynamics (MLD) among the players; convergence of MLD is a central insight of our paper. In particular, suppose that initially, each agent starts at the lowest (resp., highest) possible state. At each time step, agents observe the current empirical population state distribution, and conjecture that this distribution will remain constant for all time; with this conjecture they compute an optimal strategy, and play in the next period according to that strategy. At the next time step, the state distribution will evolve, and agents repeat the same heuristic. We show that this dynamic converges to the lowest (resp., highest) mean field equilibrium among all equilibria with nondecreasing strategies.

Note that MLD resolves both the computability and plausibility issues raised above. First, it is a natural, simple, implementable algorithm for finding a mean field equilibrium; indeed, MLD has some similarities with model predictive control or receding horizon control (Garcia et al. 1989), both popular approaches to complex dynamic control problems. Second, it corresponds to a learning dynamic that demands only a weak form of rationality and forecasting from the players, and yet yields an equilibrium in the limit.

-

3.

Separable stochastic games. Although appealing, the general theory does pose some significant issues in application: the complementarity requirements on model primitives may preclude important and interesting cases of practical interest. Complementarity is a strong requirement, but also brittle: a model that does not appear to satisfy the assumptions a priori may do so through a judicious change of variables. We employ this fact to show that a range of games that do not satisfy the assumptions of our baseline model can be studied by a suitable change of variables, provided that the payoff is separable in the state and action of a given player—often a relatively mild assumption. Notably, models with linear dynamics fall in this class. This greatly expands the set of models that can be analyzed within our framework.

-

4.

Sensitivity. Finally, essentially for free, the complementarity structure allows us to analyze changes in the equilibrium in response to changes in parameters of the game. In particular, we can predict shifts (in a first order stochastic dominance sense) of the equilibrium state distribution of players in response to exogenous parameter changes. Such sensitivity analysis, or comparative statics, allows our model to address, e.g., the value of incentives to increase security levels, or the value of increasing the quality of recommendations by a given factor.

The remainder of the paper is organized as follows. In Section 2 we introduce our basic stochastic game model as well as the formal definition of mean field equilibrium. Notably, we also discuss a justification for the use of mean field equilibrium: that it approximates equilibria of finite games well. This approximation property has been developed in a variety of specific contexts in the past (see, e.g., Glynn 2004, Huang et al. 2006, Weintraub et al. 2008, and Tembine et al. 2009), and in our context we apply the methodology developed in Adlakha et al. (2010) (inspired by Weintraub et al. 2008) to justify mean field equilibrium as a limiting notion of equilibrium.

Next, in Section 3, we define stochastic games with complementarities. We then prove our first main result: that a mean field equilibrium exists for a stochastic game with complementarities. In Section 3.2, we show that equilibria are “ordered,” in the sense that there exists a smallest and largest mean field equilibrium among all those where the equilibrium strategy is nondecreasing. In Section 4, we prove convergence of both the BRD and MLD algorithms described above. We also discuss the performance of MLD in finite systems.

In Section 5, we provide comparative statics results for the games under consideration. In Section 6, we extend our results to cover games where players’ payoffs and transition kernels may depend on the actions of others, rather than their states. In Section 7 we consider separable stochastic games with complementarities (as described above), and establish that these are a special case of our basic model of stochastic games with complementarities.

In Section 8, we revisit each of the examples described above. In particular, we provide formal verification that these examples satisfy the assumptions made in the paper to obtain existence and convergence results. Finally, in Section 9, we study a particular instance of an interdependent security game. We use this game to illustrate several computational insights, including verification of comparative statics results, as well as exploration of the performance of the MLD dynamic described above. Section 10 concludes with a discussion of extensions to include both player heterogeneity (i.e., type information) and multidimensional state and/or action spaces.

We conclude by surveying related work on mean field equilibrium. The notion of mean field equilibrium is inspired by mean field models in physics, where large systems exhibit macroscopic behavior that is considerably more tractable than their microscopic description. (See, e.g., Mézard and Montanari (2009) for background, and Blume (1993) and Morris (2000) for related ideas applied to static games.) In the context of stochastic games, mean field equilibrium and related approaches have been proposed under a variety of monikers across economics and engineering; see, e.g., studies of anonymous sequential games (Jovanovic and Rosenthal 1988, Bergin and Bernhardt 1995); stationary equilibrium (Hopenhayn 1992); dynamic stochastic general equilibrium in macroeconomic modeling (Stokey et al. 1989); Nash certainty equivalent control (Huang et al. 2006, 2007); mean field games (Lasry and Lions 2007); oblivious equilibrium (Weintraub et al. 2008, 2010); and dynamic user equilibrium (Friesz et al. 1993, Wunderlich et al. 2000). Mean field equilibrium has also been studied in recent works on information percolation models (Duffie et al. 2009), sensitivity analysis in aggregate games (Acemoglu and Jensen 2009), coupling of oscillators (Yin et al. 2010), and in scaling behavior of markets (Bodoh-Creed 2010).

2 Model and Definitions

In this section we begin with preliminaries. We define a general model of a stochastic game in Section 2.1; in the games we consider, agents take actions to update their own states, and their payoffs and state transitions may be affected by the states of others. Next, in Section 2.2, we define mean field equilibrium, and in Section 2.3 we provide a formal justification for mean field equilibrium as an approximation to equilibria in games with a large finite number of players. Finally, in Section 2.4, we discuss lattice-theoretic preliminaries necessary for the analysis in the sequel.

2.1 Stochastic Games

We consider a game played among players. A stochastic game is a tuple defined as follows.

Time. The game is played in discrete time, with time periods by .

State. The state of player at time is denoted by , where is compact. We use to denote the state of all players except player at time .

Action. The action taken by player at time is denoted by . The set of feasible actions when the player is in state is a compact set . We let , and assume that is compact as well.

Transition probabilities. The state of a player evolves according to the following Markov process. If the state of player at time is , the player takes an action at time , and the state of every other player at time is , then the next state is distributed according to the Borel probability measure , where for Borel sets ,

| (1) |

Further, given , , and , the next state is conditionally independent of all other past history of the game.

Payoff. The single period payoff to player at time is . Note that all players have the same payoff, and it is independent of the actions taken by other players.

Discount factor. The players discount their future payoff by a discount factor . Thus a player ’s infinite horizon payoff is given by:

It may initially appear unusual that we do not include the number of players as part of the specification of the game; however, this choice is deliberate. We ultimately study in a limiting regime where the number of players grows large, and as a result, mean field equilibrium is defined without regard to a fixed finite number of players. For this reason we do not include in the tuple defining . (See the next section for further discussion of the motivation for mean field equilibrium.)

In the model described above, the players are coupled to each other via their state evolution and the payoff function. In a variety of games, this coupling between players is independent of the identity of the players. The notion of anonymity captures scenarios where the interaction between players is via aggregate information about the state. Let denote the fraction of players (excluding player ) that have their state as at time , i.e.:

| (2) |

where is the indicator function that the state of player at time is . We refer to as the population state at time (from player ’s point of view).

Definition 2.1 (Anonymous Stochastic Game)

A stochastic game is called an anonymous stochastic game if the transition probability measure and payoff for player depend on only through . Through an abuse of notation, we write the transition probability measure as and the payoff function of player as .

The examples discussed in the Introduction naturally belong to the class of anonymous stochastic games. For example, in the interdependent security model (Example 1.1), it is natural to assume that a single player’s payoff is affected by the empirical distribution of security levels of other players in the network, but not by their specific identity. The same assumption is also plausible for the other examples presented earlier.

For the remainder of the paper, we focus our attention on anonymous stochastic games. For ease of notation, we often drop the subscript and to denote a generic transition probability measure and a generic payoff, i.e., we denote a generic transition probability measure by and a generic payoff by , where represents the population state of players other than the player under consideration. We let denote the set of all Borel probability measures on .

2.2 Mean Field Equilibrium

In a game with a large number of players, we might expect that fluctuations of players’ states “average out”, and hence the actual population state remains roughly constant over time. Because the effect of other players on a single player’s payoff is only via the population state, it is intuitive that, as the number of players increases, a single player has negligible effect on the outcome of the game. This intuition is formalized through the notion of mean field equilibrium (Jovanovic and Rosenthal 1988, Bergin and Bernhardt 1995, Hopenhayn 1992, Stokey et al. 1989, Friesz et al. 1993, Huang et al. 2006, 2007, Lasry and Lions 2007, Weintraub et al. 2008, 2010, Adlakha et al. 2010, Bodoh-Creed 2010).

In mean field equilibrium, each player optimizes its payoff based on only the long-run average population state. Thus, rather than keep track of the exact population state, a single player’s action depends only on her own current state as well as the long run average population state. This is motivated by the fact that a single player need not concern herself with the fine scale dynamics of competitors’ specific states. Given this simplified player behavior, note that each player must solve a dynamic program to determine their optimal strategy; the strategy chosen by each player then leads to a long-run average population state. Mean field equilibrium requires that the latter long-run average population state matches the original conjecture made by the players.

Note that in a mean field equilibrium, because players optimize holding the population state constant, their optimal strategies will depend only on their current state. We call such players oblivious, and refer to their strategies as oblivious strategies. This approach does not require players to be aware of each others’ exact states, if every player is aware of the long-run average population state. Furthermore, observe that if all players are oblivious, players’ states evolve independently.

In this section we fix an anonymous stochastic game . Formally, an oblivious strategy is a strategy that depends only on the player’s current state. We let denote the set of oblivious strategies.

Definition 2.2

Let be the set of oblivious strategies available to a player:

| (3) |

Given an oblivious strategy , a player takes an action at time . If the player conjectures the aggregate population state to be , then she also conjectures that her next state is randomly distributed according to the transition probability measure :

| (4) |

where is the conjectured long run average population state.

We define the oblivious value function to be the expected net present value for any player with initial state , when the long run average population state is conjectured to be , and the player uses an oblivious strategy . We have

| (5) |

Given a population state , a player computes an optimal strategy by maximizing their oblivious value function. Note that because the oblivious value function does not track the evolution of the population state, we should expect a player’s optimal strategy to depend only on their current state—i.e., it must be oblivious. We capture this optimization step via the operator defined next.

Define as:

Definition 2.3

The operator maps a distribution to the set of optimal oblivious strategies. That is, if and only if

Note that in principle, may be empty, though we show that under our assumptions this does not occur.

Now suppose that all players use the oblivious strategy , and the long run average population state drives their state dynamics. In this scenario, we expect the long run population state to be an invariant distribution of the strategy under the dynamics

| (6) |

We capture this relationship via the operator , defined next.

Definition 2.4

The operator maps an oblivious strategy and a distribution to the set of invariant distributions associated with the dynamics (6).

Thus, if and only for all Borel sets ,

| (7) |

Note that the image of the operator is empty if the strategy does not result in an invariant distribution, though again, we show under our assumptions that this does not occur.

We can now define mean field equilibrium. If every agent conjectures that is the long run population state, then every agent would prefer to play an optimal oblivious strategy . On the other hand, if every agent plays , and the long run population state is indeed , then must also be an invariant distribution of (6). Thus mean field equilibrium requires a consistency condition: the invariant distribution under and should be exactly .

Definition 2.5 (Mean Field Equilibrium)

A strategy and a distribution constitute a mean field equilibrium if and .

2.3 The Approximate Markov Equilibrium Property

A natural question that arises in the context of mean field equilibrium is whether it is a good approximation to a game with finitely many players. Here we present a formal justification for the notion of mean field equilibrium by considering explicitly a limiting regime where the number of players grows large.

Recall that we defined initially as a stochastic game with players. The standard solution concept for stochastic games is Markov perfect equilibrium. In a Markov perfect equilibrium, players’ strategies depend on their own current state, as well as the current states of others; we refer to such strategies as cognizant strategies. This larger state space makes Markov perfect equilibrium a much more complex equilibrium concept: Markov perfect equilibrium is typically quite challenging to compute, and demands far greater rationality on the part of the players.

It can be shown, however, that under appropriate assumptions, a mean field equilibrium is approximately a Markov perfect equilibrium as the number of players grows large. Formally, let be a mean field equilibrium, and fix a single player . Suppose that we consider a sequence of games with , where all players other than player use the oblivious strategy ; and where the initial state of all players other than player is sampled i.i.d. from . Then we can show that as , the difference between the payoff player achieves by playing and the maximum possible payoff player can achieve by playing any cognizant strategy approaches zero almost surely, for all initial states of player . Thus, in particular, is approximately optimal for player in a large finite game. A weaker version of this property, called the approximate Markov equilibrium property, was introduced by Weintraub et al. (2008); a similar notion is also studied by Glynn (2004), Huang et al. (2005), Tembine et al. (2009) and Bodoh-Creed (2010).

In order for this approximation property to hold, the key requirement is that the model primitives and must be jointly continuous in and , and the payoff function must be uniformly bounded. The intuition is that, essentially, the desired approximation property amounts to a continuity property in the value function of a player. We refer the reader to our companion paper Adlakha et al. (2010) for details of this type of result in the case of discrete state spaces. Independently of our own work, Bodoh-Creed (2010) has also derived similar conditions to ensure that mean field equilibrium approximates Markov perfect equilibrium well, over compact continuous state spaces.

For the remainder of the paper, we only study stochastic games in the limiting regime where the number of players grows large. In particular, we focus on existence of, and convergence to, mean field equilibrium. In Section 3, we establish that a mean field equilibrium always exists for stochastic games with complementarities.

2.4 Lattice-Theoretic Preliminaries

This section contains an overview of some basic definitions and notation used in the remainder of the paper. Our development requires some basic concepts from the theory of lattices. Given a partially ordered set with order , an element is called an upper bound of if for all ; similarly, is called a lower bound of if for all . We say that is a supremum or least upper bound of in if is an upper bound of , and for any other upper bound of , we have . In this case we write . We similarly define infimum (or greatest lower bound), and denote it by . The partially ordered set is a lattice if for all pairs , the elements and exist in . The lattice is a complete lattice if in addition, for all nonempty subsets , the elements and exist in .

If is a lattice, a function is supermodular if for every pair . If is also a lattice, a function has increasing differences in and if for all , , there holds . Finally, a correspondence is nondecreasing if whenever , , and , there holds , and . (For more detail on lattice programming, the reader is referred to Topkis (1998).)

Throughout this paper, we view and as lattices in the usual ordering; since these spaces are both compact subsets of , the corresponding lattices are complete (Topkis 1998). We also view the set of strategies as a lattice, under the coordinate ordering : i.e., if and only if for all .

In addition, recall that we let denote the set of all Borel probability measures on . We view as a lattice with the (first order) stochastic dominance ordering; formally, we write if and only if:

for all nondecreasing, bounded, measurable functions on (where the integral is the Riemann-Stieltjes integral). It is straightforward to show that this condition is equivalent to , where (resp., ) is the cumulative distribution function of (resp., ). It is well known that is a lattice: the lattice supremum (resp., the lattice infimum ) is found by the pointwise infimum (resp., supremum) of the corresponding distribution functions. Because is compact, it is straightforward using an analogous argument to verify that is a complete lattice (Echenique 2003).

We conclude by defining some properties of parameterized distributions we require in the sequel. Let denote a family of measures in , parameterized by , where is a lattice. Then we say is stochastically nondecreasing in if whenever is larger than , . Similarly, let denote a family of measures in parameterized by and , where both and are lattices. Then we say that has stochastically increasing differences in and if the expectation has increasing differences in and , for every nondecreasing, bounded, measurable function on .

3 Existence of Mean Field Equilibria

In this section and the following section, we consider a baseline model of stochastic games with complementarities, in which we prove existence and convergence results. In this section we establish our first main result: that there exists a mean field equilibrium for the stochastic game with complementarities. We also show an ordering result: there exists a “largest” and a “smallest” equilibrium among the set of all mean field equilibria with nondecreasing strategies.

We have the following definition.

Definition 3.1

A stochastic game with complementarities is a stochastic game that satisfies the following properties.

-

1.

Nondecreasing and supermodular payoff. The payoff is nondecreasing in , continuous in , and supermodular in . Furthermore, for fixed and , .

-

2.

Payoff complementarity. The payoff function has increasing differences in and .

-

3.

Monotone and supermodular transition kernel. The transition kernel is stochastically supermodular in and is stochastically nondecreasing in each of , , and . Further, is continuous in (w.r.t the topology of weak convergence on ).

-

4.

Transition kernel complementarity. The transition kernel has stochastically increasing differences in and .

-

5.

Monotone action set. The correspondence is nondecreasing in . Further, is nondecreasing in for all fixed .

-

6.

Countable noise. For each , , and , the support is countable.

The first assumption is natural for a range of models—if larger states are more valuable, then the payoff function will be nondecreasing in the state. The boundedness assumption on the payoff will be trivially satisfied if, e.g., is an interval and the payoff is continuous in . The second assumption ensures that there are complementarities between the state and action of a single player and the population state of other players. The next three assumptions create complementarities between state and action, as well as ensure that larger states and/or larger actions now are more likely to lead to larger states in the future. The last assumption is made to simplify later dynamic programming arguments; in particular, it allows us to ignore measurability issues when considering optimal strategies (Bertsekas and Shreve 1978). We note that if the payoff and transition kernel are continuous, then countability becomes unnecessary for our analysis, since we can restrict attention to optimal strategies that are continuous in the state.

While it may be straightforward to verify whether a payoff function exhibits the desired complementarity properties, the same verification is somewhat more challenging for the transition kernel. Thus before continuing, we provide an example of a transition kernel that exhibits the complementarity conditions required in Definition 3.1.

Example 3.2 (Mixture dynamics)

Suppose that is defined as follows:

| (8) |

Here and are both distributions on , such that first order stochastically dominates , and . If is nondecreasing in , , and , supermodular in , and has increasing differences in and , then it can be checked that the expectation of (8) against any nondecreasing function satisfies all the conditions of Definition 3.1. As one example of a that satisfies these properties, suppose:

where is the mean of . Such dynamics are commonly used in the context of games with strategic complementarities (Curtat 1996). \halmos

Informally, how might we expect players to behave in such a game? Observe that if other players have a larger population state, this increases the return to a larger state for a given player. In order to achieve a larger state, a player must take a larger action; but this also increases the likelihood of larger states in the future. All these effects conspire to create a situation where, when players are confronted with larger population states, they are likely to take higher actions. This monotonicity drives our analysis.

For the remainder of the section we fix a stochastic game with complementarities . Let denote the composition of and for the game : . A fixed point of identifies a mean field equilibrium of . Intuitively, under the assumptions we have made we might expect to be a monotone map; i.e., larger initial conjectures about the population state should lead players to take higher actions, which should in turn lead to a larger invariant distribution. Tarski’s fixed point theorem ensures monotone functions on a lattice have a fixed point.111Note that although Tarski’s theorem applies to functions, in our case is a correspondence. Zhou (1994) provides a generalization of Tarski’s theorem to correspondences.

Theorem 3.3 (Tarski 1955)

Suppose that is a nonempty complete lattice, and is a nondecreasing function. Then the set of fixed points of is a nonempty complete lattice.

We proceed to show that is monotone by showing that each of two correspondences and are monotone (with respect to the coordinate ordering on strategies in , and the first order stochastic dominance ordering on ).

Our main result in this section is the following theorem.

Theorem 3.4

There exists a mean field equilibrium for the stochastic game with complementarities .

In the next section, we sketch a proof of this theorem; and in Section 3.2, we show that if we restrict attention to equilibria where the strategy is nondecreasing, then there exists a “largest” equilibrium and a “smallest” equilibrium.

3.1 Theorem 3.4: Proof Sketch

We sketch the proof of Theorem 3.4; each step is filled in by the lemmas in the appendix.

-

Step 1.

We show is nonempty, and that optimal strategies can be identified via Bellman’s equation (Lemma 11.1).

- Step 2.

-

Step 3.

We use the complementarity properties of the previous step to show that the strategies and are nondecreasing in the state , where:

(9) We also show that and are nondecreasing in . (These facts are shown in Lemma 11.9).222See also Hopenhayn and Prescott (1992), Topkis (1998) and Smith and McCardle (2002) for other conditions that yield monotonicity of optimal solutions to dynamic programs.

- Step 4.

-

Step 5.

We conclude that the functions and are nondecreasing in , where:

(11) Thus both and possess fixed points by Tarski’s theorem (Lemma 11.15). These fixed points identify mean field equilibria.

3.2 Largest and Smallest Equilibria

Typically in games with supermodular structure, it is possible to show various ordering relationships among the equilibria. In particular, there is typically a “largest” and “smallest” equilibrium (Milgrom and Roberts 1990). In our setting, we might conjecture that the largest fixed point of (resp., the smallest fixed point of ) is the largest (resp., the smallest) mean field equilibrium of the stochastic game . However, this need not be the case: as seen above, monotonicity properties of the map are only inferred on the subset of strategies that are nondecreasing in the state. In general, such monotonicity properties might not hold over the entire strategy set—i.e., and may not be nondecreasing over the entire set . These monotonicity properties are necessary for establishing the ordering of equilibria in classical supermodular game theory.

From the discussion in the preceding paragraph, however, observe that if we restrict attention to nondecreasing strategies, then indeed an ordering result can be proven. In particular, the following corollary shows that any mean field equilibrium where the strategy is nondecreasing is bounded above by the largest fixed point of , and bounded below by the smallest fixed point of .

Corollary 3.5

Let be the largest fixed point of , and let be the smallest fixed point of , i.e.:

| (12) |

Let be any mean field equilibrium of the stochastic game with complementarities , where is nondecreasing. Then , and thus .

4 Convergence to Equilibrium

In this section we show that a mean field equilibrium can be obtained using a natural form of learning dynamics among the players. We start by considering a simple form of best response dynamics to compute equilibria, where we iteratively apply the maps and defined in (11). We argue that this process is unsatisfactory, both from a computational and modeling standpoint, and instead propose an alternate process we refer to as myopic learning dynamics; these dynamics are both computationally simpler and correspond to a natural learning behavior among the agents. We show that this process converges to mean field equilibria.

We fix a stochastic game with complementarities . Throughout this section we study in the limit of a continuum of agents, consistent with our definition of mean field equilibrium.

4.1 Best Response Dynamics

We start by considering the

following algorithm.

Algorithm L-BRD:

-

1.

Initialize the state of every agent to , and let denote the resulting population state—i.e., places all its mass on .

- 2.

-

3.

Repeat (2).

Here L-BRD denotes lower best response dynamics. Given a current population state, we compute the lowest best response of a player, and then compute the smallest invariant distribution corresponding to the resulting strategy. This is the simplest dynamic we might consider; since , we have . In spirit, this algorithm is similar to other best response dynamics that are common in the literature on supermodular games (Milgrom and Roberts 1990, Vives 1990).

We now show that this algorithm converges; and further, under an appropriate continuity condition, the limit point is the smallest mean field equilibrium. We have the following assumption.

The payoff function and the transition probability measure are both jointly continuous in their domains (where we endow with the topology of weak convergence).

The next proposition shows L-BRD converges; the proof follows by exploiting monotonicity of .

Proposition 4.1

Let be a stochastic game with complementarities. Define and iteratively according to Algorithm L-BRD. Then , and . Further, there exists a distribution and a strategy , nondecreasing in , such that converges weakly to as , and converges pointwise to as .

Thus under mild continuity conditions on the model primitives, best response dynamics converge to a mean field equilibrium. Further, the limit point is the smallest mean field equilibrium among all those where the equilibrium strategy is nondecreasing.

We conclude by noting that we can analogously define an upper best response

dynamic as follows.

Algorithm U-BRD:

-

1.

Initialize the state of every agent to ; let denote the resulting population state—i.e., places all its mass on .

- 2.

-

3.

Repeat (2).

The same conclusion as Proposition 4.1 holds for U-BRD as well, except that under Assumption 4.1, the limit point is the largest fixed point of , i.e., (cf. (12)).

We note that one alternative to L-BRD and U-BRD is presented by Sleet (2001). He suggests an algorithm based on iterative value and policy iteration to compute a mean field equilibrium of a dynamic price-setting game with stochastic, exogenous firm-specific demand shocks per period. The setting considered there is specialized, but the convergence proof also exploits monotonicity properties induced by complementarity conditions in that specific model.

4.2 Myopic Learning Dynamics

The preceding section establishes the desirable result that best response dynamics converge. However, in a dynamic context, iterative application of and is not completely satisfactory, whether viewed from a computational or modeling standpoint. First, given , computing or requires computing the invariant distribution of the Markov chain induced by or , introducing additional complexity. Second, the process of iteratively applying or does not naturally correspond to any reasonable dynamic process that agents are likely to follow in practice: it is difficult to imagine an agent first computing the invariant distribution of the current strategy in use by her competitors, and then solving a dynamic program given that invariant distribution.

By contrast, in this section we present a pair of myopic learning dynamics that address these considerations. The algorithms presented in this section are simple and easy to implement. Furthermore, they demand only a weak form of rationality from the players, thereby resolving the two main issues of computability and plausibility associated with the standard solution concept of Markov perfect equilibrium (as discussed in the Introduction).

In the myopic learning dynamic, at each time , each agent computes a best response to the current population state distribution , assuming that the population state will remain at at all future times. (This step is similar to model predictive control or receding horizon control; see, e.g., Garcia et al. (1989).) In other words, agents play according to a strategy in . This play yields a new population state at the next time step according to the transition kernel.

The algorithms we consider are reasonable in settings where agents are not likely to predict future learning by other agents. Indeed, such an assumption seems plausible precisely in the large systems that mean field equilibrium is meant to model. In such systems, myopic behavior is simple computationally; by contrast, solving a dynamic program with full knowledge of future strategies other agents will employ places unreasonable informational requirements on the agents.

We first consider an algorithm where agents play actions induced by

.

Algorithm L-MLD:

-

1.

Every agent initializes their state to at time .

-

2.

Agents observe the population state .

-

3.

An agent with state chooses the action so that , where . The agent’s next state is distributed according to .

-

4.

Repeat (2)-(3).

Here L-MLD denotes lower myopic learning dynamics. Observe that agents compute a new strategy based on the observed current population state—not based on the invariant distribution associated to the last strategy chosen. This means that two simultaneous dynamic processes are taking place: strategy revision on the part of the players, but also state update via the system dynamics (4). Due to this intertwined dynamic, novel arguments are required to prove convergence of best response dynamics (relative to usual proofs of convergence for such dynamics in supermodular games, e.g., Milgrom and Roberts 1990, Vives 1990). We also note that although the same strategy is computed by every agent, the particular action chosen will vary depending on their current state.

The preceding description yields a simple recursion for the population state at the next time step; for all Borel sets :

| (13) |

where is defined as follows:

| (14) |

Our goal is to understand the behavior of the sequence of population states , as well as the sequence of policies . We have the following proposition, which mirrors Proposition 4.1.

Proposition 4.2

Let be a stochastic game with complementarities. Define and iteratively according to Algorithm L-MLD. Then , and . Further, there exists a distribution and a strategy , nondecreasing in , such that converges weakly to as , and converges pointwise to as .

Thus we find the same result as for L-BRD: under mild continuity conditions on the model primitives, the dynamics converge to the smallest mean field equilibrium among all those where the equilibrium strategy is nondecreasing.

The proof of Proposition 4.2 proceeds as follows. We exploit two key monotonicity properties established in the course of proving existence of an equilibrium (Theorem 3.4): first, that is monotone in (Lemma 11.9 in the appendix); and second, that is monotone in , , and (Lemma 11.11 in the appendix). These two properties together allow us to establish that and form monotone sequences—even though players are reacting only to the current population state, the population state over time moves monotonically towards an equilibrium.

Note that L-MLD initializes players to the lowest state, . This behavior of L-MLD is particularly meaningful for several of the applications described in the Introduction; for example, in an interdependent security setting, we might envision a scenario where a new, more efficient technology for security is introduced. In this case the “low” initial population state might correspond to the status quo, and then the myopic learning dynamics track the adaptation of the population to a new equilibrium configuration.

A similar convergence result also holds if instead every agent starts at

the largest state , and follows the strategy

at each time step. We call this Algorithm U-MLD.

Algorithm U-MLD:

-

1.

Every agent initializes their state to at time .

-

2.

Agents observe the population state .

-

3.

An agent with state chooses the action so that , where . The agent’s next state is distributed according to .

-

4.

Repeat (2)-(3).

Note that (13) continues to hold, with chosen according to the preceding algorithm. The same conclusion as Proposition 4.2 holds for U-MLD as well, except that under Assumption 4.1, the limit point is the largest fixed point of , i.e., (cf. (12)).

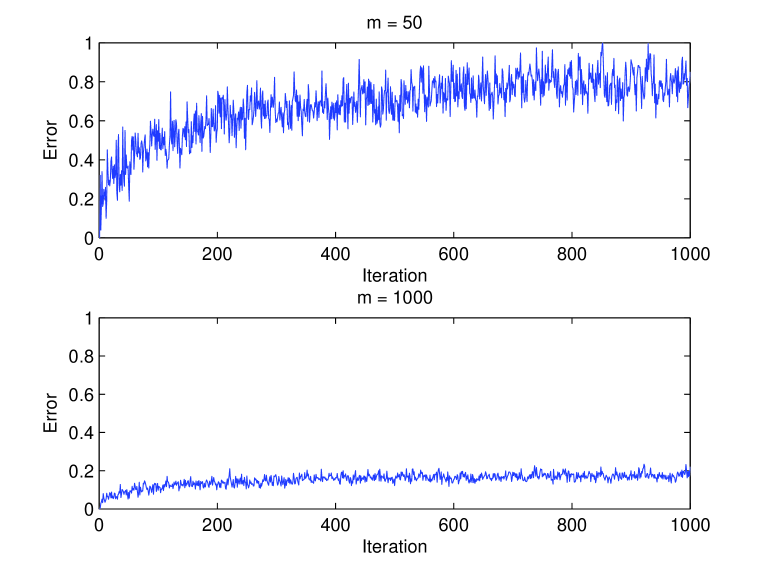

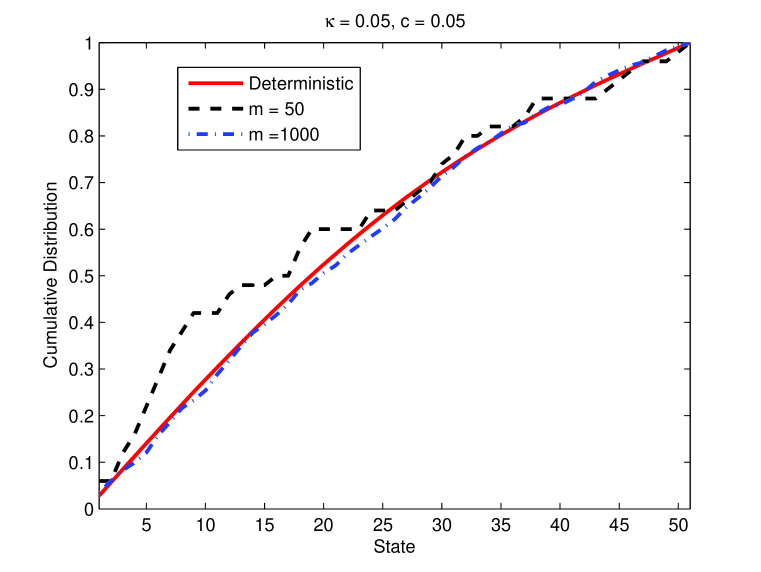

We conclude this section by discussing the behavior of myopic learning dynamics in finite systems. In particular, suppose that in a game consisting of players, each player follows the dynamic prescribed by L-MLD: each player starts in the lowest state, and then at each time step, observes the current population state and plays one step according to the optimal oblivious strategy given that population state. Because the system is finite, additional error is introduced due to the randomness in state transitions of individual agents; in particular, due to this randomness, it is not immediately guaranteed that myopic learning dynamics will converge to a mean field equilibrium in a finite game. However, if the state space is discrete, then using techniques similar to Adlakha et al. (2010) it can be shown that weakly, almost surely, where is the population state after time steps with players, and is the population state in the L-MLD dynamic after time steps in the mean field limit. Thus after sufficiently many time steps and for sufficiently large finite systems, the population state under L-MLD converges approximately to a mean field equilibrium population state. We illustrate this point later in Section 9.

5 Comparative Statics

In this section we discuss sensitivity analysis of equilibria, also known as comparative statics results. Our goal is to understand how the equilibrium distribution and optimal strategy are altered in response to changes in parameters. These results allow us to evaluate changes in equilibrium with respect to changes in a parameter.

In this section we consider a family of stochastic games with complementarities, parameterized by , where is a complete lattice. In the context of security games, this parameter could, for example, represent the effectiveness of a particular security technology. Alternatively, in the context of recommendation systems, might represent the effectiveness of the collaborative filtering engine in improving recommendations to one agent based on the profiles of other agents.

Formally, suppose we are given a family of stochastic games for with common strategy spaces, action spaces, and discount factors, where for each , is a stochastic game with complementarities, i.e., satisfies Definition 3.1 for each . We refer to as a parametric family of stochastic games with complementarities. Let and be the payoff and transition kernel, respectively, in . We make the following assumption.

The payoff has increasing differences in and . The transition kernel has stochastically increasing differences in and , and is stochastically nondecreasing in for fixed .

Under the preceding assumption, we can give a directional characterization of the movement of equilibrium in response to parameter changes.

Theorem 5.1

Such comparative statics results are commonly applied in the context of games with complementarities; but it is worth noting that in a dynamic context this result provides additional insight, because it quantifies how the distribution of agents’ states will respond as a parameter changes. This kind of insight is particularly valuable for system designers, regulators, and policy makers, where changes in equilibrium behavior due to control decisions may be challenging to characterize. As one simple consequence of the preceding theorem, suppose that in security games, an incentive is introduced for agents to invest in security as a linear rebate in the payoff, proportional to an agent’s security level . It is straightforward to check that this results in more players opting for higher investment, and thus the equilibrium population state tends to shift towards higher security levels.

6 Coupling Through Actions

In the stochastic game model considered thus far, players’ payoffs and dynamics are “coupled” through their states; formally, and depend on the population state , which is in turn a distribution over the state space . In many models, however, the coupling between agents is through their actions, rather than states; that is, is a distribution over the action set , rather than over the state space. Our analysis extends rather easily to models of this form; in this section we briefly discuss existence of, and convergence to, mean field equilibrium in such models.

Formally, an action-coupled stochastic game has the following distinctions from the (state-coupled) stochastic game defined in Section 2.

Population action distribution. We define the population action distribution as follows. Let denote the fraction of players (excluding player ) that play action at time , i.e.:

| (15) |

where is the indicator function that the action of player at time is . We refer to as the population action distribution at time (from player ’s point of view).

We let denote all Borel probability measures over . Note that the population action distribution lies in .

Transition probabilities and payoff. We denote the payoff by , and the transition kernel by , where is a population action distribution, i.e., an element of .

Recall that in defining mean field equilibrium in Section 2.2, we consider two maps and ; the former gives the set of optimal oblivious strategies given a population state , and the latter gives the set of invariant distributions under a kernel with strategy and population state . Those maps are analogously defined for action-coupled stochastic games, but with as the population action distribution rather than the population state; we omit the formal details. With a slight abuse of notation, we let be the set of optimal oblivious strategies for a player, given population action distribution ; and we let be the set of invariant distributions of the dynamics induced by oblivious strategy and population action distribution .

In order to define mean field equilibrium, we require one additional function. Given a population state and an oblivious strategy , let give the resulting population action distribution; i.e., for Borel sets :

Note that is the set of states such that . In order for this definition to be well posed, we require the strategy to be Borel measurable; to avoid this issue we simply assume that all model primitives are continuous, i.e., that Assumption 4.1 holds. Under this assumption it can be shown that we can restrict attention to Borel measurable strategies .

If every agent conjectures that is the long run population action distribution, then every agent would prefer to play an optimal oblivious strategy . On the other hand, if every agent plays , and the long run population action distribution is indeed , then must also be the population action distribution that results from an invariant distribution in . This yields the following definition of a mean field equilibrium for action-coupled stochastic games.

Definition 6.1

A strategy , population state , and population action distribution constitute a mean field equilibrium of an action-coupled stochastic game if , , and .

An action-coupled stochastic game with complementarities is then defined exactly as in Definition 3.1, but with the population state replaced by the population action distribution . Extending the argument in the proof of Theorem 3.4, we can prove the following theorem.

Theorem 6.2

Suppose Assumption 4.1 holds. Then there exists a mean field equilibrium for any action-coupled stochastic game with complementarities .

As is clear from the proof, the same monotonicity properties employed to prove existence of a mean field equilibrium can also be used to extend Corollary 3.5 (establishing the existence of a “largest” and “smallest” mean field equilibrium) as well as Proposition 4.1 and 4.2 (establishing convergence of best response dynamics and myopic learning dynamics, respectively). We omit the details of these derivations as they mirror earlier development in the paper nearly identically.

7 Separable Stochastic Games

As the preceding sections illustrate, stochastic games with complementarities possess a number of properties that make them amenable to equilibrium analysis. One potential concern, however, is that the set of models admitted by Definition 3.1 may be somewhat limiting. Consider the following example.

Example 7.1 (Linear dynamics)

Consider a simple model where the distribution of the next state of an agent is “linear” in and . Let be a zero mean random variable that takes countably many values, and fix positive constants and . We consider a state space , for some large positive constants ; and let for all , where . Define as follows:

| (16) |

In this model, the state dynamics are essentially linear, except at the boundaries of the state space (where the state is truncated to lie within ). Such a model might naturally arise in a wide range of examples, e.g., Examples 1.1, 1.2, or 1.4 (see Section 8 for details).

Unfortunately, such a kernel does not exhibit stochastically increasing differences in general. To see this, we consider a simple instance where , and . Consider any nondecreasing function , and fix and such that . Then:

In general, the right hand side exhibits increasing differences in and only if is locally convex. This is easiest to see for differentiable : in that case the cross partial derivative has to be nonnegative to ensure increasing differences, which only holds if . For general nondecreasing , therefore, the expectation need not exhibit increasing differences in and . \halmos

The preceding example highlights a deficiency in stochastic games with complementarities: while a rich class analytically, they do present some restrictions from a modeling standpoint. In this sense, complementarity can appear to be a brittle property.

However, this same brittleness can actually become an advantage: although at first glance it may appear that complementarity fails, often simple transformations can lead to games that admit analysis via complementarity methods even if the original game did not. (A common example is the class of log-supermodular games used extensively in oligopoly theory, where the logarithm of the profit function may be supermodular; see, e.g., Milgrom and Roberts (1990) and Vives (1990) for details.)

In this section we demonstrate that a wide range of models, including those with dynamics similar to Example 7.1, can be transformed to standard stochastic games with complementarities. Further, the class of models we develop has the benefit that the assumptions are typically easier to check in practice. This significantly widens the applicability of our theory to models where the desired monotonicity properties may not be immediately apparent.

The class of games we consider in this section feature a payoff that is separable in the state and action. We have the following definition.

Definition 7.2

A separable stochastic game is a stochastic game with the following additional properties.

-

1.

Actions. There exist , such that for all .

-

2.

Payoff. The single period payoff to player at time can be written as , where we refer to as the utility at state and population state , and as the cost for action .

-

3.

Transition probabilities. The state of a player evolves according to a Markov process with the following transition probabilities. If the state of player at time is and the player takes an action at time , then the next state is distributed according to the Borel probability measure , where for Borel sets ,

(17) Note that depends on and only through the function ; we refer to as the kernel parameter. We assume that takes values in a compact interval .

In this section we provide insight into separable stochastic games with complementarities. We have the following definition.

Definition 7.3

A separable stochastic game with complementarities is a separable stochastic game with the following properties.

-

1.

Nondecreasing payoff and convex cost. The utility function is nondecreasing in , and the cost function is nondecreasing and convex in . Further, for fixed , .

-

2.

Payoff complementarity. The utility function has increasing differences in and .

-

3.

Monotone transition kernel. The transition kernel is stochastically nondecreasing in and . Further is continuous in (w.r.t. the topology of weak convergence on ).

-

4.

Transition kernel complementarity. The transition kernel has stochastically increasing differences in and .

-

5.

Kernel parameter monotonicity and complementarity. The kernel function is supermodular in and , nondecreasing in the state , and concave and nondecreasing in the action .

-

6.

Countable noise. For each , the support is countable.

We proceed by reparametrizing the strategy in terms of the kernel parameter; under this reparametrization, the resulting model is revealed to be a special case of the general model studied earlier in this paper.

Formally, suppose we are given a separable stochastic game with complementarities . Before we proceed, we require some additional notation. For each , define:

| (18) |

Thus is the image of under . In addition, for each , define:

| (19) |

Thus is the minimum cost incurred to achieve kernel parameter when at state .

The next lemma establishes some basic properties of and . It uses the assumption that the cost function is a convex function of action .

Lemma 7.4

Suppose is a separable stochastic game with complementarities. Suppose and are defined as in (18) and (19), respectively. Then for each , is a compact interval, and the sets are nondecreasing in .

The function is convex and nondecreasing in on for each , and nonincreasing in for each as long as . Further, for all :

| (20) |

If , , and , then:

In other words, has decreasing differences in and .

We now use Lemma 7.4 to define a new stochastic game, which is in fact a stochastic game with complementarities as in Definition 3.1.

Proposition 7.5

Based on the preceding proposition we have the following theorem.

Theorem 7.6

Any separable stochastic game with complementarities has a mean field equilibrium.

The preceding result can be extended, of course, to provide analogs of Corollary 3.5 (existence of a largest and smallest equilibrium), as well as Propositions 4.1 and 4.2 (convergence of best response dynamics and myopic learning dynamics, respectively). (The appropriate generalization of Assumption 4.1 is that should be jointly continuous in and , and should be jointly continuous in and .) Note, however, that the dynamics defined here are in the modified strategy space, where the “action” is the kernel parameter chosen. In particular, the dynamics in the original action space may not be monotone at all; nevertheless, the eventual limit point is a mean field equilibrium.

It is also straightforward to generalize the comparative statics result in Theorem 5.1 to separable stochastic games using the same transformation as the preceding result. In addition, the definition of a separable stochastic game with complementarities can be naturally extended to separable action-coupled stochastic games with complementarities (simply by replacing the population state by the population action distribution in the payoff and transition kernel), and an argument similar to Proposition 7.5 shows that such a game can be transformed to a standard action-coupled stochastic game with complementarities.

We conclude this section by noting that the preceding results continue to hold in a setting where the payoff is not necessarily monotone, as long as dynamics are decoupled. Formally, suppose that is a stochastic game that satisfies all the conditions in Definition 7.3, except that is not necessarily nondecreasing in . Suppose in addition that does not depend on ; thus we denote the kernel simply . In this model it can again be shown that a mean field equilibrium exists, as we now describe.

The proof of Theorem 3.4 (and subsequent results on ordering of equilibria and convergence) use the fact that the payoff is nondecreasing in to show that is supermodular in and has increasing differences in and (see Lemma 11.3). In order for the expectation to preserve these properties, the integrand must be nondecreasing in state; this is why we require the payoff to be nondecreasing. However, if only depends on the kernel parameter, then we can show that has increasing differences in and , even if the payoff is not necessarily nondecreasing. For details, we refer the reader to Lemma 16.6 in the Appendix. Substitution of this lemma in the proof of Theorem 3.4 yields the desired result.

8 Examples

In this section we revisit the five examples mentioned in the Introduction: interdependent security; collaborative filtering; dynamic search with learning; coordination games; and oligopolies with complementarities. We show that each of these examples can be formalized within the framework developed in this paper, so that the existence and convergence results we have proven apply.

8.1 Example 1.1: Interdependent Security

We consider a dynamic model of interdependent security in a computer cluster, where the state gives the security level of a player. Players can improve their security level through investment; an investment incurs a cost that is convex and nondecreasing in . A higher action leads to improvement in the security level, and with no or little investment the security level deteriorates due to depreciation. Thus a reasonable model for the dynamic evolution of the security level might be the linear dynamics in (16), where and , and , , and has a negative expected value. Let be the probability of a bad event occurring when an individual computer is at the security level , and let be the cost of this bad event to the host.

We consider a simplified model where at each time step, an individual computer “talks” to a randomly selected computer in the network. (This talk can be in form of establishing a TCP connection, exchanging data, emails, etc.) Thus, at each time, there is a probability that an individual computer will suffer a bad event because of the security level of the rest of the network. Let be the fraction of all computers (except computer ) that have their security level at at time . Then, at each time step, computer receives an expected value that is given as:

The first part of the payoff reflects the security of host . The scaling factor in the second term is the probability that no bad event happens because of the individual security level. The term represents the average security level of the rest of the network. Because is decreasing, it is straightforward to verify that the product of these two terms exhibits strategic complementarities between the security level of agent , and the security level of every other agent. It follows that this is a separable stochastic game with complementarities.

8.2 Example 1.2: Collaborative Filtering

As a canonical example, we consider the collaborative filtering system used by a recommendation engine on a movie rental site such as Netflix. We let the state be the quality of a user’s profile, and assume takes values in a compact interval. The action represents the effort put forth in updating her profile, e.g., through rating more movies; actions are costly, with denoting the cost incurred by action . We assume is convex. If user does not put forth any effort at time , then the profile becomes “stale,” i.e., the quality of the profile drops over time. Thus in this model the quality can be modeled via dynamics as in (16) as well, where , , and has negative expected value.

Based on the quality of a user’s profile as well as the profile of other users in the system (captured by the population state ), the recommendation system suggests a movie to a user. Let denote the expected desirability of the movie recommended to a user, given their profile quality and the population state . Observe that will increase if increases, since a more accurate profile results in more accurate recommendations. However, for most collaborative filtering systems, it is also the case that if others have higher quality profiles, then the marginal return to a higher quality profile is higher; for example, this would be the case under a nearest neighbor algorithm as is commonly used by a variety of online recommendation systems. Thus such a model is a separable stochastic game with strategic complementarities. Collaborative filtering systems are one example of a setting with positive network effects; games with strategic complementarities are commonly used to model settings with positive network effects.

8.3 Example 1.3: Dynamic Search with Learning

We consider a model where at each time step, a trader exerts effort to search for trading partners. As discussed in Example 1.3 in the Introduction, traders’ experience grows with both their own effort and the effort of others. To formalize this notion, suppose traders choose effort each time step from , where . Let the state denote the current search productivity of a given trader; we assume where . Finally, given a population action distribution , we let be defined as:

We then assume that traders receive a payoff defined as:

where is a cost of effort. In particular, observe that the first term of the payoff increases as the search productivity increases, the players own effort increases, or the mean effort of others in the system increases.

As a trader exerts effort, they gain experience and their search becomes more productive. Further, as discussed in Example 1.3 in the Introduction, traders’ experience grows with both their own effort and the effort of others; as in our other examples, with insufficient effort the search productivity decreases as previously acquired experience becomes outdated. Thus we assume the transition kernel is defined as in (8), where:

This is a model where traders are coupled through their actions, cf. Section 6. It is straightforward to verify that this model exhibits the complementarity properties required for an action-coupled stochastic game with complementarities.

8.4 Example 1.4: Coordination Games

In this model, a collection of agents are interested in coordinating on a common state; the model we present is a related to the one studied by Huang et al. (2006). Actions can alter the state, but any nonzero actions are costly. We assume that , and . We assume dynamics are linear, cf. (16), where , and has negative expected value. Each player tries to minimize mean squared error to the other players’ average state, and incurs a quadratic cost for taking nonzero action. If is the current population state, we let:

We assume the payoff of a player is:

It is straightforward to verify that has increasing differences in and , since the cross partial derivative with respect to and is positive (Topkis 1998). It follows that has increasing differences in and . Further, is convex and nondecreasing in .

In principle we would like to claim this is a separable stochastic game with complementarities, but the payoff is not monotonic in . As discussed at the end of Section 7, however, if the transition kernel does not depend on (as is the case in (16)), then the payoff need not be monotonic in —and all our results continue to hold. Thus existence of equilibrium and convergence of MLD can be guaranteed for this model. Notably, our convergence result provides justification for a distributed control interpretation of this coordination game, where multiple individual agents can execute a myopic algorithm and yet converge to a common state.

We conclude by noting one peculiarity of our formulation: we have , so in particular, players cannot move backwards (i.e., take negative action). This assumption is made to ensure that is nondecreasing, as required for a separable stochastic game with complementarities. However, in the original formulation of Huang et al. (2006), has zero expected value, but players are allowed to take both positive and negative actions. This expanded formulation can still be analyzed using the methods of this paper.

Formally, suppose that has zero expected value, and . Then even though is no longer nondecreasing on , we can still show in this specific model that (cf. (19)) exhibits decreasing differences in and . To see this, note that with the linear dynamics of (16), for . Upon differentiating it follows that , establishing that has decreasing differences in and . By substituting this observation in the analysis of Section 7 we recover all the results of that section.

8.5 Example 1.5: Oligopolies and Complementary Goods

Consider an oligopoly scenario where the goods produced by firms are complements. As firms gain experience in production, their cost of production decreases. We let be the experience level of a firm, and let be the quantity produced by a firm. Let be the inverse demand curve seen by a firm, where is the population action distribution. Thus this is a monopolistic competition model, where firms sell differentiated products and the market clearing price seen by a firm depends on the quantities produced by all firms. The per period payoff to a firm is:

where is the cost of producing quantity when a firm’s experience level is . Note that since is the population action distribution, this is a game with coupling through actions.

We assume that firms’ experience levels increase with higher quantities produced; for example, we might consider dynamics of the form (8) with defined as:

Note in particular that in this model experience levels evolve independently across firms.

We note that the cost of production will typically decrease with the experience level. Thus, is decreasing in . Further, at a higher experience level, a firm’s marginal cost of production typically decreases, so we expect to have decreasing differences in and . Finally, since the payoff is separable in and , it has increasing differences in those two parameters.

Since goods are complements, if , then we expect for a fixed production quantity the price is higher at , i.e., for every fixed . Furthermore, it is natural that if , then for a slight increase in production, a firm can charge a higher price for its goods. In other words, should have increasing differences in and . Under these natural assumptions, it is straightforward to verify that has increasing differences between and . Thus this game is a action-coupled stochastic game with complementarities.

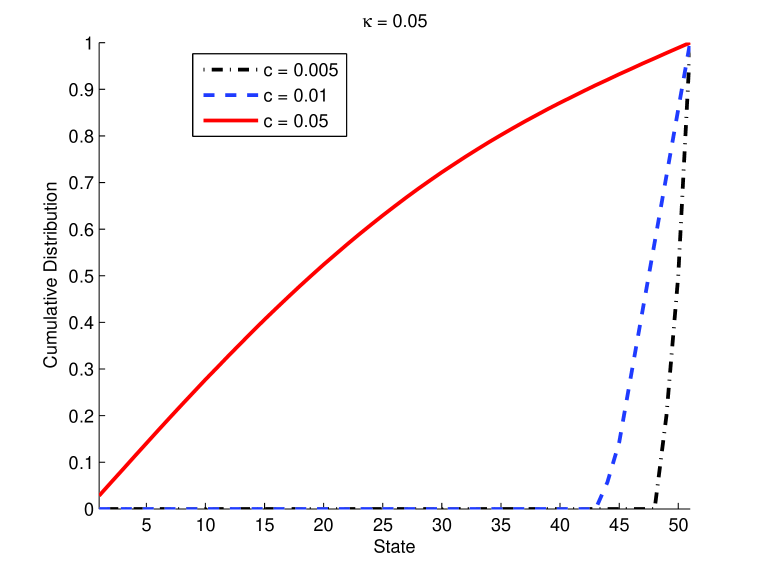

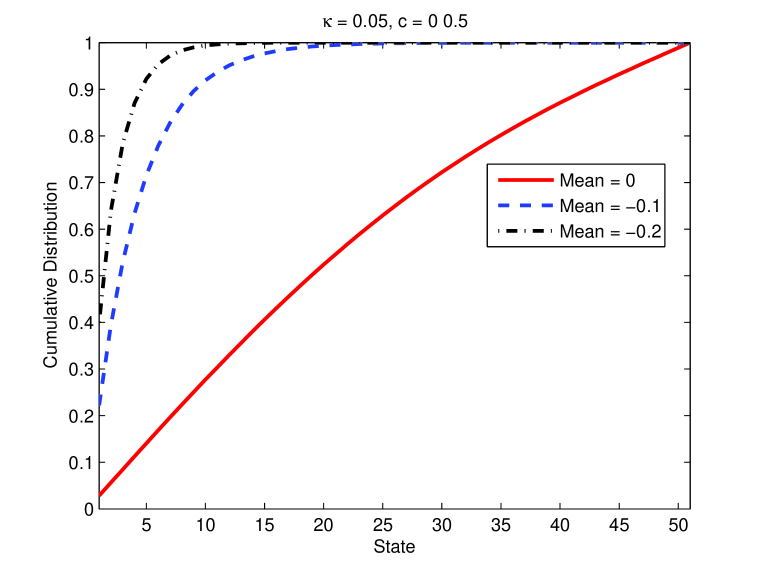

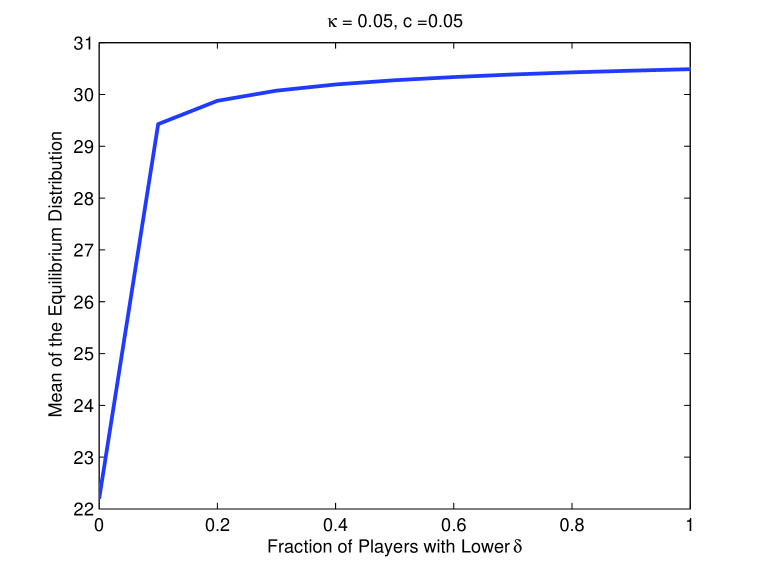

9 Numerical Analysis